United States Sodium Reduction Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

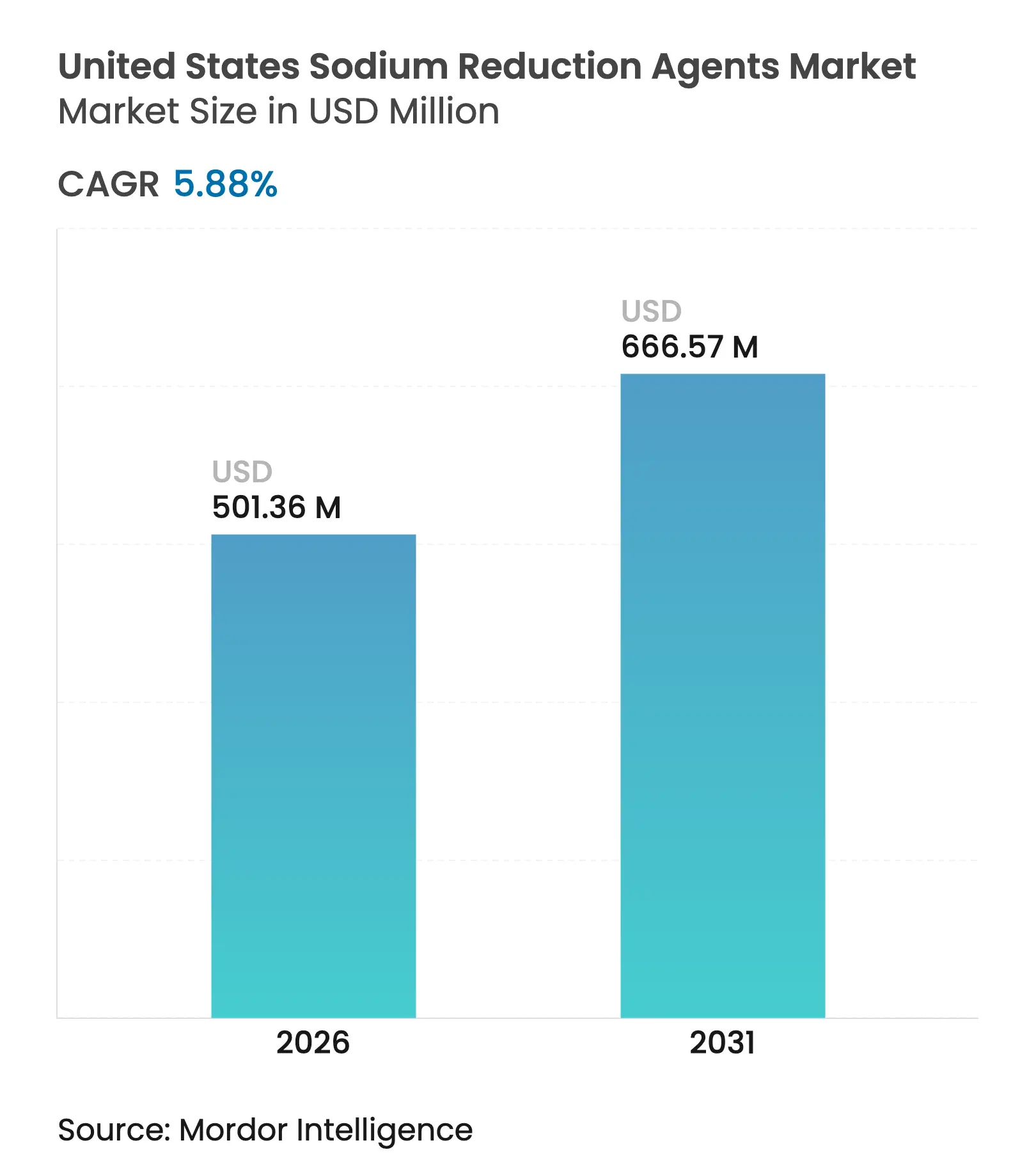

| Market Size (2026) | USD 501.36 Million |

| Market Size (2031) | USD 666.57 Million |

| Growth Rate (2026 - 2031) | 5.88 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United States Sodium Reduction Agents Market Analysis by Mordor Intelligence

The United States sodium reduction agents market size in 2026 is estimated at USD 501.36 million, growing from 2025 value of USD 473.54 million with 2031 projections showing USD 666.57 million, growing at 5.88% CAGR over 2026-2031. This growth trajectory reflects the convergence of regulatory pressure and health consciousness, with the FDA's Phase II voluntary sodium reduction targets aiming to lower average daily intake to 2,750 mg by 2030, according to the U.S. Food and Drug Administration[1]Source: U.S. Food and Drug Administration, “Guidance for Industry: Voluntary Sodium Reduction Goals,” fda.gov. The market's expansion is underpinned by preliminary data showing some achievement and creating momentum for ingredient suppliers to develop more sophisticated solutions. Synthetic solutions remain the workhorse of the United States sodium reduction ingredient market thanks to mature supply chains, but rapid advances in natural yeast extracts, mineral blends, and micro-particulate salts are lowering technical barriers. Ingredient suppliers that combine cost-effective production with sensory performance are well-positioned as FDA front-of-package labeling rules tighten. As a result, the US sodium reduction ingredient market continues to attract research and development spending from multinationals while providing white-space opportunities for niche innovators.

Key Report Takeaways

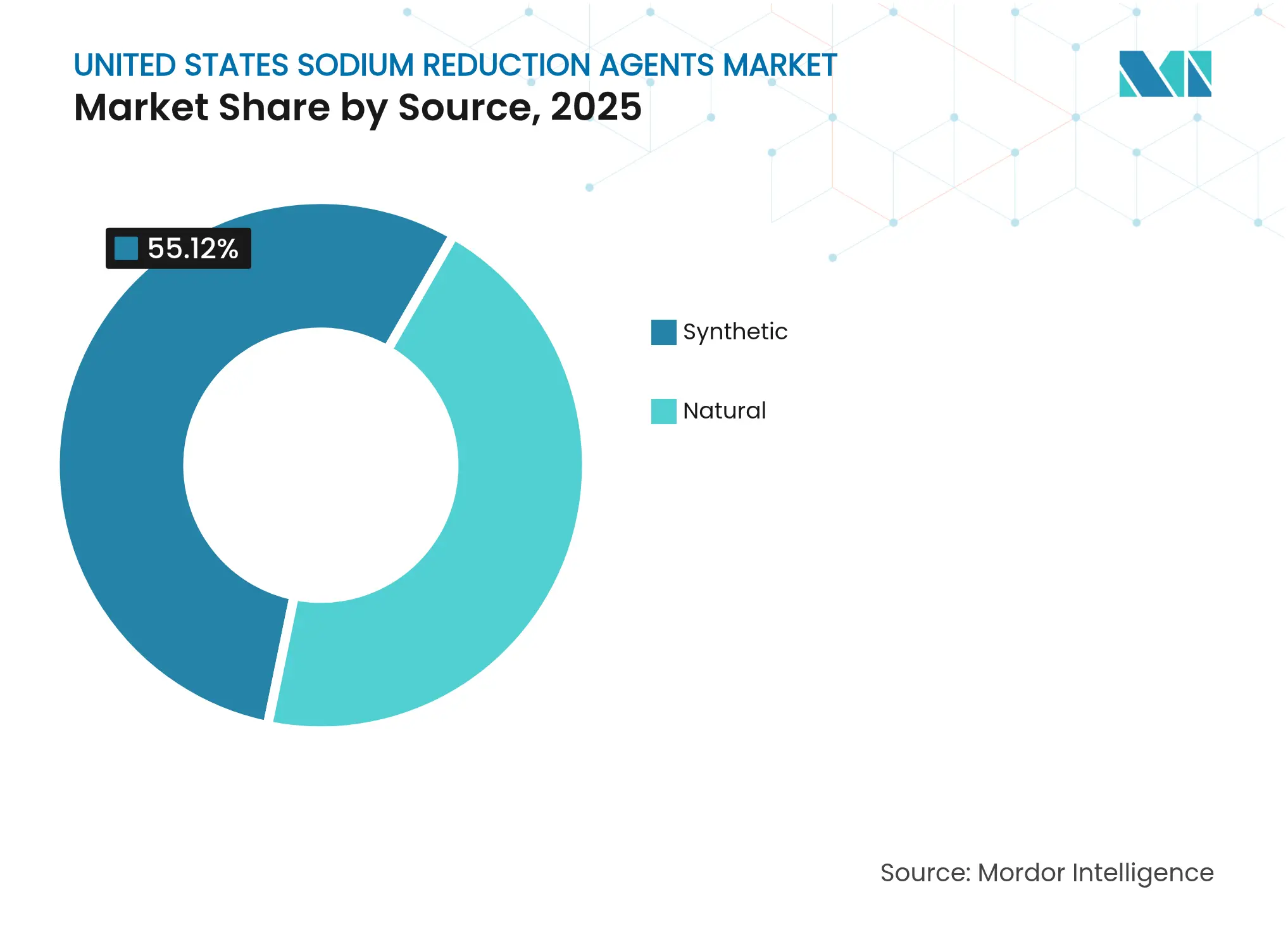

- By source, synthetic agents led with 55.12% of United States sodium reduction agents market share in 2025 while natural is projected to grow at 7.42% CAGR through 2031.

- By product type, mineral salts captured 39.20% share of the United States sodium reduction agents market size in 2025, while yeast-based agents are forecast to rise at an 8.45% CAGR to 2031.

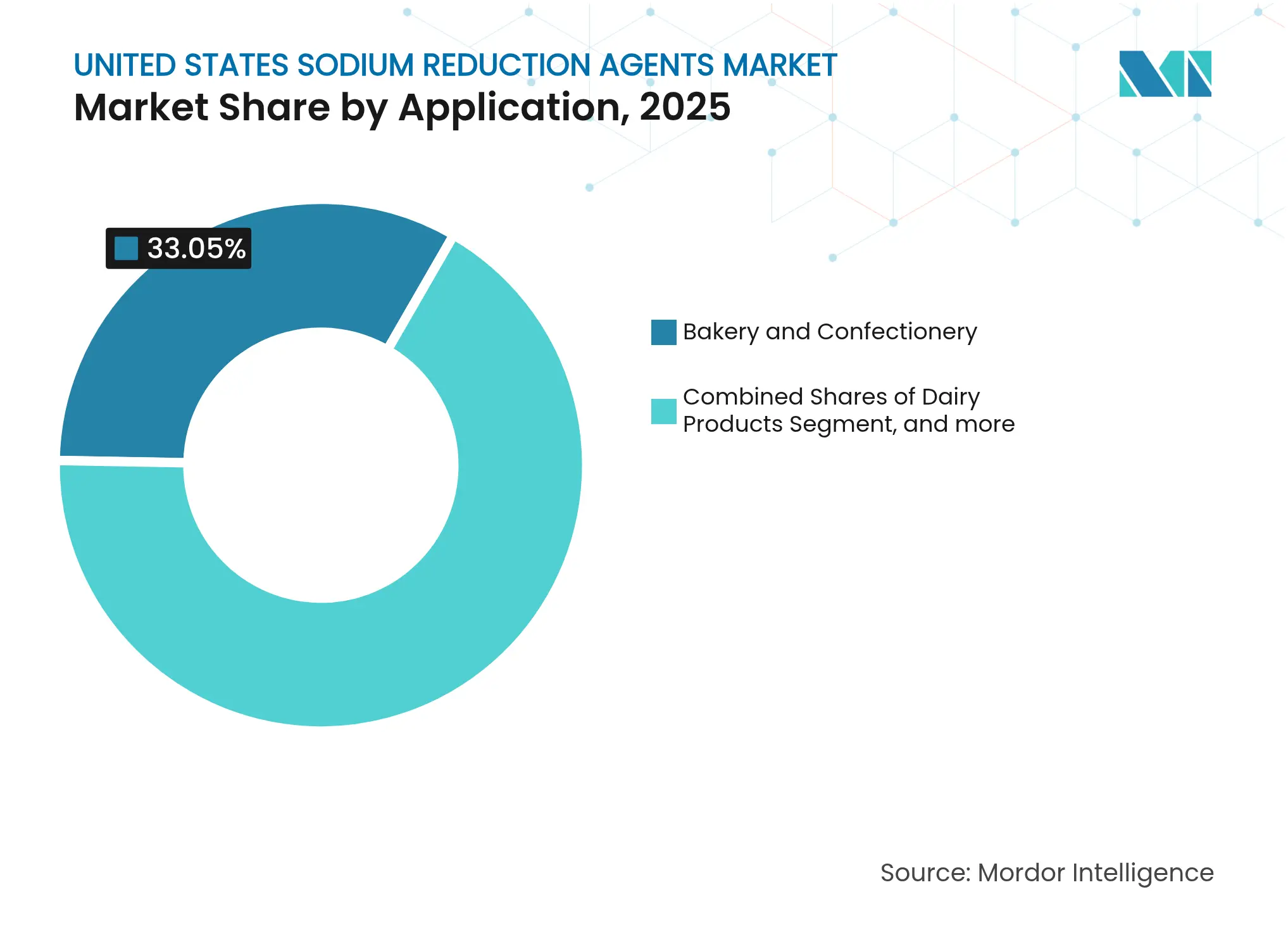

- By application, bakery and confectionery held 33.05% revenue share in 2025; dairy products record the highest projected 7.56% CAGR through 2031.

- By region, the Northeast dominated with 36.60% share in 2025, whereas the South is set for the fastest 8.12% CAGR between 2026-2031 within the United States sodium reduction agents market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Sodium Reduction Agents Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Health Consciousness and Awareness of Hypertension Rising Health Consciousness and Awareness of Hypertension | +1.2% | National, with higher impact in Northeast and West Coast | Medium term (2-4 years) | (~) % Impact on CAGR Forecasts:+1.2% | Geographic Relevance:National, with higher impact in Northeast and West Coast | Impact Timeline:Medium term (2-4 years) |

Stringent FDA Guidelines for Sodium Reduction in Processed and Packaged Foods Stringent FDA Guidelines for Sodium Reduction in Processed and Packaged Foods | +1.8% | National, with early adoption in Northeast and California | Short term (≤ 2 years) | |||

Growing Prevalence of Cardiovascular Diseases Growing Prevalence of Cardiovascular Diseases | +0.9% | National, with higher prevalence in South and Midwest | Long term (≥ 4 years) | |||

Advancements in Salt Reduction Technologies and Ingredients Advancements in Salt Reduction Technologies and Ingredients | +1.1% | National, with research and development concentration in Northeast and West | Medium term (2-4 years) | |||

Increasing Adoption by Fast-Food and QSR Chains Increasing Adoption by Fast-Food and QSR Chains | +0.7% | National, with early adoption in urban markets | Short term (≤ 2 years) | |||

Rising Popularity of Functional and "Better-For-You" Snacks Rising Popularity of Functional and "Better-For-You" Snacks | +0.5% | National, with premium positioning in coastal markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Health Consciousness and Awareness of Hypertension

The escalating awareness of hypertension's link to dietary sodium is fundamentally reshaping consumer purchasing decisions and driving ingredient demand. The American Heart Association's 2024 statistics reveal that hypertension prevalence is projected to increase from 51.2% in 2020 to 61.0% by 2050, with disproportionate impacts on Black, Hispanic, and American Indian/Alaska Native populations [2]Source: American Heart Association, “Heart Disease and Stroke Statistics 2024 Update,” heart.org. This demographic shift is compelling food manufacturers to proactively reformulate products rather than react to regulatory pressure. The CDC's Chronic Disease Indicators tool[3]Source: Centers for Disease Control and Prevention, “Chronic Disease Indicators Tool,” cdc.gov, updated in 2024, provides state-level hypertension data that enables targeted marketing of sodium-reduced products in high-prevalence regions. Consumer willingness to pay premiums for health-positioned products is creating sustainable margins for ingredient suppliers, with potassium chloride acceptance growing significantly as health messaging improves. The trend extends beyond individual health concerns to encompass family wellness, particularly as parents seek to establish healthier eating patterns for children in response to rising childhood obesity rates.

Stringent FDA Guidelines for Sodium Reduction in Processed and Packaged Foods

The FDA's Phase II voluntary sodium reduction targets are transforming the market by establishing specific benchmarks for 163 food categories according to article published by FDA (U.S. Food and Drug Administration) in Issues Draft Guidance with Lower Target Levels for Certain Foods in August 2024. The agency's initiative to reduce average sodium intake to 2,750 mg per day by 2030 creates compliance requirements that directly influence ingredient demand. The FDA's proposed front-of-package nutrition labeling system , which requires "High," "Med," or "Low" sodium categorization, makes non-compliance visible to consumers, compelling manufacturers to reformulate products or risk market share decline. This rule was commenced until July, 2025. Despite being voluntary, the regulatory framework proves effective as manufacturers anticipate potential mandatory regulations if voluntary targets remain unmet. Federal pressure intensifies through state-level initiatives, including California's Food Safety Act and West Virginia's ingredient restrictions. Additionally, the FDA's updated "healthy" nutrient content claim, finalized in December 2024, implements sodium limits that encourage reformulation across multiple product categories.

Growing Prevalence of Cardiovascular Diseases

Cardiovascular disease prevalence continues its upward trajectory, with the CDC (Centers for Disease Control and Prevention) showing the share of adults who had a heart attack/myocardial infarction in the United States as 3.2% in the Northwest region in 2023 (compared to 2.6% in 2022), 3.3% in Midwest (3.2% in 2022), 3.4% in South (3.3% in 2022), among others. The economic burden of cardiovascular diseases, significantly influenced by dietary sodium intake, creates compelling business cases for sodium reduction initiatives across the food value chain. Regional disparities in cardiovascular health outcomes are driving targeted ingredient deployment, with the highest prevalence rates among Black females (59%) and Black males (58.9%) creating opportunities for culturally relevant product reformulations according to the data published by the American Heart Association in 2024 Heart Disease and Stroke Statistics. The correlation between sodium intake and cardiovascular risk is becoming increasingly quantified, with research indicating that every dollar spent on sodium reduction can save much in healthcare costs. Healthcare system pressures are creating institutional demand for sodium-reduced products, particularly in hospital foodservice and managed care environments where population health outcomes directly impact financial performance.

Advancements in Salt Reduction Technologies and Ingredients

Recent technological developments have improved sodium reduction capabilities across food applications that were previously difficult to reformulate. These applications include processed meats, baked goods, snacks, and dairy products. New solutions address challenges related to taste, texture, and preservation, enabling manufacturers to maintain product quality while reducing sodium content. For instance, MicroSalt's microparticle technology increases the surface area exposure of salt particles, allowing for better flavor distribution and natural sodium reduction without extensive reformulation. This technology has demonstrated effectiveness in various food categories, particularly in snack foods and seasonings. in addition, DSM's Maxarome yeast extracts leverage natural nucleotides to provide umami enhancement and mask off-notes, enabling more aggressive sodium reduction strategies. The integration of biotechnology with food science has created solutions that tackle multiple formulation challenges, including flavor enhancement, microbial control, and shelf-life stability, making sodium reduction more feasible for food manufacturers across diverse product categories.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost of Sodium Reduction Ingredients High Cost of Sodium Reduction Ingredients | -0.8% | National, with higher impact in price-sensitive segments | Short term (≤ 2 years) | (~) % Impact on CAGR Forecasts:-0.8% | Geographic Relevance:National, with higher impact in price-sensitive segments | Impact Timeline:Short term (≤ 2 years) |

Complexity in Reformulating Traditional Recipes Complexity in Reformulating Traditional Recipes | -0.6% | National, with higher impact in ethnic and regional foods | Medium term (2-4 years) | |||

Challenges in Maintaining Consistent Sensory Experience Challenges in Maintaining Consistent Sensory Experience | -0.4% | National, with higher impact in premium segments | Medium term (2-4 years) | |||

Consumer Awareness Gaps Hinders Growth Consumer Awareness Gaps Hinders Growth | -0.3% | National, with state-level variations | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Sodium Reduction Ingredients

The economic premium associated with sodium reduction agents creates significant margin pressure for food manufacturers, particularly in price-sensitive categories where consumer willingness to pay for health benefits remains limited. Potassium chloride, the most widely adopted sodium substitute, typically costs 3-5 times more than sodium chloride, creating immediate raw material cost inflation that manufacturers must absorb or pass through to consumers according to Cargill. Advanced technologies like yeast extracts and amino acid blends command even higher premiums, with some specialty agents costing 10-15 times more than conventional salt. The FDA's proposed front-of-package labeling compliance costs in 2025, estimated at USD 191-530 million annually for the industry, compound ingredient cost pressures by requiring simultaneous investments in reformulation and regulatory compliance. Supply chain constraints for specialty ingredients create additional cost volatility, as limited production capacity enables suppliers to maintain premium pricing structures that may not reflect underlying production costs.

Complexity in Reformulating Traditional Recipes

Recipe reformulation complexity extends beyond simple ingredient substitution to encompass fundamental changes in processing parameters, shelf-life considerations, and sensory profile management. Traditional food formulations often rely on sodium's multifunctional properties, including moisture retention, microbial control, and texture development, requiring comprehensive reformulation approaches that address each functional role separately. The USDA's updated school meal patterns, implementing 15% sodium reduction in lunches and 10% in breakfasts by July 2027, demonstrate the technical challenges of maintaining nutritional and sensory standards while reducing sodium. Ethnic and regional food categories face particular challenges, as traditional flavor profiles may be fundamentally altered by sodium reduction, requiring extensive consumer testing and gradual reformulation strategies. The FDA's proposed amendments to standards of identity, allowing salt substitutes in standardized foods, create regulatory pathways but also introduce formulation complexity as manufacturers navigate new ingredient approval processes. Manufacturing equipment modifications may be required to accommodate new ingredient properties, creating additional capital investment requirements that smaller manufacturers may struggle to justify.

Segment Analysis

By Source: Natural Gains Momentum Despite Synthetic Dominance

Synthetic sodium reduction agents maintain their commanding position with 55.12% market share in 2025, leveraging established manufacturing infrastructure and cost advantages that enable broad market penetration across price-sensitive applications. The synthetic segment benefits from decades of research and development, resulting in highly stable and consistent performance across various food applications. Manufacturing economies of scale and optimized production processes continue to make synthetic agents an economically attractive option for food manufacturers seeking cost-effective sodium reduction solutions. However, natural sodium reduction agents are experiencing robust growth at 7.42% CAGR through 2031, driven by clean-label trends and consumer preference for recognition.

The natural segment's acceleration reflects technological advances in yeast extract production and fermentation-based ingredient development, with companies like DSM leveraging their Maxarome portfolio to deliver umami enhancement through natural nucleotides. Mushroom-based sodium reduction solutions are emerging as a particularly promising natural alternative. The FDA's GRAS recognition of various natural sodium substitutes is expanding formulation options, while consumer willingness to pay premiums for natural solutions is improving segment economics despite higher raw material costs. The natural segment is experiencing significant investment in research and development, leading to improved functionality and taste profiles. Global regulatory support and increasing consumer awareness of clean-label agents continue to strengthen the market position of natural sodium reduction solutions.

Note: Segment shares of all individual segments available upon report purchase

By Type: Yeast-Based Innovation Challenges Mineral Salt Leadership

Mineral salts command the largest market share at 39.20% in 2025, with potassium chloride serving as the primary workhorse for sodium reduction across multiple applications due to its 1:1 substitution ratio and GRAS status as cited by Food and Drug Administration (Code of federal regulations, 2025). The widespread adoption of mineral salts is further supported by their cost-effectiveness and established safety profile in food applications. Magnesium chloride is gaining traction as an alternative mineral salt, offering similar functional properties while addressing specific application needs in dairy and processed foods. The versatility of mineral salts extends beyond sodium reduction to include functional benefits such as texture enhancement and preservation.

Yeast-based agents represent the fastest-growing product category at 8.45% CAGR through 2031, driven by their superior umami enhancement capabilities and multifunctional properties. These agents address the sensory challenges associated with traditional sodium reduction by providing savory flavor enhancement that masks the metallic notes often associated with potassium chloride. The effectiveness of these solutions has led to increased adoption across various food categories, particularly in processed meats and snack foods. Amino acids and glutamates maintain steady demand across specific applications, particularly in ethnic foods where umami enhancement is culturally important, while the "Others" category encompasses emerging technologies like encapsulated oleoresins and enzyme-modified agents that enable targeted sodium reduction strategies. The market continues to evolve with innovations in ingredient combinations and processing technologies that optimize taste profiles while achieving sodium reduction goals.

By Application: Dairy Acceleration Contrasts with Bakery Stability

The bakery and confectionery segment maintains its leadership position with 33.05% market share in 2025, reflecting the sector's high sodium content and regulatory pressure to reformulate products that constitute dietary staples. Research on low-salt whole-wheat bread demonstrates the potential for spice extracts to double gamma-aminobutyric acid content while improving saltiness perception, indicating technological pathways for maintaining consumer acceptance during sodium reduction. The segment's stability reflects the technical challenges of sodium reduction in baked goods, where salt serves critical functional roles in gluten development, yeast control, and shelf-life extension. The increasing consumer demand for healthier bakery options, coupled with stringent FDA sodium reduction guidelines, drives manufacturers to adopt innovative sodium reduction solutions.

Dairy products are experiencing the fastest growth at 7.56% CAGR through 2031, driven by the sector's traditionally high sodium content and increasing regulatory scrutiny. Condiments, seasonings, and sauces face unique challenges due to their role as flavor enhancers, requiring sophisticated ingredient solutions that maintain taste impact while reducing sodium content. Meat and meat products benefit from established potassium chloride applications, while the snacks category is leveraging microencapsulation technologies to achieve significant sodium reduction without sensory compromise. The rising prevalence of cardiovascular diseases and hypertension among Americans propels food manufacturers across these segments to prioritize sodium reduction initiatives.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Northeast region commands the largest market share at 36.60% in 2025, leveraging its dense concentration of food manufacturing facilities and proximity to regulatory decision-making centers that drive early adoption of sodium reduction initiatives. The region's growth through 2030 reflects sustained investment in food processing infrastructure, with major projects like Fairlife's USD 650 million New York facility demonstrating continued commitment to the region's manufacturing base in September 2024. Consumer health awareness levels in Northeast metropolitan areas exceed national averages, creating premium market opportunities for sodium-reduced products that justify higher ingredient costs. The region's established supply chains for specialty agents and access to research institutions provide competitive advantages in developing and deploying advanced sodium reduction technologies.

The South region is experiencing the most dynamic growth at 8.12% CAGR through 2031, driven by expanding food manufacturing capacity and evolving consumer preferences toward healthier options. Manufacturing investments totaling over USD 400 million across Tennessee and South Carolina are creating new demand centers for sodium reduction ingredients, while the region's growing urban populations are driving increased health consciousness as published by Site Selection Group in February 2024. The South's higher prevalence of cardiovascular diseases, particularly among certain demographic groups, is creating targeted opportunities for sodium reduction ingredient deployment in culturally relevant food categories. State-level initiatives supporting healthier food options are amplifying federal regulatory pressure, while the region's cost advantages in manufacturing are attracting food companies seeking to implement sodium reduction strategies at scale.

The Midwest and West regions maintain complementary roles in the market ecosystem, with the Midwest providing steady demand from established processed food manufacturers and the West driving premium positioning and innovation adoption. The Midwest's agricultural infrastructure supports cost-effective ingredient sourcing, while the West's consumer willingness to pay premiums for health-positioned products creates sustainable margins for advanced sodium reduction technologies. Regional variations in regulatory implementation and consumer acceptance are creating opportunities for targeted ingredient deployment strategies that address local market conditions and preferences.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

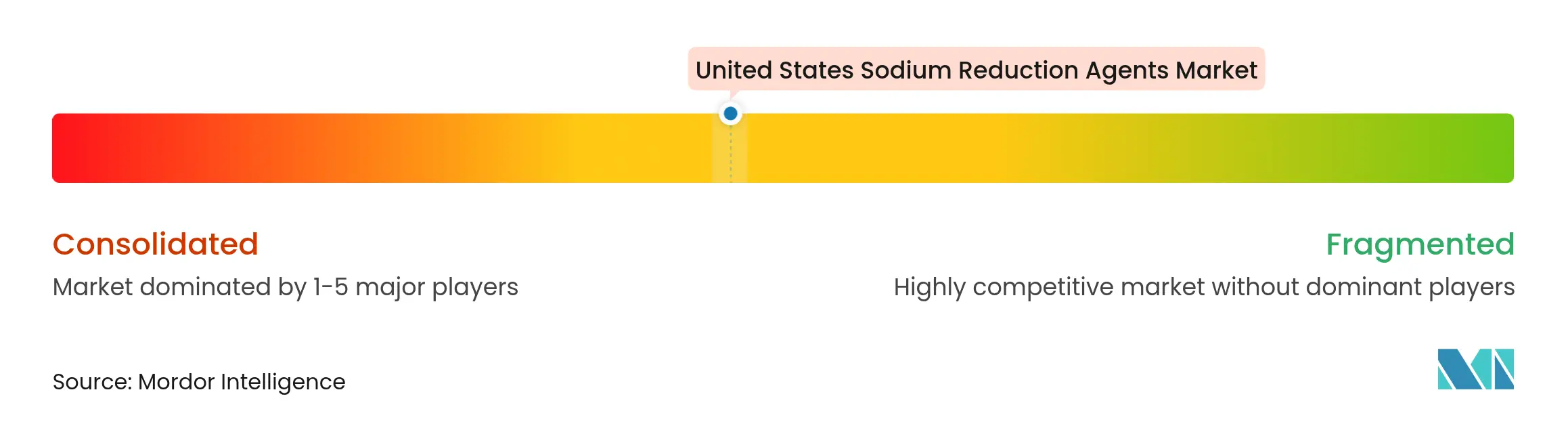

Market Concentration

The United States sodium reduction agents market exhibits moderate concentration, reflecting the presence of several established players alongside emerging technology specialists. Major players such as DSM-Firmenich AG, Kerry Group plc, Cargill, Incorporated, Tate & Lyle PLC, and Givaudan S.A. leverage their global scale capabilities to develop comprehensive sodium reduction platforms, while smaller innovators focus on breakthrough technologies that address specific application challenges.

The competitive dynamic is characterized by technology differentiation rather than price competition, as manufacturers seek solutions that deliver superior sensory outcomes while meeting regulatory requirements. Research and development investments in novel sodium reduction technologies continue to shape market growth, with manufacturers focusing on ingredients that maintain taste profiles while achieving lower sodium content. Strategic patterns center on vertical integration and technology acquisition, with companies building comprehensive portfolios that address multiple aspects of sodium reduction. The expansion of product portfolios through mergers and acquisitions enables manufacturers to offer complete sodium reduction solutions, while investments in production capabilities strengthen their market position.

Kerry Group's Tastesense platform exemplifies this approach, delivering up to 60% sodium reduction while maintaining sensory properties across diverse applications in 2024. Emerging disruptors like MicroSalt are leveraging patented microparticle technologies to create competitive advantages, while established players respond through strategic partnerships and technology licensing agreements. The FDA's GRAS recognition process creates regulatory moats for companies with approved ingredients, while patent protection enables sustained competitive advantages for breakthrough technologies.

United States Sodium Reduction Agents Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ajinomoto Health & Nutrition North America, Inc. (AHN) unveiled two innovative platforms, Salt Answer and Palate Perfect, aimed at assisting food manufacturers in navigating the growing demands for reduced sodium, enhanced taste, and efficient formulations. These introductions highlight AHN's ongoing commitment to tackling industry challenges through science-led and consumer-centric innovations.

- May 2025: SaltWise has acquired Green Salt, a company known for its sea asparagus-based salt alternative. Green Salt's product contains 50% less sodium than traditional salt and uses natural ingredients. The acquisition strengthens SaltWise's position in the U.S. salt alternatives market. Green Salt's products have received recognition from The New York Times and are used by chefs and nutritionists for their flavor profile and lower sodium content.

- May 2023: Cargill launched new mineral salt ingredient solutions in the United States, including sea salt flour and Pink Himalayan salt products, to address the increasing demand for healthier food options. The sea salt flour, a fine powder-like sodium chloride, enables precise blending and even distribution in applications such as dry soups, cereals, and snack foods. Food and beverage companies can use these products to reduce sodium levels in their formulations.

Table of Contents for United States Sodium Reduction Agents Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Health Consciousness and Awareness of Hypertension

- 4.2.2Stringent FDA guidelines for sodium reduction in processed and packaged foods

- 4.2.3Growing Prevalence of Cardiovascular Diseases

- 4.2.4Advancements in Salt Reduction Technologies and Ingredients

- 4.2.5Increasing Adoption by Fast-Food and QSR Chains

- 4.2.6Rising Popularity of Functional and Better-For-You Snacks

- 4.3Market Restraints

- 4.3.1High Cost of Sodium Reduction Ingredients

- 4.3.2Complexity in Reformulating Traditional Recipes

- 4.3.3Challenges in Maintaining Consistent Sensory Experience

- 4.3.4Consumer Awareness Gaps Hinders Growth

- 4.4Supply Chain Analysis

- 4.5Regulatory Outlook

- 4.6Porter's Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Source

- 5.1.1Synthetic

- 5.1.2Natural

- 5.2By Type Type

- 5.2.1Mineral Salts

- 5.2.2Amino Acids and Glutamates

- 5.2.3Yeast-Based Ingredients

- 5.2.4Others

- 5.3By Application

- 5.3.1Bakery and Confectionery

- 5.3.2Condiments, Seasonings and Sauces

- 5.3.3Dairy Products

- 5.3.4Meat and Meat Products

- 5.3.5Snacks

- 5.3.6Others

- 5.4By Region

- 5.4.1Northeast

- 5.4.2Midwest

- 5.4.3South

- 5.4.4West

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1DSM-Firmenich AG

- 6.4.2Kerry Group plc

- 6.4.3Cargill, Incorporated

- 6.4.4Givaudan S.A.

- 6.4.5Tate & Lyle PLC

- 6.4.6Innophos Holdings Inc.

- 6.4.7Solina Group SAS

- 6.4.8Jungbunzlauer International AG

- 6.4.9Corbion NV

- 6.4.10International Flavors & Fragrances, Inc.

- 6.4.11Sensient Technologies Corporation

- 6.4.12Ajinomoto Co., Inc

- 6.4.13The Archer-Daniels-Midland Company

- 6.4.14Nu-Tek Food Science, LLC

- 6.4.15Salt of The Earth Ltd.

- 6.4.16MicroSalt Inc.

- 6.4.17Compass Minerals International, Inc.

- 6.4.18K+S Group

- 6.4.19AngelYeast Co., Ltd.

- 6.4.20Morton Salt, Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

United States Sodium Reduction Agents Market Report Scope

The United States sodium reduction ingredients market is segmented by product type and application. Based on product type, the market is segmented into amino acids and glutamates, mineral salts, yeast extracts, and others. Based on the application, the market is segmented into bakery and confectionery, condiments, seasonings and sauces, dairy and frozen foods, meat and meat products, snacks, and others.