Mental Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

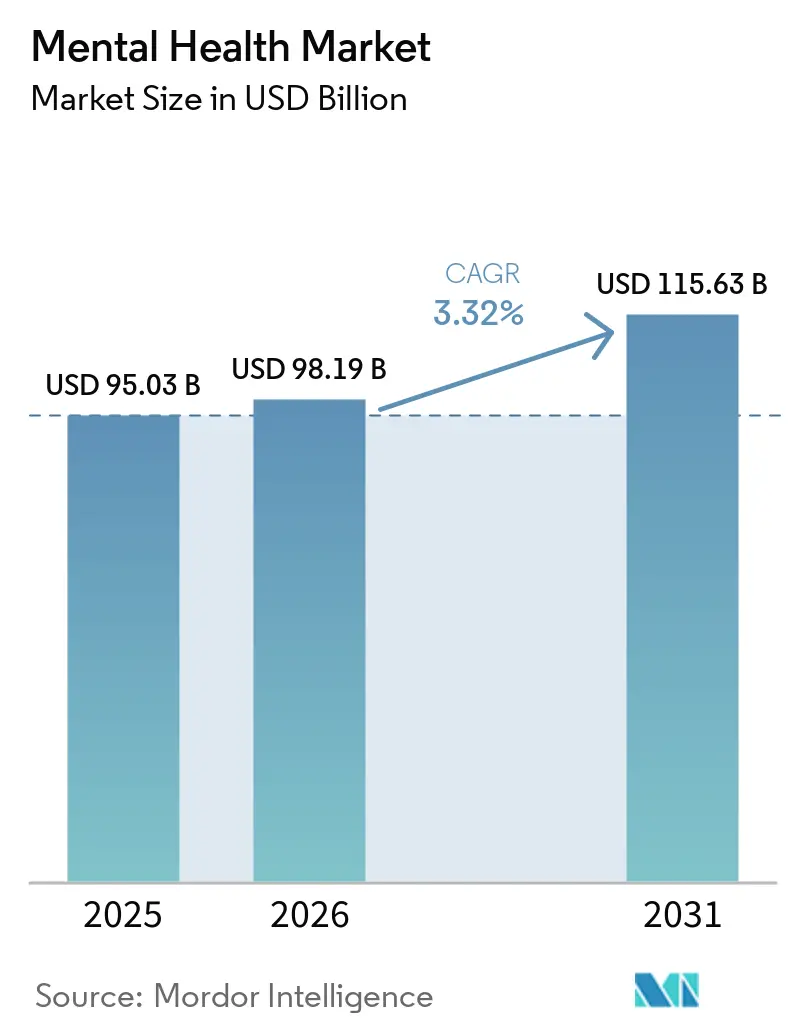

| Market Size (2026) | USD 98.19 Billion |

| Market Size (2031) | USD 115.63 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mental Health Market Analysis by Mordor Intelligence

The Mental Health Market size was valued at USD 95.03 billion in 2025 and is estimated to grow from USD 98.19 billion in 2026 to reach USD 115.63 billion by 2031, at a CAGR of 3.32% during the forecast period (2026-2031).

Uptake is shifting from brick-and-mortar therapy to reimbursed virtual visits as 14 U.S. states now enforce parity that treats behavioral and physical conditions equally. Employer-funded platforms absorbed 22% more sessions in 2025 than traditional employee assistance programs, while FDA-cleared software for anxiety and insomnia gained Medicare coverage after new CPT codes appeared in 2024. PTSD clinics opened by the U.S. Department of Veterans Affairs, together with community task-shifting models in low- and middle-income countries, are broadening reach even as psychiatrist density remains 1.9 per 100,000 population. Competitive intensity is rising because data-integrated apps such as Spring Health and Lyra Health cut time to care by roughly 40%, compressing margins for traditional providers.

Key Report Takeaways

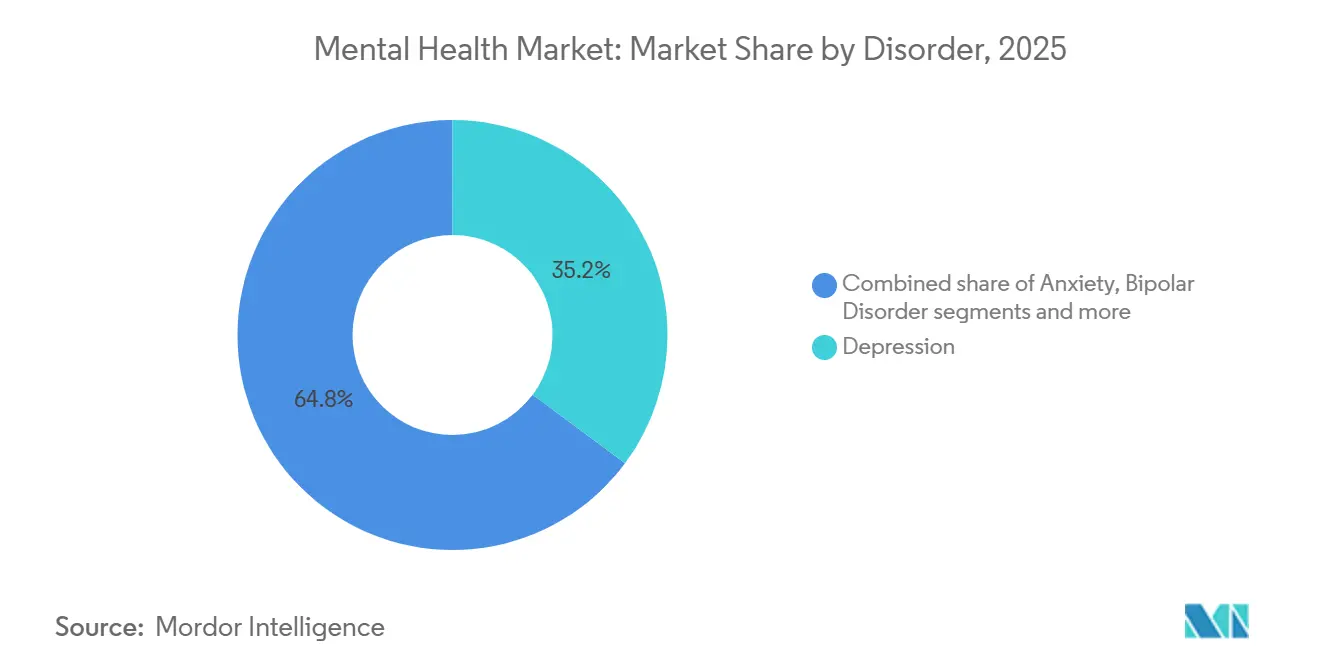

- By disorder, depression led with 35.18% revenue share in 2025, while PTSD is set to expand at a 5.22% CAGR through 2031.

- By service type, out-patient counseling held 42.21% of the mental health market share in 2025, whereas digital therapeutics are advancing at a 6.65% CAGR to 2031.

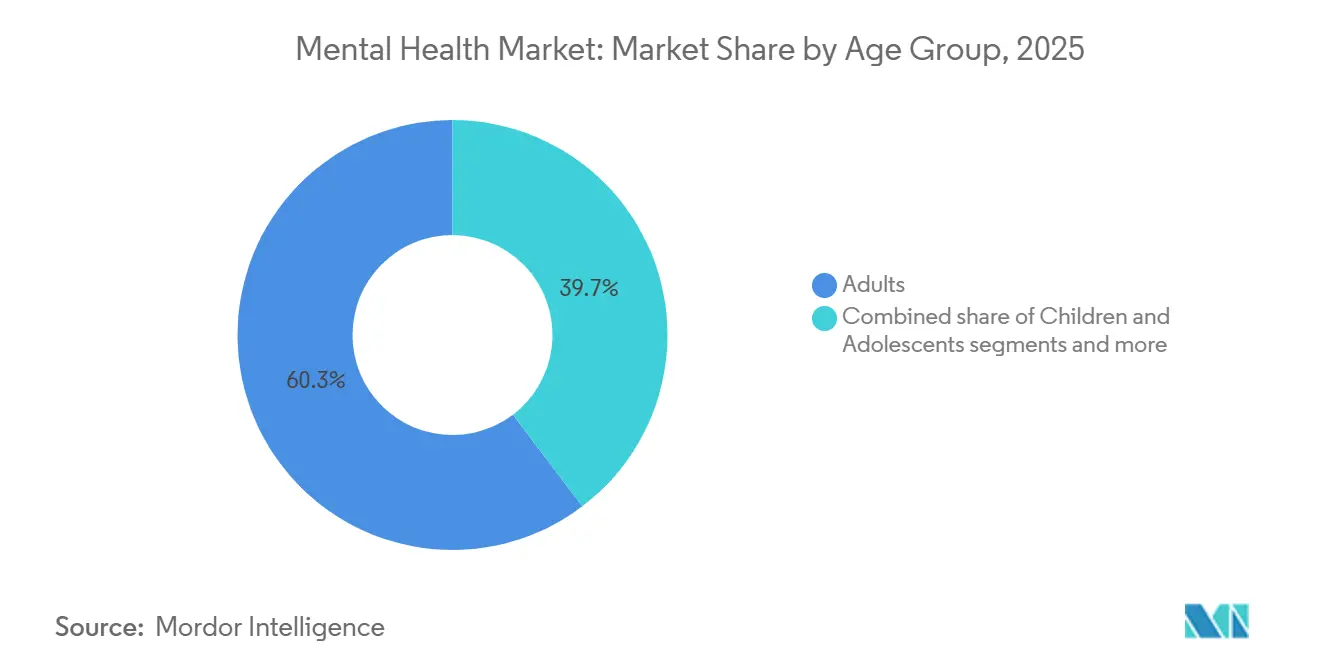

- By age group, adults aged 18–64 years captured 60.32% of spending in 2025, while the geriatric cohort is growing at a 5.12% CAGR over the same horizon.

- By end user, hospitals and clinics accounted for 45.56% share of the mental health market size in 2025, yet employers and corporate wellness platforms are progressing at a 6.98% CAGR.

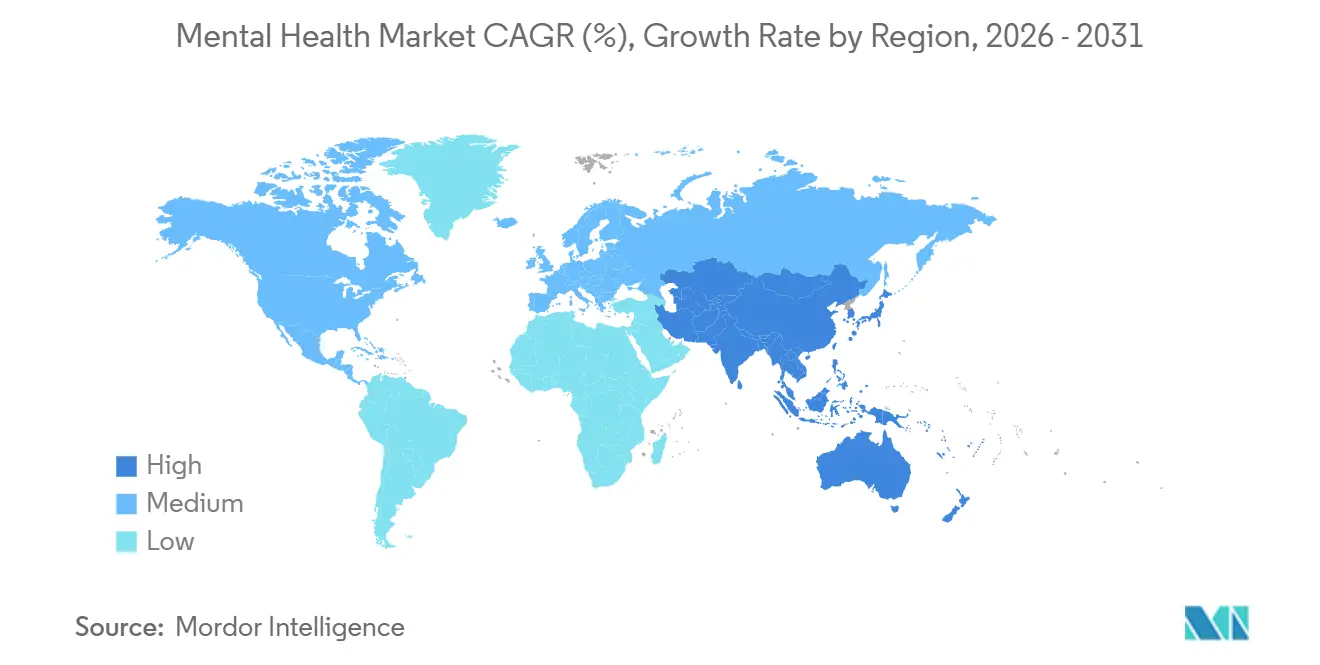

- By geography, North America led with 38.25% of global value in 2025 and Asia-Pacific is projected to record a 5.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mental Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of mental-health disorders | +0.9% | Global, strong in North America and Europe | Medium term (2–4 years) |

| Expanding adoption of tele-psychiatry and virtual care | +1.2% | North America and Europe core, rapid uptake in urban Asia-Pacific | Short term (≤2 years) |

| Government parity laws and policy initiatives | +0.7% | North America, selected EU states | Long term (≥4 years) |

| Increasing healthcare expenditure in LMICs | +0.5% | Asia-Pacific, Latin America, Sub-Saharan Africa | Long term (≥4 years) |

| AI-driven triage and personalized CBT platforms | +0.8% | North America, Western Europe, Australia | Medium term (2–4 years) |

| Employer-mandated wellbeing programs linked to ESG disclosure | +0.6% | Global, early adoption in North America and EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Mental-Health Disorders

Diagnosed cases of major depressive disorder rose 11% worldwide between 2020 and 2025, with the sharpest jump in adults aged 25–34 who entered demanding remote-work environments[1]Institute for Health Metrics and Evaluation, “Global Burden of Disease Study 2025,” healthdata.org. Anxiety now affects 301 million people, and North America saw a 9% uptick in substance-use comorbidity during 2024, which pushed metro emergency units to run at 94% capacity. Early-intervention programs in the United Kingdom trimmed first-episode psychosis admissions by 22% during 2024–2025 after mobile crisis teams began visiting within four hours of referral. The DSM-5-TR broadened criteria for avoidant or restrictive food intake disorder, triggering a 16% referral increase to specialists in 2025. Such epidemiological pressure heightens demand within the mental health market and reinforces the case for scalable community and digital models in LMICs where 90% of schizophrenia cases still go untreated.

Expanding Adoption of Tele-Psychiatry and Virtual Care

The DEA extended pandemic-era flexibilities for controlled substance prescribing via telemedicine to December 2026, sustaining a channel that covered 38% of outpatient psychiatric visits in 2025. Medicare beneficiaries conducted 14.2 million tele-behavioral sessions during that year after CMS made the home an eligible originating site, thereby removing historic geographic barriers. In Europe, EMA guidance affirmed that digital therapeutics can be prescribed alongside medication, accelerating price-negotiation cycles in Germany, France, and the Netherlands. Japan approved online initial consultations for psychiatric care in 2024 and by late 2025 tele-psychiatry accounted for 19% of outpatient visits in its two largest prefectures. Licensing reciprocity remains partial as only 39 U.S. states belong to the Interstate Medical Licensure Compact, fragmenting provider networks and raising acquisition costs for multistate platforms.

Government Parity Laws and Policy Initiatives

The U.S. Consolidated Appropriations Act of 2024 compelled group health plans to reimburse services delivered by licensed social workers and family therapists at the same rate as psychologists, adding 180,000 in-network providers in 2025. The EU Mental Health Strategy earmarked EUR 1.23 billion for integration of screening into primary care, with pilot sites already live in Poland, Portugal, and Greece. Australia pledged AUD 2.3 billion over four years to expand Headspace youth centers and to finance 60 new adult clinics, widening access in regional districts. Amendments to South Korea’s Mental Health Welfare Act mandated yearly workplace assessments for firms with more than 50 staff, cutting crisis-hotline wait times to under three minutes by mid-2025. These statutes shorten the commercialization cycle for digital therapeutics inside the mental health market because payers no longer require long bespoke negotiations.

Increasing Healthcare Expenditure in LMICs

Median mental-health budgets in LMICs climbed from 1.9% to 2.8% of total health spending between 2020 and 2025. India lifted National Mental Health Programme funding to INR 9,500 crore for 2025–2026 to establish 50 Centers of Excellence and train 10,000 physicians in mhGAP protocols. Brazil expanded its CAPS network to 3,160 units by end-2025, achieving 24-hour crisis cover in 18 capitals. Indonesia integrated mental-health screening into its national insurance scheme covering 224 million members and set aside IDR 4.2 trillion for community teams. Vietnam’s 2024–2030 plan trains 5,000 commune health workers and funds 30 district psychiatric wards. Private platforms quickly follow public money; Teladoc Health signed with Apollo Hospitals in August 2025 to pilot tele-psychiatry across 15 tier-2 Indian cities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social stigma in seeking treatment | -0.6% | Global, most acute in Asia-Pacific, Middle East, and rural areas | Long term (≥4 years) |

| Shortage of qualified mental-health professionals | -0.8% | Global, severe in LMICs and rural North America | Long term (≥4 years) |

| Data-privacy and cybersecurity concerns for digital therapeutics | -0.4% | North America, Europe, Australia | Medium term (2–4 years) |

| Reimbursement loopholes in cross-border tele-health | -0.5% | Global, concentrated in cross-state United States and intra-EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Social Stigma in Seeking Treatment

Cultural norms cast mental illness as personal weakness in parts of East Asia and the Middle East, deterring care. A 2024 APEC survey showed 61% of respondents in Indonesia, Malaysia, and the Philippines would hide a diagnosis from employers and 48% of parents opposed school screening[2]Asia-Pacific Economic Cooperation, “Mental Health Stigma Survey 2024,” apec.org. Japan’s national anti-stigma campaign launched in 2024 failed to lift treatment-seeking above 29% in 2025. Gulf nations reported that 72% of anxiety cases relied on family or religious support over licensed clinicians in 2025. Meta-analysis across Brazil, South Africa, and India confirmed that combining media outreach with lived-experience contact cut discriminatory attitudes by 12 points, yet funding is sporadic. Persistent stigma slows uptake in the mental health market and drags overall growth.

Shortage of Qualified Mental-Health Professionals

Global psychiatrist density of 1.9 per 100,000 remains one-fifth of the WHO adequacy benchmark. Sixty-three percent of U.S. counties had zero child psychiatrists in 2025, leaving pediatricians to handle complex cases. Sub-Saharan Africa employed just 1,400 psychiatrists for 1.2 billion people, and 14 countries lack residency programs. Although 12 new U.S. residency programs opened in 2024–2025, attrition of 18% undermines gains. Task-shifting where community health workers deliver manualized psychotherapy achieved remission rates above 52% in trials across Ethiopia, Nepal, and Pakistan, but only 34% of mhGAP-trained staff kept delivering services 12 months later because supervision waned.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disorder: PTSD Outpaces Depression Growth

Depression generated 35.18% of 2025 revenue, yet PTSD is projected to increase at a 5.22% CAGR, faster than the overall mental health market. Veterans Affairs opened 18 outpatient PTSD clinics in fiscal 2025, and tele-based prolonged exposure therapy achieved a 58% symptom drop among 1,240 participants[3]U.S. Department of Veterans Affairs, “PTSD Clinic Expansion 2025,” va.gov. Anxiety remains the second-largest category, supported by app-based CBT that bypasses prescriber gatekeepers. Bipolar disorder and schizophrenia rely on inpatient or intensive outpatient management, but long-acting injectables trimmed relapse risk by 30% in a 2024 meta-analysis. Eating disorders rose after DSM-5-TR revisions widened ARFID criteria, and 120,000 users engaged NOCD’s exposure-based program in 2025.

Historical dominance by depression and anxiety is moderating. Public health systems now emphasize trauma-related and geriatric-specific conditions, widening reimbursement for PTSD therapies in the United States, Canada, and Australia. Schizophrenia and bipolar segments are shifting toward community care because injectables reduce hospitalization. Collectively these trends support a diversified mental health market portfolio and widen opportunities for specialized tools.

By Service Type: Digital Therapeutics Reshape Delivery

Out-patient counseling commanded 42.21% revenue in 2025, but FDA-cleared digital therapeutics and tele-psychiatry are projected to lead service growth at a 6.65% CAGR, double the mental health market average. Adaptive software posted a 68% completion rate versus 51% for static modules in a 2025 study. Virtual visits comprised 38% of outpatient contacts after DEA kept prescribing flexibilities through 2026. In-patient stays shortened from 8.2 to 7.1 days between 2023 and 2025 as hospitals deployed step-down programs. Mobile crisis units such as New York City’s B-HEARD program diverted 87% of non-violent incidents from emergency rooms in 2025.

CMS reimbursement unlocked Medicare coverage for prescription apps, prompting 78% of commercial plans to follow suit by December 2025. Tele-psychiatry’s share may plateau once pandemic waivers expire and licensing reciprocity stalls, yet asynchronous chat programs still attract users despite being excluded from Medicare Part B in March 2025. Overall, digital modalities are solidifying as a core pillar inside the mental health market.

By Age Group: Geriatric Segment Gains Momentum

Adults aged 18–64 years spent 60.32% of total outlays in 2025, propelled by workplace stress and substance comorbidity. The geriatric cohort is accelerating at a 5.12% CAGR because Medicare Advantage bundles dementia behavioral interventions with primary care, cutting antipsychotic use by 28% in a nursing-home study covering 1,800 residents. Pediatric demand is rising as emergency mental-health visits grew 18% in 2024–2025. School-based counselors reduced initial assessment wait times to under ten days across 14,000 U.S. schools. Geriatric momentum reflects demographic aging; the group will number 1.5 billion globally by 2030, doubling dementia prevalence every five years after age 65.

Adult dominance faces saturation because only 48% of diagnosed adults seek care despite broader coverage. Tele-psychiatry is helping children in underserved counties where no child psychiatrist practices, covering 44% of pediatric sessions in 2025. Altogether, shifting age dynamics diversify demand inside the mental health market.

By End User: Corporate Wellness Platforms Surge

Hospitals and clinics captured 45.56% revenue in 2025, yet employer platforms are advancing at a 6.98% CAGR as ESG rules force disclosure of workforce mental-health metrics. Spending per employee reached USD 340 in 2025, and Modern Health plus BetterUp each saw contract growth above 28% after offering culturally responsive care modules. Community mental-health centers raised capacity 7% thanks to cost-based CCBHC grants. Home-based crisis teams cost 60% less than emergency rooms and are gaining insurer approval. Telehealth-only platforms, schools, and corrections round out the “Others” group, demonstrating 71% satisfaction in a Talkspace survey of 8,400 users.

Corporate wellness momentum signals a structural pivot in the mental health market from discretionary perk to retention necessity. Hospitals will still dominate acute care but face slower growth because value-based models punish readmissions. Future share shifts will depend on sustained CCBHC funding and licensure reform.

Geography Analysis

North America generated 38.25% of global revenue in 2025, supported by high health spending and parity legislation that added 180,000 providers to insurer networks. Medicare and Medicaid covered 14.2 million tele-behavioral sessions, while Canada cut out-of-pocket psychotherapy costs by 40% in three provinces after public reimbursement. Mexico added 120 IMSS outpatient clinics in 2024–2025, yet stigma keeps treatment-seeking below 30%. The region’s CAGR trails Asia-Pacific because insurance enrollment is near saturation and DEA waivers may sunset in 2026, capping tele-health investment. Competition is fierce with 12 listed platforms and 300 startups, driving 9% price erosion in 2025 session fees.

Europe held the second-largest share in 2025, underpinned by EUR 1.23 billion EU4Health funding for primary-care screening. Germany’s amended Digital Healthcare Act expanded DiGA listings to 14 digital therapeutics, and the United Kingdom invested GBP 2.3 billion to cut first-episode psychosis admissions by 22%. France’s national hotline logged 1.2 million calls in its first year. Southern Europe lacks community infrastructure; psychiatrist ratios in Italy are half those in Germany, keeping inpatient reliance high. The Corporate Sustainability Reporting Directive is spurring employer coverage, already adopted by 54% of midsize enterprises in three core EU markets.

Asia-Pacific is forecast to grow at 5.68% CAGR, the fastest among regions. China injected CNY 12 billion in 2024 to upgrade psychiatric hospitals and train 15,000 workers, and 320 cities now run 24-hour hotlines. India expanded its program into 150 new districts and raised funding to INR 9,500 crore for 2025–2026. Japan approved online initial consults and reached 19% tele-psychiatry share by end-2025. Australia committed AUD 2.3 billion to add 45 youth centers and 60 adult clinics. Workforce scarcity restricts Southeast Asia; Indonesia, the Philippines, and Vietnam employ fewer than 2,000 psychiatrists but pilot task-shifting across 80 districts.

Africa, the Middle East, and South America make up the balance. Brazil expanded CAPS to 3,160 units by 2025. South Africa funded integration into 1,200 primary clinics with ZAR 4.8 billion in 2024. Gulf nations still rely on informal care for 72% of anxiety sufferers. Argentina’s new tele-psychiatry portal delivered 85,000 consults during its first year. Sub-Saharan Africa’s extreme provider shortage and out-of-pocket models continue to suppress demand despite community pilot programs.

Competitive Landscape

The mental health market is fragmented, as the top five players control a notable share because state licensure limits cross-border expansion and care remains heterogenous. Universal Health Services ran 335 behavioral facilities yet still held below 8% of United States spending in 2025. Acadia Healthcare’s 250 sites ranked second but also failed to cross that 8% mark. Virtual-first providers are scaling quickly: Teladoc Health’s BetterHelp handled 4.2 million video sessions in 2025, up 19% year over year, and Talkspace’s enterprise arm grew 34% through 200 corporate deals covering 12 million workers. Spring Health’s AI engine cut appointment lead time by 40% for 8 million covered lives, and Lyra Health enabled same-day triage for 89% of referrals. Peer-support site 7 Cups enrolled 42 million users globally by 2025, illustrating consumer appetite beyond clinical channels.

Regulation shapes rivalry. HHS levied USD 4.8 million in HIPAA fines on three apps in 2025, prompting widespread encryption upgrades. The MHRA will require annual algorithm audits starting 2026, raising compliance costs that smaller entrants may struggle to meet. Lyra Health secured a U.S. patent that predicts therapy dropout, reducing attrition by 18% among 6,000 patients. CMS still bars Medicare payment for asynchronous messaging, forcing platform workflow redesign in 2025. Only 39 states belong to the licensure compact, limiting nationwide scale. Despite headwinds, employer demand, AI innovation, and global policy support keep the mental health market vibrant.

Mental Health Industry Leaders

Universal Health Services

Acadia Healthcare

Teladoc Health

CVS Health

Centene Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Government of India launched the National Mental Health Programme (NMHP). As part of the initiative, the District Mental Health Program (DMHP) is being implemented in 767 districts, supported by the National Health Mission. DMHP services at Community Health Centers (CHCs) and Primary Health Centers (PHCs) include outpatient care, assessments, counseling, psychosocial interventions, support for severe mental disorders, medication, outreach, and ambulance services.

- December 2025: UNICEF and WHO commend Nepal for launching the National Mental Health Campaign 2025 to address child and youth challenges.

Global Mental Health Market Report Scope

As per the scope of the report, mental health includes emotional, psychological, and social well-being. An altered mental health condition is considered a mental illness, which includes depression, anxiety disorder, schizophrenia, eating disorders, and addictive behaviors.

The mental health market is segmented by disorder, service type, age group, end user, and geography. By disorder, the market includes depression, anxiety, bipolar disorder, schizophrenia, substance-use disorders, eating and feeding disorders, post-traumatic stress disorder (PTSD), and other disorders. By service type, it covers in-patient treatment, out-patient counseling, emergency mental-health services, virtual and tele-psychiatry, digital therapeutics and apps, community-based rehabilitation services, and others. By age group, the segmentation includes children and adolescents (0-17 years), adults (18-64 years), and geriatric (65 years and above). By end user, the market is categorized into hospitals and clinics, community mental-health centers, home-care settings, employers and corporate wellness platforms, and others. By geography, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Depression |

| Anxiety |

| Bipolar Disorder |

| Schizophrenia |

| Substance-Use Disorders |

| Eating & Feeding Disorders |

| Post-Traumatic Stress Disorder (PTSD) |

| Other Disorders |

| In-patient Treatment |

| Out-patient Counselling |

| Emergency Mental-Health Services |

| Virtual & Tele-psychiatry |

| Digital Therapeutics & Apps |

| Community-based Rehabilitation Services |

| Others |

| Children & Adolescents (0-17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (65 yrs +) |

| Hospitals & Clinics |

| Community Mental-Health Centres |

| Home-care Settings |

| Employers & Corporate Wellness Platforms |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disorder | Depression | |

| Anxiety | ||

| Bipolar Disorder | ||

| Schizophrenia | ||

| Substance-Use Disorders | ||

| Eating & Feeding Disorders | ||

| Post-Traumatic Stress Disorder (PTSD) | ||

| Other Disorders | ||

| By Service Type | In-patient Treatment | |

| Out-patient Counselling | ||

| Emergency Mental-Health Services | ||

| Virtual & Tele-psychiatry | ||

| Digital Therapeutics & Apps | ||

| Community-based Rehabilitation Services | ||

| Others | ||

| By Age Group | Children & Adolescents (0-17 yrs) | |

| Adults (18-64 yrs) | ||

| Geriatric (65 yrs +) | ||

| By End User | Hospitals & Clinics | |

| Community Mental-Health Centres | ||

| Home-care Settings | ||

| Employers & Corporate Wellness Platforms | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the mental health market in 2026 and where is it headed by 2031?

Spending stands at USD 98.19 billion in 2026 and is on track to reach USD 115.63 billion by 2031, reflecting a 3.32% CAGR.

Which therapy channels are growing fastest in mental healthcare?

FDA-cleared digital therapeutics and tele-psychiatry are advancing at a 6.65% CAGR, roughly double the overall growth rate.

Why are employers increasing mental-health benefit spending?

IFRS S1 & S2 disclosure rules link executive pay to workforce wellbeing metrics, pushing per-employee outlays up 18% to USD 340 in 2025.

What is driving Asia-Pacific's rapid expansion in mental-health services?

Government investments, such as China's CNY 12 billion hospital upgrade and India's INR 9,500 crore program, are propelling a 5.68% CAGR through 2031.

Which regulatory changes most affect digital therapeutics reimbursement?

CMS's 2024 CPT codes opened Medicare coverage, while DEA tele-prescribing flexibilities and EU DiGA listings smooth commercial adoption through 2026.

Page last updated on: