Occupational Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

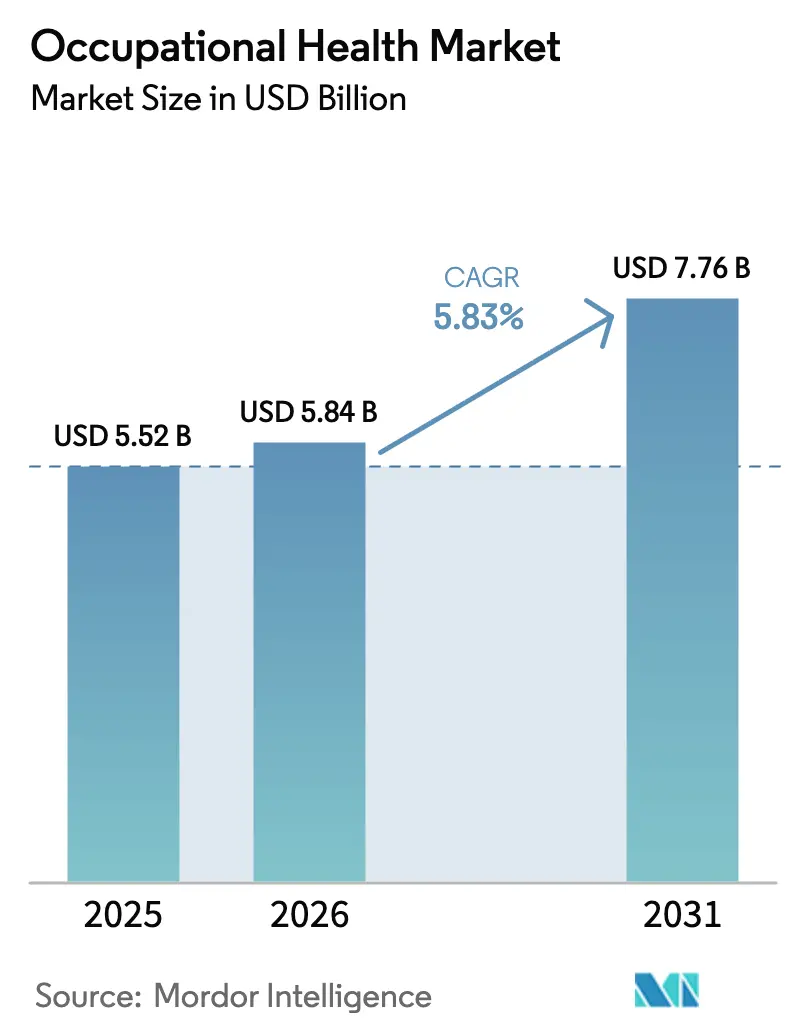

| Market Size (2026) | USD 5.84 Billion |

| Market Size (2031) | USD 7.76 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Occupational Health Market Analysis by Mordor Intelligence

The occupational health market size was valued at USD 5.52 billion in 2025 and estimated to grow from USD 5.84 billion in 2026 to reach USD 7.76 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). Across the forecast window, employers are moving from reactive health screening toward integrated wellness ecosystems that blend group health insurance incentives with data-driven preventive care. Heightened regulatory scrutiny, the rising prevalence of musculoskeletal disorders (MSDs), and accelerating digital transformation in corporate health programs combine to propel sustained spending. Technology-enabled delivery, particularly telehealth and wearable monitoring, is lowering access barriers for small businesses and supporting rapid expansion in underserved regions. Competitive advantage increasingly rests on AI-powered analytics, blockchain-secured data portability, and the ability to scale services for hybrid workforces.[1]Centers for Disease Control and Prevention, “Total Worker Health,” CDC, cdc.gov

Key Report Takeaways

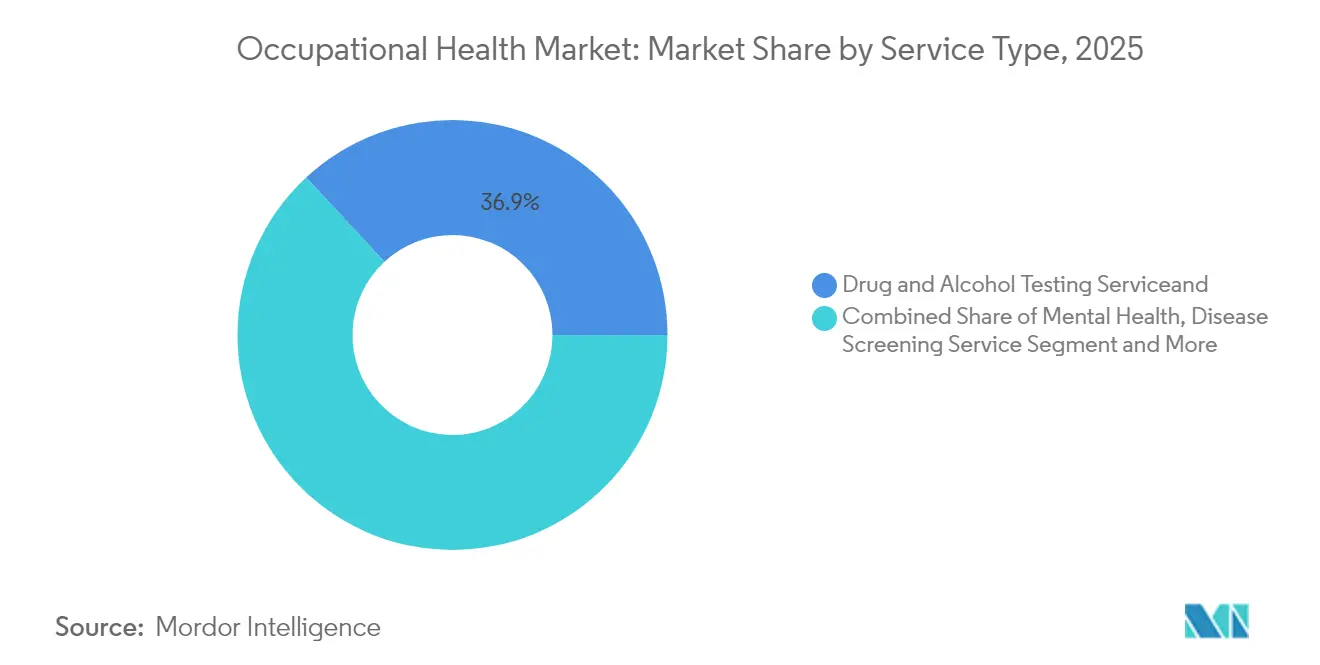

- By service type, drug and alcohol testing held 36.92% of occupational health market share in 2025, whereas mental health services are projected to expand at 10.47% CAGR through 2031.

- By service location, on-site clinics captured 42.88% revenue share in 2025; telehealth/virtual platforms are the fastest-growing segment at 10.22% CAGR to 2031.

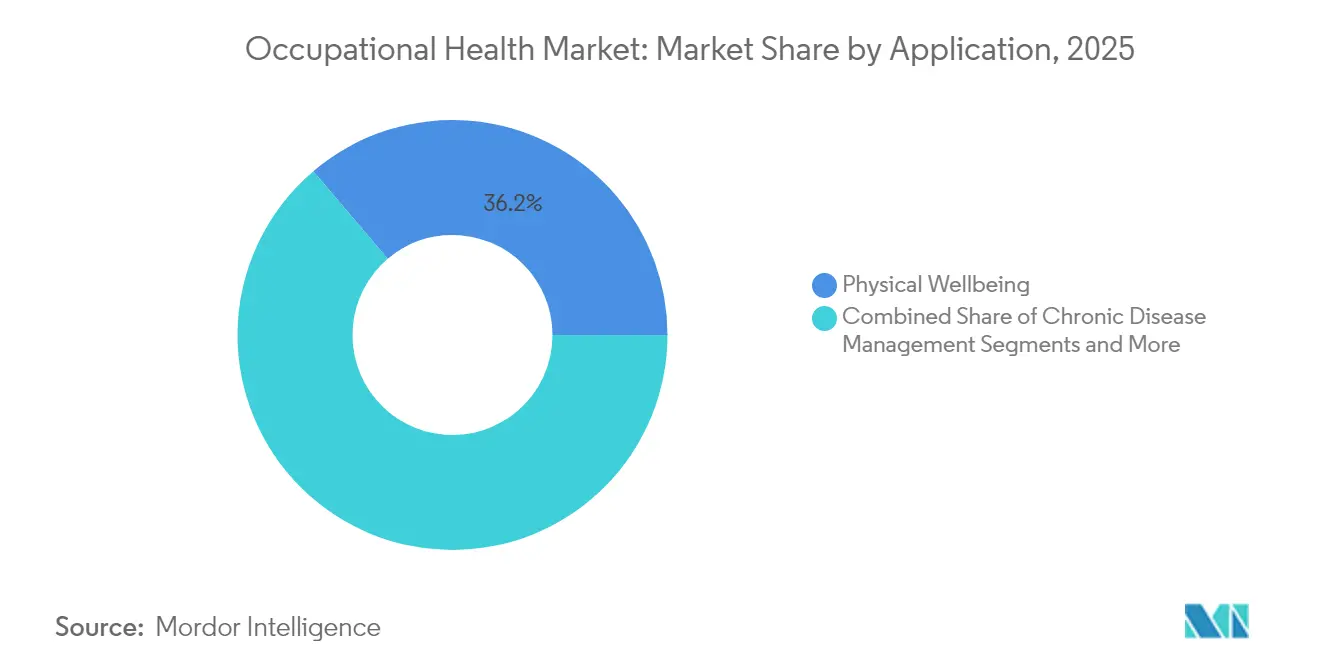

- By application, physical wellbeing dominated with 36.21% share of the occupational health market size in 2025; social and mental wellbeing applications lead growth at 9.18% CAGR.

- By organization size, large enterprises (250-4,999 employees) accounted for 49.55% of demand in 2025, while micro enterprises (<10 employees) are set to rise at 8.98% CAGR on the back of digital solutions.

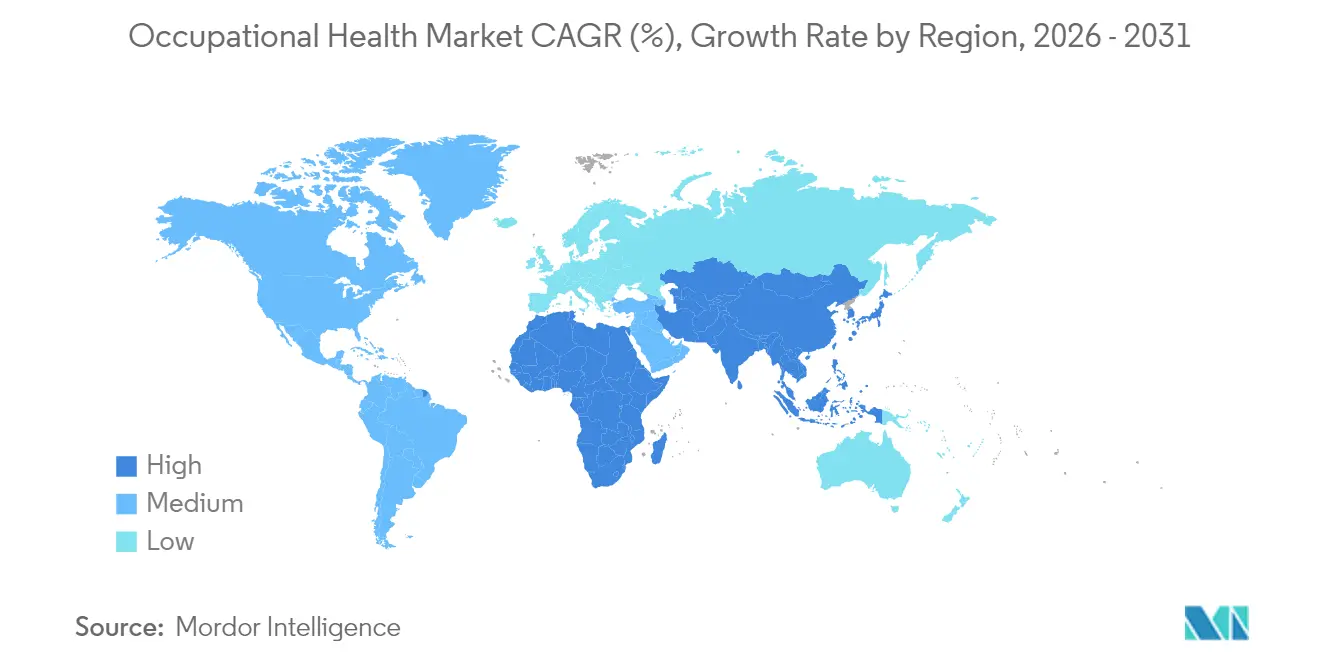

- By geography, North America commanded 32.10% of the occupational health market in 2025; Asia-Pacific is poised for the fastest expansion at 7.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Occupational Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workplace wellness integration with group health insurance | +1.8% | Global (lead: North America & Europe) | Medium term (2-4 years) |

| Stringent OH&S regulations (ISO 45001, OSHA, EU directives) | +1.5% | Global (strongest in Europe & North America) | Long term (≥ 4 years) |

| Rising burden of chronic work-related diseases (MSDs) | +1.2% | Global (notable in APAC & North America) | Long term (≥ 4 years) |

| Telehealth & remote monitoring for SMEs and gig workers | +1.1% | Global (core: APAC & North America) | Short term (≤ 2 years) |

| Blockchain-enabled employee health data portability | +0.7% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Investor pressure for ESG-linked human-capital disclosures | +0.9% | Global (developed markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Workplace Wellness Initiatives & Integration with Group Health Insurance

Employers now link wellness dashboards directly to insurance premium structures, rewarding healthy behaviors that cut long-run claims. Johns Hopkins’ Balance program illustrates this shift by engaging 4,644 moderate- to high-risk employees through digital mental-health triage, improving productivity and lowering absenteeism.[2]Kaylee T. Woodard et al., “A Population Health Approach to Workplace Mental Health,” Frontiers in Public Health, frontiersin.orgData-sharing pacts between insurers and occupational health vendors foster real-time risk stratification and personalized interventions that resonate with younger workers seeking holistic benefits packages. Insurers in turn apply actuarial discounts, creating a feedback loop that cements the occupational health market as a core pillar of talent strategy.

Stringent Global OH&S Regulations (ISO 45001, OSHA, EU Directives)

Regulatory harmonization is elevating baseline service demand. The European Union’s Directive 2019/1831 updated chemical exposure limits, prompting enterprises to upgrade monitoring protocols.[3]European Agency for Safety and Health at Work, “Directive 2019/1831 – Indicative Occupational Exposure Limit Values,” EU-OSHA, osha.europa.eu In Latin America, Brazil’s 2025 overhaul of NR-1 aligns national practice with ISO 45001, spurring small manufacturers to outsource compliance management. Mandatory continuous risk assessment is steering spending toward subscription-based occupational health programs that provide year-round oversight rather than episodic screenings.

Rising Burden of Chronic Work-Related Diseases (MSDs)

MSDs remain the costliest workplace health issue, affecting 84.3% of nurses across Asia and driving 39,200 lost workdays at Rolls-Royce in 2024.[4]Roberto Tonelli, “A Self-Sovereign Identity–Blockchain-Based Model Proposal for Deep Digital Transformation in Healthcare,” Future Internet, mdpi.com Global low-back pain DALYs are projected to top 11.6 million by 2050, pressuring employers to fund ergonomic redesigns and early physical-therapy interventions. Multinationals are co-funding research with bodies such as the National Safety Council and Amazon to deploy AI risk-scoring tools that target high-strain tasks nsc.org.

Expansion of Telehealth & Remote Monitoring for SMEs and Gig Workforce

Virtual clinics slash fixed-site overheads, letting micro firms buy bundled tele-occupational health on demand. Teladoc’s acquisition of Catapult Health marries at-home diagnostics with virtual check-ups that already cover 3 million lives in employer programs. Wearable sensors stream continuous biometric data to AI dashboards, enabling early intervention and cutting time away from work for low-acuity conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & unclear ROI for small and micro enterprises | -0.8% | Global (higher in developing markets) | Short term (≤ 2 years) |

| Shortage of trained occupational health clinicians | -0.6% | Global (acute in APAC & MEA) | Long term (≥ 4 years) |

| Data-privacy and “surveillance” push-back on wearables | -0.4% | Europe & North America | Medium term (2-4 years) |

| Automation & robotics reducing certain high-risk screenings | -0.3% | Developed markets, manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Unclear ROI for Small and Micro Enterprises

For shops with fewer than 10 employees, per-capita spend on comprehensive programs can outstrip perceived benefits, delaying uptake despite proven mental-health gains in controlled trials. Many owners cite cash-flow pressures and limited analytical capacity to quantify indirect savings from reduced absenteeism, curbing near-term expansion of the occupational health market in developing economies.

Shortage of Trained Occupational Health Clinicians Globally

India’s fast-growing manufacturing hub highlights the deficit: only a small fraction of medical schools offer dedicated occupational health tracks, forcing firms to rely on general practitioners. Worldwide, just 10-15% of workers have direct access to specialized clinicians, hampering service quality and coverage, particularly in rural areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Mental Health Services Drive Transformation

Drug and alcohol testing accounted for 36.92% of the occupational health market in 2025, largely because safety-critical industries remain bound by statutory screening rules. Mental health services, however, are on track for a 10.47% CAGR as pandemic-era awareness makes psychological support a recruitment and retention lever. The occupational health market size for mental-health offerings is expanding fastest within technology, finance, and professional services employers. Disease-screening workflows maintain steady demand thanks to regulatory schedules, while vaccination programs evolved post-COVID-19 into year-round immunization protocols. Ergonomic wellness is entering a digital phase where posture-sensing wearables flag MSD risks in real time, driving incremental revenue beyond legacy onsite assessments.

The demand inflection reflects generational shifts toward holistic care. Younger professionals show higher voluntary uptake of counseling apps bundled with employee assistance programs, lifting engagement rates and validating premium service tiers. Meanwhile, return-to-work and disability management platforms integrate virtual rehab check-ins to shorten lost-time durations, reinforcing the occupational health market as an enabler of workforce resilience.

By Service Location: Virtual Platforms Reshape Delivery Models

On-site clinics still dominate day-to-day usage, holding 42.88% revenue share, particularly among manufacturers seeking immediate triage for acute injuries. Yet telehealth is capturing share fastest at 10.22% CAGR as bandwidth and regulatory barriers fall. The occupational health market size attributed to virtual care rose sharply in 2025 when pandemic emergency provisions normalized cross-state tele-practice in the United States. Near-site hubs remain relevant for firms pooling resources in industrial parks, while mobile units serve remote oil, gas, and construction sites where connectivity remains patchy.

Hybrid scheduling models pair quarterly in-person check-ups with continuous app-based monitoring, optimizing clinician time and lowering employer costs. Wearable analytics send flagged cases to virtual physicians, accelerating interventions without disrupting operational timetables.

By Application: Social Wellbeing Gains Strategic Priority

Physical wellbeing led with 36.21% of 2025 revenue, reflecting the historical roots of occupational health in injury prevention. Social and mental wellbeing applications, the fastest-growing at 9.18% CAGR, now occupy board-level agendas as talent markets tighten. Chronic-disease management benefits from merged data feeds between primary healthcare and workplace programs, while chemical-exposure management remains a staple for pharmaceuticals and heavy industry. Emergency-and-trauma services are widening scope to include psychological first aid, again reinforcing the holistic pivot of the occupational health market.

Employers are mapping social determinants—such as commute stress and housing insecurity—into program design, signalling a future where benefits expand beyond the workplace walls.

By Organization Size: Micro Enterprises Embrace Digital Solutions

Large organizations leveraged scale to command 49.55% of 2025 spending, yet the hottest growth lies with micro enterprises, forecast at 8.98% CAGR. Subscription-based virtual bundles let tiny teams buy monthly occupational health coverage without committing capital to brick-and-mortar clinics. Small enterprises (10-49 staff) are pooling through local chambers of commerce to secure discounted tele-occupational health packages, further broadening the occupational health market.

Medium-sized firms stand at a tipping point where rising injury-rate visibility pushes them to adopt more sophisticated analytics dashboards. Very large multinationals continue to pioneer blockchain-credential pilots that streamline global employee transfers and compliance audits.

Geography Analysis

North America retains 32.10% market share, supported by OSHA requirements and strong employer benefits culture. The United States’ Total Worker Health framework integrates safety with wellness and sets best-practice benchmarks emulated elsewhere. Canada’s universal care foundation lowers out-of-pocket costs for preventive programs, while Mexico’s export-manufacturing clusters drive onsite clinic demand.

Asia-Pacific is the fastest-growing region at 7.92% CAGR. China’s vast factory workforce, India’s tightening safety codes, and Japan’s aging employees all propel service uptake. Australia adds demand through mining and construction projects in remote zones, relying on tele-medical infrastructure.

Europe benefits from harmonized EU-OSHA directives that simplify multi-country program roll-outs and sustain compliance-driven spend. Germany and the Nordics funnel investment into AI ergonomics tools, while the United Kingdom’s post-Brexit regime sparks demand for specialist advisory services. South America’s outlook brightens after Brazil updated several Norma Regulamentadora rules in 2025, aligning with ISO standards and creating new employer obligations.

The Middle East and Africa present dual dynamics: Gulf states introduce heat-stress frameworks for outdoor labor, and African mining markets slowly embed occupational health into ESG mandates.

Mordor Intelligence provides coverage of the occupational health market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The occupational health market remains moderately fragmented, yet consolidation momentum is rising. Concentra’s Nova Medical Centers takeover expanded its network to 770 sites, reinforcing its status as the largest U.S. provider. Teladoc’s Catapult integration deepens chronic-disease pathways and strengthens virtual check-up pipelines.

Technology shapes differentiation. Leaders embed predictive AI models that forecast injury risk days before incidents occur, allowing targeted interventions. Blockchain pilots slash administrative workload in multi-country credential management, while wearable vendors align with service firms to bundle hardware and clinical oversight. Emerging disruptors pitch subscription apps directly to gig-platform workers, bypassing traditional employer gatekeepers.

White-space remains in micro-enterprise coverage and in cross-border data-sharing frameworks where no single provider yet enjoys scale. Firms able to stitch together virtual, onsite, and mobile nodes under a unified analytics layer are best positioned to capture the next tranche of occupational health market growth.

Occupational Health Industry Leaders

AdvancedMD, Inc.

Examinetics

Kareo, Inc.

Optum, Inc.

Premise Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teladoc Health closed its USD 65 million Catapult Health purchase, adding at-home diagnostics and virtual preventive care for 3 million covered lives.

- January 2025: Concentra finalized the USD 265 million acquisition of Nova Medical Centers, lifting its U.S. clinic count to 770 and projecting USD 2.1 billion revenue for 2025.

- January 2025: Cority Software bought Meddbase to expand its cloud occupational health platform and deepen integration with enterprise HR systems.

Global Occupational Health Market Report Scope

As per the scope of the report, occupational health is a field dedicated to ensuring workers' safety, well-being, and performance in various professions. It involves identifying, preventing, and managing work-related injuries, illnesses, and hazards. The primary aim is to create safe work environments, enhance productivity, and support the long-term health of the workforce. This encompasses risk assessments, compliance with health and safety regulations, ergonomic practices, and wellness programs. The occupational health market is segmented by type, location, application, organization size, and geography. By type, the market is segmented into disease screening services, drug & alcohol testing services, health risk assessment services, healthcare services, physical examination services, and others. By location, the market is segmented into off-site, on-site, and telehealth services. By application, the market is segmented into physical wellbeing and social & mental wellbeing. By organization size, the market is segmented into Large Enterprises and SMEs. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America.

| Disease Screening Services |

| Drug & Alcohol Testing Services |

| Health Risk Assessment Services |

| Primary Care & Treatment Services |

| Vaccination & Immunization Services |

| Mental Health Services |

| Ergonomic & Physical Wellness Services |

| Return-to-Work & Disability Management Services |

| Others |

| On-Site Clinics |

| Near-Site Shared Clinics |

| Off-Site / External Clinics |

| Mobile Health Units |

| Telehealth / Virtual Occupational Health |

| Physical Wellbeing |

| Social & Mental Wellbeing |

| Chemical & Biological Exposure Management |

| Chronic Disease Management |

| Preventive & Lifestyle Management |

| Emergency & Trauma Management |

| Micro Enterprises (<10 employees) |

| Small Enterprises (10-49) |

| Medium Enterprises (50-249) |

| Large Enterprises (250-4,999) |

| Very Large Enterprises (5,000+) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Disease Screening Services | |

| Drug & Alcohol Testing Services | ||

| Health Risk Assessment Services | ||

| Primary Care & Treatment Services | ||

| Vaccination & Immunization Services | ||

| Mental Health Services | ||

| Ergonomic & Physical Wellness Services | ||

| Return-to-Work & Disability Management Services | ||

| Others | ||

| By Service Location | On-Site Clinics | |

| Near-Site Shared Clinics | ||

| Off-Site / External Clinics | ||

| Mobile Health Units | ||

| Telehealth / Virtual Occupational Health | ||

| By Application | Physical Wellbeing | |

| Social & Mental Wellbeing | ||

| Chemical & Biological Exposure Management | ||

| Chronic Disease Management | ||

| Preventive & Lifestyle Management | ||

| Emergency & Trauma Management | ||

| By Organization Size | Micro Enterprises (<10 employees) | |

| Small Enterprises (10-49) | ||

| Medium Enterprises (50-249) | ||

| Large Enterprises (250-4,999) | ||

| Very Large Enterprises (5,000+) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the occupational health market?

The occupational health market reached USD 5.84 billion in 2026 and is projected to grow to USD 7.76 billion by 2031.

Which service type is expanding fastest?

Mental health services are forecast to grow at a 10.47% CAGR, the quickest among all service categories.

Why are small businesses adopting occupational health programs now?

Telehealth platforms reduce upfront costs, enabling micro enterprises to subscribe to virtual occupational health packages that were previously unaffordable.

Which region will see the highest growth through 2031?

Asia-Pacific is expected to post the fastest regional CAGR at 7.92% as industrialization and regulatory enforcement accelerate demand.

How are regulations shaping market demand?

Global convergence around ISO 45001 and region-specific directives like EU-OSHA standards compel employers to adopt continuous monitoring, boosting long-term service uptake.

Page last updated on: