Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

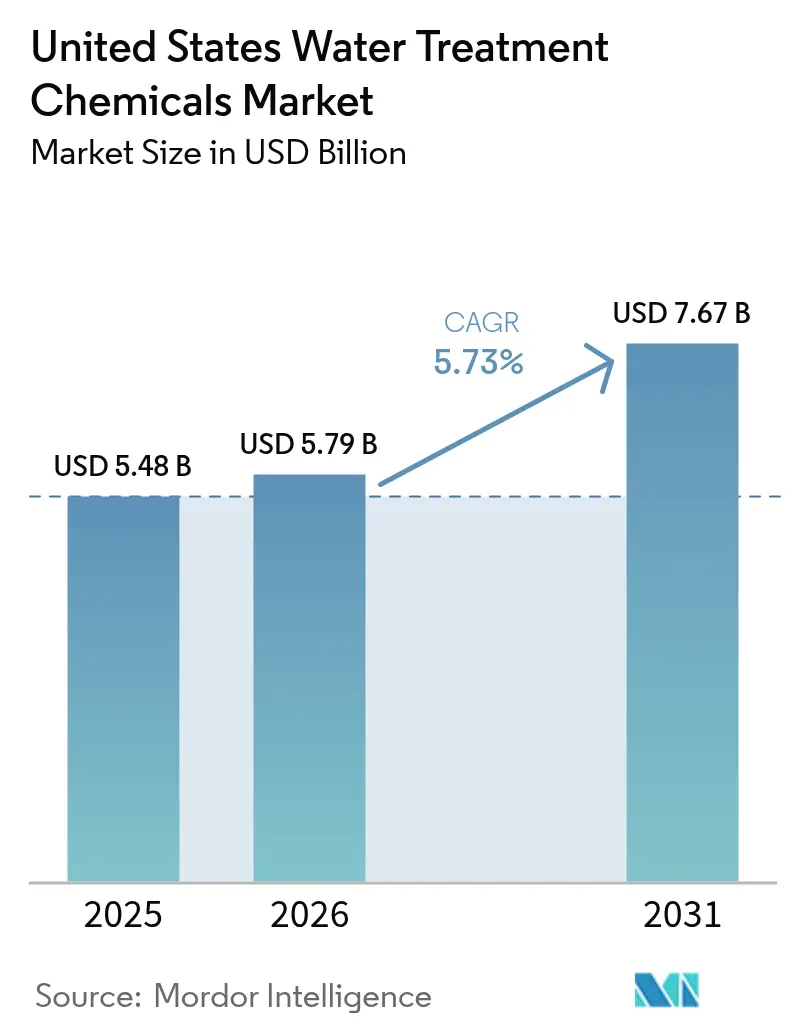

| Base Year Market Size (2025) | USD 5.48 Billion |

| Market Size (2026) | USD 5.79 Billion |

| Market Size (2031) | USD 7.67 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

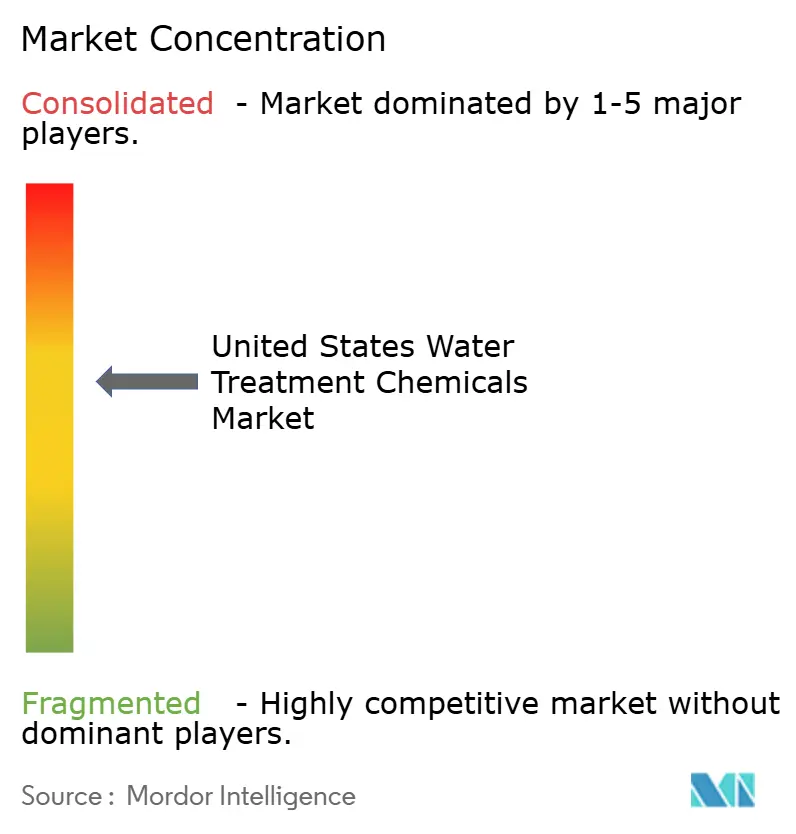

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Water Treatment Chemicals Market Analysis by Mordor Intelligence

The United States Water Treatment Chemicals Market size was valued at USD 5.48 billion in 2025 and estimated to grow from USD 5.79 billion in 2026 to reach USD 7.67 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Tightened federal PFAS rules, accelerated industrial water-reuse mandates, and the rapid adoption of digital dosing platforms are combining to boost chemical demand across municipal and industrial systems. In parallel, the U.S. Environmental Protection Agency (EPA) has earmarked USD 15 billion in infrastructure grants for PFAS remediation and lead-pipe replacement, sustaining a multi-year purchasing cycle for specialized coagulants, corrosion inhibitors, and regenerants. Southern states command the largest share because of dense petrochemical corridors and population growth, while the West records the swiftest expansion on the back of California’s reuse mandates and a booming semiconductor supply chain. Municipal utilities remain the single biggest consumer group, yet food and beverage processors post the fastest gains as stricter Food Safety Modernization Act (FSMA) hygiene protocols spur investments in clean-in-place (CIP) chemicals. Cost volatility for hydrochloric acid and caustic soda, together with rising energy prices, continues to pressure manufacturer margins, though premium specialty blends offset part of the squeeze by delivering higher value per pound of active ingredient.

Key Report Takeaways

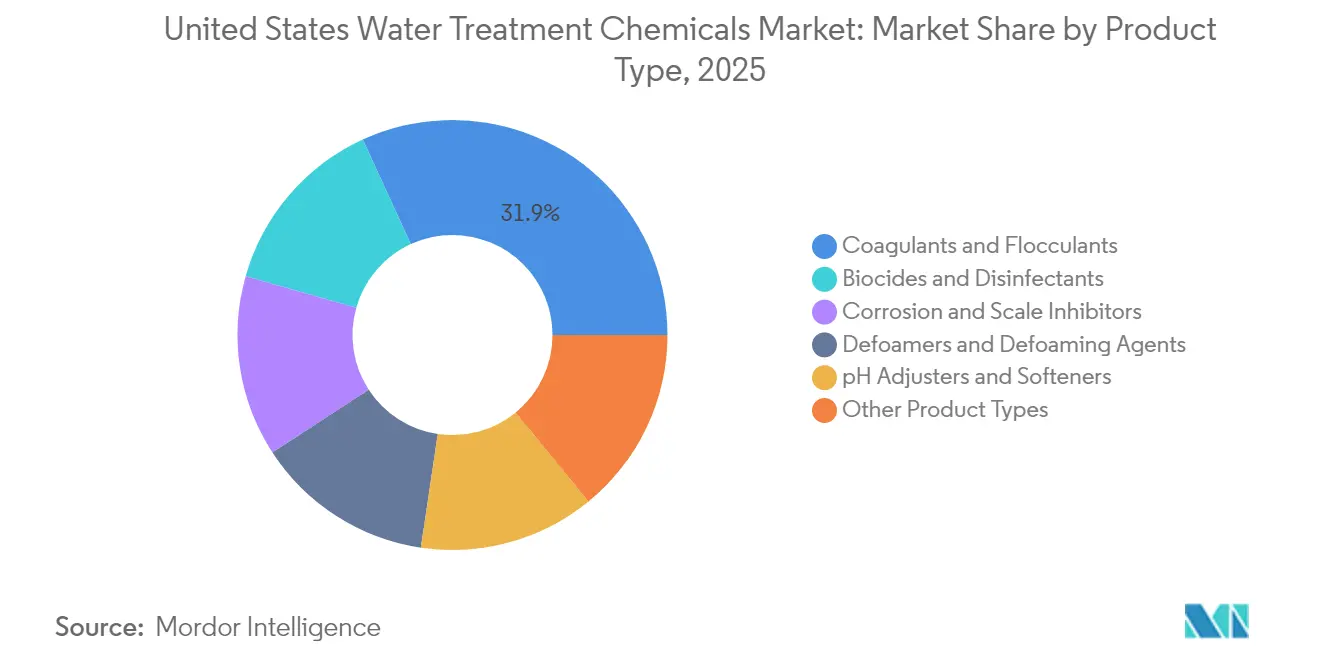

- By product type, coagulants and flocculants held 31.85% of the United States water treatment chemicals market share in 2025, while biocides and disinfectants are projected to grow at a 6.08% CAGR through 2031.

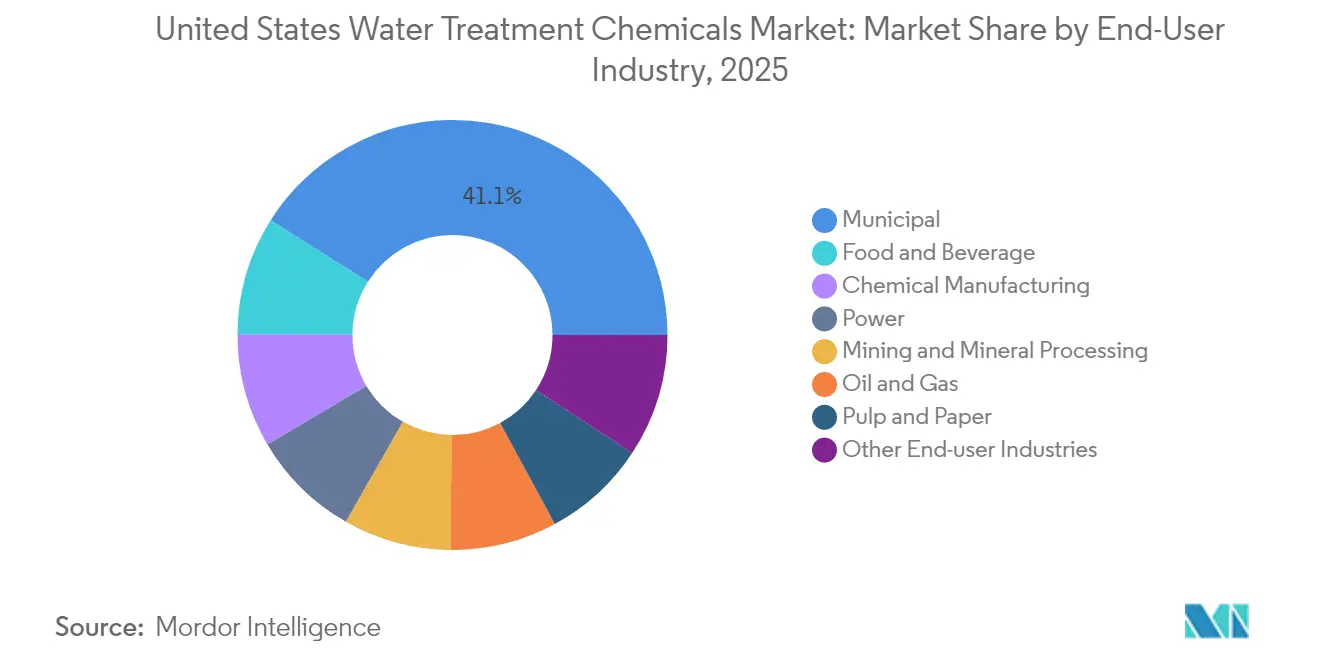

- By end-user industry, municipal utilities accounted for 41.05% of the United States water treatment chemicals market size in 2025; food and beverage processors are advancing at a 6.22% CAGR to 2031.

- By geography, the South led the United States water treatment chemicals market with a 36.10% revenue share in 2025, whereas the West is forecast to expand at a 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal PFAS and lead-pipe funding surge | +1.5% | National, strongest in Northeast and Midwest legacy networks | Medium term (2-4 years) |

| Industrial water-reuse expansion | +0.8% | West Coast and Southwest drought-prone zones | Long term (≥ 4 years) |

| Membrane-pretreatment chemicals adoption | +1.2% | Early uptake in California, Texas, Florida | Medium term (2-4 years) |

| EPA PFAS discharge limits | +0.9% | National, immediate industrial effluent impact | Short term (≤ 2 years) |

| Digital dosing and sensor-linked chemistries | +0.6% | Industrial hubs in Texas, Louisiana, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal PFAS and Lead-pipe Funding Surge

A USD 15 billion federal grant pool targeted at PFAS cleanup and legacy service-line replacement drives a pronounced increase in demand for enhanced-coagulation blends, corrosion inhibitors, and granular activated carbon (GAC) regenerants[1]U.S. Environmental Protection Agency, “Drinking Water Infrastructure Grants,” epa.gov . Smaller utilities lacking capital for advanced membranes deploy high-charge aluminum and ferric formulations because these options offer the lowest lifecycle cost for sub-nanogram PFAS removal. Simultaneously, projects replacing aged lead lines rely on phosphate-based corrosion control agents to curb lead solubility during excavation. The bulk of awards is allocated to Midwestern and Northeastern cities, which were built on 19th-century infrastructure, creating a multiyear backlog of chemical requisitions tightly linked to grant disbursement schedules. Suppliers with in-house toxicology and regulatory support win a larger share because they navigate EPA reporting and product registration steps more efficiently.

Industrial Water-reuse Expansion

California’s statewide rule requires industrial sites that consume over 1 million gallons per month to meet a 30% recycled-water threshold by 2030, thereby increasing demand for antiscalants, biocides, and cleaning formulations compatible with multiple reuse loops[2]California Water Resources Control Board, “Water Recycling Program,” waterboards.ca.gov. Semiconductor fabs in Arizona and the evolving petrochemical complexes along the Gulf rely on ultrapure water (UPW) trains that feature ion-exchange regeneration, high-purity acids, and micro-biocides to protect wafer yields. Produced-water recycling in shale plays gains traction as disposal fees exceed USD 3 per barrel, spurring the uptake of high-temperature scale inhibitors and broad-spectrum oxidants that can withstand 150,000 ppm salinity. Food and beverage plants are adding closed-loop CIP systems to counter rising municipal surcharges, which now surpass USD 15 per thousand gallons in drought-stressed counties.

Membrane-Pretreatment Chemicals Adoption

The growing deployment of reverse-osmosis (RO) and nanofiltration skids in both municipal and industrial plants shifts spending toward antiscalants formulated for low-pH operation, silica control, and iron sequestration. A nationwide pivot to membranes for PFAS abatement accelerates orders for chlorine dioxide and non-oxidizing biocides that suppress biofouling without compromising RO polyamide layers. Pharmaceutical and electronics customers negotiate premium prices for ultrapure pretreatment blends certified to have a trace-metal content of less than 1 ppb. As forward-osmosis pilots and membrane-distillation units move from pilot to early commercial scale, vendors experiment with new dispersants that maintain high flux under elevated osmotic pressures.

EPA PFAS Discharge Limits

New effluent standards capping PFOA and PFOS at 4 ppt are pushing textile finishers, aerospace platers, and landfill leachate processors to retrofit coagulation-adsorption trains or add polishing chemistries, such as functionalized ion-exchange resins. The timeline is immediate for direct-discharge permits, resulting in a front-loaded purchase curve through 2026, followed by steady-state operating volumes. Market uptake favors aluminum-chlorohydrate coagulants paired with powdered activated carbon due to their fast kinetics and lower sludge volumes compared with lime-based options.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating raw-material and energy costs | -0.7% | National; acute in Gulf Coast chlor-alkali hubs | Short term (≤ 2 years) |

| Shift to chemical-free technologies | -0.4% | Cost-sensitive municipal utilities | Medium term (2-4 years) |

| By-product toxicity regulations on biocides | -0.3% | California and Northeast first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Raw-Material and Energy Costs

Hydrochloric acid and caustic soda values rose in 2024, driven by higher natural-gas benchmarks and logistics bottlenecks, which crimped producer gross margins. Chlor-alkali units along the Gulf cut utilization during hurricane-related power disruptions, amplifying spot shortages. Municipal bid cycles, often locked a year in advance, left suppliers exposed to cost spikes they could not pass through. Smaller distributors serving rural plants faced greater pain because diesel surcharges added 8-12% to delivered pricing, yet consumption volumes stayed fixed. Larger players offset some of the impact by switching to rail and barge routes and by flexing their integrated chlorine and vinyl value chains.

Shift to Chemical-Free Technologies

Medium-sized cities are evaluating UV-AOP, ozone, and membrane bioreactor systems to reduce handling risks associated with bulk chlorine and alum sludge. Capital outlays remain the primary hurdle, but federal Build America, Buy America (BABA) funds make non-chemical gear more affordable in selected counties. When adopted, consumption of certain disinfectants falls abruptly, trimming order volumes for sodium hypochlorite and quaternary amines. Nonetheless, hybrids that still rely on specialized cleaners and residual corrosion inhibitors maintain a sizable share of chemical spend, even in “chemical-free” plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biocides Drive Growth Despite Coagulant Dominance

Coagulants and flocculants accounted for 31.85% of the United States' water treatment chemicals market share in 2025, driven by their indispensable role during primary clarification across both municipal and industrial basins. Spending on aluminum-based and polyferric blends remains stable because every gallon of raw water requires baseline particle removal, yet volume growth mirrors population growth rather than surging. Biocides and disinfectants, by contrast, record a 6.08% CAGR, the fastest among all categories. PFAS discharge limits, tighter pathogen count thresholds, and more complex membrane trains each require specialized broad-spectrum oxidants and non-oxidizing formulations. Premium corrosion and scale inhibitors post mid-single-digit growth as lead service line replacements surge. pH adjusters and softeners confront commodity pressure: caustic soda spot volatility erodes margins, yet consistent demand from power and pulp segments sustains baseline volume. Defoamers grow off a smaller base as biological systems proliferate, particularly in industrial digesters where surface tension imbalances drive foaming incidents. Specialty polymers, ion-exchange resins, and niche additives grouped under “other product types” capture semiconductor and pharmaceutical buyers willing to pay three to four times the price per pound in exchange for ppb-level purity. Digital dosing reshapes procurement logic. Buyers evaluate chemical supply through a performance lens — verified residual control, minimal sludge, and extended membrane life — rather than pounds delivered. Vendors that couple real-time telemetry with chemical packages gain share despite charging a 20-30% price premium, reinforcing an industry pivot from volume to value.

By End-User Industry: Municipal Leadership with Food and Beverage Acceleration

Municipal utilities accounted for 41.05% of the United States water treatment chemicals market in 2025, a position they are expected to maintain through 2031, as the Safe Drinking Water Act (SDWA) compliance drives consistent demand, regardless of macroeconomic cycles. Infrastructure-funded lead-line swaps and PFAS pilot rollouts maintain a healthy baseline. The food and beverage segment, however, grows at 6.22% CAGR, the fastest track among all industries, as strict FSMA hazard-analysis mandates extend sanitizing routines and drive upgrades to CIP formulations certified for direct food contact. Power generation plants remain significant buyers of scale inhibitors, pH modifiers, and oxygen scavengers for high-pressure boilers; however, the gradual retirement of coal and combined-cycle gas turbines is tempering volumetric growth. Oil and gas fields require customized chemical cocktails to treat produced water, which is often laden with scale-forming ions and bacteria. Chemical manufacturing sites push for ultra-low conductivity influent, spurring orders for high-purity acids, caustic, and mixed-bed resins. Mining and mineral processors utilize flocculants to expedite tailings dewatering, with lithium brine projects in Nevada and Arkansas serving as new growth nodes. Pulp and paper mills are shrinking in number, but the survivors are investing in advanced biocides and slime control to raise uptime, thereby sustaining a niche but sticky client base. Sales channels diverge: municipal accounts prize multi-year contracts and safety stock, while industrial buyers shift toward just-in-time (JIT) delivery buffered by on-site bulk tanks. Technical service becomes a decisive tie-breaker as plants lean on vendor chemists to troubleshoot fluctuating influent quality and changing discharge permits.

Geography Analysis

The South accounted for 36.10% of national revenue in 2025, primarily driven by Texas refineries, Louisiana's petrochemical complexes, and Florida’s expanding municipal grids. Texas alone accounts for the majority of the region’s consumption, thanks to its network of over 30 refineries and ethylene crackers that rely on continuous cooling-water treatment, boiler chemistry, and wastewater conditioning. Gulf Coast proximity to chlor-alkali plants lowers freight costs, delivering an advantage over Western counterparts.

The West is projected to post the fastest CAGR of 5.96% through 2031. California’s reuse rule requires every major industrial site to retrofit membrane trains with tailored antiscalants and oxidants. Semiconductor fabs in Arizona demand ultrapure chemicals certified to parts-per-trillion impurity thresholds. Data centers in Nevada and Utah add evaporative cooling towers that require low-phosphate, non-phosphonate antiscalants suitable for zero-liquid-discharge (ZLD) systems. High freight costs from Gulf Coast hubs are prompting distributors to establish satellite blending plants near Los Angeles and Phoenix, thereby improving lead times and reducing carbon footprints.

The Northeast captures PFAS-related funding faster than any other region, upgrading decades-old pipe networks. Short-haul distances between chemical makers in New Jersey and mid-Atlantic consumers hold freight economics in check.

Midwestern demand continues to grow at a stable pace. Agro-processing facilities buy commodity coagulants for corn wet-milling and ethanol plants, while historic steel towns gradually retrofit cooling systems. Logistics lanes radiating from Chicago support efficient railcar distribution, cushioning delivered costs despite distance from Gulf monomers.

Regulatory Landscape

The US regulatory framework for water treatment chemicals is anchored in the Safe Drinking Water Act (SDWA), under which the US Environmental Protection Agency (EPA) sets and enforces National Primary Drinking Water Regulations (NPDWR) and related compliance requirements for public water systems. In April 2024, EPA finalized PFAS drinking water requirements, including 4 ppt maximum contaminant levels for PFOA and PFOS referenced in this report context. This tightens treatment performance expectations across municipal systems and increases scrutiny on certified treatment programs and chemical selection.

Through 2026, compliance and reporting rules are also shifting. Community water systems are moving to revised Consumer Confidence Report (CCR) requirements, with implementation spanning June 2024 through December 2026, while states are required to adopt the CCR revisions by May 2026. In May 2026, EPA proposed rescinding certain 2024 regulatory determinations and associated provisions for specific PFAS (PFHxS, PFNA, HFPO-DA, and certain mixtures), adding uncertainty to compound-by-compound treatment roadmaps. At the same time, EPA advanced monitoring planning via a proposed Sixth Unregulated Contaminant Monitoring Rule (UCMR 6) that would require public water systems to monitor 30 unregulated contaminants (including select PFAS) during 2028-2030, which affects contaminant screening, pilot testing, and chemical procurement planning ahead of potential future NPDWR actions.

Value Chain Analysis

The value chain starts with upstream commodity inputs, including chlor-alkali derivatives such as caustic soda and hydrochloric acid, mineral acids and bases, and feedstocks for polymers and specialty additives. It then moves into formulation and blending for application-specific products such as coagulants and flocculants, oxidants and non-oxidizing biocides, corrosion and scale inhibitors, and membrane pretreatment blends. Manufacturing and supply in the United States include both global water-chemistry platforms and specialty producers. Examples include SNF, which has North American manufacturing footprints including Riceboro, Georgia and Plaquemine, Louisiana, and integrated solution providers such as Solenis, which combine chemistry with equipment and digital monitoring.

Downstream, chemicals move through direct sales to large municipal and industrial accounts, as well as regional distributors that handle last-mile delivery, safety stock, and on-site bulk storage. The EPA has highlighted water treatment chemical supply chain disruptions as a material operational risk, especially for small systems with limited procurement leverage and storage capacity. SDWA Section 1441 (42 USC 300j) provides a federal mechanism for public water systems and wastewater treatment works to seek assistance during critical shortages of essential treatment chemicals, including chlorine, activated carbon, lime, ammonia, soda ash, potassium permanganate, and caustic soda. This is reinforcing longer-term contracting, dual-sourcing, and service models that bundle chemical supply with monitoring and dosing optimization to reduce outage risk and manage compliance-driven demand variability.

Competitive Landscape

The United States water treatment chemicals market exhibits moderate fragmentation, yet consolidation momentum builds as compliance costs escalate. Digital integration emerges as a central battlefield. Market leaders bundle sensors, cloud dashboards, and chemicals under performance-guarantee contracts. Smaller formulators counter by specializing in high-temperature, high-salinity niches where bulk producers lack tailored SKUs. Patent filings rise for PFAS-selective adsorbents and low-halogen oxidants. Vendors with EPA-registered biocide lines and robust toxicology portfolios hold a barrier against new entrants because re-registration costs can top USD 3 million per active ingredient. Private-equity ownership climbs as platforms buy regional blenders to gain route density, then cross-sell premium polymers.

United States Water Treatment Chemicals Industry Leaders

Ecolab

Solenis

Kemira

Veolia

SNF

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Municipal compliance programs tied to PFAS and lead remain a central demand anchor for higher-value treatment chemistries, including enhanced coagulants, corrosion control agents, and adsorption and regenerant support chemicals. In October 2024, EPA finalized the Lead and Copper Rule Improvements (LCRI), requiring systems to identify and replace lead pipes within 10 years. That sustains phosphate-based corrosion control and related treatment support needs during service-line replacement work. At the same time, EPA actions in May 2026, including a proposed extension to the PFOA and PFOS MCL compliance date from April 26, 2029 to April 26, 2031 and a proposal to rescind determinations for select PFAS included in the 2024 PFAS NPDWR, are shifting the timing and compound priorities of municipal treatment rollouts. This increases the value of supplier technical support, piloting, and flexible treatment chemical programs.

A clear whitespace is emerging around domestic capacity and services that enable PFAS treatment operations at scale, particularly for activated carbon reactivation and performance-based chemical programs that reduce operational burden. In February 2026, Calgon Carbon announced a nearly USD 100 million expansion of its Columbus, Ohio facility to add about 27 million pounds per year of drinking water carbon reactivation capacity (targeted for 2028 operations), underscoring the buildout of US-based PFAS-supporting treatment supply chains. Industrial and commercial opportunities are also broadening through water reuse and high-spec applications, including semiconductor ultrapure water and data center cooling, where chemical suppliers can pair ultra-low impurity products with digital dosing and monitoring platforms to meet tighter process and discharge requirements while controlling total water and chemical consumption.

Recent Industry Developments

- June 2026: Solenis entered an agreement with Dow to become an approved service provider in Dow's Coolant Care Network for data centers. The collaboration aligns water-treatment chemistry and monitoring services with coolant management programs, strengthening Solenis positioning in data center cooling-water treatment where uptime and corrosion/scale control are tightly managed.

- December 2025: Ecolab closed its acquisition of Ovivo's electronics ultrapure water business. The deal adds specialized ultrapure water capabilities that support semiconductor manufacturing, expanding Ecolab's ability to pair high-purity chemistries with process water system expertise in a key industrial end market.

- July 2024: BASF divested its Magnafloc and Rheomax mining flocculants portfolio to Solenis. The transaction expanded Solenis's flocculant product breadth and customer reach, reinforcing its scale in polymer-based water treatment applications across industrial segments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers chemical products sold and used in the United States to treat water in municipal and industrial systems, where the chemical is applied to improve water quality, protect equipment, or meet discharge and safety requirements.

Scope exclusions: We do not count water treatment equipment, membranes, filtration media, or ongoing plant operations services unless they are priced and sold as chemicals.

Segmentation Overview

- By Product Type

- Biocides and Disinfectants

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Defoamers and Defoaming Agents

- pH Adjusters and Softeners

- Other Product Types

- By End-user Industry

- Power

- Oil and Gas

- Chemical Manufacturing

- Mining and Mineral Processing

- Municipal

- Food and Beverage

- Pulp and Paper

- Other End-user Industries

- By Geography

- Northeast

- Midwest

- South

- West

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping the U.S. demand picture and the rules that drive chemical usage, since water chemistry tends to track regulation cycles, plant operating loads, and input water quality. We referenced public sources such as the US EPA (including drinking water and wastewater rule updates), USGS water use and quality summaries, the CDC for public health related water indicators, and EIA for power generation signals that link to boiler and cooling water treatment needs.

We then used trade and operating context to keep assumptions realistic, using sources such as USITC trade statistics, association materials (including AWWA and WEF), public utility procurement notices, and company filings and investor decks for product mix and pricing commentary. In a few places, paid subscriptions were used for company financials and intelligence, patent lookups, and shipment-level import and export checks to confirm supply-side movements. The examples above are not exhaustive, and many other public documents were reviewed as well for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what the desk sources could not fully show, especially actual dosing patterns, price realization changes, and where products get substituted when budgets get tight. We spoke with participants across municipal buyers, industrial water treatment teams, and channel partners, and then aligned feedback across the Northeast, Midwest, South, and West so the model did not overweigh any single region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 35% | |

| Smaller Players: 14% | Managers: 51% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, where treatment volume and operating activity were reconstructed by end user, then converted into chemical demand using typical dosing ranges and application shares (cooling, boiler, raw water, desalination, and effluent). To keep totals grounded, we corroborated results with selective bottom-up checks such as sampled price per pound and price per gallon ranges, supplier and distributor channel checks, and implied volumes from disclosed business lines, which helped adjust areas where desk data was thin.

Key inputs that shaped the model included municipal water and wastewater throughput, industrial production signals for power and chemical manufacturing, PFAS and discharge compliance activity that shifts treatment intensity, corrosion and scale control needs tied to cooling and boiler cycles, and observable movements in key input chemicals that affect pricing. Forecasts relied mainly on scenario analysis, because demand is pulled by regulation timing and capital programs as much as it is pulled by GDP-style growth. The scenarios were calibrated using expert views on rule enforcement, infrastructure funding, and reuse adoption. Where bottom-up indicators did not cover smaller local suppliers, we filled gaps using regional penetration assumptions and then rechecked against reported procurement volumes.

Data Validation & Update Cycle

Results were checked in several ways so obvious misreads could be caught early, including variance checks against historical growth bands, cross-checks by product family, and comparisons to independent signals such as treatment throughput and industrial load changes. When a figure did not reconcile, the assumption was reopened and validated again through follow-up outreach, then reviewed by another analyst before sign-off.

The report is refreshed annually, and interim updates are made when material events shift the market outlook, such as major regulatory actions, sharp feedstock price swings, or step changes in industrial operating rates. Before delivery, a final update pass is completed so clients receive the most current view supported by the latest available inputs.

Mordor Intelligence's United States Water Treatment Chemicals Market Sizing Compared With Other Published Estimates

It is common to see different market values for U.S. water treatment chemicals, even when titles look similar, because each publisher draws the boundary in its own way. The biggest differences usually come from what is included as chemicals versus adjacent services, the mix of applications counted, and how price levels are translated across years.

By tracking application-level treatment volumes and refreshing pricing and dosing assumptions through primary checks, Mordor Intelligence keeps the count limited to chemical revenues in municipal and industrial uses, instead of blending in broader water treatment activities that inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.48 B (2025) | |

| Industry Databook A | USD 7.73 B (2024) | Uses a higher starting value that appears to bundle broader treatment areas and application buckets, and the pricing base year and segment mapping are not fully transparent for chemicals-only revenue. |

| Global Publisher B | USD 7.76 B (2025) | Likely applies a wider scope across applications and end uses with less explicit separation of chemical sales from service and treatment program value, which pushes the total upward. |

The spread is mainly explained by scope and what is treated as chemical revenue versus a wider water treatment spend pool. When the boundary is kept to chemicals and linked back to throughput, dosing intensity, and realistic price realization, the output stays easier to reproduce and easier to stress-test when conditions change.

Key Questions Answered in the Report

What is the projected value of the United States Water Treatment Chemicals Market?

It is expected to reach USD 7.67 billion, supported by a 5.73% CAGR over 2026-2031 from USD 5.79 billion in 2026.

Which product category will post the strongest growth through 2031?

Biocides and disinfectants are expected to expand at a 6.08% CAGR due to increasing demands for tougher pathogen control and membrane biofouling mitigation.

What drives chemical sales to semiconductor fabs in Arizona?

Ultrapure water requirements for advanced lithography generate orders for high-purity acids, ion-exchange resins, and antiscalants certified to meet <1 ppb metal standards.

Why do municipalities remain the largest buyer group?

Continuous Safe Drinking Water Act compliance and large-scale pipe-replacement programs keep municipal utilities using sizable chemical volumes every day.

How do digital dosing systems affect chemical consumption?

Real-time sensor-linked feed pumps reduce overdosing by 15-25%, while also creating value-based contracts that reward suppliers for guaranteed performance rather than sheer volume.

Page last updated on: