Financial Advisory Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

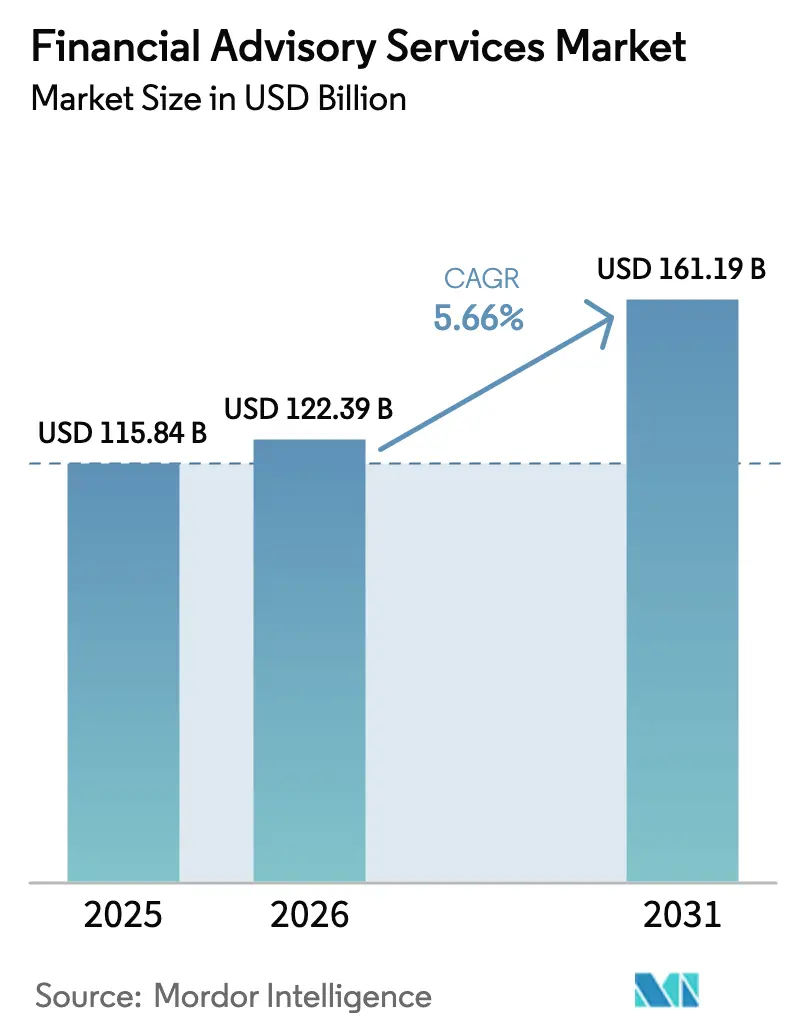

| Market Size (2026) | USD 122.39 Billion |

| Market Size (2031) | USD 161.19 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

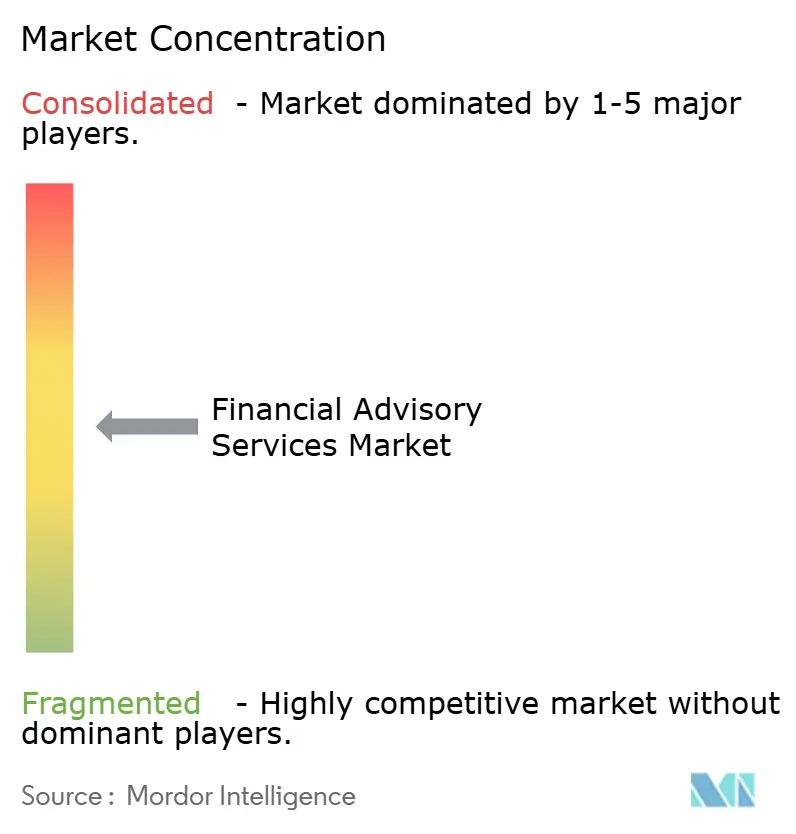

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Financial Advisory Services Market Analysis by Mordor Intelligence

The financial advisory services market size is expected to grow from USD 115.84 billion in 2025 to USD 122.39 billion in 2026 and is forecast to reach USD 161.19 billion by 2031 at 5.66% CAGR over 2026-2031. Healthy expansion is tied to rapid digitalization, tighter regulatory oversight, and shifting client expectations that reward transparent fee-based relationships. Artificial-intelligence tools are delivering hyper-personalized advice that lifts client engagement, while low-cost robo platforms continue to democratize professional portfolio management. New hybrid delivery models that connect human judgment with algorithmic efficiency are gaining momentum, particularly among affluent millennials and Gen Z heirs. Advisory firms that successfully integrate technology, address evolving ESG disclosure rules, and manage a shrinking talent pool are positioned to capture outsized gains across the financial advisory services market.

Key Report Takeaways

- By service type, investment advisory led with 38.25% share of the global financial advisory services market in 2025; it is expected to expand at a 7.29% CAGR through 2031.

- By organization size, large enterprises commanded 63.10% of the global financial advisory services market share in 2025, while SMEs are projected to grow the fastest at 6.59% CAGR through 2031.

- By industry vertical, BFSI held 35.75% of the global financial advisory services market in 2025; healthcare and pharmaceuticals are expected to be the quickest-growing verticals at 6.86% CAGR through 2031.

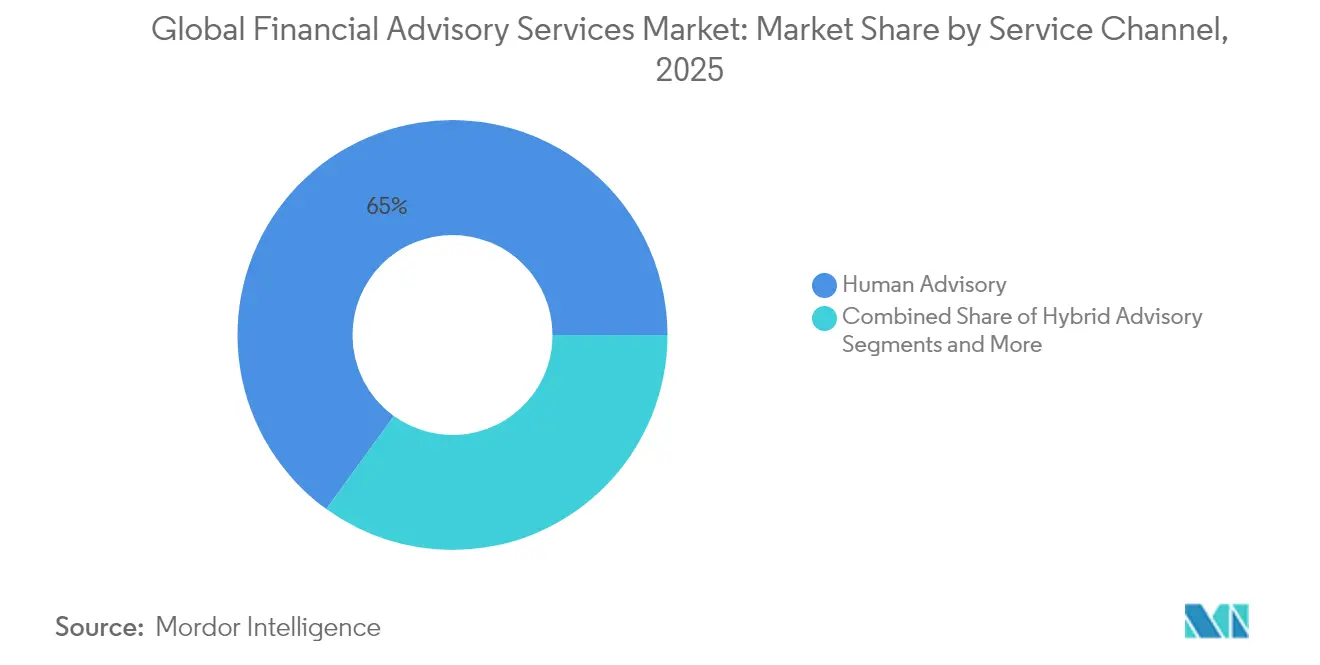

- By service channel, human advisory represented 65.02% of the global financial advisory services market share in 2025, and robo advisory is projected to register the highest 16.95% CAGR through 2031.

- By delivery mode, on-site consulting accounted for 73.40% of the global financial advisory services market size in 2025; remote and virtual consulting is expected to rise at a 10.45% CAGR through 2031.

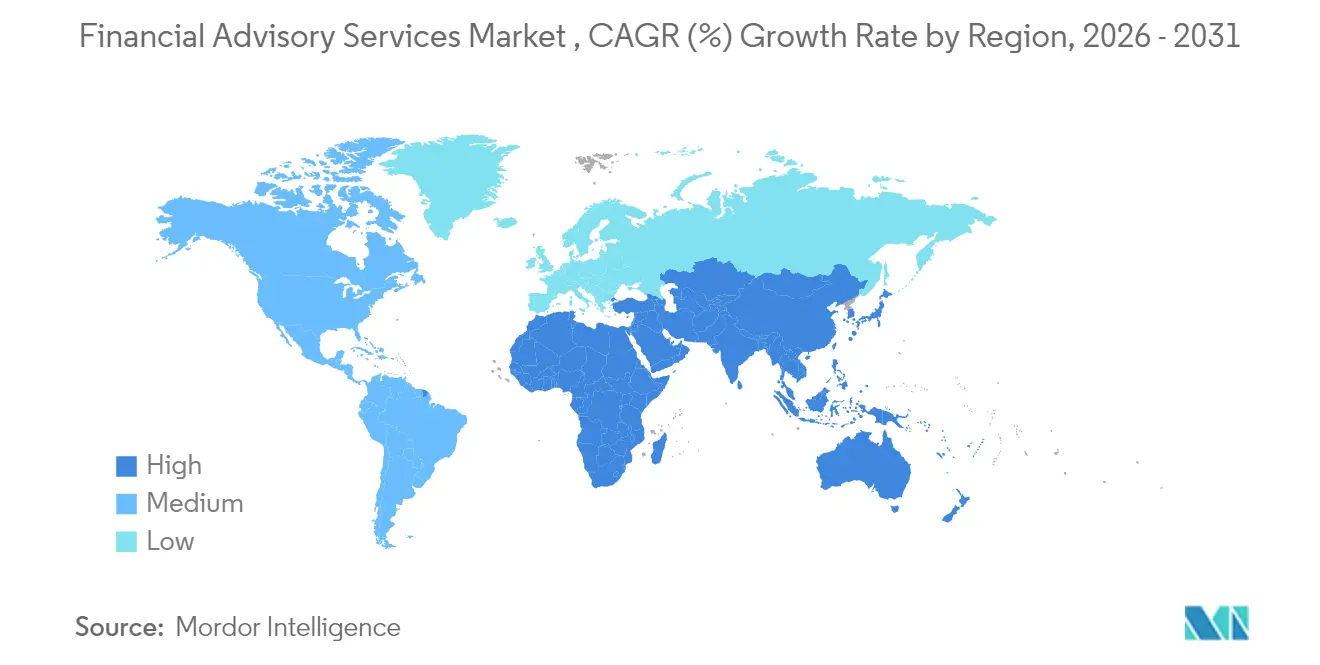

- By region, North America retained 39.95% share of the global financial advisory services market in 2025; Asia-Pacific is forecasted to post the strongest 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Financial Advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled hyper-personalized advice uptake | +1.2% | Global, early adoption in North America & APAC | Medium term (2-4 years) |

| Shift from commission to fee-based models | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Democratization via low-cost robo-platforms | +1.5% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Generational wealth transfer to digital heirs | +0.9% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Reg-tech lowering compliance burden | +0.6% | Global, regulatory-heavy markets first | Medium term (2-4 years) |

| Sovereign wealth funds outsourcing mandates | +0.4% | Middle East, APAC, selective global impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Hyper-Personalized Advice Uptake

Artificial intelligence is reshaping how advisory firms collect, process, and apply client data, creating bespoke portfolios that adapt in real time to shifting life events, tax regimes, and market conditions. Federal Reserve surveys put AI penetration among financial-services workers at 20%–40%, with year-on-year growth reaching up to 145%[1]Board of Governors of the Federal Reserve System, “Artificial Intelligence Adoption in Financial Services,” federalreserve.gov. Morgan Stanley’s wealth arm, stewarding more than USD 4.2 trillion, relies on proprietary AI research to sharpen asset allocation and deepen engagement. Where human advisers once sifted spreadsheets, machine-learning engines now scan millions of data points in seconds, freeing professionals to focus on complex planning. Adoption is particularly strong in digitally mature Asia-Pacific wealth hubs, where clients consider advanced analytics a hygiene factor rather than a differentiator. Firms that master AI-driven personalization earn higher wallet share and more durable client stickiness.

Shift From Commission to Fee-Based Models

Regulators and clients are accelerating the pivot toward fee transparency, reducing conflicts embedded in product commissions. T. Rowe Price already manages around USD 1.5 trillion on fee-aligned mandates, proving the commercial viability of asset-based charging[2]T. Rowe Price Associates, “Form ADV Part 2A,” troweprice.com. The Consumer Financial Protection Bureau has intensified its crackdown on opaque charges, labelling overdraft fees and similar levies “junk fees”. Europe’s MiFID II framework, which ring-fences advice fees, offers a blueprint now spreading to other regions. As firms pivot, stable recurring revenue streams improve valuation multiples, yet they also expose advisers to margin pressure if investment performance lags. Successful operators couple fee-based portfolios with high-touch planning, tax, and retirement strategies that reinforce perceived value.

Democratization via Low-Cost Robo-Platforms

Robo-advisors slash entry barriers by automating portfolio construction, rebalancing, and tax-loss harvesting at fractions of traditional adviser pricing. Personalized target-date funds represent the next evolution, with providers such as Capital Group and PIMCO tailoring allocations to income and contribution rates while keeping costs between fund-of-funds and bespoke mandates. Bank of America research shows young adults juggling housing costs and student debt still prioritize digital investment apps and “buy now, pay later” spending tools[3]Bank of America Institute, “Consumer Checkpoint 2025,” bofainstitute.com. As mass-affluent cohorts grow, low-friction onboarding and intuitive mobile interfaces channel a new wave of assets toward robo platforms, forcing incumbent advisers to refine value propositions or face fee erosion.

Generational Wealth Transfer to Digital-Savvy Heirs

Roughly USD 84 trillion is set to flow from baby boomers to millennials and Gen Z over two decades. A report suggests that 44% of family offices will boost commercial property exposure while screening holdings against ESG metrics. Digital natives prize seamless experiences, real-time dashboards, and sustainable portfolios, prompting advisers to add impact-scoring tools and climate analytics. Asia-Pacific captures the trend’s sharpest edge, given its high smartphone penetration and rapid wealth creation. Hybrid models combining virtual servicing with periodic in-person coaching are emerging as the standard, retaining personal trust while meeting always-on digital expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advisor talent shortage & ageing workforce | -1.1% | Global, acute in developed markets | Short term (≤ 2 years) |

| Margin compression from passive wave | -0.7% | Global, strongest in developed markets | Medium term (2-4 years) |

| Cyber-security & data-privacy liabilities | -0.5% | Global, regulatory-heavy markets first | Short term (≤ 2 years) |

| ESG-greenwashing litigations | -0.3% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advisor Talent Shortage & Ageing Workforce

More than one-third of practicing advisers in North America and Western Europe are within a decade of retirement, creating a pipeline gap that constrains capacity and stresses service levels. Younger professionals gravitate toward technology or entrepreneurial roles offering flexible schedules and equity upside, leaving advisory firms scrambling to refresh ranks. Heightened regulatory complexity further raises entry barriers, demanding advanced credentials that require time and capital to acquire. In specialties such as estate planning, advisors with deep tax knowledge command premium compensation, escalating cost structures. Firms are responding with apprenticeship tracks, tuition reimbursement, and increased reliance on digital workflows that let senior advisers support a larger client base through junior staff.

Margin Compression from Passive Investing Wave

Passive funds, ETFs, and direct indexing are siphoning assets from high-fee active strategies, prompting clients to question adviser value. Morningstar data show aggregate fund fees sliding every year since 2015, a trend unlikely to reverse. As investment selection becomes commoditized, advisers pivot to planning, behavioral coaching, and tax optimization to defend fees. Yet scaling these holistic services requires tech investments and continual staff training, placing pressure on smaller firms. European regulators’ insistence on fee unbundling intensifies the squeeze, encouraging price competition that ripples into North America and Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Investment Advisory Extends Leadership

Investment advisory services captured the largest 38.25% slice of the financial advisory services market in 2025 and will propel overall growth with a 7.29% CAGR to 2031. This combination of scale and velocity underscores the client's appetite for portfolios that integrate planning, tax, and estate considerations within single adviser relationships. As assets migrate toward fee-based accounts, the financial advisory services market size for investment advisory is projected to widen in absolute dollars at a pace that outstrips other categories. Major deal counsel, notably Capital One’s USD 35 billion purchase of Discover Financial, spotlights how corporate finance teams lean on specialist advisers for valuation, structuring, and shareholder communications.

Across the wider service landscape, accounting and tax advisory services enjoy steady uptake as multijurisdictional reporting and ESG metrics create data-collection complexity. Digital-asset and succession-planning sub-segments, housed within “other services,” register niche but rising contributions. Competitive differentiation now hinges on bundling: firms marrying investment management with holistic planning see lower churn and stronger cross-selling. As technology automates many allocation tasks, advisers redeploy bandwidth to behavioral coaching that addresses client biases and emotional triggers during volatile markets.

By Organization Size: Enterprise Clout Meets SME Momentum

Large enterprises accounted for 63.10% of the financial advisory services market in 2025, reflecting entrenched relationships and complex balance-sheet requirements that demand bespoke advisory. Treasury optimization, debt structuring, and cross-border M&A ensure sticky mandates. However, the SME cohort, aided by digital onboarding and modular service bundles, is forecasted to expand at a 6.59% CAGR, increasing its share of the financial advisory services market size. Technology platforms lower ticket-size thresholds, allowing advisers to profitably serve family-owned manufacturers, tech startups, and professional partnerships that previously relied on in-house finance staffs or retail banks.

Many SMEs face regulatory burdens similar to large corporates—such as beneficial-ownership reporting and sustainability disclosures—yet lack specialized expertise. Cloud-based dashboards that consolidate cash-flow projections, tax calendars, and portfolio analytics empower owners to act swiftly. Leading advisers deploy AI chatbots to field routine queries, reserving human interaction for annual planning and transaction events. Geographic dispersion is widening; SMEs in Southeast Asia and Latin America increasingly seek US-dollar bond issuance advice, driving cross-border engagement.

By Industry Vertical: BFSI Dominance, Healthcare Acceleration

The BFSI sector retained 35.75% of the 2025 financial advisory services market share, anchored by bank treasury units, insurer general accounts, and asset-manager affiliates that rely on external advisers for capital optimization and regulatory insight. The segment benefits from continual capital adequacy rule changes and digital banking transformations that demand strategic advice. Meanwhile, healthcare and pharmaceuticals are forecasted to deliver a 6.86% CAGR, the fastest among all verticals, lifting their contribution to the financial advisory services market share by 2031. Drug-pricing reforms, clinical-trial funding needs, and intellectual-property monetization fuel demand for bespoke financial structuring.

Information technology and telecommunications also wield significant advisory budgets, especially for cross-border cloud-data-center financing and employee-stock-plan design. Manufacturing and retail sectors continue to lean on advisers for supply-chain funding and ESG-linked lending, while public-sector entities seek guidance on green bonds and digital-identity infrastructure financing. The rise of healthcare underscores the shift toward knowledge-intensive, R&D-heavy models where access to sophisticated capital markets advice drives competitive advantage.

By Service Channel: Human Advisory Retains Core, Robo Scales Fast

Human advisers controlled 65.02% of the financial advisory services market share in 2025, safeguarding complex net-worth clients that value empathy and bespoke planning. Yet, robo platforms are projected to grow at 16.95% CAGR, steadily enlarging their slice of the overall financial advisory services market. Scale players such as Betterment and Wealthfront refine goal-based algorithms, while incumbents like Charles Schwab embed robo modules inside traditional practices to offer tiered service. The financial advisory services market size allocated to hybrid models is set to jump as advisers integrate automated tax-loss harvesting and predictive spending analytics into face-to-face engagements.

Consumer preference surveys reveal that young professionals accept chat-based check-ins and digital document vaults, reserving video calls for milestone events such as home purchases or inheritance settlements. Fee compression drives innovation; subscription pricing and pay-per-plan packages proliferate. Advisers track engagement metrics—login frequency, content-consumption patterns—to personalize outreach and pre-empt attrition.

By Delivery Mode: On-Site Strength, Virtual Uptick

On-site consulting held 73.40% of the financial advisory services market share in 2025, demonstrating that for ultra-high-net-worth families, multisession estate planning and fiduciary briefings still benefit from physical presence. The pandemic, however, normalized virtual interactions, bolstering remote consulting’s 10.45% CAGR over the forecast period. The financial advisory services market size tied to virtual delivery will more than double by 2031 if current adoption persists. Advisers increasingly organize quarterly video reviews supplemented by secure portal dashboards, which clients access on demand.

New York Life Investments notes that many female investors prefer touchpoints every 4–6 months, and virtual meetings meet that cadence without travel friction. Productivity gains surface as advisers cover broader geographies; a single specialist can advise clients in Boston, Singapore, and Dubai within a day. Compliance teams adapt by recording sessions and archiving screen shares to satisfy audit trails. Firms also roll out virtual reality pilots for immersive risk-profiling experiences, though mainstream uptake remains nascent.

Geography Analysis

North America dominated the financial advisory services market with 39.95% market share in 2025. Mature capital markets, deep wealth pools, and a rigorous yet stable regulatory environment allow advisers to price complex planning services at premium levels. New York, Chicago, and San Francisco remain command centers, housing JPMorgan Chase, Goldman Sachs, and Morgan Stanley, each managing multi-trillion-dollar books. Canadian institutions buttress regional heft; the proposed merger of Prospera, Coast Capital, and Sunshine Coast credit unions would create a purpose-driven co-operative overseeing USD 38.6 billion in assets, signaling consolidation momentum.

Asia-Pacific is projected to be the fastest-growing region, set to log an 7.78% CAGR to 2031. Rising middle-class affluence, digital-bank innovation, and progressive regulatory sandboxes cultivate fertile ground for adviser expansion. Japan’s SBI Holdings and SMBC Group will debut “Olive Infinite” in 2026, pairing algorithmic allocation with live consultants. Taiwan chose Kaohsiung as the pilot hub for an Asian asset-management centre aimed at channeling more than TWD 30 trillion into professional portfolios. Chinese and Indian fintechs continue to onboard millions of first-time investors, giving rise to regional robo leaders.

Europe contributes a sizable revenue base anchored by London, Frankfurt, and Zurich, though economic uncertainty and dense regulation temper growth. Sweden transposed the EU Corporate Sustainability Reporting Directive into national law in 2024, expanding demand for ESG audit and advisory. Brexit realignment imposes additional licensing costs and data-transfer complexities that advisers must absorb to serve continental clients from UK hubs. Meanwhile, GCC wealth centers in the Middle East recruit global advisers to steward diversified sovereign portfolios, yet political volatility in parts of Africa restrains broader regional penetration.

Mordor Intelligence provides coverage of the financial advisory services market across other key regional markets, including North America and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The financial advisory services market remains moderately fragmented, featuring global banks, Big Four consultancies, specialised boutiques, and digital disruptors. Incumbent powerhouses such as JPMorgan Chase, Bank of America, and Goldman Sachs couple balance-sheet strength with multi-disciplinary advisory arms. They invest billions in generative-AI research, client-facing apps, and data lakes to defend their share against agile fintechs. Deloitte, EY, KPMG, and PwC leverage regulatory, cybersecurity, and tax expertise to undercut investment banks in middle-market M&A and restructuring mandates.

Robo pioneers Betterment and Wealthfront exploit low-cost structures and gamified interfaces to capture mass-affluent flows. Their combined assets under management exceeded USD 65 billion in 2024, reflecting compound growth north of 25%. To respond, traditional players launch white-label robo offerings or acquire fintechs; Morgan Stanley’s 2020 E*TRADE purchase continues to yield cross-sell synergies, and its investment-management arm reached USD 1.66 trillion AUM by December 2024. Competitive battlegrounds now revolve around content (ESG research, private-market access), experience (hyper-personalized dashboards), and confidence (cyber-security certifications).

Pricing dynamics shift as client sophistication rises. Subscription tiers, performance-linked retainers, and micro-fee plans are expanding. Firms embracing advisory ecosystems—integrating legal, tax, and philanthropy partners—retain higher share of wallet. Talent strategies increasingly include in-house data scientists, behavioral psychologists, and sustainability analysts, reflecting a broadened definition of adviser expertise. The capacity to orchestrate these multidisciplinary teams while protecting client confidentiality differentiates market leaders from scale-chasing laggards.

Financial Advisory Services Industry Leaders

Bank of America Corporation

Goldman Sachs Group Inc.

Morgan Stanley

Deloitte

EY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SBI Holdings and SMBC Group unveiled plans for “Olive Infinite,” a hybrid digital asset-management service blending AI engines with personal consultation.

- April 2025: Prospera, Coast Capital, and Sunshine Coast credit unions agreed to merge, forming Canada’s largest purpose-driven credit union at USD 38.6 billion in assets.

- January 2025: Morgan Stanley Investment Management disclosed USD 1.66 trillion AUM, reversing prior outflows and marking 14% year-on-year growth.

- January 2025: The SEC charged Arete Wealth Management with “selling away” unapproved securities, reinforcing vigilance over adviser conduct.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the financial advisory services market as global fee income earned by licensed professionals and digital platforms that guide individuals, enterprises, and public bodies on investment, corporate finance, tax, retirement, and risk-management decisions, irrespective of delivery channel.

Scope Exclusion: For clarity, we exclude pure trade-execution brokerage, standalone audit engagements, and informal blog advice.

Segmentation Overview

- By Service Type

- Corporate Finance

- Accounting And Tax Advisory

- Investment

- Other Services

- By Organization Size

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By Industry Vertical

- Banking, Financial Services, Insurance (BFSI)

- IT & Telecommunication

- Manufacturing

- Retail And E-Commerce

- Public Sector

- Healthcare And Pharmaceuticals

- Other Industry Verticals

- By Service Channel

- Human Advisory

- Hybrid Advisory

- Robo-Advisory

- By Delivery Mode

- On-site Consulting

- Remote / Virtual Consulting

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with senior wealth managers, fintech founders, and corporate treasurers across five regions; through these conversations, we validated price bands, digital uptake, and compliance-cost trends that desk work could not fully capture.

Desk Research

We collected foundational data from tier-1 sources such as Federal Reserve Flow of Funds, SEC Form ADV filings, Bureau of Labor Statistics employment surveys, IMF Financial Access metrics, and OECD household savings tables to size the addressable client pools. Association whitepapers from the Investment Company Institute, CFA Institute, and Financial Planning Association sharpened service-mix assumptions.

Subsequently, we mined company 10-Ks, investor decks, and reliable press through D&B Hoovers and Dow Jones Factiva, which let us gauge fee yields, assets under advice, and technology adoption curves. The references above illustrate our approach, and numerous additional repositories informed verification.

Market-Sizing & Forecasting

We anchored 2025 revenue with a top-down client-pool model that turns household investable assets, corporate fundraising, and M&A volumes into advisory fee potential; then we cross-checked results with selective bottom-up roll-ups of publicly reporting firms.

Key variables like growth in high-net-worth individuals, average assets per planner, robo-advisory penetration, compliance-spend inflation, and cross-border deal counts feed a multivariate regression used to extend forecasts to 2030. Where data were thin, we applied conservative proxy ratios and re-tested them with experts.

Data Validation & Update Cycle

Our three-layer analyst review flags anomalies against independent AUM and fee benchmarks. We refresh the model annually and push interim updates when material events occur.

Why Mordor's Financial Advisory Services Baseline Commands Reliability

Published estimates diverge because each publisher chooses different revenue streams, client cohorts, and forecast cadences; so executives encounter wide ranges. We acknowledge that reality upfront.

We find differences arise when others include brokerage fees, freeze currency at 2022 rates, or project linear fee growth despite rising risk-free returns; whereas Mordor's disciplined scope, variable selection, and yearly refresh temper extremes and produce a balanced midpoint decision-makers trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 115.84 B (2025) | Mordor Intelligence | - |

| USD 103.01 B (2024) | Global Consultancy A | Excludes digital-only micro-advisors, fixed FX conversion |

| USD 90 B (2023) | Trade Journal B | Folds brokerage revenue, minimal primary checks |

| USD 86.26 B (2024) | Research Publisher C | Uniform 6 % CAGR, omits compliance-cost drag |

Taken together, the comparison shows how our scope-tight, annually refreshed model offers a transparent, reproducible baseline positioned logically between overly conservative and aggressive views.

Key Questions Answered in the Report

How large is the financial advisory services market today?

It generated USD 122.39 billion in 2026 and is projected to reach USD 161.19 billion by 2031 at a 5.66% CAGR.

Which region leads revenue in the financial advisory services market?

North America holds the top spot with 39.95% of 2025 market share, supported by deep capital markets and high net-worth populations.

What is driving growth in Asia-Pacific?

Rising middle-class wealth, digital adoption, and supportive regulatory sandboxes are propelling an 7.78% CAGR through 2031.

Are robo advisers replacing human advisers?

No; human advisers still managed 65.02% of market share as of 2025, but robo platforms are projected to scale quickly at 16.95% CAGR, leading to hybrid service models.

Which industry vertical is expanding the fastest?

The healthcare and pharmaceuticals segment is projected to grow at a 6.86% CAGR due to complex R&D financing and regulatory needs.

What is the biggest threat to advisory firms?

Talent shortages and ageing workforces could trim sector growth by 1.1% of the forecast CAGR unless firms recruit and implement productivity technologies.

Page last updated on: