United States Sperm Bank Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.84 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

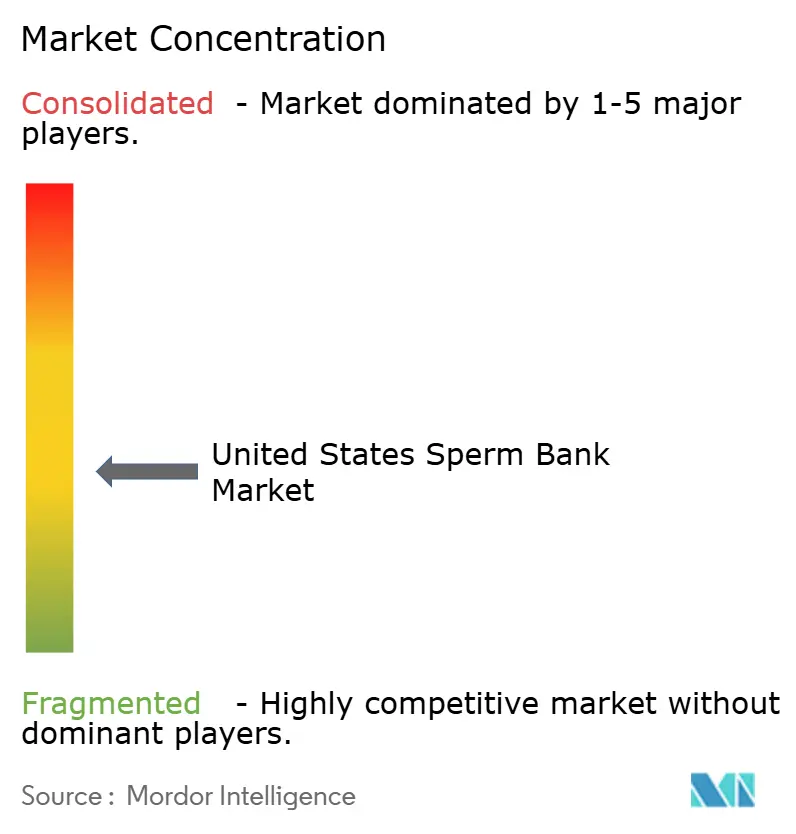

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Sperm Bank Market Analysis by Mordor Intelligence

The United States Sperm Bank Market size is projected to be USD 1.84 billion in 2025, USD 1.9 billion in 2026, and reach USD 2.26 billion by 2031, growing at a CAGR of 3.52% from 2026 to 2031.

The client base in the United States (US) sperm bank market is now much broader than its earlier focus on infertile heterosexual couples, because single women and LGBTQ+ family builders collectively account for nearly 75% of donor sperm users in assisted reproduction. That shift supports steadier repeat demand, since many recipients pursue more than 1 pregnancy over time and continue to use donor procurement, storage, and matching support across separate treatment journeys. The US sperm bank market is also gaining support from preventive sperm freezing, as peer-reviewed evidence on declining semen quality is pushing more healthy men to bank earlier rather than wait for a diagnosed fertility problem. Supply remains the main operating constraint, because leading providers report extremely low donor acceptance rates, which means even modest improvements in recruitment can quickly change usable inventory and near-term revenue conversion. Employer coverage is becoming more important for first-time adoption in the US sperm bank market, and the federal proposal on excepted fertility benefits could move more workers into subsidized sperm banking and donor sperm access beginning in 2027 if finalized.

Key Report Takeaways

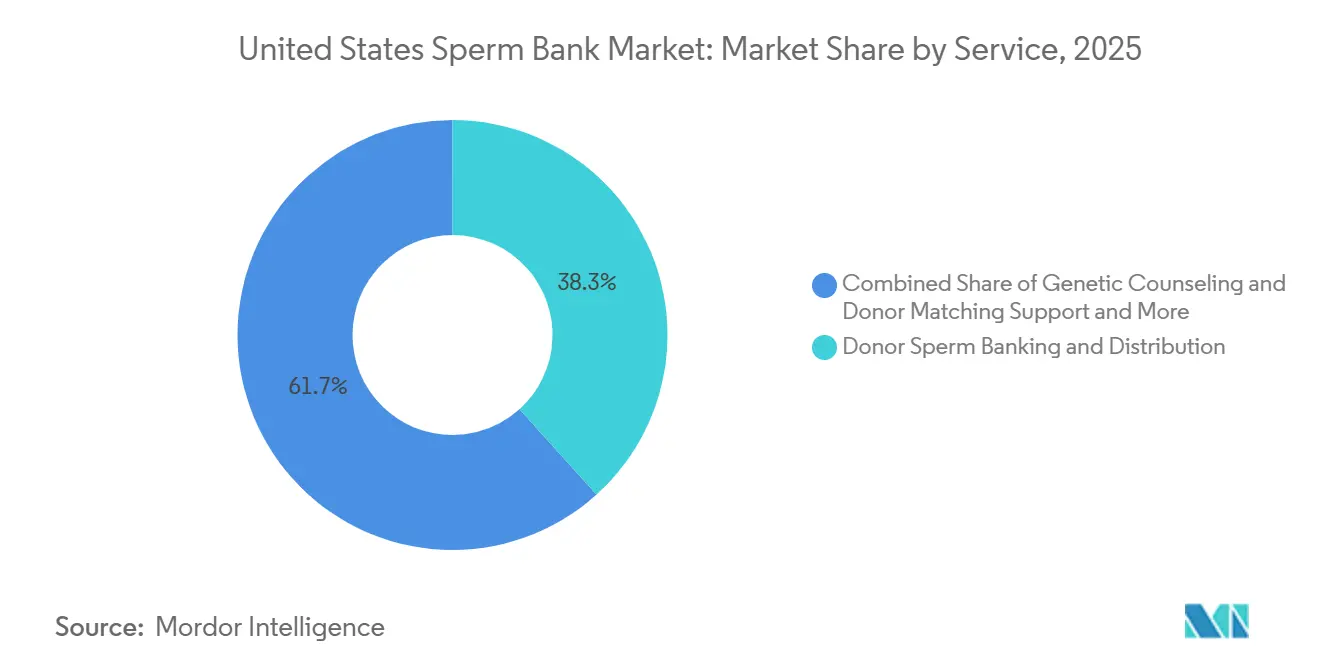

- By service, Donor Sperm Banking and Distribution led with 38.31% revenue share in 2025, while Genetic Counseling and Donor Matching Support is forecast to expand at a 6.38% CAGR through 2031.

- By donor type, Known Donor held a 55.24% share in 2025 and also recorded the highest projected CAGR at 4.52% through 2031.

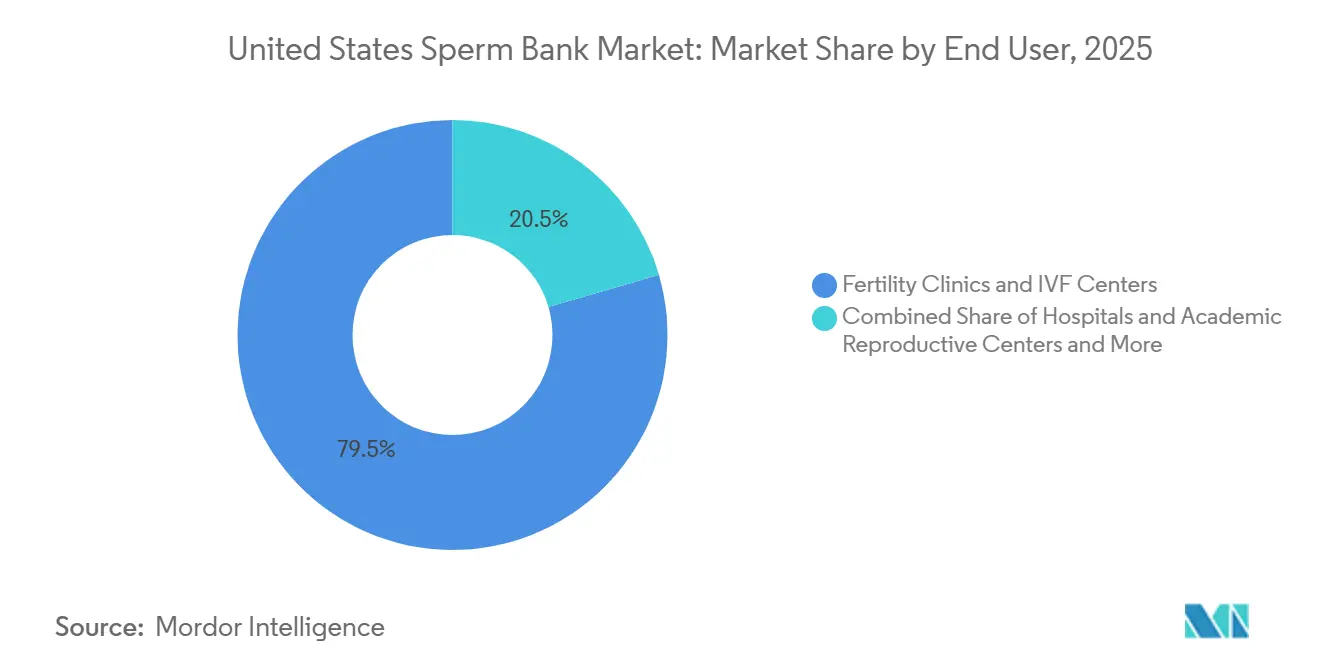

- By end user, Fertility Clinics and IVF Centers accounted for 79.52% share in 2025, while Direct-to-Consumer Fertility Preservation is projected to have a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Sperm Bank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delayed Parenthood And Male Fertility Decline | +0.9% | National, with highest concentration in urban metros including New York, Los Angeles, Chicago, and Boston | Long term (≥ 4 years) |

| LGBTQ+ And Single-Woman Family Building | +0.8% | National, with early adoption on the West Coast and in the Northeast, expanding into the South and Midwest | Long term (≥ 4 years) |

| Employer-Funded Fertility Benefits Expansion | +0.6% | National, with highest impact in California, Texas, New York, and Massachusetts | Medium term (2-4 years) |

| Expanded Carrier Screening And Donor-Matching Tools | +0.5% | National, with early gains in California, New York, and Illinois | Medium term (2-4 years) |

| Clinic-Cryobank Partnership Models | +0.4% | National, concentrated in the Mid-Atlantic, Southeast, and Pacific Northwest | Short term (≤ 2 years) |

| At-Home Collection And Digital Preservation Access | +0.4% | National, with early uptake in high broadband metros and expansion into suburban and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Delayed Parenthood and Male Fertility Decline

Later parenthood is widening the gap between the years when many men are building careers and the years when fertility is strongest, and that timing mismatch is supporting earlier preservation decisions across the US sperm bank market. This change is moving sperm banking beyond medically diagnosed infertility and into preventive use by men who want to preserve options before cancer care, military deployment, aging, or a delayed family-building decision. That matters financially because samples that enter storage earlier can stay active for years, which extends billing duration and makes long-term storage revenue less tied to immediate treatment cycles. The US sperm bank market also benefits from wider awareness that semen quality does not stay constant and can deteriorate before a fertility issue is formally diagnosed. A peer-reviewed article in Cell Death Discovery reported a continuing annual decline in sperm concentration, reinforcing the case for earlier preservation and more frequent testing among men who still see themselves as healthy. This leaves the US sperm bank market with a firmer recurring revenue base than one built only on donor vials for near-term conception.

LGBTQ+ and Single-Woman Family Building

The user mix in the US sperm bank market has moved decisively toward single women and LGBTQ+ households, and this change is now central to how demand is formed. A 2026 Boston University Law Review analysis found that unpartnered women and LGBTQ+ people together account for nearly 75% of those using donor sperm in assisted reproduction. NPR reported in January 2026 that more single women in their 40s are using IVF to have children, which keeps donor sperm demand active outside the older treatment pattern centered on heterosexual couples with infertility. Marketplace reported in 2025 that clinics were seeing continued growth in inquiries from single women planning parenthood on their own timeline, which supports a steady intake pipeline for the US sperm bank market. These clients often approach treatment as a deliberate family-building decision, which can make demand more stable even when care is paid out of pocket. The US sperm bank market also benefits because many recipients want formal screening, traceable records, and clear legal documentation that licensed cryobanks can offer more consistently than informal arrangements.

Employer-Funded Fertility Benefits Expansion

Employers are turning fertility benefits into a broader workforce benefit, and sperm freezing is moving with that shift in benefit design across the US sperm bank market. The Departments of Labor, Health and Human Services, and the Treasury published a proposed rule in May 2026 to create an excepted fertility benefit category under ERISA and the ACA, with a target effective date of January 2027[1]“Excepted Fertility Benefits,” Federal Register, federalregister.gov. This matters because employers could offer sperm banking or donor sperm support on a carve-out basis without triggering the full set of market reform requirements tied to standard medical coverage. Large institutions were already moving in this direction, with Microsoft covering sperm freezing in its 2025 Progyny benefit and Yale University and Baylor University offering egg and sperm freezing coverage effective in 2026. Once samples enter employer-sponsored plans, annual storage, renewals, and related services can continue well beyond the initial collection event. That recurring payment pattern gives the US sperm bank market a more durable institutional demand channel than it had when most users paid fully out of pocket.

Expanded Carrier Screening and Donor-Matching Tools

Genetic screening is becoming 1 of the clearest value-added layers in donor selection, and that is raising the revenue contribution of counseling and matching work in the US sperm bank market. A 2024 review in the National Library of Medicine noted that panethnic expanded carrier screening is now widely favored in gamete donation because ethnicity-based panels can miss meaningful risk in a multiethnic population. The same review described leading practice settings using panels that test hundreds of genes, which raises both the complexity and the value of donor matching discussions for intended parents. This helps explain why Genetic Counseling and Donor Matching Support is the fastest-growing service line in the US sperm bank market, as providers can charge more for support that reduces uncertainty at the point of donor selection. Screening also narrows the eligible donor pool, which makes well-curated donor catalogs more valuable to clinics and consumers once a donor has cleared the full process. Banks that combine screening results, phenotype information, and guided matching can hold a stronger position in the US sperm bank market than sellers that compete mainly on catalog volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Donor Sperm And Storage Costs | -0.6% | National, most acute in states without insurance mandates covering donor sperm | Long term (≥ 4 years) |

| Stringent Donor Screening Constraining Supply | -0.4% | National, affecting all FDA-licensed facilities under 21 CFR Part 1271 | Long term (≥ 4 years) |

| Consumer DNA Databases Weakening Anonymity | -0.3% | National, with higher regulatory pressure in Colorado and Washington | Medium term (2-4 years) |

| State Disclosure And Recordkeeping Divergence | -0.2% | Highest in Colorado and Washington, with spillover into interstate operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Donor Sperm and Storage Costs

Cost remains the clearest barrier for people who must pay directly for donor sperm, storage, and related fertility treatment without employer support or state-level benefit help. This pressure is strongest outside large employer plans and outside states where fertility coverage is already more established, which keeps parts of the US sperm bank market reliant on self-funded demand. The problem is especially visible in direct-to-consumer preservation, where the service is easier to access but reimbursement is still uneven and often absent. Microsoft, Yale University, and Baylor University now cover sperm freezing through benefit arrangements, but those examples also show how selective current access remains rather than how universal it has become. The proposed federal fertility benefit rule may improve access over time, but it has not yet removed the heavy out-of-pocket burden many families still face in 2026. Until coverage broadens materially, price will keep limiting conversion in the US sperm bank market, especially in services that depend on planned but discretionary family-building decisions.

Stringent Donor Screening Constraining Supply

Supply growth is constrained by a screening process that is intentionally difficult to pass, and this remains the main operating bottleneck in the US sperm bank market. FDA rules require donor testing for a broad infectious disease panel, and anonymous donor samples also face quarantine and repeat testing before release into clinical use[2]“Testing Donors of Human Cells, Tissues, and Cellular and Tissue-Based Products,” US Food and Drug Administration, fda.gov. When those requirements are combined with expanded genetic screening and semen quality thresholds, the usable donor pool narrows very quickly even before demand screening by recipient preferences begins. Inception Fertility said in May 2026 that MySpermBank accepts fewer than 1% of donor applicants, showing how little slack exists on the supply side even as demand expands. A thin donor pipeline creates stockouts for sought-after profiles and can slow treatment timing for clinics and recipients alike. This means the US sperm bank market can lose revenue even when demand is present, because the limiting factor becomes qualified inventory rather than buyer interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Donor Banking Leads Volume, Genetic Counseling Drives Value

Donor Sperm Banking and Distribution held 38.31% of the US sperm bank market share in 2025, making it the main volume center within the US sperm bank market. Every donor conception cycle passes through this layer, so it benefits from both clinic referrals and direct buyer demand even when the end use varies. That volume base is reinforced by the way clinics depend on stable donor catalogs, reliable shipping, and repeat purchases across insemination and IVF cycles. Client Sperm Banking and Long-Term Storage adds a separate demand stream, because healthy men, cancer patients, and employer-sponsored users are preserving samples earlier than before. Semen Analysis and Male Fertility Testing also supports activity, but part of this work is moving outside clinic walls as home-based collection and mail-in testing become more accepted across the US sperm bank market.

Genetic Counseling and Donor Matching Support is projected to grow at a 6.38% CAGR through 2031, the fastest service rate within the US sperm bank market size by service. This service is gaining value because expanded carrier screening, phenotype review, and disclosure questions are harder for intended parents to navigate without professional support. A 2025 study in the Journal of Assisted Reproduction and Genetics reported that Cryos International shifted from the term anonymous to non-ID release, reflecting how genetic databases are reshaping expectations around donor identity. That language change increases the need for counseling during donor choice, because recipients now weigh future identity access more directly than they did in earlier years. Directed Donor Screening and Quarantine remains smaller and slower to scale, but it keeps a durable role because regulated handling and release rules are difficult to bypass in the US sperm bank industry.

By Donor Type: Known Donor Ascendancy Reshapes Market Architecture

Known Donor accounted for 55.24% share of the US sperm bank market size in 2025 and is also projected to grow at a 4.52% CAGR through 2031. That combination shows that the leading donor type is still gaining momentum rather than giving way to a smaller emerging niche. The appeal of known donation is practical, because recipients can secure clearer expectations around communication, family limits, and identity disclosure while still using a licensed process. It also fits the preferences of many LGBTQ+ families who want openness but still want screening, recordkeeping, and legal structure through a regulated bank. Colorado's donor disclosure framework, effective from January 2025, has added more pressure toward transparent arrangements by tightening how identifying information and medical history must be handled.

Identity-Release Donor is acting as a middle option for recipients who want future access for the child without managing a preexisting personal relationship with the donor. Anonymous Donor still serves part of the US sperm bank market, especially where buyers prioritize immediate privacy or a donor profile not easily available in known donor channels. Even so, a 2026 article in BMC Medical Ethics noted that direct-to-consumer genetic testing is creating new ethical and practical challenges for gamete donor conception, which weakens the real-world durability of promised anonymity. A 2025 study in the Journal of Assisted Reproduction and Genetics found that donor applicants more often shifted from non-ID release to ID release than the reverse, showing that supply-side expectations are moving in the same direction as recipient demand. Together, these trends are changing how the US sperm bank industry positions donor transparency, counseling, and legal risk across its catalogs.

By End User: Clinic Dominance Is Durable, but DTC Is the Growth Engine

Fertility Clinics and IVF Centers held 79.52% of the US sperm bank market share in 2025, showing how central referral pipelines remain to the US sperm bank market. Clinics dominate because controlled handling, lab oversight, and treatment coordination are still essential for many insemination and IVF pathways. Their importance is strengthened by preferred-partner arrangements, which steer procurement through a smaller set of trusted banks and reduce friction for patients. Fairfax Cryobank's partnership with IVI RMA North America, announced in March 2026, widened that institutional channel across 27 laboratories in North America. Hospitals and academic reproductive centers add dependable demand, but their buying decisions tend to follow formal compliance and quality review processes more than consumer preference.

Direct-to-Consumer Fertility Preservation is projected to expand at a 7.25% CAGR through 2031, the fastest end-user rate within the US sperm bank market size by end user. This growth reflects the appeal of home collection, mail-in logistics, and lower coordination burden for people who are not yet ready for full clinic engagement. Legacy's May 2026 launch of an upgraded at-home kit using ProteX collection technology showed how digital platforms are pursuing clinical credibility rather than convenience alone. Remote-collection models also benefit when they can route testing and storage through regulated laboratory systems instead of informal or unverified channels. As a result, the US sperm bank market is widening beyond clinic walls without fully breaking from medical quality standards.

Geography Analysis

The West Coast remains the clearest concentration point in the US sperm bank market because it combines large cryobank capacity with deep reproductive medicine infrastructure and high visibility among intended parents. California anchors this position through California Cryobank in Los Angeles and the Sperm Bank of California in Oakland, while the Pacific Northwest adds Seattle Sperm Bank and Cascade Cryobank to the regional network. California Cryobank's waiting lists for some donors exceeded 2,500 clients in 2026, showing how quickly supply tightens in high-demand coastal metros with strong clinic activity and high willingness to pay. Regulation is also moving fastest in this part of the country, with Colorado enforcing donor disclosure rules from January 2025 and Washington maintaining disclosure obligations under its Uniform Parentage framework[3]“2024 Revised Code of Washington § 26.26A.820, Information About Donor, Disclosure,” Justia US Law, law.justia.com. That mix of dense demand and heavier compliance tends to favor banks with legal resources, broad inventories, and established shipping systems.

The Northeast and Mid-Atlantic form the second major demand corridor in the US sperm bank market, supported by Fairfax Cryobank, New England Cryogenic Center, and fertility networks spanning New York, New Jersey, Pennsylvania, and Virginia. Fairfax operates the broadest national collection footprint among major peers, which helps it attract donors and clinic relationships across multiple states instead of relying on a single regional base. Employer fertility benefits are also more visible in this corridor, and Citi's 2026 benefit design shows that large corporate plans are willing to fund broader family-building support. The March 2026 Fairfax partnership with IVI RMA North America should matter most in this corridor because it ties donor supply more closely to a large laboratory and clinic base. This leaves the region well placed for repeat procurement, storage renewal, and higher-value counseling work as institutional coverage expands.

The South and Midwest are becoming the main expansion zone for the US sperm bank market as digital-first players look for demand outside the traditional coastal core. Inception Fertility launched MySpermBank from Houston in May 2026, directly targeting broader national reach through a digital-first model and The Prelude Network's clinic footprint. These regions also fit home collection models well, because long travel times can make in-person banking impractical for suburban and rural users. As at-home services improve collection technology and shipping control, the US sperm bank market can reach underserved areas without waiting for a full buildout of local collection sites.

Competitive Landscape

The US sperm bank market is moderately concentrated at the top and fragmented below that level, which creates a field where 2 large brands still matter but no single company appears able to set the terms for the whole market. California Cryobank and Fairfax Cryobank still hold the strongest positions through brand recognition, donor depth, and clinic relationships that have been built over time. Their advantage has less to do with low pricing and more to do with inventory quality, screening rigor, shipping reliability, and trusted placement in treatment settings. That model keeps the leading firms relevant, but it also leaves room for challengers that can lower friction in donor search, sample collection, and post-selection support. Competitive pressure in the US sperm bank market is therefore increasing most quickly where technology can simplify access without weakening compliance expectations.

Inception Fertility's May 2026 launch of MySpermBank is a strong example because it places sperm banking inside a broader fertility services platform that already includes other reproductive brands and clinic relationships. Fertio's March 2026 acquisition of Cascade Cryobank is another example, bringing European Sperm Bank capabilities and donor management systems into the United States through acquisition rather than slow organic entry. Fairfax also strengthened its position in March 2026 by partnering with IVI RMA North America, which linked its donor catalog more tightly to a large clinical network. These moves show that the next competitive step in the US sperm bank market is platform integration rather than stand-alone catalog growth. They also suggest that cross-border capital and clinic-led distribution will matter more than simple geographic expansion.

White space remains strongest in military, oncology, rural, and semi-urban use cases where access to a collection site is limited and the decision to preserve sperm can be time sensitive. Legacy is aiming at that gap with an upgraded home kit designed for wider clinical use, which shows how digital entrants are trying to build trust through validated collection tools rather than convenience claims alone. On the supply side, donor recruitment remains the most defensible advantage because strict screening means even modest gains in qualified applicants can widen inventory faster than price competition can. Banks that pair strong recruitment with transparent disclosure policies and reliable clinic partnerships should keep a durable edge in the US sperm bank market.

United States Sperm Bank Industry Leaders

California Cryobank

Fairfax Cryobank

Xytex Corporation

Seattle Sperm Bank

Cryos International USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Inception Fertility launched MySpermBank, a digital-first donor sperm platform operating as a wholly owned subsidiary within The Prelude Network's 90+ clinic footprint. The platform accepts fewer than 1% of donor applicants and offers IUI, ICI, and IVF vial formats, directly competing with California Cryobank and Fairfax Cryobank for the clinic-referred donor sperm segment across the US and Canada.

- March 2026: Fertio, the international fertility care group and parent company of European Sperm Bank, acquired Cascade Cryobank of Lynwood, Washington, its first entry into the US market. The acquisition pairs Fertio's 20+ years of global donor management technology with Cascade's Early Disclosure Program, establishing a US platform focused on transparency-led donor programs.

United States Sperm Bank Market Report Scope

As per the scope of the report, a sperm bank is a facility that collects, stores, and preserves sperm for future reproductive use. It provides sperm donation services to individuals or couples seeking assisted reproductive techniques such as artificial insemination or in vitro fertilization (IVF).

The United States sperm bank market is segmented by service into distribution and banking of donor sperm, long-term storage and banking of client sperm, testing male fertility and analyzing semen, screening and quarantine for directed donors, and support for donor matching and genetic counseling. By donor type, the market is categorized into donor with known identity, anonymous donor, and donor with identity release. By end user, the market is divided into IVF centers and fertility clinics, academic reproductive centers and hospitals, and clients seeking direct-to-consumer fertility preservation. For each segment, the market size and forecast are provided in terms of value (USD).

| Donor Sperm Banking and Distribution |

| Client Sperm Banking and Long-Term Storage |

| Semen Analysis and Male Fertility Testing |

| Directed Donor Screening and Quarantine |

| Genetic Counseling and Donor Matching Support |

| Known Donor |

| Anonymous Donor |

| Identity-Release Donor |

| Fertility Clinics and IVF Centers |

| Hospitals and Academic Reproductive Centers |

| Direct-to-Consumer Fertility Preservation Clients |

| By Service | Donor Sperm Banking and Distribution |

| Client Sperm Banking and Long-Term Storage | |

| Semen Analysis and Male Fertility Testing | |

| Directed Donor Screening and Quarantine | |

| Genetic Counseling and Donor Matching Support | |

| By Donor Type | Known Donor |

| Anonymous Donor | |

| Identity-Release Donor | |

| By End User | Fertility Clinics and IVF Centers |

| Hospitals and Academic Reproductive Centers | |

| Direct-to-Consumer Fertility Preservation Clients |

Key Questions Answered in the Report

What is driving demand for sperm banking in the United States?

Demand is being supported by a broader user base that now includes large numbers of single women and LGBTQ+ households, along with more preventive freezing by men who want to preserve fertility earlier. The US sperm bank market is projected to reach USD 2.26 billion by 2031 from USD 1.90 billion in 2026 at a 3.52% CAGR.

Which service category leads revenue and which is growing fastest?

Donor Sperm Banking and Distribution led with 38.31% share in 2025. Genetic Counseling and Donor Matching Support is the fastest-growing service segment with a 6.38% CAGR through 2031.

Why are known donors gaining traction in donor programs?

Known Donor held 55.24% share in 2025 and is also the fastest-growing donor type at a 4.52% CAGR through 2031. The shift reflects stronger demand for clarity on identity, disclosure, and future communication.

Why do fertility clinics still dominate end-user demand?

Fertility Clinics and IVF Centers accounted for 79.52% share in 2025 because lab control, treatment coordination, and referral relationships still matter for many insemination and IVF cases. Clinic-bank partnerships also keep procurement concentrated in established channels.

How important is the direct-to-consumer channel now?

Direct-to-Consumer Fertility Preservation is the fastest-growing end-user category at a 7.25% CAGR through 2031. Growth is being supported by home collection, mail-in logistics, and better clinical validation for remote kits.

What is the biggest risk holding back growth?

The main risk is supply, not demand. Strict donor screening and quarantine rules keep acceptance rates extremely low, and MySpermBank reported accepting fewer than 1% of donor applicants in 2026.

Page last updated on: