India Payroll Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

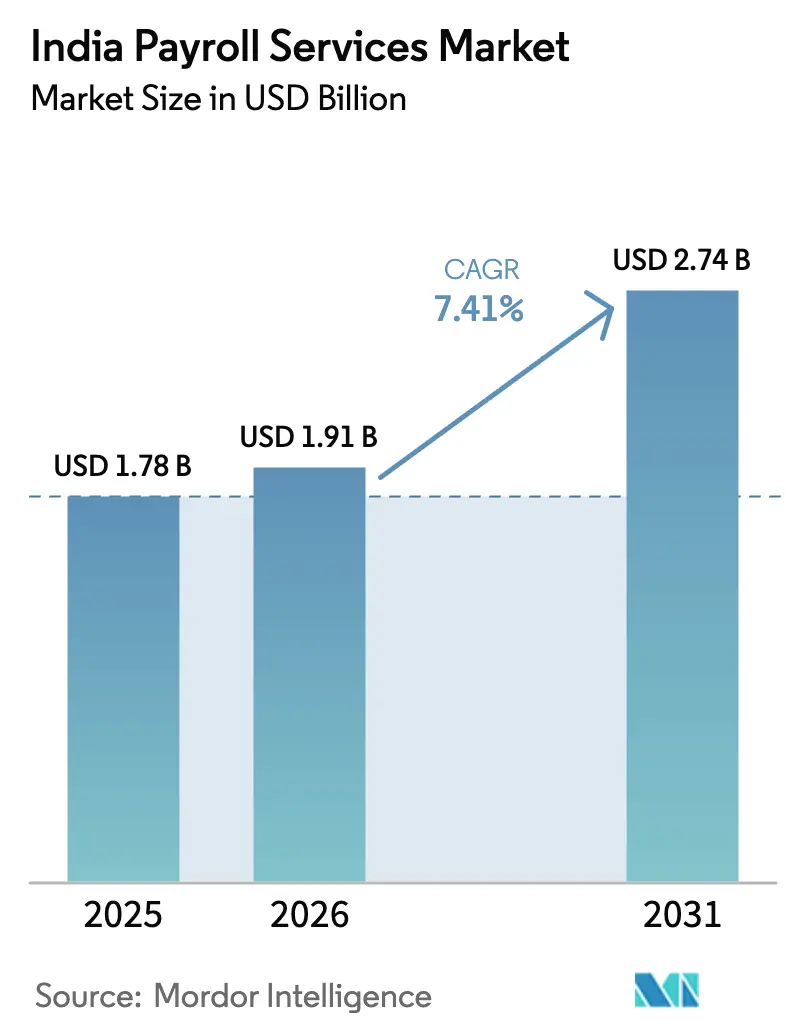

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

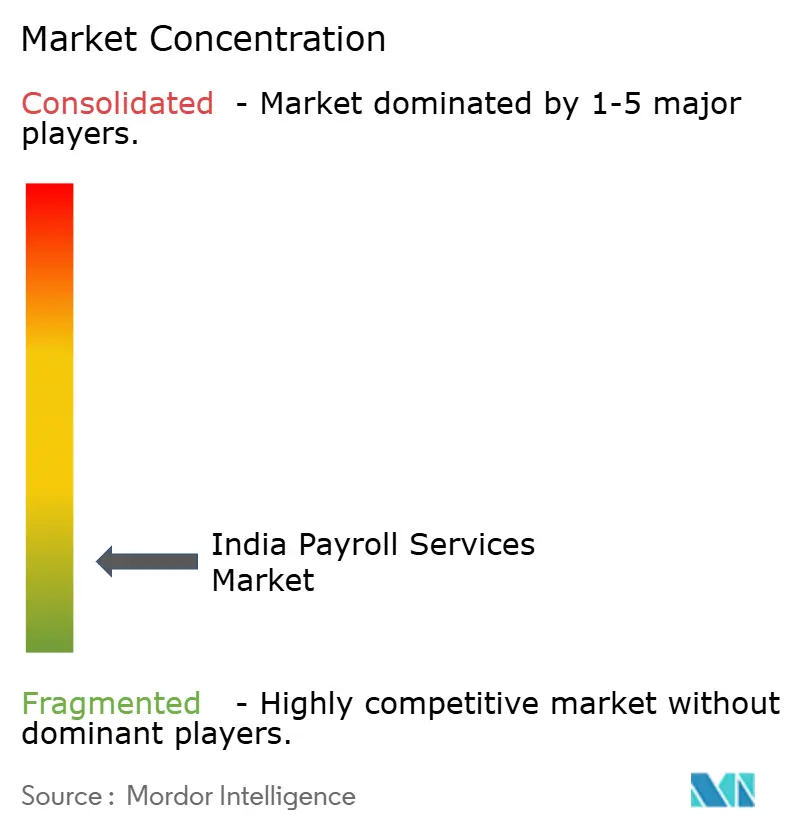

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Payroll Services Market Analysis by Mordor Intelligence

India payroll services market size in 2026 is estimated at USD 1.91 billion, growing from 2025 value of USD 1.78 billion with 2031 projections showing USD 2.74 billion, growing at 7.41% CAGR over 2026-2031. Accelerating government-led digitization programs, notably the push toward real-time statutory filings through the Unified Payments Interface, is raising the compliance bar for employers and nudging them toward professional outsourcing. Small and medium enterprises are shifting from manual spreadsheets to cloud platforms, motivated by cost efficiency and the need for on-demand regulatory updates. At the same time, India’s expanding gig workforce is complicating payroll calculations because new social-security mandates cover platform workers and inter-state migrants. Large enterprises continue to dominate revenue owing to complex multi-state operations that demand deep statutory expertise. Yet rising platform acquisitions and funding rounds show that technology innovation, not scale alone, is the core competitive lever in the india payroll services market.

Key Report Takeaways

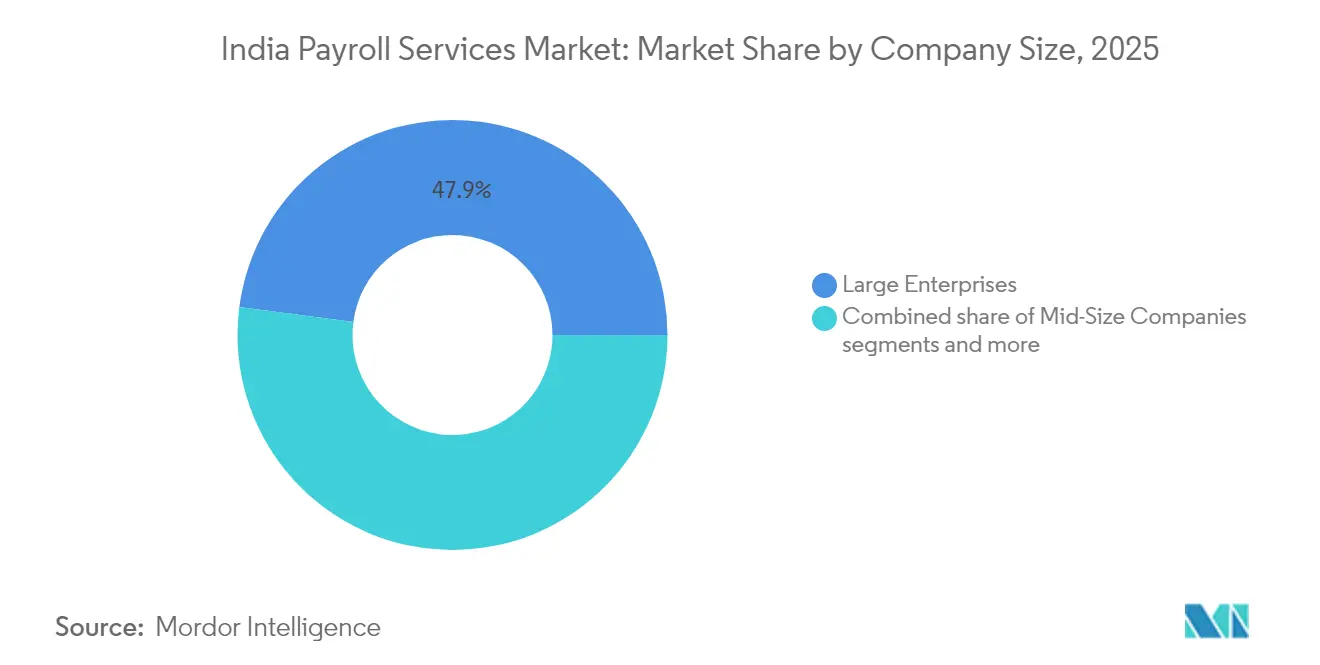

- By company size, large enterprises led with 47.92% of india payroll services market share in 2025, while small-sized companies are projected to expand at a 16.39% CAGR through 2031.

- By end-user industry, information technology captured 30.25% of India's payroll services market share in 2025; retail is forecast to grow at a 15.05% CAGR to 2031.

- By geography, South India held a 35.88% share of the Indian payroll services market size in 2025, and North-East India is advancing at a 17.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Payroll Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital compliance push | +1.8% | National with early gains in Maharashtra, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Cloud payroll adoption by SMEs | +1.5% | Tier-1 and tier-2 cities nationwide | Short term (≤ 2 years) |

| Rising statutory complexity | +1.4% | Industrialized states | Long term (≥ 4 years) |

| Gig-economy payroll needs | +1.2% | Bengaluru, Mumbai, Delhi NCR | Medium term (2-4 years) |

| UPI-based instant salary disbursement | +1.3% | Urban centers and tech-forward regions like Bengaluru, Hyderabad, Mumbai | Short term (≤ 2 years) |

| Payroll-linked credit / financial-wellness offerings | +1.6% | Nationwide, with strong traction among digitally native SMEs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government-Led Digital Compliance Push Accelerates Outsourcing

India’s e-invoicing, GST network, and Aadhaar-linked verification programs now interlock, so an error in one system exposes employers to cascading penalties [1]Mondaq, “Employment Linked Incentive Scheme – Whether a Relief or Burden on the Employers,” mondaq.com. . The Employees’ Provident Fund Organisation moved PF withdrawals to UPI rails in June 2025, demanding real-time API connectivity from payroll vendors. Digitization complexity thus enlarges the client pool for the India payroll services market because many firms lack the IT depth to maintain compliant interfaces. Service providers that embed automated statutory monitors and instant filing capabilities gain a clear edge. Their platforms pre-validate data before submission, reducing error-driven fines. As ministries introduce additional machine-readable returns, the value of outsourced compliance will rise further.

Cloud Payroll Adoption Transforms SME Operations

Subscription pricing as low as INR 139 (USD 1.67) per month for 100 employees has lowered the entry barrier for budget-conscious firms. SaaS models ensure automatic updates whenever a state revises its professional-tax slabs, shielding owners from manual spreadsheets. Integrated self-service portals free HR teams from payslip distribution and leave tracking, tasks that once consumed workdays. Cloud vendors also offer app-based onboarding that validates PAN and Aadhaar in minutes, slashing new-hire cycle times. These benefits accelerate penetration across tier-2 hubs such as Coimbatore and Nagpur, supporting volume-driven revenue growth in the India payroll services market. Competitive pressure is forcing on-premise legacy providers to pivot toward browser-based delivery to retain customers.

Rising Statutory Complexity Drives Professional Services Demand

The Code on Social Security 2020 expands coverage to gig workers and interstate migrants, fundamentally changing contribution bases[2]India Briefing, “India’s New Labor Codes Enactment Status and Delayed Implementation,” india-briefing.com. . State-specific professional-tax portals layer additional filings, with Maharashtra’s MAITRI process differing sharply from Tamil Nadu’s online system. Court rulings such as the Karnataka High Court’s April 2024 decision on expat EPF contributions illustrate how legal flux can invalidate internal payroll logic overnight. Employers, therefore, seek vendors that maintain rule libraries and push updates directly into calculation engines. Advanced platforms now alert clients before effective dates, giving HR teams a runway for documentation. Vendors that combine legal intelligence with automated patching retain stickier contracts in the India payroll services market.

Gig Economy Expansion Reshapes Payroll Requirements

Platform workers now count toward statutory headcounts, obliging aggregators to track fluctuating rosters and variable pay. Payoneer’s USD 61 million acquisition of Skuad shows investor belief in employer-of-record models that manage cross-border freelancers. Payroll engines now ingest project-level data, allocate tax at source, and disburse earnings instantly through UPI to meet worker cash-flow preferences. Real-time settlement reduces churn in ride-sharing, food-delivery, and talent platforms. Vendors that can reconcile invoices, input tax credits, and benefit accruals for high-velocity gig cohorts capture premium pricing. Such specialization strengthens competitive moats within the India payroll services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security & privacy concerns | -0.8% | BFSI and healthcare clusters | Short term (≤ 2 years) |

| SME cost sensitivity | -0.6% | Tier-2 and tier-3 cities | Medium term (2-4 years) |

| Fragmented regulatory enforcement across states | -0.7% | National, with higher complexity in industrial and high-compliance zones | Long term (≥ 4 years) |

| Limited digital literacy among micro-enterprises | -0.5% | Tier-3 and rural regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-Security Concerns Slow Enterprise Adoption

Breaches at global payroll processors have heightened scrutiny of encryption, access controls, and data-localization adherence. Multinationals demand ISO 27001 certification plus SOC 2 audit reports before onboarding vendors. Healthcare and banking clients insist that personally identifiable information remain within India-hosted servers to satisfy sectoral guidelines. Compliance adds costs that smaller providers struggle to absorb, potentially narrowing supplier choices. Enterprises weigh outsourcing benefits against reputational risk, sometimes delaying transitions even when legacy systems creak. Vendors that invest in zero-trust frameworks and transparent audit trails will reassure risk-averse sectors and unlock new bookings in the India payroll services market.

SME Cost Sensitivity Limits Premium Service Uptake

Smaller firms often regard payroll as a commodity, prioritizing headline subscription fees over advanced analytics. Price ceilings encourage freemium tiers that strip out compliance dashboards, forcing SMEs to toggle between platforms for filings. Limited budgets hamper the adoption of optional modules such as financial wellness or AI-based anomaly detection. Providers, therefore, chase volume to offset thin margins, leaning on digital channels and partner ecosystems for lead generation. Yet the approach inflates churn because bargain-seeking clients migrate when introductory discounts expire. Balancing feature richness with affordability remains a central challenge to widen penetration in cost-conscious towns across the India payroll services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Company Size: Enterprise Dominance Meets SME Growth Acceleration

Large enterprises accounted for 47.92% of India's payroll services market share in 2025, a position rooted in their multi-state footprints and high compliance exposure . These corporations favor platforms that unify attendance, expense, and statutory submissions for tens of thousands of workers. The Indian payroll services market size for small-sized companies is projected to expand at a 16.39% CAGR to 2031 as cloud SaaS slashes onboarding friction. Mid-size firms occupy the strategic middle, often piloting new modules such as predictive overtime cost modeling before such tools filter upward or downward. Vendors bundle modular pricing so that feature uptake can scale with headcount. Cross-sell from payroll into HRIS and benefits administration remains a key revenue lever.

Enterprises increasingly demand localized rule libraries to automate professional tax, labor-welfare fund, and union levy deductions across facilities. Advanced analytics flag anomalous wage movements, supporting internal audit requirements. SMEs instead desire quick configuration, templated pay-grade structures, and call-center support in regional languages. The divergence compels providers to maintain tiered product stacks within the India payroll services market. Fintech tie-ins, such as salary-linked credit, resonate with both segments but especially with smaller firms that want to boost employee retention without raising fixed payroll costs. Scale-up players differentiate by offering the same daily statutory patching engine to all tiers, ensuring uniform compliance integrity.

By End User Industry: IT Leadership Faces Retail Disruption

Information technology services held 30.25% revenue in 2025, thanks to complex variable-compensation models and global mobility programs. Frequent cross-border assignments demand split-pay calculations, shadow payrolls, and equalization agreements, needs that elevate outsourcing. Retail, meanwhile, is set for a 15.05% CAGR as organized chains formalize store-level staffing and compliance documentation. The India payroll services market size for retail employers will swell as e-commerce anchors move beyond contractor models toward permanent headcounts. Manufacturing contributes a steady demand driven by shift-differential tracking and statutory bonus computations. BFSI clients seek airtight data-security postures and audit-ready trails, pushing vendors to deliver bank-grade encryption.

Sector-specific templates now shorten implementation cycles: IT modules integrate resource-allocation codes, while retail setups include bulk roster imports for seasonal peaks. Payroll platforms plugging into warehouse WMS and POS systems enable automatic attendance reconciliation. Gig-driven industries such as food delivery create cross-sector service lines where pay cycles run daily rather than monthly, requiring high-volume transaction engines. Vendors capturing multiple verticals improve utilization of their rule-maintenance teams, spreading costs across contracts in the India payroll services market. Deep domain integrations are becoming table stakes to win renewal clauses.

Geography Analysis

South India retained 35.88% revenue share in 2025, anchored by Karnataka’s IT corridors and Tamil Nadu’s electronics hubs that collectively house large workforces requiring multi-layer compliance oversight. Regional employers face distinct professional-tax slabs and bonus obligations, prompting heavy reliance on specialized outsourcing. Early cloud adoption culture and higher digital-payments penetration hasten the uptake of real-time salary disbursement. Service providers use the region as a proving ground for AI modules before scaling nationwide. Offshore payroll processing centers located in Chennai and Bengaluru also export managed services to APAC, reinforcing South India’s strategic role within the India payroll services market.

West India captured a 25.12% share in 2025 as Maharashtra’s financial capital and Gujarat’s manufacturing clusters demand sophisticated wage-cost allocation and compliance with frequent labor-law amendments. Mumbai-based BFSI giants impose rigorous data-residency clauses, pushing vendors to invest in local Tier-IV data centers. Pune’s emergence as a global payroll hub, exemplified by Neeyamo’s service campus, underscores the region’s talent pool depth. Vendors leverage proximity to ports and logistics corridors to support export-oriented factories needing cross-border salary settlements for expatriates. State-level digitization initiatives, such as the MAITRI single-window portal, increase electronic filing volumes and reinforce third-party demand.

North-East India, though small in absolute numbers, is forecast to grow at 17.45% CAGR through 2031, lifted by infrastructure incentives that formalize employment. Government subsidies require beneficiaries to register under EPFO and ESIC, generating fresh onboarding for vendors capable of remote support. Limited local payroll talent makes outsourced cloud platforms the primary route to compliance. North India’s 18.03% share reflects Delhi NCR headquarters’ demand for consolidated reporting, yet slower outsourcing among traditional industries. Central and East India remain price-sensitive but represent growth runways as industrial corridors extend and awareness of compliance risks rises.

Competitive Landscape

The India payroll services market remains highly fragmented, with the top five vendors capturing only a limited share of total revenue in 2024. ADP India holds a leadership position, benefiting from its global platform capabilities and strong relationships with multinational corporations. Neeyamo follows, operating a centralized hub-and-spoke model that supports multi-country payroll delivery from its Pune base. Domestic players such as greytHR and Keka dominate the cloud-based SME segment, standing out through vernacular user interfaces and flexible, tiered pricing structures. Strategic consolidation is underway, with capability-led acquisitions becoming a key focus. Notable deals include TransPerfect's acquisition of Paybooks in September 2024 and Payoneer's purchase of Skuad in August 2024 to expand into employer-of-record services.

Technology investment is emerging as the key differentiator in the competitive landscape. Leading vendors are deploying AI-powered tools to detect payroll anomalies, anticipate compliance risks, and automatically update statutory rules. These platforms are also building real-time API ecosystems that integrate seamlessly with accounting, ERP, and fintech applications. This makes payroll data more actionable, especially for tasks like cash-flow forecasting and credit scoring. Specialized providers serving the gig economy are bundling instant payouts with automated worker classification, attracting digital marketplaces that previously relied on manual processes. Innovation is no longer optional—it’s central to gaining market share.

Venture capital interest in the space remains strong, reflecting confidence in market growth and tech disruption. CloudPay raised USD 120 million in August 2024 to accelerate its expansion across Asia, signaling bullish investor sentiment. In January 2024, SalarySe secured USD 5.2 million to scale its payroll-linked credit offerings. While price sensitivity remains high in tier-3 cities, especially among micro and small enterprises, enterprise clients prioritize service depth over cost. End-to-end solutions that integrate recruitment, HR information systems, and employee benefits are increasingly seen as value drivers. Compliance accuracy is now a critical differentiator, with some providers including financial penalties in SLAs for missed filing deadlines.

India Payroll Services Industry Leaders

ADP India

Neeyamo

Quess Corp (Monster Payroll)

Aon Hewitt India

Alight Solutions India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Indian government approved the Employment-Linked Incentive Scheme with USD 11.97 billion budget allocation, fundamentally reshaping payroll processing requirements through EPFO integration and Aadhaar-based payment systems. This initiative will create over 35 million new formal employment opportunities requiring sophisticated payroll processing capabilities.

- September 2024: TransPerfect acquired Paybooks Technologies, a Bengaluru-based payroll and HR technology provider, strengthening its global payroll capabilities and expanding its presence in the Indian market. This acquisition demonstrates the strategic value of Indian payroll expertise in serving multinational clients with complex compliance requirements.

- August 2024: Payoneer acquired Skuad for USD 61 million, integrating the employer-of-record and remote payroll specialist into its global payments platform. The acquisition reflects growing demand for cross-border payroll solutions and gig economy workforce management capabilities.

- August 2024: CloudPay raised USD 120 million in funding to expand its global payroll platform capabilities, with significant focus on Asian markets including India. The funding round highlights investor confidence in cloud-based payroll infrastructure and API-driven service delivery models.

India Payroll Services Market Report Scope

Payroll services refer to the external company or department within a company that manages various aspects of employee compensation. These services typically include calculating wages, withholding taxes and other deductions, distributing payments to employees, filing payroll taxes, and generating reports for accounting purposes. Outsourcing payroll services can help businesses ensure compliance with tax regulations, streamline payroll processes, and free up internal resources for other tasks. Key types in Indian payroll services include hybrid and fully outsourced.

The Indian payroll services market is segmented by type, organization size, and by end-user. Types include hybrid and fully outsourced payroll services. By organization size, there are small and medium-sized enterprises and large enterprises. The report delves into market sizes and forecasts for end-user industries such as BFSI, consumer & industrial products, IT & telecommunications, public sector, healthcare, and others. For each segment, the market size is provided in terms of value (USD).

| Small-Size Companies |

| Mid-Size Companies |

| Large Enterprises |

| Healthcare |

| Manufacturing |

| Retail |

| Hospitality |

| Information Technology |

| Finance & BFSI |

| Professional Services |

| North India |

| West India |

| South India |

| East India |

| Central India |

| North-East India |

| By Company Size | Small-Size Companies |

| Mid-Size Companies | |

| Large Enterprises | |

| By End User Industry | Healthcare |

| Manufacturing | |

| Retail | |

| Hospitality | |

| Information Technology | |

| Finance & BFSI | |

| Professional Services | |

| By Geography | North India |

| West India | |

| South India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

What is the forecast value of the india payroll services market in 2031?

The India payroll services market is projected to reach USD 2.74 billion by 2031.

Which company size segment will grow fastest to 2031?

Small-size companies are expected to post a 16.39% CAGR through 2031.

Why is retail the fastest-growing end-user vertical?

Organized retail formalization and expansion of store networks drive payroll outsourcing demand at a 15.05% CAGR.

Which region records the highest growth rate?

North-East India leads with a forecast 17.45% CAGR thanks to formalization incentives.

What technological shift is reshaping payroll services?

API-enabled real-time compliance and UPI-based instant disbursements are redefining service expectations.

Page last updated on: