Global Sperm Bank Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.12 Billion |

| Market Size (2031) | USD 7.2 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

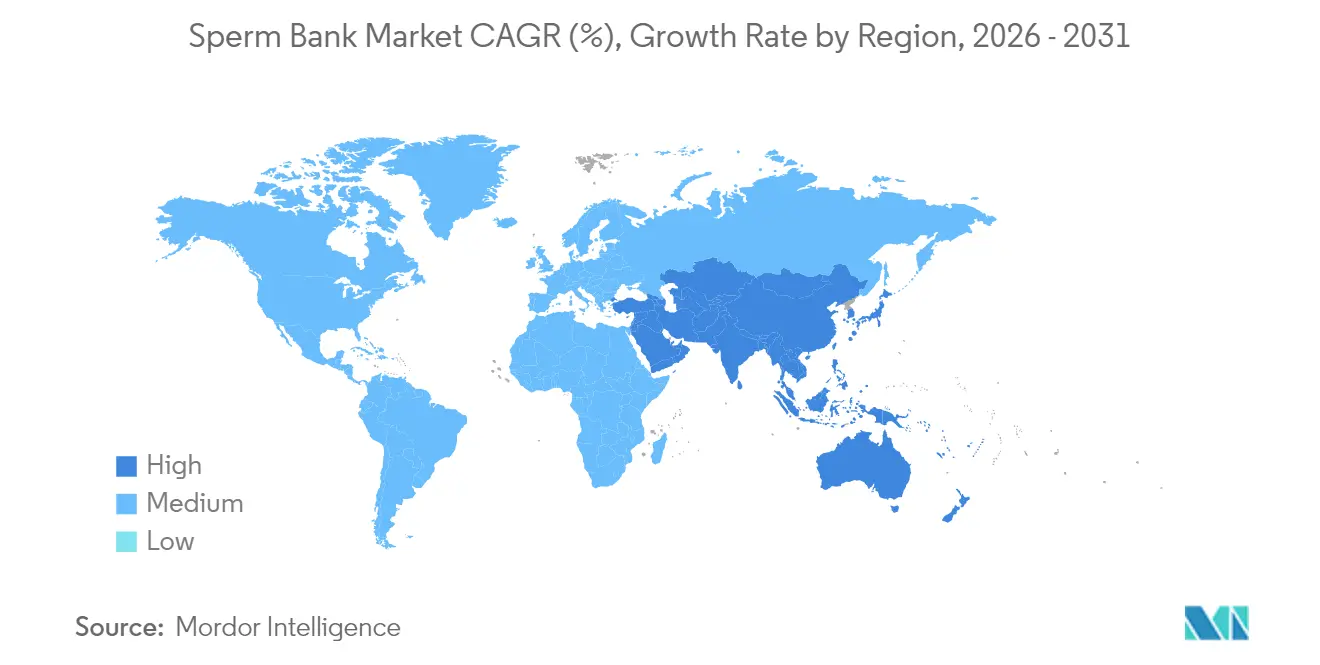

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

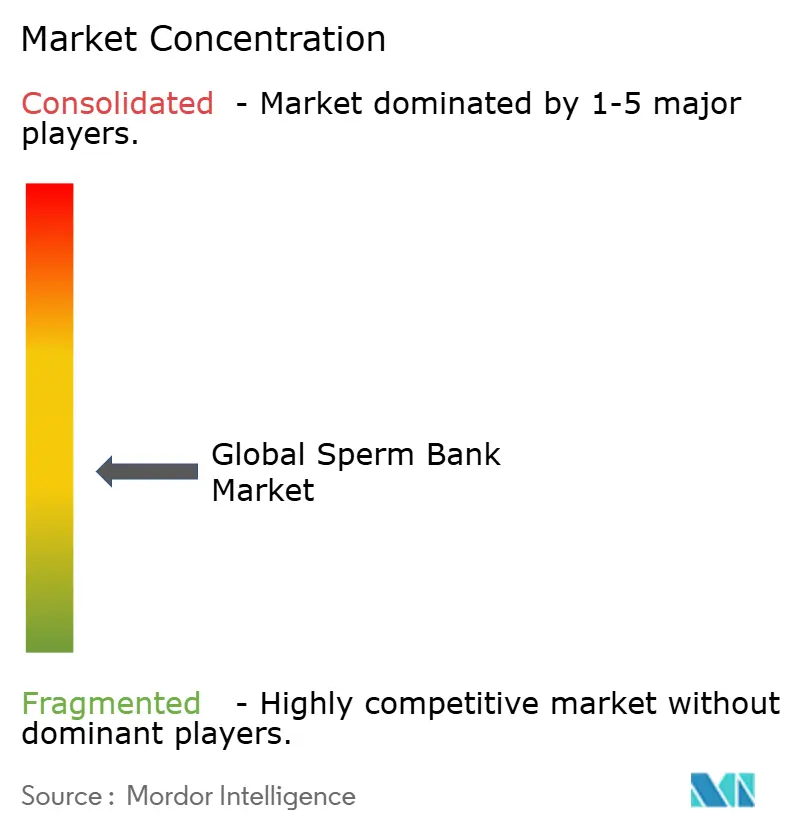

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Sperm Bank Market Analysis by Mordor Intelligence

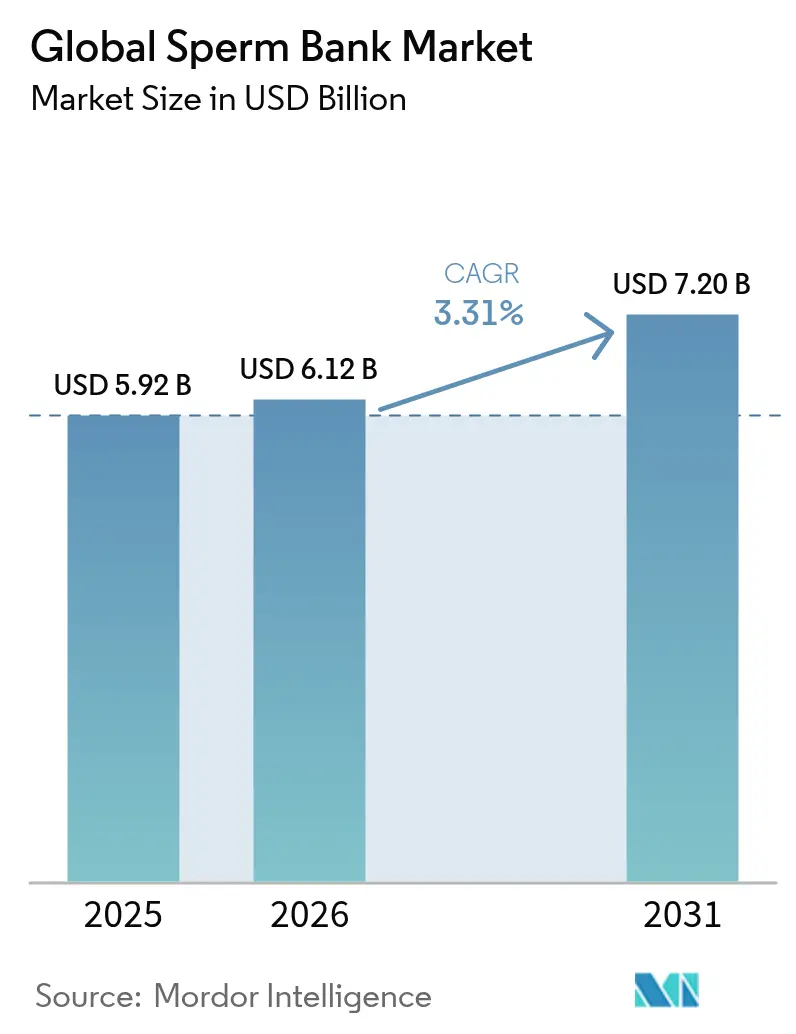

The sperm bank market size is expected to grow from USD 5.92 billion in 2025 to USD 6.12 billion in 2026 and is forecast to reach USD 7.2 billion by 2031 at 3.31% CAGR over 2026-2031. Sustained demand stems from a mix of biological pressures—declining sperm quality—and sociocultural changes that normalize diverse family structures. Recent regulatory shifts, including the Food and Drug Administration’s decision to allow donations from gay and bisexual men, could expand the donor pool by an estimated 15% and help close long-standing shortages among underrepresented ethnic groups. Employer health plans are broadening coverage for fertility preservation, and large financial-services firms now pay up to USD 24,000 for qualified fertility expenses plus USD 7,500 for medications, effectively lowering out-of-pocket costs for salaried employees. Technological improvements in vitrification are raising post-thaw survival rates above 86%, and room-temperature storage research hints at future operating-cost reductions of 40-60%. The convergence of these forces positions the sperm bank market for steady mid-single-digit growth through the end of the decade.

Key Report Takeaways

- By service type, sperm storage held 45.90% of sperm bank market share in 2025, while genetic consultation is on track for a 4.58% CAGR to 2031.

- By donor type, known donor arrangements accounted for 58.10% of the sperm bank market size in 2025; other/directed donors are growing fastest at 4.89% CAGR.

- By end-user, cancer patients represented 30.20% of the overall volume in 2025 and anchor recurring demand, whereas the “other end-users” segment is pacing ahead at 5.02% CAGR.

- By region, North America led with a 35.10% revenue share in 2025; Asia–Pacific is the fastest-expanding geography, with a 4.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Sperm Bank Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising infertility rates and delayed parenthood | +1.2% | Global—highest in advanced economies | Long term (≥ 4 years) |

| Growing acceptance of LGBTQ+ and single-parent families | +0.8% | North America and Europe; expanding to Asia–Pacific | Medium term (2-4 years) |

| Employer-sponsored fertility benefits | +0.7% | North America; emerging in Europe and Asia–Pacific | Short term (≤ 2 years) |

| Advances in cryopreservation and genetic screening | +0.6% | Global—innovation led by the United States and Europe | Medium term (2-4 years) |

| Direct-to-consumer sperm-freezing start-ups | +0.4% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Fertility tourism to donor-friendly hubs | +0.3% | Global; flows from restrictive to permissive states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infertility Rates and Delayed Paternity/Maternity

Male fertility has deteriorated sharply, with peer-reviewed studies[1]Hai, E. “Sperm freezing damage: the role of regulated cell death.” Cell Death Discovery, nature.com showing sperm concentrations falling 2.64% per year since 2000. At the same time, the average age of first-time fathers has climbed above 31 years, creating a widening gap between peak reproductive ambition and biological reality. As a result, healthy men are banking sperm earlier in life, a behavior that was marginal a decade ago but now forms a notable slice of the sperm bank market. Clinics report that many of these clients are professionals with time-sensitive career plans who view storage as an insurance policy against age-related decline. This secular demand, layered atop medical-necessity volumes, underpins a resilient baseline for revenue growth.

Growing Acceptance of LGBTQ+ and Single-Parent Families

Same-sex couples and single individuals now comprise roughly one-quarter of patients at urban fertility centers. Forthcoming federal rule changes that eliminate historic donor restrictions are expected to broaden donor diversity and temper premium pricing for scarce profiles. Insurers are beginning to treat family-building for non-heterosexual members as a basic health need; for instance, a major national payer recently extended intrauterine insemination coverage to all eligible plans irrespective of sexual orientation. Together, these shifts expand the addressable population for the sperm bank market and encourage further normalization of donor sperm use.

Employer-Sponsored Fertility Benefits

Large US employers have upgraded fertility packages from limited in-network reimbursements to full “family-building” programs that include sperm freezing, genetic testing, and multiple assisted-reproduction cycles. Progyny, a publicly traded benefit administrator, disclosed USD 787 million in 2022 revenue, underscoring demand from corporate clients. Employers favor bundled, predictable pricing, while employees gain elective coverage that previously required personal financing. The new B2B2C channel reroutes patient traffic away from traditional clinics and into networks curated by benefit managers, giving the sperm bank market a more diversified revenue base.

Advances in Cryopreservation and Genetic Screening

Modern vitrification yields post-thaw viability rates above 86%[2]Jing Shen, “Oocytes Vitrification Using Automated Equipment Based on Microfluidic Chip,” ResearchGate, researchgate.net, compared with 60-70% for older slow-freeze protocols. Concurrently, polygenic risk scoring is moving from research labs into commercial pilots, letting prospective parents rank embryo cohorts for specific health markers. Although clinical utility remains contested, the service fetches premium pricing. Researchers are also testing freeze-dried sperm stored at ambient temperature that retains fertilization capacity in animal models. If validated in humans, the method could cut ongoing storage costs in half, altering long-term profitability assumptions for the sperm bank market.

Restraints Impact Analysis of Global Sperm Bank Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness and stigma in emerging markets | −0.9% | Asia–Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Regulatory variability on donor anonymity and quotas | −0.6% | Global—highest in Europe and Asia–Pacific | Medium term (2-4 years) |

| Donor supply pressures from DNA de-anonymization | −0.5% | North America and Europe | Medium term (2-4 years) |

| Ethical pushback on expanded genetic screening | −0.3% | Developed markets with active bioethics committees | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Awareness and Social Stigma in Emerging Markets

Cultural taboos leave many men unwilling to seek evaluation, limiting penetration despite rising disposable income. Outside large metropolitan centers, clinics struggle to recruit diverse donors; in the United States, Black men make up fewer than 3% of available donors, a deficit that restricts matching options for intended parents of color. Community-focused outreach and localized education campaigns are necessary to unlock the full potential of the sperm bank market in these regions, though progress is likely to be gradual.

Regulatory Variability on Donor Anonymity and Quotas

Colorado’s Donor-Conceived Persons Protection Act, effective January 2025, caps family units per donor at 25 and mandates identification-option donors over the age of 21, compelling sperm banks to segment inventory by jurisdiction. The European Union’s forthcoming rules on substances of human origin, slated for August 2027, will standardize several compliance areas but also impose new documentation burden. Maintaining separate operational protocols for each market drains resources and complicates cross-border scale-up, tempering the global growth curve for the sperm bank market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Sperm Bank Market Segment Analysis

By Service:

Storage Dominance with Consultation GrowthSperm storage retained 45.90% of sperm bank market share in 2025 as patients prioritize safeguarding fertility ahead of chemotherapy, vasectomy, or age-related decline. Because storage fees recur annually and are often bundled with transport or thawing charges, the category contributes a disproportionate share of margin to the sperm bank market. Genetic consultation, while only a midsized revenue stream today, is expanding at a 4.58% CAGR to 2031, propelled by rising uptake of expanded carrier screening and polygenic risk tools. The growing importance of genetic literacy means clinics now employ in-house counselors to translate complex results into actionable recommendations. Over time, consultation revenue is expected to anchor higher-value packages that blend testing, counseling, and storage, reinforcing customer stickiness.

Semen analysis still forms a baseline diagnostic step, yet novel algorithms can derive fertility probabilities from routine blood tests with 74% accuracy. If commercialized at scale, such tools could shift basic analysis from laboratory microscopes to telehealth kits, forcing laboratories to reposition as advanced-testing providers. Specialty retrieval procedures—such as microsurgical epididymal sperm aspiration—and hormone modulation therapies round out the service mix. Operators that integrate these disparate offerings into seamless, app-based journeys may capture a larger share of wallet from tech-savvy patients. As such, the sperm bank market is gradually evolving from a single-product niche to a multilayer clinical services ecosystem.

By Donor Type:

Known Donors Lead Amid Transparency PressuresKnown donors accounted for 58.10% of the sperm bank market size in 2025, reflecting an enduring preference for medical and genetic transparency. DNA databases make true anonymity tenuous, prompting many recipients to select donors open to contact once offspring reach adulthood. Directed or other donor categories, registering a 4.89% CAGR, capture patients seeking granular control over donor ethnicity, education, and phenotype. Because these arrangements are often bespoke, they command higher pricing that offsets smaller volume.

Anonymity rules continue to tighten: several Australian states now require donor identity disclosure upon request, and similar bills are under debate in U.S. state legislatures. Banks must therefore design consent frameworks that balance donor privacy with evolving legal norms. Expanded eligibility, including the FDA’s removal of bans on gay and bisexual donors, is expected to relieve supply constraints and diversify profiles. Providers that streamline onboarding, automate infectious-disease testing, and offer clear counseling will likely capitalize on the shift, bolstering long-term resilience of the sperm bank market.

By End-User:

Oncology Leads; Elective Preservation AcceleratesCancer patients represented 30.20% of the sperm bank market share in 2025, underpinned by guidelines that mandate fertility counseling ahead of gonadotoxic treatment. Partnering with oncology networks secures predictable referrals, and some banks station mobile collection units near radiation centers to simplify logistics. Because long-term storage is commonplace for this cohort, average revenue per user skews higher than for elective cases. Meanwhile, the “other end-users” category—covering healthy men, transgender patients pre-transition, and high-risk occupation workers—exhibits a 5.02% CAGR and captures lifestyle-driven motivations. Marketing pivots toward convenience, privacy, and empowerment resonate strongly with this segment, nurturing brand loyalty.

Pre-vasectomy banking forms a stable but modest pillar; surgeons frequently recommend storage as a hedge against regret. Taken together, these trends indicate that the sperm bank market is shifting from reactive, medically dictated usage toward proactive life-planning behavior. Clinics that segment messaging by life stage and design modular packages stand to deepen share of household reproductive spending.

Geography Analysis

North America Sperm Bank Market

North America controlled 35.10% of the sperm bank market in 2025 and is projected to expand at a 3.18% CAGR through 2031. State mandates such as California’s SB 729 are broadening insurance coverage, and a February 2025 executive order promises streamlined federal benefits and enhanced facility security after a high-profile clinic attack. The FDA’s new donor-eligibility rules should ease diversity shortages, reducing wait times for minority families. A mature digital-health ecosystem lets clinics integrate direct shipping kits, teleconsults, and automated reminders, lowering friction for repeat transactions.

Europe Sperm Bank Market

Europe exhibits slower 2.98% growth but benefits from forthcoming harmonization under the 2027 substances-of-human-origin regulation. Denmark remains a prolific exporter, leveraging liberal compensation guidelines to supply global demand, while the United Kingdom’s cap on family units pushes surplus inventory abroad. Regulatory arbitrage has created intricate supply routes; operators that master cross-border compliance may unlock new revenues, though higher documentation costs could squeeze smaller labs out of the sperm bank market.

APAC Sperm Bank Market

Asia–Pacific is the standout growth engine at 4.55% CAGR. Middle-class expansion, rising female workforce participation, and competitive procedure pricing are attracting intra-regional medical tourists. For example, complete IVF cycles cost USD 2,700 in India compared with USD 10,200 in Singapore, prompting patients to travel for both treatment and donor sperm. Yet fragmented regulation and a shortage of trained embryologists cap immediate capacity. Public-private partnerships that subsidize laboratory certification programs and accelerate technology transfer could unlock latent demand, reinforcing the long-run opportunity set for the sperm bank market.

Competitive Landscape

The sperm bank market remains fragmented. No player controls more than a mid-single-digit share, leaving ample room for consolidation. Legacy operators such as Fairfax Cryobank and California Cryobank maintain comprehensive donor screening pipelines, nationwide shipping, and relationships with over 400 reproductive endocrinology clinics, giving them scale in compliance and logistics. Digital-first entrants like Legacy, Fellow, and Posterity Health compete primarily on user experience; direct-to-consumer kits, subscription-style storage, and transparent ancestry reports appeal to millennials comfortable managing healthcare online.

Technology now defines competitive edges. AI-assisted imaging platforms can rank motile sperm in seconds, promising improved selection for intracytoplasmic sperm injections. Devices such as the Q300 deploy optical coherence tomography to isolate top-quality cells, and early clinical data associate usage with higher fertilization rates. Larger laboratories deploy automated cryogenic monitoring systems that trigger real-time alerts if liquid-nitrogen levels fluctuate outside tolerance bands. Capital expenditures for these systems run into the millions, creating a barrier that smaller operators struggle to clear.

Financial sponsors are already shaping market structure. In December 2024, private-equity firm Astorg closed a USD 228 million purchase of Hamilton Thorne’s fertility-equipment division, citing cross-sell potential into cryobank customers. Analysts expect similar roll-ups targeting specialized retrieval centers or regional player clusters. Over time, firms with robust donor databases, proprietary analytics, and diversified service lines may emerge as “platform” consolidators, pushing the sperm bank market toward moderate concentration.

Global Sperm Bank Industry Leaders

California Cryobank

Cryos International

European Sperm Bank

Fairfax Cryobank

Seattle Sperm Bank

- *Disclaimer: Major Players sorted in no particular order

Global Sperm Bank Market Companies Covered in this Report

- Androcryos

- California Cryobank

- CryoGam Colorado

- Cryos International

- Denmark Nordic Cryobank

- European Sperm Bank

- Fairfax Cryobank

- FNCB (French National Cryobank)

- Guangzhou Sun Yat-sen Cryobank

- Indian Spermtech

- Legacy (Digital Sperm Banking)

- London Sperm Bank

- New England Cryogenic Center

- NW Cryobank

- Reproductive Medicine Associates (RMA)

- ReproTech Ltd.

- Seattle Sperm Bank

- Shanghai Human Sperm Bank

- SpermFreez Israel

- Xytex

Recent Industry Developments in Global Sperm Bank Market

- February 2025: President Trump signed an executive order to broaden IVF access for military families and federal employees, including directives for enhanced clinic security and streamlined insurance approvals.

- February 2025: Posterity Health raised USD 14 million in Series A funding to scale digital and in-clinic male fertility services, noting that 60% of patients arrive via physician referral and 40% through payer networks.

- January 2025: Colorado’s Donor-Conceived Persons Protection Act took effect, setting a 25-family limit per donor and requiring all sperm to originate from ID-option donors aged 21 or above.

- December 2024: Astorg completed a USD 228 million acquisition of Hamilton Thorne Ltd., expanding its reproductive-medicine equipment portfolio.

Global Sperm Bank Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the sperm bank market as the aggregate revenue generated by licensed facilities that procure, screen, freeze, store, and dispense human semen for assisted reproductive procedures such as donor insemination and in-vitro fertilization. The universe spans services, sperm storage, semen analysis, genetic consultation, and all donor types, across clinics, hospitals, and stand-alone cryobanks, in 17 major nations.

Scope exclusion: Animal genetics banks and direct-to-consumer home insemination kits fall outside our remit.

Segments Covered in This Report

- By Service

- Sperm Storage

- Semen Analysis

- Genetic Consultation

- Other Services

- By Donor Type

- Known Donor

- Anonymous Donor

- Other / Directed Donors

- By End-User

- Pre-vasectomy Patients

- Cancer Patients

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed reproductive endocrinologists, cryobank directors, embryologists, and payor liaisons across North America, Europe, and key Asia-Pacific hubs. These discussions clarified real-world utilisation rates, donor rejection percentages, and price dispersion, letting us adjust desk findings and align assumptions with current clinical practice.

Desk Research

We began with public health and ART registries, notably the WHO infertility fact sheets, the CDC National ART Surveillance System, and the European Society of Human Reproduction and Embryology datasets, which reveal country-level treatment cycles and success ratios. Policy and reimbursement insights were drawn from government gazettes and OECD health statistics, while trade associations such as the American Society for Reproductive Medicine provided clinical benchmark rates.

Company filings, clinic prospectuses, and investor decks supplied average selling prices for donor vials and annual storage fees, which we screened through D&B Hoovers and Dow Jones Factiva to filter anomalies. Additional shipment clues came from Volza import records for cryogenic media. The sources cited illustrate our approach; many more were consulted for verification and context.

Market-Sizing & Forecasting

A top-down model starts with national ART treatment volumes, couples this with average vials per cycle and median vial pricing to recreate 2025 revenue pools, which are then sense-checked through selective supplier roll-ups and sampled clinic invoices. Variables such as infertility prevalence, numbers of licensed sperm banks, average donor compensation, cross-border fertility tourism flows, and evolving same-sex parenting laws feed the base year and inform elasticity factors. Multivariate regression, enriched by expert consensus on regulatory and demographic drivers, projects figures to 2030. Gaps where bottom-up evidence is weak are bridged using region-specific price-volume proxies derived from primary calls.

Data Validation & Update Cycle

Our team conducts variance and plausibility checks, comparing outputs with external health spend ratios and cryogenic equipment sales. Senior reviewers sign off after anomaly resolution. Reports refresh annually, with mid-cycle revisions when material policy or technology shifts emerge. Every delivery includes a last-minute data sweep.

How Mordor Intelligence's Global Sperm Bank Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose differing geographic mixes, donor definitions, and refresh cadences.

Key gap drivers include whether anonymous-only collections are counted, how home insemination sales are treated, base-year currency conversions, and the frequency at which new clinic openings are captured before model lock-in. Mordor's disciplined scope, yearly refresh, and dual-track validation reduce those skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.92 B (2025) | Mordor Intelligence | - |

| USD 5.10 B (2023) | Global Consultancy A | Excludes Asia-Pacific micro-clinics and applies static ASPs |

| USD 4.94 B (2024) | Regional Consultancy B | Omits genetic consultation revenue; uses 2022 exchange rates |

| USD 3.54 B (2024) | Trade Journal C | Limits scope to storage fees; none of the donor insemination service revenue captured |

These contrasts show that, by aligning clinical volumes with full service lines and updating inputs each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is driving employer interest in offering sperm banking as an employee benefit?

Employers are adding sperm banking because it helps them attract and retain talent, positions them as family-friendly, and can reduce long-term medical costs by supporting early fertility preservation.

How are advances in cryopreservation technology changing service offerings at sperm banks?

New vitrification and monitoring systems improve post-thaw survival and reduce storage risks, allowing banks to market longer storage terms and bundled preservation packages with greater confidence.

Why are known-donor programs gaining popularity over anonymous donations?

DNA ancestry websites make anonymity difficult to guarantee, and many intended parents prefer transparent medical histories and the option for future contact, leading clinics to expand identity-release options.

What role does genetic counseling play in modern sperm bank services?

Genetic counselors guide patients through expanded carrier screening and risk assessment, helping them understand potential hereditary conditions and make informed donor selections.

How are digital-first startups influencing competitive dynamics in the sperm bank industry?

App-based collection kits, telehealth consultations, and AI-driven sperm analysis tools give newcomers a convenience edge, prompting traditional clinics to upgrade their user experience and technology stack.

How do emerging donor anonymity laws influence inventory management strategies at sperm banks?

Laws that cap family limits or require identity-release donors force banks to segment inventory by jurisdiction and maintain parallel tracking systems, increasing operational overhead while making flexible sourcing agreements with partner clinics more valuable.

Page last updated on: