Targeted Sequencing And Resequencing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

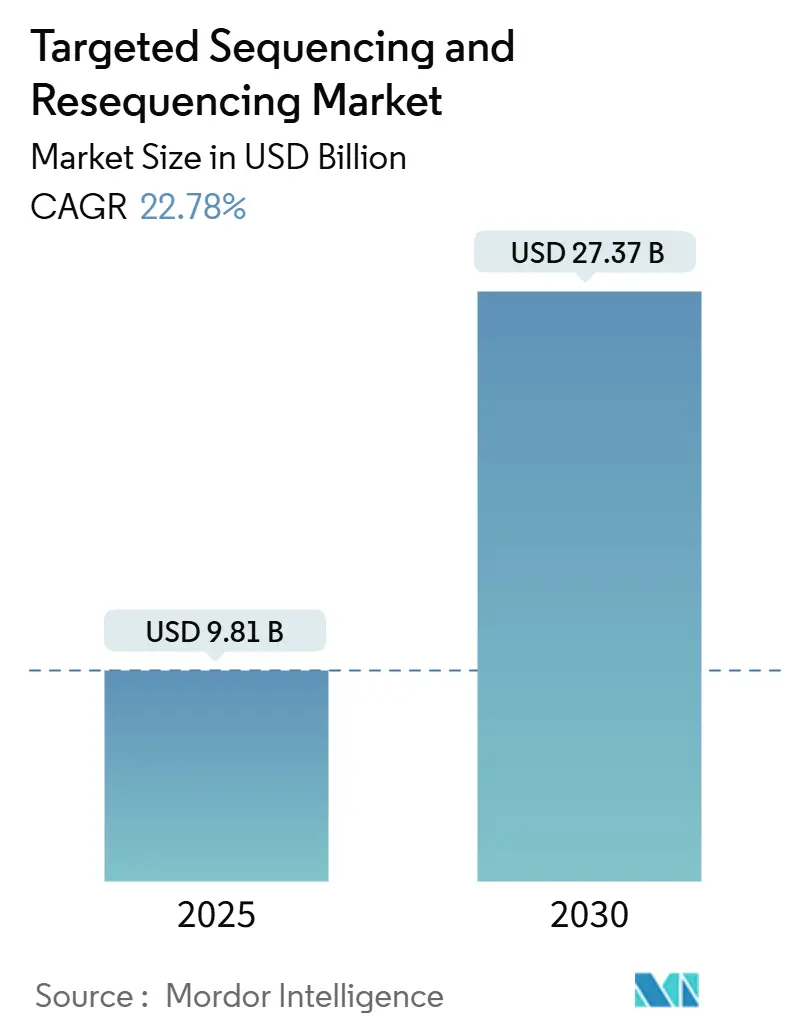

| Market Size (2025) | USD 9.81 Billion |

| Market Size (2030) | USD 27.37 Billion |

| Growth Rate (2025 - 2030) | 22.78% CAGR |

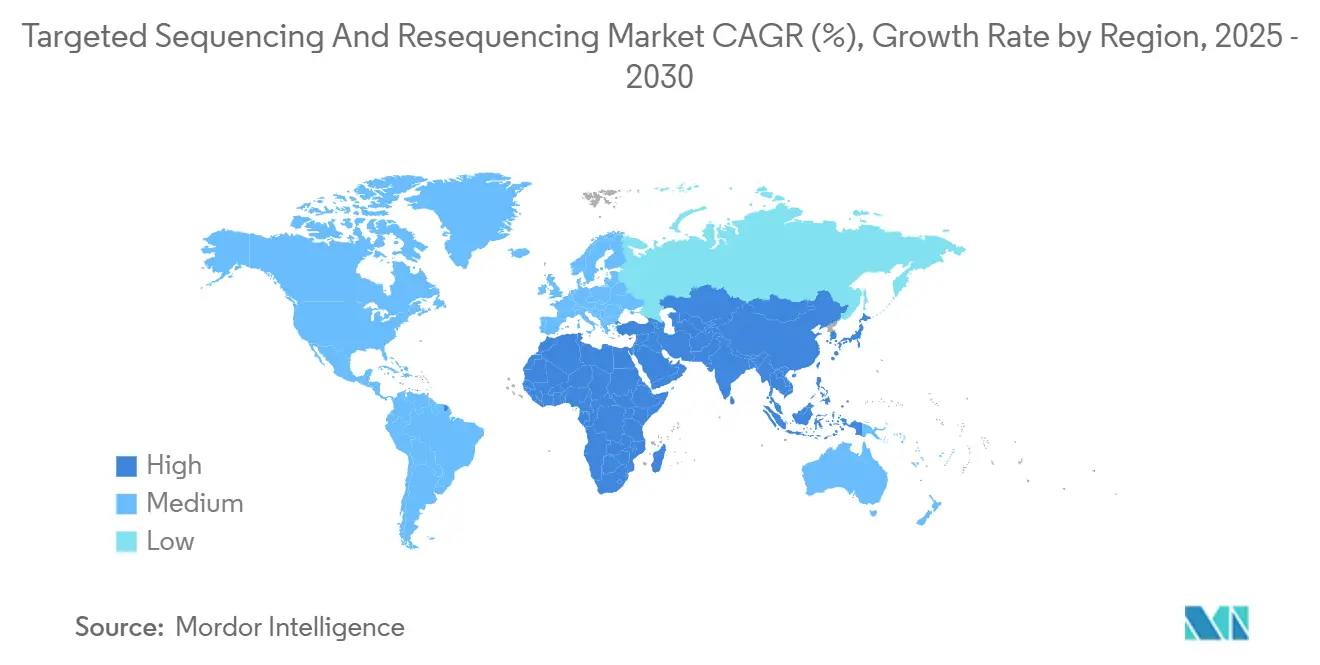

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Targeted Sequencing And Resequencing Market Analysis by Mordor Intelligence

The Targeted Sequencing And Resequencing Market size is estimated at USD 9.81 billion in 2025, and is expected to reach USD 27.37 billion by 2030, at a CAGR of 22.78% during the forecast period (2025-2030).

Accelerating cost declines in next-generation sequencing, clearer companion diagnostic regulations, and CRISPR-based enrichment workflows are expanding the routine clinical use of these technologies. Illumina’s NovaSeq X pushed raw consumable cost to USD 200 per genome in 2024, while Ultima Genomics trimmed cost-of-goods by a further 30% through unpatterned flow cells. Oncology continues to anchor test volume, but newborn genomic screening pilots and rare-disease programs are widening the customer base. Regional momentum is shifting as Asia-Pacific laboratories scale precision-medicine services and attract price-sensitive pharmaceutical outsourcing. Competitive intensity is rising as Element Biosciences, Oxford Nanopore, and other challengers target gaps in price, read length, and workflow automation.

Key Report Takeaways

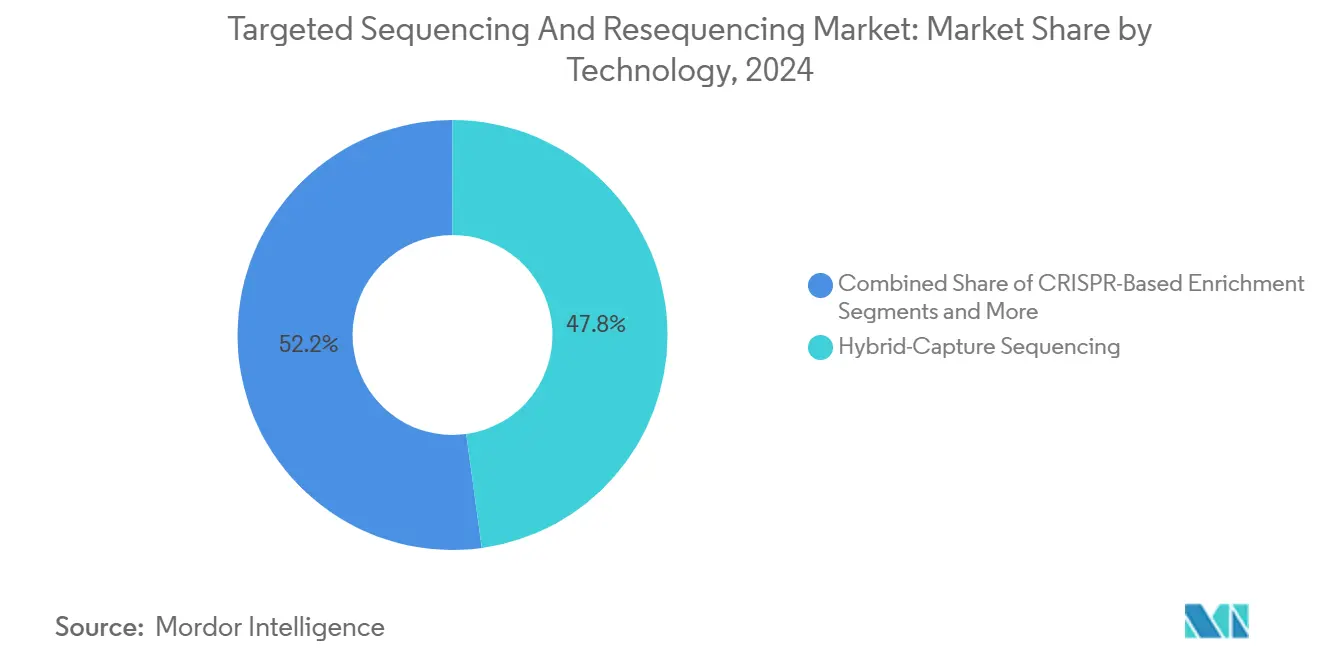

- By technology, hybrid-capture sequencing held 47.82% of the targeted sequencing and resequencing market share in 2024, while CRISPR-based enrichment is poised to grow at the fastest rate, with a 26.36% CAGR through 2030.

- By sample type, DNA dominated with 69.42% revenue share in 2024, whereas RNA sequencing is projected to accelerate at a 25.87% CAGR to 2030.

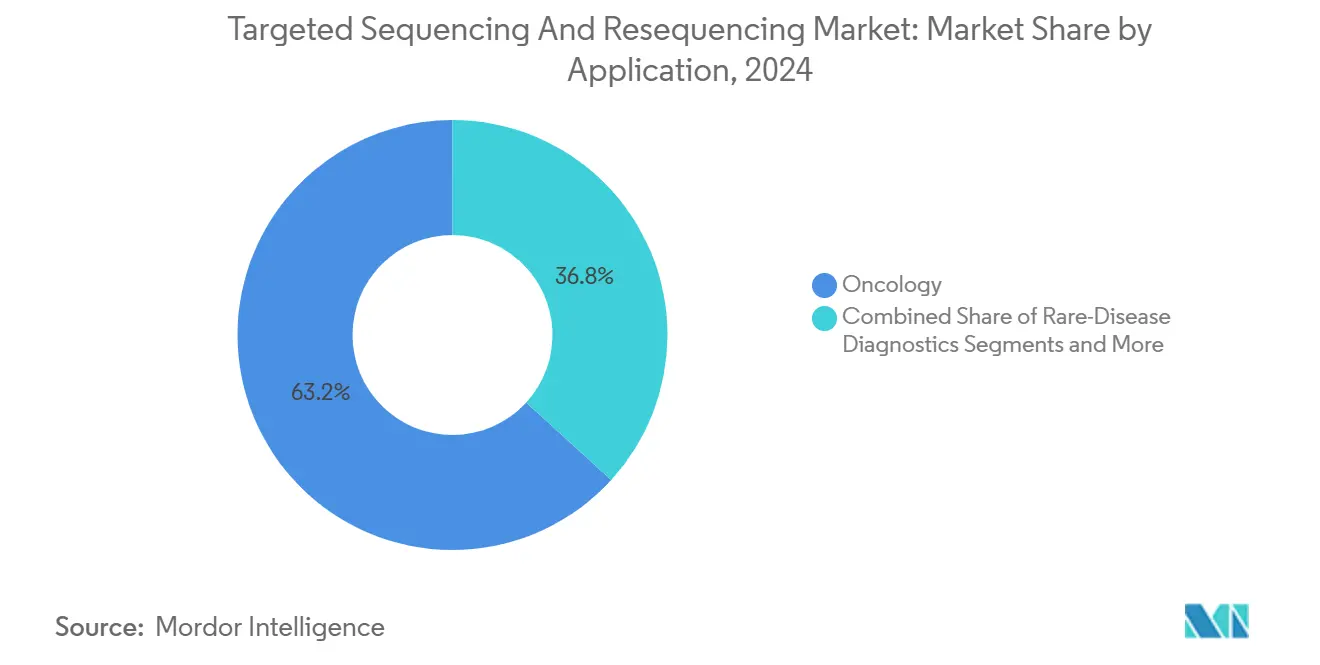

- By application, oncology commanded 63.22% of the 2024 targeted sequencing and resequencing market, yet rare-disease diagnostics is forecast to grow at a 24.78% CAGR through 2030.

- By end user, clinical and diagnostic laboratories led with a 56.86% share in 2024, while pharmaceutical and biotech companies are projected to post the highest 24.63% CAGR from 2024 to 2030.

- By geography, North America contributed 41.23% of the revenue in 2024; the Asia-Pacific region is set to expand at a 24.33% CAGR over the forecast period.

Global Targeted Sequencing And Resequencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling NGS costs and throughput gains | +4.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising oncology panel testing in clinical labs | +3.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Regulatory approvals for companion diagnostics | +3.1% | North America and EU | Medium term (2-4 years) |

| Expanded reimbursement for hereditary cancer panels | +2.7% | North America, extending to Asia-Pacific | Long term (≥ 4 years) |

| CRISPR-Cas–based target-enrichment workflows | +2.9% | Global, early adoption in research hubs | Long term (≥ 4 years) |

| Expansion of newborn genomic screening pilots | +2.1% | United Kingdom, United States, select Asia-Pacific nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling NGS Costs & Throughput Gains

Rapid cost compression is making broad panels economically comparable with single-gene assays. Ultima Genomics reached sub-USD 100 whole-genome costs in 2024, and Illumina’s NovaSeq X lowered per-sample expense by 60% compared with earlier systems.[1]Labcorp, “Labcorp Expands Collaboration With Ultima Genomics,” Labcorp, labcorp.com Labcorp scaled molecular residual disease testing after partnering with Ultima Genomics, showing how lower consumable spend unlocks new clinical services. Higher lane densities shorten run times, improving turnaround that once favored PCR. Cost and speed gains together help hospitals fold comprehensive profiling into routine oncology pathways. These dynamics underpin sustained double-digit expansion in the targeted sequencing and resequencing market.

Rising Oncology Panel Testing in Clinical Labs

Therapy guidelines now require concurrent analysis of multiple genes, prompting laboratories to replace serial single-marker tests with pan-cancer panels. The U.S. FDA classified NGS tumor-profiling assays as Class II devices in 2024, clarifying validation expectations and accelerating uptake.[2]Food and Drug Administration, “21 CFR 866.6080—NGS Tumor Profiling Test,” U.S. Food and Drug Administration, fda.gov FoundationOne CDx already spans 300 genes and carries seven breast-cancer companion indications, illustrating the breadth clinicians demand.[3]Foundation Medicine, ''FDA Approves FoundationOne Liquid CDx for PIK3CA Detection,” Foundation Medicine, foundationmedicine.com Liquid biopsy advances allow iterative monitoring without tissue re-biopsy, and AI interpretation tools reduce the informatics load on pathology teams. Collectively, these factors lift routine panel ordering volumes in oncology clinics worldwide.

Regulatory Approvals for Companion Diagnostics

The FDA’s accelerated pathways encourage drug developers to bind trials to genomic biomarkers tightly, thereby boosting demand for validated panels—FoundationOne Liquid CDx secured clearance in 2024 for PIK3CA mutation detection in breast cancer patients receiving inavolisib therapy. Parallel review by the European Medicines Agency harmonizes standards across key markets, widening commercial reach. Larger panel complexity increases the compliance burden, favoring vendors with extensive regulatory teams. Requirements for real-world evidence also privilege companies that manage longitudinal genomic datasets. These dynamics collectively add momentum to the targeted sequencing and resequencing market.

CRISPR-Cas–Based Target-Enrichment Workflows

Programmable CRISPR guides deliver higher specificity in GC-rich or repetitive loci where hybrid-capture panels struggle. Customization cycles are measured in days rather than the weeks needed for probe synthesis, benefiting fast-moving research projects. Integration with long-read instruments improves structural variant detection that short reads miss. Machine learning now optimizes guide selection for efficiency, further raising performance ceilings. Licensing complexity around foundational patents may slow broad commercialization yet early adopters in translational labs are expanding use cases. These advantages position CRISPR enrichment for outsized growth inside the targeted sequencing industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital-equipment and service-contract costs | -2.8% | Global, pronounced in emerging markets | Short term (≤ 2 years) |

| Bioinformatics talent shortage and data bottlenecks | -3.2% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Patent-pool licensing restrictions on hybrid-capture probes | -1.9% | Global, focused in competitive markets | Long term (≥ 4 years) |

| Sample QC failures in FFPE tissues causing high repeat rates | -2.1% | Global, higher impact in resource-limited settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex & Service Contract Costs

Sequencers, automation lines, and annual service contracts require investments that many hospitals and regional labs cannot justify at current test reimbursements. Deferred purchases elongate replacement cycles, slowing uptake in mid-tier facilities. Leasing models ease upfront expense but increase lifetime cost, pressuring budgets. Emerging-market buyers face import duties and limited financing options, widening the digital divide. These hurdles moderate near-term growth even as technology costs fall.

Bioinformatics Talent Shortage & Data Bottlenecks

Clinical labs report a 40% vacancy rate for qualified genomic analysts, making data interpretation the primary operational bottleneck. The skills gap drives salary inflation and staff turnover that small labs cannot match. Cloud platforms offload compute demand, yet regulations still require human sign-off, preserving labor pressure. Data storage for whole-genome pipelines strains IT budgets, especially when retention policies mandate multiyear archiving. Unless workforce development accelerates, informatics constraints will temper expansion in the targeted sequencing and resequencing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: CRISPR Disrupts Hybrid-Capture Dominance

Hybrid-capture sequencing held a 47.82% share of the targeted sequencing and resequencing market in 2024, underscoring its long validation history in clinical labs. This technology anchors multigene oncology panels and enjoys a wide installed base of automation-ready protocols. Even so, CRISPR-based enrichment is expanding at a 26.36% CAGR through 2030, and its momentum is visible in translational centers that regularly update panels for novel biomarkers. The superior on-target rate of guide RNA–directed cleavage enhances performance in GC-rich loci, while shorter design cycles enable researchers to pivot quickly when new genes enter drug pipelines. Vendors now bundle AI software that predicts guide efficiency, reducing wet-lab iterations and speeding time to result.

Workflow innovation is also reshaping economics. In 2025, several core facilities reported a 40% drop in consumable spend after shifting repetitive-region assays from hybrid-capture to CRISPR enrichment, a saving that amplified throughput gains delivered by NovaSeq X patterned flow cells. Meanwhile, amplicon sequencing retains its niche for hotspot mutation testing where panel sizes are under 50 kilobases and turnaround must stay below 24 hours. Molecular inversion probes continue to support large population-genetics studies because the circular capture design lowers reagent cost per sample at scale. Collectively, these forces keep technology diversification high even as CRISPR captures incremental share inside the targeted sequencing and resequencing market.

By Sample Type: RNA Growth Accelerates Despite DNA Dominance

DNA maintained a commanding 69.42% share of the targeted sequencing and resequencing market in 2024, reflecting mature regulatory guidance and stable reimbursement for variant detection in oncology. Hospitals also lean on existing DNA extraction workflows, minimizing change-management hurdles. Still, RNA sequencing is advancing rapidly, growing at a 25.87% CAGR as drug developers seek expression signatures that predict immunotherapy response. Pharmaceutical sponsors now incorporate transcriptomic endpoints into Phase II trials, generating consistent demand for clinical-grade RNA workflows. The cost per sample remains higher than for DNA due to ribosomal RNA depletion and quality-control steps; yet, sponsors are willing to pay the premium when gene-expression data accelerate go/no-go decisions.

Technical progress is narrowing the gap. Enzymatic repair kits that reverse formalin cross-links in FFPE RNA lifted usable-read counts by 30% in 2024, improving pass rates for archival samples. Cell-free RNA protocols entered early adopter clinics, where non-invasive monitoring of allograft rejection reduced biopsy frequency in kidney-transplant recipients. Oxford Nanopore’s duplex reads further lowered error rates, encouraging laboratories to test long-read RNA for fusion-gene detection. These advances collectively push RNA toward double-digit share by 2030, reinforcing the long-term growth profile of the targeted sequencing and resequencing market.

By Application: Rare-Disease Diagnostics Challenge Oncology Leadership

Oncology accounted for 63.22% of the targeted sequencing and resequencing market share in 2024, driven by guideline-linked reimbursement and the routine use of multigene panels in the selection of solid-tumor therapies. Volume also benefits from the rising adoption of liquid biopsies, which enables clinicians to track tumor evolution without requiring repeat tissue sampling. However, rare-disease diagnostics is posting the fastest 24.78% CAGR, driven by newborn genomic-screening pilots and expanded orphan-drug pipelines. U.S. payers now cover trio-based exome sequencing for infants in neonatal intensive care units, which is expected to increase test volumes at regional children’s hospitals.

Rare-disease programs also carry strategic importance for pharmaceutical companies because genomic diagnoses funnel patients into targeted-therapy trials. This virtuous cycle explains why biotech sponsors are underwriting sequencing costs in early access programs. Reproductive-health testing continues steady adoption, moving beyond aneuploidy to inherited single-gene disorders. Meanwhile, agrigenomics remains a specialized yet durable revenue stream for service providers operating outside the regulated clinical space. Together, this mix keeps oncology dominant yet gradually cedes share as emerging applications broaden the customer set of the targeted sequencing and resequencing market.

By End User: Pharma-Biotech Adoption Accelerates

Clinical and diagnostic laboratories held 56.86% of the targeted sequencing and resequencing market in 2024, buoyed by established payer contracts and CLIA-certified workflows. Routine ordering of hereditary cancer panels and solid tumor profiles fills sequencer capacity in these labs. Pharmaceutical and biotech companies, however, are the fastest-growing customers, with a 24.63% CAGR, because biomarker-stratified trials now dominate oncology pipelines. Sponsors often run tumor-normal sequencing at baseline, conduct longitudinal liquid biopsies, and perform RNA expression panels—all within the same study—multiplying the sample demand.

Academic centers remain vanguards of method development, but they face grant-cycle funding constraints that temper their absolute revenue contribution. Contract research organizations are filling the gap by winning multi-year sequencing contracts tied to Phase III trial execution. GeneDx’s April 2025 purchase of Fabric Genomics for USD 33 million illustrates the push to internalize AI interpretation, enabling reports to meet regulatory timelines without expanding labor headcount. End-user dynamics therefore reinforce volume diversity, an advantage that stabilizes year-over-year revenue for suppliers in the targeted sequencing and resequencing market.

Geography Analysis

North America generated 41.23% of 2024 revenue, making it the largest regional block within the targeted sequencing and resequencing market size. The U.S. landscape benefited from Medicare’s broader coverage of hereditary cancers and the FDA’s standardized oversight of laboratory-developed tests. These policies lowered adoption barriers and provided reimbursement certainty, spurring mid-tier hospitals to install mid-throughput instruments. Yet the region faces wage inflation for bioinformatics professionals, which raises total test costs and nudges some outsourcing to lower-cost providers abroad. Strengthening of U.S.-centric companion-diagnostic submissions nevertheless ensures a durable domestic pipeline of new panels.

The Asia-Pacific region is the growth engine, advancing at a 24.33% CAGR as national precision-medicine initiatives scale. China’s BGI Genomics rebounded after earlier regulatory scrutiny, leveraging export-compliant DNBSEQ instruments to win tenders in Southeast Asia. Japan’s reimbursement of tumor-agnostic panels and South Korea’s National Biobank expansion further widen the addressable volume. India’s contract-research sector offers cost-efficient genomic testing to global pharma, redirecting trial samples that once flowed to U.S. central labs. Regional diversity imposes regulatory fragmentation, yet local validation studies increasingly adopt global quality frameworks, smoothing market entry. These trends collectively position Asia-Pacific for incremental share gains inside the targeted sequencing and resequencing market.

Europe maintains steady momentum underpinned by the European Medicines Agency’s synchronized review of drugs and companion diagnostics. National health-technology-assessment bodies in Germany and France now recognize genomic profiling’s budget impact beyond oncology, opening paths for cardiogenomics and metabolic-disorder panels. However, slower economic growth constrains capital budgets, delaying instrument refresh cycles. Latin America and the Middle East & Africa remain nascent but show rising import volumes for reagent rental systems that minimize upfront spend. Together, these regions contribute diversification that cushions currency or policy shocks affecting any single geography.

Competitive Landscape

The targeted sequencing and resequencing market exhibits moderate concentration. Illumina, Thermo Fisher Scientific, and Agilent collectively controlled roughly half of 2024 reagent revenue, but challengers are closing the gap. Element Biosciences raised USD 277 million in 2024 to commercialize a sequencing-by-synthesis chemistry designed to avoid Illumina patents, placing pressure on consumable pricing. Oxford Nanopore and Pacific Biosciences dominate the long-read niche, resolving structural variants and full-length RNA isoforms. Patent litigation remains active; Illumina continues to contest Element Biosciences' filings related to dye-terminator cleavage, while BGI’s U.S. subsidiary faces injunctions limiting certain flowcell imports.

Strategic moves highlight vertical integration. Illumina’s June 2025 acquisition of SomaLogic for USD 425 million broadens its multiomics reach into proteomics, aiming to secure reagent pull-through across DNA and protein assays. Singular Genomics accepted a USD 20-per-share buyout by Deerfield Management in December 2024, a deal that provides cash to complete the clinical-grade validation of its G4 sequencer. MGI Tech’s 2024 partnership with SeqOne embeds tertiary analysis into its bioinformatics stack, addressing the informatics bottleneck that slows many mid-volume labs. These actions indicate a race to own end-to-end workflows in the targeted sequencing and resequencing market.

Pricing strategy is evolving. Larger vendors offer reagent-rental contracts that bundle instruments, service, and software into per-sample fees, shifting cap-ex to op-ex and locking customers into multiyear agreements. Smaller entrants counter with modular platforms that avoid proprietary consumables, appealing to price-sensitive laboratories in emerging markets. Software pure-plays such as DNAnexus and Intelliseq are indispensable partners; their cloud pipelines slash analysis turnaround from days to hours while meeting HIPAA and GDPR compliance. Competitive positioning therefore hinges not only on read accuracy or cost but on ecosystem breadth that simplifies daily lab operations in the targeted sequencing and resequencing market.

Targeted Sequencing And Resequencing Industry Leaders

Agilent Technologies Inc.

BGI Genomics Co., Ltd.

F. Hoffmann-La Roche Ltd

Illumina Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina acquired SomaLogic for up to USD 425 million to expand into proteomics with the SomaScan platform.

- April 2025: Illumina and Tempus AI entered a strategic partnership to accelerate AI-driven NGS test adoption.

- April 2025: GeneDx completed the acquisition of Fabric Genomics for USD 33 million to scale decentralized AI-powered testing.

Global Targeted Sequencing And Resequencing Market Report Scope

| Hybrid-Capture Sequencing |

| Amplicon Sequencing |

| CRISPR-Based Enrichment |

| Molecular Inversion Probes |

| DNA |

| RNA |

| Oncology |

| Rare-Disease Diagnostics |

| Reproductive Health & NIPT |

| Agrigenomics & Plant Breeding |

| Infectious-Disease Surveillance |

| Academic & Research Institutes |

| Clinical & Diagnostic Labs |

| Pharmaceutical & Biotech Companies |

| CROs & Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Hybrid-Capture Sequencing | |

| Amplicon Sequencing | ||

| CRISPR-Based Enrichment | ||

| Molecular Inversion Probes | ||

| By Sample Type | DNA | |

| RNA | ||

| By Application | Oncology | |

| Rare-Disease Diagnostics | ||

| Reproductive Health & NIPT | ||

| Agrigenomics & Plant Breeding | ||

| Infectious-Disease Surveillance | ||

| By End User | Academic & Research Institutes | |

| Clinical & Diagnostic Labs | ||

| Pharmaceutical & Biotech Companies | ||

| CROs & Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the targeted sequencing and resequencing market expected to grow through 2030?

It is forecast to expand from USD 9.81 billion in 2025 to USD 27.37 billion by 2030, reflecting a 22.78% CAGR.

Which technology is gaining share the quickest?

CRISPR-based enrichment is the fastest-growing segment, advancing at a 26.36% CAGR as it overcomes hybrid-capture limitations.

Why is Asia-Pacific attracting attention from sequencing vendors?

Government-funded precision-medicine initiatives, large population size, and lower operating costs are driving a 24.33% CAGR in the region.

What is the main operational bottleneck for laboratories?

A 40% vacancy rate for qualified bioinformatics staff creates data-analysis delays despite improvements in cloud pipelines.

How are pharmaceutical companies using targeted sequencing?

Sponsors embed multigene DNA and RNA panels into clinical trials to stratify patients, monitor treatment response, and accelerate drug-approval timelines.

Page last updated on: