Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

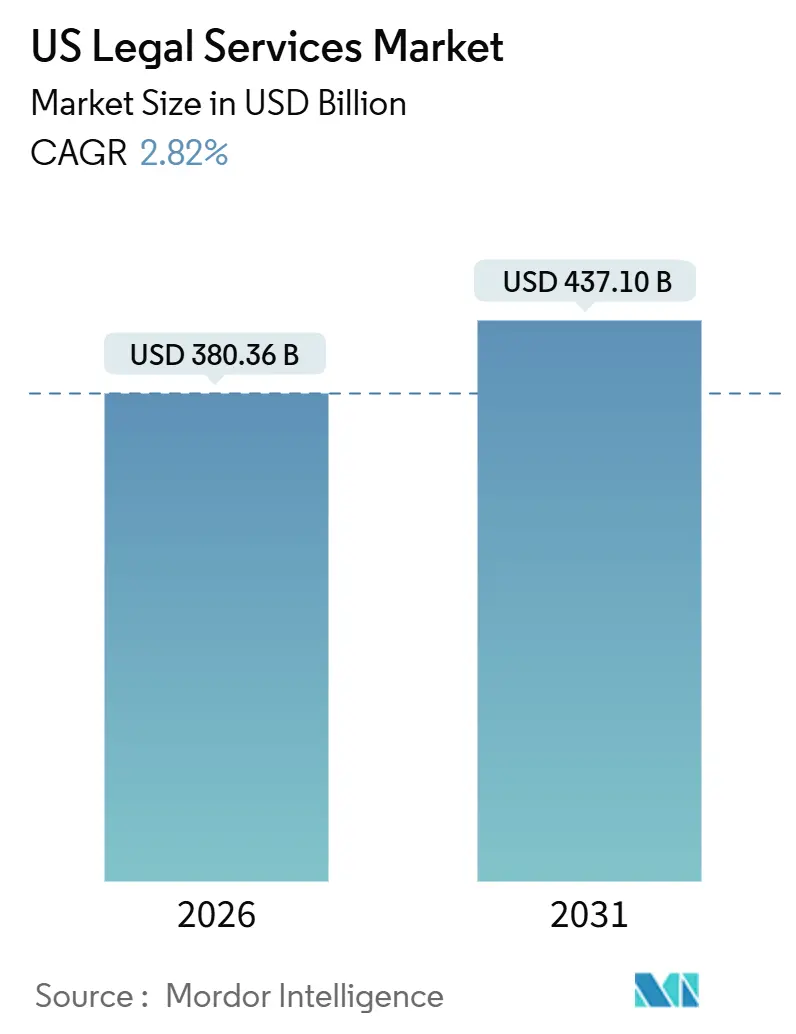

| Market Size (2026) | USD 380.36 Billion |

| Market Size (2031) | USD 437.10 Billion |

| Growth Rate (2026 - 2031) | 2.82% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Legal Services Market Analysis by Mordor Intelligence

The United States legal services market size is USD 380.36 billion in 2026 and is projected to reach USD 437.10 billion by 2031, reflecting a 2.82% CAGR through the forecast period. Growth in the United States legal services market is shaped by competing forces that include the shift toward subscription-based models, the buildup of in-house teams, and deepening demand for counsel on complex transactions and disputes. Corporate clients are pushing for outcome-based pricing and digital convenience while reserving premium billable hours for high-stakes matters that require specialized expertise. Alternative Legal Service Providers offer cost efficiency for standardized tasks, creating a complementary layer for e-discovery, document review, and contract support. The surge in fully digital service delivery and broader adoption of remote legal workflows is shifting how firms attract and retain clients in the United States legal services market.

Key Report Takeaways

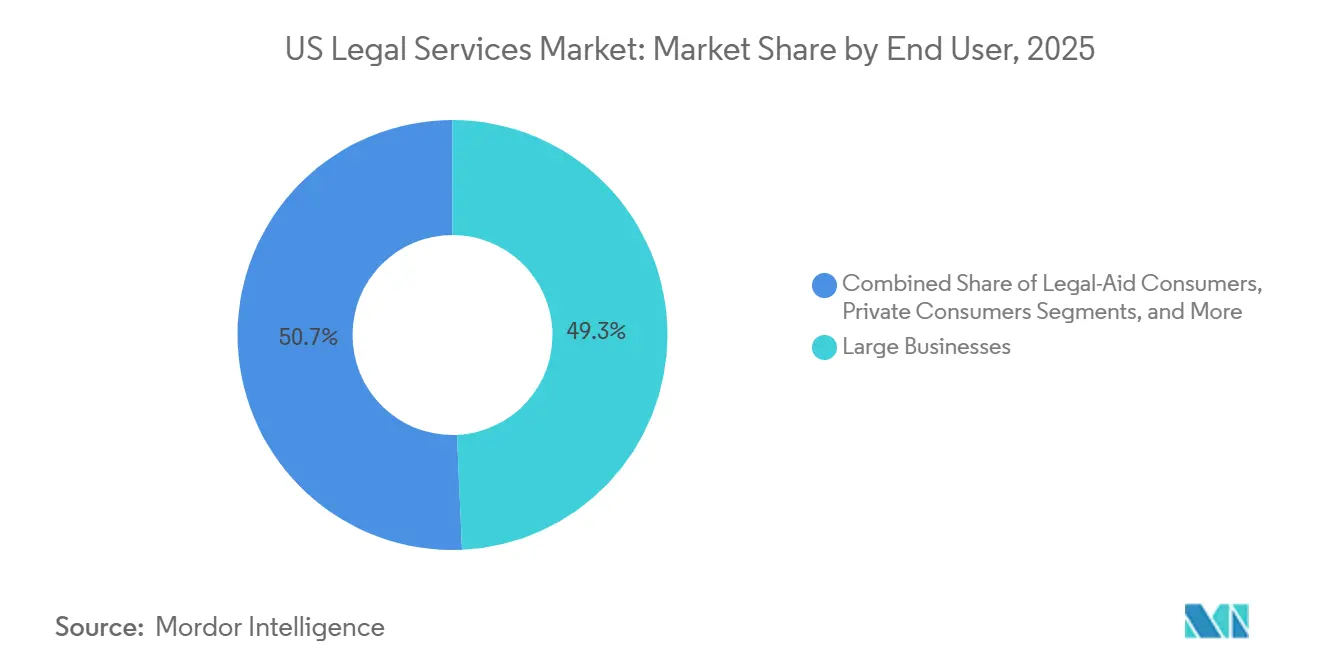

- By end-user, Large Businesses led with 49.31% of the United States legal services market share in 2025, while SMEs are projected to record the highest growth with a 3.61% CAGR through 2031.

- By application, Corporate, Financial, and Commercial Law held 43.52% of the United States legal services market share in 2025, and Other Applications are forecast to expand at a 4.57% CAGR within the United States legal services market size through 2031.

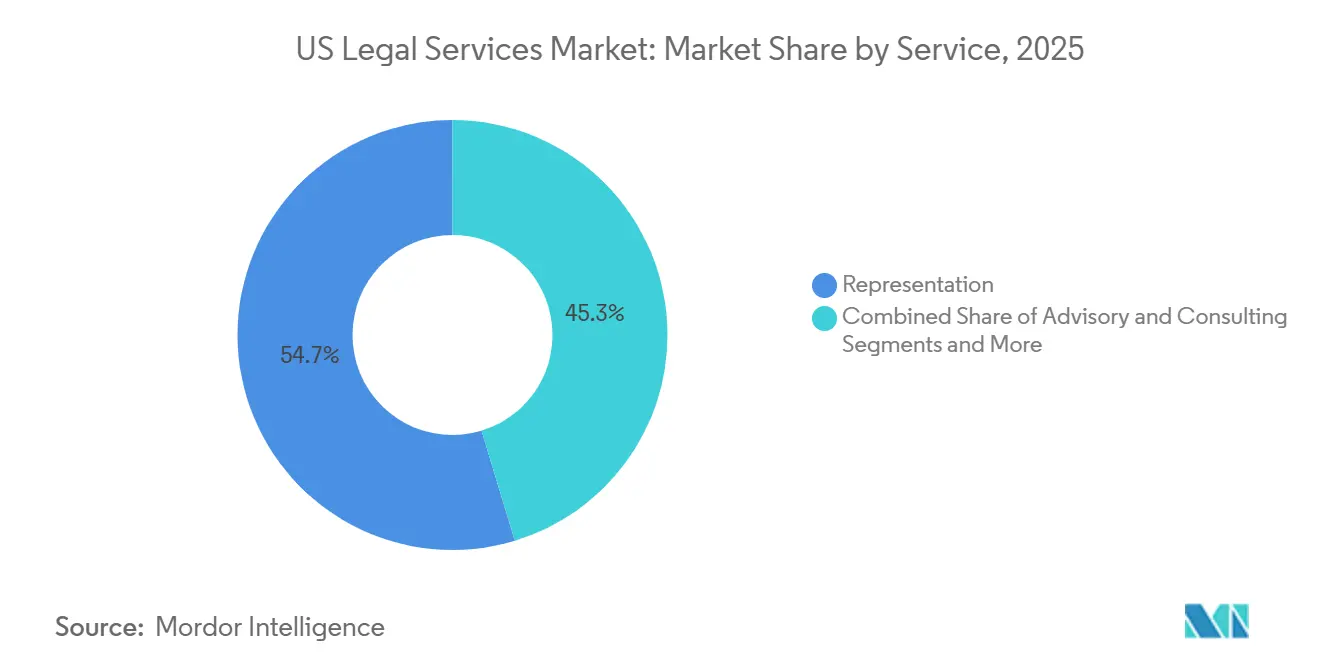

- By service, Representation captured 54.66% of the United States legal services market share in 2025, while Legal Research and Support Services are projected to post the fastest growth at a 4.23% CAGR within the United States legal services market.

- By mode of delivery, Traditional In-Person accounted for 70.42% of the United States legal services market share in 2025, while Fully Digital or Virtual delivery is projected to grow at a 6.13% CAGR within the United States legal services market.

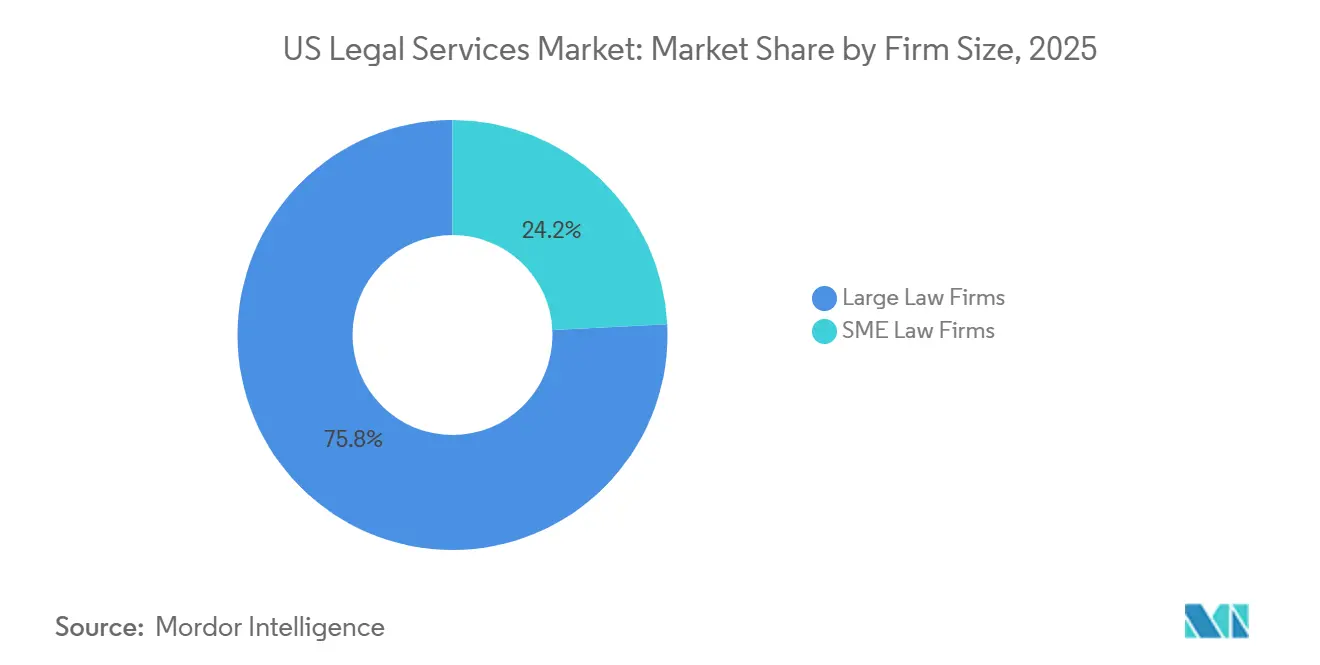

- By firm size, Large Law Firms held 75.77% of the United States legal services market share in 2025, and SME Law Firms are projected to grow at a 4.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Legal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first consumer behavior is driving DIY and unbundled legal demand | +0.6% | Global, with tech-forward states (California, Texas, Arizona) leading adoption | Medium term (2-4 years) |

| Corporate demand for ESG-linked legal advisory & compliance | +0.7% | National, with early gains in California and New York, and concentrated around Fortune 500 headquarters | Long term (≥ 4 years) |

| Near-shoring of routine work to lower-cost US states | +0.4% | Midwest and Southern states (Texas, North Carolina, Tennessee), with spillover to smaller Sunbelt metros | Medium term (2-4 years) |

| AI-powered contract analytics reducing turnaround time | +0.8% | Global adoption, highest penetration in large firms (51+ lawyers), and corporate law departments | Short term (≤ 2 years) |

| Rise of subscription-based "legal-as-a-service" models | +0.3% | National, particularly benefiting SME and consumer segments lacking traditional legal access | Medium term (2-4 years) |

| Regulatory Complexity and Litigation Risk from Evolving Data Privacy & Cybersecurity Laws | +0.5% | National, with outsized impact in California (CCPA/CPRA), Virginia, Colorado, and states adopting sector-specific privacy regimes; spillover demand from multinational clients | Short to medium term (1-3 years) |

| Source: Mordor Intelligence | |||

Digital-First Consumer Behaviour Driving DIY and Unbundled Legal Demand

Digital-first client behavior is expanding accessible entry points for legal assistance as consumers increasingly compare providers across online channels and prioritize speed, transparency, and predictable costs. The ABA’s Task Force on Law and Artificial Intelligence highlights that AI’s growing integration into legal practice, particularly in document drafting and other routine tasks, is reshaping expectations around legal service delivery, increasing consumer comfort with self-service tools, and accelerating demand for do-it-yourself and unbundled legal offerings [1]American Bar Association, “Task Force on Law and Artificial Intelligence,” American Bar Association, americanbar.org. This shift is already evident in market performance, with LegalZoom reporting Q1 2025 revenue of USD 183.1 million and a subscriber base of 1.92 million, underscoring the commercial traction of platforms that bundle filings and document generation for small businesses and entrepreneurs[2]LegalZoom, “LegalZoom Reports Strong First Quarter 2025 Financial Results,” LegalZoom Investor Relations, investors.legalzoom.com. At the same time, AI-enabled automation of low-complexity work is compressing traditional revenue streams that historically subsidized broader firm activities, prompting new pricing and delivery models. Subscription-based “legal-as-a-service” offerings with low monthly fees and transparent add-on pricing are converting latent demand from middle-income consumers who have traditionally deferred legal spend. Public polling by the National Center for State Courts further indicates widespread concern over unequal access to justice, encouraging regulators and bar associations to cautiously accommodate non-traditional delivery channels.

Corporate Demand for ESG-Linked Legal Advisory & Compliance

Regulatory and investor-driven ESG requirements are generating sustained demand for legal advisory and compliance services across the United States legal services market. California’s SB 253 mandates large companies operating in the state to disclose Scope 1 and Scope 2 emissions by 2026, triggering immediate legal work related to emissions accounting, governance frameworks, and assurance readiness. At the federal level, the introduction of a methane emissions charge for qualifying oil and gas operators is increasing the need for compliance planning, risk mitigation, and enforcement defense. In parallel, the rollout of new disclosure regimes in international markets such as Australia and Spain is pushing multinational companies to harmonize ESG reporting across jurisdictions, often requiring legal coordination to align data, attestations, and audit processes. Despite evolving federal policy signals, investor-led diligence, transaction structuring, and financing requirements continue to underpin ESG-related legal mandates, particularly in project finance and private equity.

Near-Shoring of Routine Work to Lower-Cost US States

Routine legal activities such as document review, e-discovery, and contract abstraction are increasingly being shifted from high-cost coastal markets to lower-cost regional hubs, including Austin, Raleigh, and Nashville. This domestic near-shoring strategy allows firms to preserve data sovereignty and quality control while reducing delivery costs for standardized work. Lower living expenses in these destination metros enable providers to offer more competitive pricing to corporate clients without compromising supervision or compliance standards. Industry observations indicate that midsize firms and Am Law Second Hundred practices have captured a growing share of transactional work as price-sensitive clients rebalance routine mandates away from higher-cost providers. In parallel, local bar associations and academic institutions are strengthening paralegal and legal operations talent pipelines to support this geographic shift. Collectively, these trends enhance efficiency within the United States legal services market by freeing higher-cost coastal talent to focus on strategic advisory work while relocating repeatable tasks to more cost-effective domestic locations.

Rise of Subscription-Based "Legal-as-a-Service" Models

Subscription-based legal services are gaining significant traction by offering predictable, transparent pricing that appeals to cost-conscious clients, particularly entrepreneurs and small businesses. Providers structure plans with clearly defined monthly fees and per-service charges, often leveraging modern workflows and AI-powered automation to deliver counsel efficiently while maintaining profitability. Small-business subscriptions that bundle regular access to legal advice across HR, contracts, and risk management demonstrate recurring engagements can replace traditional episodic matters. Firms adopting flat-fee pricing report higher levels of AI adoption, reflecting strong alignment between automation and predictable service delivery. Large-scale platforms illustrate robust consumer demand for packaged offerings that integrate filings, templates, and ongoing compliance support. Adoption is particularly pronounced among solo practitioners and small to mid-sized firms, while larger partnerships often retain traditional billable-hour structures that can slow flat-fee expansion. The United States Bureau of Labor Statistics projects employment of lawyers to grow by approximately 4% from 2024 to 2034, reflecting continued demand for legal services even as routine tasks are automated or outsourced, enabling alternative delivery models such as subscription-based legal services.[3]United States Bureau of Labor Statistics, “Lawyers,” Occupational Outlook Handbook

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing in-house legal teams at Fortune 1000 firms | -0.6% | National, concentrated in metros hosting Fortune 500 headquarters (NYC, Silicon Valley, Chicago) | Long term (≥ 4 years) |

| Persistent talent shortage is inflating associate salaries | -0.4% | National, most acute in high-cost metros (NYC, San Francisco, Boston, DC) | Medium term (2-4 years) |

| State-level regulatory barriers to non-law-firm ownership | -0.2% | 48 jurisdictions uphold bans; Arizona, Utah, and DC exceptions create a regional competitive advantage | Long term (≥ 4 years) |

| Cybersecurity and confidentiality concerns around cloud tools | -0.3% | National, particularly firms handling CUI, healthcare (HIPAA), or cross-border data transfers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing In-House Legal Teams at Fortune 1000 Firms

Corporate legal departments are increasingly shifting work in-house, aiming to optimize internal resources while managing outside counsel spending. Larger enterprises benefit from economies of scale, often allocating a smaller share of revenue to external legal services compared to mid-market peers. In many organizations, internal personnel costs can surpass expenditures on outside counsel, prompting a rebalancing of budgets and priorities. As alternative legal service providers (ALSPs) gain adoption, legal leaders continue to leverage panel diversification and cost-control strategies, reallocating standardized or routine tasks from traditional law firms to a mix of in-house teams and specialized providers. These dynamics reinforce a multitrack procurement model in the United States legal services market, where complex matters remain with top-tier firms while routine work is concentrated in lower-cost channels.

Persistent Talent Shortage Inflating Associate Salaries

Ongoing talent scarcity is creating challenges for legal hiring as demand in key practice areas remains strong and recruitment cycles lengthen. Many firms, including prominent litigation boutiques and regional practices, have increased first-year associate salaries to reflect workload intensity and early trial exposure, indicating that compensation pressure extends beyond the largest firms. The United States Bureau of Labor Statistics projects substantial annual lawyer openings, sustaining competition for junior and mid-level hires. To retain talent, firms are investing in mentorship, trial rotations, and peer support programs, particularly in litigation practices where early courtroom experience can be limited. These factors increase cost structures for providers and can constrain capacity in high-demand areas, contributing to ongoing wage pressure and selective price increases in the United States legal services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: SMEs Propel Affordable Access Models

Large Businesses accounted for 49.31% in 2025, while SMEs are projected to grow at a 3.61% CAGR between 2026 and 2031, making SMEs the fastest-growing client segment in the United States legal services market. Private consumers and legal-aid clients continue to drive meaningful volumes in areas such as family law, probate, and personal-injury services, where flat fees and online portals reduce barriers to entry. Programs like the ABA’s Free Legal Answers provide scalable access across 48 states and the Virgin Islands, raising awareness among consumer groups that have historically underutilized legal services. Government and public sector clients maintain steady demand across administrative law, enforcement defense, and regulatory matters, reflecting the ongoing need for specialized counsel. Corporate legal teams continue to balance internal capacity with external experts, reserving top-tier counsel for high-stakes disputes and transformational transactions.

SMEs benefit from bundled packages that integrate contract review, HR guidance, and risk management at fixed monthly rates, allowing businesses without in-house legal teams to access reliable support. Corporate law departments have reported rising matter volumes while maintaining flat budgets, creating pressure to separate high-value external work from standardized internal tasks. Legal aid and pro bono initiatives are increasingly leveraging online triage and volunteer matching platforms, expanding access for civil matters beyond traditional law firm engagements. The shift toward subscription and digital-first models aligns with evolving compliance needs and budget discipline among small enterprises. Collectively, these dynamics are expanding the client mix and reinforcing lower-friction service adoption across the United States legal services market.

By Application: Emerging Specialties Outpace Legacy Practices

Corporate, Financial and Commercial Law held 43.52% of overall applications in 2025 and continues to reflect concentration in major financial and regulatory hubs such as New York, Los Angeles, Chicago, and Washington, D.C., within the United States legal services market. Established categories such as personal injury, property, family, employment, and criminal law remain active and are supported by workflows that streamline filings, disclosures, and case management. Broader adoption of technology in these practices helps smaller firms manage higher volumes while maintaining standards of review and client communication. New coverage categories introduced by major rankings in 2025, including AI and Corporate Governance, signal greater demand for specialized counsel as novel regulatory domains mature. These shifts help reposition workload from legacy transactional areas toward forward-looking compliance and risk advisory in the United States legal services market.

Other Applications are projected to expand at a 4.57% CAGR through 2031, led by demand for cybersecurity oversight, AI liability analysis, and evolving data privacy requirements. The Federal Trade Commission updated COPPA rules in 2025 to require greater transparency and impose tighter data-sharing limits, which increased advisory demand for platforms that serve minors or collect sensitive data. The United States Department of Justice also finalized its rule on bulk data transactions in early 2025 that restricts data flows to certain jurisdictions, which now appears in cross-border diligence and contract negotiations. New practice profiles around AI, governance, and auditor liability reflect how regulatory complexity drives new buyer needs, rather than mere re-labeling of legacy commercial work. This mix of requirements supports a selective reallocation of engagement hours toward emerging domains in the United States legal services market.

By Service: Research & Support Accelerate Through AI

Representation services captured a 54.66% share in 2025 as courtroom advocacy, depositions, arbitrations, and mediations continue to require high-touch advisory and persuasion in the United States legal services market. Technology is increasingly used to support these activities, assisting with case-law summarization, exhibit management, and witness preparation while maintaining attorney oversight of strategy and outcomes. Advisory and consulting offerings, including transactional structuring, legal opinions, and regulatory interpretation, are seeing growth as corporate clients adopt capped or fixed-fee arrangements to manage costs and align incentives. Notarial services, though specialized, benefit from the expansion of remote online notarization, reducing time-to-close for eligible transactions. Across these services, technology supplements attorney work without diminishing accountability for client outcomes, reinforcing the high-value, professional nature of representation and advisory services.

Legal Research and Support Services are projected to grow at a 4.23% CAGR, the fastest rate among service categories, due to AI-enabled contract review, e-discovery, and regulatory-change monitoring. Industry surveys in 2026 show that a growing share of firms adopted AI tools in 2025 and plan further increases, especially for transcript summarization, deposition exhibit handling, and trial preparation. Contract lifecycle management and review platforms continue to shorten cycle times and redirect attorney time to higher-value tasks, with legal professionals reporting tangible business benefits from these tools. Professional guidance on AI use from bar associations and courts is expanding as providers operationalize compliance, confidentiality, and billing standards in an AI-infused workflow. These developments reinforce ongoing investment in research and support capabilities within the United States legal services market.

By Mode of Delivery: Fully Digital Channels Surge

Traditional In-Person delivery accounted for a 70.42% share in 2025 as clients continued to prioritize face-to-face interactions for high-stakes litigation, complex negotiations, and sensitive family-law matters in the United States legal services market. Hybrid work arrangements are now widespread, with legal professionals splitting time between office and remote settings as firms adjust staffing, culture, and workflows to maintain flexibility. Cloud-based technologies, including video conferencing, e-signatures, and e-filing, support remote collaboration while preserving in-person engagement for critical moments. Mature client portals allow firms to handle triage, updates, and routine interactions online, reserving direct meetings for matters that deliver the highest client value. This approach enhances access to legal services while reducing friction for routine tasks.

Digital clinics and subscription platforms highlight the growing adoption of fully virtual delivery models. Programs like the ABA’s Free Legal Answers provide virtual legal support across 48 states and the Virgin Islands, connecting clients with licensed attorneys for civil matters. Consumer-facing platforms such as LegalZoom and Rocket Lawyer offer subscription-based access to document templates and lawyer Q&A, appealing to budget-conscious users. Regulatory sandboxes in states like Arizona, Utah, and Washington allow limited non-lawyer ownership, expanding service capacity under defined oversight. Privacy and data protection requirements, including state and federal rules for minors’ information, necessitate encryption, auditing, and vendor diligence, supporting a measured and secure expansion of virtual channels in the United States legal services market.

By Firm Size: SME Firms Leapfrog Through Technology

Large Law Firms held 75.77% share in 2025, supported by deep subject-matter expertise, global footprints, and brand strength that wins mandates for complex transactions and high-stakes disputes in the United States legal services market. Concentrations of Am Law 200 attorneys in major cities, particularly New York and Washington, D.C., provide a professional base that supports premium practices. These firms invest heavily in knowledge management, cross-border capabilities, and practice-specific technology to enhance collaboration and efficiency at scale. Clients rely on these platforms for critical, high-value matters while diversifying their legal panels for routine or standardized work. This results in a barbell distribution of legal services, with premium work concentrated at large firms and standardized matters spread across alternative channels.

SME Law Firms are projected to grow at a 4.01% CAGR domestically as lightweight tech stacks, lower overhead, and process redesign enable competitive pricing without compromising quality. Smaller practices can implement AI-native tools quickly and standardize workflows across intake, research, and drafting, which helps them win recurring work from small and midsize businesses. Subscription offerings and flat-fee scoping are especially aligned with SME client expectations for price certainty and responsiveness. As corporate buyers expand their use of ALSPs and internal teams for standardized work, SME firms that specialize in advisory and dispute tactics for local markets are positioned to benefit. This dynamic supports a more balanced competitive field within the United States legal services market.

Geography Analysis

The Northeast region dominates the United States legal services market, accounting for 32.15% of total market share, driven by its concentration of major financial, corporate, and regulatory hubs such as New York City, Boston, and Washington, D.C. The region hosts a high density of large law firms, multinational corporations, investment banks, and federal institutions, which generate consistent demand for complex corporate, litigation, and regulatory legal services. Its mature legal infrastructure, strong client base, and presence of global headquarters reinforce its continued market leadership.

At the same time, growth markets such as Texas, Florida, North Carolina, and Tennessee are increasing their share of legal activity. Firms and corporate clients are drawn to these regions by expanding talent pools, lower housing costs, and business-friendly environments. Texas has emerged as a major legal hub, with national firms expanding to serve energy, private equity, and technology clients. Florida’s large attorney population and favorable cost-of-living dynamics support associate retention and lateral hiring. North Carolina and Tennessee have benefited from near-shoring trends in e-discovery and contract review, supported by local legal ecosystems that maintain attorney oversight.

In contrast, the Southeast region is projected to be the fastest-growing market, with a CAGR of 4.21% over the next five years. Rapid population growth, business relocations, rising startup activity, and expanding real estate and infrastructure development in states such as Florida, Georgia, and North Carolina are driving demand for legal services. Lower operating costs and increased corporate migration from higher-cost regions further support accelerated growth.

Competitive Landscape

The United States legal services market features a fragmented landscape where large law firms and SME providers coexist, with brand, scale, and specialized expertise driving premium engagements while cost-effective options expand for standardized tasks. Corporate legal departments increasingly rely on alternative legal service providers (ALSPs) for routine work, outsourcing defined assignments to lower-cost providers as part of panel diversification strategies. ALSPs have reached substantial revenue levels, reflecting sustained growth and growing client willingness to prioritize value over brand for repeatable services. Mergers among large and mid-sized firms continue, expanding geographic reach and adding complementary capabilities to manage complex cross-border transactions and investigations. These strategies also support multinational in-house teams that prefer a smaller number of external providers per matter.

Transatlantic combinations are growing as firms seek scale in intellectual property, finance, and global disputes to provide coordinated counsel across North America, Europe, and Asia. Recent mergers have positioned entities among the top firms by revenue and headcount in the United States and the United Kingdom. Law firms with structured AI strategies report faster returns and measurable workflow benefits compared with those adopting tools without formal programs. Professional guidance on AI usage and billing is shaping how firms price time saved through automation, with ethics opinions clarifying expectations for reasonableness and client value. These trends illustrate how investment in capabilities and policy alignment influence competitive positioning within the market.

Regulatory developments are reshaping competition, as seen with Arizona’s approval of an Alternative Business Structure for KPMG Law United States, allowing non-lawyer ownership under defined safeguards[4]Maryland State Bar Association, “KPMG Law US ABS Approval,” MSBA, msba.org. Corporate buyers continue to balance traditional law firms, ALSPs, and internal teams to match task complexity with cost and capability, often engaging specialized providers for document review, contract abstraction, and litigation support. The introduction of agentic AI tools will differentiate providers able to integrate automation without compromising quality or client oversight. Technology-enabled service models are driving experimentation with workflow design, efficiency, and value-based pricing.

United States Legal Services Industry Leaders

Latham & Watkins LLP

Kirkland Kirkland & Ellis LLP& Ellis LLP

Skadden, Arps, Slate, Meagher & Flom LLP

Cravath, Swaine & Moore LLP

Wachtell, Lipton, Rosen & Katz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Winston & Strawn and Taylor Wessing’s UK-led business announced plans to combine into a new transatlantic law firm named Winston Taylor, uniting more than 1,400 lawyers across the United States, United Kingdom, and Europe with expanded capabilities in major litigation, critical transactions, and strategic intellectual property, with completion expected in May 2026 pending partner approvals.

- December 2025: Winston & Strawn and Taylor Wessing announced they expect to merge in May 2026, forming a transatlantic law firm named Winston Taylor with more than 1,400 lawyers and roughly USD 1.75 billion in combined annual revenue, expanding integrated counsel across the United States, United Kingdom, and Europe.

- November 2025: Thomson Reuters unveiled new agentic AI capabilities for CoCounsel Legal, including workflows that can independently execute complex multi‑step legal tasks, customizable workflow plans for practice groups, and bulk document review of up to 10,000 documents, marking a significant advancement in applying AI to routine and sophisticated legal work.

- June 2025: Partners at McDermott Will & Emery and Schulte Roth & Zabel voted to merge, creating a new firm named McDermott Will & Schulte with about 1,750 lawyers across more than 20 offices globally, combining their complementary strengths in healthcare, private capital, and other key practices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States legal services market as all fee-based activities in which licensed attorneys or regulated alternative legal service providers represent, advise, or support private individuals, businesses, and governmental bodies across every branch of law. Revenue streams captured span courtroom representation, transactional advice, notarial work, legal research, discovery support, and related subscription or project fees.

Scope exclusion, internal spend: Fees paid to in-house corporate counsel and pro-bono services that generate no external invoices are not counted.

Segmentation Overview

- By End-User

- Legal-Aid Consumers

- Private Consumers

- SMEs

- Charities and NGOs

- Large Businesses

- Government and Public Sector

- By Application

- Corporate, Financial and Commercial Law

- Personal Injury

- Commercial and Residential Property

- Wills, Trusts and Probate

- Family Law

- Employment Law

- Criminal Law

- Other Applications

- By Service

- Representation

- Advisory and Consulting

- Notarial Services

- Legal Research and Support Services

- By Mode of Delivery

- Traditional In-Person

- Hybrid (Blended)

- Fully Digital / Virtual

- By Firm Size

- Large Law Firms

- SME Law Firms

- By Geography

- Northeast

- Southeast

- Midwest

- Southwest

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview managing partners, corporate legal-ops heads, staff counsel at insurers, and technology vendors across all major circuits to validate utilization rates, alternative fee adoption, and expected hourly rate progression. Structured surveys with small and midsize firms in the Midwest and Sunbelt fill geographic gaps and clarify hybrid delivery uptake.

Desk Research

We begin with publicly available, high-credibility datasets such as the Bureau of Labor Statistics Occupational Employment Survey, Administrative Office of the U.S. Courts filing statistics, U.S. Census Service Annual Survey, IRS SOI legal-entity data, and American Bar Association practitioner counts. Industry context is enriched with court fee schedules, SEC deal volumes, and state bar admission trends. For firm-level revenue splits and practice area mix, analysts extract signals from D&B Hoovers, Dow Jones Factiva, and filings lodged by publicly traded legal networks. These sources anchor baseline attorney counts, average billable rates, and workload indicators that feed the model. The examples listed are illustrative; a wider universe of secondary sources was reviewed for completeness and cross-checks.

Market-Sizing & Forecasting

A top-down build starts with attorney workforce and mean billable hours times realized hourly rates, reconstructed from BLS counts, ABA head counts, and Thomson Reuters utilization benchmarks, which are then aligned with Federal Court filing growth. Select bottom-up checks, sampled revenue disclosures from AmLaw-ranked firms, ALSP invoice analyses, and e-discovery platform throughput reconcile any variance before finalizing totals. Key variables tracked include median hourly rate inflation, case-filing growth, corporate deal count, and penetration of subscription legal plans. Forecasts run a multivariate regression with ARIMA smoothing on these drivers, while scenario inputs from primary interviews guide conservative and aggressive bounds. Gaps in micro-segment data are bridged by proxy indicators (for example, patent filings for IP law revenue).

Data Validation & Update Cycle

Outputs undergo variance screening versus third-party demand indices and quarterly earnings trends. Senior reviewers re-run anomaly filters, and any deviation beyond pre-set thresholds triggers re-contact of sources. We refresh the dataset annually and push interim updates after material regulatory changes or outsized M&A waves before final client delivery.

Why Mordor's US Legal Services Baseline Rings True

Published market values often differ because firms pick dissimilar revenue pools, pricing assumptions, and refresh cadences.

Key gap drivers arise when some studies fold in in-house counsel budgets, others drop alternative providers, or they translate billable rate growth using outdated currency and inflation factors. Mordor's disciplined scope, annual refresh, and dual-proof modelling temper these extremes, producing a centered view decision-makers can lean on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 369.93 B (2025) | Mordor Intelligence | - |

| USD 408.42 B (2025) | Regional Consultancy A | Includes in-house legal department spend and litigation funding flows, inflating totals |

| USD 304.93 B (2025) | Trade Journal B | Excludes alternative legal service providers and technology-enabled document services, suppressing value |

The comparison shows how scope breadth and variable selection swing figures by tens of billions, whereas Mordor's balanced, transparent build rests on clearly traceable drivers, giving stakeholders a dependable baseline for planning.

Key Questions Answered in the Report

What is the current size and growth outlook for the United States legal services market?

The United States legal services market size is USD 380.36 billion in 2026 and is projected to reach USD 437.10 billion by 2031 at a 2.82% CAGR, reflecting steady but measured expansion across client segments and delivery models.

Which client segment is growing fastest in the United States legal services market?

SMEs are the fastest-growing end-user segment, with a projected 3.61% CAGR to 2031 due to demand for predictable subscription offerings, digital compliance support, and on-demand advisory.

Which application areas are expected to grow fastest through 2031?

Other Applications, including cybersecurity counsel, ESG governance, and AI liability, are projected to expand at a 4.57% CAGR as new rules and assurance needs drive advisory demand.

Which service category is growing fastest in the United States legal services market?

Legal Research and Support Services are projected to grow at a 4.23% CAGR, supported by AI-enabled document review, e-discovery, and regulatory-change monitoring that reduce cycle times while maintaining attorney oversight.

How is delivery shifting between in-person and virtual channels?

Traditional In-Person held a 70.42% share in 2025, but Fully Digital or Virtual channels are projected to grow at a 6.13% CAGR through 2031, due to high adoption of cloud tools, e-signatures, and e-filing.

How are firm-size dynamics evolving among providers?

Large Law Firms held a 75.77% share in 2025 for complex mandates, while SME Law Firms are projected to grow at a 4.01% CAGR, using lightweight tech stacks and flat-fee offerings to compete effectively.

Page last updated on: