South America Sodium Reduction Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

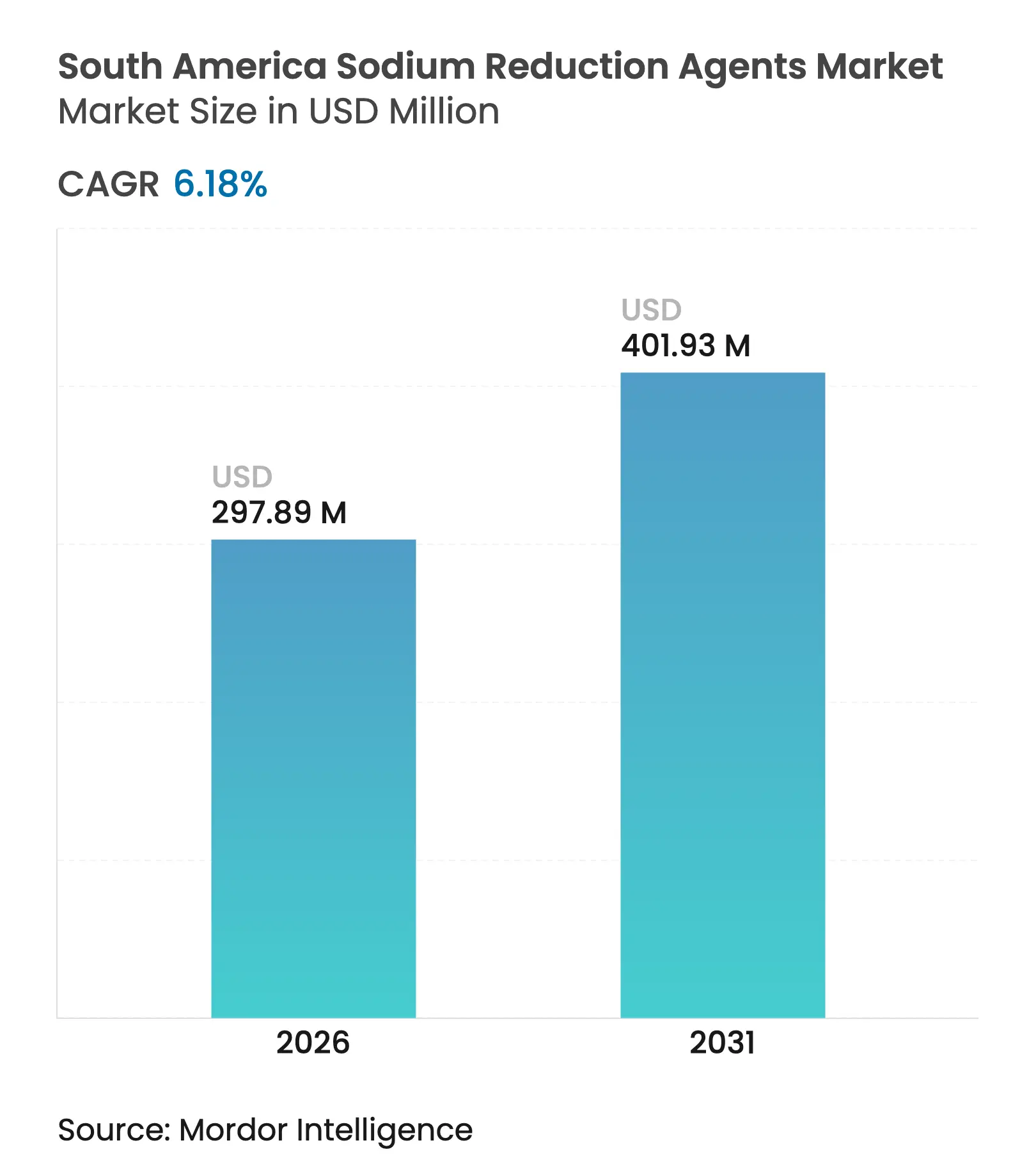

| Market Size (2026) | USD 297.89 Million |

| Market Size (2031) | USD 401.93 Million |

| Growth Rate (2026 - 2031) | 6.18 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

South America Sodium Reduction Agents Market Analysis by Mordor Intelligence

The sodium reduction agents market size in South America market size in 2026 is estimated at USD 297.89 million, growing from 2025 value of USD 280.56 million with 2031 projections showing USD 401.93 million, growing at 6.18% CAGR over 2026-2031. This growth is driven by factors such as mandatory front-of-package labeling, increasing incidence of cardiovascular diseases, and multinational reformulation mandates that position sodium reduction as a compliance necessity rather than an optional wellness initiative. Rapid urbanization, the consolidation of modern retail, and penalties for high-sodium SKUs on supermarket shelves further amplify the need for reformulation. This creates opportunities for cost-effective solutions such as potassium-chloride blends, yeast extracts, and amino-acid masking systems. Ingredient suppliers with pilot-plant capabilities and regional sensory-science expertise are well-positioned to gain market share as food processors work to meet labeling requirements, particularly in product categories like snacks, condiments, and baked goods, where sodium replacement can be achieved without compromising texture.

Key Report Takeaways

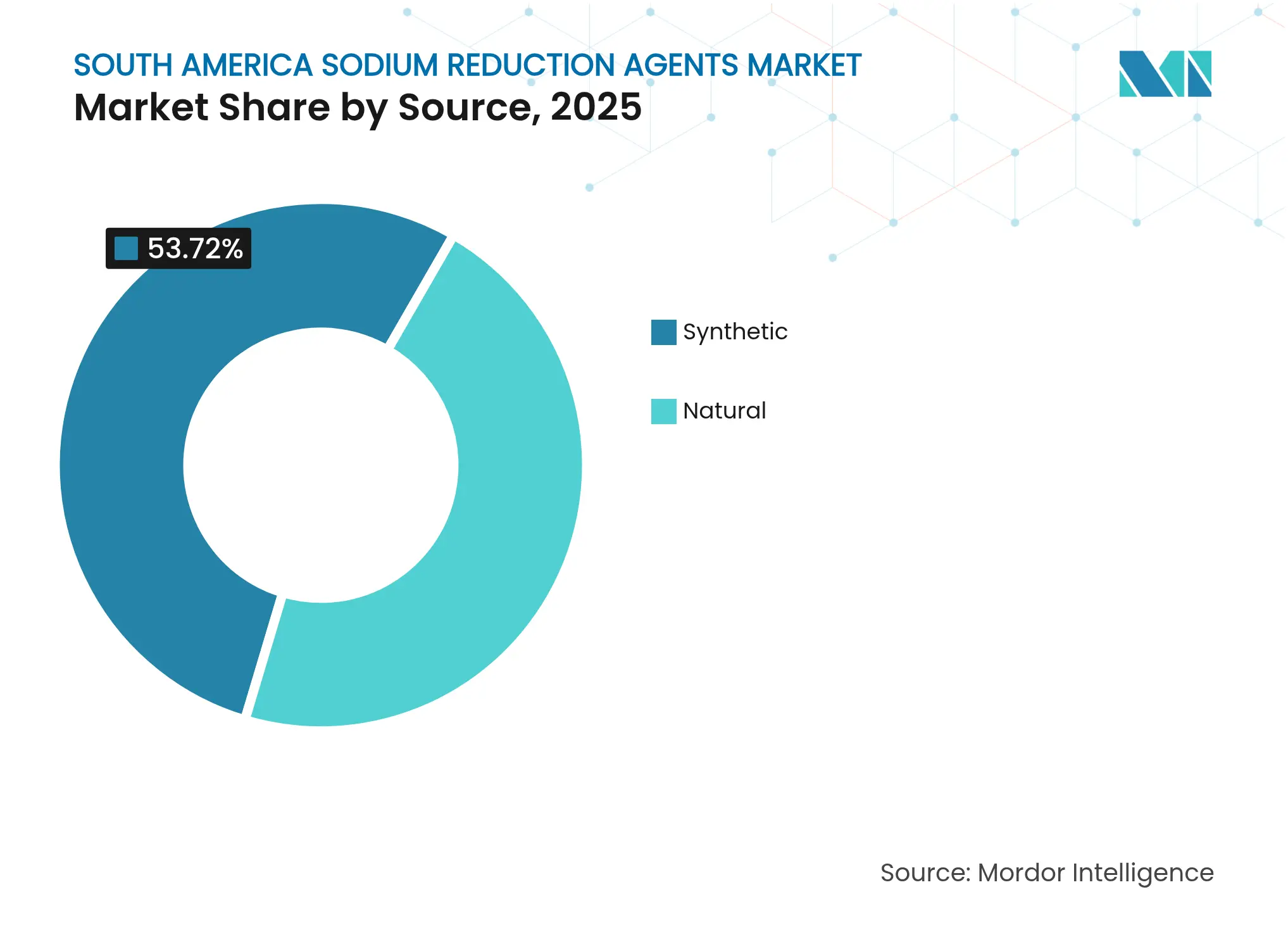

- By source, synthetic sources retained the lead with 53.72% sodium reduction agents market share in 2025, while natural sources are forecast to grow at 6.41% CAGR through 2031.

- By type, mineral salts captured a 38.10% share in 2025, yet amino acids are the fastest-advancing type at 6.78% CAGR from 2026 to 2031.

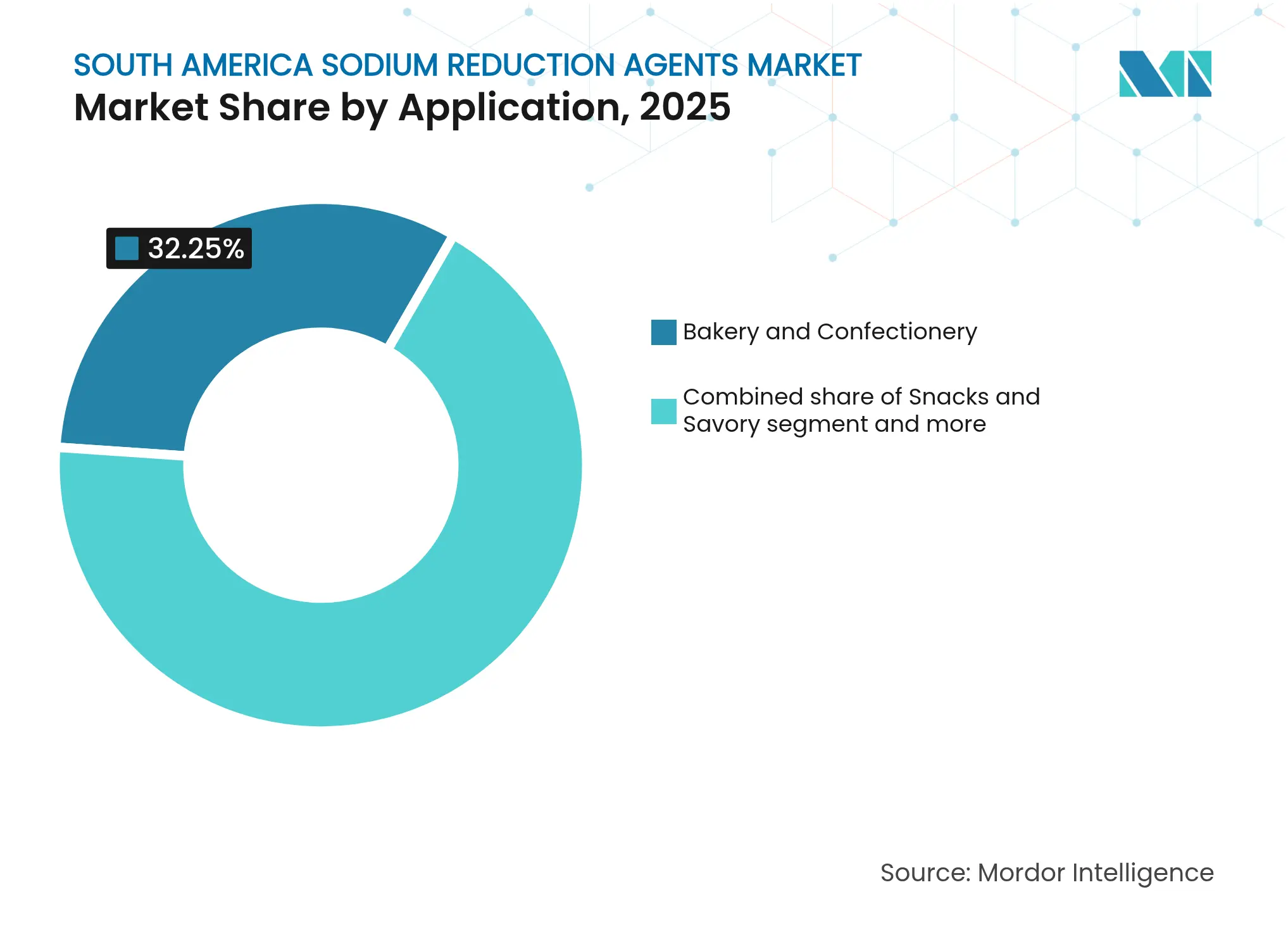

- By application, bakery and confectionery dominated applications with 32.25% share in 2025; snacks and savory products will expand the quickest at 7.12% CAGR over the same horizon.

- By geography, Brazil accounted for 57.65% of regional demand in 2025, but Colombia is set to post the strongest geographic growth at 6.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Sodium Reduction Agents Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growth in packaged and processed food consumption Growth in packaged and processed food consumption | +1.2% | Brazil, Colombia, urban centers in Argentina | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Brazil, Colombia, urban centers in Argentina | Impact Timeline:Medium term (2-4 years) |

Rising health consciousness and awareness of hypertension and CVD Rising health consciousness and awareness of hypertension and CVD | +1.5% | Pan-regional, concentrated in Brazil and Colombia | Long term (≥ 4 years) | |||

Rising popularity of functional and "Better-For-You" food products Rising popularity of functional and "Better-For-You" food products | +1.0% | Urban Brazil (São Paulo, Rio de Janeiro), Bogotá, Santiago | Medium term (2-4 years) | |||

Clean-label demand for mineral and yeast-based solutions Clean-label demand for mineral and yeast-based solutions | +0.9% | Brazil, Colombia, Argentina export-oriented processors | Short term (≤ 2 years) | |||

Mandatory and voluntary sodium-reduction regulations and policies Mandatory and voluntary sodium-reduction regulations and policies | +1.3% | Brazil (ANVISA), Colombia (INVIMA), Argentina (ANMAT) | Short term (≤ 2 years) | |||

International pressure for compliance with global health guidelines International pressure for compliance with global health guidelines | +0.8% | Pan-regional, driven by WHO/PAHO targets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growth in packaged and processed food consumption

The increasing consumption of packaged and processed foods across South America is driving significant demand for sodium reduction agents. In Argentina, urban consumers are particularly turning to processed and convenience foods due to limited time for traditional meal preparation. Sodium reduction agents enable manufacturers to reduce salt content in these products while preserving flavor and consumer acceptance. As of 2024, approximately 92.58% of Argentina's population resides in urban areas (World Bank), positioning the market for sodium reduction solutions for substantial growth alongside the rising consumption of packaged and processed foods[1]Source: World Bank, "Urban population (% of total population) - Argentina," worldbank.org. This trend presents a challenge, the growth in product categories with high baseline sodium content, such as processed meats, cheese analogs, and savory snacks, compels manufacturers to adopt sodium reduction alternatives. Failure to do so risks front-of-package warning labels, which have been associated with 15-20% declines in sales for labeled SKUs. In response, multinational brands are reformulating key SKUs using potassium-chloride blends at replacement ratios of 25-30%, a level at which consumer taste panels report minimal detection of off-notes.

Rising health consciousness and awareness of hypertension and CVD

Increasing awareness of health risks associated with high sodium intake is driving consumers to opt for healthier dietary choices, particularly those that help reduce sodium consumption without sacrificing taste. As a result, the demand for sodium reduction agents is growing, with manufacturers and food producers developing products that balance flavor and health. These solutions are becoming critical in addressing hypertension and promoting cardiovascular health. According to the World Health Organization (WHO), the prevalence of hypertension among adults aged 30–79 in Argentina reached 51% in 2024, significantly higher than the global average of 34% [2]Source: World Health Organization, "Hypertension profile," cdn.who.int. This highlights widespread exposure to elevated blood pressure and a heightened risk of cardiovascular diseases (CVD). In Brazil, the average sodium intake is 11 grams per day, while in Argentina, it is 12 grams, both more than double the WHO-recommended limit of 5 grams. This clinical urgency has prompted regulators to implement mandatory labeling and voluntary reformulation agreements with industry associations. These epidemiological trends are influencing consumer behavior: a 2024 survey in São Paulo revealed that 68% of respondents actively look for low-sodium labels, up from 51% in 2022, and 34% are willing to pay a 10-15% premium for reformulated products that maintain comparable taste.

Rising popularity of functional and "Better-For-You" food products

The growing demand for functional and "better-for-you" food products is driving the need for sodium reduction solutions across South America. In Brazil's premium retail market, this trend is particularly evident, with companies like Nestlé and Unilever introducing "conscious nutrition" product lines. These products utilize yeast-extract umami enhancers and mineral-salt systems to achieve sodium reductions of 30–40%, while maintaining taste profiles that are often challenging for reformulated products. A key strategy involves combining multiple benefits; consumers are more likely to accept slight taste modifications when products also offer features such as fiber enrichment, sugar reduction, or clean-label attributes, mitigating the sensory impact of sodium substitutes. Manufacturers are increasingly collaborating with ingredient suppliers to co-develop formulations, marking a shift from traditional procurement practices to innovation-focused partnerships.

Clean-label demand for mineral and yeast-based solutions

Consumer preference for clean-label products is a significant driver in the South American sodium reduction agents market. Health-conscious consumers are increasingly examining ingredient lists, favoring recognizable and minimally processed components over artificial additives. Mineral salts and yeast-based solutions have gained popularity as alternatives to traditional sodium chloride due to their natural appeal and ability to enhance flavor without compromising taste. In Brazil, leading food manufacturers are incorporating yeast extracts and mineral salt blends into processed foods, achieving notable sodium reductions while maintaining product palatability. These solutions are particularly prominent in the premium and functional food segments, where clean-label claims, such as “natural” or “no artificial additives,” strongly influence purchasing decisions. In Argentina and other emerging South American markets, adoption is progressing more gradually but is steadily increasing among export-oriented processors, especially in dairy and meat products, to align with regional health trends and international regulatory requirements.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Taste perception challenges of KCl and mineral salts Taste perception challenges of KCl and mineral salts | -0.7% | Pan-regional, acute in price-sensitive segments | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:Pan-regional, acute in price-sensitive segments | Impact Timeline:Short term (≤ 2 years) |

Competitive price pressure from traditional salt Competitive price pressure from traditional salt | -0.9% | Argentina, rural Brazil, value retail channels | Medium term (2-4 years) | |||

Limited local alternative ingredient production Limited local alternative ingredient production | -0.6% | Argentina, secondary cities in Colombia | Long term (≥ 4 years) | |||

Consumer awareness gaps and reformulation challenges Consumer awareness gaps and reformulation challenges | -0.5% | Rural areas, lower-income demographics across region | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Taste perception challenges of KCl and mineral salts

Replacing more than 30% of sodium with potassium chloride introduces metallic and bitter off-notes, which consumer sensory panels consistently deem unacceptable. This threshold limits the effectiveness of sodium reduction and compels manufacturers to use taste-masking agents, such as amino acids, yeast extracts, and flavor enhancers, which increase formulation costs by 12-18% [3]Source: IFT Food Science, ift.onlinelibrary.wiley.com. This sensory challenge is particularly pronounced in savory snacks and processed meats, where salt contributes not only to flavor but also to mouthfeel and texture through protein-solubilization mechanisms that potassium salts cannot fully replicate. Consequently, sodium reduction follows a logarithmic curve, initial reductions of 20-30% are achievable at relatively low costs, but further reductions demand significantly higher investments in masking technologies and consumer education. Premium brands can absorb these additional costs, but value-tier products, where price elasticity exceeds -1.5, face a difficult choice between accepting warning labels or abandoning reformulation efforts. This results in a bifurcated market, with innovation concentrated in high-margin categories, while mass-market staples remain under-reformulated, perpetuating the sodium-intake gap that regulators aim to address.

Competitive price pressure from traditional salt

Refined sodium chloride is priced at USD 80-120 per metric ton in South American spot markets, while potassium chloride is valued at USD 450-600 per ton, and yeast extracts range from USD 8,000-12,000 per ton. This creates a 4-10x cost differential, which reduces processor margins unless compensated by premium pricing or regulatory compliance advantages. The impact of this price disparity is particularly severe in Argentina, where peso depreciation and import tariffs on specialty ingredients increase the landed cost of alternatives. As a result, domestic processors often prioritize traditional salt in value-tier SKUs aimed at price-sensitive consumers. In contrast, Brazil's market demonstrates a higher acceptance of cost premiums, driven by front-of-package warnings that can lead to significant sales penalties, estimated at 15-20% volume declines for labeled products, thereby encouraging reformulation investments. Ingredient suppliers are addressing this challenge by developing mid-tier solutions, such as potassium chloride blends with 15-20% replacement ratios. These blends enable partial sodium reduction at price points 30-40% lower than full-replacement formulations, targeting the mass-market segment that cannot be economically served by pure-play alternatives.

Segment Analysis

By Source: Synthetic Dominance Reflects Cost Realities

In 2025, synthetic alternatives accounted for 53.72% of the market share, driven by their cost-efficiency and well-established supply chains. These supply chains favor ingredients such as potassium chloride and chemically synthesized amino acids over fermentation-derived natural extracts. However, natural alternatives are projected to grow at an annual rate of 6.41% through 2031, surpassing the baseline growth of synthetic alternatives. This shift is attributed to increasing clean-label mandates and consumer concerns over E-numbers, prompting a preference for yeast extracts and mineral salts derived from seawater evaporation or mineral-deposit extraction. The divergence is particularly evident in premium bakery and organic snack categories. Brands like Bauducco and Marilan have reformulated key products with natural yeast extracts to avoid synthetic-additive declarations, accepting cost premiums of 15-20% to maintain shelf placement in health-focused retail outlets.

Synthetic alternatives continue to dominate cost-sensitive applications such as industrial bread, value-tier seasonings, and bulk processed meats. In these segments, price elasticity limits the adoption of natural ingredients, and regulatory compliance is often achieved through partial sodium reduction rather than complete clean-label reformulation. In Argentina, the market remains heavily skewed toward synthetic alternatives due to import dependencies and currency volatility, which increase the costs of natural ingredients. However, export-oriented dairy processors in the country are increasingly adopting natural alternatives to meet European Union organic certification requirements. The competitive landscape favors integrated suppliers such as DSM-Firmenich and Kerry Group, which offer both synthetic and natural ingredient portfolios. These suppliers provide blended solutions that balance cost and performance, catering to diverse application requirements across the market.

Note: Segment shares of all individual segments available upon report purchase

By Type: Amino Acids Emerge as Taste-Masking Solution

Mineral salts accounted for a 38.10% market share in 2025, supported by the cost-efficiency of potassium chloride (KCl) and its effectiveness in sodium reduction, particularly in applications where bitterness can be mitigated through flavor-system design or co-ingredient synergies. Amino acids are projected to grow at a compound annual growth rate (CAGR) of 6.78% through 2031, driven by their dual role as taste enhancers and sodium-masking agents, addressing the metallic off-notes often associated with standalone KCl formulations. Lysine-KCl blends enable a 40-50% reduction in sodium content while maintaining consumer acceptance levels above 7.5 on a 10-point scale in snack applications. Glutamates, including yeast extracts, held a 28.00% market share and are expected to benefit from regulatory trends favoring clean-label products. Emerging seaweed extracts remain in an early stage of development but show potential in organic categories, such as plant-based seafood analogs, where premium pricing and ecolabels are prevalent.

The "Others" category, which includes innovative solutions like seaweed extracts and fermented vegetable powders, is still in its infancy but is anticipated to grow as ingredient innovation targets niche applications. These include organic baby food and premium plant-based meats, where clean-label requirements and premium pricing support experimental formulations. In Brazil, condiment producers segment their portfolios strategically: yeast-extract glutamates are used in premium table seasonings, amino-acid blends are incorporated into mid-priced soups, and mineral salts are utilized in cost-effective bouillon cubes. This tiered approach aligns with consumer willingness to pay across different segments, optimizing market penetration for sodium reduction agents.

By Application: Snacks Outpace Traditional Bakery Growth

In 2025, the bakery and confectionery segment accounted for 32.25% of the sodium reduction agents market. Snacks and savory products are projected to achieve the highest growth, with a CAGR of 7.12% through 2031. This growth is driven by portable formats that face front-of-package scrutiny but continue to command premium pricing. Condiments, seasonings, and sauces represent a 17.65% market share, with yeast-extract umami offering a near one-to-one replacement for salt in flavor intensity, enabling significant sodium reductions. The meat and dairy segments remain challenging yet promising, as protein-salt interactions require customized mineral matrices to maintain texture. For instance, solutions combining magnesium sulfate with potassium chloride (KCl) are undergoing testing at dairy plants aiming to reduce sodium by 25% without affecting yield.

Snack reformulations have shown scalability across products such as potato chips, extruded maize sticks, and nuts, allowing ingredient suppliers to replicate successes efficiently. In the bakery segment, dough systems require adaptation; however, improved enzyme blends have been developed to maintain gluten elasticity even with sodium reductions of up to 30%. The meat segment remains a critical area for innovation, with potential to unlock an additional USD 50 million in market size for sodium reduction agents, provided bitterness challenges can be addressed effectively.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, Brazil accounted for 57.65% of the regional sodium reduction agents market revenue, supported by its USD 200 billion food-processing industry and the black-octagon labeling system, which discourages high-sodium formulations. São Paulo and Rio de Janeiro, contributing 35% of national food sales, exhibit the highest adoption rates of salt alternatives due to the dominance of organized retail and consumer willingness to pay premiums for taste-neutral options. Ingredient multinationals focus on local basestock fermentation or import hubs at Santos to reduce lead times and mitigate currency risks.

Colombia is projected to be the fastest-growing market, with a CAGR of 6.61%, driven by urbanization exceeding 80% and the influence of store brands enforcing sodium-reduction guidelines. Bogotá, Medellín, and Cali, which together account for 55% of packaged food purchases, are early adopters of potassium-chloride blends, achieving replacement rates of 20-25%. A future Colombian labeling law, modeled after Brazil's system, is anticipated to pass by 2027, further accelerating market growth.

Argentina contributed to a significant share of the 2024 revenue. However, peso devaluation has increased import costs for specialty yeast extracts, limiting adoption outside export-oriented dairy and meat plants that must comply with European Union standards. Chile, Peru, and Ecuador collectively accounted to a small market share. These markets are advancing rapidly, with Chile's earlier labeling law demonstrating a 37% reduction in purchase volumes for products with salt warnings, a statistic frequently referenced by local regulators when drafting new measures.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

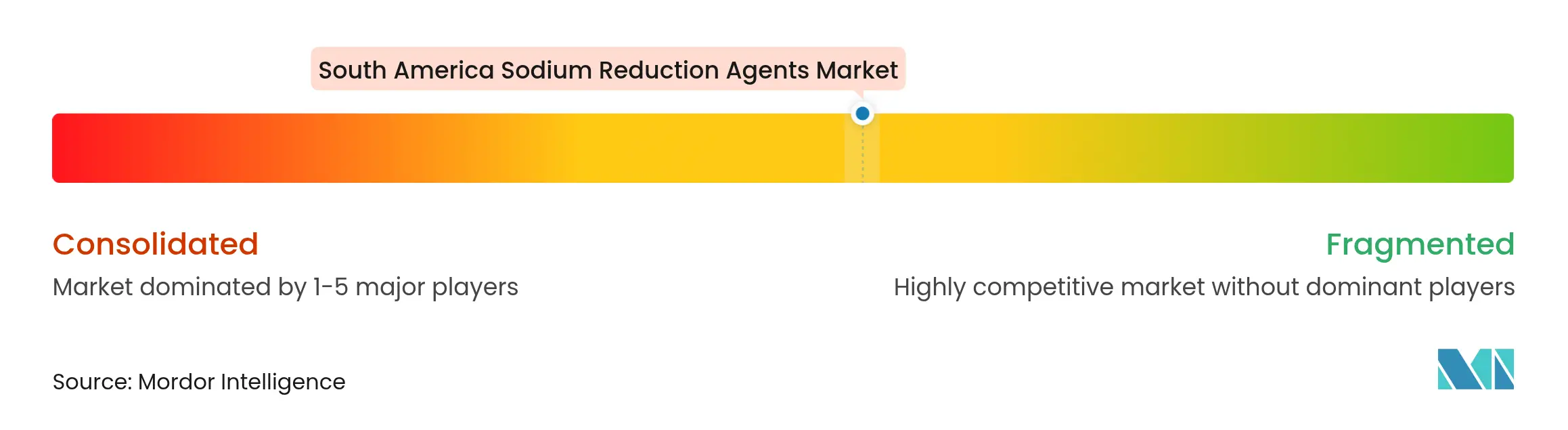

The South America sodium reduction agents market is moderately fragmented, with global ingredient companies such as Cargill, DSM-Firmenich, Kerry Group, and Tate & Lyle competing alongside regional yeast-extract specialists, Asian amino-acid exporters, and local mineral-salt distributors. Competitive differentiation in this market is driven by three key capabilities: fermentation-based clean-label solutions that provide umami depth while masking sodium, application laboratories that collaborate with processors on reformulations, and localized supply chains that reduce import-dependency risks, particularly in Argentina and secondary cities in Colombia.

Growth opportunities are concentrated in dairy and meat applications, where protein-salt interactions present technical challenges that current suppliers have not fully addressed. Additionally, mid-tier price segments offer potential for potassium-chloride blends with 20-25% replacement ratios, catering to cost-sensitive processors who are hesitant to adopt higher-cost amino-acid or yeast-extract solutions.

Technology-driven advancements are reshaping the market, with suppliers leveraging sensory-science databases, predictive modeling tools, and rapid prototyping to reduce reformulation timelines from 12-18 months to 6-9 months. This accelerated pace provides a competitive edge, particularly when regulatory deadlines are imminent. Regulatory compliance is also emerging as a significant competitive advantage. Suppliers with ISO 22000 food-safety certifications, Kosher and Halal approvals, and organic-input certifications are better positioned to serve export-oriented processors targeting premium international markets, creating switching costs that commodity suppliers are unable to match.

South America Sodium Reduction Agents Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: French fermentation specialist Lesaffre finalized a joint venture with Brazilian agribusiness Zilor by acquiring 70% of Biorigin, Zilor’s yeast-derivatives business unit. This partnership integrates Lesaffre’s Biospringer fermentation expertise with Biorigin’s natural ingredient capabilities to provide advanced yeast-based solutions for the global food and feed markets. The agreement includes Biorigin’s production facility in Quatá, São Paulo, recognized for its carbon-neutral operations, while retaining the Biorigin brand for product marketing.

- March 2023: Tate & Lyle announced IMCD as its exclusive distribution partner in Brazil. This collaboration seeks to expand Tate & Lyle’s range of sweetening, texture, stabilization, and fortification ingredient solutions across the food, beverage, nutrition, and supplement industries within the Brazilian market.

Table of Contents for South America Sodium Reduction Agents Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growth in packaged and processed food consumption

- 4.2.2Rising health consciousness and awareness of hypertension and CVD

- 4.2.3Rising popularity of functional and "Better-For-You" food Products

- 4.2.4Clean-label demand for mineral and yeast-based solutions

- 4.2.5Mandatory and voluntary sodium‑reduction regulations and policies

- 4.2.6International pressure for compliance with global health guidelines

- 4.3Market Restraints

- 4.3.1Taste perception challenges of KCl and mineral salts

- 4.3.2Competitive price pressure from traditional salt

- 4.3.3Limited local alternative ingredient production

- 4.3.4Consumer awareness gaps and reformulation challanges

- 4.4Supply Chain Analysis

- 4.5Regulatory and Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECATS (VALUE)

- 5.1By Source

- 5.1.1Synthetic

- 5.1.2Natural

- 5.2By Type

- 5.2.1Mineral Salts

- 5.2.2Amino Acids

- 5.2.3Glutamates

- 5.2.4Others

- 5.3By Application

- 5.3.1Bakery and Confectionery

- 5.3.2Condiments, Seasonings, and Sauces

- 5.3.3Dairy Products

- 5.3.4Snacks and Savory

- 5.3.5Meat and Seafood Products

- 5.3.6Other Applications

- 5.4By Geography

- 5.4.1Brazil

- 5.4.2Colombia

- 5.4.3Argentina

- 5.4.4Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1Cargill Inc.

- 6.4.2Tate & Lyle PLC

- 6.4.3Givaudan SA

- 6.4.4Kerry Group PLC

- 6.4.5Corbion NV

- 6.4.6DSM‐Firmenich

- 6.4.7Angel Yeast Co.

- 6.4.8Lesaffre (Biospringer)

- 6.4.9Sensient Technologies Corp.

- 6.4.10Archer Daniels Midland Co.

- 6.4.11Kudos Blends Ltd.

- 6.4.12NuTek Food Science

- 6.4.13Ohly GmbH

- 6.4.14Solina Group

- 6.4.15Innophos Holdings Inc.

- 6.4.16Advanced Food Systems Inc.

- 6.4.17Lallemand Bio-Ingredients

- 6.4.18Ajinomoto Co.

- 6.4.19Bunge Alimentos SA

- 6.4.20Morton Salt (K+S AG)

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

South America Sodium Reduction Agents Market Report Scope

South America sodium reduction ingredient market is segmented by product type into amino acids and glutamates, mineral salts, yeast extracts, and others. By application, the market is segmented as bakery and confectionery, seasonings and sauces, dairy and frozen foods, meat and meat products, snacks, and others. The ingredient market has also been classified by country into Brazil, Argentina, and the Rest of South America.