Composite Doors And Windows Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

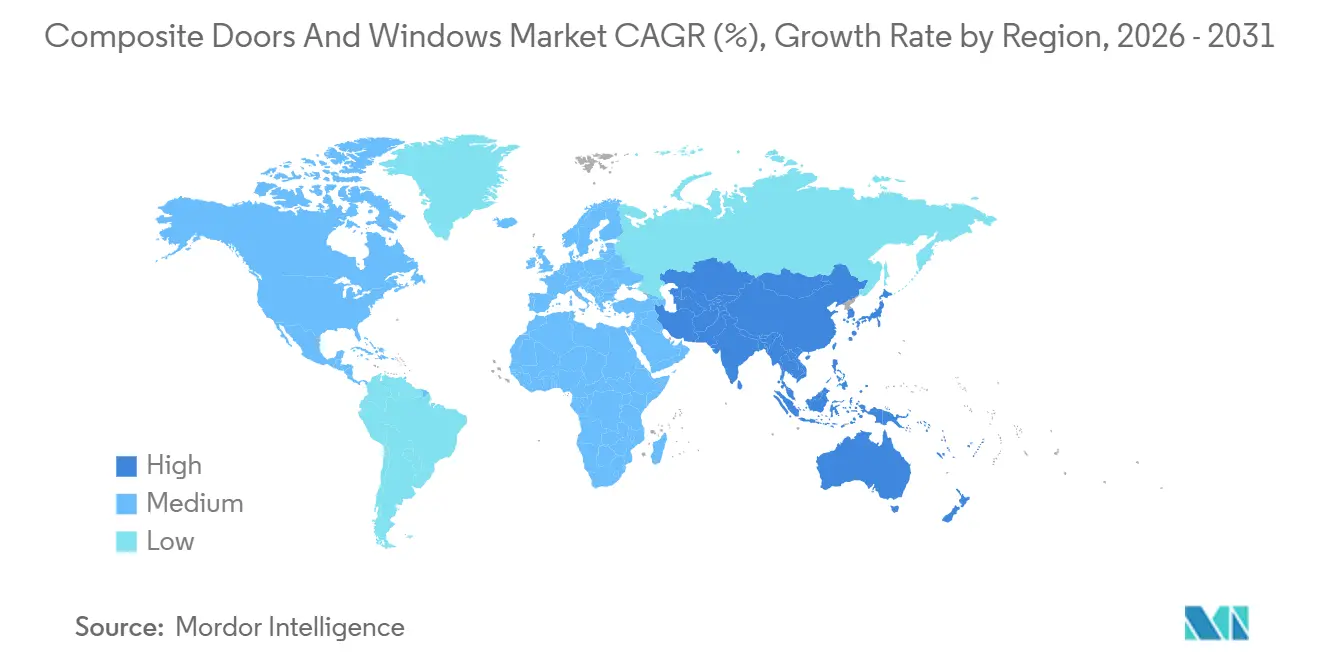

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composite Doors And Windows Market Analysis by Mordor Intelligence

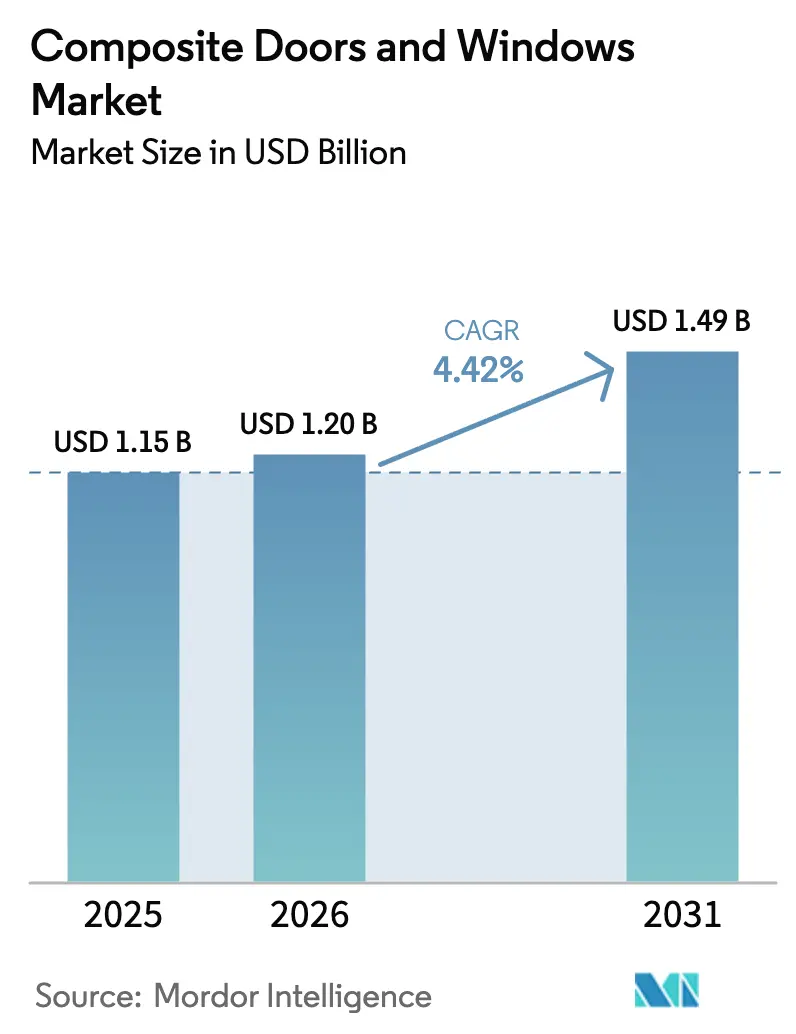

The Composite Doors And Windows Market size is expected to grow from USD 1.15 billion in 2025 to USD 1.20 billion in 2026 and is forecast to reach USD 1.49 billion by 2031 at 4.42% CAGR over 2026-2031.

Heightened thermal-performance codes, climate-risk pricing by insurers, and builder preferences for low-maintenance frames are driving demand away from traditional aluminum and vinyl towards composite alternatives, which offer high strength and very low thermal conductivity. Europe is expected to account for the largest revenue share by 2025, but growth in Asia-Pacific is accelerating due to the rise of off-site façade factories and stricter energy regulations. Glass-reinforced plastic (GRP) continues to dominate in hurricane-prone North America, where impact-rated frames provide significant wind-storm insurance discounts. Fiber-reinforced polymer (FRP) is growing rapidly as bio-attributed resins reduce embodied carbon while maintaining fire safety standards. Competitive intensity is increasing with vertical integration and material innovation, as seen in Masonite’s acquisition of PGT Innovations and Eurocell’s consolidation of four UK door brands. On the policy side, the EU Energy Performance of Buildings Directive and retrofit subsidies in Germany, France, and the UK are accelerating replacement cycles, while U.S. federal tax credits of up to USD 600 per opening are boosting demand for ENERGY STAR Most Efficient products.

Key Report Takeaways

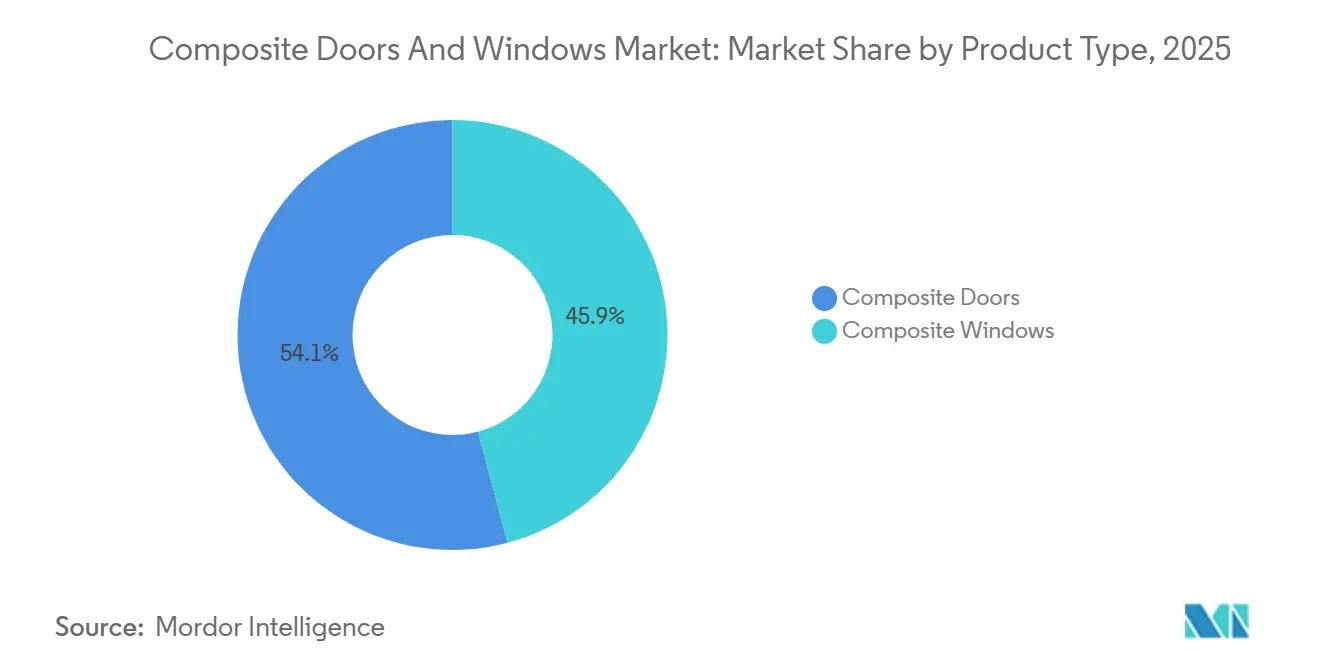

- By product type, composite doors led with 54.11% of the composite doors and windows market share in 2025, while composite windows are projected to grow at a 4.81% CAGR through 2031.

- By material type, Glass Reinforced Plastic (GRP) held 67.71% of the composite doors and windows market share in 2025, whereas Fiber-Reinforced Polymer (FRP) is forecast to register the highest 4.65% CAGR through 2031.

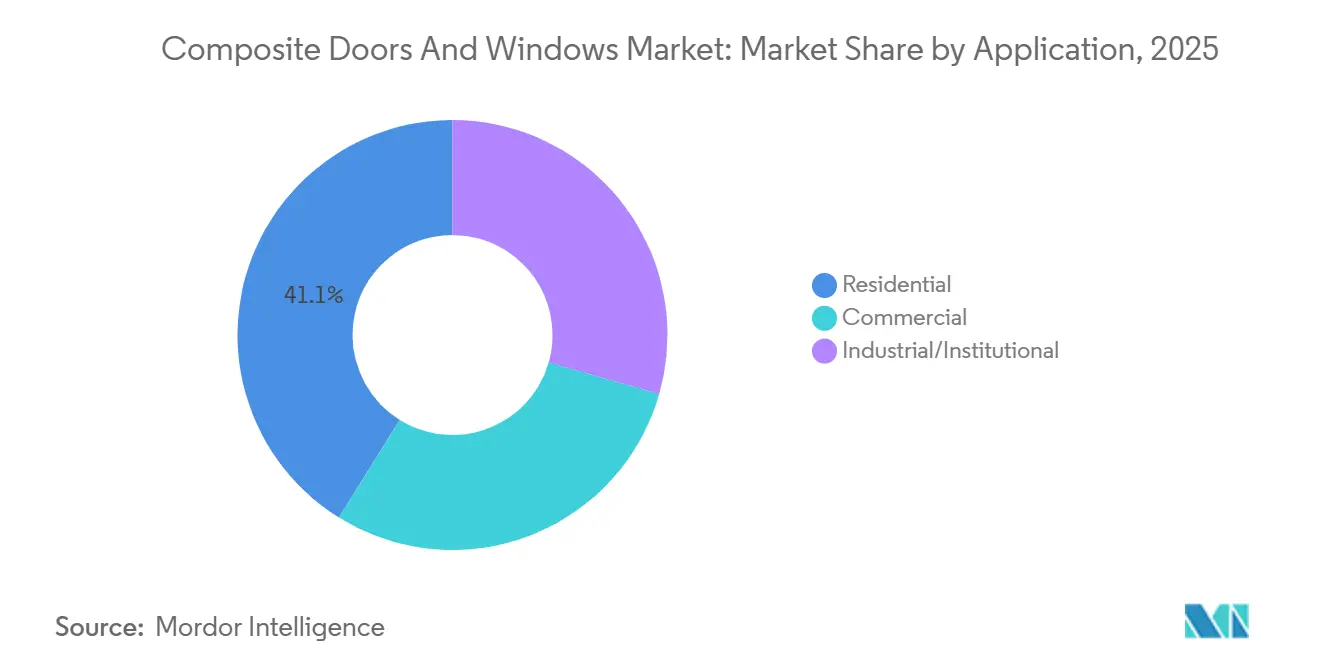

- By application, the residential segment accounted for 41.14% of the composite doors and windows market share in 2025, while the commercial segment is forecast to register the highest 4.97% CAGR through 2031.

- By geography, Europe generated 43.24% of of the composite doors and windows market share in 2025, but Asia-Pacific is anticipated to expand at a 5.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Composite Doors And Windows Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for energy-efficient building envelopes | +1.2% | Global | Long term (≥4 years) |

| Low maintenance and superior durability of composites | +0.9% | Global | Long term (≥4 years) |

| Surge in modular façade factories in emerging Asia-Pacific | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Insurance-premium discounts for hurricane-rated GRP frames | +0.6% | North America (coastal states, Florida) | Short term (≤2 years) |

| Smart-glazing-ready composite frames | +0.5% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Building Envelopes

Stricter building codes in major economies are mandating lower U-values and solar heat gain coefficients, making composite frames a preferred choice. For example, China limits window-to-wall ratios to 20-35% and caps U-values at 1.5-2.0 W/m²·K, as per[1]Ministry of Housing and Urban-Rural Development, “JGJ 26-2018 Code for Energy Conservation Design,” mohurd.gov.cn. Australia’s NCC 2022 requires glazing U-values as low as 3.8 W/m²·K, along with mandatory Window Energy Rating Scheme labeling. The EU’s recast Energy Performance of Buildings Directive mandates EPC C ratings for public and non-residential buildings by 2030, driving deep-retrofit activities. Composite profiles incorporating aerogels and vacuum insulation panels, with thermal conductivities below 0.020 W/m·K, provide phase-change buffering that reduces HVAC loads and meets Passive House U-value targets of 0.8 W/m²·K. In Florida, the Building Code enforces U-factors no greater than 0.32, encouraging developers to adopt GRP and FRP frames that comply with ASHRAE 90.1-2022 and IECC standards.

Low Maintenance and Superior Durability of Composites

GRP and wood-plastic composite (WPC) frames resist rot, corrosion, and ultraviolet degradation, eliminating the need for repainting common with wood and preventing oxidation seen in aluminum. Andersen’s Fibrex, which combines reclaimed wood fiber with vinyl polymer, has surpassed 10 million units sold and achieved an 8% extrusion yield improvement through robotics upgrades. Rehau incorporates up to 86% recycled content, diverting 70,000 tons of material annually and saving 100,000 tons of CO₂. Deceuninck’s SunShield pigment technology minimizes fading in dark frames exposed to high UV levels. Academic trials with flax-carbon bio-hybrid laminates have shown 24% higher stiffness compared to pure carbon parts, indicating potential for architectural applications.

Surge in Modular Façade Factories in Emerging Asia-Pacific

Automated factories in India and China are producing finished composite panels that are ready for on-site installation, reducing labor needs and project timelines. Modulex Global’s 40-acre facility near Mumbai manufactures up to 300,000 m² of unitized façades annually with ±1 mm tolerances. Interarch has invested INR 70 crore (approximately USD 8.4 million) in Gujarat to achieve an annual throughput of 40,000 tons for composite curtain-wall modules. These factories utilize CNC routing and robotic glass insertion, minimizing on-site rework, which can add 15-25% to stick-built wall costs. Provincial incentives in Guangdong and Jiangsu are promoting this industrialized approach as part of China’s 14th Five-Year Plan.

Insurance-Premium Discounts for Hurricane-Rated GRP Frames

Certified impact windows and doors provide Florida homeowners with wind-storm insurance discounts ranging from 10–45%, with some cases reaching 68% when combined with roof upgrades. The My Safe Florida Home program reimburses inspection and retrofit costs, reducing payback periods to under three years. GRP frames certified under ASTM E1996 and E1886 absorb debris impacts without shattering, outperforming tempered glass and vinyl in coastal testing. Neighboring Gulf and Atlantic states are introducing similar incentives as storm frequency increases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited installer awareness in developing regions | -0.4% | Developing markets in APAC, Latin America, MEA | Long term (≥4 years) |

| Ambiguous carbon-footprint labelling for hybrid WPC frames | -0.2% | EU and North America | Medium term (2-4 years) |

| Anticipated PFAS-free resin mandates raising formulation costs | -0.3% | North America and EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Limited Installer Awareness in Developing Regions

Composite frames require specialized anchoring, flashing, and sealing techniques, but certified training is limited outside North America and Europe. The FGIA InstallationMasters program is only available in English and Spanish and requires prior field experience, restricting adoption in regions like India, Indonesia, and sub-Saharan Africa. Warranty claims are 30-50% higher in areas where proper installation techniques are not followed, impacting manufacturer margins and consumer confidence. While companies like Modulex and Interarch embed installation crews within their factories, this approach is not scalable for fragmented small-contractor ecosystems. Augmented-reality tools have improved comprehension, with Andersen reporting a 25% increase in lead conversion, but language barriers and inconsistent smartphone access limit their effectiveness in rural markets.

PFAS-Free Resin Mandates Raising Formulation Costs

Seven U.S. states and the European Union are phasing out per- and polyfluoroalkyl substances (PFAS) in building products, enforcing total organic fluorine thresholds of 50-100 ppm starting in 2026[2]European Chemicals Agency, “PFAS Restriction Proposal,” echa.europa.eu. 3M’s planned exit from PFAS production by the end of 2025 is tightening the supply of additives that enhance UV stability, forcing resin manufacturers to adopt more expensive siloxane or bio-based chemistries. These alternatives are 20-40% costlier and have slower curing times. Early adopters like Rehau have introduced ARTEVO TERRA, a bio-attributed PVC that reduces CO₂ emissions in the top layer by approximately 90%, positioning compliance as a premium feature. Manufacturers face the challenge of either absorbing these higher input costs or passing them on to consumers, potentially narrowing the price gap with vinyl and aluminum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Windows Accelerate as Retrofit Cycles Shorten

Composite doors accounted for 54.11% of 2025 revenue, but the composite doors and windows market size for composite windows is projected to grow at a 4.81% CAGR through 2031, surpassing the growth rate of doors. In North America, homeowners replace windows every 15-20 years compared to 25-30 years for doors. Additionally, German and French rebates of up to EUR 60,000 per home and EUR 100 per window are driving faster payback periods. ENERGY STAR Most Efficient criteria with U-factors ≤ 0.22 continue to support premium positioning.

Rehau’s SLINOVA X sliding system with a 32 mm sash is designed for balcony doors in Europe, while Andersen’s expanded 100 Series line has exceeded 10 million units sold, highlighting scale advantages. Deceuninck and Alpen have introduced Elegant triple-pane windows with U-values as low as 0.09, catering to electrochromic retrofits. Doors remain dominant in security and egress applications, with GRP options meeting BS 6853 and EN 45545 fire safety standards.

By Material Type: FRP Gains as Carbon Reduction Takes Hold

Glass Reinforced Plastic (GRP) retained 67.71% revenue in 2025, reflecting its effectiveness in hurricane-prone areas where composite doors and windows market share benefits from 10–45% insurance discounts. However, Fiber-Reinforced Polymer (FRP) is expected to grow at a 4.65% CAGR through 2031 as continuous-fiber thermoplastic matrices reduce embodied carbon by up to 88% while meeting EN 45545 HL3 fire safety standards.

WPC adoption faces challenges due to inconsistent lifecycle labeling. A 2024 study found that older emission factors understated WPC impacts by 30%, discouraging LEED and BREEAM specifiers. Manufacturers are working to secure harmonized Environmental Product Declarations to rebuild trust. Bio-composites using hemp, jute, or bamboo fibers achieve tensile strengths near 178 MPa and withstand temperatures up to 272 °C, but extrusion capacity remains concentrated in China and India.

By Application: Commercial Segment Outpaces Residential on Curtain-Wall Demand

The residential segment captured 41.14% of 2025 revenue, supported by the USD 576 billion U.S. home-improvement pipeline. However, commercial demand is projected to grow at a 4.97% CAGR through 2031 because curtain-wall architects specify FRP mullions that deliver 900× better thermal resistance than aluminum, reducing condensation-related claims.

The composite doors and windows market size for commercial curtain walls commands installed prices of USD 150-300 per square foot versus USD 40-55 for typical residential windows, improving supplier margins. EU regulations require public buildings to achieve EPC C ratings by 2030, prompting office landlords to prioritize high-performance façades. Hospitals, schools, and laboratories are adopting GRP fire-rated doors that block smoke and toxic gases, meeting BS 476 standards.

Geography Analysis

Europe contributed 43.24% of 2025 revenue, supported by generous retrofit programs such as Germany’s BEG EM grants of up to EUR 60,000 and 20% subsidies for window upgrades. France’s MaPrimeRénov’ offers EUR 40–100 per window, and the United Kingdom’s ECO4 scheme provides GBP 5,000–15,000 based on household income. Even as Italy’s Superbonus drops to 70% in 2024 and phases out, pent-up applications are sustaining demand. The upcoming Digital Product Passport will promote transparent material data, likely favoring FRP systems with lower embodied carbon. Consolidation is accelerating, as evidenced by Eurocell’s 2025 acquisition of Alunet Group to scale delivery amid the retrofit surge.

North America is driven by hurricane risk mitigation and federal tax incentives. Wind-storm insurance discounts of 10–45% in Florida reduce GRP window payback periods to under three years, while the Energy Efficient Home Improvement Credit reimburses up to USD 600 per opening. Andersen’s USD 420 million expansion in Goodyear, Arizona, doubled Fibrex capacity and reduced freight costs by 15%, improving service in western states. Canada’s Greener Homes Grant provides CAD 125-250 per opening, and Mexico’s housing recovery in the Bajío corridor is boosting composite adoption.

Asia-Pacific posts the fastest 5.21% CAGR through 2031, fueled by off-site fabrication. Modulex Global’s mega-factory near Mumbai produces up to 300,000 m² of unitized façades annually. China’s codes cap U-values at 1.5-2.0 W/m²·K, and its 14th Five-Year Plan targets 350 million m² of retrofits, driving demand for high-performance frames. Australia’s NCC 2022 and upcoming 2025 revisions tighten thermal thresholds, while Japan’s seismic replacement initiatives target pre-1981 structures. Early but notable traction is seen in Brazil, where housing recovery is underway, and Saudi Arabia, where giga-projects such as NEOM specify low-carbon composite curtain walls.

Competitive Landscape

The composite doors and windows industry remains moderately fragmented; the five largest firms include Andersen, JELD-WEN, Pella, Eurocell Plc, and Owens Corning. M&A momentum is reshaping the field: Masonite’s USD 3.0 billion purchase of PGT Innovations in 2024 created an impact-window platform with in-house extrusion, glass tempering, and installation services. Eurocell’s 2025 roll-up of four United Kingdom door brands broadens channel access during ECO4 grant acceleration.

Scale investments are prevalent. Andersen allocated USD 420 million to expand its Arizona plant, reducing logistics costs by 15% and increasing Fibrex extrusion capacity to record levels. Rehau opened new composite profile lines in Argentina, the United Kingdom, and France to mitigate tariff risks and localize supply chains. Technology represents a share-gain lever; Andersen’s augmented-reality installer app improved closing rates by 25%, and robotics increased extrusion yield by 8%.

Innovation focuses on FRP mullions and bio-composite formulations. Deceuninck’s Innergy AP commercial system offers a 900× thermal improvement over aluminum, while Rehau’s RAU-INFINIO integrates continuous glass fibers for structural integrity and full recyclability. Smaller specialists such as Plastpro in fiberglass entry doors and Safestyle in direct-to-consumer U.K. windows pursue tightly focused business models that avoid direct competition with diversified giants. Patent filings also signal commitment; Andersen holds more than 100 active Fibrex patents, and Rehau is extending RAU-INFINIO protection across Europe and North America. JELD-WEN’s 2025 10-K revealed USD 3.211 billion revenue but also USD 334.6 million goodwill impairment amid resin inflation and PFAS-free reformulation expenses.

Composite Doors And Windows Industry Leaders

JELD-WEN, Inc.

Pella Corporation

ANDERSEN CORPORATION

Eurocell Plc

Owens Corning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Marvin launched the Vivid Collection to address a specific industry need for enhanced design flexibility. To achieve this, Marvin developed a proprietary fiberglass-reinforced composite material exclusively for window interiors, enabling larger sizes and a cleaner, more streamlined aesthetic.

- March 2025: Eurocell PLC acquired Alunet Group, which added four composite door brands to its portfolio. This initiative enhanced its U.K. retrofit market coverage during the ECO4 subsidy expansion.

Global Composite Doors And Windows Market Report Scope

Composite doors and windows are constructed using multiple materials, typically featuring a timber core combined with GRP (Glass Reinforced Plastic), PVC, or laminate skins. These products are durable, low-maintenance, and thermally efficient. They provide high security, superior weather resistance, and reduced thermal transfer compared to standard alternatives, with a significantly longer lifespan than traditional wooden options.

The Composite Doors and Windows market is segmented into product type, material type, application, and geography. By product type, the market is segmented into composite doors and composite windows. By material type, the market is segmented into glass reinforced plastic (GRP), wood-plastic composite (WPC), fiber-reinforced polymer (FRP), and other material types (carbon, bio-composite). By application, the market is segmented into residential, commercial, and industrial/institutional. The report also covers the market size and forecasts for composite doors and windows in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Composite Doors |

| Composite Windows |

| Glass Reinforced Plastic (GRP) |

| Wood-Plastic Composite (WPC) |

| Fibre-Reinforced Polymer (FRP) |

| Other Material Types (Carbon, Bio-composite) |

| Residential |

| Commercial |

| Industrial/Institutional |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Composite Doors | |

| Composite Windows | ||

| By Material Type | Glass Reinforced Plastic (GRP) | |

| Wood-Plastic Composite (WPC) | ||

| Fibre-Reinforced Polymer (FRP) | ||

| Other Material Types (Carbon, Bio-composite) | ||

| By Application | Residential | |

| Commercial | ||

| Industrial/Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the composite doors and windows market?

The composite doors and windows market stands at USD 1.20 billion in 2026 and is forecast to reach USD 1.49 billion by 2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to expand at a 5.21% CAGR through 2031, the quickest of all regions, driven by modular façade factories and stricter energy codes.

What product type leads global sales in 2025?

Composite doors led with 54.11% of 2025 revenue, although composite windows are expanding more rapidly.

Why are GRP frames prevalent in North America?

GRP frames meet stringent impact ratings that qualify homeowners for 10–45% hurricane insurance discounts, shortening payback periods to under three years.

Page last updated on: