Bioprocess Containers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

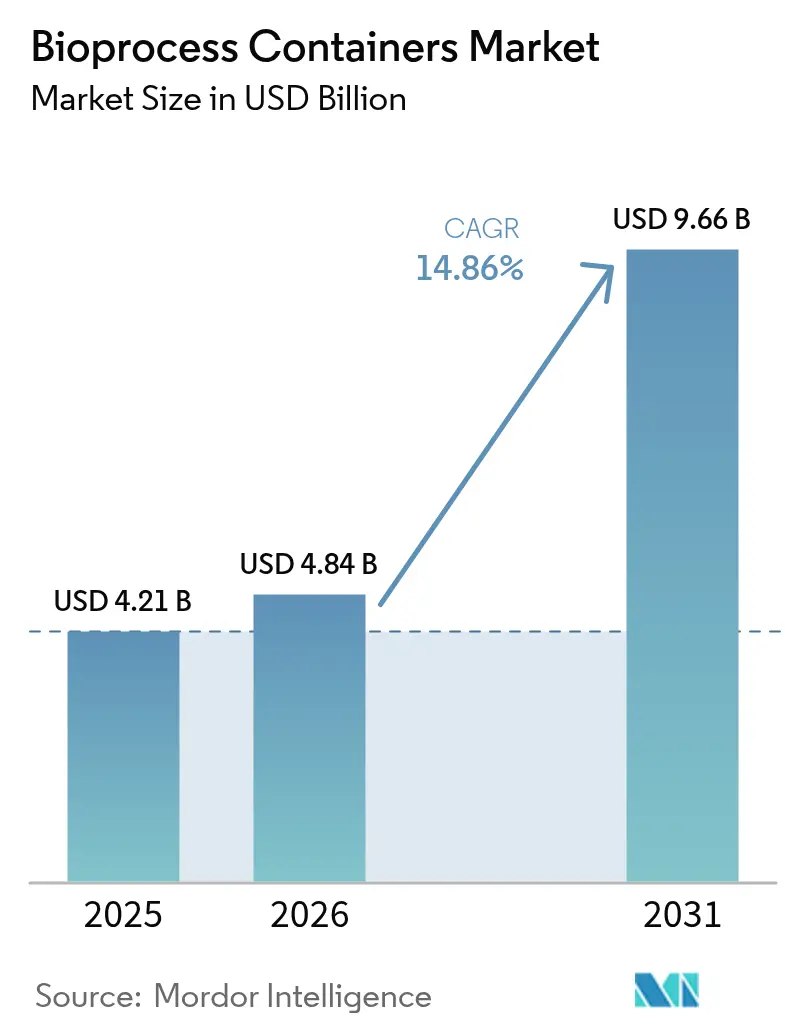

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 9.66 Billion |

| Growth Rate (2026 - 2031) | 14.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioprocess Containers Market Analysis by Mordor Intelligence

The bioprocess containers market size is expected to grow from USD 4.21 billion in 2025 to USD 4.84 billion in 2026 and is forecast to reach USD 9.66 billion by 2031 at 14.86% CAGR over 2026-2031. Rapid adoption of flexible manufacturing, pandemic-ready capacity planning, and lower capital outlays versus stainless-steel systems continue to reinforce demand for single-use containers. Biopharmaceutical manufacturers favor the technology for its proven ability to minimize cross-contamination while supporting accelerated product changeovers. Regulatory authorities now encourage closed, disposable processing trains that inherently align with automated, data-rich production lines. Together, these forces underscore how the bioprocess containers market is moving from niche installations toward mainstream status across commercial and clinical facilities.

Key Report Takeaways

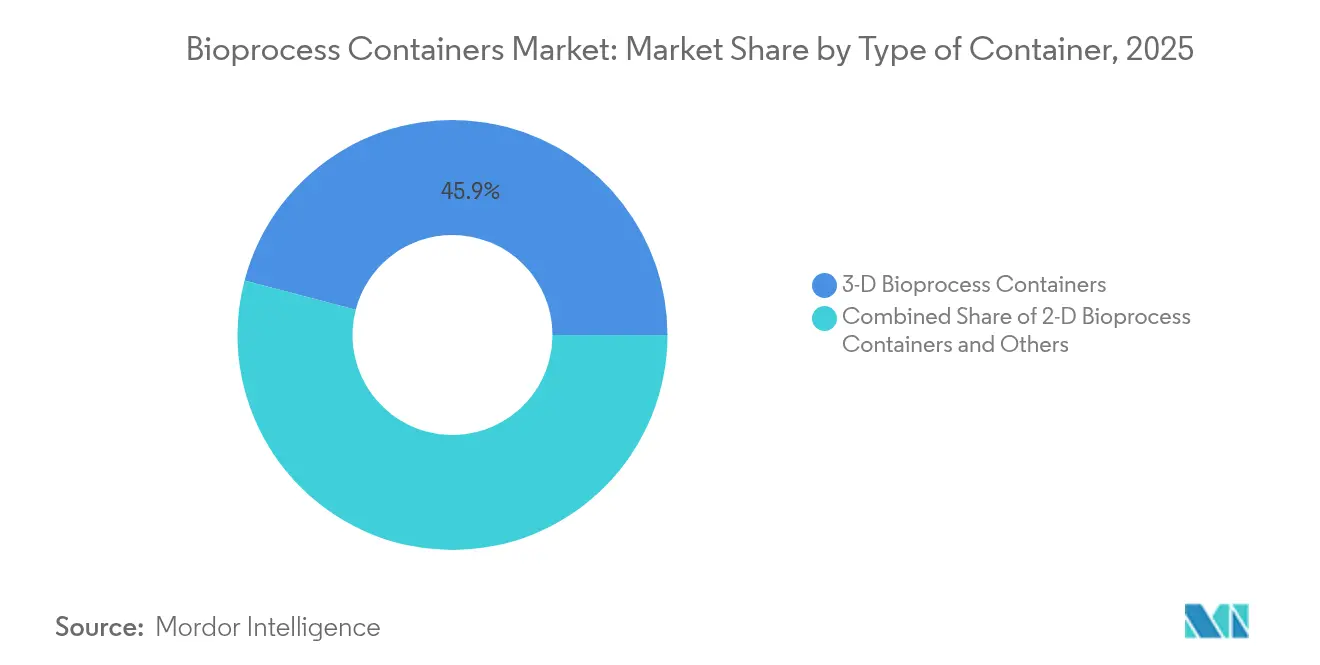

- By type, 3-D containers commanded 45.92% of bioprocess containers market share in 2025, while 2-D containers are advancing at 15.23% CAGR through 2031.

- By application, upstream processing held 54.56% share of the bioprocess containers market size in 2025, whereas downstream processing is forecast to expand at 15.62% CAGR to 2031.

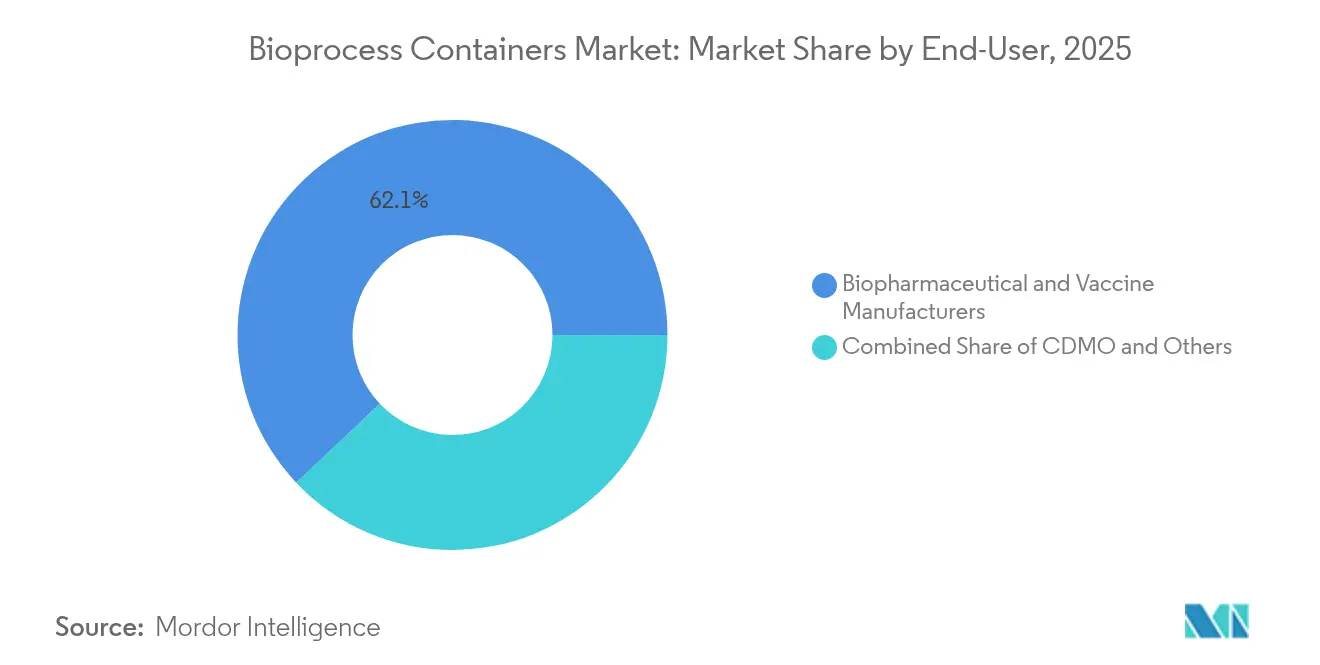

- By end-user, biopharmaceutical and vaccine manufacturers accounted for 62.05% revenue share in 2025; the CDMO segment is projected to record the fastest growth at 15.94% CAGR to 2031.

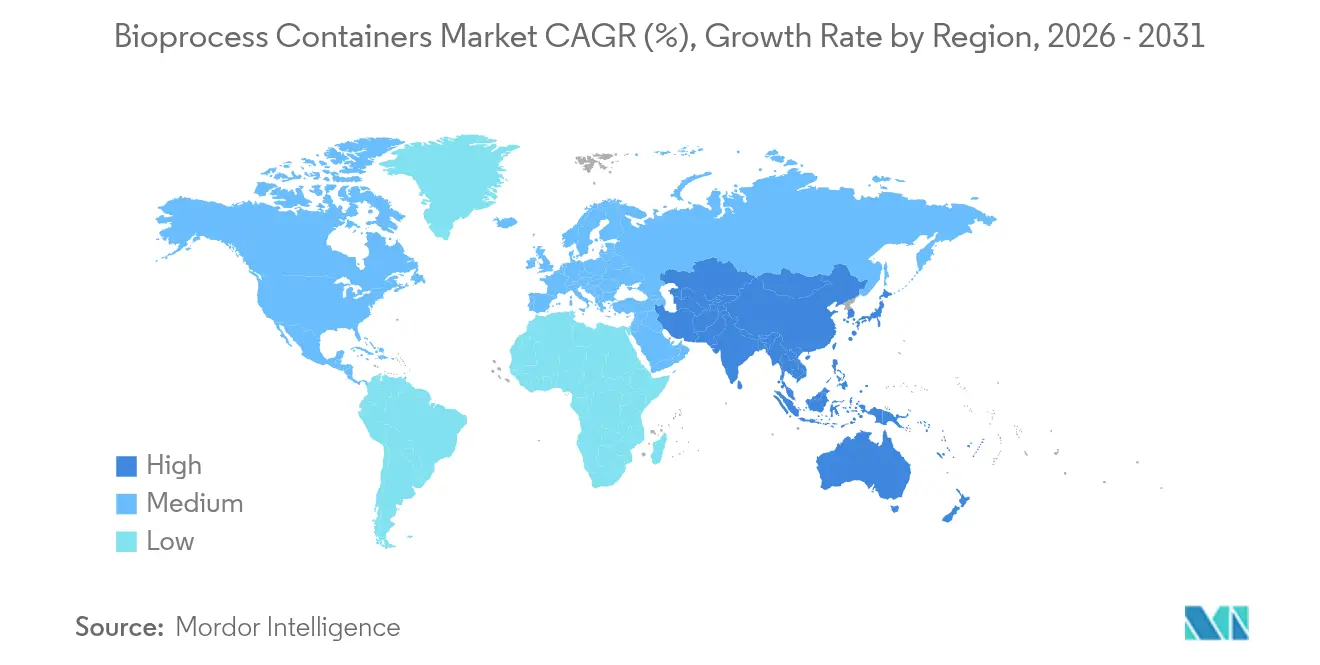

- By geography, North America led with 43.15% share in 2025, while Asia-Pacific is set to exhibit the highest regional CAGR at 16.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioprocess Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Biologics Pipeline Expansion | +2.8% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Shift Toward Single-Use Platforms In CDMO | +2.1% | Global, accelerated in Asia-Pacific | Medium term (2-4 years) |

| Pandemic-Driven Vaccine Capacity Build-Out | +1.9% | Global, with emphasis on strategic regions | Short term (≤ 2 years) |

| Growing mRNA Therapeutics Fill-Finish Demand | +2.4% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Adoption In Continuous Bioprocessing Skids | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| ESG Push For Lower Energy & Water Footprints | +1.7% | Global, with stringent requirements in EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Biologics Pipeline Expansion

More than 7,000 biologic molecules were in clinical development during 2024, and the scale of this pipeline is pushing facilities to embrace disposable processing trains that avoid costly cleaning validations. The flexibility of the bioprocess containers market enables simultaneous campaigns for monoclonal antibodies, antibody-drug conjugates, and other complex modalities without cross-over risk. Samsung Biologics’ expansion to 784,000 L capacity in 2025 illustrates how leading CDMOs are investing in large volumes of disposable reactors to satisfy diversified client pipelines. Personalized and orphan therapeutics, often produced in small batches, particularly rely on single-use containers to remain economically viable. As these molecules progress to late-phase trials, sustained container demand is expected well into the next decade.

Shift Toward Single-Use Platforms in CDMO

Contract developers now redesign greenfield plants around disposable systems to shorten tech-transfer cycles and defer heavy capital spending. The BIOSECURE Act’s scrutiny of China-centric supply chains is prompting U.S. sponsors to pivot toward domestic or ally-based CDMOs equipped with flexible, single-use suites. Lonza’s USD 1.2 billion purchase of a Californian biologics site underscores the scale of investment being funneled into modular, disposable infrastructure. Rapid campaign changeovers, lower contamination risk, and simplified scale-out strategies mean CDMOs can secure multi-product contracts and improve asset utilization. Consequently, the bioprocess containers market is garnering incremental volumes from outsourced production pipelines previously dominated by fixed stainless-steel assets.

Pandemic-Driven Vaccine Capacity Build-Out

The race to supply COVID-19 vaccines validated single-use technology as the fastest route to market-ready capacity, a lesson now embedded in national preparedness roadmaps. Facilities erected in 2020-2022 continue operating for routine vaccines, complex viral vectors, and booster programs, maintaining container demand beyond acute pandemic needs. Fujifilm Diosynth’s USD 1.6 billion expansion in Denmark integrates fully disposable upstream and downstream modules, proving that governments and private partners see single-use as strategic infrastructure. Continuous bioprocessing combined with single-use reactors further amplifies throughput while retaining agility. This sustained capacity build directly enlarges the installed base driving recurring container consumption.

Growing mRNA Therapeutics Fill-Finish Demand

mRNA pipelines now span oncology, protein replacement, and gene-editing indications that require high-integrity fill-finish operations. Disposable bags and liners minimize nucleic-acid adsorption and particle load, critical for lipid-nanoparticle encapsulated products. ProBio’s 3-month GMP plasmid DNA service leverages pre-sterilized single-use vessels to guarantee turnaround times that stainless-steel lines cannot match. Investments by Merck KGaA in an advanced mRNA research center further cement long-term adoption of container formats tailored for small-volume, high-value batches. The bioprocess containers market therefore remains tightly coupled to the evolving messenger RNA manufacturing ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Outlay For GMP-Grade Polymer Films | -1.6% | Global, with acute impact in emerging markets | Medium term (2-4 years) |

| Leachables / Extractables Compliance Burden | -1.2% | Global, with stringent requirements in US & EU | Long term (≥ 4 years) |

| Supply-Chain Volatility In Pharma-Grade Resins | -1.1% | Global, with critical dependencies in Asia-Pacific | Short term (≤ 2 years) |

| End-Of-Life Waste-Management Liabilities | -0.9% | Global, with acute pressure in EU & emerging regulations in US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay For GMP-Grade Polymer Films

Manufacturing multilayer films that satisfy pharmaceutical GMP needs involves specialized extrusion lines, clean-room environments, and advanced analytical labs that elevate upfront cost by 40-60% relative to non-GMP plants. Supply concentration in a handful of resin producers exposes end-users to price premiums and allocation risk. Sartorius’ ISCC Plus certification for bio-based polymers shows additional investment now required to meet circularity targets alongside GMP obligations. Smaller regional suppliers face steep financial barriers, limiting geographic diversification and keeping film pricing elevated through mid-decade.

Leachables / Extractables Compliance Burden

Revisions to FDA and EMA guidance in 2024 heightened documentation and long-term stability test requirements for disposable assemblies [1]GMP Journal, “The GMP Update 2023/2024,” gmp-journal.com . Sophisticated mass-spectrometry protocols, toxicological risk assessments, and product-specific interaction studies can prolong container qualification by up to 18 months, delaying commercial deployment. High analytical workloads exacerbate talent shortages in polymer science and regulatory chemistry. Although large vendors offer standardized data packages, niche or custom bags still undergo lengthy validation, tempering overall adoption speed within the bioprocess containers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Container: Scale Benefits of 3-D and Flexibility Gains of 2-D

3-D bioprocess containers preserved 45.92% of bioprocess containers market share in 2025 on the strength of large-volume reactor applications where structural support and bag integrity are critical. They dominate fed-batch monoclonal antibody production, providing up to 6,000 L working volumes in modular, disposable format. Yet growth momentum tilts toward 2-D flat-panel bags, expanding at 15.23% CAGR as perfusion and continuous culture gain mainstream acceptance. These lower-profile vessels improve oxygen transfer rates and integrate seamlessly with automated rocking platforms, supporting intensified upstream workflows.

Advances in multilayer films and gamma-stable sensors are narrowing historical performance gaps between bag geometries. Corning’s HYPERStack family offers scalable surface area for adherent cultures while retaining single-use convenience, broadening 2-D utility into viral vector and vaccine production. Hybrid concepts that merge baffle structures from 3-D bags with monitoring ports from 2-D panels are beginning to surface, targeting cell-gene factories where space constraints and sterility assurance converge. Collectively, the container type landscape illustrates how the bioprocess containers market continues to innovate around both volume scalability and process-specific flexibility.

By Application: Upstream Dominance With Downstream Acceleration

Upstream unit operations held 54.56% of the bioprocess containers market size in 2025, affirming the long-proven compatibility between disposable bioreactors and mammalian cell culture. Eliminating CIP and SIP steps reduces turnaround by several hours per batch, translating into higher facility throughput and greater multiproduct agility. Nevertheless, downstream processing is now the fastest-rising niche, projected at 15.62% CAGR as single-use chromatography columns, buffer bags, and virus-inactivation tanks gain regulatory acceptance.

Continuous downstream trains using alternating-tangential-flow filtration and disposable polishing columns are allowing facilities to pair perfusion reactors with equally agile purification. Fill-finish suites for cell and gene therapies increasingly depend on pre-sterilized liners and manifolds that protect ultra-low-volume, high-value batches from environmental excursions. These developments confirm that the bioprocess containers market is migrating beyond its upstream comfort zone to support end-to-end disposable manufacturing.

By End-User: Biopharma Core and CDMO Upswing

Biopharmaceutical and vaccine producers commanded 62.05% revenue share in 2025, underpinning the centrality of owner-operated facilities to container demand. Big Pharma’s push toward modality diversity—spanning ADCs, fusion proteins, and viral vectors—elevates the need for multipurpose cleanrooms where single-use bags facilitate faster molecule turnover.

CDMOs, however, represent the expansion frontier, rising at 15.94% CAGR as outsourcing becomes a preferred risk-mitigation strategy. These service providers invest in standardized, flexible suites that accommodate fluctuating customer pipelines, making them avid consumers in the bioprocess containers industry. Emerging CDMOs targeting advanced therapies, such as plasmid DNA and mRNA, frequently build entire greenfield sites without fixed stainless assets, reinforcing a secular shift in procurement patterns.

Geography Analysis

North America retained 43.15% share of the bioprocess containers market in 2025, supported by entrenched biotech clusters in Boston, San Francisco, and Raleigh-Durham that prioritize rapid scale-up and stringent cGMP compliance. Federal incentives aimed at reshoring critical drug supply further energize regional adoption, while a robust venture capital ecosystem finances start-ups that default to disposable technology. Canada’s Montreal hub and Mexico’s emerging biologics corridor supply additional throughput, integrating regional supply chains.

Asia-Pacific is forecast to post a 16.2% CAGR through 2031, the fastest regional trajectory in the bioprocess containers market. China’s commitment of USD 4.17 billion for biomanufacturing capacity in 2025, coupled with India’s aggressive push for global GMP accreditation, is unleashing a wave of facility construction that specifies single-use systems from inception. South Korea, Japan, and Singapore contribute advanced regulatory frameworks and high-tech talent pools, forming a diversified ecosystem that reduces dependence on Western supply routes.

Europe remains a center of pharmaceutical excellence, with Germany, France, and the United Kingdom pioneering sustainable manufacturing models that dovetail with disposable platforms. Updated EMA GMP guidelines emphasizing closed operations encourage plants to retrofit stainless skids with bag-based alternatives. Government-supported green initiatives, such as reduced water-usage mandates, favor single-use over legacy CIP-intensive equipment. Meanwhile, Middle East & Africa and South America exhibit nascent but promising adoption rates as governments seek domestic vaccine sovereignty, positioning these territories as long-term growth reservoirs for the bioprocess containers market.

Competitive Landscape

Moderate consolidation defines the current competitive hierarchy. Danaher’s USD 7.5 billion integration of Cytiva and Pall created a vertically aligned portfolio spanning filters, chromatography, and 2-D/3-D bags. Thermo Fisher Scientific and Sartorius AG follow similar one-stop strategies, combining analytics, automation, and consumables to embed themselves across customer workflows.

Material-science specialists such as Saint-Gobain Life Sciences and Entegris differentiate via high-purity polymer formulations, barrier-layer engineering, and advanced port weldability that resist extractables. These attributes resonate with cell and gene therapy producers seeking hyper-sterile, small-volume solutions, carving profitable niches outside the scope of large platform vendors.

Collaborative development agreements are proliferating, evidenced by Sartorius’ work with LFB Biomanufacturing on integrated cell-line development services [3]Sartorius, “First ISCC Plus Certifications Pave the Way for Renewable Plastics,” sartorius.com . Sustainability also drives competition: ISCC Plus-certified resin usage, recyclable packaging, and lower-carbon sterilization methods like X-ray or E-beam are becoming procurement criteria. Patent filings covering multilayer film architecture and real-time sensor-embedded bags underscore sustained R&D spend aimed at locking customers into proprietary ecosystems within the bioprocess containers market.

Bioprocess Containers Industry Leaders

Thermo Fisher Scientific Inc

Saint-Gobain S.A.

Lonza Group AG

Avantor Inc

Danaher Corporation (Cytiva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ProBio launched a guaranteed 3-month GMP plasmid DNA manufacturing service using exclusively single-use platforms.

- November 2024: Sartorius opened its Center for Bioprocess Innovation in Marlborough, Massachusetts, to accelerate disposable technology co-development with clients.

- November 2023: ALLpaQ Packaging Group appointed Alflow Scandinavia as exclusive Scandinavian distributor for its all-plastic bioprocess container range.

Global Bioprocess Containers Market Report Scope

Bioprocess containers are the disposable, flexible container systems used to catalyze ongoing bioprocesses and aid in storing sterile media in the biopharmaceutical and life sciences industries.

The Bioprocess Containers Market is Segmented by Type of Containers (2D Bioprocess Containers, 3D Bioprocess Containers, and Other Types of Containers), Application (Upstream Process, Downstream Process, Process Development), End-Users (Biopharmaceutical Companies, Life Science R&D Companies, and Other End-Users), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America Brazil, Argentina, and Rest of South America)). The report offers value (in USD) for the above segments.

| 2-D Bioprocess Containers |

| 3-D Bioprocess Containers |

| Others |

| Upstream Processing |

| Downstream Processing |

| Process Development / Scale-up |

| Fill-Finish Operations |

| Biopharmaceutical & Vaccine Manufacturers |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type of Container | 2-D Bioprocess Containers | |

| 3-D Bioprocess Containers | ||

| Others | ||

| By Application | Upstream Processing | |

| Downstream Processing | ||

| Process Development / Scale-up | ||

| Fill-Finish Operations | ||

| By End-User | Biopharmaceutical & Vaccine Manufacturers | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Bioprocess Containers Market size?

The market stands at USD 4.84 billion in 2026 and is forecast to grow at a 14.86% CAGR to USD 9.66 billion by 2031.

Why are CDMOs important to future demand?

CDMOs outsource production for multiple sponsors, and their investment in fully disposable suites is driving a 15.94% CAGR segment growth to 2031.

Which region has the biggest share in Bioprocess Containers Market?

In 2025, the North America accounts for the largest market share in Bioprocess Containers Market.

Which container type currently dominates installations?

3-D bags lead with 45.92% share in 2025, although 2-D formats are growing faster at 15.23% CAGR.

Page last updated on: