Upstream Bioprocessing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

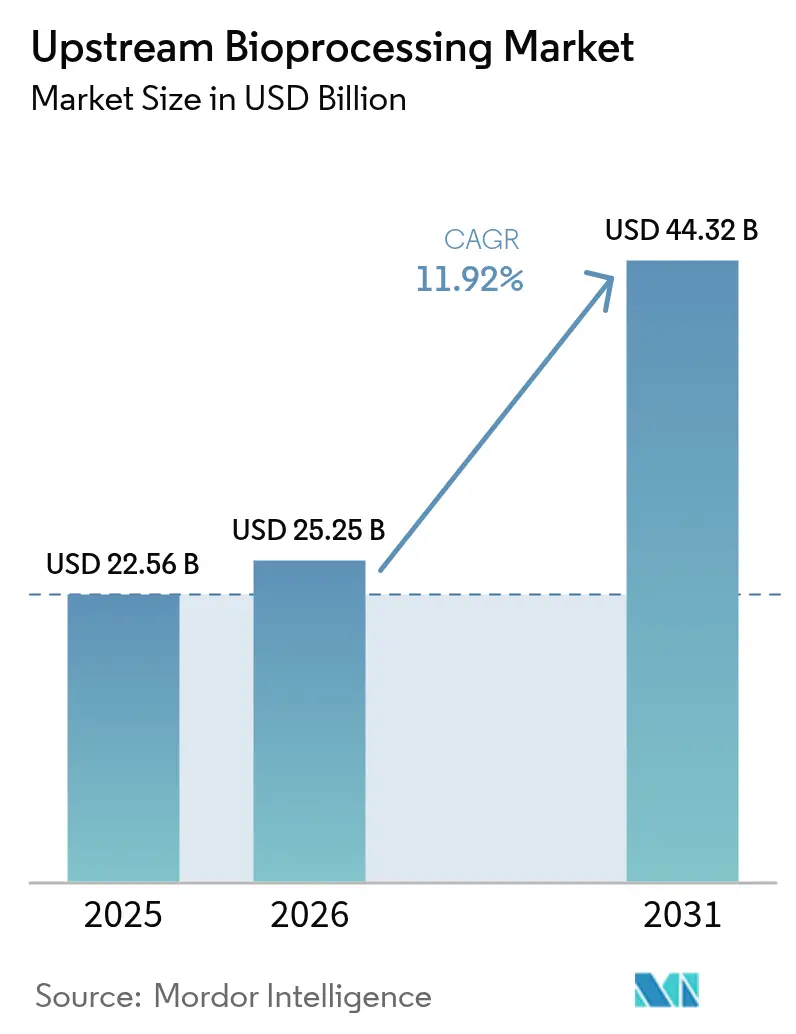

| Market Size (2026) | USD 25.25 Billion |

| Market Size (2031) | USD 44.32 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

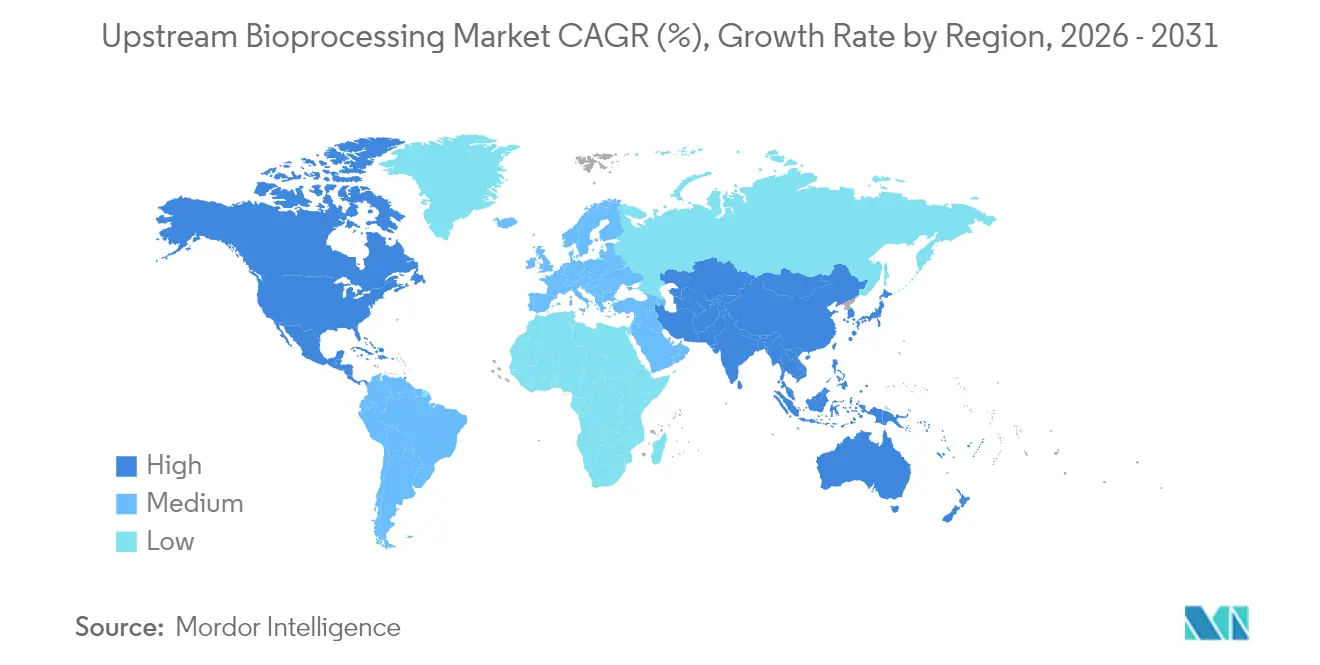

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Upstream Bioprocessing Market Analysis by Mordor Intelligence

The upstream bioprocessing market size in 2026 is estimated at USD 25.25 billion, growing from 2025 value of USD 22.56 billion with 2031 projections showing USD 44.32 billion, growing at 11.92% CAGR over 2026-2031. Growth accelerates as manufacturers adopt flexible single-use platforms, high-intensity perfusion bioreactors and AI-enabled process controls that compress scale-up timelines while meeting stringent regulatory standards [1]Thermo Fisher Scientific, “Annual Report 2025,” thermofisher.com. Intensifying demand for cell and gene therapies, biosimilars and recombinant vaccines keeps capacity additions above the historical trend, and drives supplier investments in vertically integrated component supply chains. North America retains the largest regional footprint thanks to mature biopharmaceutical clusters and FDA guidance that expedites continuous manufacturing approval [2]U.S. Food and Drug Administration, “Framework for Advanced Manufacturing,” fda.gov , yet Asia-Pacific delivers the fastest output expansion as government incentives and lower operating costs catalyze new greenfield plants. Technology convergence between single-use hardware and advanced analytics reduces total cost of ownership, supporting broader uptake by small and mid-sized sponsors. Meanwhile, consolidation among leading vendors tightens control over critical filtration, media and sensor technologies, raising competitive barriers for late entrants.

Key Report Takeaways

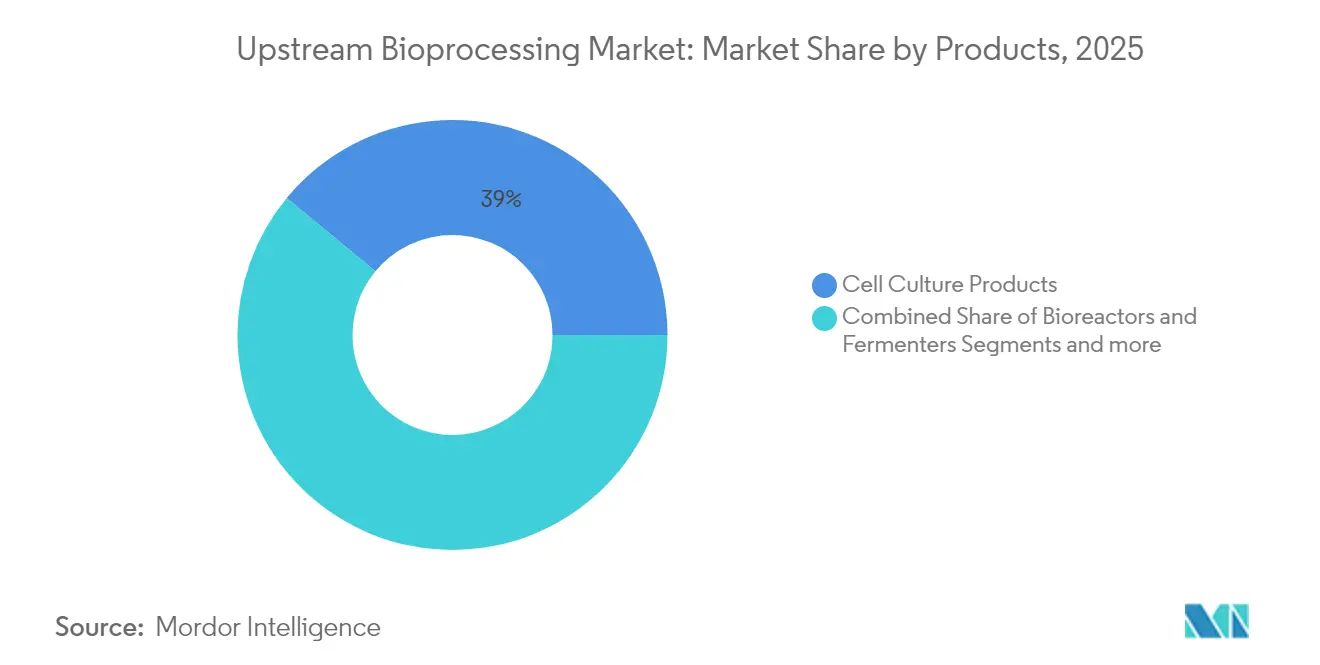

- By product, cell culture solutions held 39.01% of upstream bioprocessing market share in 2025 and bioreactors and fermenters are forecast to expand at a 12.52% CAGR through 2031.

- By usage type, single-use systems accounted for 62.55% of the upstream bioprocessing market size in 2025 while multi-use equipment records the highest projected CAGR at 12.66% to 2031.

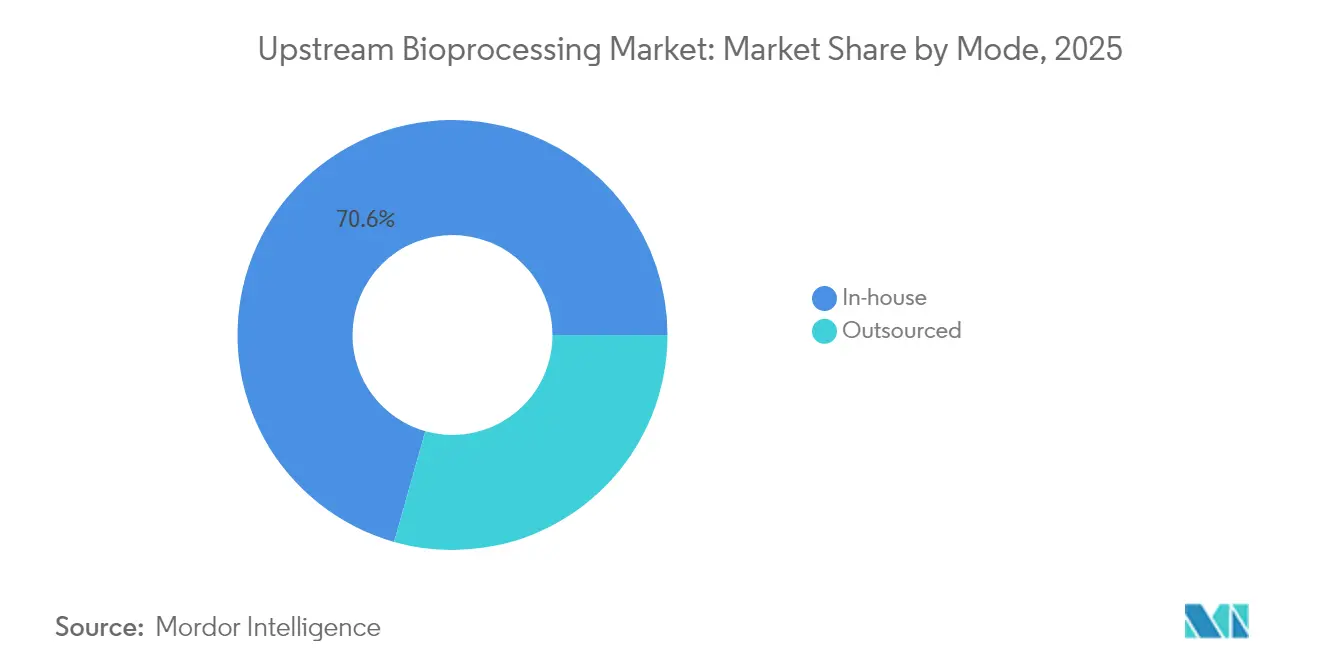

- By mode, in-house manufacturing commanded 70.62% share of the upstream bioprocessing market size in 2025, whereas outsourcing is expected to advance at a 12.61% CAGR during 2026-2031.

- By end user, contract development and manufacturing organizations captured 12.74% CAGR, the fastest of all segments, between 2026 and 2031.

- By geography, North America generated 40.78% market revenue while Asia-Pacific captured 12.8% CAGR, the fastest of all segments, between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Upstream Bioprocessing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of single-use upstream bioprocessing | +2.1% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Commercial success and rising demand for biotherapeutics | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Emergence of high-intensity perfusion bioreactors | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Government push for domestic biomanufacturing capacity | +0.9% | US, Canada, UK, India and China | Long term (≥ 4 years) |

| Integration of continuous manufacturing workflows | +0.7% | North America and Europe, pilot projects in APAC | Long term (≥ 4 years) |

| AI-driven optimisation of cell-culture parameters | +0.6% | Global, early adoption in tech-forward plants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Single-Use Upstream Bioprocessing

Single-use technologies remove the cleaning validation burden linked to stainless-steel systems and let facilities pivot between molecule classes with minimal downtime. Production flexibility improves asset utilisation, yet 2024 resin shortages exposed supply bottlenecks that prompted hybrid facilities combining disposable and reusable assets. Vendor vertical integration and polymer diversification programs will ease pressure, but lead times of 18-24 months suggest continued tightness that rewards suppliers holding strategic inventory positions.

Commercial Success & Rising Demand for Biotherapeutics

Accelerated approvals for novel biologics and breakthrough designations shorten clinical-to-commercial transition windows, amplifying upstream capacity requirements. Emerging biotechs increasingly outsource to CDMOs because the capex burden of purpose-built plants is hard to justify for molecules with unproven market trajectories. Volume bifurcation is visible: blockbuster monoclonal antibodies demand scale efficiencies while niche advanced therapies need bespoke small-batch environments.

Emergence of High-Intensity Perfusion Bioreactors

Perfusion platforms sustain cell densities up to ten-fold higher than fed-batch reactors, slashing facility footprints and cutting cost of goods sold by as much as 60% for large-volume products. Implementation challenges include continuous media exchange, cell retention device fouling and sophisticated monitoring requirements. Early movers that have mastered perfusion report first-mover advantages in productivity metrics and faster lot release cycles.

Government Push for Domestic Biomanufacturing Capacity

National security agendas fund domestic vaccine and biologics infrastructure. The US committed USD 2 billion to expand local production suites and workforce programs, mirrored by similar initiatives in Canada, the UK, India and China. Contracts often stipulate local sourcing of critical consumables, advantaging vendors with regional manufacturing footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational challenges including shear stress and scalability | -1.4% | Global, affecting high-shear processes | Short term (≤ 2 years) |

| Supply-chain volatility for single-use plastics | -0.8% | Global, acute in regions relying on Asian suppliers | Short term (≤ 2 years) |

| Skilled labour shortages in bioprocess engineering | -0.6% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Quality variability in novel cell lines | -0.4% | Global, concentrated in advanced therapy hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Operational Challenges Including Shear Stress and Scalability

Scale-up often alters hydrodynamic conditions that harm shear-sensitive cell lines, reducing viability and changing glycosylation profiles. Advanced impeller geometries and computational fluid dynamics modelling reduce turbulence, but they raise capital costs and extend qualification timelines. Perfusion configurations partly alleviate scale limitations, although they introduce extra filtration and control complexity.

Supply-Chain Volatility for Single-Use Plastics

Concentrated resin supply left many biotech firms with lead-time extensions during 2024, inflating consumable prices and delaying campaign starts. Diversification into regional polymer plants and recycled-content programs are underway, yet 18-24 months are needed before new capacity reaches commercial volumes, meaning near-term exposure persists for buyers without long-term supply contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cell Culture Dominance Drives Innovation

Cell culture media, sera and growth factors held 39.01% upstream bioprocessing market share in 2025, reflecting their pivotal role in productivity optimisation. Media formulation advances, such as chemically defined feeds, stabilise metabolites and curb lot variability. Supplements tailored to CHO or HEK lines command premium pricing, supporting solid segment margins. The bioreactors and fermenters sub-segment expands at 12.52% CAGR as single-use formats and perfusion designs enable higher titres in smaller footprints. Adoption of modular control software lets operators refine agitation, gas-transfer and temperature profiles, enhancing reproducibility. Filters, probes and ancillary accessories rise in tandem because intensified processes mandate closed fluid paths and high-resolution monitoring to avoid contamination.

Stainless-steel vessels still dominate high-volume monoclonal antibody production where depreciation is spread across multi-decade asset lives, but new builds favour single-use or hybrid operations that shorten tech-transfer cycles and minimise downtime . Perfusion units recorded double-digit adoption growth during 2024-2025 as firms chased facility densification goals. Integrated depth-filtration skids streamline harvest clarification inside disposable flow-paths, aligning with quality-by-design objectives and cutting change-over labor hours.

By Usage Type: Single-Use Systems Reshape Manufacturing

Single-use assemblies secured 62.55% upstream bioprocessing market share in 2025 due to their ability to eliminate cross-contamination risk and accelerate campaign changeovers. Disposable flow-paths suit multi-product CDMO suites and early-stage programs where batch sizes are small and timelines compressed. Large-volume biologics retain multi-use infrastructure for economic reasons, so the multi-use category grows at 12.66% CAGR through 2031 as manufacturers retrofit existing plants with advanced sensing and automation. Hybrid facilities that mix steel bioreactors with single-use seed trains balance flexibility and operating cost constraints.

Environmental sustainability debates influence equipment strategy. Users deploying high-throughput monoclonal antibody lines adopt multi-use skid technologies that lower polymer waste generation, whereas viral-vector producers prefer disposable containment to prevent cross-viral contamination. Vendor innovation now targets recycling initiatives and lower-weight films to mitigate ecological concerns without compromising sterility or leachables profiles.

By Mode: Outsourcing Accelerates Amid Capacity Constraints

In-house lines retained 70.62% upstream bioprocessing market size in 2025, anchored by large pharma’s need for process sovereignty and intellectual-property protection. However, outsourced manufacturing logs the highest 12.61% CAGR as CDMOs scale multi-tenant campuses that pool analytical labs, viral-vector suites, and high-speed perfusion reactors. CDMO capacity utilisation climbed to 85-90% during 2024, granting providers pricing power and selection control over project pipelines. Sponsors, therefore, pursue hybrid supply chains—retaining flagship biologics internally while outsourcing surge demand or specialised cell therapy steps.

In-house operators intensify existing assets through high-density fed-batch retrofits and perfusion conversions to justify capital tied up in legacy stainless-steel plants. Workforce development is critical: shortages in bioprocess engineers and automation specialists elevate recruitment costs and prolong validation schedules. Collaborative training initiatives with academic institutions alleviate skill gaps but require sustained funding.

By End User: CDMOs Emerge as Growth Catalysts

Biopharmaceutical innovators consumed 59.76% of upstream bioprocessing equipment in 2025, yet CDMOs deliver the fastest 12.74% CAGR on the back of venture-backed biotech outsourcing patterns. Niche service providers specialise in autologous cell therapy, mRNA vaccines and viral-vector supply, capturing premium pricing for expertise and rapid turnaround. Academic and research institutes buy scaled-down bioreactors to train graduates and conduct early-stage process development, fostering a skilled workforce pipeline. Government laboratories remain a small but strategic purchaser cohort, prioritising biosafety and supply-chain resilience over throughput metrics.

CDMOs seeking differentiation add integrated analytical and regulatory consultancy offerings, positioning themselves as one-stop partners from pre-clinical through commercial launch. Client stickiness rises with each incremental service layer, locking in multi-year contracts and supporting steady revenue visibility amid volatile funding cycles in the biotech sector.

Geography Analysis

North America held 40.78% upstream bioprocessing market share in 2025 as dense biopharma clusters, venture capital availability and FDA regulatory clarity foster rapid technology uptake. Federal investments totaling USD 2 billion support new fill-finish suites, single-use bag manufacturing and localised supply chains. Canada’s pandemic-preparedness grants fund modular vaccine facilities, while Mexico attracts near-shoring biologics projects seeking lower operating costs without sacrificing US market proximity. Continuous-processing guidance from the FDA accelerates adoption of end-to-end manufacturing trains, giving domestic sites an efficiency edge.

Asia-Pacific’s 12.8% CAGR through 2031 marks the highest regional pace. China subsidises domestic perfusion bioreactor development and upstream consumable plants to lessen foreign reliance. India leverages its biosimilar leadership to win multi-national tech-transfer mandates, focusing on cost-per-gram optimisation. Japan and South Korea channel R&D funds into viral-vector and iPSC therapy platforms that need highly controlled small-volume bioreactors. Regional supply-chain diversification programs encourage local resin production, reducing exposure to overseas shipping delays and tariff risks.

Europe maintains moderate growth anchored by Germany, the United Kingdom and Switzerland. EU sustainability goals motivate adoption of continuous operations and low-energy facility designs, and the European Medicines Agency provides harmonised guidance for advanced therapy medicinal products. France, Italy and Spain house specialised contract manufacturers serving niche biologic segments. European suppliers position themselves as partners in digital transformation, integrating PAT sensors and AI analytics with disposable hardware to deliver incremental productivity gains.

Competitive Landscape

The upstream bioprocessing market shows moderate consolidation as Thermo Fisher Scientific, Danaher Corporation and Sartorius AG leverage vertical integration to command filtration membranes, single-use bags, sensors and media formulations. Differentiation hinges on full-workflow portfolios rather than price competition, creating switching costs for clients embedded in proprietary automation architectures. Mid-tier players concentrate on specialised gaps such as perfusion cell-retention devices, AI-driven control software and custom media.

Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit in 2024 illustrated the imperative to secure critical downstream assets in order to offer truly end-to-end platforms. Sartorius expanded its Marlborough innovation centre, adding GMP suites to provide process-development through early-stage manufacturing services that embed its hardware into client pipelines. Danaher’s Cytiva division invested heavily in digital twins and process analytical technology, underscoring the shift toward data-driven manufacturing. White-space opportunities persist in emerging markets where cost-optimised single-use systems can displace legacy stainless-steel imports, and in advanced therapy niches where bespoke bioreactors and closed-cartridge harvest devices remain underserved.

Supply-chain resilience has become a strategic differentiator. Vendors with multiple resin and film factories across continents secure priority status in RFP evaluations. Companies that cross-license filtration media or co-develop sensors with analytics firms increase platform stickiness, ensuring multi-year consumable pull-through.

Upstream Bioprocessing Industry Leaders

Thermo Fisher Scientific Inc.

Corning, Inc

Merck KGaA

Sartorius AG

Danaher Corporation (Cytvia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Thermo Fisher Scientific and Sanofi expanded their partnership after Thermo Fisher acquired Sanofi’s sterile drug product facility in Ridgefield, NJ, adding 200 employees and strengthening US fill-finish capacity.

- April 2025: Thermo Fisher Scientific announced a USD 2 billion US investment plan over four years, dedicating USD 1.5 billion to manufacturing expansion and USD 500 million to R&D for high-impact innovation.

- November 2024: Sartorius Stedim Biotech opened a Center for Bioprocess Innovation in Marlborough, Massachusetts, featuring research labs and process-development services with two GMP suites scheduled for 2025.

- October 2024: Thermo Fisher Scientific introduced Accelerator Drug Development services at CPHI Milan, broadening CDMO and CRO offerings across biologics, small molecules and advanced therapies.

Global Upstream Bioprocessing Market Report Scope

As per the scope, upstream bioprocessing involves using living cells to obtain desired products. This process starts from early cell separation and cultivation to cell culture expansion to harvest the final product.

The upstream bioprocessing market is segmented by product (cell culture products, bioreactors/fermenters, filters, bioreactors accessories, and other products), usage type (single-use and multi-use), mode (in-house and outsourced), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Cell Culture Products | Media |

| Sera & Reagents | |

| Supplements & Growth Factors | |

| Bioreactors and Fermenters | Stainless-steel Bioreactors |

| Single-use Bioreactors | |

| Perfusion Bioreactors | |

| Filters | |

| Bioreactor Accessories | |

| Other Products |

| Single-use |

| Multi-use |

| In-house |

| Outsourced |

| Biopharmaceutical Companies |

| Contract Manufacturing Organisations (CMOs/CDMOs) |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Cell Culture Products | Media |

| Sera & Reagents | ||

| Supplements & Growth Factors | ||

| Bioreactors and Fermenters | Stainless-steel Bioreactors | |

| Single-use Bioreactors | ||

| Perfusion Bioreactors | ||

| Filters | ||

| Bioreactor Accessories | ||

| Other Products | ||

| By Usage Type | Single-use | |

| Multi-use | ||

| By Mode | In-house | |

| Outsourced | ||

| By End User | Biopharmaceutical Companies | |

| Contract Manufacturing Organisations (CMOs/CDMOs) | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is global upstream bioprocessing capacity growing?

Installed capacity expands at a 11.92% CAGR through 2031 as more firms adopt flexible single-use and perfusion technologies.

Which region will add the most new upstream suites through 2031?

Asia-Pacific posts the highest 12.8% growth as China, India and South Korea subsidise domestic biomanufacturing.

Why are single-use systems preferred for early-stage programs?

Disposable assemblies remove cleaning validation steps, cut changeover time and support rapid multi-product scheduling.

What drives CDMOs share gains in biologics production?

Emerging biotech firms outsource to CDMOs to avoid capex and to access specialised expertise in cell and gene therapy.

Which technology offers the greatest productivity uplift?

High-intensity perfusion bioreactors lift cell densities 5-10 fold, reducing facility footprints and cost of goods sold.

How are suppliers mitigating resin shortages?

Vendors invest in regional polymer plants and diversify material sourcing, though new capacity takes up to two years to come on-line.

Page last updated on: