HR Professional Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 89.75 Billion |

| Market Size (2031) | USD 126.85 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Professional Services Market Analysis by Mordor Intelligence

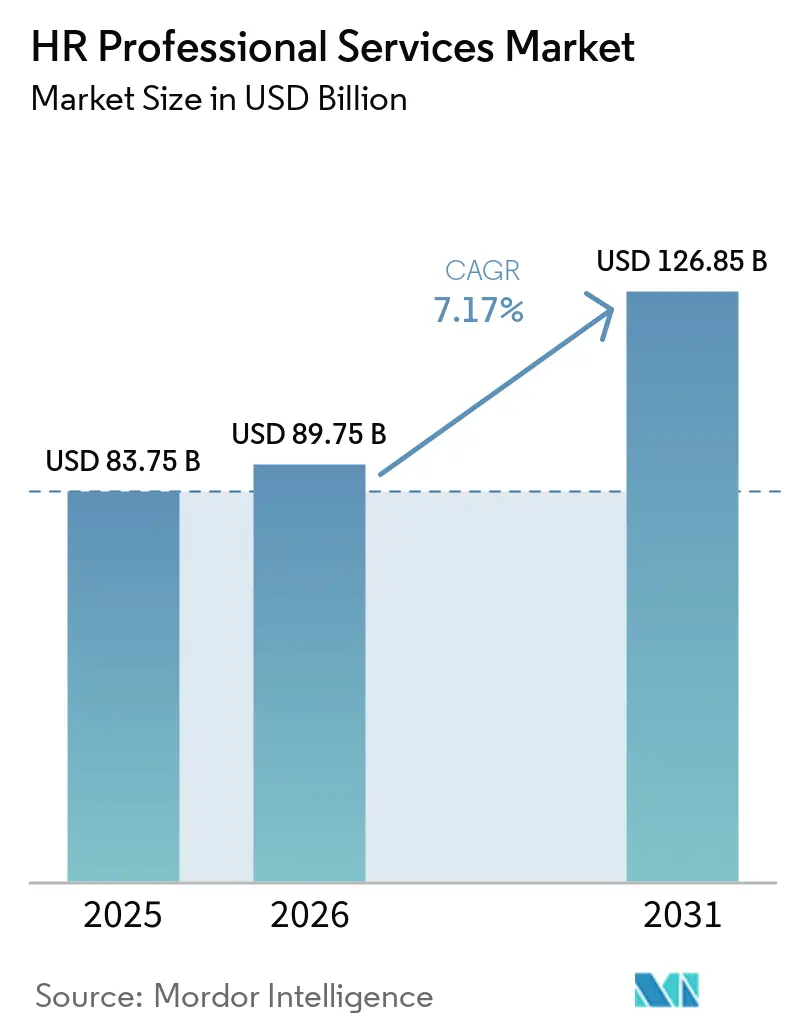

The HR professional services market size was valued at USD 83.75 billion in 2025 and estimated to grow from USD 89.75 billion in 2026 to reach USD 126.85 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031). Robust enterprise demand for multi-country compliance, rapid cloud migration of legacy HR suites, and adoption of outcome-based contracts are sustaining double-digit project pipelines across North America, Europe, and a fast-expanding Asia-Pacific client base. Generative AI has moved from pilot stage to scaled deployment, trimming time-to-hire by 30% and raising candidate quality scores, which directly elevates service fee potential for specialist providers. Mid-sized enterprises are shifting from traditional outsourcing toward modular Software-as-a-Service subscriptions that embed analytics and automated workflows, compressing vendor selection cycles and expanding addressable volumes for platform-centric suppliers. Currency-adjusted cost arbitrage remains relevant but is increasingly complemented by hyper-local compliance expertise, especially in emerging markets where regulatory change velocity often exceeds 12 substantive updates per jurisdiction annually. Meanwhile, rising cyber-insurance premiums and data-sovereignty rules are pressuring delivery margins, prompting providers to invest in privacy-by-design architecture and distributed data centers. Fragmented competitive dynamics keep pricing disciplined yet provide fertile ground for niche entrants offering AI-native solutions that monetize predictive workforce insights.

Key Report Takeaways

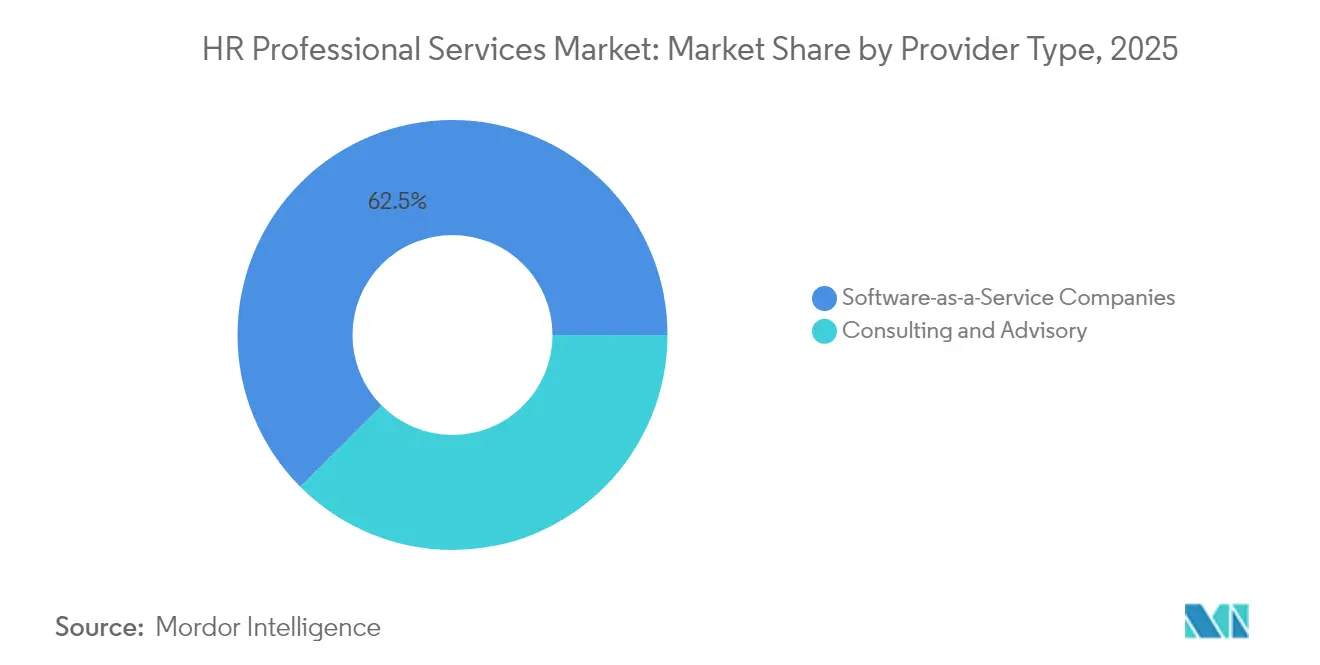

- By provider type, consulting & advisory services led with 37.52% share of the HR professional services market size in 2025; software-as-a-service companies are projected to expand at a 14.67% CAGR to 2031 within the HR professional services market.

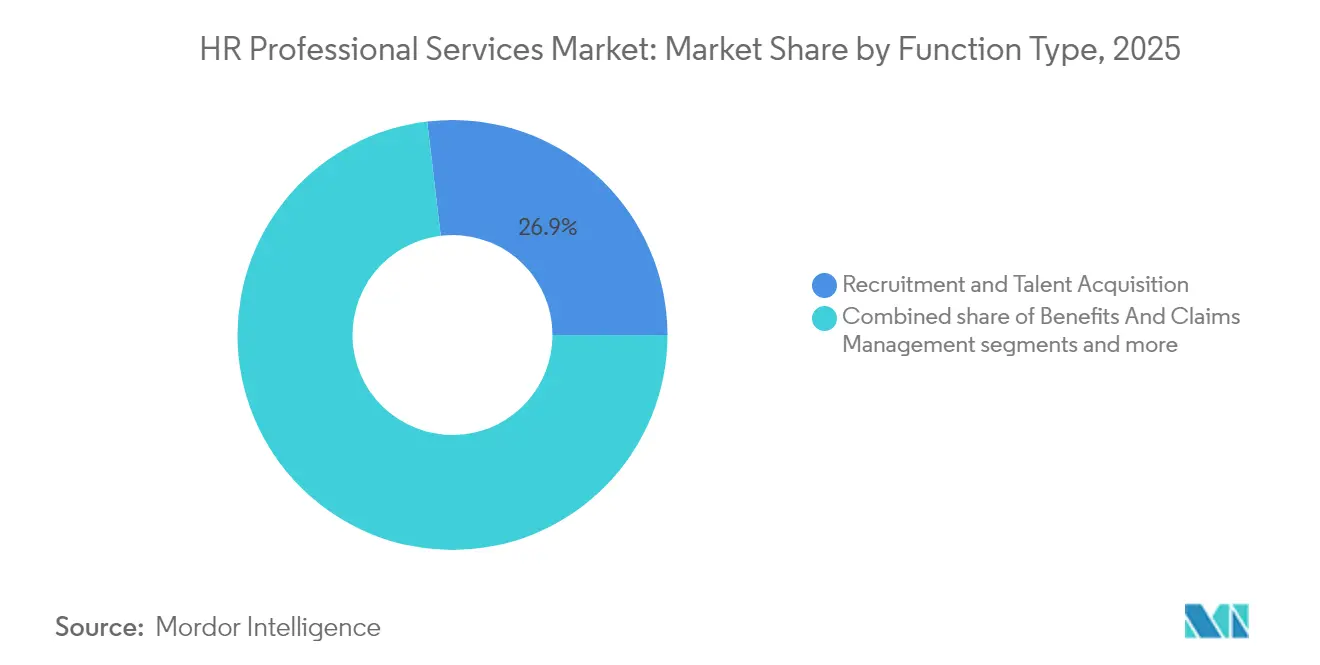

- By function type, recruitment & talent acquisition accounted for a 26.88% share of the HR professional services market size in 2025, and workforce planning & analytics is advancing at a 11.9% CAGR through 2031.

- By end-user industry, IT & telecom held 21.93% of the HR professional services market share in 2025, while healthcare is forecast to grow at 11% CAGR to 2031.

- By geography, North America commanded a 39.45% share of the HR professional services market size in 2025, whereas Asia-Pacific is on course for a 10.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HR Professional Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen-AI powered recruitment automation | +1.8% | Global, strongest in North America & APAC | Medium term (2-4 years) |

| Data-driven payroll error-prediction tools | +1.2% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Hyper-local compliance expertise demand | +1.5% | APAC core, spill-over to MEA & South America | Long term (≥ 4 years) |

| Integration of HR analytics into ERP stacks | +1.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Cloud migration of legacy HR suites | +1.4% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Rise of outcome-based HR service contracts | +0.8% | North America & Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gen-AI Powered Recruitment Automation

Generative AI is redefining talent acquisition economics by automating résumé parsing, initial screenings, and predictive fit scoring, which collectively shrink average hiring cycles by one-third[1]ORACLE Corporation, “Oracle Human Capital Management,” oracle.com. . Early adopters are layering proprietary large-language-model prompts onto applicant-tracking systems, creating sticky platform dependencies that favor service providers owning integrated IP. Vendors pairing AI sourcing with human interview coaching report notable improvements in first-year retention, a metric now embedded in outcome-based fee schedules. Regulatory bodies in North America have issued preliminary algorithmic bias guidelines, pushing providers to build transparent model-audit trails into their offerings. SaaS-first recruitment engines consequently enjoy a pricing premium because built-in governance reduces client compliance risk. Competitive differentiation is shifting toward domain-specific training data; healthcare, banking, and public sector examples dominate early proof points. As these engines mature, mid-market buyers increasingly bypass traditional RPO bids, accelerating direct platform subscriptions that widen the HR professional services market addressable pool.

Data-Driven Payroll Error-Prediction Tools

Machine-learning models embedded in global payroll service workflows now flag anomalies such as duplicate records or irregular tax code application before funds disburse, slashing remediation costs that historically averaged USD 291 per error[2]ADP, “ADP Investor Relations Quarterly Earnings,” adp.com. . The predictive accuracy rises with transaction volume, which places small providers at a disadvantage and fuels consolidation interest from larger payroll aggregators. CFOs perceive error-avoidance capabilities as compliance insurance, legitimizing 20-25% service fee uplifts compared with batch-processing contracts. Integration APIs feed audit logs directly to enterprise resource planning systems, satisfying SOX 404 evidence requirements without manual reconciliations. Vendors are bundling payroll analytics dashboards, turning operational data into strategic workforce cost intelligence. The complexity of country-specific tax reforms encourages clients to extend contract durations, locking in providers for full regulatory cycles. These dynamics reinforce sticky recurring revenue streams that underpin long-run margins within the HR professional services market.

Hyper-Local Compliance Expertise Demand

Divergent labor codes across emerging economies are multiplying the legal permutations global employers must monitor, driving demand for on-ground advisory teams fluent in local statutes[3]Littler, “Global Guide to Employee Privacy 2024 Edition,” littler.com. . Multinationals face a moving target as governments introduce worker-data residency rules and re-classify gig contracts, amplifying non-compliance penalties that frequently exceed 300% of foregone service fees. Providers securing certified experts in regions such as Southeast Asia and Sub-Saharan Africa are posting 40-50% annual revenue gains, propelled by green-field manufacturing projects and shared-services hubs. These local credentials generate defensible competitive moats against purely virtual rivals. Clients emphasize real-time legislative monitoring that feeds automated policy updates into HR information systems, tightening provider-client IT integrations. Data-localization constraints are prompting service partners to spin up in-country cloud instances, raising capex but unlocking premium localization fees. Over time, cross-regional knowledge networks built by these specialists should catalyze broader platform standardization and elevate the overall HR professional services market sophistication.

Integration of HR Analytics into ERP Stacks

Enterprise-grade ERP vendors have embedded workforce analytics that display attrition forecasts, compliance dashboards, and skills-gap heat maps within unified finance-to-supply-chain cockpit views. Implementation complexity around data cleaning and role-based access controls underpins multi-million-dollar professional services engagements. Providers differentiate by offering blueprinting workshops that map analytic outputs to regulatory filings and board-level human-capital disclosures, turning technology adoption into governance enablers. Once deployed, analytics modules surface real-time labor cost variances that feed budgeting processes, fostering cross-sell opportunities for compensation consulting. Change-management streams now rival technical integration in both scope and revenue as companies retrain line managers to interpret predictive dashboards. Service partners embed continuous-improvement sprints, converting one-off projects into annual optimization retainers. These factors collectively elevate segment profitability and cement the HR professional services market relevance to C-suite digital-transformation roadmaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & residency regulations | -0.9% | Global, strongest in Europe & North America | Short term (≤ 2 years) |

| Shortage of multi-country payroll talent | -0.7% | Global, most acute in APAC & MEA | Medium term (2-4 years) |

| Fragmented labour laws in emerging markets | -0.8% | APAC, Latin America, Africa – especially in high-growth, low-regulation economies | Medium to long term (3–5 years) |

| Rising cyber-insurance premiums for HRO firms | -0.6% | Global, with highest pressure in digitally dependent markets like North America and APAC | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Residency Regulations

Tightening global privacy laws such as GDPR and China’s PIPL obligate providers to segment infrastructure by jurisdiction, adding 15-20% to operating costs and diluting scale benefits. Ongoing regulatory churn forces recurrent system redesigns, with audit cycles now standard practice across client contracts. Cross-border data-transfer restrictions compel in-country encryption key management, elevating technical-architect skill requisites. Providers absorb incremental cyber-insurance premiums, which have climbed 8-12% since 2024 in response to ransomware risk [4]Aon, “Cyber Insurance Market Update Q3 2024,” aon.com.. Clients consequently scrutinize vendor security certifications, embedding ISO 27001 clauses into master service agreements. Failure to demonstrate end-to-end compliance can disqualify bidders from enterprise RFP shortlists, limiting revenue pipelines. Cumulatively, these pressures temper near-term margin expansion within the HR professional services market.

Shortage of Multi-Country Payroll Talent

A shrinking pool of certified payroll experts who can navigate overlapping tax codes and labor statutes across 60-plus countries constrains delivery capacity. Training a new specialist to full competency spans up to 24 months, during which supervised productivity lowers team utilization. Salary inflation for experienced practitioners has run 12-15% annually since 2024 as vendors compete for scarce talent pools. Providers respond with internal academies and micro-credentialing programs, yet these pipelines have not offset immediate demand spikes. Outsourcers are experimenting with AI rule engines to automate statutory updates, but human validation remains essential for penalty-bearing filings. Capacity bottlenecks can delay service onboarding by several weeks, occasionally triggering client penalty clauses. This talent deficit therefore trims projected growth for global-scale payroll engagements within the HR professional services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider Type: SaaS Models Accelerate Growth

Software-as-a-Service suppliers are on track to post a 14.67% CAGR to 2031, reflecting the fastest expansion among provider categories as self-service workflows gain board-level sponsorship. The HR professional services market size for these platforms is widening because mid-market buyers increasingly favor subscription economics over multi-year consulting retainers. SaaS vendors embed analytic dashboards that visualize hiring funnel velocity, compliance alerts, and absenteeism trends, traits that compress decision cycles and shrink change-management budgets. Consulting & Advisory firms still held 37.52% revenue share in 2025 through complex transformation mandates tied to mergers, regulatory remediation, and post-cloud optimization. Hybrid service models are emerging in which consultants white-label partner SaaS modules, blending advisory revenue with license resale in an effort to defend wallet share. Oracle’s acquisition of HiredScore and Workday’s AI roadmap underscore a platform-first race to internalize talent-matching algorithms, putting margin pressure on pure-play consultancies.

Consulting incumbents counter by packaging outcome-based SLAs that guarantee regulatory audit readiness or retention uplift, thereby monetizing domain expertise beyond billable hours. Many firms now operate venture studios that spin out niche HR tech assets to secure intellectual-property leverage in negotiations. In parallel, SaaS leaders cultivate certified implementation ecosystems to reduce onboarding friction and unlock scale beyond internal service benches. This reciprocal interdependence blurs categorical boundaries, with cross-selling agreements proliferating. Client procurement teams thus weigh total-cost-of-ownership scenarios comparing bundled advisory plus SaaS fees to stand-alone platform subscriptions. As ecosystems mature, platform governance standards emerge, making interoperability and open APIs critical vendor-selection criteria.

By Function Type: Analytics Drive Transformation

Recruitment & Talent Acquisition retained the largest functional foothold at 26.88% in 2025, sustained by persistent skilled-labor shortages and pressure to compress vacancy cycles. Workforce Planning & Analytics, though smaller, is forecast to deliver a 11.9% CAGR as predictive modeling becomes mainstream in budgeting processes. Early adopters embed scenario-planning widgets that quantify overtime trade-offs, voluntary attrition risk, and skills adjacency, which expands cross-functional HR budgets toward data-science engagements. Payroll & Compensation Management continues to generate stable annuity streams but wrestles with declining unit prices as automation scales. Benefits & Claims Management is regaining momentum because hybrid work arrangements complicate eligibility tracking and wellness program ROI quantification. Emerging sub-segment activity around employee-experience orchestration sits at the convergence of wellness, engagement, and performance analytics solutions, representing a white-space growth avenue.

Function overlap intensifies as platforms surface single dashboards integrating talent acquisition KPIs with payroll variance and learning-path completion, promoting unified data governance. Providers that historically specialized in isolated offerings are broadening their scope to defend their share of wallet, often via strategic alliances or tuck-in acquisitions. Analytics-driven insights also catalyze consulting attach services such as change-management workshops and compliance reporting automation. ISO 30414 human-capital disclosure norms add urgency because listed companies must publish standardized metrics that span multiple HR functions. In practice, clients prefer service partners capable of translating analytic outputs into board-level narratives that link workforce levers to financial outcomes. Vendors seizing this advisory role deepen client entrenchment and increase renewal rates.

By End-User Industry: Healthcare Leads Growth

Healthcare organizations exhibit the fastest adoption rate at 11% CAGR through 2031 as staffing shortages, regulatory scrutiny, and value-based care reimbursement schemes intensify pressure for effective workforce operations. HIPAA compliance adds layers of privacy complexity that favor specialized vendors versed in protected health information handling. IT & Telecom firms remain the largest contributors, accounting for 21.93% revenue share in 2025, largely because global delivery footprints require sophisticated multi-country payroll orchestration. BFSI clients engage providers to manage labor-risk metrics tied to Basel III and Dodd-Frank guidelines, prompting heightened demand for workforce-compliance analytics. Manufacturing enterprises pursue HR services to underpin Industry 4.0 upskilling, aligning predictive maintenance staffing with production digitization timelines. Retailers focus on seasonal scheduling optimization and flexible pay cycles that integrate earned-wage access fintech APIs.

Sector-specific regulations drive tailored service blueprints that improve vendor differentiation and pricing leverage. Providers develop vertical solution catalogs detailing typical integrations for example, time-and-attendance links with electronic health records in hospitals or anti-money-laundering screening workflows in banking. Cross-industry platform modules promote scale economies, yet domain-specific compliance accelerators frequently dictate final vendor selection. Clients increasingly request benchmark dashboards comparing their workforce metrics to sector peers, a feature that creates network-effect moat advantages for providers with extensive industry datasets. These dynamics encourage continuous investment in domain specialists who translate generic HR technology into contextualized business outcomes. As vertical sub-segments grow, new entrants targeting singular industries can carve niches despite the broader fragmentation of the HR professional services market.

Geography Analysis

North America preserved its lead with 39.45% revenue share in 2025 owing to high enterprise outsourcing maturity and a robust ecosystem of HR technology vendors that feed adjacent service streams. The region’s regulatory heterogeneity across federal, state, and provincial jurisdictions sustains demand for localized compliance advisory. Canada posts above-average growth as provincial employment codes drive incremental platform configurations, while Mexico’s near-shoring boom triggers bilingual HR policy harmonization projects that command premium rates. U.S. providers have expanded bilingual service hubs along the southern border to capture emerging maquiladora payroll volumes. A steady flow of venture capital into HR tech start-ups further fuels innovation cycles, enabling service partners to bundle proprietary tools into managed-service agreements.

Asia-Pacific represents the fastest-growing geography with a projected 10.07% CAGR, propelled by economic expansion and digital-government initiatives that mandate electronic payroll filing and real-time labor data reporting. India’s service-delivery heritage is evolving from cost-centric outsourcing to value-added HR analytics exports, drawing multinational headquarters projects that require integrated global-in-country delivery models. China’s stringent data-localization laws encourage joint-venture structures wherein foreign providers leverage domestic cloud infrastructure to meet residency requirements. Southeast Asia’s talent-scarce markets rely on external providers for compliance and payroll scale, fostering high contract-renewal rates. Australia and South Korea show steady uptake of outcome-based contracts, validating premium pricing when vendors present clear retention or diversity KPIs. Emerging economies such as Vietnam and Indonesia are leapfrogging legacy on-premises systems, adopting mobile-first HR applications that integrate with regional e-wallet ecosystems for flexible pay disbursement.

Europe records a relatively restrained CAGR outlook as GDPR compliance costs add 15-20% to provider operating expenses and macroeconomic uncertainty tempers corporate IT budgets. Nevertheless, specialized vendors fluent in works-council negotiations and co-determination statutes secure long-term engagements in Germany and France. The United Kingdom’s post-Brexit divergence from EU labor codes creates niche advisory demand for companies straddling both territories. BENELUX and Nordic clients display the highest appetite for performance-linked contracts, reflecting mature analytics adoption and cultural emphasis on measurable outcomes. Southern Europe lags due to higher unemployment and budget constraints, yet public-sector modernization projects financed by EU recovery funds are emerging. Providers operating pan-European data mesh architectures differentiate on privacy engineering, reducing compliance overhead for multi-jurisdiction clients.

Mordor Intelligence provides coverage of the hr professional services market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The HR professional services market remains highly fragmented, with the top five vendors collectively holding a relatively small portion of the total market, reflected in a moderate concentration score of 4. Leading global providers like ADP maintain their competitive edge by leveraging proprietary technology platforms and multi-country payroll licenses, enabling them to secure enterprise contract renewals across over 60 countries. Randstad NV capitalizes on staffing depth to embed recruitment process outsourcing bundles into broader managed-service agreements, creating pipeline synergies. Technology-native players, notably Workday and Oracle, accelerate share capture by embedding AI-driven analytics that elevate license pull-through within professional-service engagements. Simultaneously, regional specialists use hyper-local compliance expertise as a differentiator, often outmaneuvering large vendors on regulatory nuance in emerging markets.

Acquisition activity intensified in 2024, with Paychex’s USD 4.1 billion takeover of Paycor consolidating mid-market payroll and human-capital management capabilities. SAP’s purchase of SmartRecruiters added AI-sourcing capabilities that dovetail with its SuccessFactors suite, reinforcing an end-to-end platform narrative. Vendor strategy converges around bundled IP: embedded analytics reduce client switching costs and drive multi-year contract lock-ins. Investment priorities tilt toward privacy-engineering talent, edge-data architectures, and automated compliance orchestration to meet stringent sovereignty mandates. Niche disruptors offering embedded payroll-fintech or employee-experience APIs continue to raise venture funding, targeting sub-segments overlooked by full-suite incumbents. Yet scale barriers related to global regulatory coverage push many start-ups into white-label partnerships with established payroll networks.

Sustained fragmentation motivates alliances among mid-tier vendors seeking to meld complementary strengths. Consultants partner with SaaS platforms for implementation expertise, while payroll networks license niche analytics engines to broaden functional depth. These arrangements respond to buyer preference for single-provider accountability without sacrificing best-of-breed functionality. Strategic joint ventures in high-growth geographies such as the Middle East illustrate alternative expansion routes that minimize direct capital deployment while securing market footholds. Meanwhile, AI governance and ethical hiring frameworks create differentiation levers for firms that proactively audit and certify model fairness. Providers able to document bias-mitigation strategies are shortlisted in heavily regulated verticals, particularly government and healthcare.

HR Professional Services Industry Leaders

ADP

Randstad NV

Adecco Group

ManpowerGroup

Korn Ferry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Workday partnered with Microsoft to embed AI-powered workforce planning tools directly into Microsoft Viva, targeting the platform’s 345 million global Microsoft 365 users. This move signals a shift toward integrated HR analytics within productivity ecosystems, challenging traditional standalone HR solutions.

- January 2025: ManpowerGroup launched its Skills-Based Workforce Intelligence platform, providing real-time labor market insights and skills gap analysis for enterprise clients. The platform integrates with existing HRIS systems to provide predictive workforce planning capabilities and competitive intelligence on talent availability.

- January 2025: ADP launched its Global Payroll Connect platform in 15 new countries (including Vietnam, Nigeria, and Chile) with a USD 45 million investment, expanding unified payroll services to over 60 countries. This strengthens ADP’s position in serving multinational clients with complex compliance needs.

- February 2024: Oracle completed a USD 665 million acquisition of HiredScore, gaining advanced AI capabilities in talent acquisition, including proprietary algorithms for candidate matching and bias detection. This enhances Oracle’s competitiveness in the recruitment process outsourcing (RPO) space.

Global HR Professional Services Market Report Scope

Professionals in this division take care of issues and requirements related to the organization's human capital or the employees. It is beneficial to comprehend the primary roles and obligations of human resources professionals, whether you are thinking about a career in this field or you need to hire HR specialists for your company.

The HR professional services market is segmented By Provider Type (Consulting Companies, Software-as-a-Service Companies), By Function Type (Recruitment And Talent Acquisition, Benefits And Claims Management, Workforce Planning and Analytics, Payroll And Compensation Management, and Other Functions), By End User Industry (BFSI, Healthcare, IT and telecom, Manufacturing, Retail, Government, and Other Industries), by Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers Market size and forecasts for HR Professional Services Market in value (USD Million) for all the above segments.

| Consulting Companies |

| Software-as-a-Service Companies |

| Recruitment And Talent Acquisition |

| Benefits And Claims Management |

| Workforce Planning and Analytics |

| Payroll And Compensation Management |

| Other Functions |

| BFSI |

| Healthcare |

| IT and Telecom |

| Manufacturing |

| Retail |

| Government |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (SG, MY, TH, ID, VN, PH) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Provider Type | Consulting Companies | |

| Software-as-a-Service Companies | ||

| By Function Type | Recruitment And Talent Acquisition | |

| Benefits And Claims Management | ||

| Workforce Planning and Analytics | ||

| Payroll And Compensation Management | ||

| Other Functions | ||

| BFSI | ||

| Healthcare | ||

| IT and Telecom | ||

| Manufacturing | ||

| Retail | ||

| Government | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (SG, MY, TH, ID, VN, PH) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large will the HR professional services market be by 2031?

It is projected to reach USD 126.85 billion, reflecting a 7.17% CAGR from 2026.

Which functional area is expanding fastest within HR services?

Workforce Planning & Analytics leads with a 11.9% forecast CAGR as predictive modeling becomes standard.

Why is Asia-Pacific growing faster than other regions?

Rapid digital-government mandates, economic expansion, and stringent data-localization laws generate strong demand for sophisticated HR services.

What drives the shift toward outcome-based contracts?

Clients seek measurable improvements in retention, diversity, and productivity, aligning vendor fees with clear business results.

Which provider type shows the highest growth rate?

Software-as-a-Service vendors are set to post a 14.67% CAGR through 2031, outpacing traditional consulting firms.

Page last updated on: