North America Financial Advisory Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

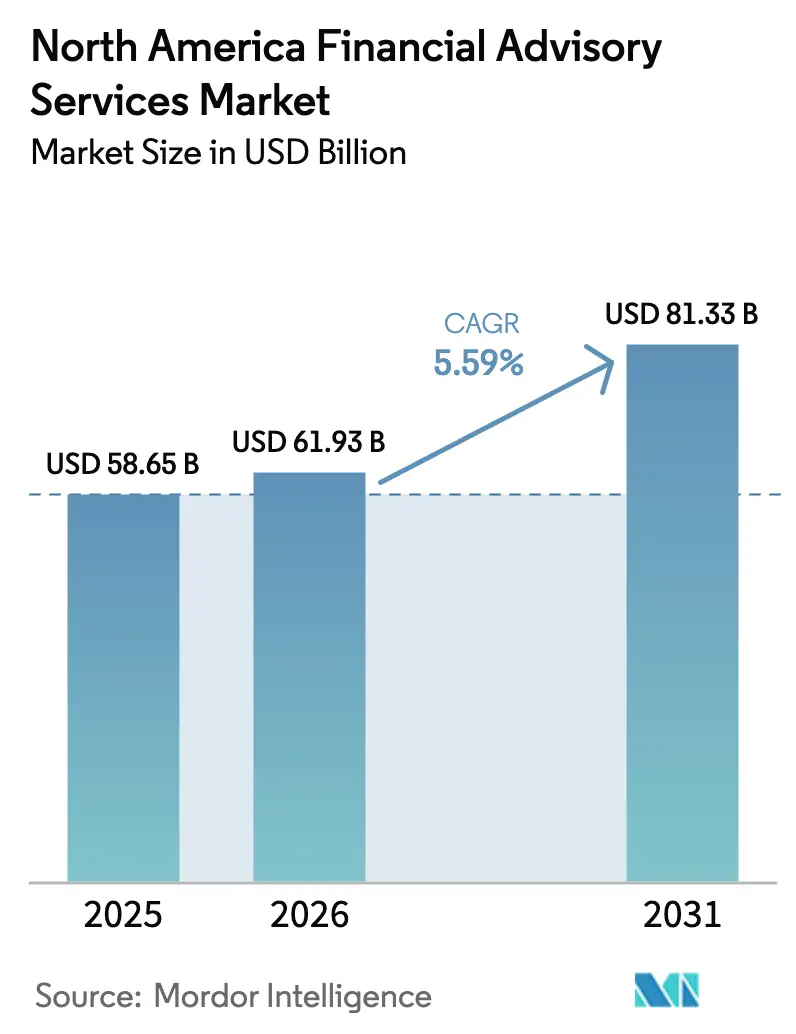

| Base Year Market Size (2025) | USD 58.65 Billion |

| Market Size (2026) | USD 61.93 Billion |

| Market Size (2031) | USD 81.33 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

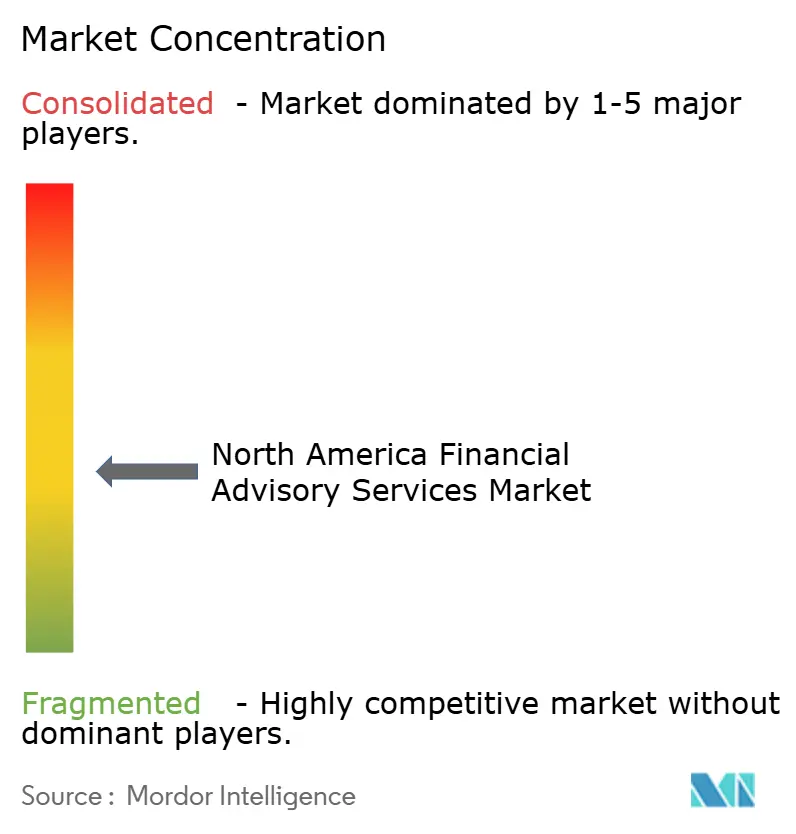

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Financial Advisory Services Market Analysis by Mordor Intelligence

The North America financial advisory market size is expected to grow from USD 58.65 billion in 2025 to USD 61.93 billion in 2026 and is forecast to reach USD 81.33 billion by 2031 at 5.59% CAGR over 2026-2031. Client expectations, regulatory tightening, and rapid technology adoption combine to lift revenue potential even as price pressure increases. Digital platforms widen access to advice, while a historic wealth transfer forces firms to rebuild service models for younger, tech-centric investors[1]CNBC, “81% of millionaire heirs plan to switch advisers,” cnbc.com. Private-equity-funded consolidation brings economy-of-scale advantages in compliance, cybersecurity, and analytics, yet specialist boutiques continue to win mandates in complex cross-border, ESG, and alternative-asset domains. Fee compression remains a challenge as custodians slash ETF prices and robo platforms scale, prompting advisers to shift the conversation from basis points to holistic value. Overall, the North America financial advisory market illustrates a two-track structure: large platforms dominate mainstream households, while focused experts capture niche, high-margin segments.

Key Report Takeaways

- By service type, investment services led with a 36.02% share in the North America financial advisory market in 2025 and are forecasted to grow at a 6.95% CAGR through 2031, consolidating their role at the heart of the North America financial advisory market.

- By organization size, large enterprises held 65.62% of the North America financial advisory market share in 2025, while SMEs are projected to expand at a 6.25% CAGR as digital tools narrow the scale gap.

- By industry vertical, the BFSI segment accounted for 29.55% of the North America financial advisory market size in 2025, whereas IT & Telecommunication is projected to advance at a 6.45% CAGR.

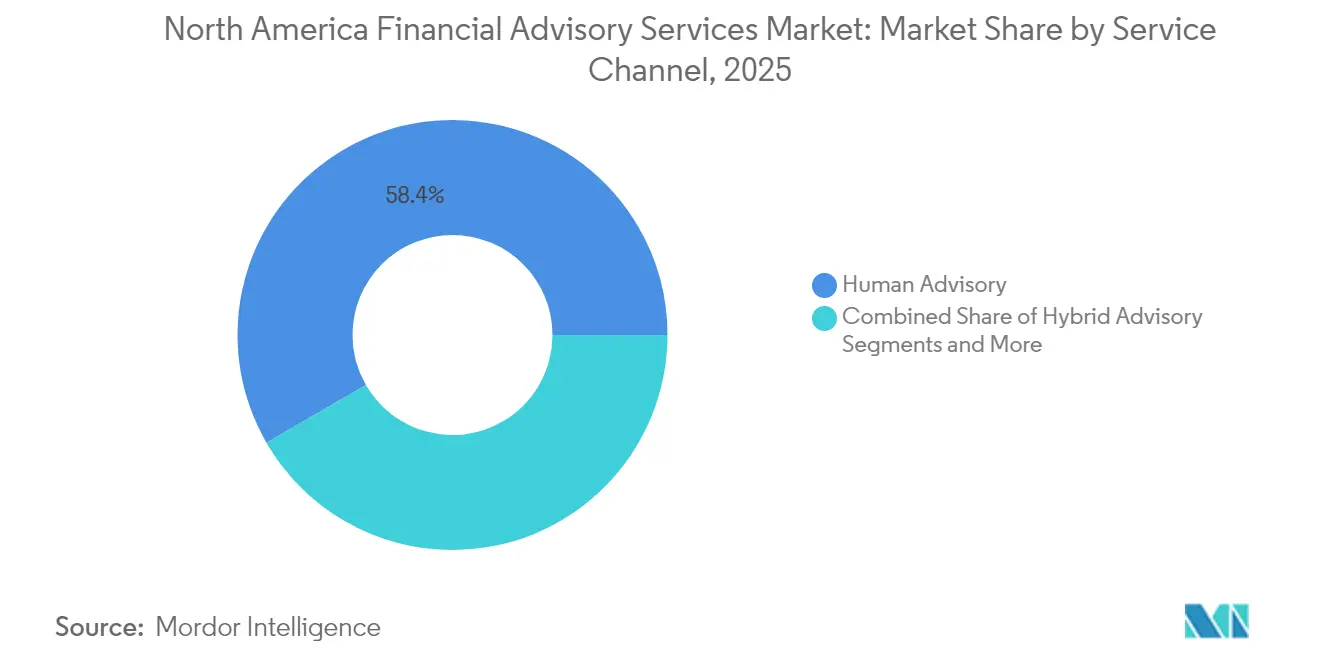

- By service channel, human advisory retained 58.35% share of the North America financial advisory market in 2025, yet robo-advisory is rising at a 9.84% CAGR through 2031.

- By delivery mode, on-site consulting commanded 71.60% of the North America financial advisory market size in 2025, while remote consulting is expected to climb at a 8.90% CAGR.

- By country, the United States captured 87.40% share of the North America financial advisory market in 2025, yet Mexico is forecasted to post the fastest 6.40% CAGR, opening diversification avenues.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on financial advisory services market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Financial Advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of robo- and AI-enabled advisory tools | +1.2% | USA leading, Canada moderate, Mexico emerging | Medium term (2-4 years) |

| Accelerating HNWI population and investable assets | +0.9% | Region-wide, metro clustering | Long term (≥ 4 years) |

| Surge in PE-backed mid-market M&A deal volume | +0.8% | USA dominant, Canada spillover | Short term (≤ 2 years) |

| Regulatory shift toward fiduciary duty | +0.6% | USA primary, Canada alignment | Medium term (2-4 years) |

| ESG-linked mandates reshaping propositions | +0.5% | Global, North America leadership | Long term (≥ 4 years) |

| Generational wealth transfer to digital investors | +0.7% | Regional wealth centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Robo- & AI-Enabled Advisory Tools

Robo services now manage multi-hundred-billion portfolios, with Vanguard at USD 206.6 billion and Schwab at USD 65.8 billion. Agentic AI engines already automate personalized advice for numerous households, promising significant value for the banking sector each year. Although 96% of advisers believe generative AI will transform service, only 41% currently scale deployments, giving early adopters a cost advantage. Platforms such as Range have raised USD 28 million to deliver AI-guided wealth plans for affluent clients, signaling investor confidence in digital-first models[2]WealthManagement.com, “Range raises USD 28 million,” wealthmanagement.com. The strategic imperative across the North America financial advisory market is to blend human empathy with machine efficiency.

Accelerating HNWI Population & Investable Assets

North America added a record number of high-net-worth individuals in 2025, outpacing every other region. More than half now demand ESG filters, and an even larger share plan to increase ESG allocations within two years. Ultra-wealthy households prioritize private equity, sustainable funds, and concierge-style services that carry premium fees. Wealth concentration lifts revenue per client, but younger heirs prefer tech-centric, purpose-driven advice, pressuring legacy engagement formats. Advisors successful in the North America financial advisory market, therefore, integrate family-office, tax, and digital delivery capabilities.

Surge in PE-Backed Mid-Market M&A Deal Volume

Private equity continues to reshape the competitive map, highlighted by LPL Financial’s USD 2.7 billion purchase of Commonwealth and Focus Financial’s combination of Buckingham Strategic Wealth with The Colony Group. Deal flow is propelled by recurring revenue and fragmented supply that invite roll-up strategies. Yet frequent ownership changes test client patience, so acquirers must balance financial engineering with cultural continuity to protect retention across the North America financial advisory market[3]Financial Planning, “Compliance costs surge under Reg-BI,” financial-planning.com.

Regulatory Shift Toward Fiduciary Duty (SEC Reg-BI)

SEC Regulation Best Interest imposes disclosure, care, conflict, and compliance obligations that elevate operating costs but reward transparent models. Firms demonstrating superior fiduciary alignment gain trust in a landscape where 80% of heirs plan to work with professionals’ post-inheritance. State-level cybersecurity proposals add further compliance layers, advancing providers with robust systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from passive and digital competitors | -0.8% | USA primary, Canada moderate | Medium term (2-4 years) |

| Escalating compliance and audit-trail costs | -0.6% | Region-wide | Short term (≤ 2 years) |

| Aging advisor workforce and talent pipeline gaps | -0.9% | USA and Canada | Long term (≥ 4 years) |

| Rising cyber-risk undermining client trust | -0.4% | Global, elevated in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fee Compression from Passive & Digital Competitors

Schwab’s June 2025 decision to slash ETF fees by up to 50% underscores accelerating price competition. Passive investing’s share of U.S. fund assets continues to climb, forcing advisers to defend pricing through holistic planning and alternative-asset access. Hybrid fee structures combining flat retainers and outcome-based incentives gain traction across the North America financial advisory market.

Aging Advisor Workforce & Talent Pipeline Gaps

Close to 40% of U.S. advisers are within a decade of retirement, and recent annual headcount growth stands at just 0.3%. Only 2,579 new advisers entered the profession in 2024, and attrition remains high, widening the supply gap. Remote collaboration tools help older advisers extend careers, but firms still need structured mentorship and AI-assisted onboarding to safeguard capacity across the North America financial advisory market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Investment Services Drive Growth

Investment services held the largest share at 36.02% in the North America financial advisory market in 2025 and are projected to expand at 6.95% CAGR through 2031, anchoring the North America financial advisory market. Multi-asset mandates now include private equity feeders, ESG overlays, and direct-indexing portfolios attractive to digital-native investors. The North America financial advisory market size for investment services is projected to swell as rising alternative allocations demand tailored structuring.

Corporate finance advisory remains resilient on mid-market M&A and succession deals, while accounting and tax advice scales with cross-border complexity. Other services- estate planning, philanthropy, and concierge support- grow fastest as wealthy families seek comprehensive stewardship. Advisers coupling investment depth and lifestyle capabilities therefore secure a higher wallet share in the North America financial advisory market.

By Organization Size: SME Growth Challenges, Enterprise Dominance

Large enterprises controlled 65.62% of the North America financial advisory market in 2025, wielding deep compliance and technology budgets that defend mass-affluent franchises. Yet SMEs are expected to outpace at 6.25% CAGR, aided by cloud tools and AI-based productivity that minimize scale disadvantages. The North America financial advisory market size tied to SMEs is set to widen as boutique firms carve niches in ESG consulting and crypto tax planning.

Personalized engagement, transparent pricing, and quick innovation cycles bolster SME appeal among younger investors. However, mid-sized firms face a squeeze: they must either specialize or merge upward to keep pace with widening compliance and cybersecurity demands in the North America financial advisory market.

By Industry Vertical: Technology Sector Wealth Creation Drives Growth

BFSI accounted for 29.55% of the North America financial advisory market in 2025, driven by complex regulatory needs and large asset pools, while IT & Telecommunication is poised for the fastest 6.45% CAGR thanks to option-rich liquidity events and cryptocurrency holdings. Advisers versed in equity-compensation strategies and token taxation stand out.

Manufacturing and retail owners prioritize succession and retirement planning, whereas healthcare executives lean on advisers for biotech windfalls and charitable trusts. Public-sector mandates add low-volatility revenue streams. Deep vertical expertise yields higher retention and pricing power within the North America financial advisory market.

By Service Channel: Digital Transformation Accelerates

Human advice held a 58.35% share in the North America financial advisory market in 2025, reinforcing that empathy drives complex financial decisions. Yet, robo platforms are set to grow 9.84% per year through 2031. Hybrid delivery models dominate new client wins, blending algorithmic rebalancing with scenario coaching in the North America financial advisory market.

Custodians integrate planning dashboards into mobile banking apps, turning day-to-day cash movement into holistic advice moments. Competition has shifted toward speed, data visualization, and embedded ESG scoring rather than raw investment alpha. AI chatbots answer routine queries instantly and escalate nuanced issues, elevating adviser productivity across the North America financial advisory market.

By Delivery Mode: Remote Capabilities Enable Market Expansion

On-site engagements controlled 71.60% of the North America financial advisory market share in 2025, but remote consulting is projected to escalate at 8.90% CAGR as clients accept video, shared screens, and digital signatures. The North America financial advisory market benefits as firms serve cross-border households without opening extra branches.

Cyber-risk awareness drives investment in end-to-end encryption and biometric log-ins, helping maintain trust and regulatory compliance. Advisers who toggle seamlessly between in-person and virtual modes strengthen loyalty, particularly among bi-national families who prize flexible scheduling in the North America financial advisory market.

Geography Analysis

The United States accounted for 87.40% of the North America financial advisory market in 2025, supported by deep capital markets, dense adviser networks, and robust fiduciary frameworks. A looming talent shortfall, however, threatens capacity as veteran advisers exit faster than replacements enter. Fee-based contracts continue to expand, illustrating the North America financial advisory market’s resilience despite compliance costs.

Canada offers steady growth within a consolidated banking system where six institutions hold a significant share of assets. Title protection for financial planners and a consumer-driven banking framework modernize the competitive landscape. HNWI inflows to Toronto, Vancouver, Montreal, and Calgary sustain premium demand. Cross-border estate and tax planning remains a lucrative niche in the North America financial advisory market.

Mexico is set for the fastest 6.40% CAGR, propelled by fintech expansion and regulatory modernization. The economy expanded 0.2% in Q1 2025 despite U.S. softness, signaling resilience. Search funds and new private-equity vehicles broaden advisory addressable markets, while heightened tax transparency boosts cross-border structuring opportunities.

Mordor Intelligence provides coverage of the financial advisory services market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The North America financial advisory market shows moderate concentration as PE-backed aggregators, banks, and asset-manager affiliates buy scale through acquisition. LPL’s integration of Atria Wealth Solutions, adding 2,400 advisers and USD 100 billion in client assets, typifies the roll-up thesis. Charles Schwab’s fee cuts aim to defend custodial dominance by tightening the price floor for ETFs.

Technology-first challengers raise meaningful capital; Range, for example, has secured USD 40 million to automate planning for HNW clients. These players operate at materially lower cost-to-serve and target digitally native households. Concurrently, specialist boutiques command loyalty among ultra-wealthy families by offering customized, high-touch services that large platforms struggle to replicate.

Mid-sized firms that cannot match scale economics or deep specialization face strategic pressure to merge or sell. The resulting barbell market forces participants to pick between industrial-grade efficiency and expert-led intimacy within the North America financial advisory market.

North America Financial Advisory Services Industry Leaders

Deloitte

PwC

Ernst & Young

KPMG

McKinsey & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Toronto-based KORT Payments bought Paysafe’s direct-marketing processing business under a five-year earn-out, expanding payment reach across North America.

- April 2025: Prospera Credit Union, Coast Capital Savings, and Sunshine Coast Credit Union agreed to merge, forming Canada’s largest purpose-driven credit union with CAD 38.6 billion in assets.

- January 2025: Focus Financial Partners acquired Merriman Wealth Management, adding USD 4.16 billion in AUM.

- December 2024: Range closed a USD 28 million Series B to scale its AI-driven platform for HNW clients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America financial advisory services market as fee- or asset-based guidance delivered by licensed firms on investment management, corporate finance, tax and accounting structuring, transaction support, and risk consulting to individuals, SMEs, and large enterprises across the United States, Canada, and Mexico. Activities are measured on revenue earned within the region, irrespective of global client origin, and include hybrid and robo-enabled advice.

Scope Exclusion: pure online brokerage commissions and stand-alone insurance agency fees are outside this scope.

Segmentation Overview

- By Service Type

- Corporate Finance

- Accounting And Tax Advisory

- Investment

- Other Services

- By Organization Size

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By Industry Vertical

- Banking, Financial Services, Insurance (BFSI)

- IT & Telecommunication

- Manufacturing

- Retail And E-Commerce

- Public Sector

- Healthcare And Pharmaceuticals

- Other Industry Verticals

- By Service Channel

- Human Advisory

- Hybrid Advisory

- Robo-Advisory

- By Delivery Mode

- On-site Consulting

- Remote / Virtual Consulting

- By Country

- USA

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with portfolio managers, CPA partners, independent advisors, and fintech platform executives across multiple U.S. states and the two largest Canadian provinces. Discussions clarified fee compression, digital adoption rates, and regional client mix, allowing us to validate secondary indicators and refine service-mix assumptions.

Desk Research

We began with public macro sets from the Federal Reserve, Statistics Canada, Mexico's CNBV, and industry groups such as the Investment Company Institute and the North American Securities Administrators Association. Company 10-Ks, Form ADV filings, and investor decks supplied revenue splits, while transaction volumes came from S&P Capital IQ and the U.S. M&A Statistics database. Additional context on private wealth trends was drawn from Capgemini's World Wealth Report and patent analytics via Questel to track robo-advisory IP expansion. These sources are illustrative; many more were tapped to corroborate figures and fill data gaps.

Market-Sizing & Forecasting

A blended top-down, bottom-up model anchors the baseline. National advisory revenue pools were first estimated from reported AUM, average fee schedules, and penetration of advised assets, then cross-checked with sampled firm roll-ups and channel checks. Key variables like HNWI population growth, SME formation rates, median advisory fee (bps), M&A deal count, robo-advisory penetration, and shifts to fee-only models drive our multivariate regression forecast to 2030. Where firm-level data were missing, gaps were bridged using peer averages adjusted for client mix and service breadth.

Data Validation & Update Cycle

Outputs move through anomaly scans, senior analyst reviews, and variance checks against macro indicators before sign-off. We refresh models annually and issue interim tweaks when material events, such as regulation, major acquisitions, or macro shocks, alter assumptions.

Why Mordor's North America Financial Advisory Services Baseline Is Dependable

Published estimates often diverge; scope choices, pricing bases, and refresh cadence typically drive the spread.

Key gap drivers include differing treatment of hybrid-advice fees, inclusion or exclusion of corporate restructuring revenue, and currency conversion timing. Mordor's disciplined segmentation and yearly refresh reduce these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 58.65 B (2025) | Mordor Intelligence | - |

| USD 63.90 B (2024) | Regional Consultancy A | Combines wealth-management AUM fees with advisory revenue, inflating totals |

| USD 12.00 B (2025) | Industry Journal B | Counts only disclosed fee income, omitting corporate finance and transaction support |

| USD 36.15 B (2025) | Global Consultancy C | Uses survey sample of mid-market firms; excludes large-bank advisory arms |

The comparison shows that when scope is either too broad or too narrow, numbers swing widely. By grounding estimates in verifiable revenue, calibrated variables, and a clear refresh rhythm, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the North America financial advisory market?

The market totals USD 61.93 billion in 2026 and is forecast to reach USD 81.33 billion by 2031.

Which service type grows fastest in the North America financial advisory market?

Investment services lead growth with a 6.95% CAGR through 2031 while already holding the largest revenue share.

How quickly is robo advice expanding?

Robo platforms in the North America financial advisory market are projected to grow at a 9.84% CAGR, far ahead of human-only channels.

Why is Mexico the fastest-growing geography?

Fintech expansion, regulatory modernization, and steady GDP growth propel Mexico to a 6.40% CAGR.

What drives fee compression in advisory services?

Aggressive ETF price cuts and the rise of low-cost digital competitors push traditional advisers to compete on comprehensive planning rather than standalone investment fees.

How is private equity reshaping the competitive landscape?

PE-backed consolidators acquire independent firms for scale but must balance financial returns with client retention to sustain long-term value.

Page last updated on: