Operations Advisory Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

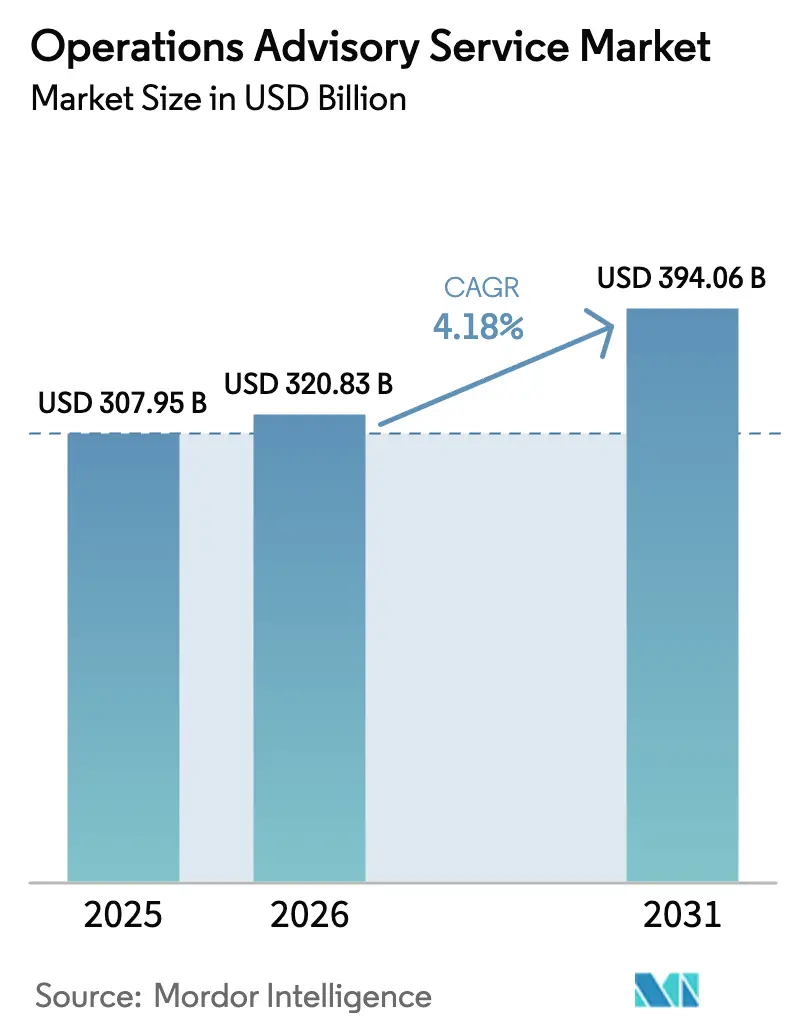

| Market Size (2026) | USD 320.83 Billion |

| Market Size (2031) | USD 394.06 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

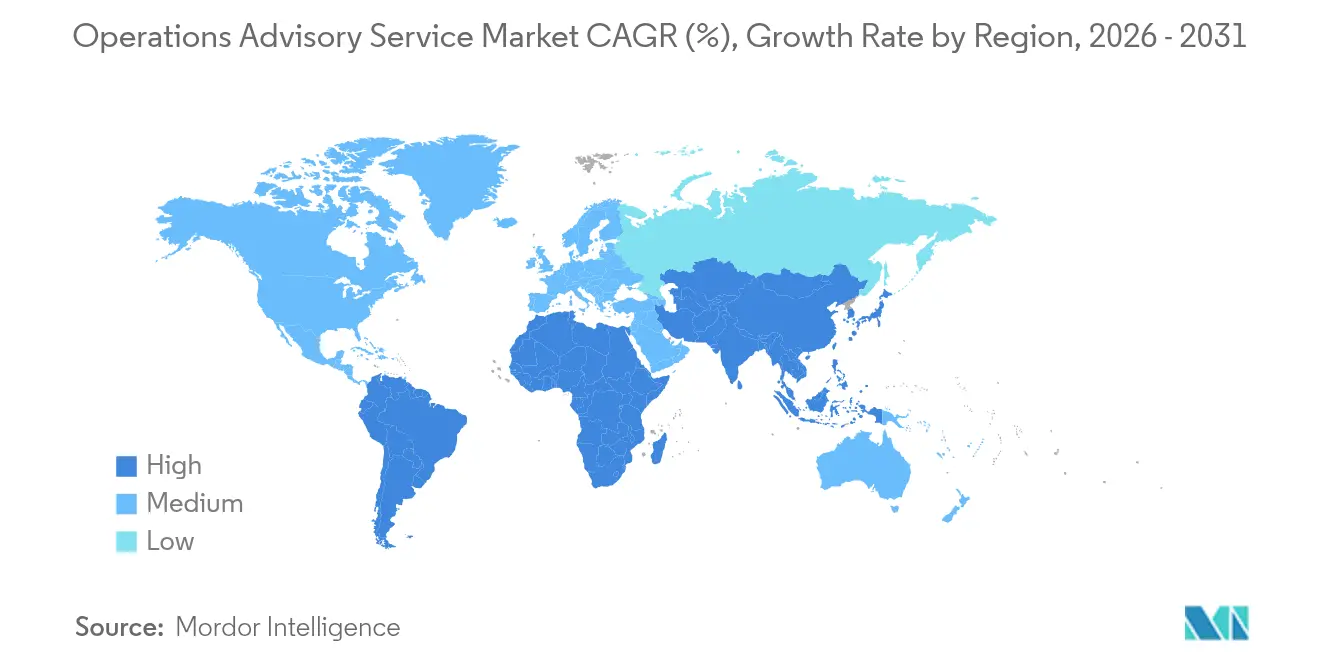

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Operations Advisory Service Market Analysis by Mordor Intelligence

The operations advisory service market size is expected to grow from USD 307.95 billion in 2025 to USD 320.83 billion in 2026 and is forecast to reach USD 394.06 billion by 2031 at 4.18% CAGR over 2026-2031. The operations advisory service market is evolving away from labour-arbitrage toward resilience and value creation, as enterprises recalibrate global networks in response to pandemic-era supply-chain shocks. Client mandates now blend cloud-native ERP migration, digital-twin modelling, and prescriptive AI analytics that collectively boost throughput while curbing discretionary spend. Large enterprises continue to dominate contract value, yet small and medium-sized enterprises (SMEs) are expanding engagement volumes as outcome-linked pricing trims up-front expense and clarifies payback timelines. Competitive differentiation in the operations advisory service market hinges on proprietary data platforms, verticalized accelerators, and multidisciplinary talent capable of translating analytics into board-level action.

Key Report Takeaways

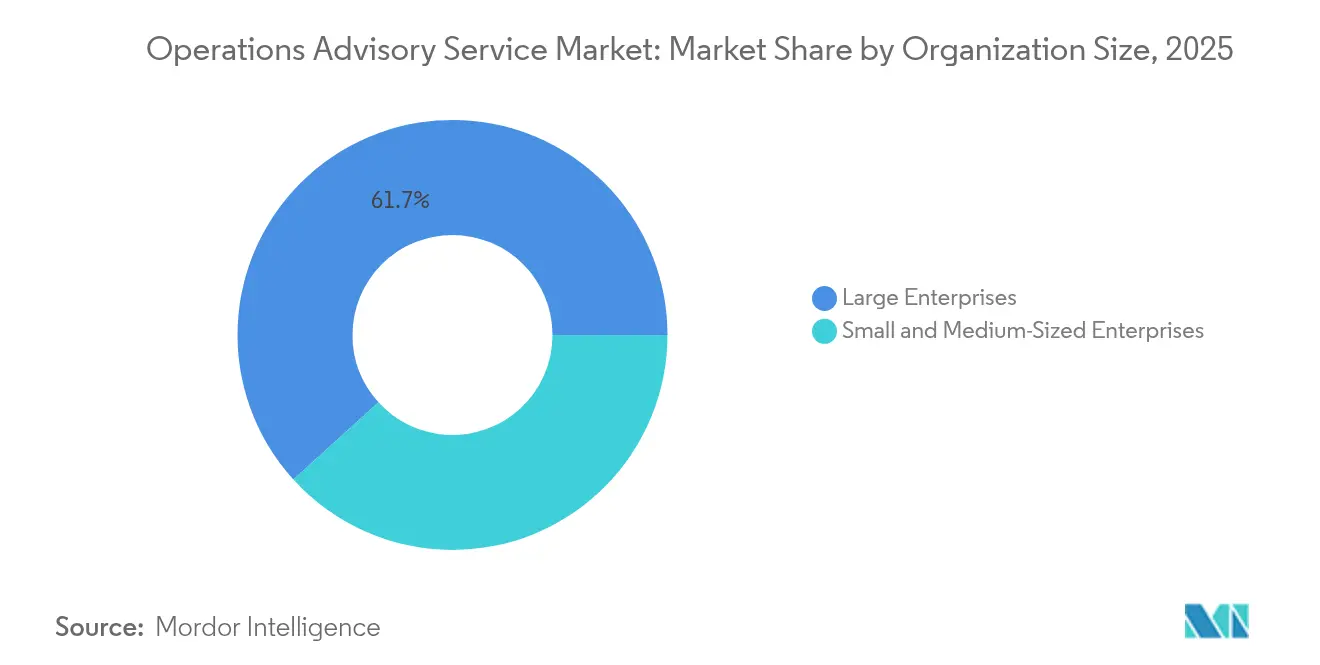

- By organization size, large enterprises held 61.74% of the operations advisory service market share in 2025. SMEs are expanding at a 14.05% CAGR to 2031, the fastest of any size segment within the operations advisory service market.

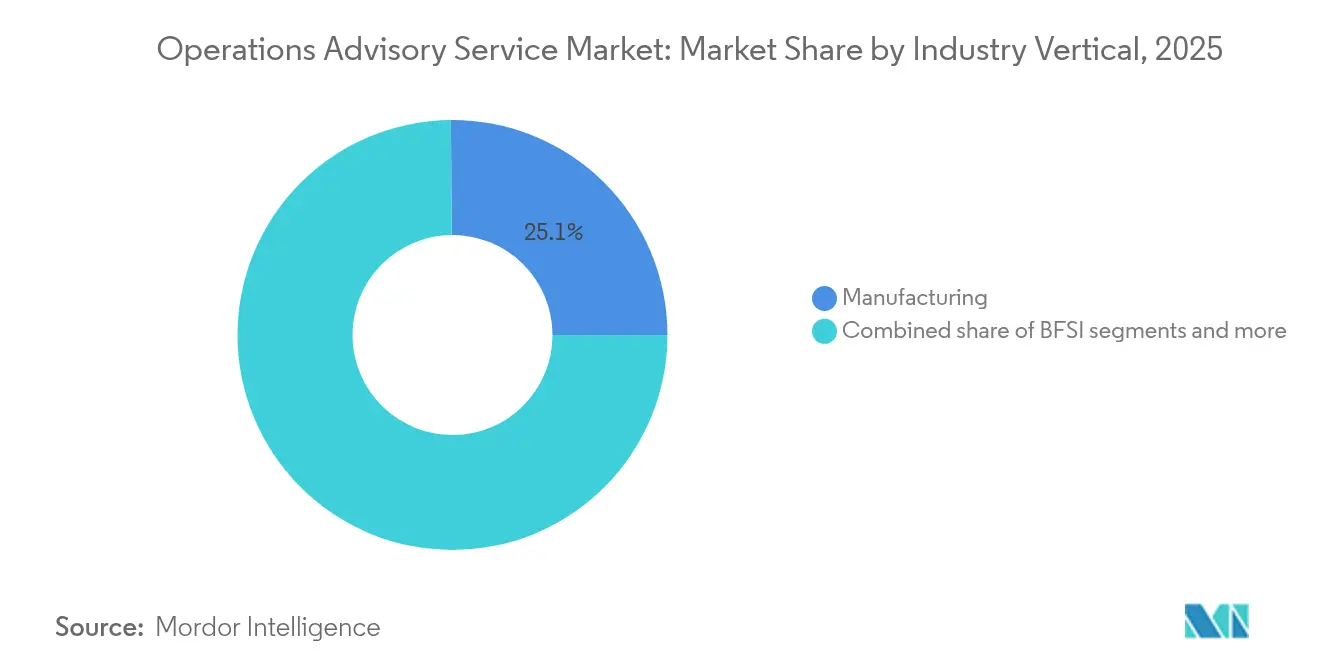

- By industry vertical, manufacturing contributed 25.12% revenue share in 2025, the highest in the operations advisory service market. Retail and e-commerce are forecast to post a 14.89% CAGR through 2031, emerging as the fastest-growing vertical in the operations advisory service market.

- By application, supply-chain consulting captured 29.76% of the operations advisory service market size in 2025. Digital process management is set to grow at a 15.42% CAGR over the same horizon, the steepest application-level trajectory in the operations advisory service market.

- By geography, North America led with 39.02% revenue share in 2025. Asia-Pacific is projected to accelerate at a 12.74% CAGR to 2031, the quickest regional pace in the operations advisory service market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Operations Advisory Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid post-pandemic supply-chain resilience investments | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing regulatory complexity across global operations | +0.8% | Global, particularly the EU, North America, and APAC financial centres | Long term (≥ 4 years) |

| Cloud-native ERP migration waves | +0.7% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Digital-twin adoption for process optimisation | +0.6% | Manufacturing hubs in Germany, the US, China, and Japan | Long term (≥ 4 years) |

| Outcome-based fee models are attractive to SMEs | +0.5% | Global, with early adoption in North America & Western Europe | Short term (≤ 2 years) |

| ESG-linked operational transparency mandates | +0.4% | EU leadership, spreading to North America & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Post-Pandemic Supply-Chain Resilience Investments

Manufacturers, retailers, and logistics providers that endured capacity bottlenecks during 2020–2021 now fund multi-sourcing, near-shoring, and buffer-stock strategies that embed risk metrics alongside cost and service level targets. Advisory projects routinely layer digital control-towers with prescriptive analytics, unlocking 10-15% throughput gains and 5-10% landed-cost reductions without additional asset spend [1]McKinsey & Company, “A More Resilient Supply Chain From Optimized Operations Planning,” mckinsey.com . A limited number of global enterprises have successfully institutionalized comprehensive end-to-end risk governance frameworks. These organizations have demonstrated the capability to sustain a multi-year pipeline by effectively integrating strategic modelling with tactical execution, ensuring alignment between long-term objectives and operational decision-making. North American and European corporations lead investment momentum, while tier-one Asian suppliers scale similar playbooks to remain preferred partners. The operations advisory service market, therefore, captures durable demand as companies convert emergency responses into systemic resilience programs.

Increasing Regulatory Complexity Across Global Operations

Cybersecurity disclosure rules, ESG reporting mandates, and shifting trade-sanctions regimes now intersect, forcing operations leaders to juggle compliance and productivity. The U.S. Securities and Exchange Commission’s 2024 cybersecurity rule raised governance thresholds for issuers and advisers[2]U.S. Securities & Exchange Commission, “Cybersecurity Risk Management and Incident Disclosure,” sec.gov . The European Union's Corporate Sustainability Reporting Directive has intensified data-collection requirements across supply chains, compelling organizations to reassess their environmental, social, and governance (ESG) strategies. As a result, many surveyed companies are increasing their ESG budgets to ensure compliance and enhance sustainability performance. Advisory engagements are shifting from checklist audits to integrated programs that treat regulatory readiness as a competitive edge rather than a sunk cost. This dynamic propels the operations advisory service market as clients navigate multilayer frameworks spanning data protection, carbon accounting, and human-rights diligence.

Cloud-Native ERP Migration Waves

Legacy on-premises suites cannot surface real-time data or integrate AI modules, pushing enterprises toward cloud-first platforms that embed analytics, IoT feeds, and sustainability ledgers. The share of companies budgeting more than USD 1 million for procurement AI is expected to double between 2024 and 2025, intensifying demand for partners who can synchronize ERP modernization with intelligent-automation roadmaps[3]SupplyChainBrain, “Procurement Staffing in 2025: Five Key Trends,” supplychainbrain.com. Advisory teams orchestrate data-cleansing sprints, process re-design, and change-management offices, typically under hybrid delivery models that combine near-shore architects and on-site agile squads. North America drives early adoption, but data-sovereignty clauses in Europe and Asia are catalyzing regional migrations, broadening addressable revenue for the operations advisory service market.

Digital-Twin Adoption for Process Optimisation

Digital twins create high-fidelity replicas of assets, lines, or entire plants, enabling simulation of parameter changes before physical intervention. Despite the current adoption rate being 21%, an overwhelming 97% of users have reported measurable value realization. These benefits include enhancements in operational efficiency, such as extended mean-time-between-failure intervals, as well as significant reductions in energy consumption[4]PricewaterhouseCoopers, “2025 Digital Trends in Operations Survey,” pwc.com . Advisory firms integrate engineering know-how with data-science stacks to calibrate sensors, build predictive models, and operationalize governance for version control and cyber-resilience. Germany, the United States, Japan, and coastal China remain early adopters, but accelerated industrial policy in Southeast Asia is widening the client base for digital-twin projects inside the operations advisory service market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of experienced operations consulting talent | -0.9% | Global, acute in North America & Western Europe | Medium term (2-4 years) |

| Data-security concerns in remote advisory delivery | -0.6% | Global, heightened in regulated industries | Short term (≤ 2 years) |

| Hyper-automation tools are cannibalising classic advisory | -0.5% | Advanced markets: North America, EU, Japan | Long term (≥ 4 years) |

| Pricing pressure from gig-talent & boutique firms | -0.4% | Global, most intense in mature consulting markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Experienced Operations-Consulting Talent

The availability of hybrid skill sets that integrate process re-engineering, data-science literacy, and sector-specific expertise remains limited, creating a significant talent gap. Professionals with over a decade of experience in lean practices, artificial intelligence, and regulatory frameworks are commanding higher compensation levels, thereby exerting increased margin pressures on established firms. According to Korn Ferry's internal data, senior advisory roles have experienced double-digit fee inflation, prompting firms to accelerate the development of academy programs and establish partnerships with universities to address the talent shortage. However, the time required to develop proficiency in these roles often spans up to 24 months, resulting in short-term capacity limitations. These constraints are impeding the growth potential of the operations advisory service market in the near term.

Hyper-Automation Tools Cannibalising Classic Advisory

Robotic process automation, low-code platforms, and AI-powered analytics now execute repeatable diagnostics previously staffed by junior consultants. KPMG notes that subscription software is displacing full-time advisory headcount in invoice processing, basic inventory analytics, and tolerance checking. Firms respond by pivoting to governance frameworks, complex system integration, and human-machine orchestration—higher-value offerings less susceptible to automation. Still, overall billable hours for low-complexity work are falling, moderating revenue growth potential within the operations advisory service market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Strategic Scale vs. Agile Growth

Large enterprises generated 61.74% of 2025 billings inside the operations advisory service market, reflecting their need for global coordination across ERP migrations, supply-chain redesigns, and integrated ESG dashboards. Typical engagements span 18–36 months, manage hundreds of stakeholder touchpoints, and fuse legacy infrastructure with AI micro-services. These clients also pilot autonomous agents that reconcile inter-company transactions nightly, delivering real-time visibility to CFOs. Historical data show that during macro shocks, large enterprises sustain advisory spend to mitigate risk, stabilizing baseline revenue for the operations advisory service market.

SMEs post the fastest trajectory at 14.05% CAGR to 2031, enabled by cloud collaboration tools, standardized playbooks, and outcome-based pricing. Their shorter decision cycles—often champion-led rather than committee-driven—accelerate contract signatures and change adoption. SMEs also leverage advisory know-how to secure certifications or regulatory clearances needed for cross-border trade. Providers that package diagnostics into subscription portals capture disproportionate SME wallet share inside the operations advisory service market.

By Industry Vertical: Manufacturing’s Commanding Lead and Retail’s Agile Upswing

Manufacturing captured 25.12% of 2025 revenues as factories modernize with Industry 4.0 technologies, predictive maintenance, and energy-optimization algorithms. Engagements frequently integrate value-stream mapping, sensor retrofits, and model-predictive control, driving rapid payback and multi-site rollouts. The vertical also pioneers ESG reporting within production workflows, elevating demand for advisory capabilities that marry operational efficiency with carbon intensity reduction.

Retail and e-commerce, forecast at a 14.89% CAGR, accelerate due to omnichannel fulfillment, last-mile orchestration, and real-time inventory visibility. Consultants design dark stores, micro-fulfillment hubs, and AI-driven demand forecasts that harmonize online and brick-and-mortar operations. Beyond these two poles, BFSI sustains spend on operational risk frameworks and cyber-resilience, while public-sector agencies seek digital permitting and citizen-service redesign. Each vertical’s unique compliance and demand patterns create rich specialization niches within the operations advisory service market.

By Application: Supply-Chain Dominance and Process-Management Momentum

Supply-chain advisory commanded 29.76% of 2025 revenue, as C-suites prioritized visibility, dual sourcing, and geopolitically informed network design. Consultants increasingly operate concurrent-planning engines that feed scenario results directly into executive S&OP meetings, linking strategy to execution. Engagements also embed sustainability metrics—such as scope 3 emissions—into supplier scorecards, reinforcing compliance.

Digital process management will expand at 15.42% CAGR through 2031, transforming RPA pilots into enterprise-scale orchestration layers. Advisory teams deploy process-mining diagnostics, co-create citizen-developer centers, and craft governance models that ensure continuous improvement. Financial operations, human-resource optimization, and manufacturing operations round out application demand, each requiring tailored methodologies but sharing an analytics-first mindset characteristic of the operations advisory service market.

Geography Analysis

North America produced 39.02% of 2025 revenue across the operations advisory service market, underpinned by stringent regulatory regimes and leading adoption of AI-enabled operational modernization. Fortune 500 corporations accelerate generative-AI pilots for planning, risk scoring, and customer-service triage. Canada and Mexico contribute regional lift via supply-chain sovereignty investments and USMCA-driven compliance programs. Mature procurement functions and outcome-based contracting norms push advisers to deliver quantified value on every engagement, reinforcing competitive rigor within the operations advisory service market.

Asia-Pacific is projected to log a 12.74% CAGR to 2031, reflecting China’s industrial-upgrade agenda, India’s digital public-infrastructure builds, and Southeast Asia’s manufacturing corridor expansions. Japanese automotive groups run digital-twin factories, and South Korean electronics conglomerates deploy autonomous production planners. Variability in regulatory maturity and local languages necessitates in-country alliances and culturally attuned change leadership, expanding partner ecosystems inside the operations advisory service market.

Europe maintains a robust share, anchored by Germany’s Industry 4.0 initiatives and the EU’s sustainability legislation. Advisory demand spans circular-economy roadmaps, carbon-neutral supply networks, and post-Brexit customs optimization in the United Kingdom. France and Italy focus on aerospace and luxury-goods modernization, while Nordic countries invest in renewable-energy operations and green-hydrogen value chains. Strict data-protection statutes encourage near-shore delivery hubs in Poland and Portugal, adding complexity yet boosting specialized employment throughout the operations advisory service market.

Competitive Landscape

The operations advisory service market demonstrates moderate concentration, with top-tier providers capturing a substantial portion of 2024 revenues, yet leaving opportunities for specialized firms to carve out niches. Deloitte continues to lead the market, reporting USD 37.5 billion in consulting receipts by combining deep sector expertise with strategic technology alliances. Capgemini is set to acquire WNS for USD 3.3 billion, expanding its agentic-AI talent pool and business process services infrastructure. Cognizant recorded USD 27.8 billion in trailing-12-month bookings while introducing Agent Foundry, an autonomous-agent platform operationalizing AI across finance, supply chain, and customer support functions. This demonstrates how leading firms integrate advanced technology solutions to enhance operational efficiency and advisory capabilities globally.

Marsh McLennan has broadened its risk-advisory offerings through the USD 7.75 billion acquisition of McGriff, reflecting growing convergence between insurance consulting and operational resilience services. Boutique and specialist disruptors are leveraging cloud-based analytics, micro-specialization, and innovative service models to compete effectively with incumbents. These smaller players frequently target high-value niches, such as pharmaceutical quality systems or renewable-asset maintenance, providing deep expertise at competitive pricing. Cloud adoption and industry-specific digital tools enable these firms to deliver scalable solutions without replicating full-service consulting breadth. As a result, market dynamics increasingly favor both large integrated firms and agile niche providers coexisting within the operations advisory space.

Talent scarcity continues to present a systemic challenge across the operations advisory service market, driving firms to escalate investments in internal academies and AI-driven augmentation programs. These initiatives aim to increase consultant productivity, offset rising wage inflation, and maintain delivery quality across complex client engagements. While these strategies reinforce barriers to entry for new competitors, they also limit rapid scaling opportunities even for established players. The combined effect of talent constraints, technological investment, and client expectations is shaping a competitive landscape focused on specialized expertise, operational excellence, and digital transformation. Overall, the market is evolving into a hybrid environment where technology, skill, and strategic acquisitions define success.

Operations Advisory Service Industry Leaders

Accenture

Deloitte

PwC

Ernst & Young

KPMG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Capgemini agreed to acquire WNS for USD 3.3 billion, expanding its intelligent operations reach and agentic AI capabilities.

- July 2025: Cognizant posted USD 27.8 billion trailing-12-month bookings and debuted Agent Foundry, which orchestrates autonomous agents across finance, supply chain, and customer experience.

- March 2025: Kearney’s annual COO survey showed 97% of companies investing in generative AI, up from 32% in 2024, underscoring rapid technology adoption across the operations advisory service market.

- September 2024: Marsh McLennan completed the USD 7.75 billion McGriff acquisition to broaden combined risk and operations advisory offerings.

Global Operations Advisory Service Market Report Scope

Operations consulting, or operations management, is advisory and implementation services that improve a company's internal operations and performance in the value chain.

Operations Advisory Service Market is segmented by organization size (large enterprises and small & medium-sized enterprises), industry vertical (BFSI, IT and Telecom, manufacturing, retail, and e-Commerce, public sector, healthcare, and others), application (supply chain, financial operations, human resource operations, project management, process management, manufacturing operations, and others), and region (North America, South America, Asia-Pacific, Europe, and Middle East & Africa). The report offers market size and forecasts for the Operations Advisory Service Market in value (USD) for all the above segments.

| Large Enterprises |

| Small & Medium-Sized Enterprises |

| BFSI |

| IT and Telecom |

| Manufacturing |

| Retail and E-Commerce |

| Public Sector |

| Healthcare |

| Others |

| Supply Chain |

| Financial Operations |

| Human Resource Operations |

| Project Management |

| Process Management |

| Manufacturing Operations |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Organization Size | Large Enterprises | |

| Small & Medium-Sized Enterprises | ||

| By Industry Vertical | BFSI | |

| IT and Telecom | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Public Sector | ||

| Healthcare | ||

| Others | ||

| By Application | Supply Chain | |

| Financial Operations | ||

| Human Resource Operations | ||

| Project Management | ||

| Process Management | ||

| Manufacturing Operations | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the operations advisory service market in 2026 and what is its expected value by 2031?

It stands at USD 320.83 billion in 2026 and is projected to reach USD 394.06 billion by 2031, reflecting a 4.18% CAGR over 2026-2031.

Which geographic region accounts for the greatest share of spending on operations advisory services?

North America leads with 39.02% of global revenue in 2025, driven by complex regulatory regimes and rapid adoption of AI-enabled transformation programs.

Which application area is generating the strongest demand for advisory support?

Supply-chain engagements dominate at 29.76% of 2025 revenue as companies invest in resilience, dual-sourcing strategies, and end-to-end visibility platforms.

Why are small and medium-sized enterprises (SMEs) accelerating their use of advisory services?

Outcome-based fee models tie consultant compensation to measurable results, lowering up-front costs for SMEs and making high-quality expertise more accessible.

How are AI tools such as digital twins reshaping operations consulting projects?

With the help of AI copilots, process-mining, and digital-twin simulations, companies can achieve predictive optimization, leading to enhanced uptime and energy savings—all without the need for new capital investments.

What factors could restrain growth in the sector over the next five years?

Skill-set shortages, data-security concerns in remote delivery, automation-driven fee compression, and pricing pressure from gig-economy consultants may moderate expansion.

Page last updated on: