United States Private 5G Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

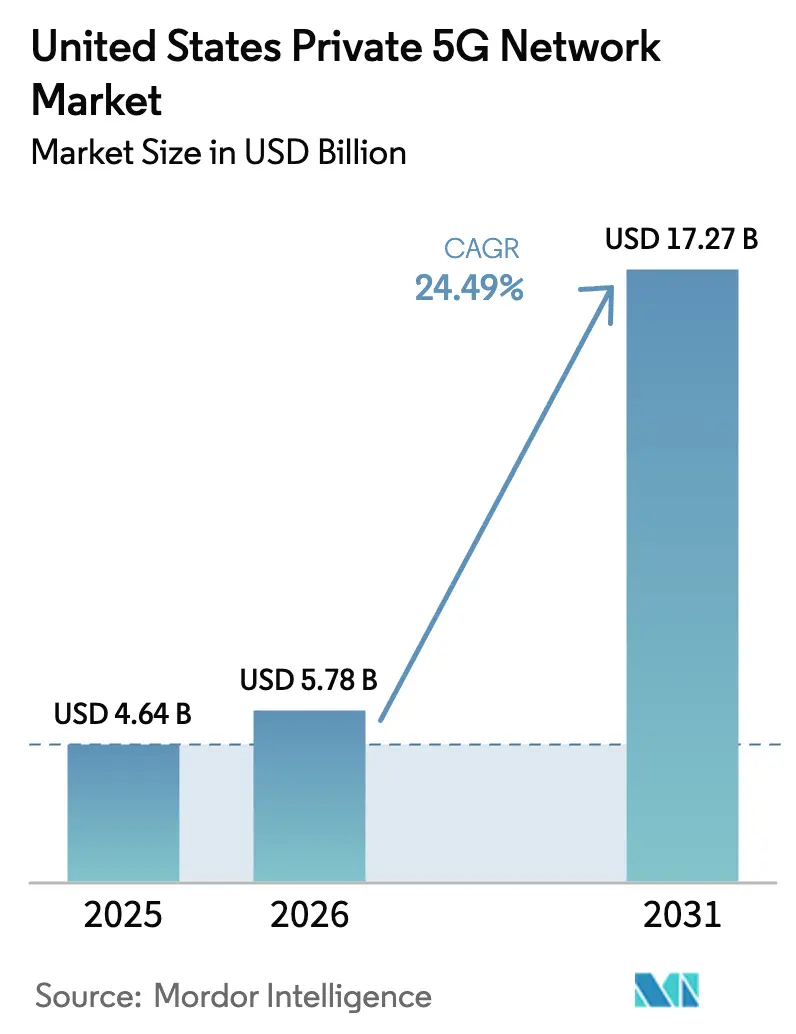

| Base Year Market Size (2025) | USD 4.64 Billion |

| Market Size (2026) | USD 5.78 Billion |

| Market Size (2031) | USD 17.27 Billion |

| Growth Rate (2026 - 2031) | 24.49% CAGR |

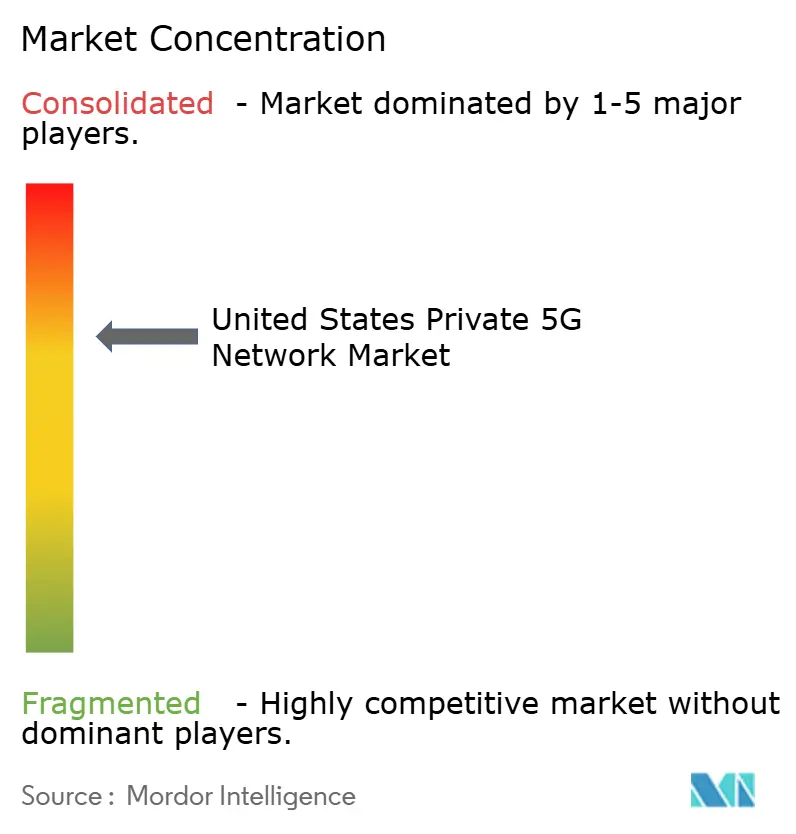

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Private 5G Network Market Analysis by Mordor Intelligence

The United States Private 5G Network Market size was valued at USD 4.64 billion in 2025 and estimated to grow from USD 5.78 billion in 2026 to reach USD 17.27 billion by 2031, at a CAGR of 24.49% during the forecast period (2026-2031).

Strong growth reflects three inter-linked forces: spectrum liberalization through Citizens Broadband Radio Service (CBRS), large federal incentives to reshore advanced manufacturing, and enterprise demand for ultra-low-latency edge computing. The 2024 CBRS modernization rules opened unencumbered access for 72 million additional Americans, improving the economics of private deployments and accelerating time-to-market. Manufacturing adoption remains the primary revenue driver, yet healthcare, utilities, and logistics facilities now pilot mission-critical applications ranging from robotic surgery to automated port operations. Competitive intensity is rising as traditional telecom vendors, neutral-host specialists, and cloud hyperscalers form joint go-to-market programs, while the Department of Defense’s mandate for private 5G across 800+ bases creates a sizeable public-sector demand pool.

Key Report Takeaways

- By end-user industry, manufacturing led with 37.40% of the United States Private 5G Network market share in 2025, while healthcare is forecast to expand at a 29.6% CAGR through 2031.

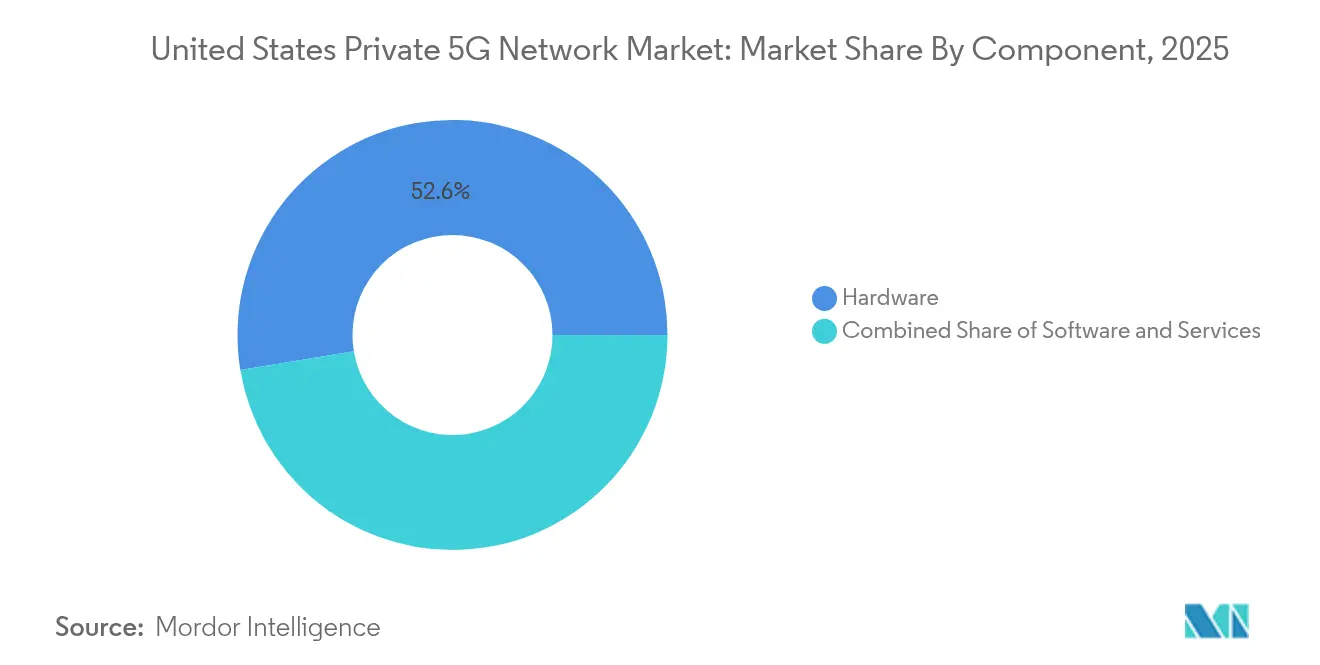

- By component, hardware held 52.60% revenue share in 2025; services record the highest projected CAGR at 25.8% through 2031.

- By frequency, sub-6 GHz commanded 77.10% share in 2025; mmWave is growing fastest at a 30.7% CAGR to 2031.

- By spectrum ownership, shared CBRS accounted for a 61.30% share in 2025 and is advancing at a 24.9% CAGR, thanks to rule reforms that boost spectrum certainty.

- By enterprise size, large enterprises represented 67.20% of active networks in 2025, but small and medium enterprises (SMEs) are registering a 27.8% CAGR as Network-as-a-Service (NaaS) models lower capex thresholds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Private 5G Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for dedicated Industry 4.0 networks | 6.20% | National manufacturing hubs | Medium term (2-4 years) |

| Spectrum liberalization (CBRS) accelerates rollouts | 5.80% | Urban centers nationwide | Short term (≤ 2 years) |

| Edge/IoT latency requirements | 4.90% | Industrial corridors | Medium term (2-4 years) |

| Federal reshoring incentives | 3.70% | Rust & Sun Belt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Dedicated Industry 4.0 Networks

Manufacturing plants now treat private 5G as core operational infrastructure rather than pilot technology. BMW’s Spartanburg facility coordinates autonomous robots and vision systems in real time, driving measurable throughput gains[1]Tejas Mehra, “BMW Expands Private 5G at Spartanburg,” tecknexus.com. Tesla integrates Ericsson radios to cut factory cabling costs by up to 40%. John Deere targets a 90% reduction in wired links as it shifts to 5G for machine control and predictive maintenance. Semiconductor fabs deploy private 5G to support chemical monitoring and automated transport, boosting yield stability. The pattern signals that private 5G will become baseline infrastructure for next-generation U.S. manufacturing sites through 2030.

Spectrum Liberalization (CBRS) Accelerates Rollouts

The FCC’s August 2024 update extended transmit-expiry timers and expanded Dynamic Protection Areas, cutting planning risk for enterprises. Active CBRS devices rose to 400,403 by July 2024, with 71.4% operating in General Authorized Access mode, underscoring the appetite for low-cost unlicensed spectrum. Rural installations doubled, proving CBRS effective in low-density areas. Collaborative coexistence rules now let multiple enterprises share spectrum inside industrial parks, further lowering entry barriers. These reforms cement CBRS as the default spectrum path for the United States Private 5G Network market.

Edge/IoT Latency Requirements Drive Private 5G

The Department of Homeland Security expects 55.7 billion connected devices by 2025, pushing compute workloads towards the edge. Toyota Material Handling and CJ Logistics cite real-time monitoring gains after switching to private 5G. Remote telesurgery between Orlando and Dubai proved sub-10 ms latency viability for healthcare. Southern California Edison’s Nokia-powered grid network demonstrates energy-sector interest in fault isolation and distributed resource management. As artificial intelligence converges with edge compute, latency-sensitive workflows will multiply, keeping demand elevated.

Federal Reshoring Incentives Spur Factory Upgrades

The CHIPS Act earmarked USD 52.7 billion for domestic semiconductor capacity, while the Inflation Reduction Act introduced advanced-manufacturing tax credits. Manufacturing construction spending hit an annualized USD 189 billion in 2024, and new mega factories now specify private 5G in their digital blueprints. The American Jobs Plan’s procurement commitments add tailwinds for smart factories that require deterministic wireless connectivity. Clustering of fabs in Arizona, Texas, and Ohio is creating regional private-5G demand hubs serviced by local system integrators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront implementation costs | -4.30% | SMEs nationwide | Short term (≤ 2 years) |

| Rising cyber-liability under new federal rules | -2.20% | Defense contractors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Implementation Costs

Enterprise deployments range from USD 250,000 to USD 1.2 million, challenging SME budgets. A single 5G base station can cost USD 100,000-200,000, while integration services often double total spends. Roll-outs can stretch 6-12 months, requiring scarce 5G engineering talent. NaaS providers such as Boldyn Networks mitigate capex with subscription models and expect 30-40% cost reductions through shared infrastructure. Volume chipset production is also reducing radio prices by 15% yearly, easing the cost curve.

Rising Cyber-liability Under New US Federal Rules

CMMC 2.0 elevates security requirements for defense-facing enterprises, adding compliance layers to private networks Department of Defense. The Cyber Incident Reporting for Critical Infrastructure Act may impose USD 2.6 billion in collective compliance costs across more than 300,000 entities. FCC labeling now obliges IoT device makers to meet NIST benchmarks, narrowing device choices and increasing costs. NIST’s 5G security guidance stresses zero-trust frameworks that require extra investment in identity management and encryption[4]National Institute of Standards and Technology, “Zero-Trust Architecture for 5G,” nist.gov. Upcoming supply-chain security rules from the Department of Commerce deepen due diligence needs for component sourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Hardware Dominance

Hardware accounted for 52.60% of the United States Private 5G Network market share in 2025, confirming the capital-intensive nature of cellular infrastructure. Yet services are expanding at a 25.8% CAGR as enterprises outsource design, operation, and life-cycle management to specialist providers. The shift stems from limited in-house 5G expertise and growing demand for turnkey monitoring, spectrum coordination, and cybersecurity.

Managed offerings from Boldyn Networks, HPE Aruba Networking, and Celona highlight a pivot to recurring revenue. Ericsson’s 5G Core-as-a-Service with Google Cloud lets enterprises launch networks in weeks, scaling resources elastically while paying only for usage. As service models mature, many buyers prefer minimal capex and rapid commissioning over equipment ownership. This trend suggests services could eclipse hardware revenues before 2030, realigning the value chain around operations rather than radios.

By Frequency: mmWave Surges Despite Sub-6 GHz Leadership

Sub-6 GHz bands held 77.10% share in 2025 because CBRS grants wide-area coverage with moderate infrastructure counts. mmWave, while coverage-limited, registers a 30.7% CAGR on the back of bandwidth-intensive use cases such as AR-guided assembly and 4K machine-vision analytics.

T-Mobile’s mid-band optimization reached 388 Mbps median enterprise speeds, demonstrating the productive ceiling of sub-6 GHz for mainstream workloads. Indoors, Ericsson’s Radio Dot mmWave solution cuts energy use up to 70%, supporting multiple carriers inside high-density venues. As Release 18’s 5G-Advanced features unlock improved beamforming and positioning accuracy, mmWave economics will continue to improve, extending adoption beyond today’s early industrial clusters.

By Spectrum Ownership: Shared CBRS Maintains Dual Leadership

Shared CBRS held 61.30% revenue share in 2025 and is growing at 24.9% CAGR as rule tweaks extend protection periods and simplify coexistence. Enterprises appreciate near-licensed performance without auction costs, and rural adopters now represent 67.5% of all CBRS devices.

Specialized aggregators like Citizens Band License Company are purchasing disparate PAL holdings to build statewide footprints, further reducing leasing complexity for enterprises. Licensed spectrum remains essential for airports, utilities, and defense bases requiring deterministic performance, while unlicensed 5 GHz Wi-Fi still supports non-critical sensor traffic. The blended spectrum approach gives U.S. buyers flexibility unmatched in most other regions.

By Enterprise Size: SMEs Accelerate Despite Large-Enterprise Dominance

Large corporations commanded 67.20% of deployments in 2025, leveraging deep capital and IT capabilities. However, SME uptake is accelerating at 27.8% CAGR as subscription-based 5G LAN products reduce financial barriers.

Platforms from Amantya Tech and HPE Aruba Networking bundle radios, SIM administration, and lifecycle support into monthly fees. Stanford Health Care’s neutral-host model shows that shared infrastructure can match Wi-Fi coverage with fewer access points, cutting opex. Fewer than 20 radios can deliver blanket coverage for many facilities, further improving the SME business case. As integration tools mature, SME adoption is set to broaden the addressable base of the United States Private 5G Network market.

By End-User Industry: Healthcare Surges While Manufacturing Leads

Manufacturing captured a 37.40% share in 2025, reflecting early Industry 4.0 pilots that demonstrated clear ROI. Fabs, automotive lines, and heavy-equipment plants rely on private 5G for robotic coordination and predictive analytics.

Healthcare is the fastest mover with a 29.6% CAGR to 2031 as hospitals deploy low-latency networks for remote surgery, patient telemetry, and secure asset tracking. Defense drives additional volume under the 800-base private-5G mandate, while ports such as Jacksonville and Long Beach install Nokia’s Digital Automation Cloud to automate container movements. The broadening mix of verticals ensures sustained multi-segment momentum for the United States Private 5G Network industry.

Geography Analysis

The United States leads global private 5G adoption thanks to CBRS access, sizable stimulus funding, and early industrial use cases. CBRS liberalization uniquely allows American enterprises to build deterministic networks without costly spectrum auctions. Concentrations of manufacturing in the Rust Belt and newly built mega-fabs across the Sun Belt dominate early deployment maps, driven by federal reshoring incentives.

Rural coverage gaps are narrowing after the FCC’s USD 9 billion 5G Fund allocations. T-Mobile already reaches its 90% rural-population target, while AT&T leverages FirstNet to extend low-band coverage. Neutral-host providers have rolled out more than 50 private networks in metros from New York to Dallas, helping venue owners improve indoor performance without dense macro cells.

The Department of Defense spreads demand across every state through its base program, and multiple state universities have launched CBRS testbeds to train the next cohort of 5G engineers. West Virginia and Wyoming saw the sharpest year-over-year rise in 5G availability in 2024 after new mid-band allocations. This combined urban-rural expansion sustains year-round demand cycles for equipment suppliers and integrators.

Competitive Landscape

The United States Private 5G Network market shows moderate concentration. Nokia and Ericsson maintain leadership, backed by extensive patent portfolios and carrier relationships. Nokia added 55 private-wireless customers in Q4 2024, bringing its global count to 850; 24% sit in North America. Ericsson reported 17% growth in enterprise wireless despite broader revenue softness and holds more than 60,000 granted patents.

Cloud hyperscalers, neutral-host specialists, and system integrators are reshaping the field. Ericsson’s 5G Core-as-a-Service with Google Cloud exemplifies a pivot to software-defined architecture that reduces hardware lock-in. Verizon and Cummins’ neutral-host deployment signals the carrier’s willingness to combine public and private assets for enterprise customers[2]Ellen Murphy, “Verizon and Cummins Combine Neutral Host with Private 5G,” verizon.com. Boldyn Networks’ EUR 300 million commitment to Private 5 G-as-a-Service indicates growing investor confidence in managed models.

Patent-licensing remains a competitive lever as Samsung, Huawei, and Qualcomm collectively hold more than 25,000 essential 5G patents, creating royalty flows that can offset hardware margin compression. Open RAN preferences in DoD contracts open the door to new entrants fluent in interoperable software stacks, potentially diluting traditional vendor dominance over time. As a result, partnership ecosystems rather than discrete vendors increasingly decide deal wins.

United States Private 5G Network Industry Leaders

Anterix, Inc.

Motorola Solutions, Inc.

Cisco Systems, Inc.

Telefonaktiebolaget LM Ericsson

Hewlett Packard Enterprise Company (HPE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson and Google Cloud launched Ericsson On-Demand, a carrier-grade 5G core-as-a-service platform with AI-driven troubleshooting and pay-per-use billing.

- June 2025: The city of Istres, France, activated a private 5G network with Ericsson, SPIE, and Unitel to enable AI-based urban solutions.

- April 2025: Verizon introduced 5G Standalone network slicing for first-responder vehicles across 29 U.S. markets under the Frontline Network Slice program.

- April 2025: Nokia’s Q1 2025 results showed a 27% rise in enterprise sales, with private-5G revenues driving 13.5% of total; the company also extended a multi-year 5G deal with T-Mobile US.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, powered by Mordor Intelligence, defines the United States private 5G network market as all revenue earned from enterprise-owned or agency-owned 5G equipment and services, radio units, core software, orchestration tools, and ongoing managed or professional support, deployed on-premises or across restricted-access campuses. Networks may run in licensed, shared CBRS, or unlicensed spectrum across sub-6 GHz and millimeter-wave bands and support use cases in manufacturing, utilities, logistics hubs, healthcare complexes, and public-safety estates.

Scope Exclusion: Public carrier 5G slices resold to enterprises without dedicated on-site radio assets lie outside this market.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Frequency

- Sub-6 GHz

- mmWave

- By Spectrum Ownership

- Licensed

- Shared/CBRS

- Unlicensed

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Industry

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Healthcare

- Defense and Public Safety

- Other Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with network integrators, CBRS administrators, factory OT managers, hospital CIOs, and utility telecom leads across the Midwest, Gulf Coast, and Pacific corridors. Insights on cell-site counts, typical service bundles, and adoption pacing filled gaps and cross-checked desk findings.

Desk Research

We began with FCC CBRS installation rolls, NTIA spectrum-allocation updates, and CTIA small-cell counts to benchmark real deployment density. Economic tables from the Bureau of Economic Analysis and monthly industrial production indices revealed spending capacity, while trade groups such as the Industrial Internet Consortium and US Energy Association clarified vertical pain points. Company 10-Ks, investor presentations, and reputable press traced pilot budgets and contract flows. Paid intelligence from D&B Hoovers and Dow Jones Factiva enriched supplier splits and deal timelines. The sources named are illustrative; analysts referenced many more during validation.

Market-Sizing & Forecasting

A top-down construct starts with active private base-station counts, aggregates them into network clusters, then multiplies by vertical-specific average spend. Supplier roll-ups and sampled ASP multiplied by volume checks act as a bottom-up reasonableness filter; this is where Mordor Intelligence differentiates. Key variables include CBRS PAL issuance, industrial-robot shipments, edge-server sales, and federal smart-manufacturing grants. Five-year projections stem from multivariate regression and are subsequently stress-tested through scenario analysis for spectrum-pricing shocks.

Data Validation & Update Cycle

Outputs undergo variance checks against independent indicators before a second analyst review. Models refresh each year, with interim updates triggered by policy shifts or landmark contracts, so clients always receive the latest view.

Why Mordor's United States Private 5G Network Baseline Commands Reliability

Published figures vary because firms apply differing inclusion rules, input proxies, and refresh rhythms. By anchoring totals to verifiable deployment data and dual-path modelling, our baseline stays tightly linked to observable spend.

Key gap drivers include omission of service revenue, blending of LTE and early 5G counts, or use of global ASPs that ignore CBRS discounts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.64 B (2025) | Mordor Intelligence | - |

| USD 0.53 B (2023) | Regional Consultancy A | Hardware only; shared-spectrum sites excluded |

| USD 2.00 B (2025) | Trade Journal B | Mixes LTE with 5G; omits managed-service revenue |

These contrasts show Mordor Intelligence's deployment-anchored, transparently sourced baseline is the most dependable starting point for strategic planning.

Key Questions Answered in the Report

What is the United States Private 5G Network market size in 2026?

The market stands at USD 5.78 billion in 2026 and is forecast to reach USD 17.27 billion by 2031.

What compound annual growth rate (CAGR) is expected for the market through 2031?

The United States Private 5G Network market is projected to grow at a 24.49% CAGR between 2026 and 2031.

Which industry holds the largest share of private 5G deployments today?

Manufacturing leads with 37.40% of all U.S. private 5G installations because Industry 4.0 upgrades demand deterministic wireless connectivity.

Why is CBRS spectrum critical to private 5G adoption in the United States?

CBRS lets enterprises access mid-band spectrum without expensive auctions, lowering deployment costs and accelerating rollouts nationwide.

How quickly are small and medium enterprises (SMEs) adopting private 5G?

SME deployments are expanding at a 27.8% CAGR as Network-as-a-Service offerings remove high upfront capital requirements.

Who are the primary technology vendors in the United States Private 5G Network market?

Nokia and Ericsson dominate the current market share, but cloud hyperscalers, neutral-host specialists, and managed-service providers are growing rapidly, diversifying the competitive landscape.

Page last updated on: