United States Lawn Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 60.0 Billion |

| Market Size (2026) | USD 62.91 Billion |

| Market Size (2031) | USD 79.68 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

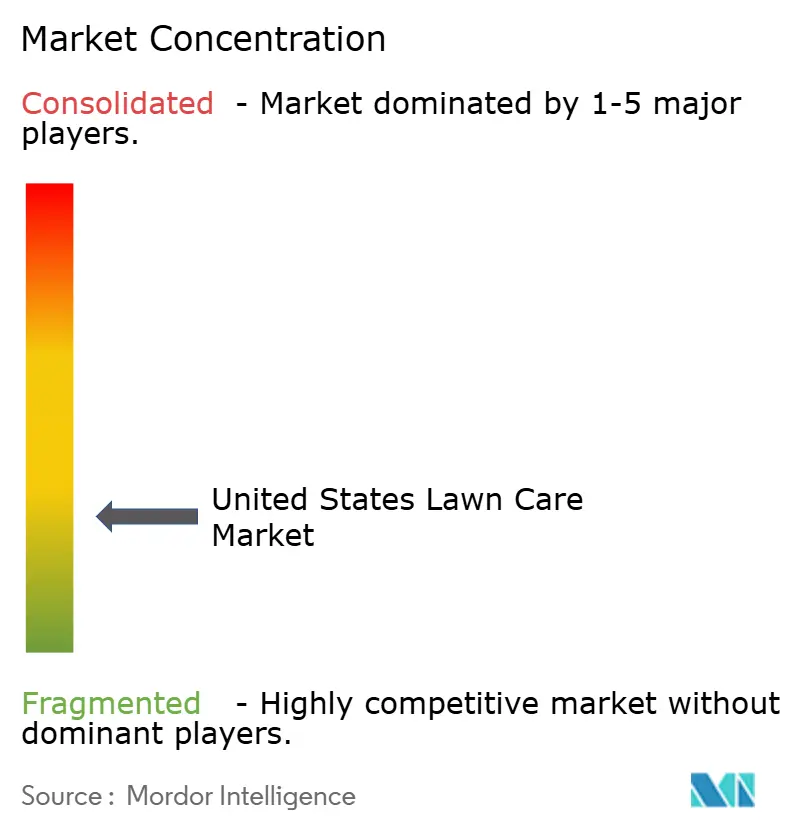

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Lawn Care Market Analysis by Mordor Intelligence

The United States lawn care market size was valued at USD 60.0 billion in 2025 and estimated to grow from USD 62.91 billion in 2026 to reach USD 79.68 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). Population growth in Sun Belt states, increasing adoption of professional services over do-it-yourself approaches, and adoption of smart and autonomous equipment drive spending on lawn maintenance, design, and related services. Commercial and industrial clients generate over 50% of market revenue as companies outsource grounds maintenance operations. Service providers improve profit margins through route optimization technology, digital booking systems, and efficient irrigation solutions, despite rising fuel and labor costs. The market remains highly fragmented, presenting opportunities for consolidation, while specialized service providers maintain competitive advantages through expertise and environmental certifications.

Key Report Takeaways

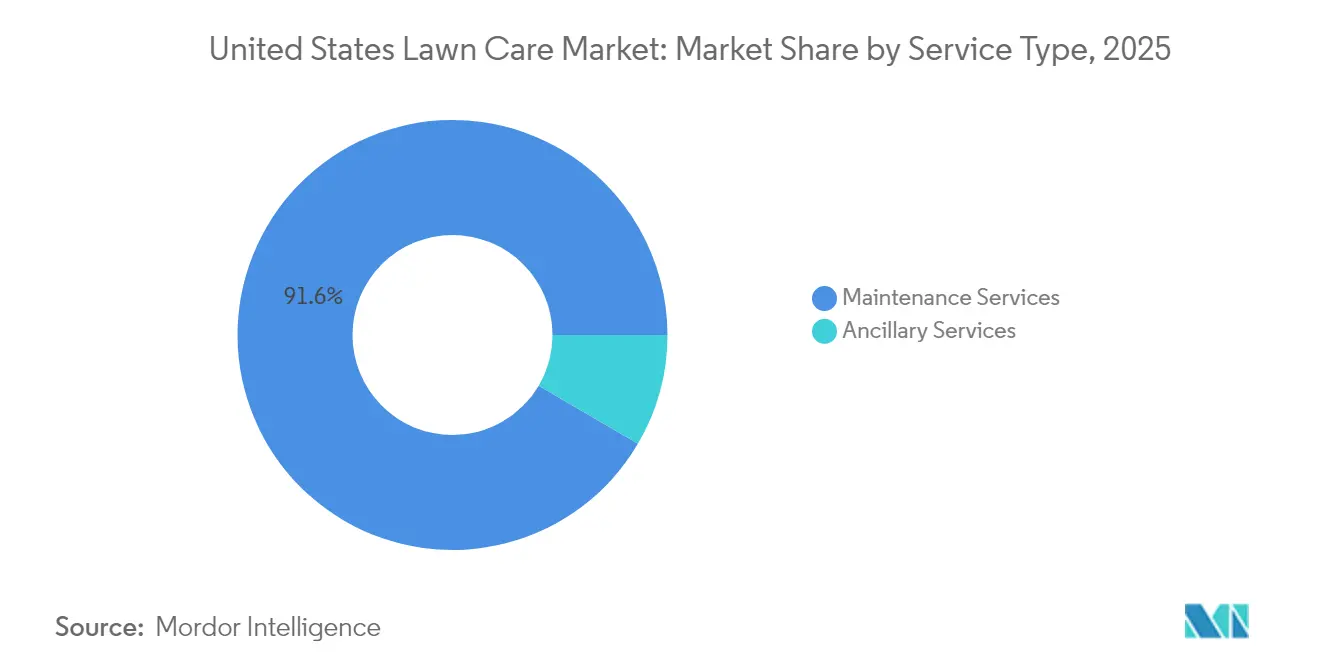

- By service type, maintenance captured 91.55% of the United States lawn care market share in 2025, and is projected to expand at a 5.18% CAGR to 2031, outpacing all other service categories.

- By application, commercial and industrial sites led with 53.72% revenue share in 2025; golf courses and sports facilities are forecast to grow at a 10.05% CAGR through 2031.

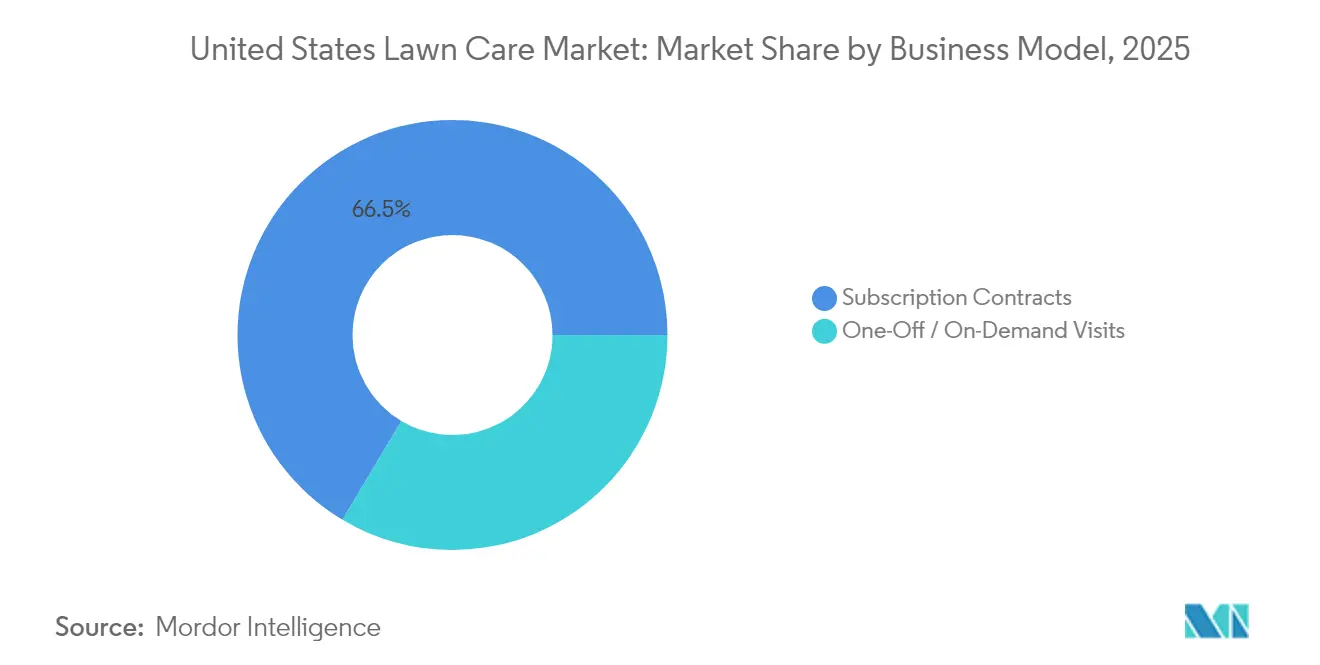

- By business model, subscription contracts held 66.45% of the United States lawn care market size in 2025, while one-off and on-demand visits are projected to record the highest CAGR at 10.22% from 2025 to 2031.

- By distribution channel, direct in-house teams accounted for a 58.63% share of the market size in 2025, whereas online marketplaces are advancing at an 10.94% CAGR.

- BrightView Holdings, Inc., The Davey Tree Expert Company, TruGreen Limited Partnership, Ruppert Landscape, Inc., and Gothic Landscaping, Inc. are major players in the landscaping services market, operating in a highly fragmented and competitive environment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Lawn Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing migration to Sun Belt states increasing lawn footprints | +0.8% | Southeast and Southwest | Medium term (2-4 years) |

| Growth in golf course renovations and new short-course formats | +0.6% | Nationwide, affluent metros | Long term (≥ 4 years) |

| DIY-turned-DIWM (Do-It-With-Me) consumer trend | +0.9% | Nationwide, millennial-dense metros | Short term (≤ 2 years) |

| Rapid adoption of robotic and autonomous mowing equipment | +0.5% | Commercial settings, premium residential | Medium term (2-4 years) |

| Rising millennial home-ownership and outdoor living upgrades | +0.7% | Suburban Sun Belt markets | Short term (≤ 2 years) |

| Landscaping tax incentives in water-stressed municipalities | +0.4% | California and broader Southwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ongoing Migration to Sun Belt States Increasing Lawn Footprints

The southern United States gained 1.8 million new residents in 2024, marking the region's fastest population growth in over two decades[1]Source: Ramsey Archibald, “Southern boom fueled fastest U.S. growth in decades, new Census estimates show,” AL.com, al.com.. This demographic shift generates increased demand for lawn care services through new residential construction, retail developments, and municipal projects. The expansion of commercial facilities, including corporate campuses and logistics centers, further strengthens market growth by requiring comprehensive grounds maintenance in regions with year-round growing seasons. Service providers operating in Texas, Florida, and adjacent growth markets benefit from sustained revenue opportunities linked to population expansion and employment growth. Infrastructure development in Sun Belt metropolitan areas requires landscaping services for government projects, business complexes, and mixed-use properties.

Growth in Golf Course Renovations and New Short-Course Formats

Golf course renovation projects and entertainment venues require specialized turf design, precise mowing specifications, and premium hardscape elements. Golf operators focus on attracting younger players through short courses and entertainment facilities that combine visually appealing landscapes with high-maintenance requirements. The Hermann Park Golf Course plans a USD 30 million renovation in August 2025, led by the Astros Golf Foundation. The project aims to enhance community facilities, expand the driving range to increase revenue, install a stormwater recapture and irrigation system, and construct a new clubhouse. Short courses and entertainment venues incorporate extensive landscaping features, including decorative components, lighting systems, and specialized turf varieties that need regular professional maintenance. This market segment enables landscaping companies to develop technical expertise and secure premium projects that set them apart from standard maintenance service providers.

DIY-Turned-DIWM (Do-It-With-Me) Consumer Trend

The household outsourcing of lawn maintenance increased significantly, driven by homeowners seeking convenience and consistent property aesthetics. Millennials, who represent the largest homebuyer segment, frequently use mobile applications to schedule mowing, fertilization, and design services, strengthening digital revenue streams. Service providers benefit from recurring maintenance contracts that increase customer lifetime value, while peer referrals reduce customer acquisition costs. The market extends beyond basic lawn care to include landscape design, seasonal planting services, and outdoor living space improvements, enabling providers to expand their service offerings and implement premium pricing strategies.

Rapid Adoption of Robotic and Autonomous Mowing Equipment

Research indicates that autonomous mowers improve turf density and cut quality while reducing labor requirements by up to 30%[2]Source: P. Agustin Boeri, “Autonomous Compared with Conventional Mower Use on St. Augustinegrass Lawn Quality,” HortTechnology, journals.ashs.org. Commercial landscaping companies use autonomous mower fleets to address labor shortages and enable continuous operation with reduced noise and emissions. This allows companies to shift workers to specialized tasks such as landscape design, installation, and client management while maintaining competitive maintenance service rates. Companies that implement autonomous mowing technology gain competitive advantages and develop integrated service offerings that combine automation with conventional landscaping services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute seasonal labor shortages despite H-2B visa caps increases | −0.6% | Nationwide, agriculture-heavy regions | Short term (≤ 2 years) |

| Escalating fuel and equipment costs squeezing margins | −0.4% | Nationwide, rural service areas | Medium term (2-4 years) |

| Rising liability insurance premiums for contractors | −0.3% | Nationwide, high-risk services | Long term (≥ 4 years) |

| Fragmented regulatory codes across states inflating compliance cost | −0.2% | Multi-state operators, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Seasonal Labor Shortages Despite H-2B Visa Caps Increases

Despite the approval of 64,716 additional visas for 2025, the demand for seasonal workers exceeds 200,000 positions, resulting in understaffing during peak growth periods[3]Source: U.S. Citizenship and Immigration Services, “DHS, DOL Make Nearly 65,000 Additional H-2B Visas Available for Fiscal Year 2025,” uscis.gov. Small operators with limited administrative resources struggle to navigate visa processes, forcing them to either restrict service expansion or increase wages at the expense of profit margins. Processing delays affect scheduling, increase customer turnover risk, and push larger companies toward automation investments. The labor shortage compels businesses to constrain service growth, raise wages for domestic worker recruitment, and implement labor-saving technologies that require significant capital investment.

Escalating Fuel and Equipment Costs Squeezing Margins

Fluctuating diesel prices and equipment costs strain cash flows, particularly for companies operating in single markets. These cost pressures significantly affect smaller operators who cannot achieve economies of scale in equipment purchases and fuel procurement. Larger companies gain competitive advantages through volume-based discounts and investments in fuel-efficient equipment. California's upcoming zero-emission equipment regulations in 2024 introduce additional financial burdens, requiring companies to adopt higher-priced battery-powered equipment while maintaining service standards[4]California Air Resources Board, Public Hearing to Consider Proposed Amendments to the Small Off-Road Engine Regulations: Transition to Zero Emissions, arb.ca.gov . Large enterprises further strengthen their market position by utilizing scale purchasing and telematics to control fuel consumption, increasing the cost differential with local independent operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Maintenance Dominates Revenue Streams

Maintenance services accounted for 91.55% of the United States lawn care market share in 2025, providing stable recurring revenue through residential and commercial client contracts. Subscription-based service packages combining mowing, fertilization, weed control, aeration, and irrigation maintenance help companies reduce customer acquisition costs while improving route efficiency. The segment's high margins, particularly in fertilization and weed control services, stem from specialized chemical expertise and licensing requirements that create entry barriers. Regular mowing services provide frequent customer contact opportunities, enabling providers to expand revenue through seasonal plantings and hardscape maintenance. The growing adoption of smart irrigation controllers that optimize water usage and detect system issues aligns with environmental sustainability requirements. The maintenance segment is projected to grow at a CAGR of 5.18% during 2026-2031, driven by increased professional service outsourcing, demographic shifts, and technological improvements in service delivery.

Ancillary services demonstrate accelerated growth as residential customers seek enhanced outdoor living features, including fire pit installations, landscape lighting, and pollinator gardens. This service diversification helps providers reduce seasonal revenue fluctuations and offset increased labor costs, supporting the expansion of comprehensive service providers.

By Application: Commercial Leadership with Golf Surge

Commercial and industrial sites contributed 53.72% of the United States lawn care market share in 2025, as organizations outsource grounds maintenance to focus on their primary operations. Multi-property portfolios prefer service providers who offer standardized maintenance levels, sustainable landscaping, and Environmental, Social, and Governance (ESG)- aligned performance reporting. Golf courses and sports facilities, though a smaller market segment, are projected to grow at a 10.05% CAGR through 2031, driven by new entertainment formats and facility renovations targeting younger demographics. These properties require specialized turf management, precise maintenance, and integrated lighting systems, enabling premium pricing and long-term contracts.

The residential segment maintains steady demand, with millennials viewing lawn care services as a fundamental household expense similar to cleaning services. This market diversification helps service providers maintain stability during economic fluctuations. Municipal contracts provide consistent revenue but involve public bidding processes and wage requirements that may reduce profit margins compared to private sector work.

By Business Model: Subscriptions Drive Stability

Subscription contracts accounted for 66.45% of the United States lawn care market share in 2025, providing predictable cash flows that support equipment financing and workforce scheduling. Customers benefit from fixed monthly invoices that facilitate budgeting and access to multiple services through a single provider. The subscription model allows landscaping companies to optimize routes and resource allocation, reducing operational costs and improving service efficiency compared to traditional on-demand services. Regular customer interactions foster trust relationships that facilitate expansion into additional services such as landscape design, hardscaping, and seasonal maintenance. Digital platforms enhance subscription management through automated scheduling, service customization, and customer communication features that improve service delivery and satisfaction.

On-demand services, facilitated by mobile applications, are growing at a 10.22% CAGR as customers schedule specific services such as aeration, leaf clean-up, or holiday lighting without long-term commitments. This flexible model attracts new customers and serves as an entry point for recurring service upsells, despite higher revenue variability. Companies that implement both subscription and on-demand models effectively serve diverse customer segments while balancing seasonal fluctuations.

By Distribution Channel: Direct Teams Maintain Control

In-house crews account for 58.63% of the market revenue in 2025. This operational model enables companies to maintain high service quality, a strong brand reputation, and healthy customer relationships. Centralized training programs ensure consistent safety protocols and horticultural practices, reducing liability risks. The direct in-house approach enables companies to exert control over service delivery, customer interactions, and pricing, thereby helping to build strong market positions and foster customer retention.

Online marketplaces are growing at a 10.94% CAGR, simplifying service discovery for homeowners and small businesses through price transparency and customer reviews. Independent operators utilize these platforms to optimize route efficiency, while larger companies develop proprietary applications to safeguard customer data and capitalize on additional sales opportunities. The distribution channels continue to adapt as customers increasingly demand instant scheduling and digital payment options. Franchise systems facilitate geographic expansion with reduced capital investment while ensuring consistent brand standards and operational procedures across regions. This evolution in distribution channels creates growth opportunities for companies that combine efficient digital customer acquisition with reliable service delivery to gain market share from traditional competitors.

Geography Analysis

The Southeast commands the majority of the United States lawn care market share due to population growth, diverse industries, and climate conditions, enabling continuous service delivery. The relocation of corporate headquarters to Texas and Florida generates substantial commercial contracts with strict maintenance requirements, benefiting large-scale providers capable of comprehensive grounds maintenance services.

The Southwest region shows the highest projected growth rate. Business relocations to Phoenix and Las Vegas, along with water conservation mandates, drive demand for drought-resistant landscaping, efficient irrigation systems, and artificial turf. Contractors specializing in desert landscaping and understanding local rebate programs have an advantage, as municipalities encourage alternatives to traditional grass lawns. The presence of regional sports facilities increases service requirements, necessitating advanced turf management expertise.

The Northeast and Midwest maintain steady growth through established residential areas, educational institutions, and healthcare facilities requiring specialized maintenance and comprehensive service contracts, including leaf and snow removal. Boston and New York suburban areas sustain premium pricing as homeowners prioritize aesthetic maintenance but lack time and resources for self-maintenance. In California, environmental regulations drive demand for electric equipment and water-efficient designs, requiring service providers to modernize equipment and adapt plant selections. The Pacific coast's high property values and environmental awareness support investment in native plants and efficient irrigation systems, despite seasonal limitations in specific areas.

Competitive Landscape

The market remains highly fragmented, with the five largest firms - BrightView Holdings, Inc., The Davey Tree Expert Company, TruGreen Limited Partnership, Ruppert Landscape Inc., and Gothic Landscaping Inc. - collectively holding a smaller share of the United States lawn care market in 2024. BrightView Holdings maintains its market leadership through multi-state branch networks, enabling the company to secure long-term corporate and municipal contracts. In August 2024, the Davey Tree Expert Company expanded its market presence through strategic acquisitions, including VanCurren Service and Midwest Land Clearing. TruGreen focuses on residential lawn fertilization and weed control programs, supported by its national call center infrastructure.

Private equity firms maintain a significant interest in the lawn care market, attracted by consistent cash flows and consolidation opportunities. Platform companies pursue acquisitions to increase operational capacity, expand geographic coverage, and enhance service offerings in tree care and pest management. Technology adoption creates competitive advantages, as demonstrated by BrightView's implementation of autonomous mowers and AI-based scheduling systems, reducing labor dependencies. Medium-sized independent operators adapt by implementing digital solutions for route optimization, customer interfaces, and performance tracking, which improve customer retention and pricing accuracy.

Environmental responsibility has become a key competitive factor in the market. Customers increasingly demand carbon footprint assessments, electric equipment options, and native landscaping solutions that minimize water and chemical usage. Companies that demonstrate quantifiable sustainability results gain advantages, particularly in institutional and municipal contract bids. The market's fragmented nature continues to drive consolidation, with well-capitalized companies positioned to increase market share through operational improvements and strategic acquisitions.

United States Lawn Care Industry Leaders

BrightView Holdings, Inc.

The Davey Tree Expert Company

TruGreen Limited Partnership

Ruppert Landscape Inc. (Knox Lane LP)

Gothic Landscaping Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: LawnStarter, a digital marketplace for outdoor services professionals, expanded USD 100 million in bookings and achieved profitability for the second consecutive year. The company implemented artificial intelligence and machine learning solutions to enhance its outdoor services operations.

- August 2024: The Davey Tree Expert Company acquired VanCurren Service and Midwest Land Clearing, broadening service scope across the Great Lakes region.

- June 2024: Kian Capital Partners announced a strategic investment in Diamond Landscaping to accelerate the acquisition-led expansion of high-end residential services.

United States Lawn Care Market Report Scope

This market study is focused on lawn care and maintenance services. The lawn care market mainly involves lawn mowing and maintenance, lawn aeration, fertilization, weed control services, sprinkler system maintenance, and winterization, dethatching and power raking, lawn replacement and restoration costs, and other services that help in the maintenance and care of lawns.

The United States Lawn Care Market is segmented by Service Type (Maintenance Services and Ancillary Services) and Application (Commercial and Residential). The report offers market size and forecast value (USD) for all the above segments.

| Maintenance Services | Mowing |

| Fertilization and Weed Control | |

| Irrigation System Maintenance | |

| Pest Control | |

| Ancillary Services | Landscape Design and Installation |

| Hardscaping Services | |

| Snow Removal |

| Residential |

| Commercial and Industrial |

| Golf Courses and Sports Facilities |

| Municipal and Government |

| Subscription Contracts |

| One-Off / On-Demand Visits |

| Direct In-House Teams |

| Franchise Network |

| Online Marketplaces |

| By Service Type | Maintenance Services | Mowing |

| Fertilization and Weed Control | ||

| Irrigation System Maintenance | ||

| Pest Control | ||

| Ancillary Services | Landscape Design and Installation | |

| Hardscaping Services | ||

| Snow Removal | ||

| By Application | Residential | |

| Commercial and Industrial | ||

| Golf Courses and Sports Facilities | ||

| Municipal and Government | ||

| By Business Model | Subscription Contracts | |

| One-Off / On-Demand Visits | ||

| By Distribution Channel | Direct In-House Teams | |

| Franchise Network | ||

| Online Marketplaces | ||

Key Questions Answered in the Report

How large is the United States lawn care market in 2026?

The United States lawn care market is valued at USD 62.91 billion in 2026 and is projected to reach USD 79.68 billion by 2031.

Which segment holds the highest United States lawn care market share?

Maintenance services dominate with 91.55% of revenue in 2025.

What is driving the rapid growth of golf course and sports facility lawn care?

Renovation cycles and entertainment-focused short-course formats are pushing this segment to a 10.05% CAGR through 2031.

How are labor shortages being addressed by lawn care providers?

Companies are combining higher wages, H-2B visa hiring, and accelerated adoption of autonomous mowing technology to mitigate workforce gaps.

Why are subscription contracts popular among commercial and residential clients?

Subscriptions provide predictable monthly costs, consistent service quality, and enable providers to optimize routing and resource utilization.

Page last updated on: