United Kingdom Homeware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 40.25 Billion |

| Market Size (2026) | USD 41.73 Billion |

| Market Size (2031) | USD 51.19 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

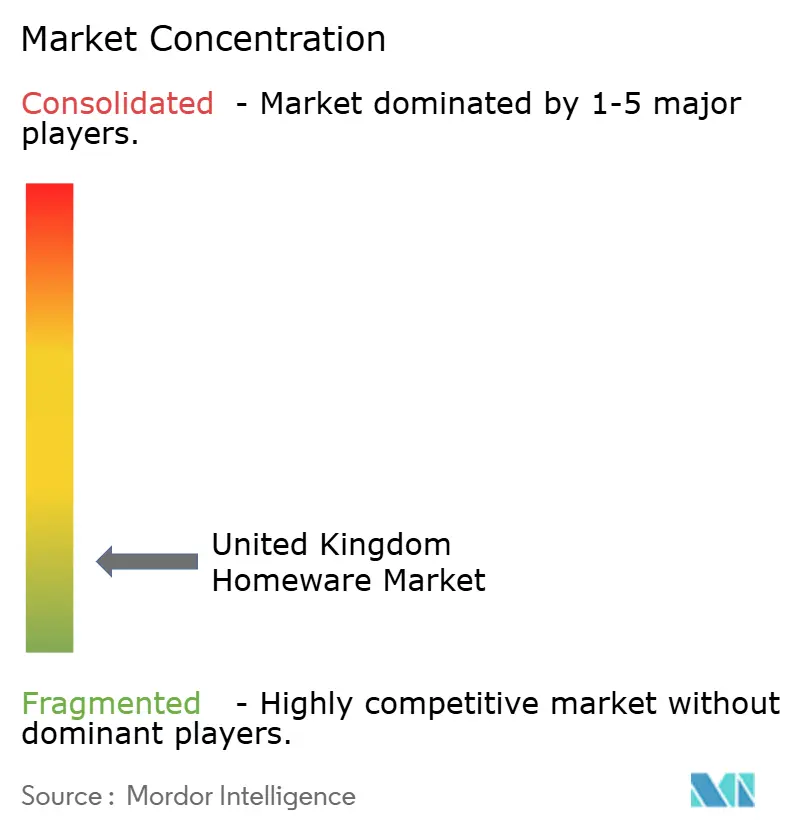

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Homeware Market Analysis by Mordor Intelligence

The United Kingdom homeware market size is expected to grow from USD 40.25 billion in 2025 to USD 41.73 billion in 2026 and is forecast to reach USD 51.19 billion by 2031, reflecting a 4.17% CAGR over 2026-2031. This growth profile aligns with a steady pivot toward hybrid living, a refurbishment cycle tied to an ageing housing stock, and regulatory pressure from extended producer responsibility, which is tightening packaging standards and future end-of-life rules for household goods. Inflation eased into late 2025, helping stabilize planning and replenishment, yet price sensitivity remains evident in big-ticket categories as real incomes normalize following prior shocks. Industry leaders protect margin through vertical integration, targeted SKU expansion, and data-driven operations, including investments in factory capacity, livestock visibility, share buybacks, and AI-assisted delivery scheduling. A shifting trade backdrop also matters, as goods exports to the EU remain below pre-2019 levels in real terms, channeling effort toward domestic market share capture and supply diversification.

Key Report Takeaways

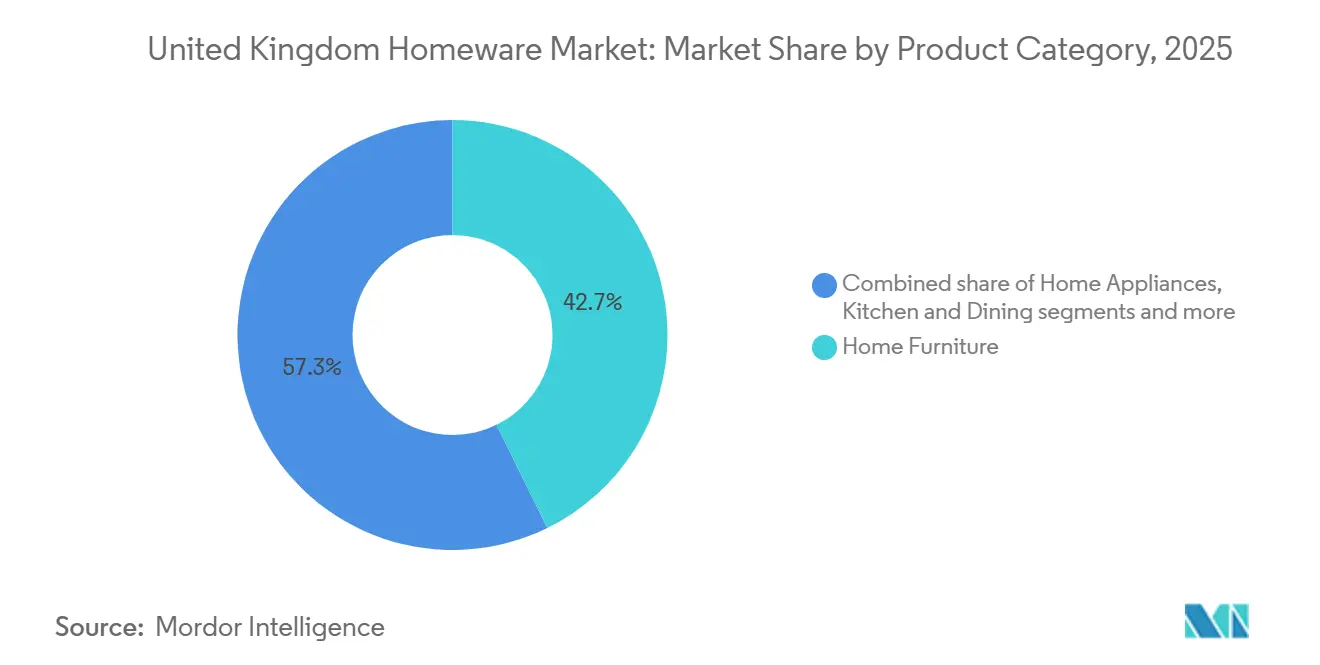

- By product category, home furniture led with 42.73% of the United Kingdom homeware market share in 2025, while home fragrance & candles is forecast to expand at a 5.84% CAGR to 2031.

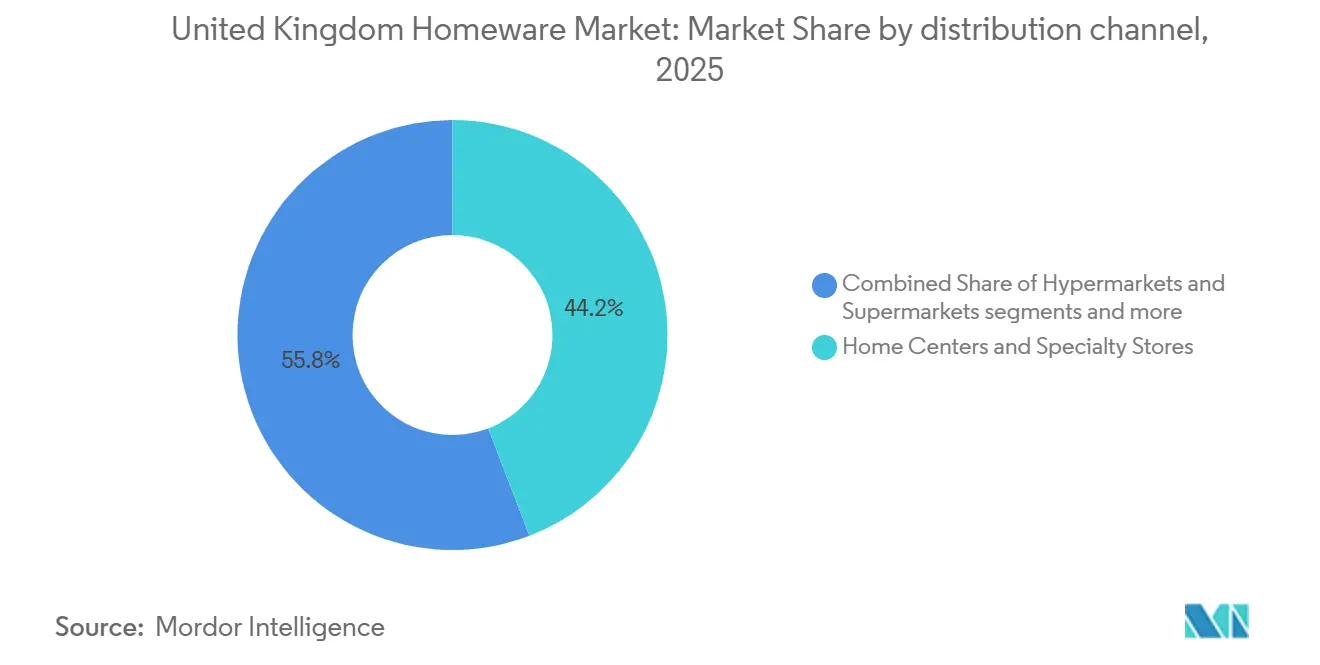

- By distribution channel, home centers and specialty stores accounted for 44.18% of the United Kingdom homeware market share in 2025, while the online channel recorded the highest projected CAGR at 6.39% through 2031.

- By geography, England accounted for 49.44% of the United Kingdom's homeware market in 2025 and is projected to grow at a 4.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Homeware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Penetration and Channel Shift | + 1.2% | Global, led by England's metro areas | Short term (≤ 2 years) |

| Home-Renovation Boom from Hybrid Working & Housing Turnover | + 1.3% | England, Scotland (ageing housing stock) | Medium term (2-4 years) |

| Sustainability and Circular Economy Demand Shaping Purchasing | + 0.5% | National, concentrated in London, the South East | Long term (≥ 4 years) |

| Multifunctional/Space-Saving Furniture for Urban Living | + 0.9% | London, Birmingham, Manchester urban cores | Medium term (2-4 years) |

| AI-driven Personalization Lifting Basket Size & Retention | + 0.6% | National, with the highest adoption in England | Short term (≤ 2 years) |

| Residential Micro-Unit Conversions are Boosting the Furnishing Need | + 0.4% | London, Greater South East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Penetration and Channel Shift

The United Kingdom homeware market continues to migrate online as retailers invest in visual tools, stock transparency, and faster fulfillment to reduce friction in complex categories such as cabinets, sofas, and appliances. Digital execution is now central to growth since omnichannel operators that tie together data hubs, delivery optimization, and curated merchandising convert browsing into orders more efficiently than static storefronts. DFS reported higher-order intake in FY2025, supported by AI-enhanced marketing and machine-learning route scheduling, demonstrating how analytics-led logistics can improve conversion and on-time delivery at scale[1]London Stock Exchange, “DFS Furniture plc: FY25 Preliminary Results,” London Stock Exchange, londonstockexchange.com. Trade-focused networks are also blending proximity with digital visibility, as shown by Howdens’ Live-Stock rollout and Click & Collect services that extend choice without losing depot speed advantages. Post-Brexit trade frictions shifted more inventory focus to domestic channels, reinforcing the digital shift by increasing online assortment depth that might otherwise have been reserved for export flows[2]UK Parliament POST, “The Circular Economy and Sustainable Manufacturing,” UK Parliament, post.parliament.uk. As channel economics rebalance, the United Kingdom homeware market rewards operators that link real-time inventory with targeted recommendations and time-definite delivery promises, thereby reducing abandonment and increasing repeat purchase rates.

Home-Renovation Boom from Hybrid Working and Housing Turnover

Hybrid work has reshaped room planning and pushed more households to convert existing spaces into work zones, supporting steady demand for desks, storage, task lighting, modular seating, and fitted cabinetry in the United Kingdom homeware market. Evidence from European housing research shows that remote workers are more likely to move and adjust their dwelling choices, triggering repeat furnishing cycles during and after relocation. Professional-led renovations and trade specialist involvement remain important, as cabinet design, material selection, and installation quality drive outcomes that generalists struggle to match. England’s higher housing turnover and retail density reinforce this upgrade loop by shortening the path from inspiration to installation for fitted and freestanding projects. When households postpone major moves, they still refresh décor and textiles between cycles, keeping baskets active across seasons even as mortgage rates slow transactions. Together, these behaviors extend a multi-year refurbishment runway for the United Kingdom homeware market as homeowners optimize comfort, productivity, and energy performance within existing footprints.

Sustainability and Circular-Economy Demand Shaping Purchasing

Extended Producer Responsibility for packaging took effect in 2024 for qualifying businesses, which embeds reporting and fee structures that influence packaging selection, recyclability, and upstream supplier choices in homeware categories. The Furniture and Furnishings Fire Safety Amendment, effective October 30, 2025, tightened labeling and record-keeping for remaining in-scope items, which raises compliance requirements for multi-SKU assortments and encourages clearer product documentation. United Kingdom policy bodies outline a broader shift toward circular manufacturing, steering investment toward take-back, repair, and recycled inputs that align with buyer preferences for durability and traceability. Industry surveys indicate that most furniture firms plan sustainability investments over the next five years, signaling expansion of reverse logistics, refurbishment programs, and materials stewardship across leading retail propositions. Major retailers now highlight recycled content and modular designs that extend product lifecycles, which appeals to value- and eco-conscious households seeking to reduce waste without sacrificing function or style. As these standards mature, the United Kingdom homeware Market sees brand preference tilt toward credible circular claims supported by transparent processes and accessible aftercare services.

Multifunctional and Space-Saving Furniture for Urban Living

Space constraints in major cities and the normalization of hybrid work push demand for modular, foldable, and convertible furniture that unlocks storage and workspace within existing rooms in the United Kingdom homeware market. Product development increasingly favors formats that reconfigure quickly and pair with vertical storage, which allows households to switch between work, leisure, and hosting without adding square footage. Builders and trade depots have expanded ranges and components that fit small footprints while maintaining premium finishes, durable surfaces, and installation quality across kitchens and living areas. With input costs still relevant to pricing and value perception, households evaluate multi-use pieces on total lifetime durability and warranty support, which sustains interest in quality engineering and dependable materials. Retail displays and online configuration tools that visualize small-room layouts lower purchase risk and increase basket size, thereby accelerating the adoption of multifunctional, space-saving lines. Over the forecast period, these solutions capture a growing share of furniture refresh projects in the United Kingdom homeware market as households prioritize flexibility, comfort, and efficient storage in compact floor plans.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Led Squeeze on Discretionary Spending | -0.80% | National, sharper in Wales, Northern Ireland | Short term (≤ 2 years) |

| Volatile Raw-Material & Freight Costs Pressuring Margins | -0.60% | National, concentrated impact on SME importers | Medium term (2-4 years) |

| Post-Brexit Customs Frictions Hitting SME Import Flows | -0.40% | National, acute for EU-facing SMEs | Long term (≥ 4 years) |

| Tougher Reverse-Logistics & Disposal Rules Raising Costs | -0.30% | National, front-loaded in England, Wales | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Led Squeeze on Discretionary Spending

Inflation peaked in 2022 and eased into late 2025, improving planning visibility but not immediately restoring all discretionary categories to prior momentum. The CPI index showed annual inflation at 3.4% in December 2025, a level that still demanded careful pricing and promotion management for big-ticket homeware purchases. In this setting, the United Kingdom homeware market sees a split between value-driven essentials and well-targeted premium propositions where brand equity or innovation supports price realization. Appliance leaders continue to launch new features and designs to defend share through performance, which reduces direct price exposure while keeping upgrade cycles active. For retailers, a disciplined markdown strategy and bundling help maintain gross margin while aligning with consumer expectations as purchasing power resets across cohorts. The net effect is a gradual normalization path where promotions, financing, and product storytelling shape basket size more than simple list-price changes in the United Kingdom homeware market.

Volatile Raw-Material & Freight Costs Pressuring Margins

Input volatility continues to shape pricing and assortment decisions, with producer price data showing wood-product input costs up 3.3% year-on-year in January 2026, while furniture output prices rose 1.8% over the same period. That gap tightens headroom for pass-through and encourages SKU rationalization, as duplication or low-velocity variants depress margins. Vertical integration buffers some of this pressure by moving more value-add in-house, as seen in Howdens’ internal production of end panels and frontals alongside a higher FY2024 gross margin of 61.6%. Operational savings also accrue when delivery networks are optimized, and waste is reduced, which is one reason DFS exceeded its multi-year cost-savings target ahead of schedule in FY2025. For non-integrated players, vendor consolidation and evergreen assortments can protect margin without eroding choice, though execution depends on dependable logistics and accurate demand planning in the United Kingdom homeware market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Home Furniture Commands, Fragrance Races Ahead

Home furniture captured 42.73% of the United Kingdom homeware market share in 2026, reflecting the scale of replacement and upgrade projects across living, bedroom, and workspace zones. The category remains a core basket driver because modular seating, storage, and cabinetry support evolving multiuse floor plans tied to hybrid working and family routines. Home textiles and soft furnishings extend refresh cycles between major purchases, while décor and lighting accentuate function-led reconfigurations that increase dwell time in renovated rooms. Circularity also comes into play as repair, reupholstery, and resale options gain prominence within brand and retailer propositions, helping defend premium positioning on quality. In appliances, innovation waves around air, cleaning, and compact storage create periodic step-change demand that sustains the higher-ticket end of the United Kingdom homeware market.

Home fragrance & candles is the fastest-growing product group with a 5.84% CAGR for 2026-2031, supported by wellness gifting and low-barrier refreshes that align with seasonal décor. Portmeirion’s Wax Lyrical business posted strong growth and returned to profitability in FY2024, demonstrating how a portfolio mix and channel reach can unlock scale even in discretionary categories. The textiles and soft furnishings lane continues to adapt to regulatory expectations as EPR frameworks mature in the United Kingdom, a factor that is driving clearer labeling, improved recyclability, and take-back experimentation. Premium small appliances benefit from ongoing R&D investment that widens differentiation with each product cycle, as seen in Dyson’s pipeline and engineering footprint expansion. Collectively, these product trends anchor the United Kingdom homeware industry to a balanced growth mix that combines core furniture demand with higher-velocity accessory and appliance refreshes.

By Distribution Channel: Specialists Hold Share, Online Accelerates

Home centers and specialty stores accounted for 44.18% of 2026 sales, reflecting the continued importance of hands-on design support, project planning, and installation coordination in complex home categories. Specialist networks strengthened coverage through new depot openings and digital tools that improve product availability and pickup options, keeping these formats resilient as shoppers mix online research with in-person verification. General merchandise formats remain relevant for staples and seasonal rotations, yet deep category curation favors specialists that can field trained advisors and complete-room solutions. As price sensitivity persists across parts of the category spectrum, omnichannel specialists who align financing options, delivery windows, and post-purchase service see higher retention and lower return costs.

The United Kingdom homeware market size for the online channel is projected to expand at a 6.39% CAGR through 2031, supported by richer product visualization, better returns workflows, and route-optimized delivery. Operators that ingest data across marketing, inventory, and delivery improve recommendation accuracy and reduce late or failed deliveries, thereby increasing conversion rates. Even trade-facing models now combine depot proximity with live stock status and click-and-collect convenience, which underscores the omnichannel baseline for growth. Online selection depth also benefits from reshoring and import recalibration, which keep more inventory focused on domestic demand as customs processes evolve. Taken together, the United Kingdom homeware industry now treats the digital storefront as a primary sales engine rather than a supplemental catalog.

Geography Analysis

England remains the center of gravity for the United Kingdom's homeware market, accounting for 49.44% of the 2025 value and growing at a 4.76% CAGR through 2031, driven by higher retail density, faster delivery networks, and broader specialist coverage. The combination of large catchment areas, active renovation cycles, and better execution of click-and-collect keeps conversion rates healthier in England across both project-led and accessory-driven baskets. London and major cities also benefit from deeper digital engagement that supports richer merchandising experiences and route-optimized deliveries, which pull forward purchases that might otherwise wait for in-store confirmation.

Scotland sees steady demand for fitted furniture, textiles, and décor as households upgrade energy use and optimize layouts for work and leisure, yet delivery costs per drop can be higher due to the geographic spread. Retailers tackle this by concentrating showrooms and depots around population centers while using online tools to extend the long tail of assortments beyond floor space. Returns and installation scheduling also shape satisfaction in regional markets, which is why operators invest in better slotting and capacity planning to protect NPS and repeat rates. Sustainability expectations continue to rise and inform brand selection, which explains the growing interest in longevity, repair options, and credible circular claims across product types in the United Kingdom homeware market.

Wales and Northern Ireland exhibit selective growth that depends on store coverage, cross-border rules, and freight flows. The evolving customs framework matters for operators that source through the Republic of Ireland or ship finished goods to and from the EU, which adds planning steps and documentation to everyday replenishment. In these areas, omnichannel approaches that rely on regional pickup and scheduled deliveries can balance choice and cost, while compliance with safety and labeling regulations remains a constant operational requirement. As coverage improves, the United Kingdom homeware market benefits from more even access to curated assortments across the devolved nations, opening the door to growth in accessories, small appliances, and space-efficient furniture.

Competitive Landscape

The United Kingdom homeware market remains moderately fragmented, featuring a mix of vertically integrated leaders, omnichannel specialists, and focused direct brands. Howdens illustrates the advantages of integration by manufacturing more components in-house and by deploying live inventory and click-and-collect capabilities that lift service and margin together[3]Howden Joinery Group PLC, “Media Centre Archive: February 27, 2025,” Howden Joinery Group PLC, howdenjoinerygroupplc.com. DFS highlights the role of data harmonization and AI-enabled logistics in raising order intake and optimizing capacity across the network in FY2025. In appliances, Dyson underscores the importance of R&D investment and IP development in sustaining differentiation, with multi-country engineering footprints and a pipeline of product introductions.

Leaders use selective partnerships and brand-building to protect pricing when input costs rise faster than consumer tolerance for price increases[4]Office for National Statistics, “Producer Price Inflation, UK: January 2026,” Office for National Statistics, ons.gov.uk. Investment in omnichannel mechanics is now standard since time-definite delivery and clearer returns reduce risk for shoppers in complex categories like sofas, cabinets, and premium small appliances. Integrated sustainability programs also create commercial moats as EPR requirements and safety rules add reporting and traceability costs that are easier to absorb at scale.

White space continues to open in circular propositions as brands invest in packaging improvements, repair services, and materials stewardship to enhance retention across multiple purchase cycles. Portfolio balance is another differentiator because businesses that anchor in core furniture demand and augment with high-velocity accessories and fragrances tend to smooth revenue across seasons. The result is a field where execution discipline around network design, supplier resilience, and product development cadence can matter as much as price in defining share gains within the United Kingdom homeware market.

United Kingdom Homeware Industry Leaders

DFS Furniture plc

Dyson Ltd.

Dreams Ltd.

Silentnight Group

Portmeirion Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dreams Ltd completed the purchase of its High Wycombe 'Bedquarters' office building, consolidating operational headquarters and signaling a long-term commitment to UK manufacturing.

- April 2025: Matalan announced a USD 33 million investment in United Kingdom stores for 2025-2026, refurbishing 30 existing outlets, launching 10 new or relocated stores (in London, Essex, Hampshire, Northern Ireland), installing self-service checkouts and digital capabilities, and securing funding to expedite its transformation plan.

- October 2024: Dreams Ltd launched its first premium concept store, designed for smaller high-street locations, expanding its reach into urban centers where traditional superstore formats are unviable.

United Kingdom Homeware Market Report Scope

The UK homeware market is segmented by product (home furniture, home textiles, home appliances, floor covering products, home décor products, and other products (lighting, bathroom accessories, tableware, etc.)) and by distribution channel (supermarkets and hypermarkets, specialty stores, online distribution channels, and other distribution channels).

The report offers market size and forecasts for the UK homeware market value in value (USD billion) for all the above segments.

| Home Furniture | Living Room and Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Other Home Furniture | |

| Home Textiles | Bed Linen |

| Bath Linen | |

| Kitchen Linen | |

| Upholstery and Curtains | |

| Other Home Textiles | |

| Kitchen & Dining | Cookware |

| Dinnerware | |

| Others | |

| Home Décor & Accessories | Vases |

| Frames | |

| Decorative Lighting | |

| Wall Décor | |

| Others | |

| Home Fragrance & Candles | |

| Home Appliances | |

| Other Products (bathroom accessories, garden décor, etc.) |

| Hypermarkets and Supermarkets |

| Home Centers and Specialty Stores |

| Online |

| Other Distribution Channels |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product Category | Home Furniture | Living Room and Dining Room Furniture |

| Bedroom Furniture | ||

| Kitchen Furniture | ||

| Home Office Furniture | ||

| Other Home Furniture | ||

| Home Textiles | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery and Curtains | ||

| Other Home Textiles | ||

| Kitchen & Dining | Cookware | |

| Dinnerware | ||

| Others | ||

| Home Décor & Accessories | Vases | |

| Frames | ||

| Decorative Lighting | ||

| Wall Décor | ||

| Others | ||

| Home Fragrance & Candles | ||

| Home Appliances | ||

| Other Products (bathroom accessories, garden décor, etc.) | ||

| By Distribution Channel | Hypermarkets and Supermarkets | |

| Home Centers and Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the United Kingdom homeware market size and growth outlook to 2031

United Kingdom homeware market size is USD 41.73 billion in 2026 and is forecast to reach USD 51.19 billion by 2031 at a 4.17% CAGR.

Which product categories are leading and which are growing fastest in the United Kingdom homeware space ?

Home furniture leads with 42.73% share in 2025, while home fragrance & candles is the fastest-growing segment with a 5.84% CAGR for 2026-2031.

How is the online channel performing within the United Kingdom Homeware Market?

The online channel is projected to grow at a 6.39% CAGR through 2031, supported by better visualization, returns processes, and delivery optimization.

What regulatory factors are most influential for United Kingdom homeware operators in 2026?

Extended Producer Responsibility requirements for packaging and updated furniture fire-safety labeling rules shape reporting, design, and reverse logistics planning.

Which strategic moves by leading companies signal how competition is evolving?

Howdens expanded in-house manufacturing and live stock visibility, DFS scaled a data hub and AI-led route planning, and Dyson invested in R&D and new product categories.

Page last updated on: