Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

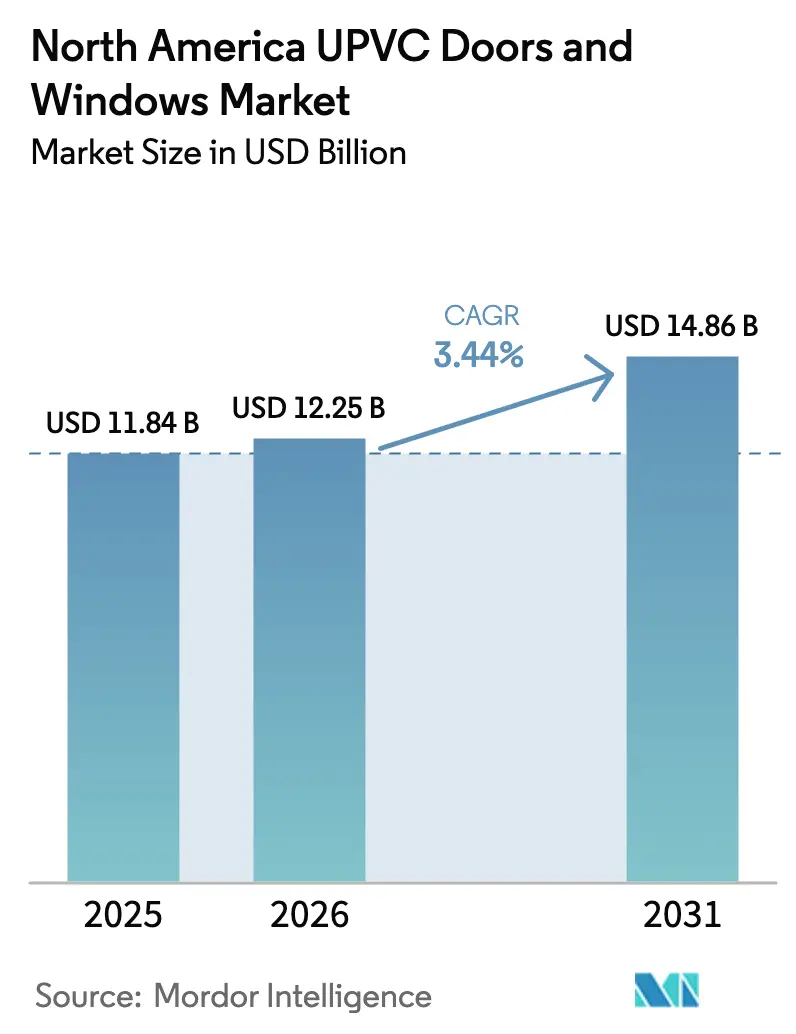

| Base Year Market Size (2025) | USD 11.84 Billion |

| Market Size (2026) | USD 12.25 Billion |

| Market Size (2031) | USD 14.86 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

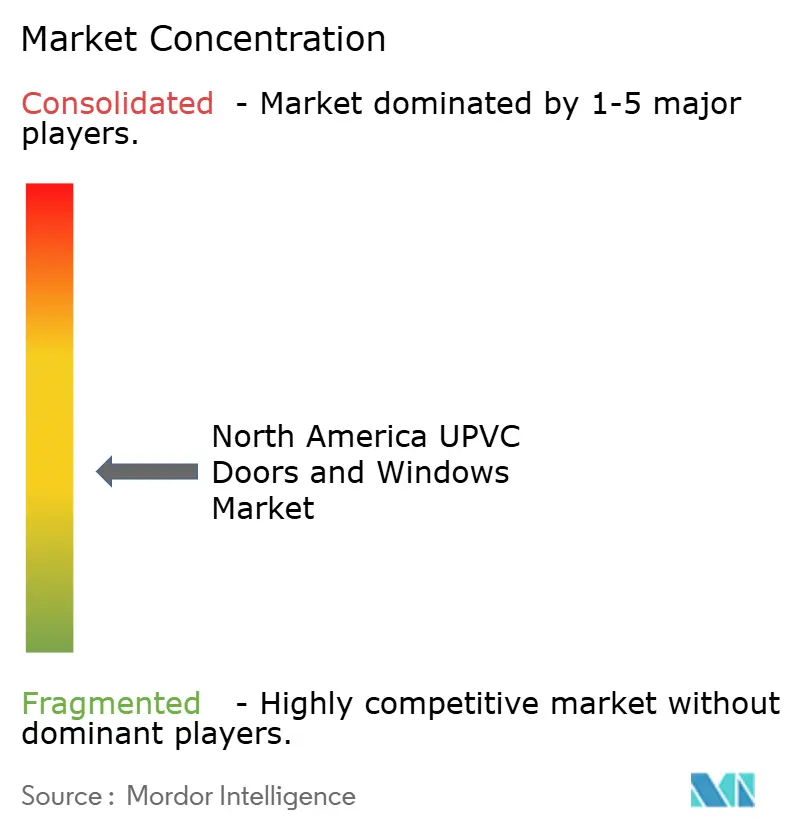

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America UPVC Doors And Windows Market Analysis by Mordor Intelligence

The North America UPVC Doors And Windows Market size is expected to grow from USD 11.84 billion in 2025 to USD 12.25 billion in 2026 and is forecast to reach USD 14.86 billion by 2031 at 3.44% CAGR over 2026-2031.

Growth tracks a durable replacement cycle as older housing and code-tightening upgrade pathways favour efficient fenestration, while channel mix shifts toward omnichannel buying and manufacturer-direct installation services that compress dealer margins without compromising service. Federal incentives lower payback periods and accelerate the adoption of ENERGY STAR Most Efficient-certified units, which in practice steers many projects toward higher performance U-factors and SHGC thresholds in colder and mixed climates[1]Source: ENERGY STAR, “Residential Windows and SGD ENERGY STAR Most Efficient 2025 Criteria,” ENERGY STAR, energystar.gov. Florida’s wind-borne debris and impact requirements, alongside grant programs that subsidize hardened openings, keep coastal demand resilient through seasonal storm windows and door replacements. Manufacturers respond with installation innovations and digital tools that shorten cycle times, simplify tax-credit eligibility verification, and reduce call-backs, which support unit economics in a tight labour market. Geographically, the United States remains the demand anchor, Mexico outpaces in growth due to code modernization and industrial build-outs, and Canada stays tied to policy signals surrounding ENERGY STAR program administration and national code updates.

Key Report Takeaways

- By product type, uPVC windows led with 65.83% of the North America uPVC doors and windows market share in 2025 and are forecast to expand at a 4.13% CAGR through 2031.

- By end user, the residential segment held 58.14% of the North America uPVC doors and windows market share in 2025, while the commercial segment records the highest projected growth at a 3.92% CAGR through 2031.

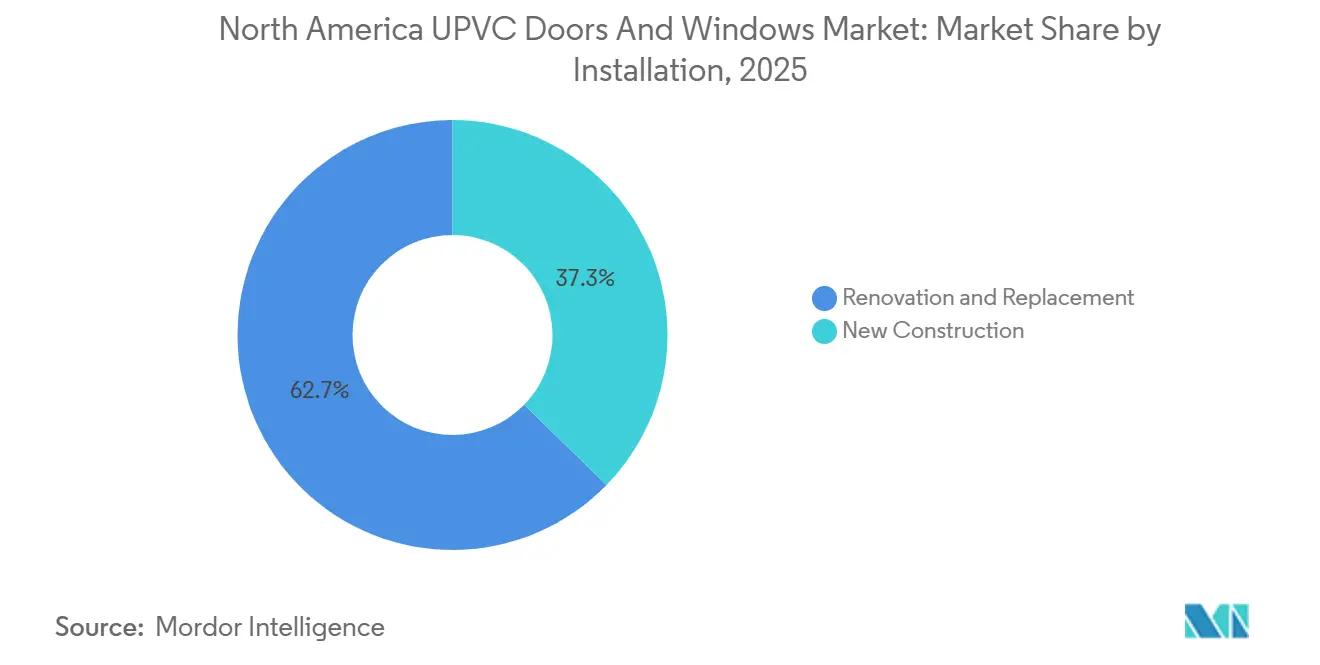

- By installation, renovation and replacement accounted for 62.72% of the North America uPVC doors and windows market share in 2025 and are advancing at a 3.58% CAGR through 2031.

- By distribution channel, distributor and dealer networks held 54.68% of the North America uPVC doors and windows market share in 2025, while retail and online distribution is the fastest expanding channel at a 4.82% CAGR through 2031.

- By geography, the United States accounted for 83.71% of the North America uPVC doors and windows market share in 2025, while Mexico posts the highest forecast growth at a 4.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America UPVC Doors And Windows Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent energy-efficiency regulations & incentives | +0.8% | Global, strongest in California, Washington State, Canada (ENERGY STAR Version 5.0) | Medium term (2-4 years) |

| Renovation-led demand surge | +0.9% | United States core, spillover to Canada | Short term (≤ 2 years) |

| Material cost-advantage vs. wood & aluminum | +0.5% | National, amplified in cost-sensitive Midwest markets | Medium term (2-4 years) |

| Insurance-driven uptake of hurricane-rated uPVC | +0.6% | Coastal Florida, Gulf Coast, Southeast Atlantic regions | Short term (≤ 2 years) |

| Recycled-content extrusion capacity expansion | +0.3% | National, led by states with PCR mandates | Long term (≥ 4 years) |

| Smart-sensor-ready profile adoption | +0.4% | Metropolitan areas, expanding to suburban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy-Efficiency Regulations & Incentives

Energy-efficiency criteria continue to tighten across the region, with ENERGY STAR Version 7.0 pushing U-factors lower and raising SHGC expectations for high-performance fenestration, which effectively steers many premium residential lines toward triple-pane options in northern zones[2]Source: Andersen Windows, “ENERGY STAR version 7.0: Your quick guide to what’s changed,” Andersen Windows, andersenwindows.com. Federal support bolsters local adoption through programs and grants that help jurisdictions move to more efficient model codes, which in turn nudge builders and remodelers toward low U-factor windows that meet the prescriptive path or earn credits under performance paths within the 2024 IECC. DOE guidance and the Energy Saver framework document how low-e and advanced glazing reduce heating and cooling loads, and those savings tie into incentive programs and homeowner tax credits that improve ROI on fenestration upgrades. NFRC’s 2023 technical updates to U-factor and SHGC procedures strengthen the linkage between product testing and real-world label values, which helps mitigate warranty disputes and supports compliance across code jurisdictions. California’s Title 24 Part 6 2025 update moves the state toward tighter envelope baselines and heat pump norms, and it often raises the performance bar for windows and doors in ways that cascade into product development and stocking strategies across national portfolios.

Renovation-Led Demand Surge

Replacement momentum remains a defining growth axis for the North America uPVC doors and windows market as aging housing and energy-bill sensitivity prioritize envelope improvements that deliver measurable comfort and utility-bill outcomes. Code updates and available credits make it easier for homeowners to pick compliant products, claim tax benefits through standardized forms, and move forward with multi-opening projects that would otherwise be delayed. Utility programs and local initiatives add stackable rebates that further compress the payback period, keeping replacement activity resilient during phases of higher interest rates and constrained new-home supply. National associations and rating councils have standardized rating protocols for U-factor and Solar Heat Gain Coefficient (SHGC), which simplifies specifying and comparing windows and doors across brands, and this reduces friction in the sales process for replacement decisions. Manufacturers have introduced installation systems that allow faster, cleaner replacements from the interior, which lowers project disruption and labour hours, raising throughput per crew and helping alleviate skilled installer bottlenecks.

Material Cost-Advantage vs. Wood & Aluminum

uPVC maintains a favourable installed-cost position against many wood and aluminum alternatives in typical residential and low-rise settings, and this price-performance mix supports its share in replacement-heavy markets where budget and speed are decisive. Energy performance gains are accessible across uPVC product lines due to design flexibility and insulated framing strategies that achieve compliant U-factors without exotic materials, which helps projects qualify for tax credits and rebate programs. In cold or mixed climates, ENERGY STAR Most Efficient criteria and IECC prescriptive values steer buyers into configurations where uPVC’s thermal profile performs well at mainstream price points. National Fenestration Rating Council (NFRC) labelling assures buyers and inspectors that certified performance aligns with code and incentive documentation, and this standardization reduces the soft costs of selecting uPVC options for multifamily retrofits or phased single-family projects. As codes add performance pathways and cities adopt stretch codes, manufacturers can offer uPVC models that meet those thresholds while keeping installed costs in a range acceptable to cost-sensitive homeowners and small commercial operators.

Smart-Sensor-Ready Profile Adoption

Smart-ready window and door systems connect fenestration to home and building controls, enabling ventilation scheduling, security monitoring, and energy management that supports code compliance and voluntary program targets. As ENERGY STAR and International Energy Conservation Code (IECC) pathways reward reduced overall energy loads, connected openings complement HVAC and shading controls to improve comfort and outcomes aligned with performance-based compliance. Manufacturers that publish clear documentation, integration guides, and performance data ease adoption by builders and retrofit contractors who want verified pathways to rebates and credits. The rating council and code bodies provide the framework to verify the envelope’s contributions to energy models, and smart control layers build on that framework to fine-tune usage and indoor air quality. Over time, metropolitan early adopters shape preferences that spread into the suburbs as product costs fall and user familiarity grows, especially when manufacturers integrate sensors and connectivity without adding complexity to installation or service.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC resin price volatility | -0.6% | National, exacerbated by import tariff risks | Short term (≤ 2 years) |

| Competition from thermally broken aluminum | -0.5% | High-end residential, commercial markets in colder and coastal jurisdictions | Medium term (2-4 years) |

| ESG limits on virgin PVC | -0.4% | States with PCR focus, large corporate procurement policies | Long term (≥ 4 years) |

| Skilled installer shortage | -0.4% | National, most acute in metropolitan centres | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Thermally Broken Aluminum

Thermally broken aluminum continues to improve U-factors and assembly techniques to meet stricter code thresholds, which narrows uPVC’s thermal advantage in certain commercial and high-end residential specifications. In cold climate zones under 2024 IECC and ASHRAE 90.1, aluminum systems that integrate thermal breaks, warm-edge spacers, and triple glazing can achieve performance levels that satisfy prescriptive paths, and architects often prefer the slimmer sightlines and span capacity for larger openings. Code adoption trends elevate minimums for fixed and operable fenestration, and these thresholds open pathways for aluminum products to qualify while maintaining aesthetic and structural preferences in commercial use cases. In coastal markets, corrosion-resistant finishes and impact-rated configurations are widely available for aluminum, which, when combined with code compliance, present credible alternatives to uPVC where project design requires tall or wide spans. Even with higher installed costs, aluminum’s durability and form factor can justify specifications where lifecycle considerations, façade design, and project budgets align under strict code constraints.

Skilled Installer Shortage

Labor scarcity constrains throughput for fabricators and installers and pushes wages higher, which can outpace price increases and compress margins during periods of cost sensitivity. Industry associations and training platforms are scaling programs to close skills gaps for Computer Numerical Control (CNC) operation, welding, glazing, and automated line maintenance, but enrollment still trails the volume of open positions in many metro areas. Manufacturers are investing in automation, including robotics and Automated Guided Vehicles (AGVs), to reduce per-unit labour hours and improve consistency, which helps mitigate staffing gaps and supports dealer and retail service level agreements. Installation innovations that enable interior mounting reduce scaffolding costs and exposure to weather, allowing crews to complete more openings per day and increase monthly installed capacity without sacrificing quality. Workforce development remains a priority for associations and companies because it directly influences replacement cycle velocity and the ability to fulfill larger commercial awards on schedule.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Windows Lead, Yet Growth Parity Signals Maturation

uPVC windows captured 65.83% of the 2025 North America uPVC doors and windows market share, and are set to grow at a 4.13% CAGR through 2031. Intensifying ENERGY STAR criteria and IECC updates elevate the required performance for residential and light commercial fenestration, which in practice keeps window specifications front and centre due to their contribution to envelope U-factors and Solar Heat Gain Coefficient (SHGC) targets across climate zones. Products that meet ENERGY STAR Most Efficient thresholds or comply with stretch codes gain an advantage by simplifying rebate and tax credit documentation for homeowners and builders. Labelling and performance verification through the National Fenestration Rating Council’s updated procedures further streamlines code inspections and aligns expectations for delivered U-factor and SHGC, which reduces rework and warranty claims. For owners and facility managers, the lifecycle equation pairs thermal performance with installed cost and maintenance profile, which supports the use of uPVC across a wide span of typical openings in residential and smaller commercial projects in the North America uPVC doors and windows market.

uPVC doors maintain growth parity because code and insurance requirements for impact-rated entries remain prominent in coastal states, and because insulated uPVC door systems can reach attractive R-values while keeping installed costs accessible for replacement projects. As jurisdictional energy standards move toward higher envelope baselines in 2026, manufacturers have focused on improved cores and glazing options to meet U-factor targets for half-light and full-light door designs where daylighting is desired. The NFRC framework helps buyers compare door and window performance on a uniform basis, and this transparency supports broader adoption of performance-tiered uPVC offerings. Installation tools and knockdown frame options introduced by leading brands shorten install times, which raises throughput per crew and lowers total cost of ownership for time-sensitive remodelling projects. Over the forecast period, product development targeting thermal bridging, hardware integration, and smart-ready features keeps both windows and doors aligned with evolving code and user-experience expectations across the North America uPVC doors and windows market.

By End User: Commercial Outpaces Residential Despite Smaller Base

The residential segment remained the largest by volume with 58.14% share in 2025, benefiting from an entrenched replacement cycle and tax credits that promote whole-home upgrades, while the commercial segment is the fastest growing with a 3.92% CAGR on specifications tied to ASHRAE 90.1 and performance-led code paths. Energy modelling for performance-based compliance and evolving municipal standards push commercial owners to evaluate envelope improvements that reduce whole-building loads, which can tilt specifications toward higher-performing fenestration configurations[3]Source: U.S. Department of Energy, “Commercial and Residential Building Energy Codes,” DOE, energycodes.gov. Utility programs and public-sector procurement standards encourage the selection of products with clear performance documentation, environmental transparency, and durability, which aligns with uPVC offerings that meet certified thresholds at competitive cost. Institutional buyers often weigh lifecycle and warranty support heavily, an area where manufacturer-direct installation and service programs have grown to ensure product performance and compliance alignment. Residential momentum remains resilient as households leverage tax credits, while installers rely on standardized documentation like Qualified Manufacturer Identification Numbers to simplify claims.

Commercial buyers also benefit from code consistency and labelling assurance across multi-jurisdiction portfolios, which reduces compliance risk when deploying retrofit programs at scale in the North America uPVC doors and windows market. For institutional facilities and light industrial buildings, budgets and maintenance practicalities favour materials that deliver reliable thermal performance and cost control under frequent use, which positions uPVC for non-structural, standard-size openings. In office-to-residential conversions and adaptive reuse, uPVC’s thermal and acoustic characteristics are often sufficient when paired with appropriate glazing and spacer technologies to meet code and comfort goals. Public incentives, where available, add further support when projects can document code or performance gains for envelope upgrades as part of whole-building energy plans. This demand profile underscores why commercial growth can edge ahead of residential, even as residential retains the larger share in the North America uPVC doors and windows market.

By Installation: Renovation Sustains Lead as Aging Stock Drives Replacement

Renovation and replacement accounted for 62.72% of 2025 installations and are forecast to grow at a 3.58% CAGR through 2031, supported by tax incentives, rebate stacks, and code minimums that are easier to hit with modern uPVC assemblies that have verified labels and performance data. The North America uPVC doors and windows market benefits from simplified filing mechanics for credits under Form 5695 and from clear Qualified Manufacturer Identification Number requirements that standardize eligibility and documentation. Utility rebate programs in select states add stackable benefits on top of federal credits, which together can recover a meaningful portion of installation costs for qualifying projects. In coastal markets, grants for impact-rated units further subsidize upgrades, reinforcing replacement cycles tied to weather resilience and insurance underwriting incentives. Fast-install systems and interior mounting options help crews complete more openings per day with fewer safety risks and lower disruption for occupants, which favours replacement projects on tight timelines.

New construction retains a significant role, and growth continues as builders align with the 2024 IECC across adopting jurisdictions and adjust plan sets to meet prescriptive U-factors or to access performance credits where envelope improvements are cost-effective. Larger builders and multifamily developers benefit from standardized code compliance and labelling that reduce inspection friction and allow smoother scheduling through procurement and installation. In net new builds, uPVC is competitive for standard-size openings, with strong performance at accessible installed costs where sightline preferences and structural spans do not require specialty framing. Programs that recognize efficient envelopes and qualify projects for credits or green certifications encourage builders to consider higher-performing fenestration as part of broader HVAC and envelope optimization. The balance remains tilted toward renovation and replacement because incentives, installed-cost dynamics, and shorter cycle times match homeowner priorities in the North America uPVC doors and windows market.

By Distribution Channel: Retail/Online Surge Reflects Direct-to-Consumer Shift

Distributor and dealer networks held 54.68% share in 2025, yet retail and online are the fastest-growing channels at a 4.82% CAGR to 2031, reflecting sustained shifts to digital research, configuration, and scheduling alongside showroom support. Manufacturer-direct sales and service models deepen as brands invest in digital content, showrooms, and launch programs that reinforce product education and streamline the sales-to-installation workflow. Tax credits and code documentation hosted on manufacturer sites give buyers confidence that chosen models meet program thresholds during the purchase process, which reduces reliance on third-party interpretation and helps avoid errors in claims. Associations support the channel transition through training, market studies, and best practice sharing that help dealers and installers add value on complex or multi-measure projects. In parallel, product labeling and NFRC resources allow online spec comparisons that build buyer comfort with selecting higher-performance SKUs in the North America uPVC doors and windows market.

Omnichannel models blend configurator-led research, showroom confirmation, and manufacturer or certified installer execution, which reduces friction and ensures compliance with impact-rated and code-labelled products. At major industry events, brands highlight installation systems and performance upgrades that translate directly into channel value propositions, which in turn strengthen their direct sales motions and support dealer partnerships on complex jobs. Documentation for energy credits and rebates remains easier to access through manufacturer sites, which nudges shoppers into ecosystems where eligibility is guaranteed, and paperwork is standardized. As jurisdictions refine energy codes and municipalities adopt stretch codes, distributors and retailers that align with manufacturer-led documentation and training will be better positioned to handle compliance questions during peak seasons. This channel evolution favours players who can blend digital discovery, verified documentation, and high-quality installation at scale across the North America uPVC doors and windows market.

Geography Analysis

The United States accounted for 83.71% of 2025 revenues, and it advances at a 3.22% CAGR through 2031 as the North America uPVC doors and windows market stays replacement-led with new construction steadying where code adoption is consistent, and builder pipelines are disciplined. Federal tax credits and a growing web of state and utility rebate programs create strong conditions for compliant products to carry a larger portion of replacement projects in colder and mixed climates. Local code enforcement and stretch code adoption elevate baselines in key states, which in turn raises performance tiers for fenestration and keeps uPVC well positioned in standard residential openings. In Florida and other coastal jurisdictions, impact-rated products dominate weather-hardening strategies under the Florida Building Code and related approvals frameworks, and insurer incentives encourage full-system upgrades rather than piecemeal replacements. National rating and labeling systems remain essential to simplify cross-state specification and inspection for production builders and multi-jurisdiction owners.

Mexico posts the fastest forecast growth at a 4.94% CAGR as nearshoring and industrial construction sustain demand and as regional codes and standards incorporate tighter thermal performance for fenestration in relevant building types. The North America uPVC doors and windows market benefits from cross-border product strategies that leverage United States labelling and performance documentation, which many buyers and inspectors are familiar with, particularly for light commercial and institutional settings. Trade normalization under updated frameworks and manufacturer expansion of regional support improve availability and shorten lead times for code-compliant fenestration. As climate and comfort requirements translate into procurement checklists for large projects, uPVC’s balance of installed cost and thermal results supports adoption where aluminum’s structural advantages are not required. Over the forecast period, product documentation and training for installers will be important to maintain quality and ensure code alignment during rapid growth phases.

Canada’s trajectory reflects policy signals around ENERGY STAR for products, provincial programs, and national code evolution, which together influence the cadence of fenestration upgrades across regions with varied heating degree-day profiles. Discussions about program administration create uncertainty for rebate-linked purchases, yet Natural Resources Canada’s criteria and labelling resources provide a domestic framework for product eligibility and climate-zone alignment. Provincial pathways, such as British Columbia’s step code approach, show how multi-year planning can guide product roadmaps and installer training with predictable milestones. As public-sector and institutional buyers ask for performance and environmental documentation, uPVC’s value proposition remains centred on certified performance and cost stability in standard apertures. Across the region, cross-border companies will continue to emphasize harmonized labelling, code familiarity, and service networks that support consistent outcomes in the North America uPVC doors and windows market.

Competitive Landscape

Competitive dynamics point to a moderate concentration with several national brands and many regional players, and strategies focus on installation innovation, selective consolidation, and supply chain resilience that can handle tariff and code variability across jurisdictions. One pillar of differentiation is installation efficiency, where systems designed for interior mounting reduce labour hours and weather exposure while simplifying homeowner scheduling, which supports higher throughput in replacement-heavy channels. Another pillar is automation, as leading manufacturers add robots and AGVs to boost line speed, quality consistency, and uptime in response to persistent skilled labour shortages in fabrication and assembly[4]Source: ASSEMBLY Magazine, “Pella Opens a Window on Automation,” ASSEMBLY Magazine, assemblymag.com. A third pillar is targeted M&A to secure component supply and regional capacity, exemplified by acquisitions aimed at strengthening component availability and stabilizing cost structures in a volatile trade environment. Documentation, labelling, and code literacy also form a quiet moat, as teams that can navigate jurisdictional differences deliver smoother inspections and lower rework risks across the North America uPVC doors and windows market.

Companies have highlighted a set of moves in 2025 that align with this strategy. Andersen Corporation announced the acquisition of Bright Wood Corporation to secure component continuity and to strengthen resilience against supply fluctuations, which supports consistent service levels across regions[5]Source: PR Newswire, “Andersen Corporation Announces Acquisition of Bright Wood,” PR Newswire, prnewswire.com. Pella earned industry recognition for its interior installation system and continued to invest in product lines that accelerate install times and reduce crew exposure, which improves project economics for busy replacement seasons. Pella also advanced factory automation to mitigate labour constraints and improve assembly throughput, which helps maintain lead times and quality under sustained demand. JELD-WEN undertook portfolio simplification and announced workforce reductions to reduce costs and focus operations, which continues a multi-year effort to streamline its manufacturing footprint and improve margins under mixed demand.

Marketing and channel approaches reflect a stronger direct connection with end buyers, including digital content, design tools, and showroom experiences that help homeowners and commercial buyers validate performance and aesthetic choices prior to ordering. Manufacturers also emphasize program eligibility and tax-credit qualifiers in their documentation, which allows sales teams to reassure purchasers about compliance and payback trajectories during consultations. Across the North America uPVC doors and windows market, scale players and regional specialists compete through responsiveness, code and inspection fluency, and installation productivity, with the aim of protecting margins while offering tangible value to property owners. The combination of innovation, selective consolidation, and code-driven performance tiers should maintain a healthy balance between national brands and agile local providers that can quickly adjust to climate-specific and code-specific needs in their service territories.

North America UPVC Doors And Windows Industry Leaders

Andersen Corporation

Pella Corporation

JELD-WEN Holding Inc.

Cornerstone Building Brands (MI Windows)

Ply Gem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Andersen Corporation acquired Bright Wood Corporation, the largest independent United States manufacturer of window and patio door components, reinforcing component continuity during tariff and supply variability. The combined capabilities are positioned to stabilize production planning across Andersen’s network and to maintain service levels during peak replacement cycles. Bright Wood continues to operate with dedicated leadership to serve industry customers as part of the transition.

- December 2025: GEALAN, a European manufacturer in uPVC systems, launched United States operations in February 2025 with facilities in Heath, Ohio. This expansion introduces German-engineered tilt-and-turn windows, GEALAN-acrylcolor® technology, and energy-efficient solutions to American manufacturers, builders, and architects, reflecting the company’s commitment to delivering innovative products and strengthening its presence in the United States market.

- September 2025: United Window & Door, a regional vinyl window and door manufacturer, announced a USD 6.5 million expansion of its New Jersey facilities. The project will add 40,000 square feet of production space, advanced manufacturing technology, and a second automated line, increasing capacity by 250,000 windows annually and creating over 75 new jobs.

- February 2025: Pella debuted redesigned Lifestyle Series wood sliding patio doors at IBS 2025, featuring standard knockdown frames on multi-panel sets and optional triple-pane glass that meets ENERGY STAR in all 50 states. The design aims to streamline installation while providing contemporary aesthetics with narrow bottom rails and improved energy performance options. The launch comes as Pella marks its 100th anniversary and highlights channel partnerships.

North America UPVC Doors And Windows Market Report Scope

UPVC, also called unplasticized polyvinyl chloride, is low maintenance and cost-effective material used in building and construction, especially in pipework and window frames. The North America UPVC Doors and Windows Market is segmented by product type (UPVC doors and UPVC windows), end-user (residential, commercial, industrial and construction, and other end-users), distribution channel (offline stores and online stores), and geography (United States, Canada, Mexico and rest of North America). The report offers Market size and forecasts for North America UPVC Doors and Windows Market in transaction volume and/or revenue (USD) for all the above segments.

By Product Type

| uPVC Doors | Sliding Doors |

| Casement Doors | |

| Tilt & Turn Doors | |

| French Doors | |

| Others | |

| uPVC Windows | Sliding Windows |

| Casement Windows | |

| Tilt & Turn Windows | |

| Others (Picture / Fixed Windows,Awning Windows) |

By End User

| Residential |

| Commercial |

| Industrial & Institutional |

By Installation

| New Construction |

| Renovation & Replacement |

By Distribution Channel

| Direct Sales (Manufacturers) |

| Distributor / Dealer Network |

| Retail & Online |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | uPVC Doors | Sliding Doors |

| Casement Doors | ||

| Tilt & Turn Doors | ||

| French Doors | ||

| Others | ||

| uPVC Windows | Sliding Windows | |

| Casement Windows | ||

| Tilt & Turn Windows | ||

| Others (Picture / Fixed Windows,Awning Windows) | ||

| By End User | Residential | |

| Commercial | ||

| Industrial & Institutional | ||

| By Installation | New Construction | |

| Renovation & Replacement | ||

| By Distribution Channel | Direct Sales (Manufacturers) | |

| Distributor / Dealer Network | ||

| Retail & Online | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the North America uPVC doors and windows market?

The North America uPVC doors and windows market size is estimated at USD 12.25 billion in 2026, with a forecast to reach USD 14.86 billion by 2031 at a 3.44% CAGR.

Which product categories are leading, and how fast are they growing in North America?

UPVC windows lead with 65.83% share in 2025, and uPVC windows are projected to grow at a 4.13% CAGR through 2031.

Which installation type is driving demand across North America?

Renovation and replacement accounted for 62.72% of 2025 installations and are advancing at a 3.58% CAGR as incentives, documentation, and installation systems support faster upgrades.

What are the main policies influencing specification in North America?

ENERGY STAR Version 7.0, the 2024 IECC, Title 24 Part 6 (2025 update), and NFRC labelling set the performance and documentation baseline for compliant fenestration.

Which end-user categories are increasing the adoption of uPVC solutions?

Residential holds the largest volume share, while commercial is the fastest-growing end user as ASHRAE 90.1-aligned pathways support envelope improvements under performance-led compliance.

Where is the fastest regional growth in North America?

Mexico records the highest growth at a 4.94% CAGR, while the United States remained the revenue anchor with 83.71% share in 2025.

Page last updated on: