India Accounting Professional Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

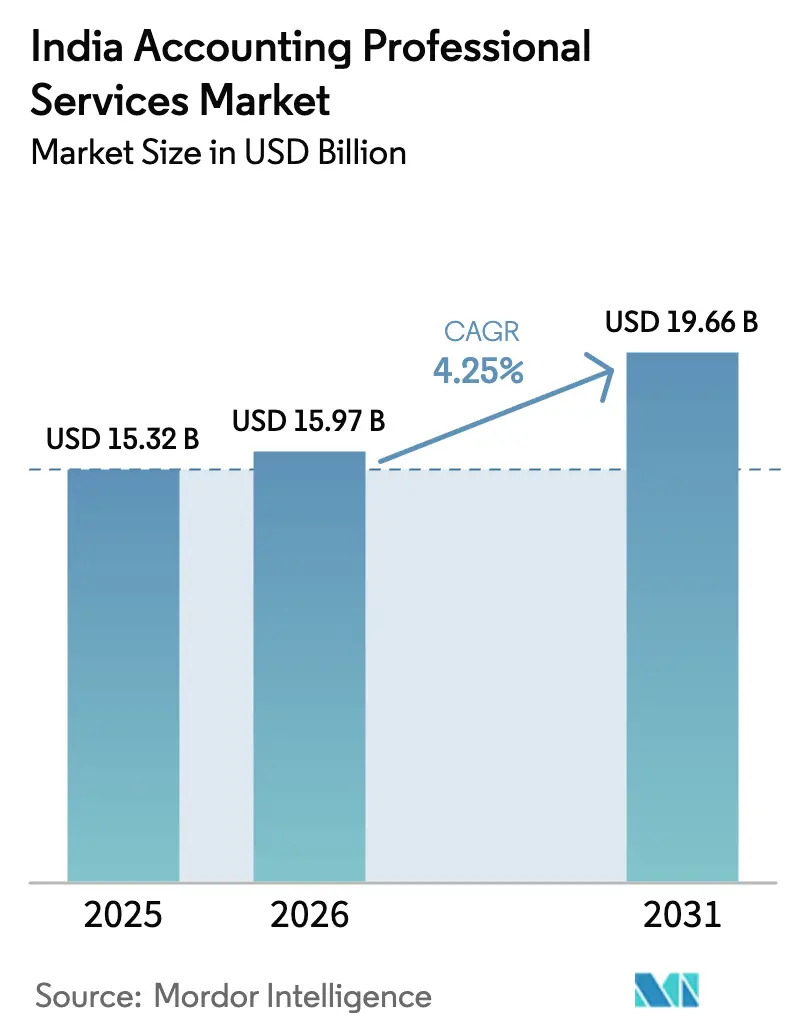

| Base Year Market Size (2025) | USD 15.32 Billion |

| Market Size (2026) | USD 15.97 Billion |

| Market Size (2031) | USD 19.66 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

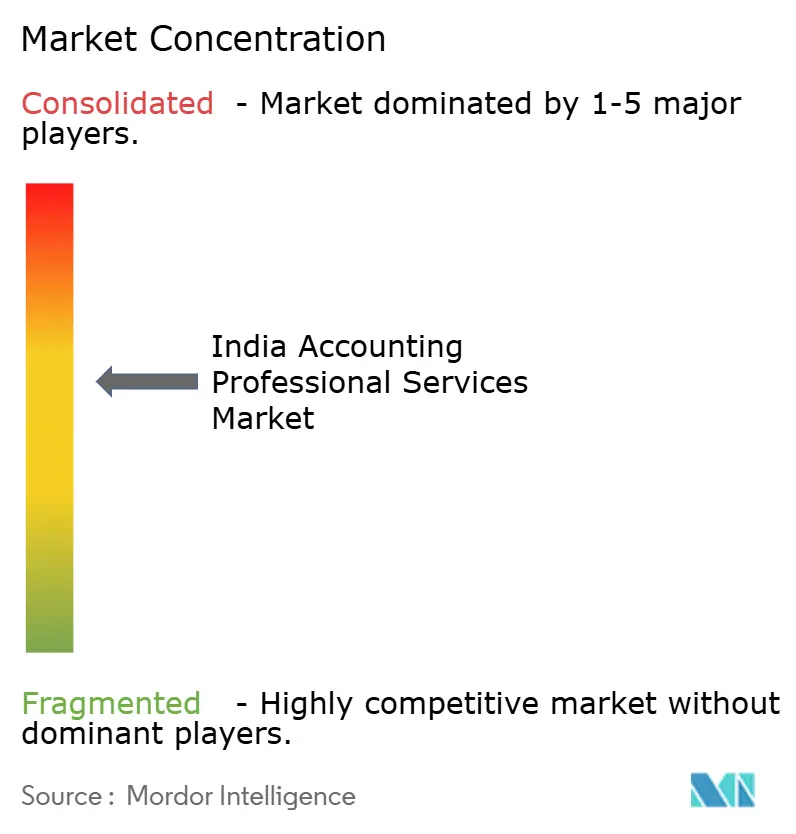

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Accounting Professional Services Market Analysis by Mordor Intelligence

India accounting professional services market size in 2026 is estimated at USD 15.97 billion, growing from 2025 value of USD 15.32 billion with 2031 projections showing USD 19.66 billion, growing at 4.25% CAGR over 2026-2031. Robust digital-first mandates, expanded enforcement by the National Financial Reporting Authority (NFRA), and the Reserve Bank of India’s (RBI) stricter fraud-risk directives are steering demand away from routine compliance toward technology-enabled, insight-led engagements. The government plans to amend the Companies Act and Limited Liability Partnership Act to let domestic firms merge, thereby creating indigenous “Big Four” equivalents, adding a strategic layer to competition, with international players generating USD 5.42 billion in FY25 revenue. Big international firms remain influential, yet their dominance is tempered by mandatory auditor rotation that will force 242 listed companies to appoint new firms in 2025-26. Tier-2 cities capture fast-rising Global Capability Centre (GCC) footprints, enabling firms to blend metro-grade expertise with regional cost advantages. Healthcare and life-sciences engagements outpace the broader market as the sector grapples with expanded compliance for clinical data and supply-chain transparency.

Key Report Takeaways

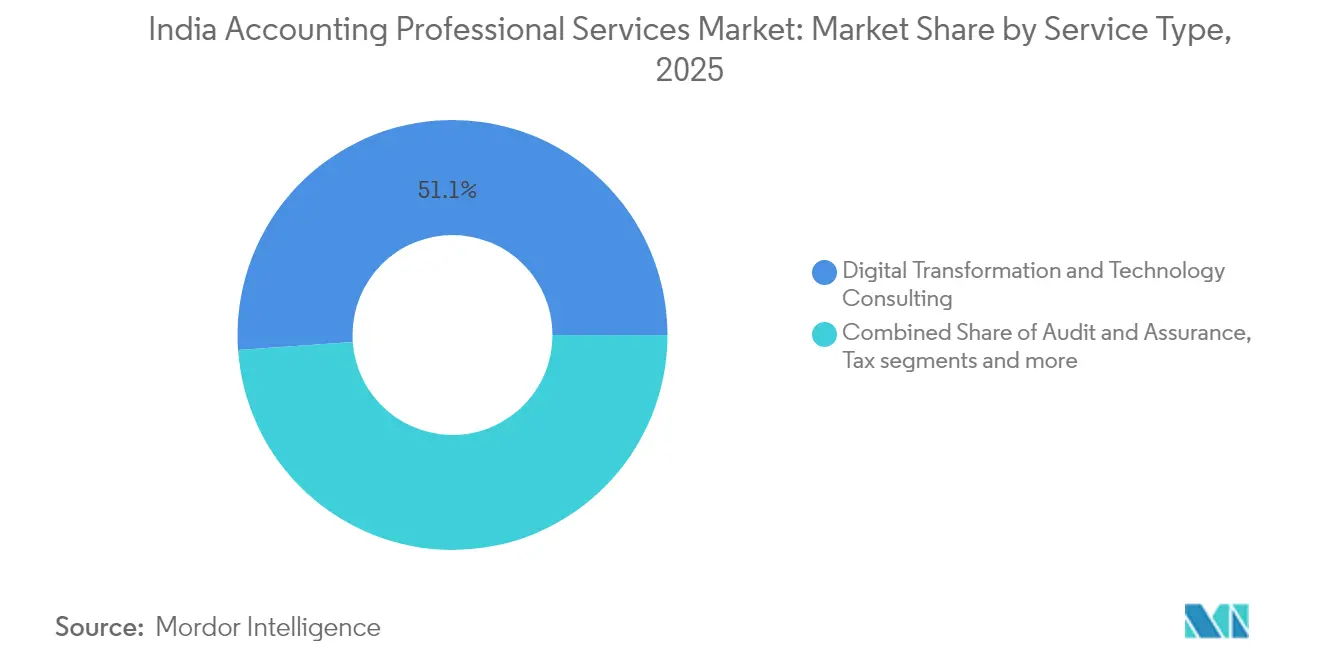

- By service type, digital transformation & technology consulting led with 51.12% revenue share in 2025; the segment is projected to log the fastest 8.25% CAGR through 2031.

- By client size, large enterprises held 46.05% of the India accounting professional services market share in 2025, while start-ups & early-stage firms are set to expand at a 6.98% CAGR to 2031.

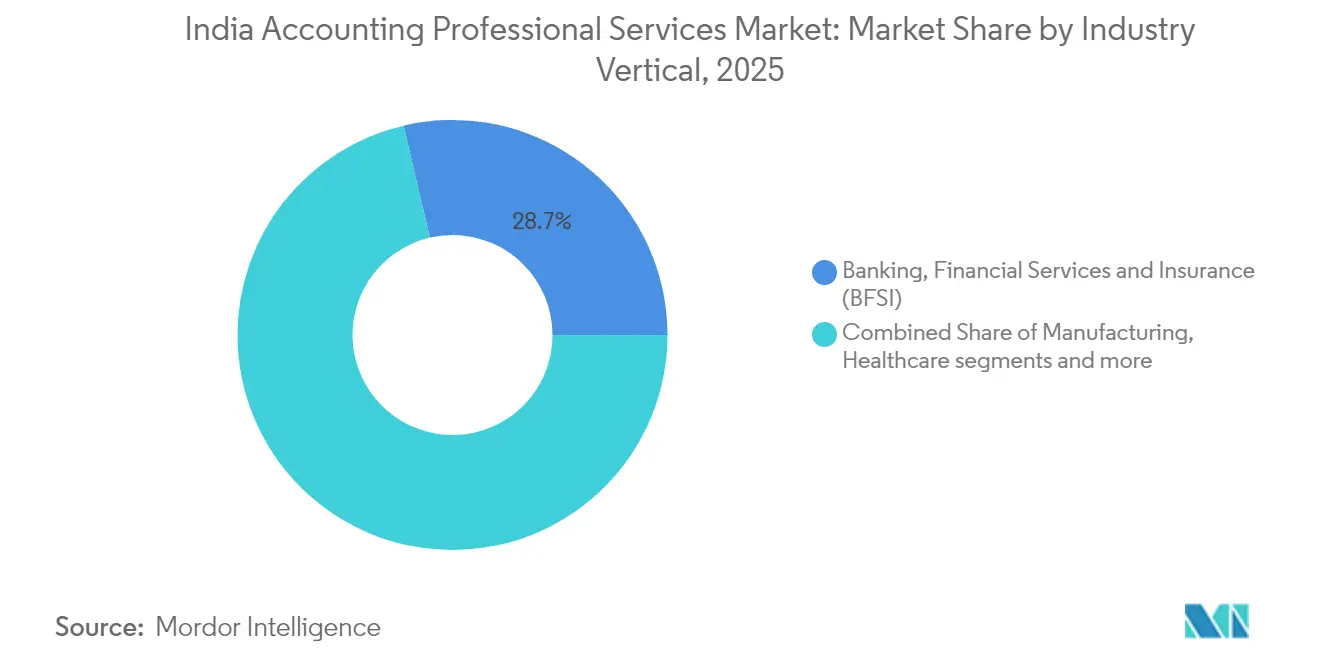

- By industry vertical, banking, financial services & insurance accounted for 28.65% revenue in 2025; healthcare & life sciences is on track for a 6.12% CAGR through 2031.

- By regional tier, Tier-1 cities commanded 42.62% of the market in 2025, whereas Tier-2 cities are poised for a 7.52% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Accounting Professional Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of digital transformation & technology consulting spend | +1.8% | National; strongest in Tier-1 metros | Medium term (2-4 years) |

| Rising regulatory compliance complexity | +1.2% | BFSI hubs nationwide | Short term (≤ 2 years) |

| Growth of Global Capability Centres & shared service hubs | +0.9% | Tier-1 expanding to Tier-2 | Long term (≥ 4 years) |

| Mandatory auditor rotation raising demand for independent assurance | +0.7% | Listed-company cluster | Short term (≤ 2 years) |

| Government push for indigenous Big-Four champions | +0.5% | National | Long term (≥ 4 years) |

| Adoption of AI-driven continuous audit & compliance platforms | +0.4% | Initial Tier-1 pilot sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Digital Transformation & Technology Consulting Spend

Enterprises are moving core finance processes onto cloud-native and analytics-rich platforms to align with RBI’s real-time fraud-monitoring norms and GST e-invoicing extensions to smaller taxpayers. Big accounting networks earned USD 2.41 billion from technology consulting in FY24 and have doubled STEM talent ratios since 2023, reflecting a pivot toward cybersecurity, AI model-risk, and cloud-cost governance advisory. The Union Budget 2025’s simplified direct-tax code and presumptive regime for electronics manufacturing bolster demand for automated compliance engines. Mid-tier firms are following suit by forming platform alliances with enterprise software vendors, an approach that compresses delivery cycles and enhances audit-trail transparency. As firms embed continuous-control monitoring and predictive analytics, the India accounting professional services market demonstrates higher average billing rates for tech-infused assignments. Corporate boards increasingly treat technology competence as a prerequisite when selecting statutory auditors, funneling more engagements into digital-first service lines.

Rising Regulatory Compliance Complexity

GST-Returns 2.0, new e-invoicing thresholds, and NFRA’s expanded inspection docket created a multi-layer compliance web. In 2024, NFRA levied USD 0.19 million in penalties on audit firms for quality lapses, underscoring the cost of non-compliance. RBI circulars now oblige banks to adopt AI-enabled fraud analytics and furnish granular incident reporting within 24 hours, elevating demand for forensic accounting and process audits[1]Grant Thornton Bharat, “RBI Fraud-Risk Mandate Deep-Dive,” grantthornton.in . SEBI’s Business Responsibility and Sustainability Reporting (BRSR) mandate adds ESG disclosures to annual accounts, compelling listed firms to enlist cross-disciplinary advisory help. SME promoters cite process complexity as a top challenge, prompting the outsourcing of indirect-tax reconciliations. Heightened penalties have increased the perceived cost of non-compliance, driving steady deal flow into assurance and risk advisory corridors.

Growth of Global Capability Centers & Shared Service Hubs

India’s 1,580 GCCs produced USD 46 billion in exports in FY 2023, a figure expected to climb to USD 110 billion by 2030[2]NASSCOM, “India GCC Trends 2024,” nasscom.in. Twenty-four centers exceeded USD 1 billion revenue for the first time in FY 2024, signaling strategic maturity. GCC finance chiefs seek partners that can design internal control frameworks compliant with both Indian and home-country regulations. Accounting firms respond by packaging “capability-center-as-a-service,” bundling entity setup, transfer-pricing policies, and shared-services automation. Cost arbitrage in Tier-2 locations such as Pune and Ahmedabad, combined with improving infrastructure, has shifted 15% of new GCC mandates outside the traditional metros. These developments position the India accounting professional services market for structurally higher technology-driven outsourcing revenue.

Mandatory Auditor Rotation Increasing Demand for Independent Assurance

Auditor-tenure caps will trigger the biggest reshuffle since 2018, with 242 listed entities obligated to appoint fresh auditors in FY 2025-26. Joint-audit arrangements rose to 157 in FY 2024-25, as companies pursue continuity while complying with rotation rules. NFRA inspection reports reveal deficiencies in related-party transaction testing, encouraging boards to evaluate firms based on control-testing depth. Mid-tier networks stand to gain as firms diversify beyond the Big Four audit pool. Premium pricing has already improved for multi-location group audits, especially those requiring International Standard on Auditing 600 consolidation work. The net effect is a visible pipeline of high-value, multi-year assurance contracts fueling the India accounting professional services market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of skilled accounting professionals & high attrition | -0.8% | Nationwide, severe in Tier-1 | Short term (≤ 2 years) |

| SME shift toward DIY SaaS accounting platforms | -0.6% | Tier-2/3 business belts | Medium term (2-4 years) |

| Prospective caps on audit-firm market share to curb concentration | -0.4% | National, affecting Big Four primarily | Medium term (2-4 years) |

| Intensifying regulatory scrutiny & penalties on audit quality | -0.5% | National, focused on listed companies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Skilled Accounting Professionals & High Attrition

India needs about 130,000 new Chartered Accountants annually to meet domestic demand and offshore work, but the current pipeline remains well below that threshold[3]International Federation of Accountants, “Talent Pipeline Report 2025,” ifac.org . U.S. firms have increased offshore hiring; one global network plans to more than double its India workforce by 2027. Wage inflation for qualified seniors averages 12% in metros, pushing domestic mid-tier firms into aggressive campus-recruiting and early-promotion programs. ICAI shortened the articleship period from three to two years in 2024 to entice students, yet retention issues persist post-qualification. Volume churn erodes institutional memory, lengthens engagement cycles, and raises onboarding costs, dampening near-term profitability across the India accounting professional services industry.

SME Shift Toward DIY SaaS Accounting Platforms

Digitally confident MSMEs now gravitate to low-cost cloud packages that handle bookkeeping, invoicing, and GST returns. Tally Solutions’ award-winning MSME program combines discounted licenses with expedited bank integrations, intensifying price competition; cloud packages start under USD 12 per month. Zoho Books and QuickBooks offer tiered subscriptions that enable micro-enterprises to bypass external accountants for routine filings. While complex statutory audits still require professional sign-off, the base volume of transactional compliance for small entities declines. Professional firms are repositioning as strategic advisors—focusing on internal-control reviews, valuations, and risk assessments that software alone cannot deliver. The challenge is managing capacity utilization amid a shrinking pool of low-complexity assignments in the India accounting professional services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology Consulting Commands Growth Momentum

Digital transformation & technology consulting contributed 51.12% of the India accounting professional services market and setting the tone for advisory-led growth. The segment’s 8.25% forecast CAGR will widen the gap with traditional audit streams as enterprises bundle ERP cloud migration, AI audit model validation, and cyber-risk analytics into multi-year statements of work. Audit & assurance retains defensive relevance because mandatory rotation reinforces demand for fresh perspectives, yet fee pressure persists without complementary tech capability. Tax & regulatory engagements escalate around GST 2.0 reconciliation and the new direct-tax code, while risk advisory capitalizes on ESG and supply-chain reporting mandates. Business services & outsourcing benefits from India’s expanding GCC base, which assigns controllership, accounts payable, and treasury support to external shared-service specialists.

Fee structures are changing: high-end technology consulting now operates on outcome-linked retainers, whereas statutory audits follow volume-based ceilings set by regulators. Firms that successfully cross-sell consulting into audit clients see utilization gains and margin uplift. Together, these shifts confirm that the India accounting professional services market is entering a hybrid era where compliance anchors coexist with analytics-rich, platform-centric growth.

By Client Size: Enterprise Sophistication Sustains Premium Pricing

Large enterprises generated 46.05% of 2025 billings as they integrate multi-jurisdiction controls and IFRS-to-Ind-AS mappings. However, start-ups & early-stage firms, propelled by USD 2.8 billion in Q1-2025 IPO proceeds, are projected to expand fastest at 6.98% CAGR, demanding CFO-as-a-service models and IPO readiness reviews. Mid-market entities leverage budget-friendly shared-service bundles, while government & public sector undertakings procure transparency audits aligned with the Public Financial Management System. MSMEs sit at a strategic crossroads: do-it-yourself platforms fulfil basic tax tasks, yet rising regulatory complexity nudges them toward periodic professional intervention.

Talent scarcity influences client-mix economics: senior-partner hours continue to bias toward marquee accounts, compressing capacity for smaller engagements unless profitable automation offsets labor. Success, therefore, hinges on balanced portfolio management within the India accounting professional services industry and disciplined resource allocation across client tiers.

By Industry Vertical: BFSI Retains Lead, Healthcare Accelerates

The BFSI sector absorbed 28.65% of 2025 revenue as banks adopted stringent fraud-risk management frameworks and insurers digitised policy-administration controls. Engagements range from loan-book analytics to recovery-risk dashboards that regulators now inspect. Fintech collaborations expand the audit scope to include model-risk validations and API-security assessments. Healthcare & life-sciences, meanwhile, records a 6.12% CAGR as pharma and med-tech companies adjust to evolving clinical-data standards and supply-chain traceability requirements. Information technology & ITeS benefits from GCC hub growth, whereas manufacturing leverages Union Budget incentives for electronics and defence corridors.

Cross-sector overlaps emerge: banks finance healthcare M&A that demands combined due diligence; consumer-goods players enter digital payments that entail fintech compliance. Such convergence multiplies advisory entry points, cementing the primacy of sector-specific expertise in the India accounting professional services market.

Geography Analysis

Tier-1 centres, Delhi NCR, Mumbai, Bengaluru, Chennai, Hyderabad, and Kolkata, anchor the India accounting professional services market, maintaining premium pricing based on regulatory adjacency. Delhi concentrates on policy advisory and public-sector audits, whereas Mumbai’s financial district powers capital-market and treasury-risk mandates. Bengaluru’s startup density yields valuation and share-based payment complexities; Chennai’s auto-component ecosystem demands cost-accounting analytics; Hyderabad’s life-sciences hub elevates clinical-audit work; and Kolkata handles eastern-region public-sector banks. Talent costs climbed 12% in these metros in 2024, tightening margins and incentivizing off-site execution models.

Tier-2 cities marked the fastest 7.52% CAGR as GCCs and regional conglomerates migrate for cost and talent access. Pune leads automotive, engineering, and shared-finance centers; Ahmedabad mixes textiles, pharma, and commodities financing; Jaipur has micro-finance and tourism conglomerates; Kochi advances maritime logistics and IT services. State governments extend 50% property-tax waivers and fast-track land approvals, lowering the total cost of ownership for professional-services operations. Firms increasingly station tax-processing, management-reporting, and AI-model testing teams in these hubs while keeping partner signoffs in metros, thus realizing blended margins without sacrificing quality.

Tier-3 and emerging cities, though small at present, project long-term importance through Digital India penetration, GST registration drives, and one-district-one-product export schemes. Smart-city investments improve connectivity in Agartala, Dharwad, and Rourkela, promising eventual demand for assurance and consulting. SaaS adoption remains highest in these markets, pressuring traditional bookkeeping fees but also generating data streams that consultants can mine for performance benchmarking. Consequently, end-to-end service propositions, advisory design in metros, execution in Tier-2, and scalable compliance in Tier-3, characterize future delivery architecture for the India accounting professional services market.

Competitive Landscape

The top six networks audited 326 of 483 Nifty-500 companies in 2024, confirming a tightly concentrated audit arena that co-exists with fast diversifying advisory plays. Auditor-rotation deadlines in 2025-26 put 50% of current mandates in play, catalysing strategic alliances between Big-Four offshoots and high-quality domestic firms to defend ground. Technology capability drives differentiation: leading networks have introduced AI-assisted sampling engines to halve substantive-testing hours, while mid-tier challengers deploy blockchain-based confirmation platforms to validate trade receivables in real time.

Talent wars intensify; collective hiring plans exceed 43,000 over the next four years, aggravated by U.S. firms offshoring audit and tax work at premium wage scales. Attrition surpasses 25% for associates in Mumbai and Bengaluru, prompting firms to implement rapid-upskilling academies and flexible work locations in Tier-2 cities. Regulatory scrutiny also shapes competition: NFRA’s 94 enforcement orders since 2022 and commentary on audit-quality lapses have pushed firms to invest in second-party reviews, data-quality portals, and control-testing templates.

Government ambition to seed a home-grown Big-Four cluster is the wild card. Domestic mid-tiers explore mergers to build national footprints, while foreign networks lobby for regulatory neutrality. Strategic moves in 2024-25 include Grant Thornton’s forensic partnership with IndusInd Bank for a USD 175 million derivatives review and EY’s integrated GCC advisory bundle targeting USD 2 billion revenue by 2027. Disruptors in specific niches, ESG assurance, crypto-tax advisory, gain traction but lack scale to dent mainline revenue. Taken together, technology depth, talent resilience, and regulatory capital are decisive factors in the evolving India accounting professional services market.

India Accounting Professional Services Industry Leaders

PwC India

EY India

Deloitte India

KPMG India

Grant Thornton Bharat

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Prime Minister’s Office initiated consultations on policies to nurture indigenous Big-Four-scale accounting firms, signalling possible legislative revisions.

- March 2025: IndusInd Bank appointed Grant Thornton for a forensic review of USD 175 million in derivatives valuation discrepancies.

- January 2025: ICAI released CA GPT, integrating 5,000 listed-company annual reports and AI-enabled analytics modules.

- November 2024: NFRA published its first annual inspection reports on major audit firms, outlining remedial expectations.

India Accounting Professional Services Market Report Scope

Accounting professionals are experts at maintaining financial records, including accounts, financial statements, and financial plans. They have expertise in audits and account analysis. They offer guidance on implementing profitable and cost-effective business strategies and assist organizations in resolving their financial issues. The India Accounting Professional Services Market is segmented By Type of Service (Tax Preparation Services, Bookkeeping Services, Payroll Services, and Others), By Region (North, South, East, and West).

| Audit & Assurance |

| Tax & Regulatory |

| Advisory & Consulting |

| Risk Advisory |

| Business Services & Outsourcing |

| Digital Transformation & Technology Consulting |

| Large Enterprises |

| Mid-Market Enterprises |

| Micro, Small & Medium Enterprises (MSMEs) |

| Start-ups & Early-stage Firms |

| Government & Public-Sector Undertakings (PSUs) |

| Banking, Financial Services & Insurance (BFSI) |

| Information Technology & ITeS |

| Manufacturing & Industrial |

| Healthcare & Life Sciences |

| Consumer & Retail |

| Energy & Utilities |

| Infrastructure, Real Estate & Construction |

| Telecommunications & Media |

| Public Sector & NGOs |

| Logistics & Transportation |

| Tier-1 Cities (Delhi NCR, Mumbai, Bengaluru, Chennai, Kolkata, Hyderabad) |

| Tier-2 Cities |

| Tier-3 & Emerging Cities |

| By Service Type | Audit & Assurance |

| Tax & Regulatory | |

| Advisory & Consulting | |

| Risk Advisory | |

| Business Services & Outsourcing | |

| Digital Transformation & Technology Consulting | |

| By Client Size | Large Enterprises |

| Mid-Market Enterprises | |

| Micro, Small & Medium Enterprises (MSMEs) | |

| Start-ups & Early-stage Firms | |

| Government & Public-Sector Undertakings (PSUs) | |

| By Industry Vertical | Banking, Financial Services & Insurance (BFSI) |

| Information Technology & ITeS | |

| Manufacturing & Industrial | |

| Healthcare & Life Sciences | |

| Consumer & Retail | |

| Energy & Utilities | |

| Infrastructure, Real Estate & Construction | |

| Telecommunications & Media | |

| Public Sector & NGOs | |

| Logistics & Transportation | |

| By Regional Tier | Tier-1 Cities (Delhi NCR, Mumbai, Bengaluru, Chennai, Kolkata, Hyderabad) |

| Tier-2 Cities | |

| Tier-3 & Emerging Cities |

Key Questions Answered in the Report

What is the current size of the India accounting professional services market?

The India accounting professional services market size stands at USD 15.97 billion in 2026 and is projected to reach USD 19.66 billion by 2031 at a 4.25% CAGR.

Which service segment leads the market?

Digital transformation & technology consulting commands 51.12% share and is forecast to grow at 8.25% CAGR, outpacing traditional audit and tax lines.

Why are Tier-2 cities important for accounting firms?

Tier-2 hubs offer 10%-35% cost savings, state incentives, and expanding GCC footprints, which together support a 7.52% CAGR—higher than metro growth.

How will mandatory auditor rotation affect competition?

Rotation will free 242 listed-company mandates in 2025-26, opening doors for mid-tier firms and prompting alliances among established networks.

Page last updated on: