Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

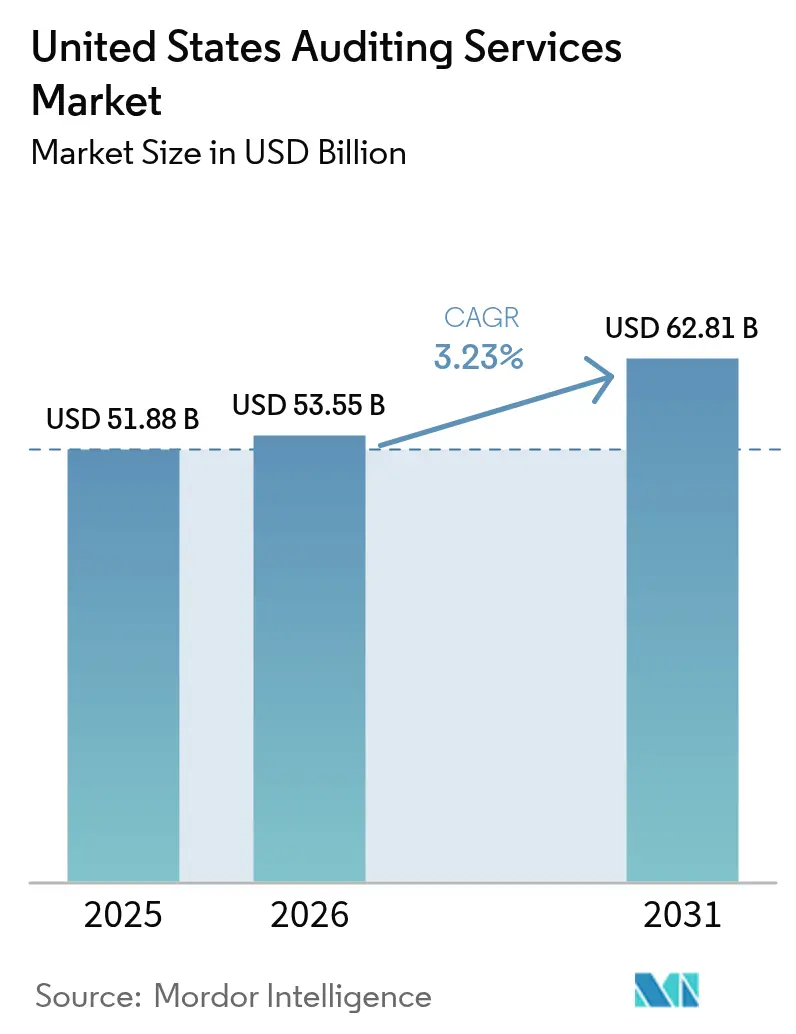

| Base Year Market Size (2025) | USD 51.88 Billion |

| Market Size (2026) | USD 53.55 Billion |

| Market Size (2031) | USD 62.81 Billion |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Auditing Services Market Analysis by Mordor Intelligence

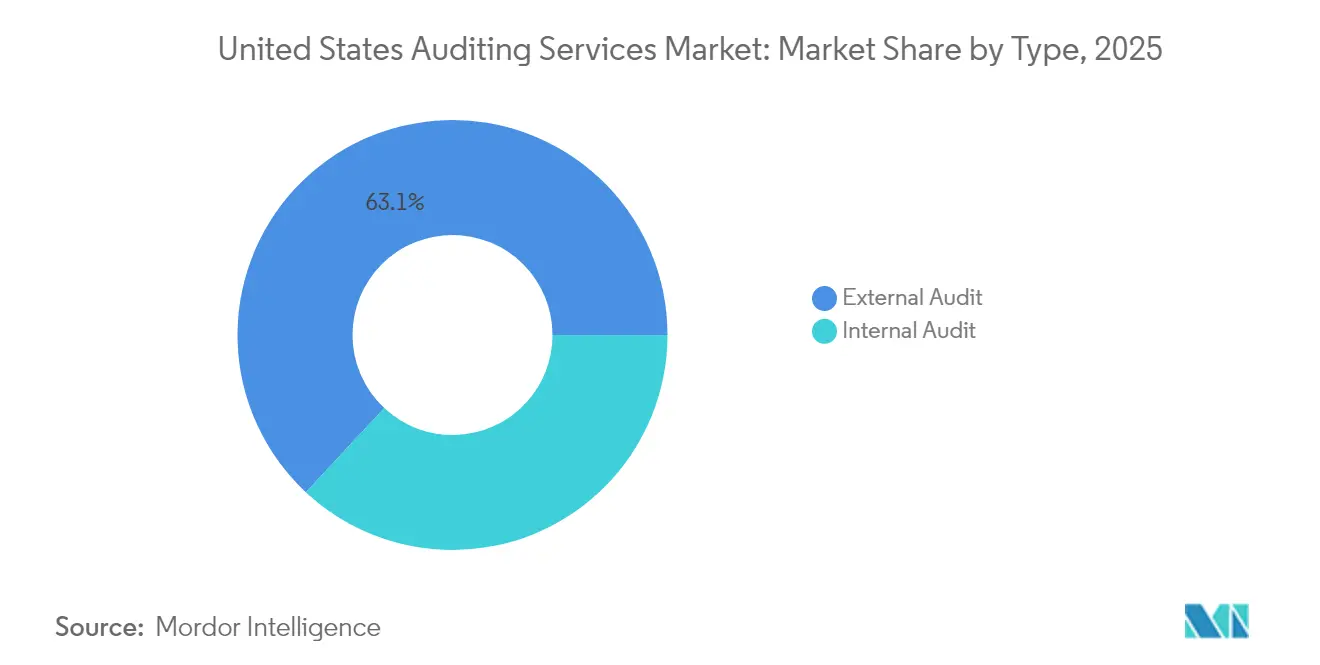

The United States auditing services market size in 2026 is estimated at USD 53.55 billion, growing from 2025 value of USD 51.88 billion with 2031 projections showing USD 62.81 billion, growing at 3.23% CAGR over 2026-2031. This growth trajectory reflects the United States auditing services market transition from a compliance-centric model toward integrated assurance that covers cybersecurity, ESG disclosures, and operational risk. Intensifying SEC oversight of internal controls, mounting cyber threats, and mandatory sustainability assurance are combining to lift demand, while automation platforms and offshore delivery temper pricing power. The United States auditing services market is further buoyed by federal infrastructure spending that triggers single-audit requirements, although labor shortages and fee pressure from analytics-driven efficiency gains remain structural brakes. External audit commands 63.63% revenue in 2024, but internal audit services, strengthened by continuous monitoring technologies and enterprise risk management adoption, are advancing at a 9.15% CAGR through 2030. Information-system auditing is growing fastest within service lines as clients integrate IT control testing into statutory audits.

Key Report Takeaways

- By type, external audit captured 63.05% of the United States auditing services market share in 2025, while internal audit is on track for a 8.72% CAGR through 2031.

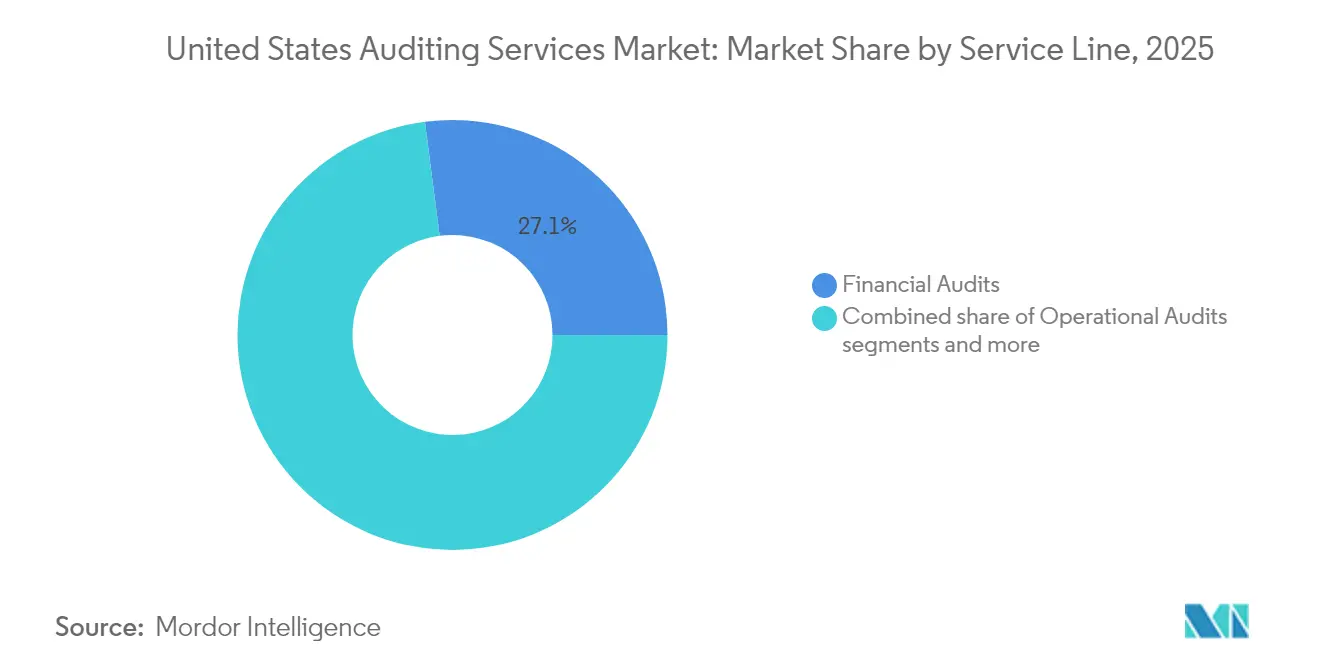

- By service line, financial audits led with 27.05% of the United States auditing services market size in 2025, whereas information-system audits are poised to grow at a 12.18% CAGR to 2031.

- By end-user industry, the BFSI segment commanded 22.10% of the United States auditing services market size in 2025, but IT & telecommunications is projected to register the highest 8.29% CAGR between 2026 and 2031.

- By geography, the South accounted for 29.05% of the United States auditing services market size in 2025, while the West is forecast to record a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Auditing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened SEC enforcement of internal-control rules | 0.8% | National, concentrated in major financial centers | Medium term (2-4 years) |

| Rising cyber-risk demanding integrated IT audits | 0.6% | National, with higher impact in tech-heavy regions | Short term (≤ 2 years) |

| Mandatory ESG-related assurance for listed firms | 0.4% | National, with early adoption in California and Northeast | Medium term (2-4 years) |

| Rapid adoption of continuous audit analytics platforms | 0.3% | National, led by large metropolitan areas | Short term (≤ 2 years) |

| SME demand for SOC 2 Type II attestation to win SaaS contracts | 0.2% | West Coast and Northeast technology corridors | Short term (≤ 2 years) |

| Expansion of federal infrastructure spend triggering single-audit requirements | 0.1% | National, with concentration in infrastructure-heavy states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened SEC Enforcement of Internal-Control Rules

The Securities and Exchange Commission's intensified focus on internal control deficiencies is reshaping audit scope and methodology requirements across public companies. SEC enforcement actions increased 22% in 2024, with particular emphasis on management's assessment of internal control over financial reporting and auditor testing procedures [1]: Public Company Accounting Oversight Board, “2024 Inspections Summary,” pcaobus.org. . This regulatory pressure creates sustained demand for external audit services as companies invest in control remediation and enhanced testing protocols. The PCAOB's expanded inspection focus on audit quality indicators and risk assessment procedures forces audit firms to allocate additional resources to control testing, directly impacting billable hours and engagement profitability while strengthening market demand for specialized internal control advisory services.

Rising Cyber-Risk Demanding Integrated IT Audits

Cybersecurity incidents affecting financial reporting systems have prompted regulators and audit committees to demand integrated IT audit procedures within traditional financial audits. The SEC's cybersecurity disclosure rules, effective December 2023, require public companies to disclose material cybersecurity incidents within 4 business days, creating audit implications for subsequent financial reporting periods. Audit firms are rapidly expanding their IT audit capabilities, with KPMG investing over USD 1 billion in audit technology platforms that integrate cybersecurity risk assessment with financial audit procedures. This convergence of financial and IT auditing creates new revenue streams while requiring significant upfront investment in specialized talent and technology platforms.

Mandatory ESG-Related Assurance for Listed Firms

The SEC's climate disclosure rules, adopted in March 2024, establish the first federal mandate for sustainability-related assurance services, fundamentally expanding the addressable audit market beyond traditional financial reporting. Large accelerated filers must obtain limited assurance over Scope 1 and 2 greenhouse gas emissions beginning in 2029, with reasonable assurance required by 2033 [2]Faegre Drinker, “SEC Issues Final Climate Disclosure Rules for Public Companies,” faegredrinker.com. . This regulatory shift creates an estimated USD 2-3 billion annual market opportunity for specialized ESG assurance services, though current provider capacity remains severely constrained. The intersection of financial reporting and sustainability metrics requires audit firms to develop new competencies in environmental data verification, carbon accounting methodologies, and climate risk assessment procedures.

Rapid Adoption of Continuous Audit Analytics Platforms

Artificial intelligence and machine learning technologies are enabling real-time audit testing capabilities that expand traditional audit scope while improving efficiency metrics. EY's deployment of its EYQ artificial intelligence platform across 180 countries, with over 75% of staff utilizing the technology for audit procedures, demonstrates the sector's rapid technology adoption. These platforms enable continuous monitoring of financial transactions, automated exception testing, and predictive risk analytics that identify potential misstatements before traditional year-end audit procedures. The technology shift allows audit firms to offer enhanced services while maintaining competitive pricing, though initial implementation costs and training requirements create near-term margin pressure for adopting firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortages inflating bill rates | -0.4% | National, acute in metros | Short term (≤ 2 years) |

| Automation reducing repeat audit hours | -0.3% | National, tech-forward firms | Medium term (2-4 years) |

| Growing use of internal shared-service centers | -0.2% | National, more prevalent among large firms | Medium term (2–4 years) |

| Litigation exposure and rising E&O insurance premiums | -0.3% | National, with concentration in litigious sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Shortages Driving Bill-Rate Inflation

The accounting profession faces an unprecedented talent crisis with CPA exam candidates declining 17% between 2020 and 2024, while demand for audit services continues to expand. This supply-demand imbalance has driven audit staff compensation increases of 15-25% annually, forcing firms to raise client billing rates and potentially pricing out smaller clients from professional audit services. The shortage particularly affects experienced senior and manager-level professionals, creating bottlenecks in audit execution and quality review processes. Firms are responding through accelerated offshore delivery models, increased automation, and alternative staffing arrangements, though these solutions require 2-3 years to fully implement and may not fully offset domestic talent constraints.

Automation Reducing Repeat Audit Hours

Advanced audit technologies are systematically eliminating routine testing procedures that historically generated substantial billable hours, creating deflationary pressure on traditional audit engagement economics. Data analytics platforms can now perform comprehensive transaction testing in hours rather than weeks, while artificial intelligence algorithms identify anomalies and risk patterns that previously required extensive manual procedures [3]AuditBoard, “AI in Audit: Transforming the Future of Financial Reporting,” auditboard.com. . This efficiency gain benefits clients through reduced audit fees but pressures firm profitability unless offset by expanded service offerings or premium pricing for specialized expertise. The transition forces audit firms to shift from time-based billing toward value-based pricing models while investing heavily in technology infrastructure and staff retraining programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Internal Audit Transformation Accelerates

Internal audit services are experiencing rapid growth at 8.72% CAGR through 2031, significantly outpacing external audit's more modest expansion, as organizations recognize internal audit's strategic value beyond traditional compliance functions. External audit maintains market dominance with 63.05% share in 2025, reflecting regulatory requirements for public company audits and the substantial revenue base of Big Four firms serving large corporate clients. The internal audit segment's acceleration reflects enterprise demand for continuous risk monitoring, operational efficiency assessments, and integrated governance frameworks that extend beyond financial reporting compliance.

Protiviti's expansion of internal audit services through technology-enabled continuous monitoring platforms exemplifies the segment's evolution toward real-time assurance capabilities. Internal audit functions increasingly incorporate cybersecurity risk assessment, ESG reporting validation, and third-party risk management, creating new revenue streams that command premium pricing compared to traditional compliance-focused procedures. The Institute of Internal Auditors' emphasis on digital transformation and data analytics capabilities reflects the profession's shift toward strategic advisory roles that directly support executive decision-making and board oversight responsibilities.

By Service Line: Information Systems Drive Growth

Information system audits represent the fastest-growing service line at 12.18% CAGR through 2031, reflecting the critical intersection of cybersecurity risks and financial reporting integrity in an increasingly digital business environment. Financial audits command the largest market share at 27.05% in 2025, benefiting from mandatory requirements for public company audits and the substantial engagement fees associated with large corporate clients. Compliance audits maintain a steady demand at 22.00% market share, driven by expanding regulatory requirements across healthcare, financial services, and government contracting sectors.

Advisory and consulting services capture 18.00% market share while growing at 9.72% CAGR, as audit firms leverage client relationships to provide broader business advisory services beyond traditional assurance functions. Operational audits and investigation audits serve specialized market niches, with investigation services particularly benefiting from increased corporate governance scrutiny and whistleblower protection regulations. The ISACA organization's emphasis on IT governance and risk management frameworks supports the information systems audit segment's expansion, as organizations recognize the critical importance of technology controls in maintaining financial reporting reliability and operational resilience.

By End-User Industry: Technology Sector Leads Growth

The IT and telecommunications sector demonstrates the highest growth trajectory at 8.29% CAGR through 2031, driven by rapid digital transformation, cybersecurity threats, and venture capital due diligence requirements that demand specialized audit expertise. Banking, financial services, and insurance maintain the largest market share at 22.10% in 2025, reflecting the sector's regulatory complexity, systemic risk considerations, and mandatory audit requirements for financial institutions. Healthcare and life sciences represent a significant portion of the auditing market and are experiencing strong growth, fueled by strict FDA regulations, oversight of clinical trials, and mandates around healthcare data privacy. The government and public sector also hold a large share, driven by federal single audit requirements and increasing demands for transparency at the state and local levels. Manufacturing remains a key vertical, with demand for audits focused on supply chain risk, environmental compliance, and operational efficiency. The energy and utilities sector is expanding steadily, supported by ongoing infrastructure investments and evolving environmental regulations. Across these industries, the blending of traditional financial audits with sector-specific compliance needs is creating opportunities for firms to offer specialized services at premium rates.

Geography Analysis

The South region dominates the United States auditing services market with a 29.05% share in 2025, benefiting from robust manufacturing growth, energy sector investments, and favorable business climates that attract corporate relocations requiring audit services. The region's growth trajectory at 6.18% CAGR through 2031 reflects continued economic expansion in Texas, Florida, and North Carolina, where technology companies and financial services firms establish major operations . Federal infrastructure spending through the Infrastructure Investment and Jobs Act particularly benefits Southern states with major transportation and energy projects requiring single audit compliance procedures for federal grant recipients.

The Northeast region captures a significant market share in 2025, leveraging its concentration of financial services firms, pharmaceutical companies, and established corporate headquarters that require sophisticated audit services. Despite mature market conditions, the region maintains good CAGR growth through 2031, supported by ESG reporting mandates that particularly affect large public companies concentrated in New York and Massachusetts. The region's regulatory expertise and proximity to SEC headquarters create competitive advantages for audit firms serving complex public company clients with specialized compliance requirements.

The West region demonstrates the highest growth potential at 6.88% CAGR through 2031, driven by technology sector expansion, venture capital activity, and California's leadership in environmental regulation that creates demand for specialized assurance services. The West region leads the auditing market in 2025, driven by the presence of high-growth companies in Silicon Valley that demand SOC 2 attestations, cybersecurity audits, and IPO readiness services. Meanwhile, the Midwest plays a major role as well, with strong demand stemming from its manufacturing base and agricultural commodity trading firms. These organizations often require specialized audit procedures focused on derivative instruments and commodity price risk management, making the region a key hub for industry-specific audit expertise.

Competitive Landscape

The U.S. auditing services market shows moderate concentration, with the Big Four firms collectively dominating the majority of market share. This oligopolistic structure enables them to command premium pricing for complex engagements while facing limited competition in more standardized audits. Their scale allows for global methodology standardization and over a billion dollars in annual technology investments, reinforcing their competitive edge. Regulatory expertise also provides a significant barrier that smaller firms struggle to overcome cost-effectively. These advantages create high entry barriers, allowing the leading firms to continually reinvest in AI, offshore delivery models, and specialized sector knowledge.

Despite the dominance of the Big Four, new growth avenues are emerging in niche audit services such as cybersecurity, ESG assurance, and support for technology startups. In these specialized areas, traditional Big Four approaches may be unnecessarily complex and costly for clients. Mid-tier firms like BDO, RSM, and Grant Thornton are capitalizing on this gap by offering tailored services, competitive pricing, and flexible delivery. Their deep industry expertise and responsiveness appeal to mid-market clients seeking more personalized audit experiences. These dynamics are enabling smaller firms to gradually gain ground in specific high-growth segments.

Regulatory pressure is also shaping the competitive landscape, with PCAOB inspections highlighting quality control issues across both large and small firms. This has intensified the focus on strong internal quality management and ongoing improvement efforts. Firms with robust systems in place are better positioned to withstand regulatory scrutiny and deliver consistent audit quality. As regulators prioritize effectiveness over firm size, the playing field is subtly shifting in favor of firms that can demonstrate operational excellence. In this evolving environment, audit quality and innovation are becoming as important as scale.

United States Auditing Services Industry Leaders

Deloitte

PwC

EY

KPMG

BDO USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FORVIS officially launched operations as the 8th largest accounting firm in the United States following the completed merger of BKD and Dixon Hughes Goodman, creating a USD 1.2 billion revenue platform with enhanced geographic coverage and industry specialization capabilities to compete more effectively with Big Four firms for middle-market clients.

- February 2025: KPMG US announced the launch of KPMG Law, expanding legal services capabilities to provide integrated audit, tax, and legal advisory services for complex transactions and regulatory compliance matters, marking the first major Big Four expansion into legal services since Sarbanes-Oxley restrictions.

- January 2025: Crowe LLP announced a strategic partnership with OpenAI to integrate generative artificial intelligence capabilities into audit procedures, focusing on automated risk assessment, document review, and anomaly detection to enhance audit quality while reducing engagement hours.

- December 2024: Baker Tilly and Moss Adams completed their merger discussions, creating a combined USD 2.8 billion revenue firm with strengthened West Coast presence and enhanced technology sector expertise, representing the largest mid-tier accounting firm merger in recent years.

United States Auditing Services Market Report Scope

Audit services mean the audit of annual financial statements and other procedures required by the statutory auditor to form an opinion on the company's financial statements and issue a report as required under section 143 of the Companies Act, 2013. The report covers a complete background analysis of the US property management market. It includes the assessment of the economy and the contribution of the economic sectors, market overview, market size estimation for key segments and emerging trends in the market segments, market dynamics, insights, and key statistics.

The US Auditing Services Market is segmented by type, service line. By type, the market is sub-segmented into internal audits and external audits. By service line, the market is sub-segmented into operational audits, financial audits, advisory and consulting, investigation audits, information system audits, compliance audits, and others. The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Type

| Internal Audit |

| External Audit |

By Service Line

| Operational Audits |

| Financial Audits |

| Advisory and Consulting |

| Investigation Audits |

| Information System Audits |

| Compliance Audits |

| Other Service Lines |

By End-User Industry

| BFSI |

| Manufacturing |

| Government & Public Sector |

| Healthcare & Life Sciences |

| IT & Telecom |

| Energy & Utilities |

| Other Industries |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Type | Internal Audit |

| External Audit | |

| By Service Line | Operational Audits |

| Financial Audits | |

| Advisory and Consulting | |

| Investigation Audits | |

| Information System Audits | |

| Compliance Audits | |

| Other Service Lines | |

| By End-User Industry | BFSI |

| Manufacturing | |

| Government & Public Sector | |

| Healthcare & Life Sciences | |

| IT & Telecom | |

| Energy & Utilities | |

| Other Industries | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the projected value of the United States auditing services market by 2031?

The market is forecast to reach USD 62.81 billion by 2031.

Which audit service line is growing fastest through 2031?

Information-system audits are projected to expand at a 12.18% CAGR.

Which U.S. region shows the highest growth for audit services?

The West region is expected to record the quickest 6.88% CAGR.

What key regulation is expanding ESG assurance demand?

The SEC’s 2024 climate-disclosure rule introduces phased assurance over greenhouse-gas emissions.

Page last updated on: