Market Overview

| Study Period | 2021 - 2031 |

|---|---|

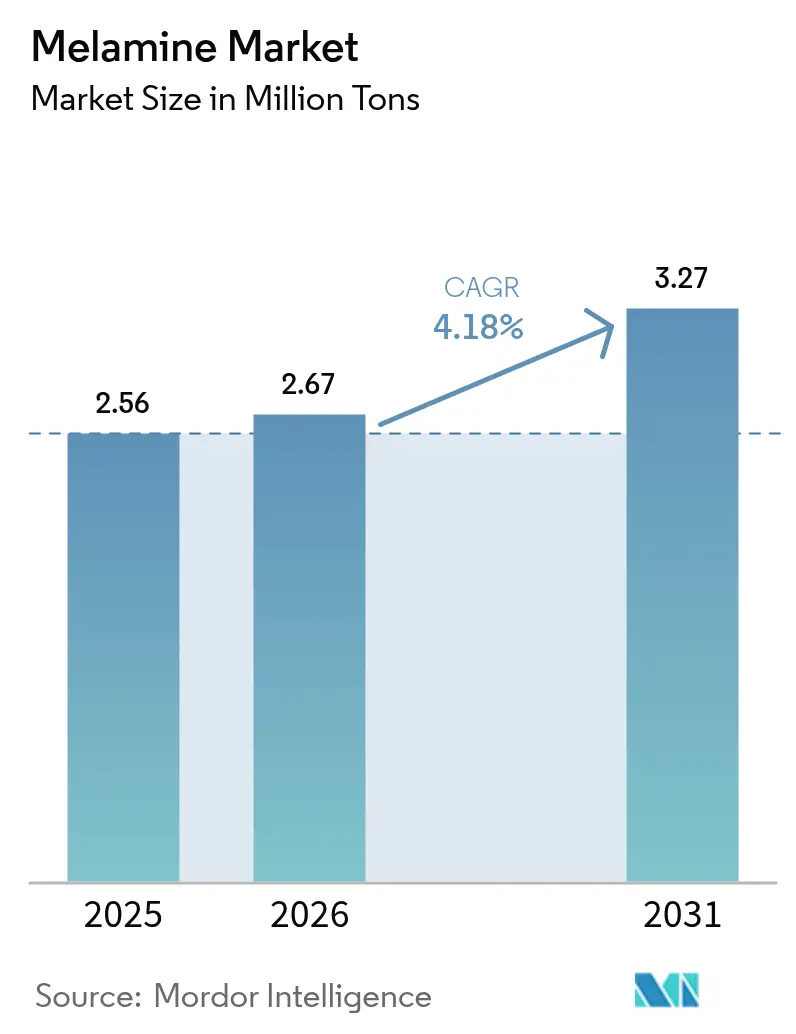

| Market Volume (2026) | 2.67 Million tons |

| Market Volume (2031) | 3.27 Million tons |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

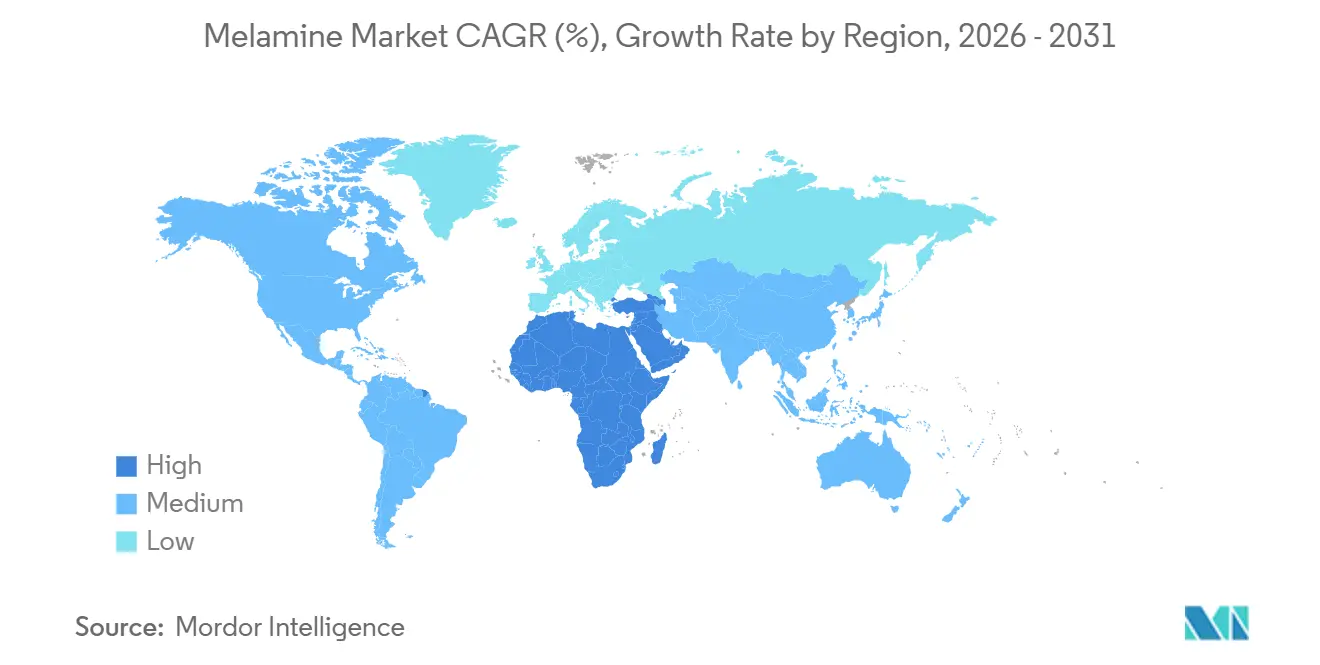

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Melamine Market Analysis by Mordor Intelligence

The Melamine Market size is expected to grow from 2.56 Million tons in 2025 to 2.67 Million tons in 2026 and is forecast to reach 3.27 Million tons by 2031 at 4.18% CAGR over 2026-2031.

Construction recovery in the United States and the European Union is lifting demand for melamine-rich wood adhesives that meet tightening indoor-air-quality rules[1]United States Environmental Protection Agency, “TSCA Title VI Formaldehyde Standards,” epa.gov. In Asia-Pacific, integrated urea–melamine complexes in China and India are scaling output for high-pressure laminates and molding compounds[2]China Petroleum and Chemical Industry Federation, “Annual Chemical Statistics 2025,” cpcif.org.cn. Middle East and Africa producers are capitalizing on low-cost gas feedstock, adding capacity that positions the region for the fastest geographic growth through 2031. Specialty uses such as ASTM E84 Class A melamine foam in aerospace and rail cabins are creating a high-margin sub-segment that supplements core laminate demand.

Key Report Takeaways

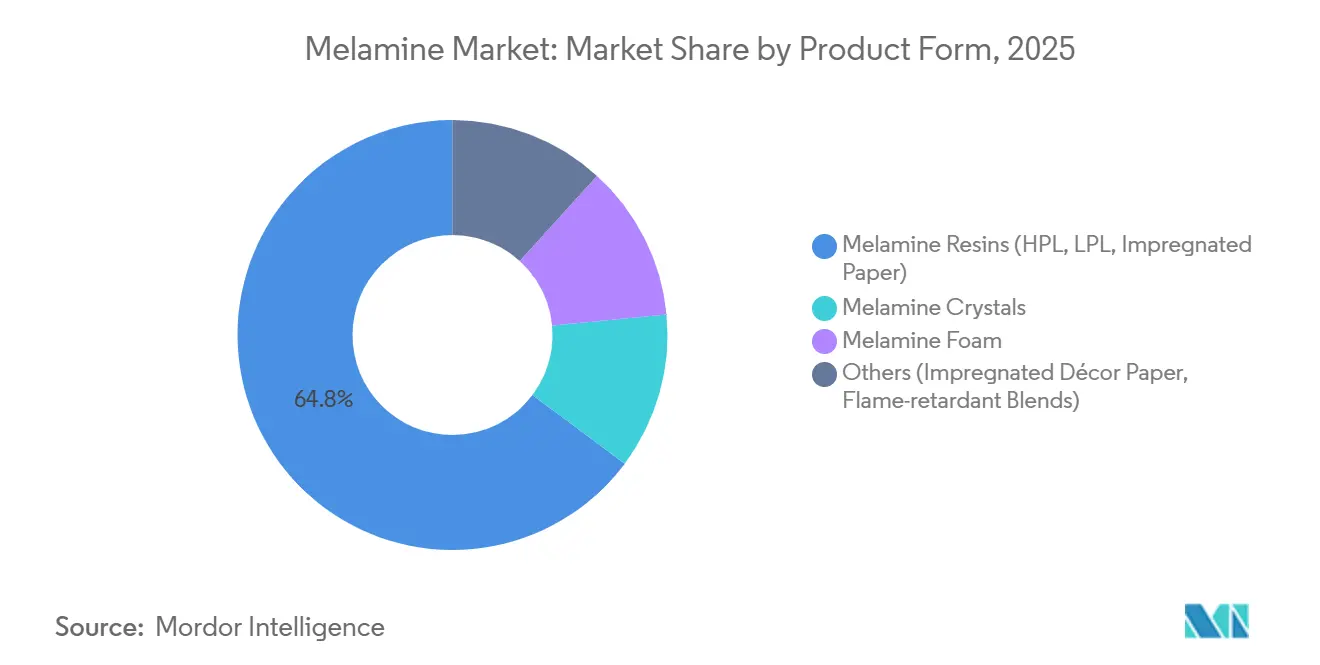

- By product form, melamine resins accounted for 64.78% of the melamine market share in 2025, while melamine foam is poised to advance at a 4.78% CAGR to 2031.

- By application, laminates dominated with 48.15% share of the melamine market size in 2025, and flame-retardants and textile resins are set to grow at a 4.55% CAGR through 2031.

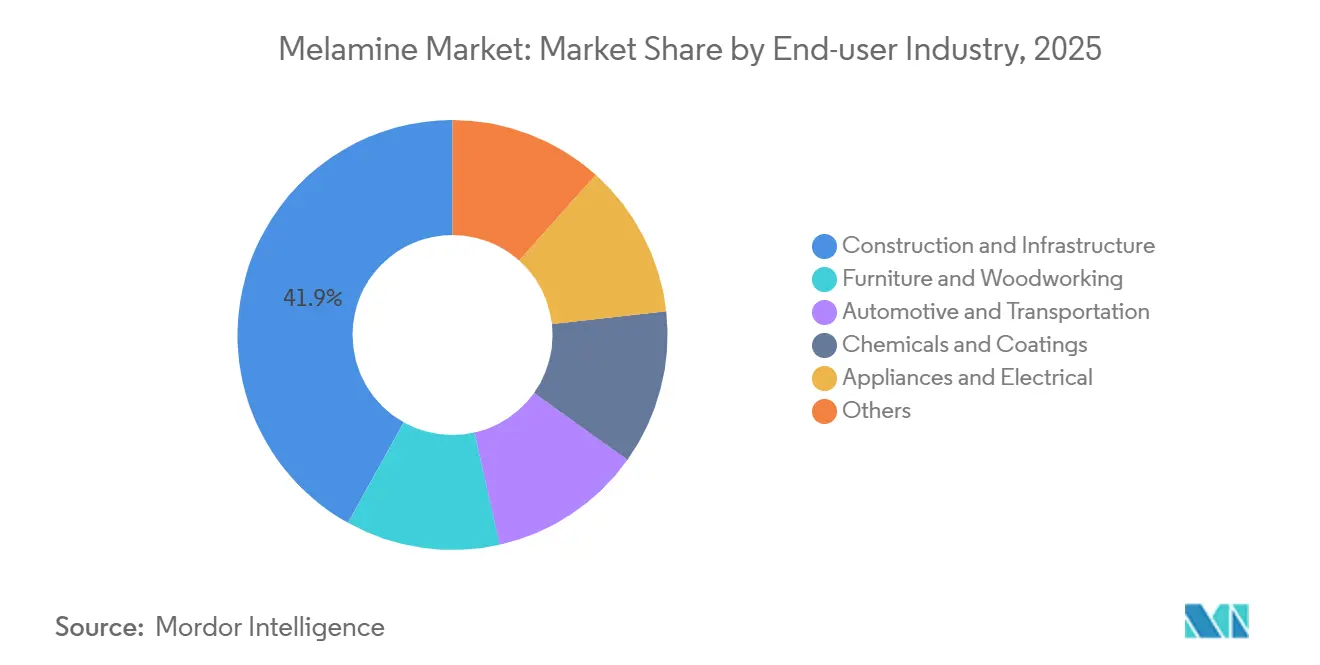

- By end-user, construction and infrastructure captured 41.92% of the 2025 volume, whereas automotive and transportation represent the fastest-growing user group at a 4.42% CAGR to 2031.

- By geography, Asia-Pacific retained 51.16% of global volume in 2025, and the Middle East and Africa region is projected to record the highest regional CAGR at 4.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Melamine Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in laminated flooring and furniture demand in emerging economies | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Construction rebound in US/EU boosting wood-adhesive consumption | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Industrial expansion in Asia-Pacific spurring HPL and molding compounds uptake | +1.0% | Asia-Pacific, particularly China and India | Medium term (2-4 years) |

| Lightweight, heat-resistant melamine foams for aero and rail acoustics | +0.5% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Adoption of low-carbon urea-to-melamine processes (green ammonia routes) | +0.4% | Europe and Middle East, with pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Laminated Flooring and Furniture Demand in Emerging Economies

Rapid urbanization and rising disposable incomes in Asia-Pacific are steering consumers toward engineered wood products that rely on melamine laminates for scratch resistance and aesthetic variety. India’s furniture sector, estimated at USD 18 billion in 2024, is spreading modular kitchens and flat-pack furniture across second-tier cities, boosting laminate consumption per dwelling. China’s wood-based panel output surpassed 300 million m³ in 2024, and thermally fused laminate lines that consume melamine-impregnated décor paper now anchor export-oriented capacity. E-commerce platforms shorten delivery cycles, favoring suppliers with on-site resin impregnation that lowers lead time. Stricter indoor-air-quality rules are prompting higher melamine-to-urea ratios in adhesives, which multiply volume demand even when overall panel output grows modestly. Consequently, incremental furniture and flooring growth translates into outsized melamine uptake in the melamine market.

Construction Rebound in US / EU Boosting Wood-Adhesive Consumption

U.S. housing starts climbed to 1.43 million units in 2024, reversing a prior lull and reviving oriented strand board and particleboard demand. The European Union’s Renovation Wave targets 35 million building upgrades by 2030, fueling timber-frame and interior-fit-out projects that specify melamine-bonded panels. EPA TSCA Title VI caps formaldehyde emissions well below what urea-formaldehyde resins can meet, so panel mills are shifting to MUF adhesives with 15%–25% melamine content. Although melamine raises adhesive cost by up to USD 80 per ton, green-building certifications generate price premiums that offset the expense. North American mills are also sourcing melamine domestically to curb tariff and logistics exposure, strengthening local supply resilience for the melamine market.

Industrial Expansion in Asia-Pacific Spurring HPL and Molding Compounds Uptake

Integrated complexes in China and India convert ammonia, urea, and melamine on one site, achieving cost positions 10%–15% below European averages. Gujarat State Fertilizers & Chemicals ramped capacity in 2024 to meet Indian HPL producers that serve commercial interiors and metro projects. Southeast Asian infrastructure—mass-rapid-transit systems across Jakarta, Bangkok, and Manila—specifies ISO 4586-compliant laminates, raising regional draw for melamine resins. Molding compounds made from melamine and cellulose are gaining ground in appliance and electric-vehicle parts that require arc resistance, positioning the melamine market for downstream value capture. Electric-mobility programs further enlarge the addressable pool by demanding flame-retardant components compliant with UL 94 V-0.

Lightweight, Heat-Resistant Melamine Foams for Aero and Rail Acoustics

Melamine foam offers densities near 10 kg/m³ and achieves ASTM E84 Class A ratings, meeting FAA cabin safety norms while trimming aircraft weight. Airbus and Boeing cabin suppliers specify the material for overhead bins and sidewalls, where every kilogram saved lowers fuel burn. Rail operators in Europe and Asia deploy melamine foam in HVAC ducts and under-floor panels to satisfy EN 45545-2 fire-behavior codes. The foam’s noise-reduction coefficient approaches 1.0, which is prized in electric vehicles where motor silence makes road noise more obvious. Chinese producers are narrowing cost gaps, broadening availability for commercial construction acoustics. These dynamics establish melamine foam as a specialty growth engine inside the wider melamine market.

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter formaldehyde-emission norms in EU and North America | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Bio-based adhesive substitutes (soy, lignin, liquefied wood) | -0.3% | North America and Europe, niche adoption in Asia-Pacific | Medium term (2-4 years) |

| Urea price volatility linked to fertilizer-market disruptions | -0.5% | Global, with acute impact in Europe and South Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Formaldehyde-Emission Norms in EU and North America

EPA TSCA Title VI and CARB Phase 2 mandate emissions below 0.09 ppm for particleboard, thresholds unattainable with plain urea-formaldehyde systems. Panel mills must add melamine or switch to polyurethane, increasing adhesive cost and squeezing margins for smaller operators. Europe’s REACH program lists melamine as an SVHC, triggering authorization hurdles that lengthen product-approval cycles. Some West Coast U.S. mills have already migrated to no-added-formaldehyde adhesives for premium product lines. Short-run demand may dip as manufacturers recalibrate formulations, though higher melamine loading per batch keeps absolute tonnage relatively stable in the melamine market.

Bio-Based Adhesive Substitutes

Soy-protein, lignin, and liquefied-wood resins are gaining LEED credits for interior panels in green buildings. Moisture resistance and pot life lag behind melamine-formaldehyde, confining use to niche plywood and furniture. Lignin supply is tied to paper-mill economics, and soy isolate output is under 1 million tons per year, capping growth potential. Premium pricing of 5%–10% persuades only sustainability-driven buyers, so displacement of melamine remains gradual. Nonetheless, continued research and development signal a moderate long-term challenge to the melamine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Resins Remain the Workhorse while Foam Accelerates

Melamine resins for high-pressure laminates and impregnated paper captured 64.78% of 2025 volume, reflecting deep integration with laminate flooring and furniture production lines across China, India, and the EU. This share anchors the melamine market size for commodity grades, and capacity additions in Asia-Pacific ensure stable supply even as formaldehyde regulations tighten.

Demand for melamine foam is growing at a 4.78% CAGR to 2031, outpacing total market growth as aerospace, rail, and electric-vehicle makers prioritize weight reduction and flame safety. Although foam accounts for a small slice of melamine market share today, its high unit value and expanding acoustic uses position it as the specialty bright spot of the decade.

By Application: Laminates Lead yet Flame-Retardants Gain Speed

Laminates commanded 48.15% of tonnage in 2025, supported by rising modular furniture adoption and renovation activity worldwide. The segment will keep anchoring absolute demand, since each square meter of HPL consumes 150–200 g of resin.

Flame-retardants and textile resins are advancing at a 4.55% CAGR, aided by bans on halogenated chemistries and stricter fire codes in public transport. Their climb broadens the application base of the melamine market beyond construction into protective apparel and electronics.

By End-User Industry: Construction Dominates yet Automotive Gains Momentum

Construction and infrastructure absorbed 41.92% of 2025 demand, with housing starts and renovation mandates underpinning panel and laminate purchases. Strong refurbishment programs in Europe reinforce this bedrock for the melamine industry.

Automotive and transportation volumes are expanding at a 4.42% CAGR as electric-vehicle platforms integrate melamine foam for cabin acoustics and melamine molding compounds for high-voltage connectors. Over the forecast window, mobility applications will add incremental tonnage and value, reinforcing diversification inside the melamine market.

Geography Analysis

Asia-Pacific accounted for 51.16% of global volume in 2025, owing to integrated urea–melamine complexes and proximity to furniture export clusters. China alone operates over 1.5 million tons of capacity, while India’s GSFC is scaling plants that feed growing HPL lines across Gujarat and Maharashtra. Japan and South Korea supply premium electronic-grade resins, adding value-focused diversity.

Middle East and Africa posted the fastest regional growth at 4.35% CAGR, powered by Qatar Melamine Company’s 60,000 ton plant and Borouge’s 80,000 ton expansion that leverages low-cost gas feedstock. GCC construction booms and Vision 2030 industrialization plans amplify downstream demand for laminates and panels.

North America and Europe together accounted for a significant market share in 2025. U.S. producers such as Cornerstone Chemical benefit from shale-gas economics and reshoring of panel supply chains. Europe is restructuring under high energy prices; Grupa Azoty idled Polish output, while CBAM favors imports from low-carbon exporters. South America remains a net importer but is adding volume as Brazilian housing starts recover.

Competitive Landscape

The melamine market is moderately consolidated, with the top five players holding a significant market share. Leading players in the market, including BASF, OCI, Qatar Melamine, EuroChem, and AGROFERT, control roughly half of the global installed capacity. Vertical integration secures ammonia and urea feedstock, buffering margin exposure to gas price swings that drove European spot urea beyond USD 400 tons in 2024.

Process innovation shapes cost curves. OCI and EuroChem patents describe a single-vessel urea-to-melamine conversion that cuts energy by nearly one-fifth and lowers capital intensity. BASF completed a debottlenecking that lifted German capacity by 10,000 tons while trimming gas use 12%, illustrating continual process tweaks.

Specialty niches offer price premiums. BASF’s Basotect foam leads aerospace and rail acoustics, commanding multiples over commodity resin pricing. Chinese entrants such as Junhua Acoustic Materials are targeting cost-driven mid-tier sectors. Bio-based adhesive suppliers remain peripheral, limited by performance gaps and feedstock constraints. Regulatory shifts, especially REACH SVHC listing, add compliance complexity yet also raise entry barriers that incumbent leaders can manage.

Melamine Industry Leaders

BASF SE

OCI NV

Borealis AG

Grupa Azoty

Qatar Melamine Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF increased Ludwigshafen melamine capacity by 10,000 tons, installing waste-heat recovery that cuts gas consumption 12%.

- January 2025: OCI filed a patent for an integrated urea–melamine reactor expected to save 18% energy, with pilot deployment slated for 2026 in the Netherlands.

Global Melamine Market Report Scope

Melamine, a nitrogen-rich organic compound with the chemical formula C3H6N6, serves a wide range of industrial and construction purposes. It is a key material in the production of glues, laminates, molding compounds, paints, and flame retardants. The commercial manufacturing of melamine primarily utilizes two raw materials: urea and dicyandiamide.

The melamine market is segmented by product form, application, end-user industry, and geography. By product form, the market is segmented into melamine crystals, melamine resins (HPL, LPL, impregnated paper), melamine foam, and others (impregnated décor paper, flame-retardant blends). By application, the market is segmented into laminates, wood adhesives, molding compounds, paints and coatings, and flame retardants and textile resins. By end-user industry, the market is segmented into construction and infrastructure, furniture and woodworking, automotive and transportation, chemicals and coatings, appliances and electrical, and others. The report also covers the market size and forecast for the melamine market in 16 countries across major regions. For each segment, the market sizing and forecast have been done based on volume (tons).

By Product Form

| Melamine Crystals |

| Melamine Resins (HPL, LPL, Impregnated Paper) |

| Melamine Foam |

| Others (Impregnated Décor Paper, Flame-retardant Blends) |

By Application

| Laminates |

| Wood Adhesives |

| Molding Compounds |

| Paints and Coatings |

| Flame-retardants and Textile Resins |

By End-user Industry

| Construction and Infrastructure |

| Furniture and Woodworking |

| Automotive and Transportation |

| Chemicals and Coatings |

| Appliances and Electrical |

| Others |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Form | Melamine Crystals | |

| Melamine Resins (HPL, LPL, Impregnated Paper) | ||

| Melamine Foam | ||

| Others (Impregnated Décor Paper, Flame-retardant Blends) | ||

| By Application | Laminates | |

| Wood Adhesives | ||

| Molding Compounds | ||

| Paints and Coatings | ||

| Flame-retardants and Textile Resins | ||

| By End-user Industry | Construction and Infrastructure | |

| Furniture and Woodworking | ||

| Automotive and Transportation | ||

| Chemicals and Coatings | ||

| Appliances and Electrical | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the melamine market?

The melamine market is estimated at 2.67 million tons in 2026 and is on track to hit 3.27 million tons by 2031.

How fast is global melamine demand growing?

Demand is forecast to rise at a 4.18% CAGR from 2026 to 2031, supported by construction, furniture, and specialty foam applications.

Which product form dominates sales?

Melamine resins for laminates lead with 64.78% of 2025 volume, far ahead of other forms such as crystals and foam.

Which region offers the highest growth prospects?

The Middle East and Africa region is projected to log the fastest regional CAGR at 4.35% through 2031 due to low-cost gas-based capacity additions.

What is driving specialty melamine foam demand?

Aerospace, rail, and electric-vehicle manufacturers are adopting lightweight Class A fire-rated melamine foam to cut weight and meet stricter acoustic and safety standards.

How are formaldehyde regulations affecting melamine consumption?

Stricter emission caps in North America and Europe are forcing panel mills to switch to higher-melamine MUF adhesives, raising resin intensity per panel and sustaining overall melamine tonnage.

Page last updated on: