United States Payroll Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

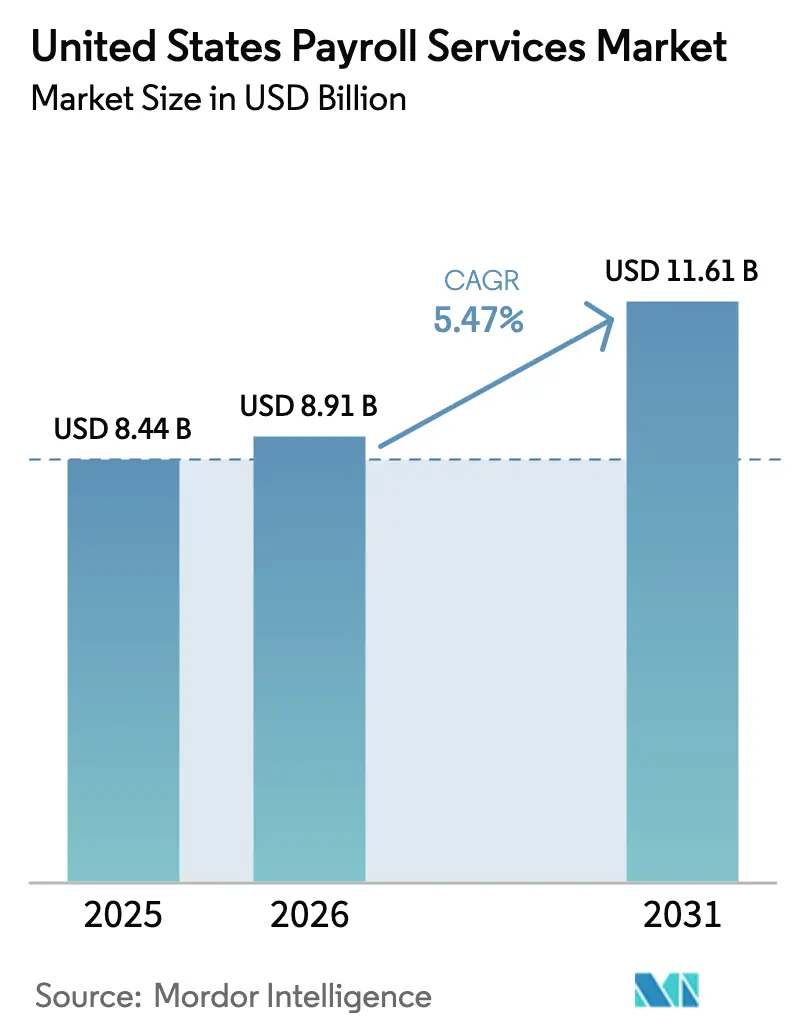

| Base Year Market Size (2025) | USD 8.44 Billion |

| Market Size (2026) | USD 8.91 Billion |

| Market Size (2031) | USD 11.61 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Payroll Services Market Analysis by Mordor Intelligence

The United States payroll services market size is expected to grow from USD 8.44 billion in 2025 to USD 8.91 billion in 2026 and is forecast to reach USD 11.61 billion by 2031 at 5.47% CAGR over 2026-2031. Demand growth originates from mounting regulatory complexity, rapid technology shifts, and rising employer focus on cost containment. Employers must now comply with the U.S. Department of Labor’s July 2024 overtime threshold of USD 43,888, which forces modernization of legacy payroll systems[1]U.S. Department of Labor, “Overtime Rule Changes,” DOL.gov.. Twenty-three states also operate paid family and medical leave schemes with unique wage bases and contribution schedules, amplifying the compliance burden facing multi-state employers. Small companies, most of which lack internal payroll expertise, increasingly outsource to contain administrative costs, protect data, and maintain accuracy. Concurrently, embedded payroll delivered by fintech platforms broadens the United States payroll services market’s addressable base by blending payments, benefits, and tax functionality under one user interface.

Key Report Takeaways

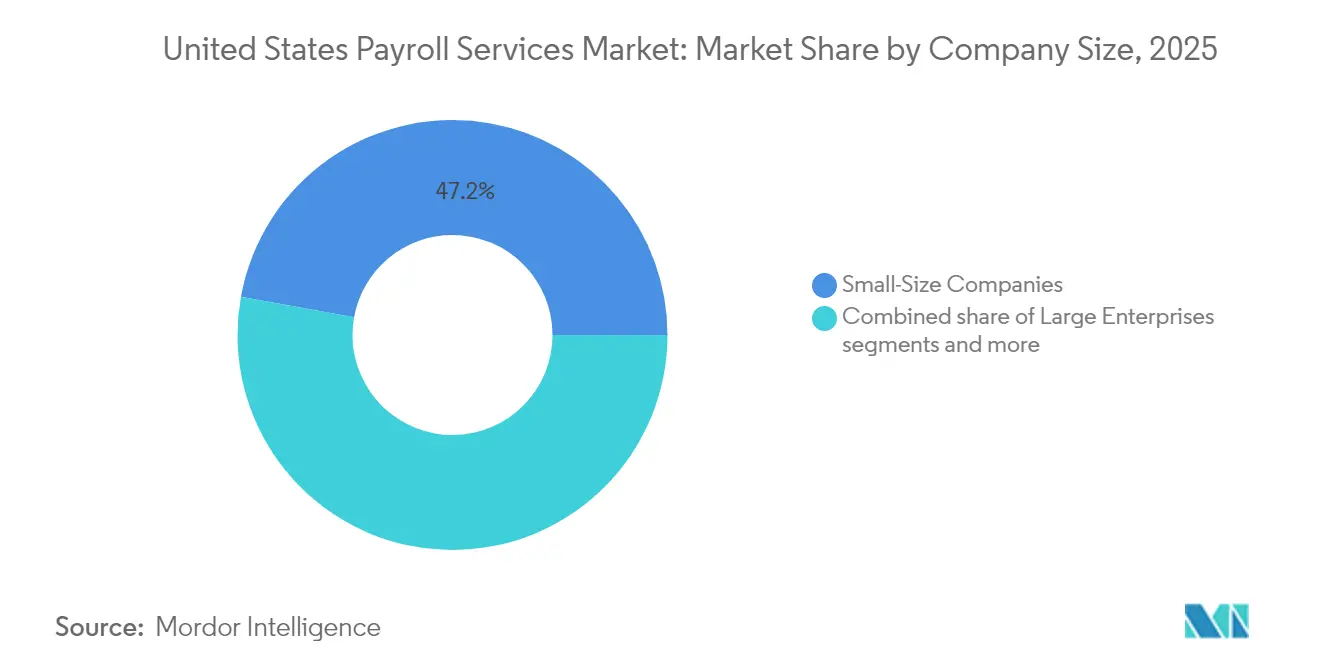

- By company size, Small-Size Companies held 47.15% of the United States payroll services market share in 2025, while Small-Size Companies are projected to log the fastest 10.95% CAGR through 2031.

- By end user, healthcare accounted for 21.05% of the United States payroll services market size in 2025; the IT sector is forecast to post the highest 10.49% CAGR to 2031.

- By geography, the South dominated with 34.98% of the United States payroll services market share in 2025, whereas the West is advancing at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on payroll services market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Payroll Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based payroll adoption surge | +1.8% | National; early gains in West and Northeast | Medium term (2-4 years) |

| Escalating multi-state tax & labor complexity | +2.1% | National; strongest in South and West multi-state corridors | Long term (≥ 4 years) |

| SMB outsourcing to reduce burden | +1.5% | National; concentrated in manufacturing-heavy Midwest | Short term (≤ 2 years) |

| HCM–payroll platform convergence | +1.2% | National; enterprise-focused in Northeast financial centers | Medium term (2-4 years) |

| Earned-wage-access (EWA) embedded in payroll suites | +1.3% | National, with early adoption in service-sector hubs | Short term (≤ 2 years) |

| AI-driven anomaly detection cutting error costs | +1.6% | National, strongest uptake in large-scale enterprise payrolls | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cloud-based Payroll Adoption Surge

Cloud migration accelerates because employers prefer platforms that deliver automatic updates, 24/7 accessibility, and lower infrastructure costs. ADP’s cloud architecture already processes payroll for more than 41 million workers, showcasing the model’s scalability and reliability[2]ADP Editorial Team, “The Potential of Payroll in 2025,” ADP.com. . For small and mid-size businesses, a cloud deployment typically closes within days, far quicker than the weeks demanded by on-premise installations. Seamless software updates remove the need for continuous IT patching and reduce disruption risk. Enhanced encryption coupled with SOC 2-type certifications ensures data security, an attribute that now ranks alongside cost in vendor selection criteria. Collectively, these benefits sustain elevated adoption rates across the United States payroll services market.

Escalating Multi-state Tax & Labor Compliance Complexity

Employers operating across jurisdictions navigate divergent income-tax regimes ranging from 2.5% in North Carolina to 11.5% in New Jersey, plus two states that levy none[3]American Payroll Association, “State Paid Family Leave Programs,” Payroll.org. . Remote work further expands exposure to multiple wage bases and paid family leave premiums, complicating calculations and increasing audit risk. The July 2024 federal overtime rule enlarged eligibility pools and introduced new salary thresholds, compounding administrative requirements. Companies increasingly regard outsourcing as a form of risk transfer, shifting liability for miscalculations to specialized vendors. Payroll providers respond by embedding automated rule engines that monitor legislative feeds and apply rate changes instantly. This structural complexity remains a durable engine of demand in the United States payroll services market.

SMB Outsourcing to Reduce Administrative Burden

Rising compliance workload coincides with labor shortages, prompting small businesses to offload payroll and concentrate on revenue-generating tasks. The American Psychological Association found 45% of workers put in longer hours than desired in 2024, underscoring the need for efficiency tools [4]American Psychological Association, “U.S. Workers Adjust to the Changing Nature of Employment,” APA.org.. Payroll mistakes directly erode employee satisfaction, with 55% of workers prepared to leave after a single pay error. Growing adoption of four-day workweeks implemented by 22% of employers in 2024 requires complex proration that many SMB tools cannot deliver. Earned-wage access and mobile pay slips have become differentiators for small firms in tight labor markets. Consequently, SMB outsourcing continues to underpin the expansion of the United States payroll services market.

HCM–Payroll Platform Convergence

Unified human-capital suites eliminate data silos by integrating time tracking, benefits, and payroll on a single database. Providers such as Paycom supply real-time synchronization that boosts accuracy and reduces manual inputs. Financial executives prioritize functionality and user experience over headline cost savings, according to a 2024 TD Securities survey. Converged platforms also introduce AI-driven validations that flag anomalies before payroll submission, improving compliance and reducing re-processing. In-house IT teams gain relief because one platform handles upgrades for all modules simultaneously. Demand for integrated suites intensifies among mid-market employers, influencing competitive positioning within the United States payroll services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & data-privacy concerns | -0.9% | National; heightened in regulated northeastern sectors | Short term (≤ 2 years) |

| High switching & implementation costs | -0.7% | National; most acute for enterprise deployments | Medium term (2-4 years) |

| Integration hurdles for fragmented SMB tech stacks | -0.8% | National, especially in legacy-system-dependent regions | Medium term (2–4 years) |

| Fintech-led embedded payroll cannibalizing standalone revenues | -1.0% | National, with early impact in startup and gig-economy hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-security & Data-Privacy Concerns

Payroll repositories store Social Security numbers and bank details, making them lucrative targets for cybercriminals. Average breach remediation costs reached USD 4.88 million in 2024, including fines, litigation, and customer notification. Regulated sectors such as healthcare and financial services apply rigorous due diligence checklists that lengthen vendor onboarding. Only 23% of surveyed payroll leaders currently deploy AI in core processes, citing security worries as the primary barrier. Providers counter with multifactor authentication, data-loss-prevention software, and continuous penetration testing, yet perception gaps persist. These concerns slow adoption and cap growth potential for certain buyer cohorts within the United States payroll services market.

High Switching & Implementation Costs

Migrating payroll platforms involves transferring historical records, re-establishing integrations, and running dual systems for validation cycles. Enterprises often allocate several months and sizable budgets to complete conversions, elevating the total cost of ownership during the transition window. Extended timelines fuel reluctance to switch providers even when superior functionality exists. Incumbent vendors leverage this dynamic to extend contracts and upsell modules, limiting churn. For mid-market firms with limited cash flow, migration outlays can postpone technology upgrades despite clear efficiency gains. The switching hurdle remains a structural restraint on competitive turnover in the United States payroll services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Company Size: Small Enterprises Drive Market Foundation

Small-sized companies accounted for 47.15% of the United States payroll services market share in 2025 and are projected to expand at a 10.95% CAGR through 2031. Capacity limitations encourage these firms to outsource as a cost-effective alternative to staffing an internal payroll desk. Earned-wage access, contractor payment modules, and automated multi-state tax updates make professional services indispensable. Mid-size employers follow with 33.95% share and 10.08% growth, reflecting their cross-border expansion and need for advanced analytics. Large enterprises, possessing dedicated HRIS teams, selectively outsource high-complexity functions yet still post an 7.82% CAGR courtesy of digital transformation mandates. Together, these dynamics sustain diversified demand across the United States payroll services market.

Second-stage adoption patterns see small firms purchase basic calculation services initially, then layer in benefits administration, time tracking, and analytic dashboards as headcount rises. Cloud architectures align variable fees to employee volume, easing budget forecasting and improving scalability. Automation also unlocks compliance confidence by regularly synchronizing with federal and state repositories for payroll tax changes. In states that enforce paid family leave levies, automatic rate updates protect small employers from inadvertent under-withholding. Such features amplify perceived value and deepen client-vendor relationships. Consequently, small-enterprise momentum remains a core growth pillar for the United States payroll services market.

By End User: Healthcare Complexity Drives Specialization

Healthcare organizations held a 21.05% slice of the United States payroll services market size in 2025, propelled by multi-layer wage rules and union accords that few in-house teams can manage. Shift differentials, on-call premiums, and statutory overtime multipliers require configurable rule engines. Outsourcing partners deliver templates that encode these nuances and keep pace with legislative change. Professional services firms occupy an 17.85% share as they seek granular project billing and client cost allocation. The IT vertical represents the fastest 10.49% CAGR thanks to stock-based compensation and fully remote workforces operating across tax regimes. Collectively, these verticals reinforce demand diversity.

Manufacturers rely on providers for prevailing wage compliance, union payroll, and complex overtime averaging, contributing a 10.90% share. Finance sector buyers require support for bonus accruals, deferred compensation, and stringent regulatory reporting across state lines, holding a 14.95% share. Retailers and hospitality chains use automated tip reporting, scheduling, and seasonal worker administration to control labor costs and maintain compliance in high-turnover environments. As each vertical confronts distinct legislation, specialized rule libraries and domain expertise emerge as differentiators. Vendors that embed tailored templates can capture incremental share within the United States payroll services market.

Geography Analysis

The South controlled a 34.98% stake in the United States payroll services market in 2025, buoyed by corporate relocations to states like Texas and Florida that boast favorable tax codes. Outsourcing gains momentum as employers juggle local payroll taxes, municipal reporting, and expanding multi-location footprints. Projected growth of 8.05% through 2031 aligns with population inflows, manufacturing expansion, and steady service-sector hiring. Parallel adoption of earned wage access tools addresses liquidity needs among large hourly workforces. Compliance with new overtime thresholds poses additional challenges for Southern manufacturers, further catalyzing outsourcing. The South thus remains a pivotal revenue engine for providers seeking scale.

The West is forecast to deliver an 8.12% CAGR, the highest among regions, driven by technology clusters grappling with California’s intricate labor statutes and stock-compensation rules. Employers demand platforms that accommodate remote workers scattered across multiple states and time zones. Complexities surrounding contractor classification under Assembly Bill 5 push gig-economy startups toward managed payroll solutions. Stock-option taxation and equity vesting schedules heighten configuration requirements, amplifying the need for specialist expertise. Embedded payroll capabilities integrated into fintech dashboards gain traction among early-stage firms seeking rapid deployment. Combined, these forces make the West a leading growth theater within the United States payroll services market.

The Northeast accounted for a significant portion of the market in 2024 and is expected to grow steadily through 2030, maintaining one of the fastest paces of expansion among all regions. Financial services headquarters generate complicated bonus pools, deferred-compensation plans, and stringent regulatory reporting, all fertile ground for premium solutions. Healthcare institutions add further demand owing to union obligations and variable shift differentials. Meanwhile, the Midwest’s share benefits from manufacturing revival and agricultural entities adopting digital wage tools for seasonal labor cycles. Multi-state payroll within interstate transport corridors complicates compliance and elevates outsourcing appeal. Uniformly, regional legislative divergence ensures a continuous opportunity for providers possessing geographic specialization.

Competitive Landscape

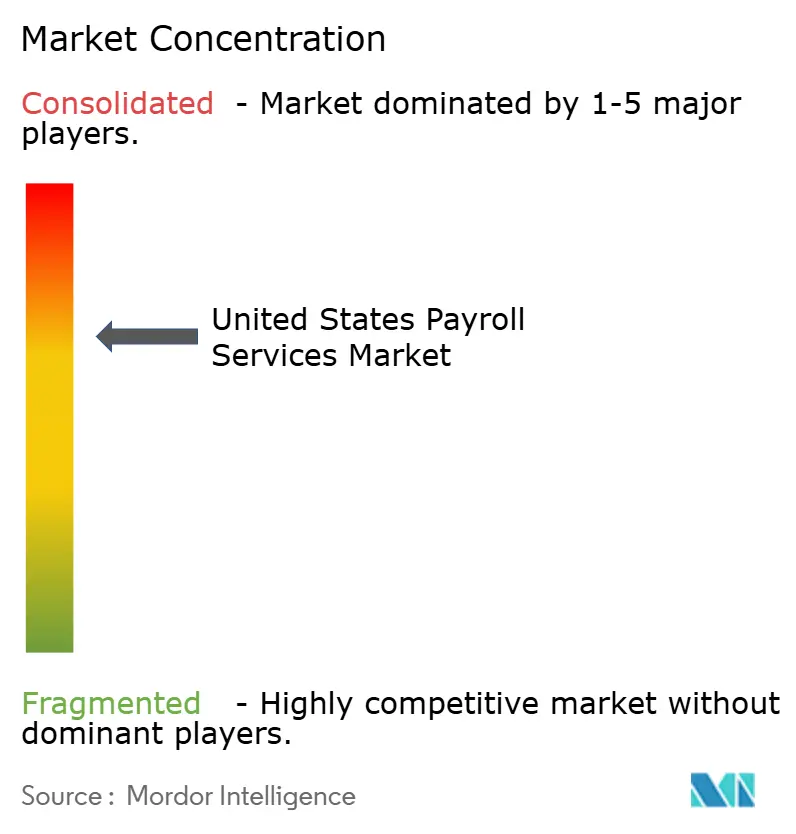

The United States payroll services market shows moderate concentration, with the top five vendors controlling a substantial portion of total revenue in 2025. ADP leads the market, driven by its comprehensive HCM integration suite, extensive compliance resources, and its AI-powered Assist platform, which identifies anomalies across a vast client base of over one million businesses. Paychex accelerated to 12% after closing its USD 4.1 billion acquisition of Paycor in April 2025, bolstering mid-market reach and AI analytics capability. Paylocity commands 9% through cloud-native architectures that attract tech-savvy SMBs, and Paycom follows at 8% owing to its single-database model that fuses HR and payroll modules. Beyond these leaders, niche vendors target healthcare or construction verticals with specialized rule sets.

Technology differentiation centers on AI-driven fraud detection, predictive gross-to-net simulations, and real-time compliance alerts. Vendors partner with fintech platforms to embed white-label payroll into broader financial ecosystems, widening exposure but squeezing standalone margins. Consolidation continues as investors favor scalable cloud assets; Vensure Employer Solutions completed its 75th acquisition by buying Execupay in October 2024, adding 800,000 worksite employees and expanding PEO capacity. Meanwhile, PrismHR’s January 2025 merger with Vensure elevates its technology stack and national footprint. Market entrants emphasize API-first design to capitalize on the embedded payroll wave reshaping distribution within the United States payroll services market.

Incumbents also pour resources into cybersecurity, adopting zero-trust frameworks and achieving ISO 27001 certifications to reassure regulated clients. Provider roadmaps integrate earned wage access, on-demand paycards, and vernacular mobile apps that improve employee experience. Re-bundling of scheduling, benefits, learning, and analytics within payroll stacks supports higher revenue per client. Nevertheless, switching costs remain sizeable, anchoring customer churn near historic lows. Specialty vendors can still thrive by attacking vertical or regional niches neglected by generalist giants. This competitive equilibrium underpins sustainable, albeit contested, growth for the United States payroll services market.

United States Payroll Services Industry Leaders

ADP

Paychex

Paylocity

Paycom

Intuit QuickBooks Payroll

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Paychex completed its USD 4.1 billion acquisition of Paycor, expanding AI-driven HR capabilities and mid-market reach. The transaction consolidates two significant players and creates enhanced competitive positioning against enterprise-focused rivals through combined technology platforms and customer bases.

- January 2025: Vensure Employer Solutions merged with PrismHR, marking the company's 75th acquisition as part of its aggressive roll-up strategy in the payroll and HR services sector. The merger strengthens Vensure's technology platform and expands its Professional Employer Organization capabilities.

- October 2024: Vensure completed its acquisition of Execupay, adding 800,000 worksite employees to its platform and demonstrating continued consolidation in the mid-market payroll services segment. The acquisition enhances Vensure's scale and geographic coverage across multiple markets.

- July 2024: Vensure completed its acquisition of Execupay, adding 800,000 worksite employees to its platform and demonstrating continued consolidation in the mid-market payroll services segment. The acquisition enhances Vensure's scale and geographic coverage across multiple markets.

United States Payroll Services Market Report Scope

The payroll services market refers to the industry segment comprising companies that offer outsourced payroll processing and related services to businesses. These services typically include calculating employee wages, withholding taxes, issuing paychecks or direct deposits, and ensuring compliance with regulatory requirements. Payroll service providers offer businesses scalable solutions to streamline payroll administration, improve accuracy, and mitigate legal and regulatory risks.

The US payroll services market is segmented by company and end user. By company, the market is segmented into small-size companies, mid-size companies, and large enterprises. By end user, the market is segmented into healthcare, manufacturing, retail, hospitality, IT, finance, and professional services. The report offers the market sizes and forecasts in terms of value (USD) for all the above segments.

| Small-Size Companies |

| Mid-Size Companies |

| Large Enterprises |

| Healthcare |

| Manufacturing |

| Retail |

| Hospitality |

| IT |

| Finance |

| Professional Services |

| Northeast |

| Midwest |

| South |

| West |

| By Company Size | Small-Size Companies |

| Mid-Size Companies | |

| Large Enterprises | |

| By End User | Healthcare |

| Manufacturing | |

| Retail | |

| Hospitality | |

| IT | |

| Finance | |

| Professional Services | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How large is the United States payroll services market in 2026?

It is valued at USD 8.91 billion and is forecast to reach USD 11.61 billion by 2031, implying a 5.47% CAGR over 2026-2031.

Why are small businesses outsourcing payroll in greater numbers?

Rising regulatory complexity and limited in-house expertise drive SMBs to external providers that assure accuracy, reduce risk, and free owners to focus on core operations.

What regional segment is growing fastest for payroll services?

The West is projected to grow at 8.12% CAGR through 2031, powered by technology sector expansion and complex California labor laws.

What impact do new overtime rules have on payroll vendors?

The July 2024 salary threshold hike increases employer compliance needs, prompting many to adopt outsourced solutions for accurate overtime calculations and reporting.

Page last updated on: