Market Overview

| Study Period | 2021 - 2031 |

|---|---|

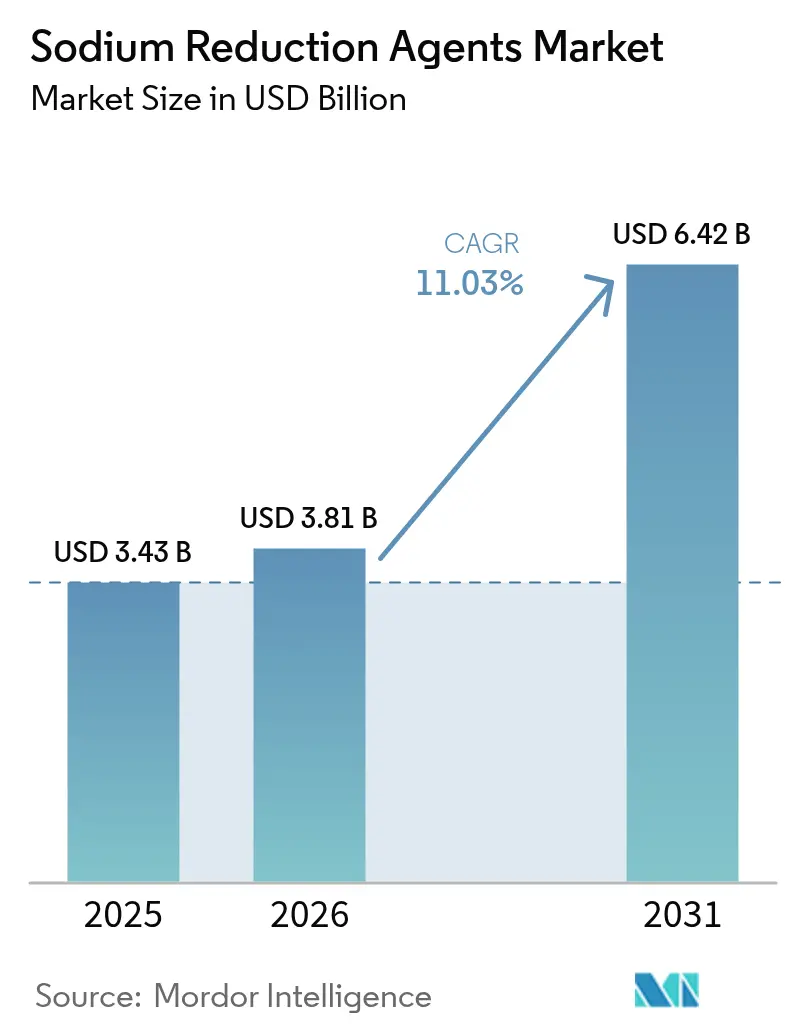

| Market Size (2026) | USD 3.81 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Reduction Agents Market Analysis by Mordor Intelligence

The Sodium Reduction Agents market size was valued at USD 3.43 billion in 2025 and estimated to grow from USD 3.81 billion in 2026 to reach USD 6.42 billion by 2031, at a CAGR of 11.03% during the forecast period (2026-2031). This reflects a strong Compound Annual Growth Rate (CAGR) of 11.19%. This growth is being driven by a combination of factors, including stricter regulatory oversight, the increasing prevalence of hypertension, and corporate commitments to Environmental, Social, and Governance (ESG) initiatives. These elements are collectively pushing food manufacturers to reformulate processed food products. Potassium-based mineral salts, yeast extracts, and innovative enzyme systems are at the forefront of this reformulation process, serving as essential tools for achieving sodium reduction. Additionally, the implementation of stringent front-of-pack labeling regulations across regions such as North America, Europe, Asia-Pacific, and the Middle East is further boosting demand for sodium reduction solutions. Ingredient suppliers are increasingly focusing on developing products that not only deliver measurable health benefits but also maintain flavor quality, enabling them to support a premium pricing strategy within the Sodium Reduction Agents market. Companies that can effectively combine technical expertise, a deep understanding of regional regulatory requirements, and advanced flavor-masking technologies are positioning themselves to gain a competitive advantage in this evolving market.

Key Report Takeaways

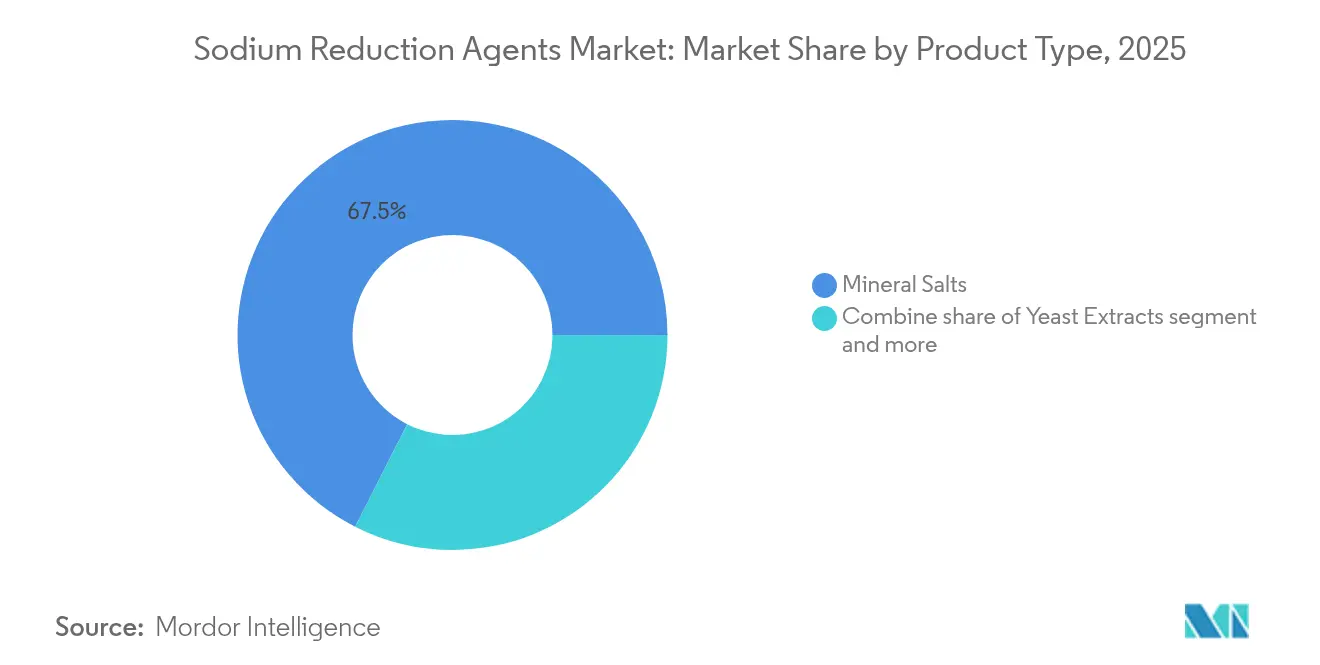

- By product type, mineral salts dominated the sodium reduction agents market in 2025, securing 67.52% of the share. Yeast extracts, benefiting from a clean-label positioning, are set to grow at the fastest pace, with a projected CAGR of 11.85% through 2031.

- By form, powdered forms are set to command 59.78% of the market, while liquid formats, essential for sauces and marinades due to their need for uniform dispersion and rapid flavor release, are on track for a 12.18% CAGR.

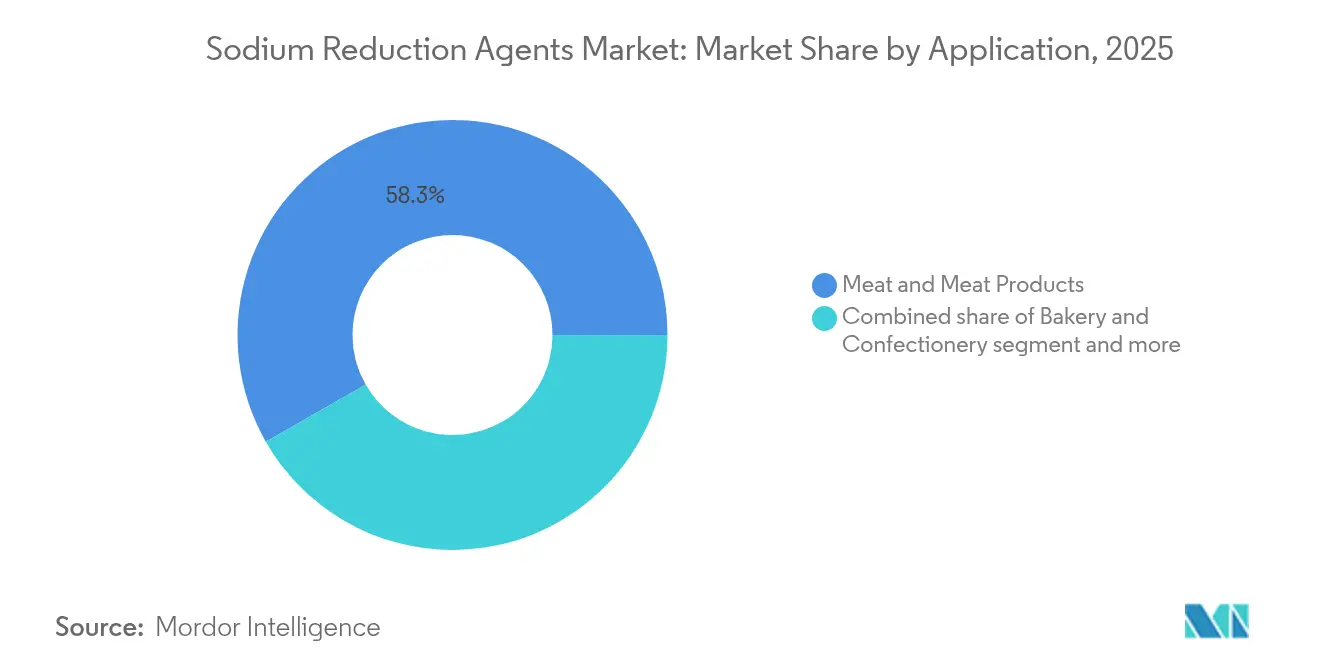

- By application, meat and meat products, accounting for 58.26% of application revenue in 2025, are projected to grow at an 11.72% CAGR, highlighting their challenges in sodium reduction and microbial control.

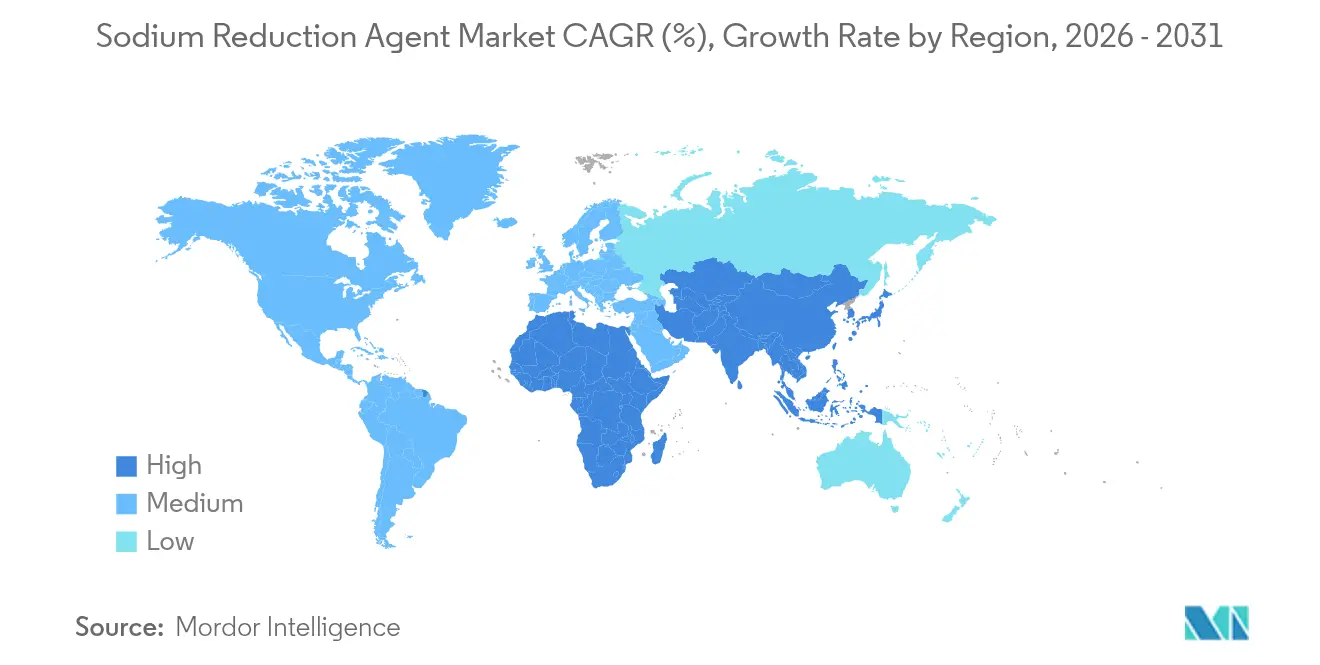

- By geography, North America led the market in 2025 with 36.12% of the value, but Asia-Pacific is set to outpace with the fastest growth at an 11.36% CAGR, driven by a new national salt-reduction framework.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sodium Reduction Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impact of hypertension and cardiovascular disease on sodium reduction ingredient demand | +2.3% | Global, with acute burden in North America, Europe, and Eastern Mediterranean Region | Medium term (2-4 years) |

| Regulatory sodium-reduction targets and their influence on food reformulation | +2.1% | North America, Europe, PAHO member states (Americas), Saudi Arabia, emerging Asia-Pacific | Short term (≤ 2 years) |

| Consumer-driven shift in sodium reduction preferences | +1.5% | North America, Western Europe, urban Asia-Pacific (China, Japan, Australia) | Medium term (2-4 years) |

| Corporate health and ESG commitments driving SRI adoption | +1.4% | Global, led by multinational food corporations headquartered in North America and Europe | Long term (≥ 4 years) |

| Advancements in mineral salt flavor performance | +1.8% | Global, with resarch and development concentrated in North America and Europe; rapid adoption in Asia-Pacific | Medium term (2-4 years) |

| Clean-label and natural positioning of yeast extracts and plant-based umami systems | +1.9% | North America, Europe, urban Asia-Pacific; expanding to South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Impact of Hypertension and Cardiovascular Disease on Sodium Reduction Ingredient Demand

Reducing global sodium intake from the current average of 3,400 milligrams (mg) per day to the World Health Organization (WHO)-recommended 2,300 mg could prevent an estimated 2.5 million deaths annually, primarily from hypertension and cardiovascular diseases. In the Eastern Mediterranean Region, 38% of adults aged 30-79 are living with hypertension, with over half (51%) unaware of their condition [1]Source: World Health Organization, “Guidelines and advocacy materials,” emro.who.int. This creates a significant opportunity as diagnosis rates improve and public health campaigns raise awareness. In response to this health challenge, food manufacturers are rethinking their approach to sodium reduction agents. These agents are no longer viewed as mere expenses but as critical tools to mitigate risks, avoid regulatory penalties, and protect brand reputation in markets where high-sodium products face front-of-pack warning labels. Potassium chloride offers a unique advantage: it not only reduces sodium content but also increases potassium intake. This is particularly important, as most Americans consume only half of the recommended potassium levels. As a result, potassium chloride is increasingly recognized as a key clinical solution in food formulations. Additionally, formulators are prioritizing ingredients that deliver measurable health benefits over those that provide only minor taste improvements. This shift in strategy benefits suppliers who can offer validated clinical data, bioavailability studies, and comprehensive organoleptic profiles.

Regulatory Sodium-Reduction Targets and Their Influence on Food Reformulation

The U.S. Food and Drug Administration's (FDA) updated draft guidance on voluntary sodium reduction targets, along with the United States Department of Agriculture's (USDA) school meal standards, are driving a reformulation wave across North America. These standards require a 15% sodium reduction for lunches and a 10% reduction for breakfasts by July 2027. Similarly, the Pan American Health Organization (PAHO) introduced regional sodium reduction targets in February 2021, aiming for a 15% reduction by 2022 and 30% by 2025 across 18 countries. However, as of 2025, only 47% of packaged foods met the 2022 target. In Argentina, Act 26.905 achieved a 93.7% compliance rate among regulated products. However, the law excludes high-sodium items such as meat and fish condiments (averaging 13,500 mg per 100 g) and leavening flour (averaging 757 mg per 100 g), creating opportunities for sodium reduction agents in these unregulated categories. Looking ahead, Saudi Arabia's Saudi Food and Drug Authority (SFDA) will require restaurants and cafes to label high-salt menu items starting July 1, 2025. This regulation extends sodium reduction efforts beyond packaged goods to the foodservice sector[2]Source: World Obesity Federation, “Saudi Arabia Policies, Interventions and Actions,” data.worldobesity.org. The contrast between voluntary measures in regions like North America and parts of Europe, and mandatory regulations in Argentina, Saudi Arabia, and Peru (which includes front-of-pack labeling), is driving demand for flexible sodium reduction platforms. These platforms can be adjusted to meet specific regional standards without requiring extensive reformulation.

Consumer-Driven Shift in Sodium Reduction Preferences

Consumers are more likely to accept lower-sodium products when changes are made gradually and subtly, rather than through sudden reformulations that can lead to taste rejection. Research shows that replacing 25-30% of salt with potassium chloride in bakery items can significantly cut sodium levels without compromising taste. This finding has led to a consensus in the industry favoring partial substitution methods. However, despite these efforts, consumer awareness hasn't translated into actual buying habits. For example, a study by the Pan American Health Organization (PAHO) across 34 countries in the Americas revealed that while 26 nations rolled out consumer awareness initiatives, none launched mass media campaigns aimed at changing behaviors [3]Source: Pan American Health Organization, “Mapping Dietary Salt/Sodium Reduction Policies,” paho.org. This highlights a significant gap between educating consumers and driving action. In a move that could influence purchasing decisions, the United States Food and Drug Administration (FDA) in December 2020 approved the label "potassium salt" as a more consumer-friendly alternative to "potassium chloride." Suppliers, including Cargill, are closely monitoring this shift. Meanwhile, formulators are integrating sodium reduction into broader clean-label strategies. They are promoting yeast extracts and plant-based umami systems as "natural" flavor enhancers, avoiding the chemical undertones associated with mineral salts. This approach appeals to health-conscious consumers who are cautious about ingredient lists with overly technical terms.

Corporate Health and ESG Commitments Driving SRI Adoption

Global food companies are incorporating sodium reduction goals into Environmental, Social, and Governance (ESG) frameworks, recognizing reformulation as a significant risk factor that attracts investor attention and requires public reporting. Mars has pledged to reduce sodium levels in its European product portfolio to meet World Health Organization (WHO) benchmarks. Similarly, Unilever and Nestlé have included sodium reduction targets in their annual sustainability reports, linking these goals to executive compensation through health and nutrition Key Performance Indicators (KPIs). This transition from voluntary commitments to measurable and auditable objectives is driving consistent demand for sodium reduction agents with traceability and third-party validation. Institutional investors are increasingly applying ESG criteria that penalize companies falling behind on public health metrics. The pharmaceutical-grade salt supply chain—highlighted by Brenntag Specialties' December 2024 appointment as the global distributor for K+S's APISAL Sodium Chloride and high-purity potassium chloride—demonstrates the alignment of food-grade sodium reduction agents with medical nutrition standards. This alignment allows product developers to claim clinical-grade purity and regulatory compliance for both food and pharmaceutical applications. Companies that align their sodium reduction strategies with Science Based Targets or WHO Best Buys for Non-Communicable Disease (NCD) prevention gain better access to sustainability-linked financing and retail shelf space in markets where governments promote healthier product portfolios.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and consumer acceptance challenges | -1.2% | Global, most acute in emerging markets with limited exposure to reduced-sodium products | Short term (≤ 2 years) |

| Technical difficulties in replacing salt's multifunctional role | -0.9% | Global, particularly in meat processing, dairy, and bakery applications | Medium term (2-4 years) |

| Higher costs of ingredients and reformulation | -0.7% | Emerging markets (South America, Middle East and Africa, parts of Asia-Pacific) and cost-sensitive categories | Short term (≤ 2 years) |

| Limited awareness and priority in emerging markets | -0.6% | South America, Middle East and Africa, rural Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste and Consumer Acceptance Challenges

Potassium chloride's bitter and metallic off-notes, especially when used above 30% substitution levels, pose a significant sensory hurdle for broader acceptance. This challenge is pronounced in neutral-flavored applications, like deli poultry, where seasoning struggles to mask the taste deviation. Formulators have observed that while seasoned products, such as meat sticks, can handle a sodium reduction of up to 50%, lightly flavored items face consumer rejection if they exceed a 25-30% substitution. In October 2024, the Institute for the Advancement of Food and Nutrition Sciences highlighted the limitations of simply removing sodium. They emphasized salt's crucial sensory roles—enhancing flavor, reducing bitterness, and potentiating sweetness. This underscores the need for holistic strategies, blending technological solutions, flavor maskers, and consumer education. Emerging markets show a pronounced sensitivity to taste deviations. This is largely because consumers in these regions haven't had a gradual introduction to lower-sodium products. Such dynamics not only extend reformulation timelines but also necessitate significant investments from manufacturers in localized sensory testing and iterative product launches. A glaring oversight is the absence of behavior-change mass media campaigns across all 34 PAHO member states. This gap is critical: without priming consumers, even the most technically sound reformulations stand on shaky ground. If public health messaging doesn't recalibrate taste expectations, these products risk market failure.

Technical Difficulties in Replacing Salt's Multifunctional Role

Salt serves multiple purposes beyond enhancing flavor, including antimicrobial action, water binding, protein solubilization, and texture modification. These functions make it difficult to find effective substitutes in meat, dairy, and bakery products. For example, traditional bacon and ham formulations use salt to achieve a 56-day shelf life. In comparison, reduced-salt versions with only 2.3% salt can sustain a shelf life of just 28 days, increasing the risk of Clostridium botulinum (a harmful bacterium) and reducing microbial control. In natural cheeses, replacing sodium chloride (table salt) with potassium chloride can impact its ability to combat Listeria. Similarly, substituting sodium lactate with potassium lactate or using clean-label alternatives like cultured wheat instead of sodium propionate can affect microbial growth. These changes require rigorous validation through challenge tests and shelf-life studies. Additionally, achieving equivalent antimicrobial activity often demands higher quantities of potassium-buffered vinegar compared to sodium-buffered vinegar. When reducing or replacing high-sodium ingredients, it is critical to maintain the levels of active components to ensure product safety and quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mineral Salts Dominate, Yeast Extracts Surge

In 2025, mineral salts held a significant 67.52% market share, largely due to the versatility and cost-effectiveness of potassium chloride (KCl) as a direct replacement for sodium chloride (NaCl) in various applications. Potassium chloride enables sodium reductions of 25-50% in meat formulations and 10-25% in bakery products. Products like Cargill's Potassium Pro and FlakeSelect lines offer particle-engineered variants that improve solubility, enhance topical adherence, and maintain saltiness perception at lower dosages. Other mineral salts, such as magnesium sulfate, potassium lactate, and calcium chloride, cater to specific needs. For example, potassium lactate extends the shelf life of processed meats while contributing to sodium reduction, and calcium chloride improves texture in dairy products and canned vegetables.

Yeast extracts are expected to grow at a compound annual growth rate (CAGR) of 11.85% from 2026 to 2031, making them the fastest-growing product type. This growth is fueled by their clean-label appeal and umami-rich flavor profiles, which help mask the metallic taste of potassium chloride. Companies like Angel Yeast, Ohly, and Corbion have expanded their offerings with naturally derived yeast extracts that exclude hydrolyzed vegetable proteins, aligning with consumer preferences for simpler and more recognizable ingredient lists.

By Form: Powder Leads, Liquid Accelerates

In 2025, powder and granule forms made up 59.78% of the market share, underlining their strong presence in products like dry seasoning blends, bakery mixes, and meat rubs. These forms are preferred due to their excellent flowability, dispersibility, and shelf stability. For instance, Cargill's FlakeSelect line and Alberger flake salts showcase advancements in the powder segment, focusing on particle-engineered solutions that enhance surface area and amplify the perception of saltiness. This allows manufacturers to achieve desired sensory profiles while reducing sodium levels.

Liquid forms are expected to grow at a compound annual growth rate (CAGR) of 12.18% from 2026 to 2031, marking the fastest growth among all forms. Their increasing adoption is driven by their effectiveness in applications like sauces, marinades, dressings, and injection brines, where uniform dispersion and quick flavor release are crucial. Liquid yeast extracts and liquid potassium lactate solutions enable precise dosing and address the dust and handling issues often associated with powders, especially in automated production lines. Furthermore, the dairy and frozen foods industry is increasingly using liquid sodium reduction agents in processed cheese and ice cream formulations. Liquid emulsifying phosphates and liquid mineral salts integrate seamlessly into existing production processes, ensuring operational efficiency.

By Application: Meat Products Lead, Condiments Reformulate

Meat and meat products made up 58.26% of application demand in 2025 and are expected to grow at a compound annual growth rate (CAGR) of 11.72% through 2031. This growth underscores the category's dual challenges: salt plays a critical role in antimicrobial protection and water-binding, but processed meats are a significant contributor to sodium intake in the population. For example, regular bacon and ham formulations typically include about 3.5% salt to achieve a 56-day shelf life, while reduced-salt versions with 2.3% salt offer only a 28-day shelf life. This highlights the balance required between reducing sodium levels and maintaining food safety. According to Cargill, more seasoned meat products, such as meat sticks, can handle up to a 50% sodium reduction, whereas lightly flavored deli poultry can only tolerate a 25-30% reduction before reaching consumer rejection thresholds.

Potassium lactate is gaining traction in processed meats due to its dual functionality: it extends shelf life while also contributing to sodium reduction, addressing both food safety and regulatory compliance in one ingredient. Condiments, seasonings, and sauces are another priority for reformulation because of their high sodium content. Products like sauces, dips, gravies, and condiments have median sodium levels of 7.8 milligrams per kilocalorie (mg per kcal), the highest among all food categories.

Geography Analysis

North America led the market with 36.12% of the market value in 2025, driven by regulatory measures and corporate initiatives. The United States Food and Drug Administration's (FDA) voluntary sodium reduction targets and the United States Department of Agriculture's (USDA) upcoming school meal standards, requiring a 15% sodium reduction in lunches and 10% in breakfasts by July 2027, are significant contributors. Additionally, corporate Environmental, Social, and Governance (ESG) commitments from multinational food companies headquartered in the region are accelerating sodium reduction efforts. The FDA's approval in December 2020 to use the term "potassium salt" on ingredient labels has also reduced consumer resistance to potassium chloride, with suppliers like Cargill closely monitoring its impact on consumer purchase intent. In Canada, voluntary sodium reduction targets and mandatory front-of-pack labeling enforcement starting January 2026 are expediting reformulation in processed meats, bakery, and dairy categories. Meanwhile, Mexico's involvement in Pan American Health Organization (PAHO) sodium reduction initiatives and rising middle-class demand for health-focused products are expanding the market beyond the United States and Canada. Despite these advancements, cost pressures in foodservice and private-label segments remain a challenge for adopting multi-ingredient solutions.

The Asia-Pacific region is expected to grow at the fastest rate, with a Compound Annual Growth Rate (CAGR) of 11.36% from 2026 to 2031. This growth is fueled by national salt reduction frameworks and front-of-pack labeling initiatives in key countries such as China, India, Japan, and Australia. In China, national health initiatives and Japan's Ministry of Health, Labour and Welfare guidelines are driving both domestic and multinational food companies to reformulate products to meet local compliance standards. This has created a demand for sodium reduction agents tailored to traditional high-sodium condiments like soy sauce and miso. In India, the Food Safety and Standards Authority of India (FSSAI) is developing sodium benchmarks for packaged foods, while Australia's food standards body has aligned its targets with World Health Organization (WHO) sodium reduction guidelines. These regulatory efforts are encouraging reformulation across the region, making Asia-Pacific a key growth area for sodium reduction solutions.

Europe is witnessing steady progress, supported by WHO sodium reduction benchmarks, FoodDrinkEurope voluntary guidelines, and country-specific initiatives such as the United Kingdom's sodium reduction program and Germany's Federal Ministry of Food and Agriculture (BMEL) strategy. These measures have led to gradual reformulation across processed food categories. For instance, Mars has committed to sodium reductions aligned with WHO benchmarks across its European portfolio, reflecting the region's emphasis on corporate accountability and public health partnerships. Additionally, the European Union's discussions on front-of-pack labeling and potential harmonization of sodium targets across member states are creating regulatory clarity, benefiting early adopters of sodium reduction agents.

In South America, progress remains uneven. Argentina's Act 26.905 has achieved 93.7% compliance among covered products, but the law excludes high-sodium categories such as meat and fish condiments and leavening flour, limiting its overall impact. This highlights the challenges in achieving comprehensive sodium reduction across the region, despite some advancements in compliance.

Regulatory Landscape

Regulation is increasingly shaping sodium-reduction reformulation, with global guidance anchored to the World Health Organization (WHO) target of a 30% relative reduction in mean population salt intake by 2030 (extended from the earlier 2025 timeline). In May 2026, WHO launched a revamped SHAKE technical package that emphasizes structured policy action, including reformulation programs, front-of-pack labeling, and controls on marketing. This reinforces government-led pathways that translate into clearer demand signals for sodium reduction ingredient systems across packaged food and foodservice.

At the country level, manufacturers face a wider mix of voluntary and draft or mandatory approaches. In the United States, the FDA has advanced Phase II voluntary sodium reduction targets via draft guidance (Edition 2) covering 163 food categories, extending the earlier Phase I framework and keeping reformulation pressure on large processed categories. In July 2026, Nigeria's NAFDAC published draft Reduction of Sodium in Processed and Pre-Packaged Food Regulations 2026, outlining progressive reduction phases (15% and 30%), which shows how emerging markets are formalizing requirements that can increase uptake of mineral salts, yeast extracts, and flavor-modulation platforms designed to meet specific sodium thresholds and labeling needs.

Value Chain Analysis

The sodium reduction agents value chain begins upstream with producers of mineral salts (notably potassium chloride and other potassium, calcium, and magnesium salts), yeast extracts and fermentation-derived savory systems, and enabling technologies such as microstructured salt crystals and taste-modulation ingredients. Ingredient manufacturers and blenders supply standardized powders, granules, and liquids to food processors, who then execute application-specific reformulation for categories where salt has multiple functional roles, including flavor enhancement, water binding, protein solubilization, and microbial control, especially in meat processing, bakery, dairy, and high-sodium condiments.

Midstream, technical service and application labs support processors as they balance sodium targets with sensory acceptance and shelf-life validation, often using partial substitution (NaCl/KCl blends) backed by bitterness-masking and umami systems. Downstream, distributors and channel partners support regional availability and documentation needs, while compliance is governed by labeling and category benchmarks influenced by bodies such as the US FDA and WHO. Bottlenecks remain where potassium salt off-notes, process interactions, and microbiological constraints require iterative trials and challenge testing, which increases development time and favors suppliers that can provide integrated ingredient systems plus formulation support.

Competitive Landscape

The sodium reduction agents market is moderately fragmented, indicating that no single company dominates the space. Instead, a variety of ingredient suppliers, including Kerry Group, DSM-Firmenich, Cargill, Givaudan, Angel Yeast, Tate & Lyle, Ingredion, and International Flavors & Fragrances (IFF), compete by leveraging their expertise in formulation, understanding of regional regulations, and advanced flavor-masking technologies. Products such as Cargill's Potassium Pro and FlakeSelect lines, Kerry's Tastesense Salt platform, and DSM-Firmenich's yeast extract portfolios highlight the industry's shift from basic salt substitutes to innovative solutions that combine taste, functionality, and clean-label requirements in a single ingredient system.

Smaller companies like Nu-Tek Natural Ingredients and Advanced Food Systems are focusing on proprietary potassium-salt processing methods that reduce bitterness without relying on bitter blockers. These solutions are particularly appealing to formulators who prioritize clean-label declarations over cost considerations. There are also untapped opportunities in enzyme-based sodium reduction platforms that hydrolyze proteins to release savory peptides, microstructured salt particles that enhance saltiness perception through increased surface area, and potassium-based emulsifying phosphates that can replace sodium phosphates in processed cheese and dairy products.

Ajinomoto's expertise in glutamates and Ohly's advancements in yeast extracts position these companies to meet the growing demand in Asian markets, where umami intensity is a key taste preference. The competitive landscape is shifting from simply supplying ingredients to offering integrated reformulation services. Companies that provide sensory testing, shelf-life validation, regulatory compliance documentation, and application-specific technical support are forming long-term partnerships with food manufacturers navigating complex sodium reduction mandates. Compliance with the Pan American Health Organization's (PAHO) updated sodium reduction targets for 2022 and 2025 remains uneven, with only 47% of packaged foods meeting the 2022 benchmarks. This underscores the continued need for next-generation sodium reduction agents that balance technical functionality, sensory appeal, and cost-effectiveness across diverse food applications.

Sodium Reduction Agents Industry Leaders

Kerry Group plc

DSM-Firmenich

Cargill Inc.

Givaudan S.A.

Angel Yeast Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is the shift from single-ingredient substitution to engineered platforms that preserve saltiness perception and product performance, creating room for suppliers that can support faster reformulation with fewer recipe changes. This is visible in 2026 launches focused on improving salt-perception efficiency and simplifying adoption, including Landa Labs ultra-thin salt flake technology positioned to raise perceived salt impact at lower sodium levels and Nedmag's Novasal Blend positioned as a direct, 1-to-1 salt replacement approach for sodium reduction. These directions address processors working through tighter sodium benchmarks across multiple food categories, where shorter development cycles and sensory consistency can influence purchasing decisions.

Another opportunity is multifunctionality, where sodium reduction is bundled with other nutrition and formulation goals, expanding the value proposition beyond compliance. Examples in 2026 include MicroSalt Fibre, which combines low-sodium salt with functional fiber, and Griffith Foods launching a sodium solutions initiative positioned for deep reductions in snack and protein applications. On the demand side, May 2026 WHO SHAKE updates and Nigeria's 2026 NAFDAC draft sodium reduction regulation highlight expanding government-led programs, increasing the addressable market for traceable, application-ready systems (mineral salts plus yeast extracts and flavor modulation) that can be tuned to local benchmarks and labeling rules.

Recent Industry Developments

- May 2026: Griffith Foods launched Craveable Impact: Sodium Solutions, positioning the platform to deliver substantial sodium reductions in snack and protein applications while maintaining eating quality. The launch highlights demand for application-ready systems that combine taste modulation with sodium reduction rather than relying on straightforward salt replacement alone.

- October 2025: dsm-firmenich inaugurated the Van Marken Food Innovation Center in Delft, Netherlands, to accelerate diet transformation workstreams, including salt reduction. The facility expansion strengthens the company’s capability to develop and scale sodium reduction and flavor modulation solutions with customer co-creation support in Europe.

- April 2024: Kerry launched Tastesense Salt, designed to deliver salt and savory taste without increasing sodium content by restoring salty impact, body, and linger. This product launch broadened the toolkit available to food manufacturers seeking sodium reduction while managing sensory acceptance in reformulated products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of ingredients and blends used by food producers to reduce sodium in finished products while keeping acceptable taste, texture, and shelf life, across major processed food categories and regions.

Scope exclusions: This sizing excludes low sodium claims that come only from portion control or recipe adjustments that do not involve a sodium reduction agent ingredient.

Segmentation Overview

- By Product Type

- Amino Acids and Glutamates

- Mineral Salts

- Potassium Chloride

- Magnesium Sulphate

- Potassium Lactate

- Calcium Chloride

- Yeast Extracts

- Others

- By Form

- Powder/Granules

- Liquid

- By Application

- Bakery and Confectionery

- Condiments, Seasonings and Sauces

- Dairy and Frozen Foods

- Meat and Meat Products

- Snacks

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the demand context and anchor a few measurable signals, before assumptions were stress tested with interviews. We reviewed public nutrition and health references that discuss sodium intake and reformulation pressure, along with food production and trade signals that influence ingredient demand.

Sources consulted include public datasets and publications such as the World Health Organization guidance on sodium reduction, US FDA sodium-related initiatives and labeling references, USDA FoodData Central for nutrient benchmarks, FAOSTAT for food production indicators, and UN Comtrade for trade flows in relevant food categories and salts. We also reviewed company annual reports, investor presentations, and reputable press for reformulation activity, plus paid subscriptions used for company financials and intelligence and for patent databases to track ingredient innovation. This list is illustrative only, and many other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on checking what portion of reformulation activity is actually solved using sodium reduction agents, and how pricing and dosage levels move by food category. We spoke with a mix of ingredient suppliers, food manufacturers, and technical specialists across APAC, EMEA, and the Americas so that desk assumptions on adoption, use rates, and mix by product type could be corrected where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 16% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where the starting point came from the processed food demand pool and sodium reduction penetration by major food categories, which was then translated into ingredient value using typical dosage ranges and average selling prices. Once the first cut was built, selective bottom-up checks were used, such as rolling up sampled supplier revenues by product type and cross-checking channel pricing, to keep the total realistic.

Key inputs that moved the model included reformulation pace in bakery, snacks, sauces, and processed meat, the mix shift between mineral salts, yeast extracts, and amino acids and glutamates, typical inclusion rates (grams per kilogram of finished food), average price ranges by form (powder or liquid), and regional adoption differences tied to labeling and sodium targets. Where country detail was thin, gaps were handled by using proxy food output and category mix splits, followed by interview-based adjustments so the assumptions stayed consistent with what practitioners see.

Forecasting relied mainly on scenario analysis, because adoption is driven by policy pressure, manufacturer reformulation roadmaps, and consumer preference, which do not move in a straight line each year. The base case was guided by expert consensus on adoption curves and expected pricing progression, and it was then checked against historical movement in related food output indicators so growth stayed plausible.

Data Validation & Update Cycle

Model outputs were validated in layers, first by checking internal consistency across product types, forms, and applications, and then by comparing the implied ingredient demand against independent signals like processed food output trends and reported reformulation activity. When large variances showed up, assumptions were revisited, and respondents were re-contacted if the gap could not be explained by mix, pricing, or timing.

Before sign-off, the file is reviewed by another analyst for logic, unit handling, and outliers, and then a final pass is completed right before delivery so late-breaking changes are reflected. The report is refreshed annually, with interim updates triggered by material events such as major regulatory actions, pricing shocks in key mineral salts, or visible shifts in product reformulation commitments.

Mordor Intelligence's Global Sodium Reduction Agents Market Market Size Compared Against Other Published Estimates

Published market sizes for sodium reduction agents often do not match because the included ingredient set and the counting unit are not the same, even when the titles look similar. Differences also show up when a study leans more on broad health narratives instead of linking adoption to specific processed food categories and realistic inclusion rates.

The main gap comes from whether broader sodium reduction ingredients and adjacent salt substitutes sold at retail are bundled into the same number, where Mordor Intelligence counts only sodium reduction agent demand tied to formulated food applications and then prices it using form-specific ASPs that are validated in interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.81 B (2026) | |

| Industry Publisher A | USD 1.42 B (2024) | Uses an earlier base year and tends to mix end-user and channel views (including broader retail and distribution channel splits), which can undercount B2B ingredient value when dosage and form-specific pricing are not explicitly modeled. |

| Industry Publisher B | USD 1.50 B (2024) | Leans on a broad definition of sodium reduction solutions and a long-range CAGR narrative, while product scope and application-to-ingredient conversion logic are not clearly tied back to food category adoption and inclusion rate assumptions. |

Overall, the spread is mainly explained by scope and conversion logic, not just growth rates. By keeping the sizing tied to measurable food application demand signals, and then pressure testing ASP and use-rate assumptions with practitioners, the resulting value stays easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the current value of the Sodium Reduction Agents market?

The market is valued at USD 3.81 billion in 2026 and is set to reach USD 6.42 billion by 2031.

Which product type holds the largest Sodium Reduction Agents market share?

Mineral salts, led by potassium chloride, captured 67.52% of 2025 revenue.

Why are yeast extracts gaining popularity in sodium reduction?

Yeast extracts provide clean-label umami flavor that masks metallic notes from potassium salts and are forecast to grow at a 11.85% CAGR through 2031.

Which region will grow fastest in adopting sodium reduction agents?

Asia-Pacific is projected to expand at an 11.36% CAGR from 2026 to 2031 as China, India, and Japan enact stringent salt-reduction frameworks.

Page last updated on: