Ureteroscopes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ureteroscopes Market Analysis by Mordor Intelligence

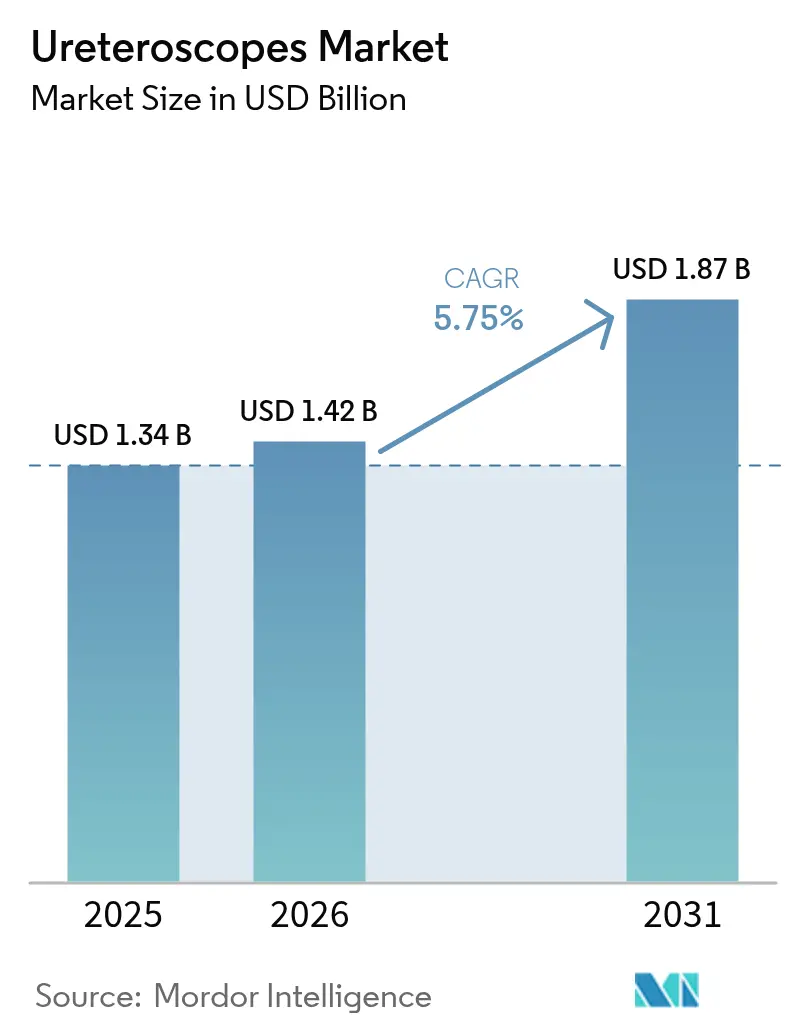

The ureteroscope market size was valued at USD 1.34 billion in 2025 and estimated to grow from USD 1.42 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031). The current upswing is tied to sustained growth in kidney-stone incidence, a rapid shift toward same-day minimally invasive procedures, and a succession of digital flexible platform launches that sharpen visualization while trimming procedure time. Hospitals still anchor procedure volume; however, ambulatory surgical centers (ASCs) are scaling faster as Medicare’s 2.9% outpatient rate hike and the continued pass-through code C1747 lift reimbursement for single-use devices[1]Federal Register, “Medicare and Medicaid Programs: Hospital Outpatient Prospective Payment and Ambulatory Surgical Centers Payment Systems for CY 2025,” federalregister.gov. Flexible digital scopes dominate purchasing because wider 270° deflection angles and pixel-dense CMOS sensors elevate stone-free rates, while single-use variants win share in settings that prioritize infection control and zero downtime. Competitive intensity has sharpened as incumbents defend reusable portfolios and, in parallel, debut disposable lines that erase historic gaps in optics and durability, shortening replacement cycles across the ureteroscope market.

Key Report Takeaways

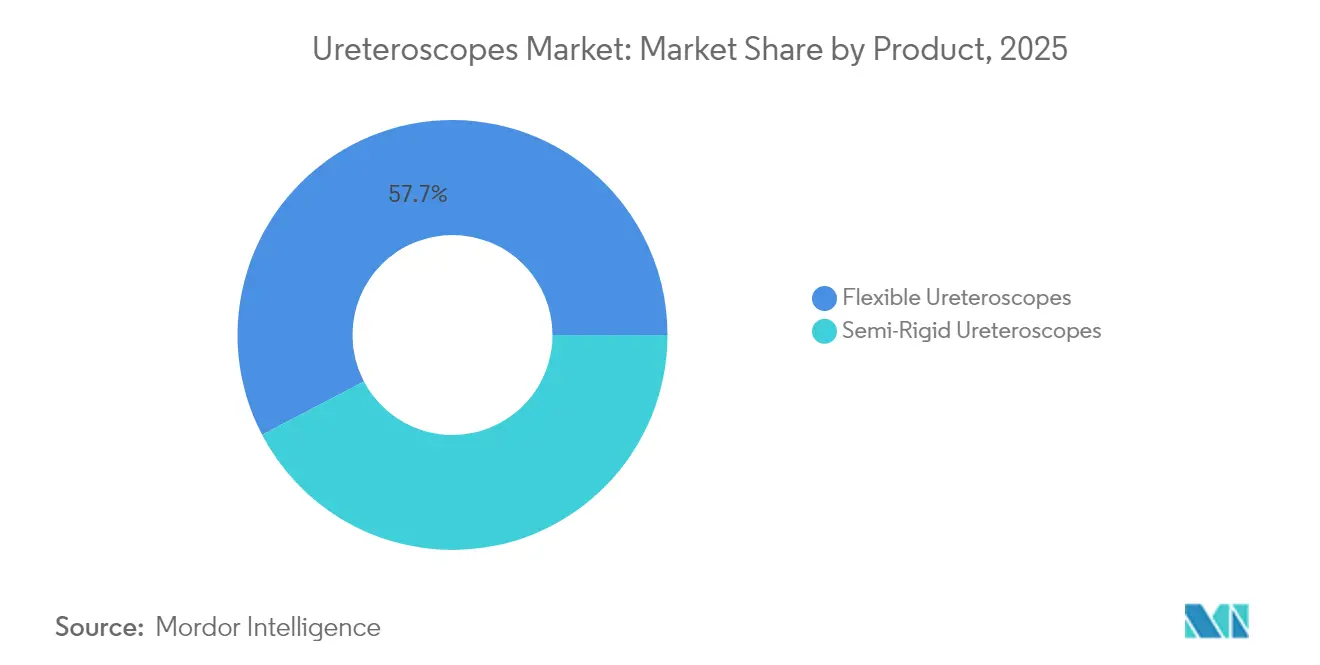

- By product category, flexible ureteroscopes led with 57.68% of ureteroscope market share in 2025, whereas semi-rigid systems are projected to expand at a 8.89% CAGR to 2031.

- By usability, reusable devices captured 70.85% share of the ureteroscope market size in 2025, while single-use scopes hold the highest projected CAGR at 9.78% through 2031.

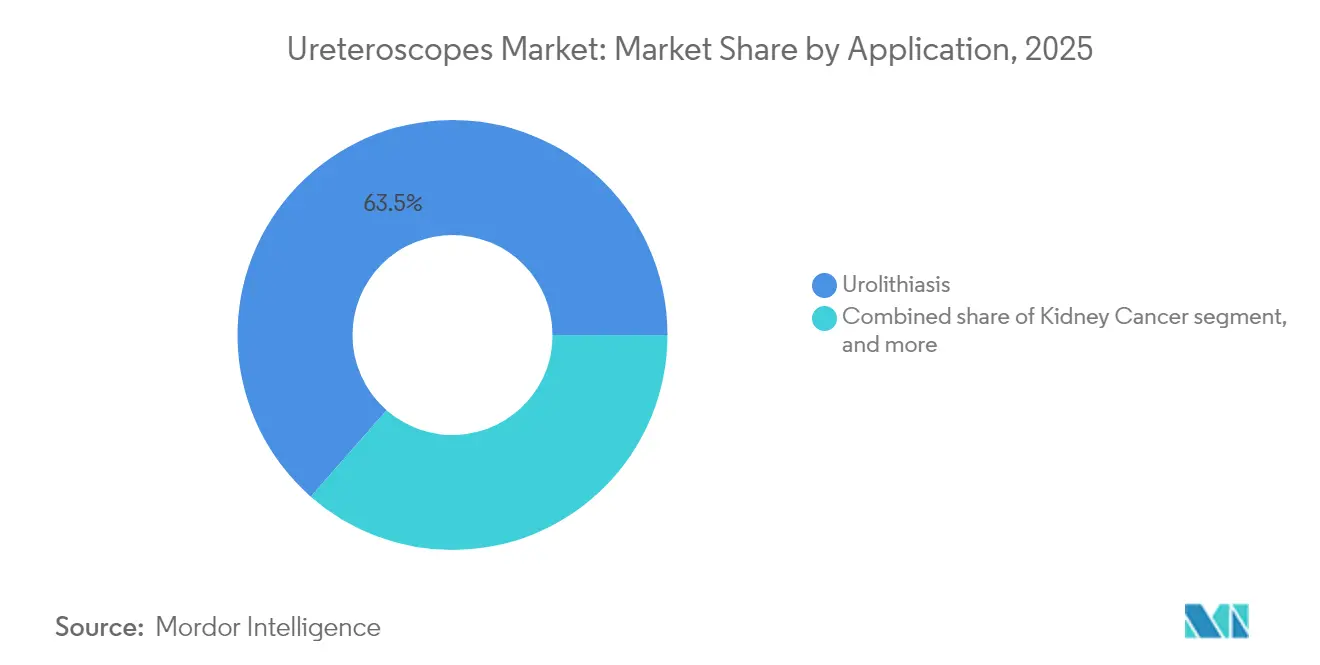

- By application, urolithiasis dominated at 63.54% share of the ureteroscope market size in 2025; urinary-stricture treatment is advancing at a 7.54% CAGR to 2031.

- By end user, hospitals controlled 60.52% revenue share in 2025, but ASCs record the fastest growth at an 8.12% CAGR through 2031.

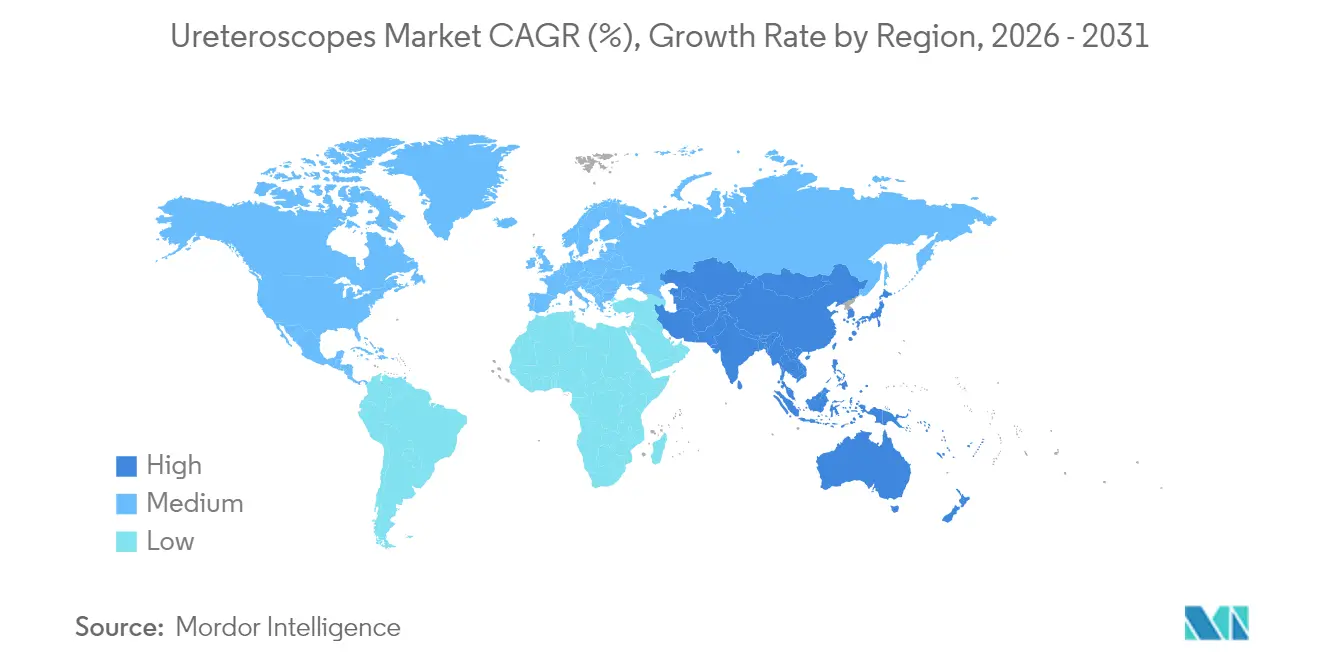

- By geography, North America commanded 37.75% of ureteroscope market share in 2025; Asia-Pacific is forecast to grow at a 6.85% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ureteroscopes Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global burden of urolithiasis & related disorders | +1.8% | Eastern Europe, Central Asia, global | Long term (≥ 4 years) |

| Shift toward minimally invasive stone-management procedures | +1.4% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Advancements in digital flexible & single-use ureteroscope technology | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Increasing healthcare spending & reimbursement support for endourology | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Growth of ambulatory surgical centers performing ureteroscopy | +1.1% | North America, Europe, emerging Asia | Medium term (2-4 years) |

| Integration of high-power laser lithotripsy & imaging enhancements | +1.0% | Global high-income markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Urolithiasis & Related Urological Disorders

Kidney-stone incidence hit 106 million cases in 2021 and continues to climb, providing a constant pipeline of candidates for endoscopic stone removal. The gender gap narrows each year; U.S. prevalence among women rose from 6.5% in 2007-2008 to 9.1% in 2017-2020, prompting vendors to refine ergonomics that suit broader anatomies. Regional dynamics vary: Eastern Europe and Central Asia register rising case loads, whereas several East-Asian nations report modest declines, steering sales targets accordingly. Pediatric stone disease, exceeding 3 million annual cases, fuels demand for ultra-miniature shafts that limit ureteral trauma, underpinning long-term growth in the ureteroscope market.

Shift Toward Minimally Invasive Stone-Management Procedures

European Association of Urology guidelines now recommend ureteroscopy ahead of shock-wave therapy for stones under 20 mm, citing stone-free rates between 81%-94%[2]European Association of Urology, “EAU Guidelines on Urolithiasis,” uroweb.org. Same-day discharge cuts facility costs and boosts ASC throughput, while machine-learning algorithms streamline case selection, reducing intra-operative surprises. Combined, these factors enlarge procedural volume, reinforcing expansion of the ureteroscope market.

Advancements in Digital Flexible & Single-Use Ureteroscope Technology

Olympus earned FDA clearance in May 2025 for its EVIS X1 imaging system and associated flexible ureteroscopes that embed Extended Depth-of-Field (EDOF™) optics, enhancing lesion visibility by 22% versus prior generation scopes. Boston Scientific’s LithoVue Elite adds real-time intrarenal-pressure monitoring and received an FDA nod in 2024, streamlining decision-making during lithotripsy. Cook Medical joined the fray in March 2025 with the single-use Ascend scope, further widening disposable choices. These technology leaps maintain surgeon confidence and shorten upgrade cycles across the ureteroscope market.

Increasing Healthcare Spending & Reimbursement Support for Endourology

CMS upheld a 2.9% outpatient payment increase and retained pass-through code C1747 for single-use ureteroscopes in 2025, adding USD 1,150 in extra reimbursement per case and improving provider economics. Similar tariff uplifts in Germany and the United Kingdom bolster hospital budgets, sustaining steady unit demand in the ureteroscope market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & maintenance cost of digital ureteroscopes | –0.9% | Developing regions, global | Medium term (2-4 years) |

| Limited availability of trained endourologists in developing regions | –0.7% | Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Stringent device sterilization & regulatory compliance requirements | –0.5% | Europe, North America | Medium term (2-4 years) |

| Environmental & waste-management concerns over disposable scopes | –0.3% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Maintenance Cost of Digital Ureteroscopes

A modern digital flexible scope often exceeds USD 20,000 and carries USD 6,000-8,000 in annual service, deterring cash-strapped hospitals. Although disposables bypass repair bills, their per-procedure expense can outstrip local tariffs in emerging economies, slowing uptake and tempering ureteroscope market expansion.

Environmental & Waste-Management Concerns over Disposable Scopes

Life-cycle analyses find single-use devices emit more greenhouse gases than reusable counterparts, prompting European tenders to weigh carbon scores alongside price. Hospitals lacking advanced waste streams incur added disposal fees, posing a mild drag on the ureteroscope market’s migration to disposables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Digital Flexibility Drives Procedural Evolution

Flexible designs held 57.68% of the ureteroscope market in 2025, buoyed by pixel-dense sensors that boost calyceal visualization and ultra-slim 7.5 Fr shafts that ease access without prior dilation. A multicenter study published in May 2025 comparing a 6.3 Fr and 7.5 Fr disposable scope logged stone-free rates of 95% and 92.9%, respectively, and shaved operative time by 4.5 minutes with the smaller device. Semi-rigid systems, prized for durability, grow at 8.89% CAGR because budget-sensitive hospitals regard them as a low-risk entry point, subtly lifting overall ureteroscope market size.

Manufacturers now differentiate through software rather than optics alone. Boston Scientific’s pressure-monitoring layer and Olympus’s EDOF imaging illustrate value-add pathways that influence tender outcomes. Meta-audits show a generational decline in shaft diameter correlating with fewer ureteral dilations and shorter hospital stays, fostering healthy replacement timelines across the ureteroscope market.

By Usability: Single-Use Revolution Challenges Reprocessing Paradigm

Reusable scopes retain 70.85% share because high-volume centers amortize capital quickly and value established reprocessing protocols. Yet single-use devices expand at a 9.78% CAGR, propelled by data linking disposables to lower post-operative infection rates and zero repair downtime. Portable form factors allow ASCs lacking autoclaves to perform advanced lithotripsy, widening ureteroscope market size in decentralized corridors.

Cost divides opinion: 59.11% of urologists cite price as the prime barrier, but total-cost-of-ownership studies show parity once repair, sterilization labor, and scope loss are tallied. Optical parity debates have subsided; LithoVue Elite’s 270° deflection and full-HD sensor now match many reusable benchmarks, smoothing adoption curves.

By Application: Urolithiasis Dominates While Strictures Gain Momentum

Urolithiasis captured 63.54% of ureteroscope market size in 2025, supported by guideline preference and rising metabolic risk factors. Thulium-fiber lasers, robot-assisted navigation, and AI-guided fragment detection further lift stone-free rates, keeping procedure volumes robust. Diagnostic scopes for hematuria and upper-tract carcinoma leverage identical optics, broadening clinical touchpoints.

Urinary strictures register the fastest growth at a 7.54% CAGR. Accessory kits now enable precise incision and balloon dilation, reducing recurrence. Hotspots include South Asia and parts of Latin America, where infectious etiologies make strictures prevalent, injecting fresh volume into the ureteroscope market.

By End User: Ambulatory Settings Challenge Hospital Dominance

Hospitals held 60.52% revenue in 2025 owing to critical-care capacity and access to high-powered lasers. Recent reimbursement boosts safeguard margins, and hybrid fleets—premium reusable units backed by single-use standbys—mitigate downtime.

ASCs, however, post an 8.12% CAGR as payers redirect elective stone cases to outpatient venues. Cook Medical’s 40-second setup Ascend scope and Ambu’s aScope 5 streamline turnover, widening procedural capacity and redistributing ureteroscope market share toward community facilities.

Geography Analysis

North America retained a 37.75% share of the ureteroscope market in 2025, fueled by 9.25% kidney-stone prevalence among U.S. adults and broad coverage for digital scopes. The 2025 outpatient payment bump bolsters ROI, encouraging both academic hospitals and ASCs to refresh fleets. Realtime pressure-monitoring models such as LithoVue Elite help manage complex cases, cementing premium-product demand.

Europe ranks second. Single-use uptake is brisk in the United Kingdom and Germany; conversely, Scandinavian buyers weigh environmental metrics, tempering disposable growth. Southern and Eastern Europe unlock latent demand via modernization funds, broadening ureteroscope market presence across the continent.

Asia-Pacific is the fastest-growing region at a 6.85% CAGR through 2031. China’s centralized value-based procurement compresses pricing yet drives bulk orders; Japan and South Korea adopt ultra-slim digital scopes early, while India’s private-hospital boom fuels volume growth. Divergent price tiers oblige suppliers to tailor portfolios, enlarging ureteroscope market size across both premium and cost-sensitive segments.

Competitive Landscape

The ureteroscope market exhibits moderate concentration: Olympus, Boston Scientific, and Stryker together hold around 60% of global revenue. Olympus leverages its optical pedigree, releasing a 4 K flexible platform that offers 30% sharper images and a 12% wider deflection span versus prior models. Boston Scientific differentiates with single-use innovation and intrarenal-pressure analytics, while Stryker bundles ergonomic scopes with its accessory ecosystem, strengthening lock-in.

Challengers exploit niches: Ambu transferred single-use expertise from bronchoscopy to urology and reported 10.6% Q4 2024 urology revenue growth after FDA clearance of the aScope 5 Uretero. Cook Medical’s March 2025 Ascend launch intensifies price pressure in disposables, and Chinese players capitalize on local procurement quotas to expand semi-rigid penetration. Software-driven advantages—AI-computed fragment sizing, pressure alerts, and automated irrigation—now steer tenders as much as hardware, driving frequent upgrades in the ureteroscope market.

Sustainability has emerged as a new battleground. Olympus pilots bioplastic housings, Ambu trialed a take-back recycling program, and Boston Scientific conducts cradle-to-grave audits to reassure eco-conscious buyers. Simultaneously, M&A activity targets imaging start-ups and robotics firms that can accelerate software layers, ensuring innovation pipelines stay robust.

Ureteroscopes Industry Leaders

Olympus Corporation

Richard Wolf GmbH

Stryker Corporation

PENTAX Medical (Hoya Corporation)

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CMS retained pass-through payment code C1747 for single-use ureteroscopes, preserving an extra USD 1,150 reimbursement per outpatient case.

- May 2025: Olympus secured FDA 510(k) clearance for its EVIS X1 imaging platform and compatible flexible ureteroscopes featuring EDOF optics.

- March 2025: Cook Medical launched the Ascend Single-Use Flexible Ureteroscope, cutting mean setup time to 40 seconds in validation runs.

- November 2024: Ambu gained FDA clearance for the aScope 5 Uretero and reported 10.6% year-over-year Q4 endoscopy revenue growth.

- April 2024: Olympus introduced a next-generation 4 K digital flexible ureteroscope platform in North America and Europe, claiming 30% sharper imaging and a 12% wider deflection span.

Global Ureteroscopes Market Report Scope

Ureteroscopes are endoscopic devices used in ureteroscopy. These are used to treat and diagnose renal and upper urinary tract diseases.

The ureteroscopes market is segmented by product (flexible ureteroscope and semi-rigid ureteroscope), application (urolithiasis, kidney cancer, urinary stricture, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across significant regions, globally. The report offers the value (in USD million) for the above segments.

| Flexible Ureteroscopes | Digital Flexible Ureteroscopes |

| Fiber-optic Flexible Ureteroscopes | |

| Semi-Rigid Ureteroscopes |

| Single-Use / Disposable Ureteroscopes |

| Reusable Ureteroscopes |

| Urolithiasis |

| Kidney Cancer |

| Urinary Stricture |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Flexible Ureteroscopes | Digital Flexible Ureteroscopes |

| Fiber-optic Flexible Ureteroscopes | ||

| Semi-Rigid Ureteroscopes | ||

| By Usability | Single-Use / Disposable Ureteroscopes | |

| Reusable Ureteroscopes | ||

| By Application | Urolithiasis | |

| Kidney Cancer | ||

| Urinary Stricture | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the ureteroscope market in 2026?

The ureteroscope market is valued at USD 1.42 billion in 2026 and is set to expand to USD 1.87 billion by 2031 at a 5.75% CAGR.

Which product category leads revenue?

Flexible digital ureteroscopes command 57.68% of 2025 revenue due to superior maneuverability and imaging clarity.

Why are single-use ureteroscopes gaining momentum?

ASCs and hospitals adopt single-use designs to curb infection risk, avoid repair downtime, and benefit from continued pass-through reimbursement, supporting a 9.78% CAGR for this segment.

Which region offers the highest growth potential?

Asia-Pacific is forecast to advance at a 6.85% CAGR through 2031, propelled by higher stone prevalence, rising insurance coverage, and hospital investment.

Who are the leading companies in the ureteroscope market?

Olympus, Boston Scientific, and Stryker jointly hold about 60.0% of global revenue, while Ambu and Cook Medical are scaling quickly in disposables.

What drives adoption in ambulatory surgical centers?

Favorable reimbursement, same-day discharge protocols, and fast-setup single-use scopes enable ASCs to deliver ureteroscopy at lower overall cost than inpatient facilities.

Page last updated on: