Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

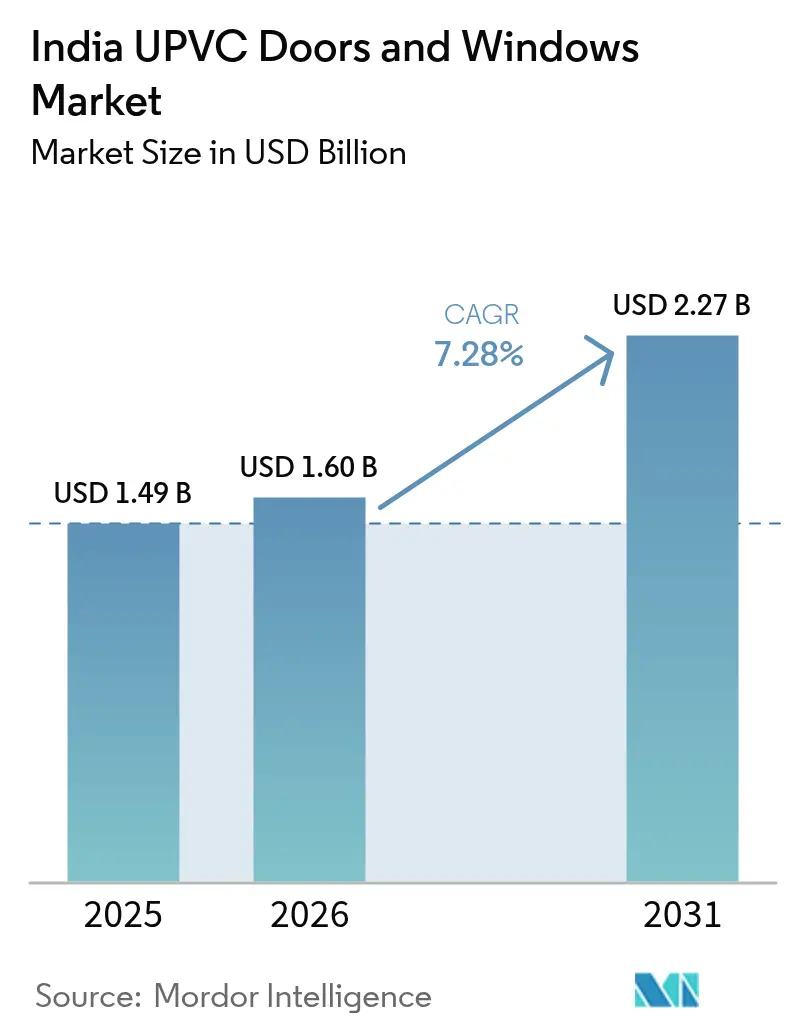

| Base Year Market Size (2025) | USD 1.49 Billion |

| Market Size (2026) | USD 1.6 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India UPVC Doors And Windows Market Analysis by Mordor Intelligence

The India UPVC windows and doors market size was valued at USD 1.49 billion in 2025 and estimated to grow from USD 1.6 billion in 2026 to reach USD 2.27 billion by 2031, at a CAGR of 7.28% during the forecast period (2026-2031). This trajectory aligns with India’s wider construction pipeline, which targets USD 1 trillion in value by 2030. Government programs such as the PM Surya Ghar Yojana, backed by INR 75,021 crore (USD 9,030 million), are unlocking large-scale retrofit demand for energy-efficient fenestration[1]Source: Press Information Bureau, “PM Surya Ghar Yojana Details,” pib.gov.in. Parallel support from Pradhan Mantri Awas Yojana-Urban 2.0 is propelling adoption into Tier-II and Tier-III cities. Growing consumer preference for low-maintenance products and impending domestic PVC capacity additions further reinforce the expansion outlook.

Key Report Takeaways

- By product type, UPVC windows led with 55.68% revenue share in 2025 for India UPVC Doors and Windows; UPVC doors are projected to grow at an 8.12% CAGR through 2031.

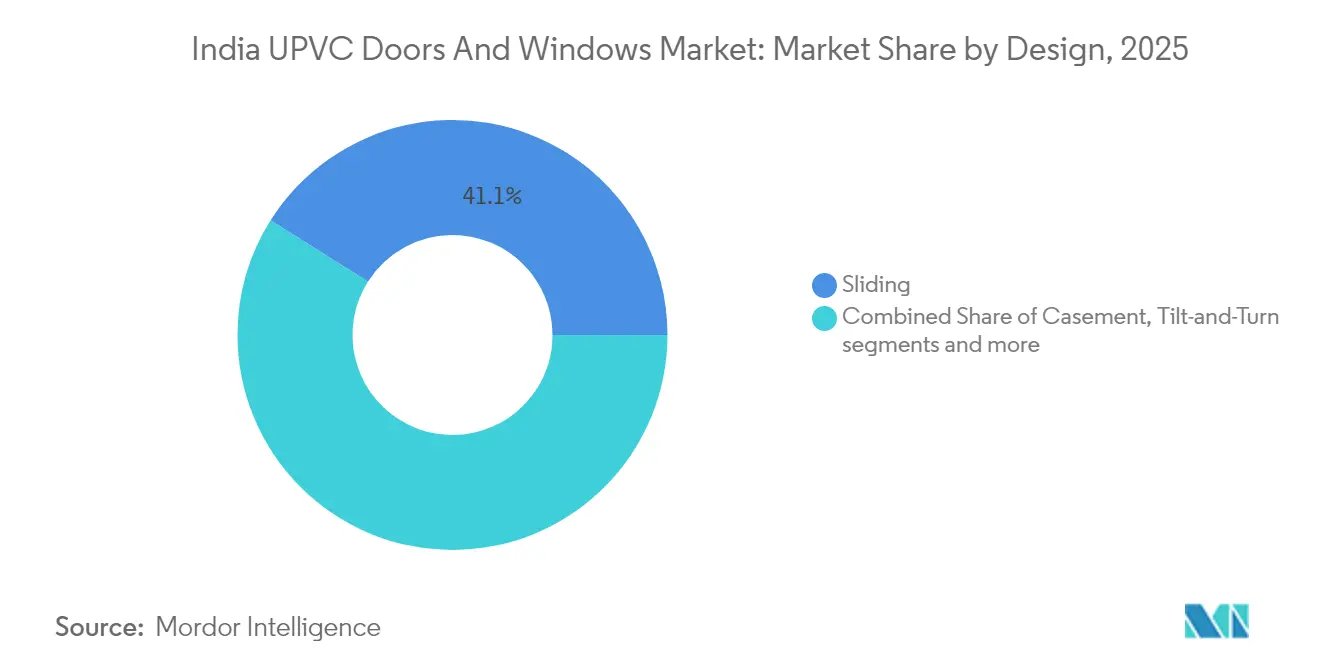

- By design type, sliding configurations accounted for 41.05% share in 2025, while tilt-and-turn systems are forecast to expand at a 7.62% CAGR to 2031.

- By installation type, new construction held 60.30% share in 2025; replacement & renovation is advancing at a 7.74% CAGR through 2031.

- By end-user, residential applications contributed 66.55% share of India UPVC Doors and Windows in 2025, whereas commercial is set to rise at an 8.57% CAGR through 2031.

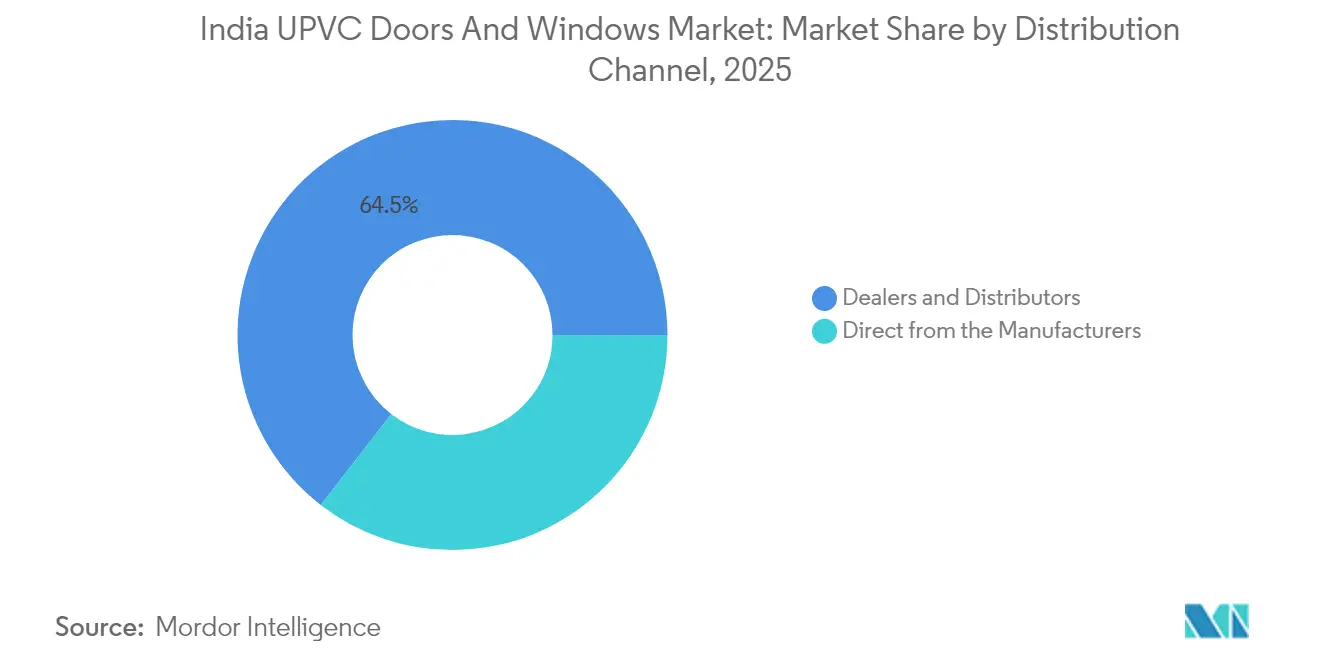

- By distribution channel, dealers and distributors captured 64.50% share in 2025 and are anticipated to register a 7.43% CAGR during 2026-2031.

- By region, South India represented 29.10% of 2025 revenue, while West India is expected to post the highest 8.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India UPVC Doors And Windows Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push for energy-efficient, green & affordable housing schemes | 1.8% | National, with early gains in metros and Tier-II cities | Medium term (2-4 years) |

| Rising consumer preference for low-maintenance fenestration in Tier-II & III cities | 1.5% | Tier-II & III cities across all states | Long term (≥ 4 years) |

| Accelerated real-estate renovations post-COVID unlocking retrofit demand | 1.2% | Urban centers and suburban developments | Short term (≤ 2 years) |

| Rapid expansion of organised retail showrooms & e-commerce configurators | 0.9% | National, concentrated in urban markets | Medium term (2-4 years) |

| Domestic PVC capacity additions (Reliance, Adani) reducing raw-material cost volatility | 0.8% | National manufacturing and supply chain | Long term (≥ 4 years) |

| Integration of smart-home sensors & IoT-ready locks into uPVC profiles | 0.6% | Metro cities and premium residential segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Push for Energy-Efficient, Green & Affordable Housing Schemes

Multiple federal initiatives, including PM Surya Ghar Yojana and Pradhan Mantri Awas Yojana-Urban 2.0, link housing subsidies with energy-efficient construction requirements that favor UPVC fenestration. The Energy Conservation Building Code 2017 update created voluntary tiers that reward 25%–50% energy savings, positioning UPVC profiles as a compliant solution[2]Source: Bureau of Energy Efficiency, “ECBC 2017 Update,” beeindia.gov.in. Upcoming Energy Conservation & Sustainable Building Code guidelines referenced in the Economic Survey 2024-25 further embed thermal-performance metrics in building approvals. These policy layers support India’s 2070 net-zero pledge, driving developers to specify high-insulation windows and doors. Consequently, the India UPVC windows and doors market receives a sustained boost from public-sector housing pipelines that extend well beyond metros.

Rising Consumer Preference for Low-Maintenance Fenestration in Tier-II & III Cities

Housing transactions in Tier-II and Tier-III cities expanded at 14% CAGR between 2021 and 2023, outpacing metro growth and creating new demand hubs for durable fenestration. Dual-income households in these cities prioritize products that minimize upkeep, and UPVC’s resistance to termites, corrosion and weathering aligns with that expectation. Coastal zones in Karnataka, Tamil Nadu, and Gujarat adopt UPVC quickly because salt-laden air accelerates the degradation of wood and basic aluminum alternatives. Organized retail showrooms, such as Fenesta’s 250-plus dealer network, improve product visibility and technical guidance for new buyers. These factors collectively expand the India UPVC windows and doors market into geographies that once relied almost entirely on lower-performance materials.

Accelerated Real-Estate Renovations Post-COVID Unlocking Retrofit Demand

Remote-work adoption reshaped home usage patterns and drove a significant rise in renovation spending, while also shortening the typical renovation cycle from long-term intervals to more frequent refreshes. Homeowners now prioritize energy efficiency, noise reduction, and indoor air quality, attributes where UPVC outperforms traditional frames. Luxury and premium residential projects, which led price appreciation in 2024, favor high-specification UPVC systems with multi-chamber profiles and advanced glazing. Real-estate sales totaling roughly 230,000 units in the first nine months of 2024 confirm steady demand for retrofit-friendly products. This renovation momentum broadens revenue for manufacturers beyond new-build channels within the India UPVC windows and doors market.

Rapid Expansion of Organised Retail Showrooms & E-Commerce Configurators

Fenestration purchase journeys are shifting toward omnichannel models where consumers research online and finalize in showrooms, elevating transparency and customization. Dealer footprints have grown sharply, and virtual configurators let buyers visualize styles, colors and hardware before committing. Smartphone penetration and digital payments accelerate this trend, especially among younger homeowners in emerging cities. Manufacturers leverage these platforms to upsell premium glazing and smart-lock options that lift average selling prices. The result is stronger brand differentiation and faster market penetration across varied income tiers within the India UPVC windows and doors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GST bracket (18%) versus 12% on aluminium & wood alternatives | -1.4% | National, affecting all market segments | Short term (≤ 2 years) |

| Persistent skilled-installer deficit causing quality-perception issues | -0.9% | National, more acute in Tier-II & III cities | Medium term (2-4 years) |

| Import dependence for premium hardware & multi-chamber profiles | -0.7% | National, concentrated in premium residential and commercial segments | Medium term (2-4 years) |

| Rising competition from thermally-broken aluminium systems in premium segment | -0.5% | Metro cities and high-end residential projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High GST Bracket (18%) Versus 12% on Aluminium & Wood Alternatives

PVC polymers classified under HSN 3904 attract 18% GST, while aluminum and wood frames fall into the 12% band, imposing a 6-percentage-point price handicap on UPVC products[3]Source: ClearTax, “GST Rates on Building Materials,” cleartax.in. The differential amplifies upfront cost gaps in price-sensitive segments, especially in Tier-II and Tier-III cities where awareness of lifecycle savings remains limited. Manufacturers respond with value-engineering and financing schemes that highlight energy-bill reductions over the product lifespan. Nonetheless, higher tax outlays constrain rapid adoption even when performance credentials are superior. Market participants anticipate that future GST rationalization could unlock faster growth for the India UPVC windows and doors market.

Persistent Skilled-Installer Deficit Causing Quality-Perception Issues

Roughly half of India’s PVC processing capacity sits underutilized due to shortages of trained technicians, demonstrating sector-wide skill gaps. Improper installation can degrade airtightness and water resistance, undermining performance advantages that differentiate UPVC from rivals. Companies such as VEKA India run multiday fabrication programs followed by on-site support, but the scale of these efforts trails market expansion. Absence of standardized vocational curricula keeps many installers reliant on informal apprenticeships that vary widely in quality. Limited skilled labor therefore restricts consumer confidence and slows penetration across the India UPVC windows and doors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Windows Drive Volume, Doors Accelerate Growth

UPVC windows captured 55.68% of the India UPVC windows and doors market share in 2025, reflecting their role as the primary entry point for energy-efficient fenestration. The segment benefits from higher replacement frequency and direct alignment with policy-linked thermal-performance goals that award green-building credits. Premium product lines now feature multi-chamber profiles and laminated finishes that meet evolving aesthetic expectations in metros and Tier-II cities alike. Manufacturers also localize resin compounds for UV resistance, ensuring structural integrity under intense Indian sunlight[4]. Together, these factors keep windows the largest revenue contributor within the India uPVC windows and doors market.

UPVC doors represent the fastest-growing product segment, advancing at an 8.12% CAGR for 2026-2031 and steadily raising their contribution to the India UPVC windows and doors market size. Increased awareness of multi-point locking and steel-reinforced frames boosts adoption in premium and mid-market housing, where security is a key purchase criterion. Longer door replacement cycles reduce price sensitivity, enabling upselling of designer infill panels and electronic access controls. Product launches featuring aluminium-look foils and cool-color technology further expand appeal to architects who prefer metallic aesthetics without thermal penalties. As a result, doors are expected to narrow the historical volume gap with windows by 2030.

By End-Use Sector: Residential Dominance, Commercial Acceleration

The residential segment held 66.55% of the India UPVC windows and doors market in 2025, supported by federally subsidized housing pipelines and rising disposable incomes among first-time homeowners. Government grants that mandate innovative green materials steer low-income buyers toward UPVC, bolstering demand in both metros and emerging cities. Developers highlight reduced maintenance and energy savings to justify UPVC premiums in mid-income projects where lifecycle costs influence purchasing decisions. Rapid urbanization and a younger demographic further shorten renovation cycles, sustaining repeat demand even in saturated localities. Consequently, residential construction anchors baseline volume for the India UPVC windows and doors market.

Commercial applications are projected to rise at an 8.57% CAGR through 2031, making them the quickest revenue driver in the India uPVC windows and doors market size. Bureau of Energy Efficiency star-rating protocols influence architects to specify UPVC profiles with low U-values to earn compliance points and tenant leasing premiums. Developers also favor UPVC for acoustic insulation, a growing concern in high-density business districts. As multinational firms expand satellite offices in Tier-II hubs, specification norms established in metros replicate nationwide. This momentum positions commercial builds as the fastest contributor to incremental revenue through 2030.

By Design Type: Sliding Leads, Tilt-and-Turn Emerges

Sliding formats retained a 41.05% share in 2025 because their compact operating footprint suits India’s space-constrained apartments. Simple hardware architecture keeps unit prices competitive, enhancing suitability for affordable housing schemes that aim to maximize value per square foot. Manufacturers now offer larger-panel sliders with reinforced rollers that meet higher wind-load standards in coastal states. Enhanced mosquito-screen integrations and smooth-track innovations further improve user experience and after-sales perception. These refinements cement sliding units as volume leaders within the India UPVC windows and doors market.

Tilt-and-turn systems are forecast to expand at a 7.62% CAGR, translating European ventilation versatility into premium Indian projects. The dual-action hardware lets occupants pivot sash orientation for breeze control and easy exterior cleaning, appealing to high-rise dwellers concerned about safety. Increased marketing by German and Belgian profile suppliers highlights multipoint seals that boost thermal ratings, justifying higher prices. Availability of custom color laminates and minimalist handle sets aligns with contemporary interior trends favored by architects. Momentum in luxury and smart-home projects will gradually lift the segment’s contribution to overall industry revenue.

By Installation Type: New Construction Stable, Renovation Accelerates

New-build projects accounted for 60.30% of demand in 2025, anchored by robust housing completions under PMAY-U 2.0 and ongoing commercial tower pipelines. Developers leverage bulk procurement to lock in favorable UPVC pricing, absorbing GST differentials through scale efficiencies. Large parcel developments in the Mumbai-Pune and Delhi-NCR corridors adopt factory-finished frames to compress site timelines and assure quality. Central approvals increasingly include green-building clauses, ensuring that UPVC remains a specification standard for energy-code compliance. This consistent baseline shields the India UPVC windows and doors market from short-term construction volatility.

Replacement and renovation demand is growing at a 7.74% CAGR, adding higher-margin opportunities to the India UPVC windows and doors market size. Post-pandemic homeowners upgrade to double-glazed units and laminated doors that improve comfort during work-from-home routines. The PM Surya Ghar program creates bundled retrofits where solar roofs pair with better insulated fenestration to maximize energy gains. Specialty installers now market modular replacement kits that limit wall disturbance, reducing perceived hassle for occupants. This channel generates premium average selling prices, lifting profitability for manufacturers and dealers alike.

By Distribution Channel: Dealers and Distributors Dominate, Omnichannel Gains

Dealers and distributors accounted for 64.50% of India UPVC windows and doors market share in 2025, underscoring their role as the primary route-to-market across metros and smaller cities. Their extensive showroom networks provide tactile product demonstrations that digital platforms cannot fully replicate. Credit facilities and localized inventory help smaller contractors meet quick-turn project timelines, maintaining channel relevance. Dealer exclusivity agreements also support consistent pricing and after-sales service quality. These strengths secure the channel’s leadership in the India UPVC windows and doors market.

Despite high penetration, the dealer-distributor channel is still forecast to grow at a 7.43% CAGR between 2026 and 2031, keeping pace with overall industry expansion. Manufacturers partner with dealers to introduce virtual configurators that blend online visualization with in-store confirmation, enhancing customer engagement. Loyalty programs for architects and installers encourage repeat specification of branded profiles, increasing throughput per outlet. Training modules delivered via augmented reality further professionalize showroom staff, differentiating the channel from smaller informal retailers. As a result, omnichannel-ready dealers will remain critical gatekeepers for future volume.

Geography Analysis

South India contributed 29.10% of 2025 revenue, making it the largest regional slice of the India UPVC windows and doors market share. Southern states like Karnataka and Tamil Nadu exhibit double-digit growth rates as Bengaluru’s tech expansion and Chennai’s industrial parks spur both residential and commercial building demand. Air-conditioned offices and data centers prioritize low U-value fenestration to curb cooling loads, raising adoption of triple-seal UPVC assemblies. Local fabrication units in Chennai and Hyderabad cut lead times, enabling project managers to align with tight construction schedules. In parallel, Kerala’s coastal belt shows rising retrofits driven by salt-spray corrosion issues afflicting aluminum frames. These patterns highlight climate-specific drivers that diversify regional growth levers.

West India is projected to register the fastest 8.29% CAGR from 2026 to 2031, outpacing all other regions in expanding the India UPVC windows and doors market size. Maharashtra commands the largest share of the India UPVC windows and doors market, supported by dense construction activity along the Mumbai–Pune corridor and well-established plastics clusters near Mumbai Port. The state’s humid coastal climate accelerates wood decay, prompting builders to specify UPVC for moisture resistance and energy efficiency. Gujarat follows closely owing to feedstock access and extrusion hubs such as Vadodara, where multiple multinational profile suppliers operate plants. Port infrastructure at Kandla streamlines resin and hardware imports, cementing the region as a distribution gateway to western and northern India. These fundamentals collectively generate high baseline volume and technical expertise.

Tier-II and Tier-III cities across Uttar Pradesh, Rajasthan and Madhya Pradesh now account for more than 40% of new housing launches, surpassing metros on unit counts. Organized retail penetration brings UPVC showrooms to cities like Indore, Jaipur and Lucknow, extending technical advisory services to first-time buyers. Skill shortages present a challenge, but industry associations collaborate with ITIs to roll out fabrication-installer courses that improve service quality. Government road and rail investments enhance logistics networks, reducing freight costs and delivery times for bulky frames. As awareness builds, these emerging markets will provide the steepest growth trajectory through 2030.

Competitive Landscape

The India UPVC windows and doors market remains moderately fragmented, with the top five players holding major market share in 2024. International brands such as Fenesta, VEKA India, Rehau, and Deceuninck leverage global R&D to position premium, high-specification systems that command higher margins. Domestic challengers like Encraft and Prominance compete on localized product formulations, quicker after-sales response, and price flexibility. Capacity expansion is underway, with Fenesta operating seven ISO-certified factories and exceeding 4 million window installations to date. Such vertical integration strengthens end-to-end quality control.

Strategic differentiation increasingly centers on technology adoption, including in-house testing rigs for wind, water and air infiltration comparable to EN-standard benchmarks. Manufacturers also emphasize installer-training academies that certify fabricators and site crews, mitigating industry-wide skill shortages. Smart-home partnerships are emerging, exemplified by tie-ups with IoT lock providers that integrate seamlessly into multi-chamber frames. Domestic resin plants from Adani and Reliance promise stable feedstock, enabling suppliers to hedge against currency-induced price swings. Combined, these moves sharpen competitive edges without triggering a price-only race to the bottom.

M&A remains limited, but joint-venture extrusion facilities have surfaced around Gujarat and Telangana to capture regional demand and shorten delivery cycles. Marketing budgets now prioritize digital configurators that allow virtual walk-throughs of color and hardware choices, enhancing customer engagement in both metros and smaller towns. Loyalty programs for architects incentivize repeat specification, building brand stickiness at the design stage. Suppliers also explore recycled-PVC lines to align with ESG mandates from institutional investors funding real-estate projects. Collectively, these strategies suggest competition will pivot toward service and innovation rather than scale alone.

India UPVC Doors And Windows Industry Leaders

Fenesta Building Systems

VEKA / NCL VEKA

Aparna Venster

Encraft India

Prominance Window Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SBM Gold Announces Expansion Into uPVC Doors and Windows, Reinforces Market Leadership in Building Solutions

- July 2024: Adani Group resumed construction of its USD 4 billion PVC plant at Mundra, Gujarat, targeting 2 million TPA capacity with phase-one completion by December 2026, the largest single PVC investment in India.

- April 2024: Epigral Ltd commissioned an additional 45,000 TPA CPVC resin line at Dahej, Gujarat, raising total capacity to 75,000 TPA and supporting downstream building-material producers.

India UPVC Doors And Windows Market Report Scope

UPVC, also referred to as unplasticized polyvinyl chloride, is low maintenance and cost-effective material used in building and construction, especially in pipework and window frames. A complete background analysis of the Indian UPVC doors and windows market, which includes an assessment of the UPVC doors and windows market in India, emerging trends by segments and regional markets, and significant changes in market dynamics and market overview, is covered in the report. The report also features qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across key points in the industry's value chain. The Indian UPVC doors and windows market is segmented by product type (UPVC doors and UPVC windows), end user (residential, commercial, industrial and construction, and other end users), and distribution channel (offline stores and online stores).

By Product Type

| UPVC Windows |

| UPVC Doors |

By Design Type

| Sliding |

| Casement |

| Tilt-and-Turn |

| Others (French, Awning, etc.) |

By Installation Type

| New Construction |

| Replacement & Renovation |

By End-user

| Residential |

| Commercial |

| Industrial & Infrastructure |

By Distribution Channel

| Direct from the Manufacturers |

| Dealers and Distributors |

By Region

| North |

| West |

| South |

| East |

| By Product Type | UPVC Windows |

| UPVC Doors | |

| By Design Type | Sliding |

| Casement | |

| Tilt-and-Turn | |

| Others (French, Awning, etc.) | |

| By Installation Type | New Construction |

| Replacement & Renovation | |

| By End-user | Residential |

| Commercial | |

| Industrial & Infrastructure | |

| By Distribution Channel | Direct from the Manufacturers |

| Dealers and Distributors | |

| By Region | North |

| West | |

| South | |

| East |

Key Questions Answered in the Report

What is the 2026 size of the India UPVC windows and doors market?

It stands at USD 1.6 billion in 2026.

How much growth is projected through 2031 for India’s uPVC windows and doors suppliers?

Revenue is forecast to reach USD 2.27 billion by 2031, reflecting a 7.28% CAGR during 2026-2031.

Which product type currently generates the most revenue in India’s uPVC fenestration space?

UPVC windows lead with 55.68% share of 2025 sales.

Which regional cluster shows the highest consumption of UPVC windows and doors in India?

South India contributes 29.10% of national revenue, the largest regional slice as of 2025.

Which sales channel handles the majority of transactions for UPVC windows and doors in India?

Pradhan Mantri Awas Yojana-Urban 2.0 links subsidies to innovative, green building materials.

Page last updated on: