Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

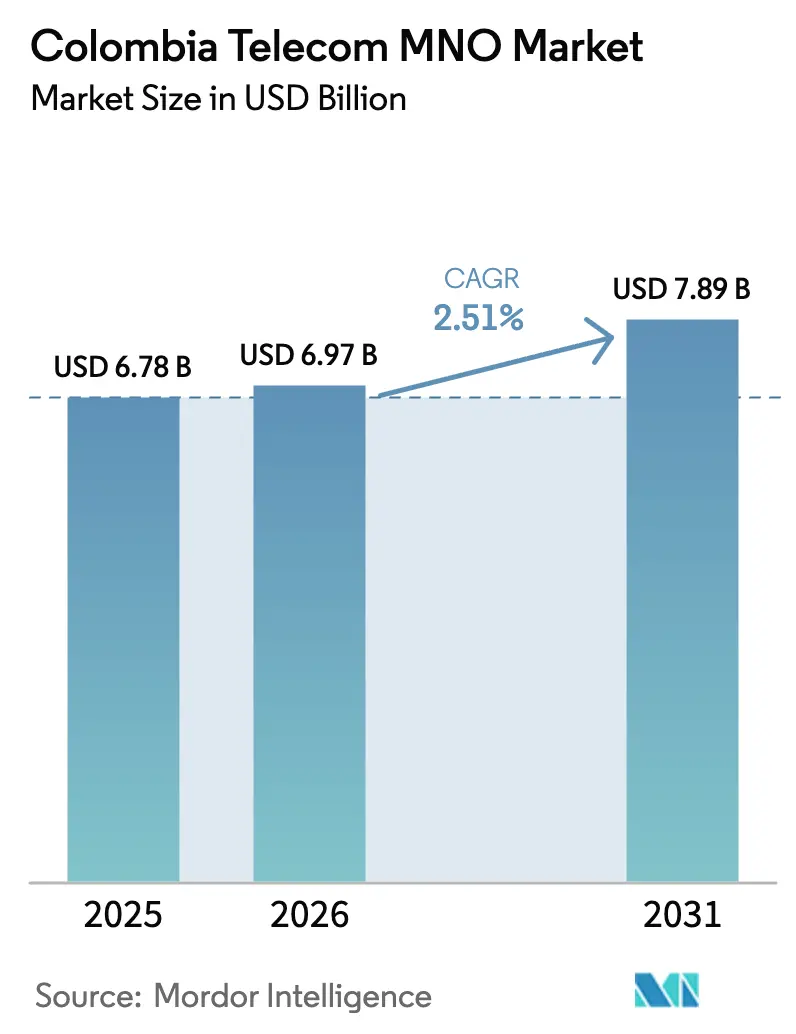

| Base Year Market Size (2025) | USD 6.78 Billion |

| Market Size (2026) | USD 6.97 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 2.51% CAGR |

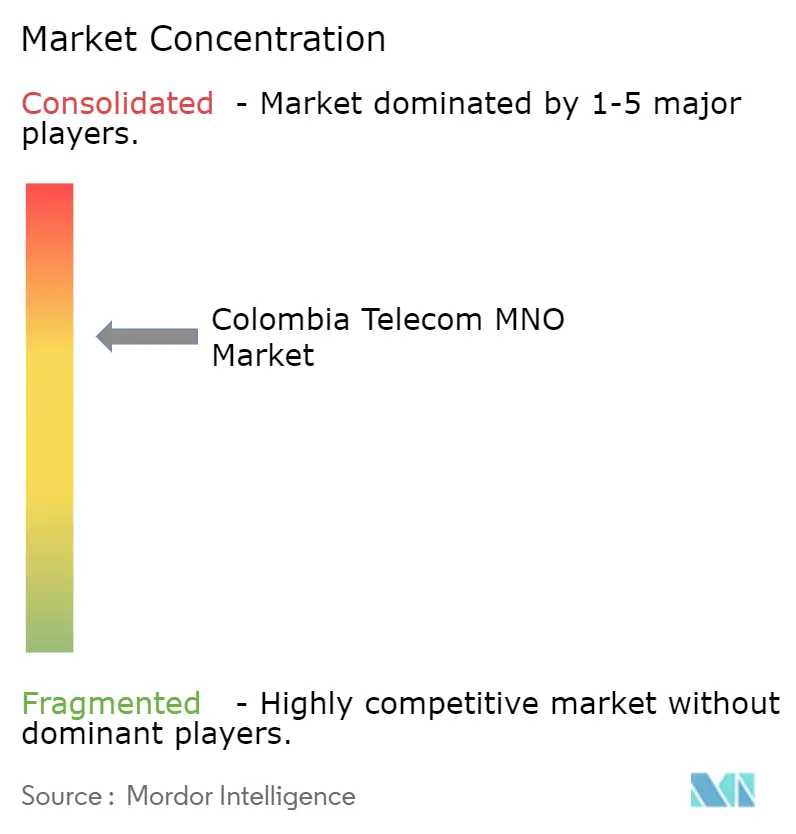

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Telecom MNO Market Analysis by Mordor Intelligence

The Colombia telecom MNO market size is projected to be USD 6.78 billion in 2025, USD 6.97 billion in 2026, and reach USD 7.89 billion by 2031, growing at a CAGR of 2.51% from 2026 to 2031. Robust fiber backhaul investments, 5G spectrum deployment, and a pivot toward enterprise-grade private networks underpin this moderate expansion even as consumer data tariffs remain under pressure. Operators are tilting capital toward low-latency edge infrastructure that can support network slicing for manufacturers and logistics hubs, a strategy that stabilizes margins against decelerating consumer ARPU. Consolidation momentum, most notably Millicom’s integration of Movistar, creates a scaled challenger to Claro and accelerates rural coverage through shared infrastructure. Satellite-terrestrial backhaul partnerships meanwhile compress the rural usage gap by lowering per-subscriber acquisition costs in low-density municipalities.

Key Report Takeaways

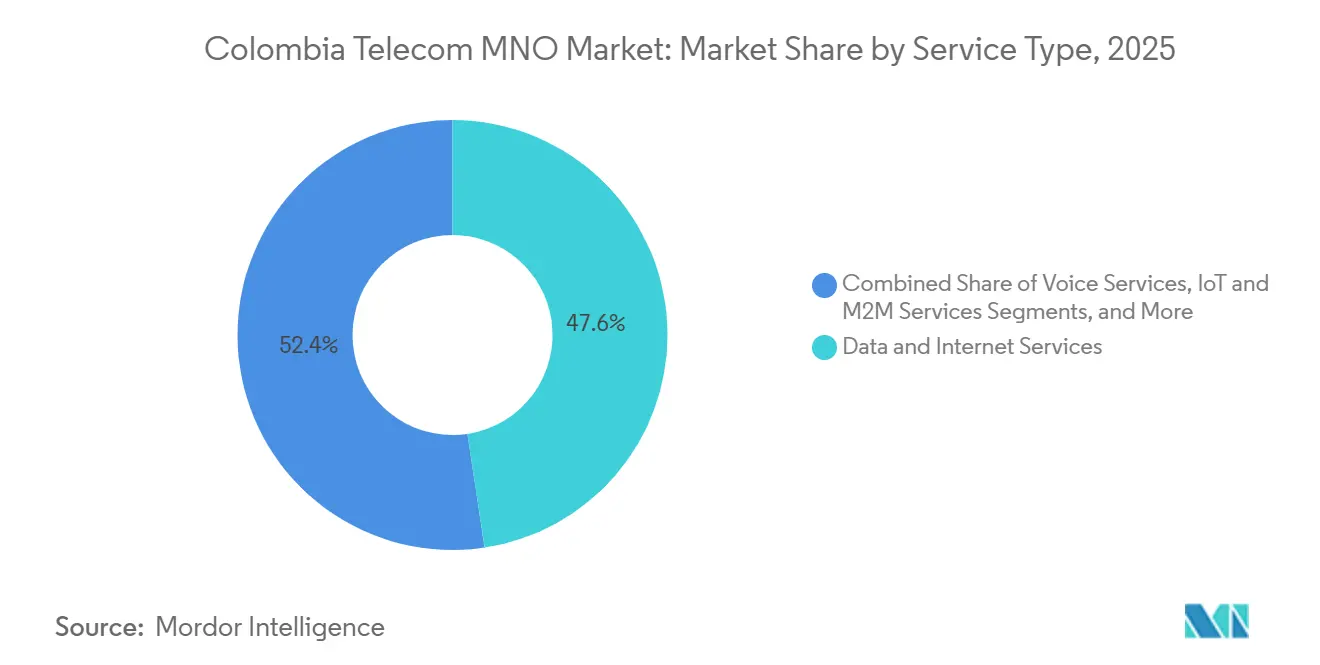

- By service type, Data and Internet services led with a 47.62% revenue share of the Colombia telecom MNO market in 2025. IoT and M2M services are forecast to expand at a 2.89% CAGR to 2031, the fastest growth among all service categories.

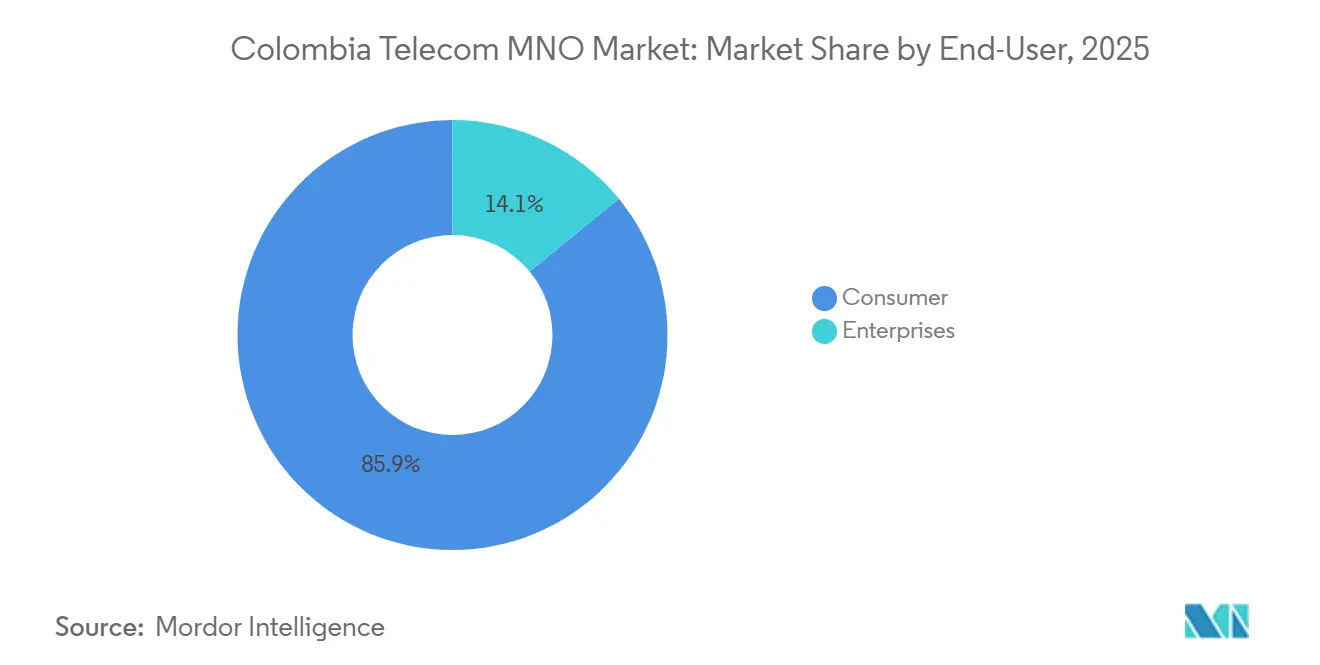

- By end user, consumer subscribers captured 85.94% of 2025 revenue, while the enterprise segment is projected to grow at a 3.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Auction 5G Spectrum Rollout Accelerating Enterprise Digitalization | +0.6% | Nationwide, Early Gains in Bogotá, Medellín, Cali, Barranquilla | Medium Term (2–4 Years) |

| Rapid FTTH Build-Outs in Secondary Cities by Tier-1 Operators | +0.5% | Cundinamarca, Atlántico, Valle del Cauca | Medium Term (2–4 Years) |

| Surge in Mobile-Only Households Boosting Wireless ARPU | +0.4% | Urban and Peri-Urban Areas | Short Term (≤ 2 Years) |

| Network-Sharing Accords Among Carriers Lowering Rural Coverage Capex | +0.3% | Amazonas, Guainía, Chocó | Long Term (≥ 4 Years) |

| API Monetization via GSMA Open Gateway Unlocking New B2B Revenue Streams | +0.2% | Enterprise Clusters Nationwide | Medium Term (2–4 Years) |

| Satellite Backhaul Agreements Enabling Affordable Remote Coverage | +0.2% | Remote Rainforest Regions | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Post-Auction 5G Spectrum Rollout Accelerating Enterprise Digitalization

The December 2023 allocation of 3.5 GHz airwaves gave operators 200 MHz of contiguous spectrum, allowing non-stand-alone 5G networks to blanket more than 50 cities by early 2025. Claro’s 1,600 active 5G sites already support 5 million users, but the strategic lift comes from industrial slices that guarantee sub-20 ms latency for robotics and real-time logistics monitoring.[1]Claro Colombia Press Releases, “5G Deployment Updates,” claro.com.co Manufacturers in Cundinamarca signed multi-year private-network contracts priced at three to five times consumer ARPU, turning spectrum into a premium B2B input.[2]América Móvil Investor Relations, “Financial Information,” americamovil.com Regulatory quality-of-service thresholds issued by the CRC protect these verticals from capacity dilution. As more low-latency edge nodes launch, the Colombia telecom MNO market gains a repeatable enterprise revenue engine.

Rapid FTTH Build-Outs in Secondary Cities by Tier-1 Operators

Fiber overtook cable as the dominant fixed line technology in 2024, and tier-1 carriers extended gigabit coverage to mid-tier cities such as Barranquilla and Pasto. Claro’s COP 30 billion (USD 7.7 million) spend in Barranquilla during 2025 laid 503 km of new fiber, delivering symmetrical speeds that cater to remote workers and SMEs. Bundled fiber-mobile packages reduce churn and offload high-volume residential traffic from mobile spectrum, freeing 4G and 5G capacity for IoT. MinTIC’s dark-fiber leasing rules further accelerate reach by letting regional ISPs piggy-back on tier-1 backbones.[3]MinTIC, “Connectivity Programs,” mintic.gov.co These converged strategies raise household data ceilings and lift blended ARPU, sustaining topline growth for the Colombia telecom MNO market.

Surge in Mobile-Only Households Boosting Wireless ARPU

About 35-40% of urban households abandoned fixed broadband in 2025 and switched to tiered unlimited mobile plans that include 100 GB to 200 GB fair-use thresholds. These subscribers consume up to 70% more data than dual-service users, expanding wireless ARPU even as inflation weighs on discretionary spend.[4]Banco de la República, “Monetary Policy and Inflation Report,” banrep.gov.co Operators have responded with differentiated price points, capturing premium margins without alienating prepaid segments. The CRC tracks substitution trends quarterly to prevent capacity hoarding that could inflate tariffs. The phenomenon strengthens revenue diversity and cushions the Colombia telecom MNO market against fixed-line erosion.

Network-Sharing Accords Among Carriers Lowering Rural Coverage Capex

Tigo and Movistar’s joint venture pools 1,500 rural towers and slices per-site capex by up to 50%. Shared environmental permitting shortens rollout cycles to six months, and combined radio equipment halves energy costs for low-load sites. The model shines in Amazonas and Guainía, where subscriber density is under 10 users/km². Claro prefers a Starlink backhaul route, but the CRC permits both strategies as long as retail brands remain distinct. Lower capital intensity lets operators redirect savings toward urban 5G densification, sustaining service quality and profitability for the Colombia telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic Slowdown Compressing Discretionary Data Spend | -0.4% | Nationwide | Short Term (≤ 2 Years) |

| High Tower Rental and Energy Costs Pressuring EBITDA Margins | -0.3% | National, Acute in Remote Areas | Medium Term (2–4 Years) |

| Persistently High Rural Usage Gap Despite Nationwide Coverage | -0.2% | Amazonas, Guainía, Chocó | Long Term (≥ 4 Years) |

| Legal Challenges Over Incumbent Market Dominance Delaying Network Consolidation | -0.2% | Nationwide Regulatory Proceedings | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Macroeconomic Slowdown Compressing Discretionary Data Spend

GDP growth cooled to 2.5-2.8% in 2025-2026 while inflation hovered above 5%, prompting the central bank to hold its policy rate at 9.25%. Prepaid top-ups fell 5-7% y-o-y in early 2025 as households prioritized staples over larger data bundles. Fiscal constraints limit universal-service subsidies, shifting the rural coverage burden entirely to operators. The pressure caps short-term ARPU and chips 0.4 percentage points off the forecast CAGR for the Colombia telecom MNO market.

High Tower Rental and Energy Costs Pressuring EBITDA Margins

Energy and lease expenses now absorb nearly one-third of mobile OPEX, with diesel volatility inflating remote-site costs. Towercos indexed rents to inflation, lifting annual lease escalators to 5-8%. Carriers are retrofitting 1,500-2,000 sites with solar and batteries, but payback stretches to four years. SBA Communications sold 206 towers in 2024, underscoring capital flight from an unfavorable lease environment. Elevated operating costs shave 0.3 percentage points from CAGR forecasts for the Colombia telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Enterprise IoT Outpaces Consumer Data Growth

Data and Internet services delivered 47.62% of 2025 revenue, anchoring the Colombia telecom MNO market share leadership at the category level. Growth, however, is slowing as average smartphone consumption nears 10 GB/month and price competition intensifies. By contrast, IoT and M2M connections are scaling at a 2.89% CAGR, helped by logistics telematics and precision-agriculture sensors that require guaranteed low-bandwidth connectivity. Private LTE slices inside automotive plants in Cundinamarca are priced at premiums worth three to five times consumer ARPU, a margin enhancer for operators. SMS and circuit-switched voice continue a managed retreat as OTT apps dominate, while bundled PayTV and OTT video contribute a stable mid-single-digit share despite content cost drag. Over the forecast horizon, operators will sunset 2G and 3G bands, forcing legacy M2M devices to migrate to NB-IoT; the upgrade cycle will widen the Colombia telecom MNO market size for IoT services.

Growth prospects favor machine-centric segments because spectrum refarming and network slicing enable differentiated SLAs unreachable in the best-effort consumer internet tier. Regulatory exemptions that free IoT SIMs from consumer-protection disclosure shorten enterprise sales cycles and support faster activation. As 5G SA cores launch from 2027 onward, ultra-reliable low-latency communication will open additional verticals such as autonomous mining trucks in Antioquia. Collectively, these dynamics shift revenue composition toward high-stickiness enterprise contracts, broadening the recurring portion of the Colombia telecom MNO market.

By End User: Enterprise Margins Trump Consumer Volume

Consumer lines represented 85.94% of 2025 revenue, but penetration already exceeds 130% of the population, limiting fresh subscriber adds. Enterprises, though smaller in volume, are forecast to grow at 3.21% through 2031 as IoT, network slicing, and API monetization take hold. Financial institutions now embed carrier Number Verification APIs into onboarding flows, paying per-transaction fees that carry 90% gross margins. Logistics companies are replacing satellite GPS trackers with NB-IoT tags that cost one-tenth as much and integrate seamlessly into carrier billing, lifting the Colombia telecom MNO market size for enterprise contracts.

On the consumer side, mobile-only households are boosting traffic and partially offsetting prepaid spending softness. Unlimited plans anchored at 100-GB tiers segment higher-value customers without alienating price-sensitive users. Nevertheless, competition from four facilities-based operators compresses headline ARPU growth. Regulatory oversight ensures consumer surplus is protected, even as operators pursue fatter enterprise margins. The dual-speed demand curve will keep blended growth modest but steady, preserving a sustainable cash flow profile across the broader Colombia telecom MNO market.

Geography Analysis

Colombia’s rugged topography fragments network economics, making regional strategy pivotal. Bogotá and Medellín account for roughly 45% of mobile revenue thanks to dense population and corporate clusters that favor 5G monetization. Secondary cities such as Cali and Barranquilla are fast followers: Claro invested COP 30 billion (USD 7.7 million) in Barranquilla’s fiber build in 2025, widening converged uptake and pushing the local Colombia telecom MNO market share for fixed-mobile bundles past 60%.

In contrast, remote departments in Amazonas and Guainía register 96% population coverage but only 65-70% active internet usage, reflecting affordability hurdles. SES’s O3b mPOWER constellation now backhauls traffic from micro-cells that serve fewer than 100 subscribers, trimming cost per rural user by 30-40%. MinTIC’s Centres Digitales Wi-Fi program anchors tower demand but touches just 3% of residents, so operators rely on shared sites to stretch scarce capex.

Valle del Cauca and Antioquia showcase a third archetype, where export-oriented agribusiness deploys dense sensor networks for soil-moisture and pest control. These verticals lift IoT penetration far above the national mean, expanding the Colombia telecom MNO market size within enterprise corridors. Spectrum is plentiful here because consumer load is moderate, letting carriers pilot standalone 5G slices for autonomous drones without congesting retail traffic. The geographic patchwork means operators must juggle three playbooks, urban densification, shared rural coverage, and vertical-specific IoT, to capture full-stack growth.

Competitive Landscape

Claro retains 50.4% of total mobile subscribers and 68.7% of the nascent 5G base, yet structural concentration is easing as Millicom completed its USD 214.4 million purchase of Movistar in February 2026. The Tigo-Movistar combination will control roughly 35-40% of subscriber lines, creating a scaled rival that can challenge Claro on spectrum depth and rural penetration. SIC conditioned the deal on wholesale MVNO access and enterprise-rate caps, ensuring downstream competition persists.

WOM’s January 2025 restructuring under SUR Holdings preserved a fourth facilities-based operator, a critical check on potential duopoly pricing in peri-urban zones. Its three-year grace period on spectrum fees diverts cash to network expansion in underserved corridors. Strategic differentiation now centers on enterprise IoT stacks, gigabit fiber expansion, and API monetization via the GSMA Open Gateway, all of which promise margin lift uncorrelated with consumer subscriber volume. Claro filed 47 edge-computing patents in 2024-2025, signaling a pivot toward private 5G and low-latency analytics that smaller peers may struggle to mirror.

Tower economics remain a friction point. Lease escalators and high diesel costs erode EBITDA, prompting carriers to exit non-core sites or retrofit renewables. SBA Communications’ 2024 exit illustrates investor caution. Operators answer with joint rural builds and selective urban densification, balancing capex discipline with service-quality mandates. The net result is a tri-polar competitive field where Claro guards incumbency, the new Tigo-Movistar entity scales converged bundles, and WOM plays price disruptor in high-churn prepaid pockets, collectively shaping the trajectory of the Colombia telecom MNO market.

Colombia Telecom MNO Industry Leaders

Claro Colombia

Movistar Colombia

Tigo Colombia

WOM Colombia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Millicom closed the USD 214.4 million acquisition of Telefónica’s 67.5% stake in Movistar Colombia, gaining 12 million subscribers and multi-band spectrum holdings.

- February 2026: Claro, Movistar, and Tigo launched GSMA Open Gateway APIs that deliver SIM-swap and number-verification functionality to fintech apps, cutting authentication costs by up to 70%.

- January 2026: Claro announced 5 million 5G users across 50 cities and committed to doubling its 5G footprint in 2026 with an enterprise-first rollout priority.

- November 2025: SIC approved the Tigo-Movistar merger with MVNO access obligations and enterprise-rate caps to safeguard downstream competition.

Colombia Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.

The Colombia Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How Large Will Colombia's Mobile Network Operator Revenue Pool Be in 2031?

Forecasts put it at USD 7.89 billion, reflecting a 2.51% CAGR from 2026.

Which Service Line Is Expected to Grow Fastest Over the Next Five Years?

IoT and M2M connections, expanding at a 2.89% CAGR on rising industrial adoption.

What Share of Subscribers Does Claro Hold in the Nascent 5G Segment?

About 68.7% of Colombia's early 5G user base as of January 2026.

How Will Millicom's Acquisition of Movistar Affect Competitive Dynamics?

The combined Tigo-Movistar entity will control 35-40% of lines, creating a scaled rival that challenges Claros leadership while maintaining four-operator infrastructure competition.

What Is the Biggest Immediate Cost Pressure on Colombian Operators?

Escalating tower leases and energy costs, which together absorb close to one-third of operating expenditure.

Why Is the Rural Usage Gap Still Wide Despite Near-Universal Coverage?

Affordability constraints and low digital literacy mean only 65-70% of rural residents actively use mobile internet, even though 4G signals reach 96% of the population.

Page last updated on: