Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.02 Billion |

| Market Size (2026) | USD 19.94 Billion |

| Market Size (2031) | USD 25.28 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Valves Market Analysis by Mordor Intelligence

The US valves market size is expected to grow from USD 19.02 billion in 2025 to USD 19.94 billion in 2026 and is forecast to reach USD 25.28 billion by 2031 at 4.86% CAGR over 2026-2031. The outlook reflects sustained investment in shale-oil refracturing, federally funded water infrastructure upgrades, and the acceleration of Industrial IoT adoption. Valve suppliers capture recurring revenue from shorter replacement cycles in unconventional oilfields, while municipalities leverage federal grants to modernize legacy distribution networks with smart, lead-free components. In parallel, data center expansion, hydrogen hub development, and carbon capture projects present high-value opportunities that reward manufacturers capable of meeting stringent performance standards. Competitive intensity centers on technology integration and rapid response to steel-price volatility, prompting many producers to diversify materials and expand aftermarket services. Cybersecurity readiness, predictive maintenance capabilities, and hydrogen-ready designs now influence procurement decisions as much as price and lead time.

Key Report Takeaways

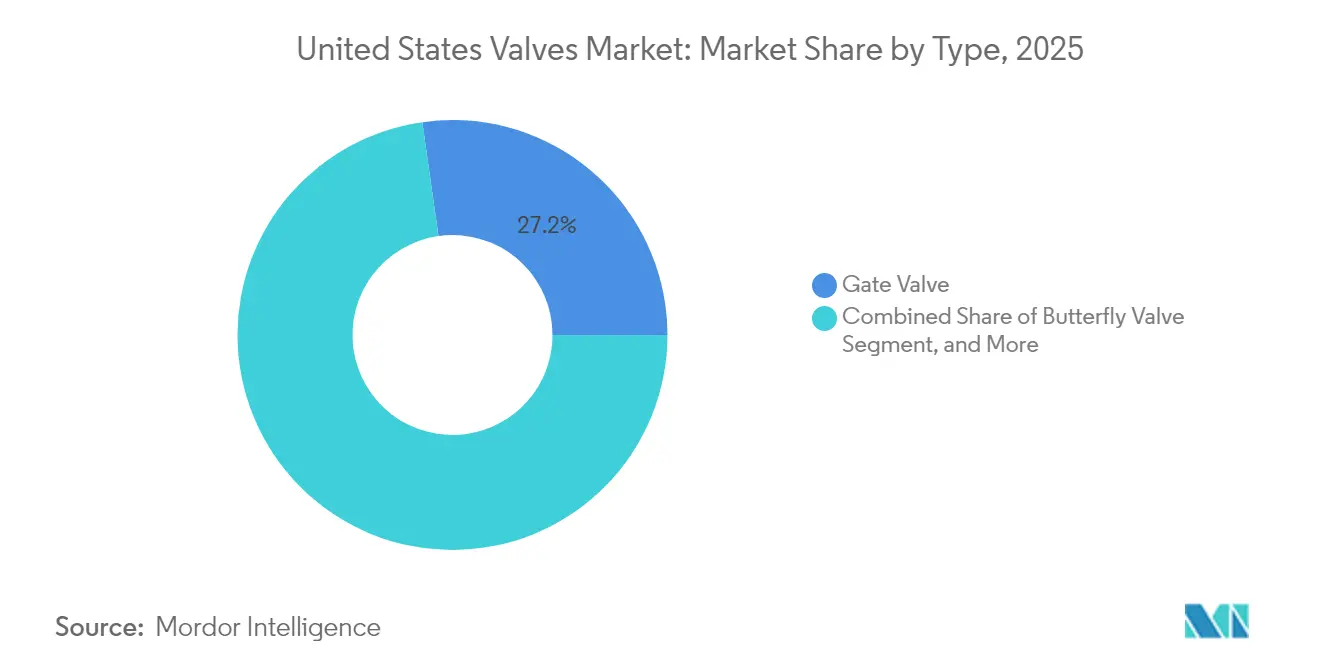

- By valve type, gate valves led with 27.24% of the US valves market share in 2025, while butterfly valves are projected to expand at a 5.05% CAGR through 2031.

- By material, steel commanded a 40.88% share of the US valves market size in 2025, whereas plastic materials were projected to record the highest CAGR of 4.92% from 2025 to 2031.

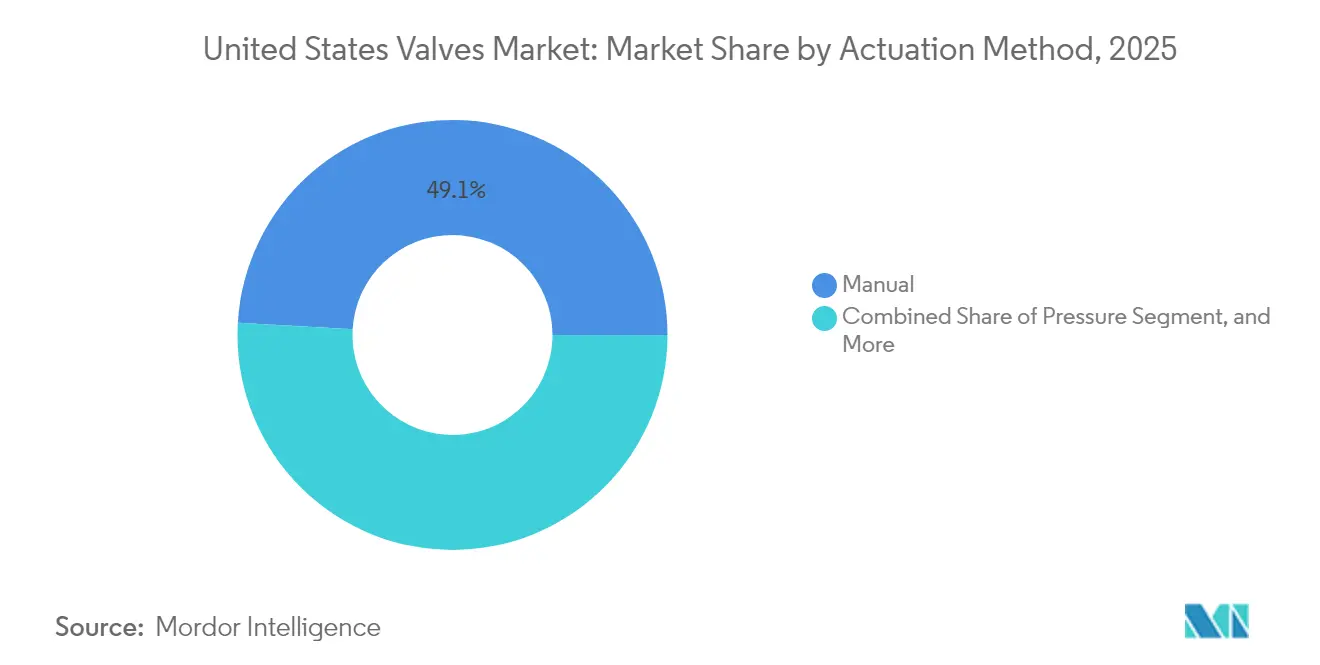

- By actuation method, manual products accounted for a 49.10% share of the US valves market size in 2025; electric actuation is projected to advance at a 5.44% CAGR through 2031.

- By end-user, the oil and gas sector represented a 32.40% share of the US valves market size in 2025; however, the food and beverage sector is forecasted to grow at a 5.03% CAGR through 2031.

- By region, the South held 35.22% of the US valves market share in 2025, while the West is set to post the fastest 5.68% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shale-oil refracturing activity boosting valve replacements | +0.8% | South, West | Medium term (2-4 years) |

| Accelerating federal funding for water infrastructure modernization | +0.6% | National (priority in Northeast and Midwest) | Long term (≥ 4 years) |

| Industrial IoT-enabled predictive maintenance adoption | +0.5% | National (early gains in Midwest) | Medium term (2-4 years) |

| Hydrogen-ready valve design standards emerging | +0.4% | West Coast and Gulf Coast | Long term (≥ 4 years) |

| Federal investment tax credits for carbon-capture projects | +0.3% | South and Midwest | Long term (≥ 4 years) |

| Growth of modular data centers requiring precision cooling valves | +0.2% | West and South | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shale-Oil Refracturing Activity Boosting Valve Replacements

Refracturing campaigns shorten valve lifecycles from 18-24 months to 12-15 months, driving steady aftermarket demand in Permian and other shale hotspots. Pressure cycling above 10,000 psi necessitates premium designs with enhanced sealing and corrosion resistance.[1]U.S. Energy Information Administration, “Shale Oil Production and Refracturing Activities,” eia.gov Aftermarket providers benefit from higher replacement frequency, while OEMs capture value through upgraded materials and service agreements. Rising refracturing intensity also spurs demand for control valves that can modulate flow during multi-stage treatments. Suppliers able to certify products for rapid deployment gain a competitive edge in this time-sensitive environment.

Accelerating Federal Funding for Water Infrastructure Modernization

The Infrastructure Investment and Jobs Act allocates USD 55 billion for water systems, much of which targets aging valves that entered service 30-50 years ago. Municipalities prioritize smart, lead-free, and remotely actuated valves to increase leak detection efficiency and regulatory compliance. EPA revolving funds supplement federal grants, ensuring a steady pipeline of projects through 2030. Suppliers offering turnkey packages, including valves, actuators, and monitoring software, capture higher margins, especially in the Northeast and Midwest, where replacement urgency is acute. Long procurement cycles favor vendors with proven municipal references.

Industrial IoT-Enabled Predictive Maintenance Adoption

Manufacturers that embed sensors in critical valves enable analytics platforms to detect wear before catastrophic failure, resulting in up to a 30% reduction in valve-related downtime in early pilot programs.[2]Industrial Internet Consortium, “Industrial IoT Adoption Trends,” iiconsortium.org This capability resonates in the Midwest industrial belt, where unplanned shutdowns carry high opportunity costs. Integrating edge processing and open communication protocols differentiates suppliers and justifies premium pricing. Predictive maintenance also shifts revenue toward subscription-based software and services, diversifying income streams beyond initial equipment sales.

Hydrogen-Ready Valve Design Standards Emerging

New DOE-backed standards require materials that withstand hydrogen embrittlement and limit leakage to below 10^-6 sccs.[3]U.S. Department of Energy, “Hydrogen Program Plan,” energy.gov California and Gulf Coast hubs demand certified valves for pipelines, refueling stations, and industrial processes. Manufacturers that deploy specialized coatings and precision machining can extend valve life by up to 60%, thereby reducing the total cost of ownership for operators. Early compliance positions suppliers to win long-term framework agreements as the hydrogen economy scales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel and alloy price volatility squeezing OEM margins | -0.4% | National, strongest in steel-intensive regions | Short term (≤ 2 years) |

| Skills gap in smart-valve commissioning and maintenance | -0.3% | National, acute in rural and industrial areas | Medium term (2-4 years) |

| Cybersecurity concerns slowing connected valve deployments | -0.25% | National, critical infrastructure sites | Medium term (2-4 years) |

| High upfront cost of valve automation systems limiting adoption | -0.2% | National, cost-sensitive municipal and industrial users | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steel and Alloy Price Volatility Squeezing OEM Margins

Spot steel prices fluctuated 40-60% in 2024, compressing margins for valve makers locked into long-term contracts. Smaller companies lacking hedging programs face greater earnings swings, sometimes redesigning products with alternative materials. Surcharge clauses and index-based pricing help larger firms offset volatility, but implementation requires customer negotiation and system updates. Volatility also complicates inventory planning, raising working capital requirements and potentially delaying innovation spending.

Skills Gap in Smart-Valve Commissioning and Maintenance

Roughly 35-40% of current technicians need upskilling to install and service connected valves, according to industry surveys. Rural municipalities and small plants feel the pinch most acutely, which slows the adoption of advanced automation. Training programs and partnerships with technical colleges progress slowly, leaving operators dependent on third-party specialists and elevating lifecycle costs. Vendors that bundle training and remote support differentiate their offers but must absorb additional service costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gate Valves Lead Despite Butterfly Surge

Gate valves held 27.24% of the U.S. valve market share in 2025, reflecting their entrenched use in pipelines and water networks, where tight shut-off is mandatory. Their established specifications make them the default choice in many engineering standards, supporting steady demand for replacement. Butterfly valves gain momentum with a 5.05% CAGR, prized for compact footprints and fast quarter-turn operation in HVAC and automated process lines. The U.S. valves market size for butterfly designs grows as facility owners prioritize energy efficiency and remote control. Globe and check valves remain staples for throttling and backflow prevention, while control valves occupy higher-value niches driven by precision requirements. Growth in additive manufacturing prototypes enables rapid customization; however, large-scale production still favors traditional casting due to cost and durability considerations.

Engineering teams are increasingly evaluating total installed cost rather than purchase price, benefiting butterfly valves where weight savings reduce structural and actuation expenses. Conversely, gate valves maintain dominance in corrosive or abrasive services by offering robust wedge seals and full-bore flow paths. Digital position feedback retrofits allow legacy gate valves to integrate with plant DCS platforms, extending service life and aligning with modern monitoring strategies. Vendors that can support mixed fleets of gate and butterfly valves through unified asset-management software win maintenance contracts, thereby deepening customer stickiness in the U.S. valves market.

By Material: Steel Dominance Faces Plastic Challenge

Steel products held a 40.88% market share in 2025, underpinned by their high tensile strength and temperature tolerance, which are essential for upstream energy and chemical processing applications. Improved metallurgy and coatings extend mean time between failure, safeguarding steel’s role in critical services. Plastic valves grow at the fastest rate, with a 4.92% CAGR, driven by their corrosion resistance and lower installation weight in water treatment and certain chemical processes. The U.S. valves market size for plastics is expected to expand further as utilities address lead-replacement mandates.

Utilities weigh lifecycle costs, often selecting plastic for low-pressure lines where corrosion drives frequent steel replacement. Hybrid solutions, such as plastic-lined steel bodies, strike a balance between strength and chemical resistance, capturing a share of the mid-pressure range. Alloy-based materials maintain a premium position in extreme environments, such as nuclear and aerospace applications, although limited volumes restrict their market share. Cast iron continues to serve legacy municipal systems, but its use is slowly declining due to its weight and corrosion drawbacks. Material innovations remain pivotal to meeting increasingly stringent environmental and performance standards, especially as the introduction of hydrogen services presents new compatibility challenges.

By Actuation Method: Manual Methods Persist Despite Electric Growth

In 2025, manual actuation commanded a 49.10% share of the U.S. valves market, underscoring a persistent preference for straightforward, low-capex solutions, especially when automation offers minimal added value. Beyond their primary function, manual overrides play a pivotal role as safety backups in various process industries. Meanwhile, electric actuation is experiencing the fastest growth at a 5.44% CAGR, driven by the integration of IoT, the demand for precise control, and a decline in actuator costs. With the U.S. valves market increasingly leaning towards connected assets, plant operators are gravitating towards electric units that continuously relay health data to predictive maintenance platforms.

Pneumatic actuators are gaining traction in hazardous zones, prioritizing intrinsic safety, whereas hydraulic units continue to be indispensable in high-force scenarios, like those involving large-diameter pipeline valves. Additionally, hybrid electro-hydraulic systems are gaining traction in subsea applications, offering redundancy but also introducing heightened maintenance challenges.

By End-User Industry: Oil and Gas Leadership Challenged by Food Processing Growth

Oil and gas accounted for 32.40 of % U.S. valves market share in 2025, encompassing production, midstream, and refining applications that rely on a broad spectrum of valve types. Activity levels in shale basins and Gulf Coast petrochemical complexes reinforce near-term demand. The food and beverage segment posts the fastest 5.03% CAGR as stringent hygiene rules drive frequent valve replacement with sanitary-design units. Growth parallels investments in automation, such as packaging and cleaning-in-place systems, which demand corrosion-resistant and easily cleanable valves.

Chemical processing, power generation, and water and wastewater treatment present stable replacement cycles tied to regulatory compliance and infrastructure aging. Pharmaceutical manufacturing, although lower in volume, commands high ASPs due to documentation and validation requirements. The mining, pulp, and paper industries seek abrasion-resistant designs, supporting niche suppliers. Collectively, diversified demand profiles buffer the U.S. valves industry against commodity price swings, fostering moderate overall growth.

Geography Analysis

The South led the US valves market with a 35.22% share in 2025. Texas and Louisiana continue investing in refining, LNG export terminals, and carbon-capture retrofits that rely heavily on severe-service valves. Federal incentives for CO₂ sequestration further amplify demand for high-pressure, corrosion-resistant designs. Offshore platforms in the Gulf of Mexico add specialized subsea valve requirements, reinforcing regional dominance.

The West posts the fastest 5.68% CAGR through 2031 as data-center build-outs in Arizona, Nevada, and California mandate precision cooling valves. Renewable energy projects, such as concentrated solar and geothermal plants, introduce high-temperature and erosive service conditions that favor the use of advanced materials. California’s hydrogen-hub roadmap accelerates early deployment of hydrogen-ready valves, positioning the region at the forefront of next-generation specifications.

In the Northeast, aging water distribution networks drive replacement programs, which are financed by federal and state grants. Utilities specify smart, lead-free valves with remote monitoring, creating steady opportunities for IoT-enabled products. The Midwest, anchored by automotive and chemical plants, emphasizes predictive maintenance and process optimization, spurring demand for control valves integrated with plant MES systems. Although exhibiting lower headline growth, both regions generate consistent aftermarket revenue streams that are critical to manufacturer profitability.

Competitive Landscape

The US valves market shows moderate concentration. Top multinationals, such as Emerson Electric, Flowserve, and Crane, capture a significant share through broad portfolios and global service networks. Mid-tier specialists focus on niche technologies, such as severe-service ball valves or sanitary stainless-steel lines, leveraging agility and customer intimacy to counterbalance the scale advantages of larger rivals. Consolidation persists, as illustrated by Flowserve’s USD 290 million acquisition of MOGAS Industries, which enhances its high-pressure ball valve offering and reinforces its energy-sector exposure.

Digitalization differentiates competitors. Emerson’s DeltaV integration for smart positioners underscores strategic emphasis on predictive analytics and seamless control-system compatibility. Parker-Hannifin’s Ohio facility expansion showcases the company's investment in advanced automation and clean-room production to support growing demand from the aerospace and industrial sectors. Cybersecurity and API connectivity become critical tender requirements, prompting alliances with software vendors and cloud providers.

Disruptive entrants are exploring additive manufacturing for rapid prototype turnaround and custom geometries, yet they face hurdles related to scale and certification. Established players respond with in-house 3D printing centers and material R&D to shorten development cycles. Market share battles are increasingly hinging on life-cycle service contracts, spare parts availability, and the ability to train customer personnel on smart-valve platforms. Suppliers offering integrated packages-comprising hardware, software, and field services-strengthen their competitive moats as the US valves market transitions toward outcome-based procurement models.

United States Valves Industry Leaders

Emerson Electric Co.

Schlumberger Limited

Flowserve Corporation

Crane Company

Rotork plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rotork acquired SignalFire Wireless Telemetry for USD 85 million to integrate long-range wireless monitoring and diagnostics into its electric actuator product line.

- June 2025: Crane Company committed USD 120 million to expand its Mansfield, Ohio facility, adding additive-manufacturing capacity for severe-service metal-seated valves.

- April 2025: Flowserve launched a cloud-based digital twin platform that delivers real-time performance modeling and predictive maintenance for its control valve portfolio.

- February 2025: Emerson Electric opened a USD 40 million valve innovation center in Houston dedicated to hydrogen-ready valve design, testing, and rapid prototyping.

United States Valves Market Report Scope

A valve is a mechanical device that controls the flow of fluids such as liquid, gas, or slurries in a pipe or another enclosure medium. The valves are of different types and have specific functions according to which they are used for various applications in the industries such as oil and gas, chemical, waste and wastewater, and others.

The US Valves Market Report is Segmented by Type (Ball Valve, Butterfly Valve, Gate Valve, Globe Valve, Check Valve, Plug Valve, Control Valve, Other Types), Material (Steel, Cast Iron, Alloy-Based, Plastic, Other Materials), Actuation Method (Manual, Pneumatic, Electric, Hydraulic, Other Methods), End-User Industry (Oil and Gas, Power Generation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Ball Valve |

| Butterfly Valve |

| Gate Valve |

| Globe Valve |

| Check Valve |

| Plug Valve |

| Control Valve |

| Other Types |

By Material

| Steel |

| Cast Iron |

| Alloy-Based |

| Plastic |

| Other Materials |

By Actuation Method

| Manual |

| Pneumatic |

| Electric |

| Hydraulic |

| Other Actuation Methods |

By End-User Industry

| Oil and Gas |

| Power Generation |

| Chemical |

| Water and Wastewater |

| Mining |

| Food and Beverage |

| Pharmaceuticals |

| Other End-User Industries |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Type | Ball Valve |

| Butterfly Valve | |

| Gate Valve | |

| Globe Valve | |

| Check Valve | |

| Plug Valve | |

| Control Valve | |

| Other Types | |

| By Material | Steel |

| Cast Iron | |

| Alloy-Based | |

| Plastic | |

| Other Materials | |

| By Actuation Method | Manual |

| Pneumatic | |

| Electric | |

| Hydraulic | |

| Other Actuation Methods | |

| By End-User Industry | Oil and Gas |

| Power Generation | |

| Chemical | |

| Water and Wastewater | |

| Mining | |

| Food and Beverage | |

| Pharmaceuticals | |

| Other End-User Industries | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the US valves market?

The US valves market size stands at USD 19.94 billion in 2026.

How fast is the US valves market expected to grow?

It is projected to expand at a 4.86% CAGR, reaching USD 25.28 billion by 2031.

Which valve type is growing the quickest?

Butterfly valves show the highest growth, advancing at a 5.05% CAGR through 2031.

Which region leads US valve demand?

The South accounts for 35.22% of national demand due to energy and petrochemical activity.

What is the main restraint on smart-valve adoption?

A nationwide skills gap in commissioning and maintaining connected valves slows deployment.

Which actuation technology is gaining ground fastest?

Electric actuators record the strongest 5.44% CAGR as plants digitize operations.

Page last updated on: