Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

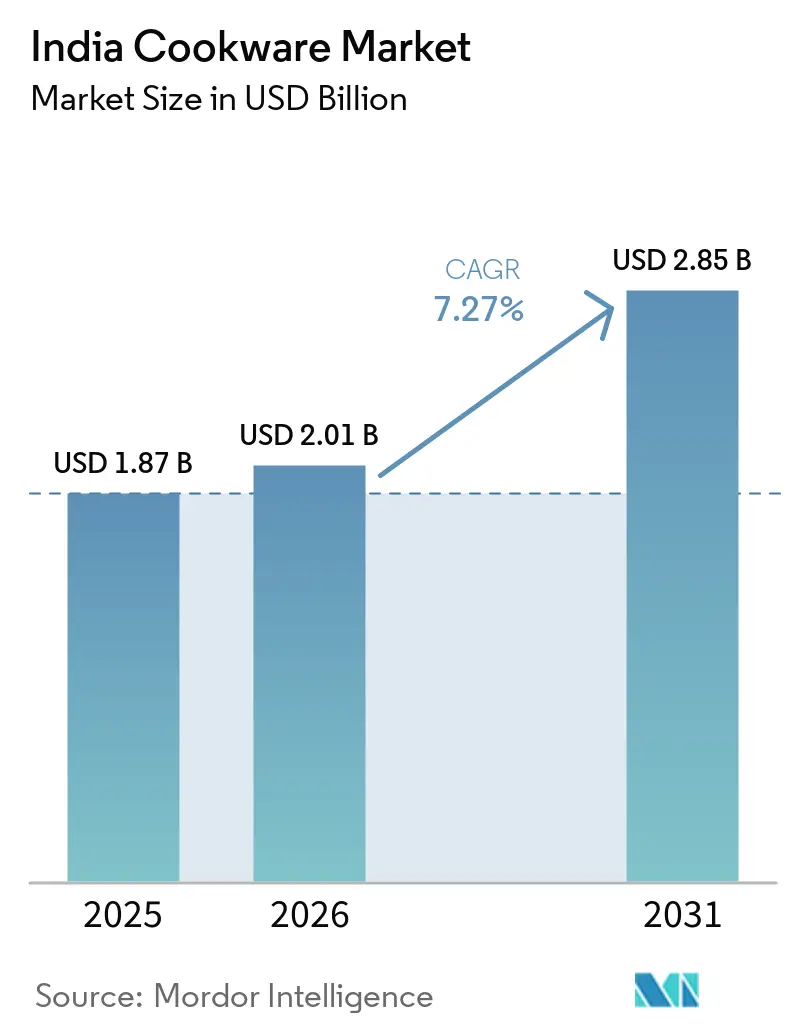

| Base Year Market Size (2025) | USD 1.87 Billion |

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

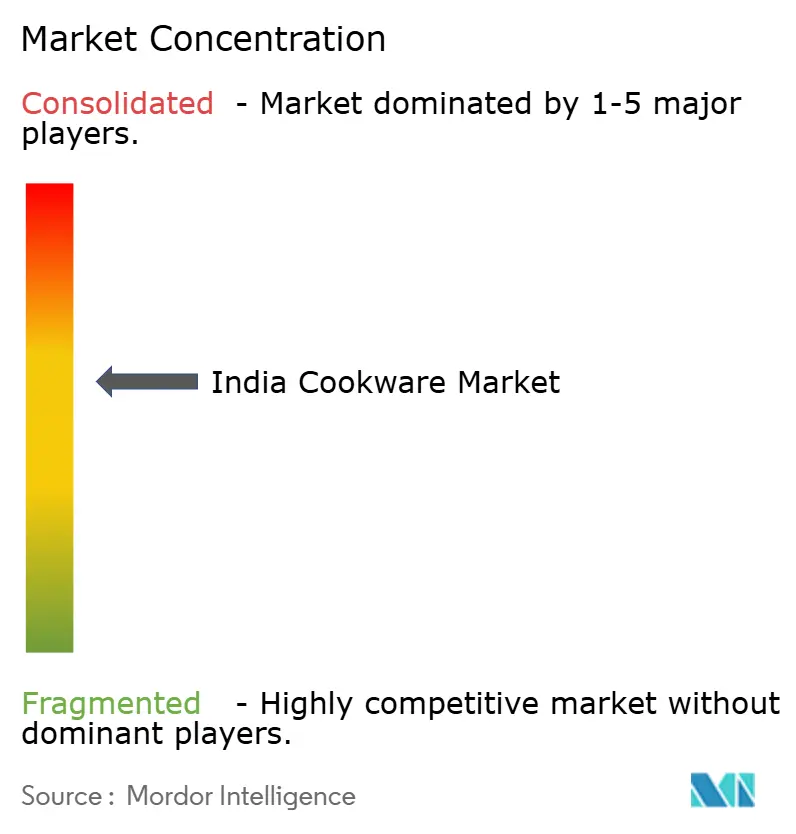

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cookware Market Analysis by Mordor Intelligence

The India cookware market size was valued at USD 1.87 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 2.85 billion by 2031, at a CAGR of 7.27% during the forecast period (2026-2031). Rising disposable incomes, rapid urbanization, and mandatory BIS standards have accelerated the consumer shift from unorganized to organized retail, boosting penetration of branded pots, pans, and pressure cookers across metro and Tier-2 cities[1] Source: SGS India, “Mandatory BIS Certification for Stainless-Steel Cookware,” sgs.com. Health concerns linked to PFAS/PFOA chemicals continue steering households toward stainless steel, cast iron, and ceramic alternatives, reinforcing premiumization trends even in value-focused segments. The e-commerce boom and direct-to-consumer (D2C) storefronts now shorten purchase cycles and elevate product discovery, enabling mid-size brands to challenge legacy players with agile pricing and faster launches. Simultaneously, the Production Linked Incentive (PLI) scheme’s investment outlay catalyzes local manufacturing capacity, strengthening supply chains and lowering dependence on imports for the India cookware market[2]Source: Press Information Bureau, “Performance of the ‘Make in India’ Initiative,” pib.gov.in..

Key Report Takeaways

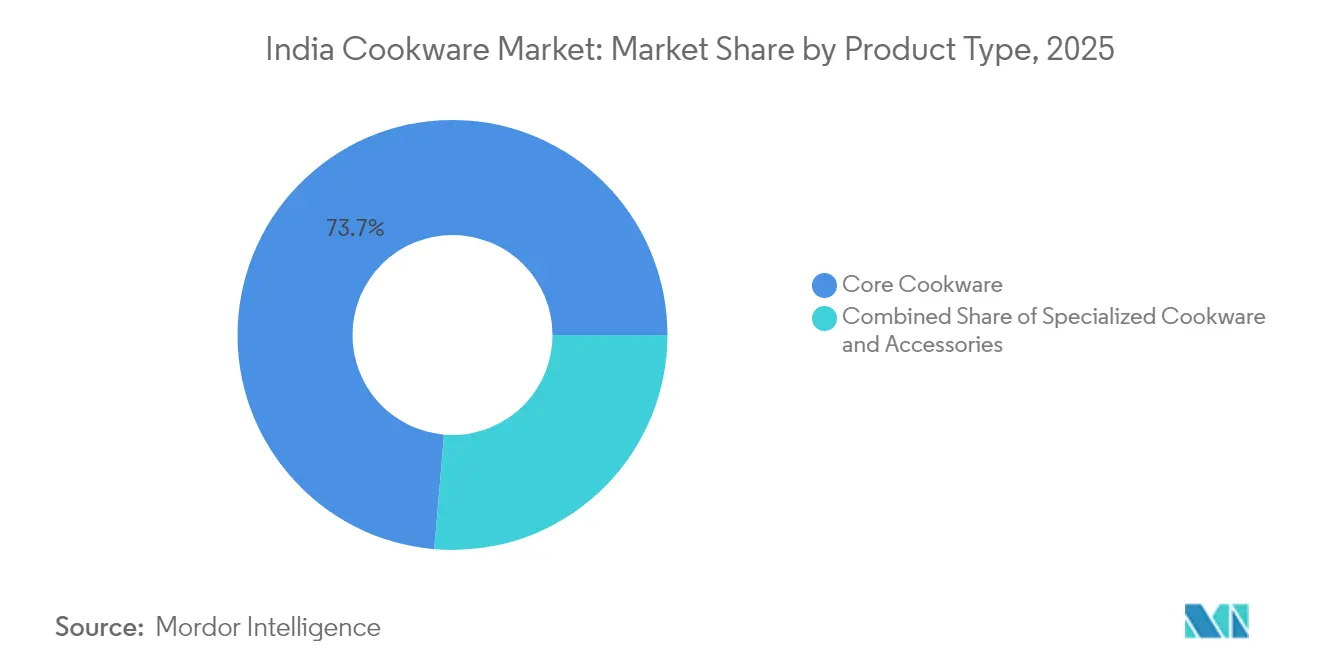

- By product type, core cookware commanded 73.65% of the India cookware market share in 2025, while specialized cookware is forecast to expand at a 9.03% CAGR through 2031.

- By material, stainless steel held a 34.95% share of the India cookware market size in 2025, whereas cast iron is projected to grow at a 7.86% CAGR to 2031.

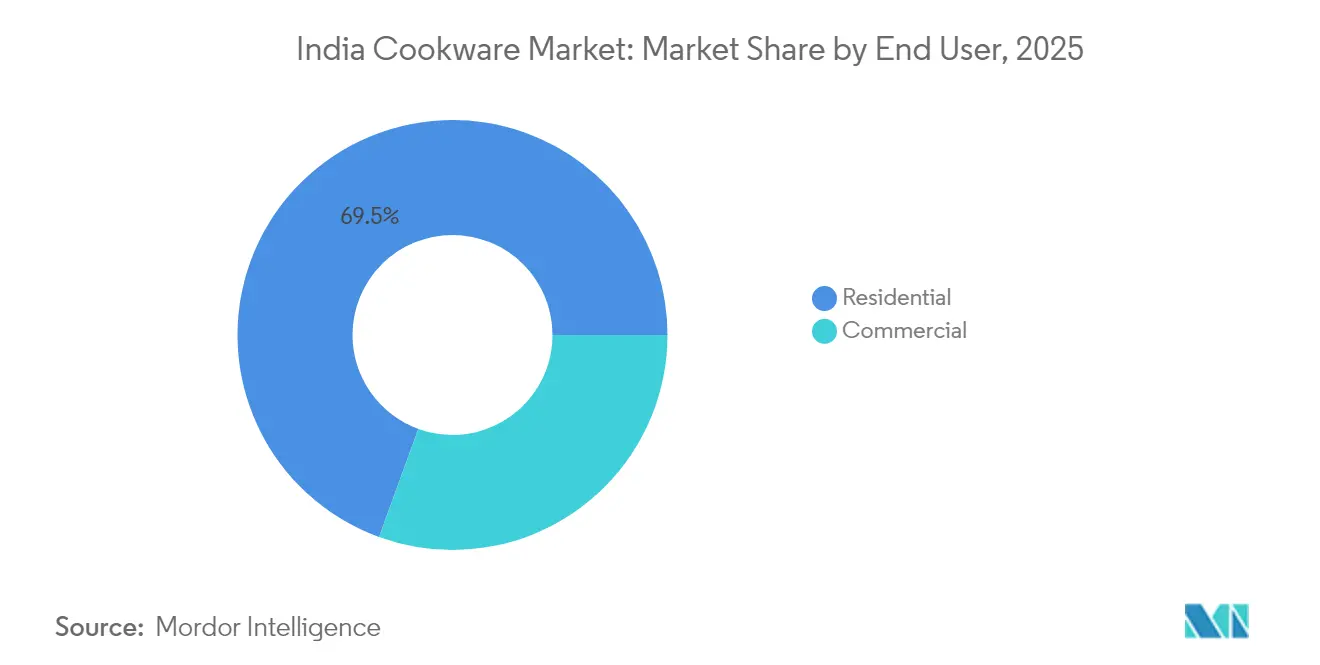

- By end user, the residential segment dominated with 69.45% revenue share in 2025, while commercial applications are advancing at an 8.31% CAGR through 2031.

- By distribution channel, offline retail retained 66.65% of the India cookware market share in 2025, yet online sales will rise at a 8.68% CAGR over the forecast horizon.

- By Region, South India retained 34.75% of the India cookware market share in 2025, yet North India's 9.24% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cookware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & urbanization | +1.8% | National, with early gains in Tier-2 cities | Medium term (2-4 years) |

| Growth of e-commerce & omni-channel retail | +1.5% | Urban centers, expanding to semi-urban areas | Short term (≤ 2 years) |

| Shift toward health-oriented non-stick & ceramic cookware | +1.2% | Metro cities and affluent suburban markets | Long term (≥ 4 years) |

| “Make in India” incentives boosting domestic manufacturing | +0.9% | Manufacturing hubs in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Premiumization via social-media culinary trends | +0.7% | Urban millennials and Gen-Z demographics | Short term (≤ 2 years) |

| Uptake of induction-compatible cookware | +0.6% | Energy-conscious households nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes & Urbanization

Improved purchasing power and lifestyle aspirations are expanding the India cookware market beyond essential pressure cookers toward premium Dutch ovens and sauté pans. Middle-class households now prioritize durability and aesthetics when upgrading kitchenware, which strengthens brand loyalty among certified products. Southern metros post the highest per-capita monthly spends, but Tier-2 cities are catching up quickly, widening the organized retail footprint. The demographic dividend of Gen-Z consumers accelerates first-time purchases of cookware sets geared toward compact apartments. Together, these income gains add steady volume growth and encourage category upgrades across the socioeconomic spectrum[3] Source: Mitsui & Co. Global Strategic Studies Institute, “India’s Middle-Class Consumption Outlook,” mitsui.com.

Growth of E-commerce & Omni-channel Retail

Digital marketplaces simplify product comparison, review reading, and same-day delivery, all of which shorten decision time for cookware purchases. D2C brands exploit lower distribution costs to package value-added accessories such as glass lids and silicone handles without retail markups. Legacy manufacturers adopt omni-channel strategies, integrating click-and-collect models that merge online ordering with neighborhood store pick-ups. Social-commerce livestreams further expand reach by demonstrating cookware performance in real-time, building consumer trust. As mobile internet penetration rises, rural shoppers gain access to the same assortment previously limited to urban malls, broadening the India cookware market.

Shift Toward Health-oriented Non-stick & Ceramic Cookware

Publicized warnings from the Indian Council of Medical Research regarding PFAS/PFOA leaching out of scratched Teflon coatings prompt households to favor ceramic-coated and cast-iron skillets. Manufacturers respond by investing in sol-gel and titanium-reinforced surfaces that withstand higher temperatures without toxic fumes. Consumers equate heavier build quality with safety, elevating cast iron’s value proposition despite higher upfront prices. Cooking influencers amplify these messages, showcasing nutrient retention and even heat distribution advantages. This health-centric narrative sustains long-term demand for premium alternatives and underpins margin expansion opportunities for organized players.

“Make in India” Incentives Boosting Domestic Manufacturing

The PLI program reimburses approved plants based on incremental sales, motivating cookware companies to automate forming, polishing, and anodizing lines. State governments in Gujarat and Tamil Nadu offer additional subsidies on land and power tariffs that reduce fixed overheads for greenfield factories. Local sourcing agreements for stainless steel coils and aluminum ingots lower freight costs and hedge currency risks for exports. Indian brands also gain faster design-to-market cycles, enabling them to tailor product specs for domestic cooking styles without waiting for imported molds. Overall, national industrial policy strengthens resilience across the India cookware market supply chain.

Restraints Impact Analysis*

| Restraint | (–) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large unorganised sector & high price sensitivity | –1.4% | Rural and semi-urban markets nationwide | Long term (≥ 4 years) |

| Volatile raw-material prices (Al & SS) | –0.8% | Manufacturing centers and cost-sensitive segments | Short term (≤ 2 years) |

| PFAS/PFOA regulatory scrutiny on non-stick coatings | –0.6% | Urban health-conscious demographics | Medium term (2-4 years) |

| Limited IoT infrastructure slowing smart-cookware adoption | –0.3% | Tech-forward urban households | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Large Unorganised Sector & High Price Sensitivity

Street-market vendors and local metal-smiths are selling aluminum wares at prices up to 40% lower than branded counterparts. These low-cost offerings cater to price-sensitive consumers, particularly in lower-income brackets, where immediate affordability takes precedence over long-term benefits. As a result, many consumers delay upgrading to certified products, which are often perceived as expensive. To address this challenge, organized players are re-engineering their entry-level SKUs by using thinner gauges and adopting minimal packaging strategies to reduce costs and narrow the price gap. However, mandatory BIS labeling, which ensures product quality and safety, has increased compliance costs for these organized players. In contrast, unorganized sellers often bypass these regulations, allowing them to maintain their competitive pricing and market share. This dynamic creates a significant barrier to the acceptance of premium products, particularly in price-sensitive regions.

Volatile Raw-Material Prices (Al & SS)

In the Indian cookware market, manufacturers grapple with sharp fluctuations in LME aluminum futures and nickel-linked stainless-steel surcharges. These swings erode gross margins, especially for those with extended procurement cycles. While firms hedge using quarterly contracts, sudden spikes still compress EBITDA. This compression prompts selective price hikes, a move that teeters on the edge of demand elasticity. As working capital shifts towards inventory, R&D budgets sometimes take a hit, leading to a deceleration in the pace of innovation. Export orders, often bound by fixed quotes, find themselves in a bind, facing either renegotiation or penalty clauses when there's an unexpected surge in raw-material costs. Additionally, the unpredictability of raw material prices complicates long-term strategic planning, as firms struggle to balance cost management with maintaining competitive pricing. Smaller players in the market, with limited financial resources, are particularly vulnerable to these fluctuations, often facing reduced profitability or even operational disruptions. Thus, commodity volatility poses a significant operational challenge for the Indian cookware market, impacting both short-term performance and long-term growth prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized Solutions Drive Premium Growth

Specialized cookware's 9.03% CAGR through 2031 significantly outpaces core cookware's market-leading 73.65% share in 2025, indicating consumer willingness to invest in category-specific solutions that enhance cooking efficiency and food quality. Core items such as pressure cookers and fry pans still dominate household penetration, yet price competition compresses their margins. Social-media recipe trends motivate enthusiastic home cooks to buy incremental pieces that optimize specific dishes, extending lifetime customer value for brands. This blended strategy sustains revenue growth without over-exposing inventories to fashion cycles.

Premium specialization also aids channel segmentation, since e-commerce excels at explaining nuanced features, whereas mass merchants rely on foot traffic for core offerings. Manufacturers invest in modular handle systems and universal lids to cross-sell accessories that lift average selling prices. Commercial buyers increasingly specify standardized SKUs for institutional kitchens, directing core volumes toward stainless collections with reinforced rims for durability. Gift-pack promotions during festive seasons further accelerate turnover, validating higher price points for innovative forms. Altogether, specialty adoption drives brand differentiation in the India cookware market while core lines supply stable baseline demand.

By Material: Cast-Iron Renaissance Challenges Stainless-Steel Dominance

Stainless steel retained a 34.95% hold on the India cookware market share in 2025 due to proven durability and corrosion resistance, but cast iron is expected to outpace all rivals at an 7.86% CAGR to 2031. Government-mandated IS 14756:2022 standards reinforce confidence in steel grades free from harmful admixtures, sustaining its volume leadership. Cast-iron skillets, griddles, and woks regain favor among health-minded consumers seeking natural seasoning and higher iron intake. Vendors lighten traditional cast iron through precision milling, improving usability without sacrificing heat retention. Ceramic-coated aluminum rounds out mid-price tiers, bridging cost and wellness expectations.

Material diversity lets brands target micro-segments; for instance, carbon steel appeals to professionals wanting searing capability minus the heft of cast iron. Copper occupies niche gourmet kitchens, prized for rapid thermal response despite premium costs. Emerging silica-ceramic blends promise PFAS-free non-stick performance, though scalability remains limited. Glass-top bakeware benefits from aesthetic transparency, supporting oven-to-table presentations that resonate with social-media plating culture. Such layered positioning ensures broad appeal across disposable-income bands inside the India cookware market.

By End User: Commercial Segment Accelerates Amid HoReCa Expansion

Hotels, restaurants, and caterers collectively generated a robust 8.31% CAGR within the India cookware market between 2026 and 2031, underpinned by tourism recovery and cloud-kitchen proliferation. Institutional buyers prioritize total cost of ownership, gravitating toward thick-gauge stainless steel and cast iron capable of enduring high-BTU burners. Volume contracts negotiated through e-procurement portals streamline procurement cycles and secure bulk discounts. Residential consumers, while still representing 69.45% of 2025 revenue, increasingly emulate professional standards by purchasing tri-ply multilayered vessels. That emulation boosts average selling prices even in the household segment.

Urban nuclear families opt for space-saving stackable sets, reflecting shrinking kitchen footprints in high-rise apartments. Cookware brands co-produce recipe booklets and QR-linked video tutorials to guide first-time users, enhancing perceived value. In the commercial channel, hygiene certifications and HACCP compliance form key tender criteria, favoring organized suppliers with documented quality systems. Shared-kitchen startups lease premium cookware to culinary entrepreneurs, creating recurring revenue for equipment providers. Consequently, dual-track strategies are essential for sustained competitiveness across end-user categories inside the India cookware market.

By Distribution Channel: Digital Disruption Reshapes Retail Landscape

Offline outlets such as hypermarkets and specialty stores retained 66.65% share in 2025, yet online portals will log a striking 8.68% CAGR, steadily eroding the gap. Webshops let brands narrate ingredient-safe coatings and induction compatibility in multimedia formats, addressing product-knowledge deficits common in crowded store aisles. Flash sales and influencer coupon codes compress adoption timelines, enabling faster inventory turnover than traditional festive-season peaks. Retailers integrate endless-aisle kiosks so shoppers can order out-of-stock SKUs online with home delivery, blending convenience across channels. Flexible return policies further dismantle buyer hesitancy around higher-priced premium cookware.

Brick-and-mortar stores still excel at tactile validation, where heft and handle ergonomics influence purchase decisions. D2C models offset the absence of physical trials through 30-day risk-free usage offers, funded by savings on wholesale margins. Commercial customers rely on direct sales teams that provide specification advice, cook-line layout planning, and after-sales training. Marketplace algorithms spotlight emerging regional brands based on customer reviews, injecting competitive variety and pushing incumbents toward continuous innovation. Overall, channel interplay defines success in the India cookware market by balancing reach, education, and experiential engagement.

Geography Analysis

South India contributed 34.75% of 2025 revenue on the strength of culinary traditions that prize specialty tools like idli steamers and appachatty pans, bolstered by higher per-capita incomes in Chennai, Bangalore, and Hyderabad. Metropolitan tech salaries encourage discretionary kitchen upgrades, while state-level incentives for food-processing clusters create institutional demand for durable commercial vessels. The India cookware market size for South India also benefits from mature retail infrastructure, allowing omnichannel models to flourish through click-and-collect services. Meanwhile, proximity to steel and aluminum ports lowers inbound freight costs for manufacturers, securing price advantages. Cultural gifting practices during Pongal and Onam festivals further elevate cookware unit sales in the region.

North India claims the fastest 9.24% CAGR outlook through 2031, reflecting accelerating urbanization in Delhi NCR, Punjab, and Uttar Pradesh. The adoption curve in this belt lags the south, leaving ample room for premium upgrades as disposable incomes converge. Cookware marketers tailor compact, multi-use pots suitable for smaller modular kitchens prevalent in high-density housing projects. Retail expansion into organized malls and neighborhood electronics chains amplifies footprint without cannibalizing existing mom-and-pop outlets. Government-led Smart City missions enhance logistics efficiency, trimming delivery times and supporting online penetration across the India cookware market.

Western states like Maharashtra and Gujarat leverage industrial baselines that foster manufacturing synergies, enabling rapid product development cycles. Producers located near raw-material sources hedge commodity price swings better than inland rivals, lending supply-chain resilience. East India, by contrast, provides cost-effective labor pools and rising middle-class segments hungry for branded cookware at attainable prices. Brands deploy phased rollouts, starting with core SKUs that educate consumers before layering specialized pieces. This regionally nuanced approach balances inventory risk and maximizes growth potential across the national India cookware market.

Competitive Landscape

The India cookware market exhibits moderate fragmentation with established players like TTK Prestige, Hawkins Cookers, and Stovekraft competing against emerging D2C brands and unorganized sector participants, creating a three-tier competitive structure based on brand recognition, distribution reach, and price positioning. TTK Prestige leverages multi-plant capacity and celebrity endorsements to preserve brand recall even as export volumes fluctuate amid shipping constraints. Hawkins Cookers sustains loyalty through product durability and a nationwide network of service centers offering gasket and safety-valve replacements. Stovekraft invests in influencer-backed digital launches to capture online shoppers migrating to non-stick ceramic coatings. Emerging D2C entrants differentiate on design aesthetics and toxin-free warranties, appealing to urban millennials swayed by environmental messaging. Unorganized manufacturers still dominate rural storefronts, but mandatory BIS compliance raises their entry barriers, nudging gradual consolidation in favor of certified players.

Strategic plays increasingly revolve around capacity upgrades; Borosil earmarked INR 250 crore for a new Gujarat plant targeting INR 7,000 crore topline by 2028, signaling bullishness on domestic demand. Cross-licensing with global coating specialists accelerates technology transfer, bringing diamond-reinforced sol-gel finishes to mid-tier price points. Partnerships with power-utility e-marketplaces channel induction-ready sets to government employees availing payroll deductions, cementing volume stability. Sustainability drives spur adoption of recyclable packaging and renewable-energy sourcing, framing environmental performance as a competitive differentiator. Collectively, these initiatives intensify innovation velocity and heighten quality benchmarks across the India cookware market.

IoT integration will remain exploratory until broadband penetration rises, prompting companies to focus on ergonomic gains such as stay-cool handles and glass-infused lids. After-sales ecosystems offering spare parts via micro-fulfillment centers fortify customer retention strategies. Retail data analytics guide SKU rationalization, trimming slow movers to free capacity for high-growth specialty profiles. Brand collaborations with culinary institutes serve dual objectives of product testing and influencer marketing. Overall, success hinges on balancing tradition-rooted functionality with contemporary health and convenience priorities within the dynamic India cookware market.

India Cookware Industry Leaders

TTK Prestige

Hawkins Cookers Ltd.

Stovekraft Ltd.

Wonderchef Home Appliances Pvt. Ltd.

Butterfly Gandhimathi Appliances Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vinod Cookware unveiled the “Ferona” matte-enamel cast-iron collection catering to health-conscious consumers.

- August 2025: Airlock India launched “Trivedh,” a premium tri-ply range focused on energy efficiency and durability.

- July 2025: Cumin Co. introduced India’s first 100% toxin-free enamel cast-iron line positioned for modern living spaces.

- May 2025: Pots and Pans released the Meyer Presta Tri-Ply Pressure Cooker series featuring an advanced safety valve and universal cooktop compatibility.

India Cookware Market Report Scope

Cookware is one of the most widely demanded products as people are adopting urbanization. A complete background analysis of the India Cookware Market includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles covered in the report. The India Cookware Market is segmented by Products (Pots & Pan, Cooking Racks, Cooking Tools, Microwave Cookware, and Pressure Cookers), by Materials (Stainless Steel, Aluminium, Glass, and Others), by End User (Residential, Commercial), and by Distribution Channel (Hypermarkets and Supermarkets, Specialty Store, Online, and Other Distribution Channels)

By Product Type (Value)

| Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | |

| Pressure Cookers & Steamers | |

| Cookware Sets | |

| Specialized Cookware | Dutch Ovens & Casseroles |

| Specialty Cookware (Idli, Appam, Dosa, etc.) | |

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | |

| Accessories (Lids, Handles) |

By Material (Value)

| Stainless Steel |

| Aluminium |

| Cast Iron |

| Carbon Steel |

| Copper |

| Ceramic/Glass |

| Silicone |

| Other Coated Substrates |

By End User (Value)

| Residential |

| Commercial (HoReCa, Institutional, Catering) |

By Distribution Channel (Value)

| Offline Retail | Super/Hypermarkets |

| Department Stores | |

| Specialty Stores | |

| Online | E-commerce Marketplaces |

| Brand Webshops | |

| B2B / Direct Sales |

By Region

| North India |

| South India |

| West India |

| East & Northeast India |

| By Product Type (Value) | Core Cookware | Pans (Fry/Saute, Grill, Wok/Kadhai, Crepe) |

| Pots (Sauce, Stock, Dutch Oven) | ||

| Pressure Cookers & Steamers | ||

| Cookware Sets | ||

| Specialized Cookware | Dutch Ovens & Casseroles | |

| Specialty Cookware (Idli, Appam, Dosa, etc.) | ||

| Bakeware (Ovenware, Muffin trays, Cake tins, etc.) | ||

| Accessories (Lids, Handles) | ||

| By Material (Value) | Stainless Steel | |

| Aluminium | ||

| Cast Iron | ||

| Carbon Steel | ||

| Copper | ||

| Ceramic/Glass | ||

| Silicone | ||

| Other Coated Substrates | ||

| By End User (Value) | Residential | |

| Commercial (HoReCa, Institutional, Catering) | ||

| By Distribution Channel (Value) | Offline Retail | Super/Hypermarkets |

| Department Stores | ||

| Specialty Stores | ||

| Online | E-commerce Marketplaces | |

| Brand Webshops | ||

| B2B / Direct Sales | ||

| By Region | North India | |

| South India | ||

| West India | ||

| East & Northeast India | ||

Key Questions Answered in the Report

How large will household demand for cookware be by 2031 in India?

Household demand is projected to keep residential sales above 69% of overall revenue even in 2031, supported by a growing middle class and persistent premiumization.

Which material category is showing the fastest growth?

Cast-iron vessels are set to expand at an 7.86% CAGR through 2031 owing to health perceptions and improved product ergonomics.

What role does e-commerce play in cookware distribution?

Online portals are forecast to grow at a 8.68% CAGR, enabling brands to bypass traditional retail margins and reach consumers in semi-urban areas.

Why is North India attracting cookware manufacturers?

Rapid urbanization and rising nuclear families produce the fastest 9.24% regional CAGR, offering significant catch-up potential for premium upgrades.

How is government policy influencing production?

The PLI scheme and BIS certification drive domestic capacity expansion and quality differentiation, making India a more self-reliant manufacturing hub for cookware.

Page last updated on: