Smart Cities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

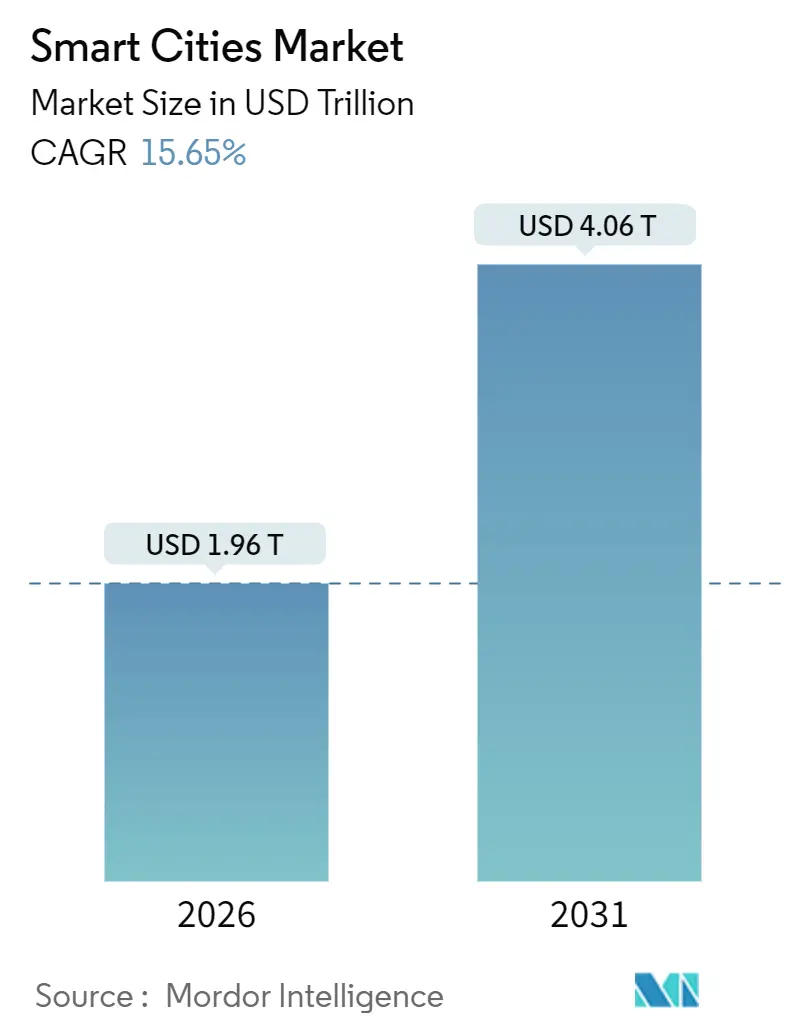

| Market Size (2026) | USD 1.96 Trillion |

| Market Size (2031) | USD 4.06 Trillion |

| Growth Rate (2026 - 2031) | 15.65% CAGR |

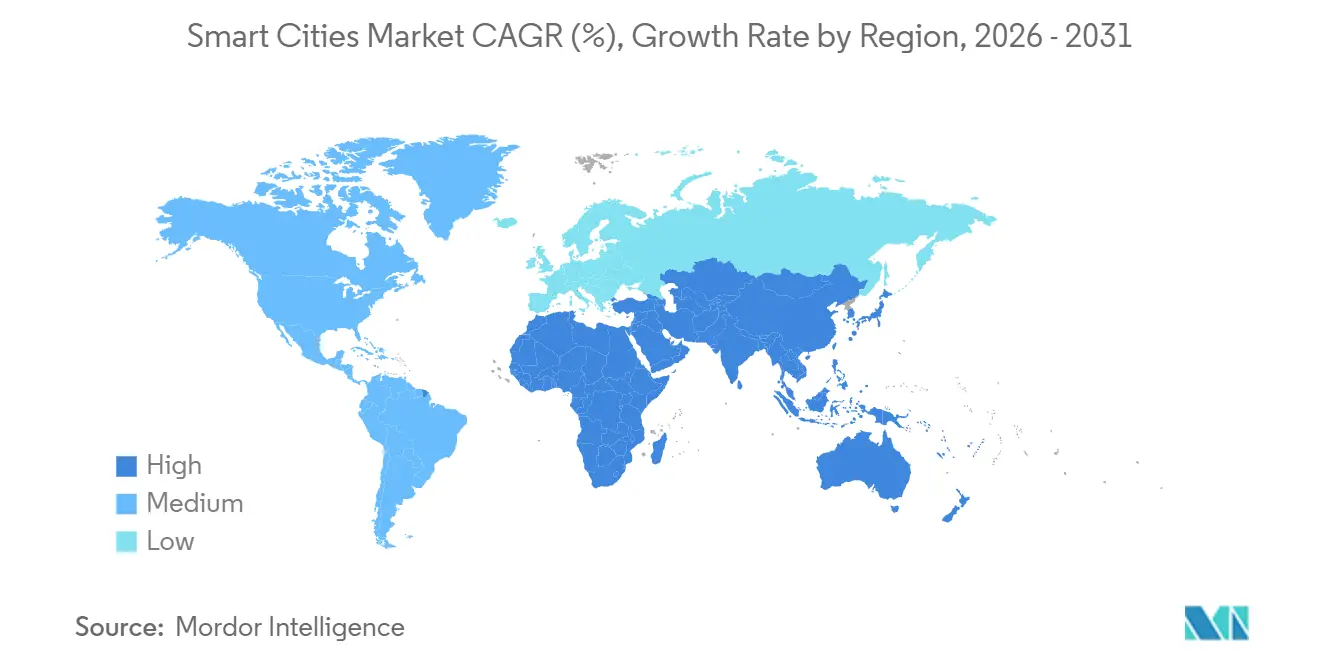

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Cities Market Analysis by Mordor Intelligence

The smart cities market size is valued at USD 1.96 trillion in 2026 and is projected to reach USD 4.06 trillion in 2031, translating into a 15.65% CAGR over the forecast period. Growing sovereign-data policies, generous national grant programs, and escalating climate-resilience mandates are steering procurement toward interoperable, domestically hosted platforms. Asia Pacific currently anchors the largest revenue pool, yet Africa’s leapfrog deployments are generating the fastest percentage growth. Hardware spending still dominates, but a clear pivot toward subscription-based analytics is transferring value to software vendors. Meanwhile, hybrid cloud architectures are moving into the mainstream as municipalities seek both compliance and scalability.

Key Report Takeaways

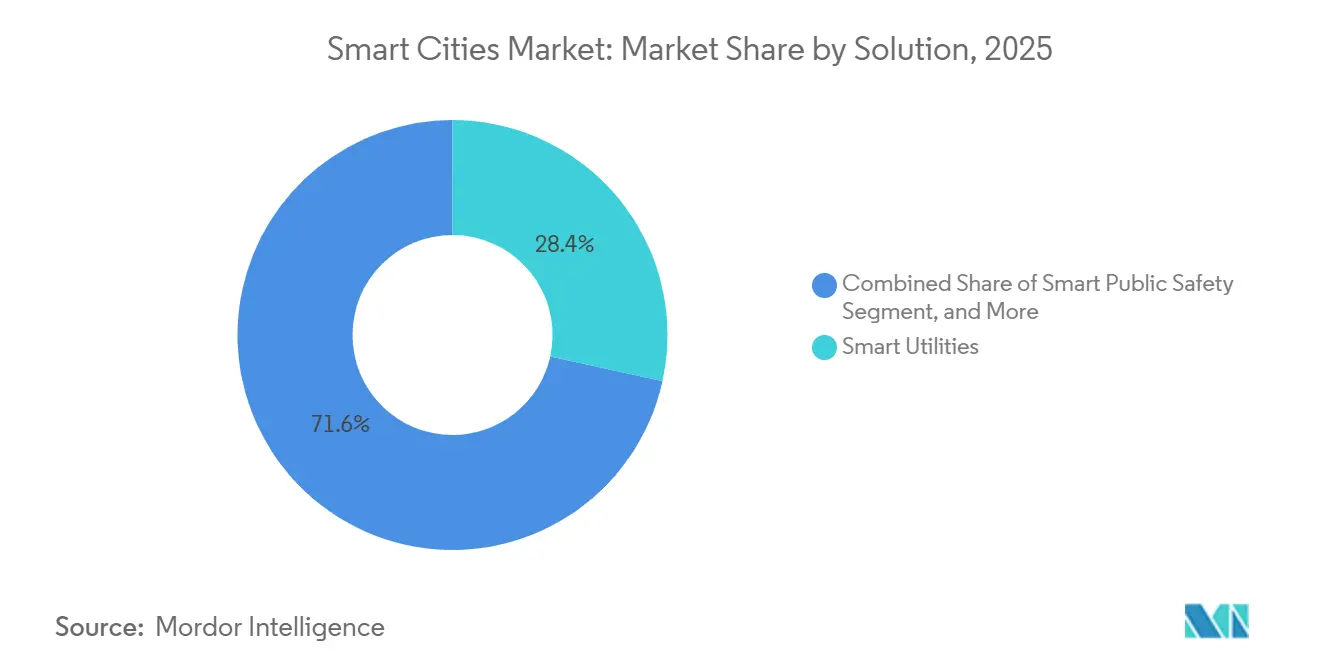

- By solution, smart utilities held 28.44% revenue share in 2025 while smart public safety systems are expected to post the fastest 17.24% CAGR to 2031.

- By component, hardware captured 54.46% of the smart cities market share in 2025, whereas software platforms are forecast to advance at a 16.24% CAGR through 2031.

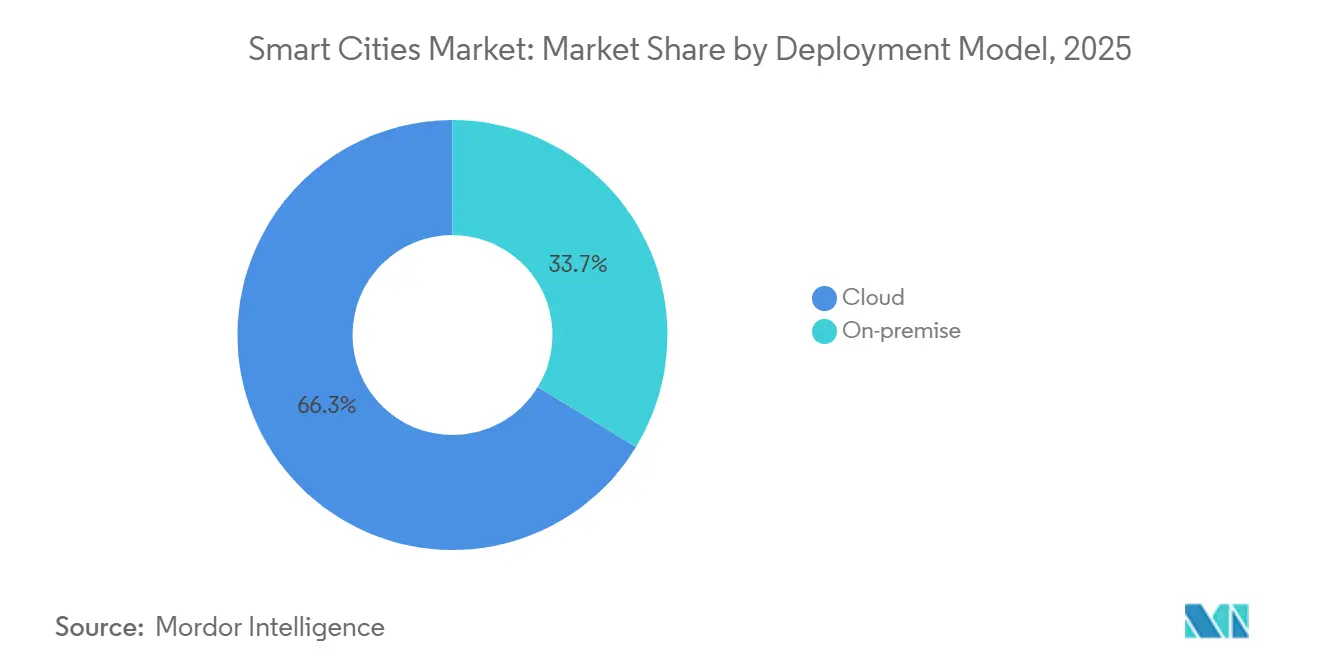

- By deployment model, cloud solutions controlled 66.28% of spending in 2025 and are poised to expand at a 17.86% CAGR, outpacing on-premise alternatives.

- By end-user, government accounted for 48.34% of demand in 2025, yet transportation and logistics operators represent the fastest-growing segment with a 16.16% CAGR through 2031.

- By geography, Asia Pacific generated 39.58% of smart cities market revenue in 2025, Africa is projected to record an 18.09% CAGR through 2031, the highest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Cities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Government Funding for Integrated Infrastructure | +3.2% | Global, with concentration in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Rising Adoption of AI and IoT Platforms | +3.8% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Climate-Resilience Mandates Elevating Sensor Deployments | +2.7% | Global, with emphasis on coastal cities in North America, Europe, and Asia Pacific | Long term (≥ 4 years) |

| Data-Driven Urban Services Demand in Megacities | +2.9% | Asia Pacific, Middle East, and South America megacities | Medium term (2-4 years) |

| Energy-Positive District Pilots Accelerating Utilities Spend | +1.9% | Europe and North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Digital-Twin Adoption Shortening Municipal Procurement Cycles | +2.1% | North America and Europe, with pilot programs in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Government Funding for Integrated Infrastructure

Multi-modal grant programs are shifting risk from local balance sheets to national budgets. The United States ARPA-I has earmarked USD 2 billion for proof-of-concept projects that combine electric-vehicle charging, smart streetlights and storm-water sensors within shared conduit, cutting installation costs by nearly 40%.[1]United States Department of Energy, “ARPA-I Integrated Infrastructure Funding,” energy.gov The United Kingdom’s Local Digital Fund committed GBP 500 million (USD 635 million) in 2025 to standardize application programming interfaces across council services, giving residents single-portal access to parking permits and waste-collection schedules.[2]UK Government Digital Service, “Local Digital Fund,” gov.uk Japan’s Digital Agency allotted USD 1.2 billion to reinforce mid-tier cities with fiber backhaul and edge compute nodes that double as disaster-response hubs. Collectively, these programs accelerate adoption in municipalities that lack bonding authority, smoothing the near-term revenue curve for vendors across the smart cities market.

Rising Adoption of AI and IoT Platforms

Cities are moving from descriptive dashboards to prescriptive analytics that automate resource allocation. Singapore’s Smart Nation machine-learning models predicted bus crowding with 92% accuracy in 2025, trimming average commute times by 11 minutes. ITU’s Y.4000 standards, ratified in 2024, unlocked true plug-and-play interoperability, letting procurement teams swap out sensors without being locked into monolithic suites. Munich’s open-source digital twin processed 2.3 billion sensor readings to optimize snow-removal routes, slashing fuel use by 18% and saving EUR 4.2 million (USD 4.6 million) in overtime. Such examples validate the value proposition and shorten payback periods, spurring incremental demand in the smart cities market.

Climate-Resilience Mandates Elevating Sensor Deployments

Updated climate-adaptation rules are turning real-time sensing from a nice-to-have into a regulatory requirement. The European Union now obliges every city above 100,000 residents to publish live flood forecasts by 2027, a move driving mass procurement of ultrasonic level sensors and predictive hydrology models. New York City’s FloodNet expanded to 500 intersections in 2025, enabling early closure of subway entrances and cutting evacuation delays by 22%. Tokyo’s 2024 ordinance injected indoor air-quality sensors into new commercial buildings, feeding geospatial dashboards that inform traffic-restriction policies during high-ozone days. These mandates steadily lift the baseline spend on environmental monitoring within the smart cities market.

Data-Driven Urban Services Demand in Megacities

Population density exceeding 10 million residents pushes analog service models to their limits. São Paulo’s route-optimization software lowered garbage-truck mileage by 14% and saved BRL 38 million (USD 7.6 million) in fuel in 2025. The World Bank’s Global Platform for Sustainable Cities offers concessional financing to projects that deliver measurable cost savings inside two years, nudging administrators to prioritize data-centric solutions. Shenzhen’s traffic-management center integrates feeds from 18,000 cameras, cutting average intersection wait times by 19% in 2025. These hard cost reductions reinforce the business case for continuous investment across the smart cities market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Retrofit and Integration Costs | -2.4% | Global, particularly acute in North America and Europe legacy cities | Short term (≤ 2 years) |

| Cyber-Security and Data-Privacy Concerns | -1.8% | Global, with heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Municipal Debt-Ceiling Pressure Post-COVID | -1.3% | North America, Southern Europe, and select South American cities | Short term (≤ 2 years) |

| Political Resistance to Urban Surveillance Analytics | -0.9% | North America and Europe, with localized opposition in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Retrofit and Integration Costs

Legacy assets in mature cities lack spare conduit, power capacity or network backhaul, forcing expensive civil works before sensor rollouts. The American Society of Civil Engineers pegged vehicle-to-infrastructure upgrades at USD 175,000-250,000 per intersection in 2025, roughly four times the greenfield cost. Chicago’s smart-streetlight initiative absorbed USD 18 million in unforeseen transformer upgrades, delaying completion by 14 months.[3]City of Chicago, “Smart Streetlight Program Update,” chicago.gov Integration complexity further inflates budgets as municipalities translate data from decades-old SCADA systems into cloud-ready formats, often requiring bespoke middleware that adds 15-25% to licensing fees. These barriers can postpone deal closure and slow initial uptake in the smart cities market.

Cyber-Security and Data-Privacy Concerns

High-profile breaches elevate cyber security from an IT matter to a political flashpoint. The 2024 ransomware attack on Dallas prompted the United States Cybersecurity and Infrastructure Security Agency to demand air-gapped backups for all federally funded smart-city projects, raising total system costs. Under GDPR, European cities must anonymize facial data within 90 days, pushing compute to the edge and reducing algorithm accuracy by up to 12% relative to cloud processing. Baltimore canceled its aerial-surveillance pilot in 2025 because of privacy concerns, underlining how regulatory uncertainty can strand investments. As a result, procurement teams often favor vendors that bundle zero-trust architectures and third-party penetration testing, adding expense and lengthening sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Utilities Modernization Drives Near-Term Revenue While Public Safety Gains Momentum

Smart utilities represented 28.44% of total revenue in 2025, buoyed by mandates for advanced metering and automated fault isolation. The United States Department of Energy’s Grid Resilience and Innovation Partnerships program alone released USD 3.5 billion to projects that demonstrate real-time voltage optimization, slicing outage durations by up to 50%. Smart public safety solutions are set to deliver the fastest 17.24% CAGR, as municipalities deploy interconnected gunshot-detection microphones and AI-based crime prediction. For instance, the Los Angeles Police Department’s upgraded real-time crime center cut property-crime response times by 14% in 2025.

Multiple adjacent domains round out the portfolio. Smart mobility takes advantage of Society of Automotive Engineers V2X protocols standardized in 2024, improving traffic-signal coordination and reducing congestion. Smart buildings rely on automated HVAC and occupancy analytics that hit a typical three-year payback. Pilot smart healthcare kiosks in underserved neighborhoods demonstrate early success in trimming emergency-room backlog. Smart security applications address perimeter protection for water-treatment plants and substations, leveraging Transportation Security Administration pipeline directives to justify investment. Together these subcategories reinforce the breadth of the smart cities market.

By Component: Hardware Dominates Spending but Software Captures Value Migration

Hardware commanded 54.46% of 2025 outlays, reflecting the tangible nature of sensors, cameras and edge servers that deliver instant visibility. Bosch magnetometer parking nodes, deployed across 120 cities, cut average parking search time by eight minutes and trimmed local emissions by 2.3% in pilot zones. In contrast, software platforms are forecast to climb at a 16.24% CAGR, as municipalities pivot toward subscription fees that bundle analytics updates and security patches. Microsoft's Azure Digital Twins gave 18 cities the ability to simulate congestion-pricing zones in silico, helping avoid politically risky missteps.

Services bridge the two worlds, especially for smaller municipalities lacking deep IT benches. The Linux Foundation reports 340 municipal installations of its open-source FIWARE and CityGML frameworks as of 2025, up from 210 a year earlier, signaling confidence in community-supported stacks. The shift toward software-defined infrastructure further weakens vendor lock-in, letting cities change analytics vendors without ripping out hardware, a trend that structurally benefits the smart cities market.

By Deployment Model: Cloud Gains Share as Sovereignty Concerns Drive Hybrid Architectures

Cloud deployments captured 66.28% smart cities market share in 2025 and are expected to sustain a 17.86% CAGR to 2031. Amazon Web Services expanded GovCloud to new jurisdictions, offering physically isolated regions that satisfy data-residency requirements while preserving access to AI accelerators. Germany’s Federal Office for Information Security recommends hybrid architectures that keep personally identifiable information on municipal servers and route anonymized workloads to public clouds, achieving compliance without forfeiting elasticity.

Edge computing blurs the traditional cloud-versus-on-premise line. Verizon’s Mobile Edge Compute, live in 45 United States cities, enables autonomous-vehicle coordination with sub-20-millisecond latency. International standards such as ISO 27001 and the NIST Cybersecurity Framework now appear explicitly in request-for-proposal language, giving certified vendors a bidding advantage. These developments entrench a long-run preference for hybrid deployments inside the smart cities market.

By End-User: Government Anchors Demand While Logistics Operators Accelerate Adoption

Government and municipal departments generated 48.34% of 2025 revenue, motivated by rising service-quality expectations amid flat tax receipts. Conversely, transportation and logistics operators are projected to grow at a 16.16% CAGR through 2031. UPS integrates its ORION route-optimization with adaptive traffic signals in 80 cities, saving 10 million gallons of fuel annually and trimming delivery times by 6%.

Commercial building owners adopt demand-response systems that cut energy bills in real time, with Honeywell logging a 22% uptick in enterprise deployments during 2025. Utilities play a dual role as adopters and infrastructure hosts, renting pole space and fiber pairs to city IT departments. Duke Energy’s collaboration with AT&T to mount 5G radios on distribution poles exemplifies the convergence of power and telecom assets that underpins continued smart cities market expansion.

Geography Analysis

Asia Pacific generated 39.58% of smart cities market revenue in 2025, underpinned by China’s mandate to establish 500 smart cities by 2030. The Ministry of Housing and Urban-Rural Development requires every city above 1 million residents to operate an integrated command center, accelerating demand for domestic platforms offered by Huawei and Alibaba Cloud. India’s Smart Cities Mission disbursed INR 480 billion (USD 5.8 billion) across 100 municipalities, showing measurable congestion reductions of 16% on pilot corridors. Japan’s Society 5.0 funded 23 digital-twin pilots in 2025, including a Tokyo model that simulates earthquake evacuations in near real time.

Africa is projected to record an 18.09% CAGR through 2031, the highest worldwide. The African Development Bank’s USD 2.5 billion African Urban Agenda prioritizes water-loss detection and prepaid metering. Cape Town’s smart water grid plugged leaks fast enough to defer a ZAR 4.2 billion (USD 230 million) desalination plant. Kigali’s city-wide IoT backbone, built with Korea Telecom, reduced lighting and waste-collection costs by 12%. These leapfrog deployments validate software-defined infrastructure in bandwidth-constrained environments, propelling the smart cities market across frontier economies.

North America benefits from federal cost-sharing programs but contends with fragmented procurement rules. Europe’s focus on open-source and data sovereignty drives uptake of locally hosted clouds, underwritten by the EUR 7.5 billion (USD 8.76 billion) Digital Europe Programme. The Middle East is building showcase greenfield cities such as NEOM that embed autonomous mobility and blockchain land registries from day one. South America relies on concession models; São Paulo alone attracted USD 420 million in private capital for smart lighting in 2024. Collectively, these patterns diversify addressable revenue streams, adding resilience to the global smart cities market.

Competitive Landscape

Moderate concentration defines the competitive arena. Siemens and Schneider Electric monetize existing building-automation and grid-management footprints, cross-selling smart-city modules to entrenched customers. Cisco and Huawei bundle networking gear with traffic-management and video-analytics software, whereas hyperscalers like Microsoft, AWS and Alibaba Cloud offer municipal-specific compliance tiers that shorten time-to-deployment. An IEEE patent review shows Chinese firms filed 42% of smart-city patents in 2025, highlighting an innovation tilt toward Asia Pacific.

White-space remains in interoperability middleware. Vendors such as Itron and Sensus specialize in translating legacy SCADA protocols into modern APIs, partnering with equipment incumbents to win retrofit contracts. Startups including Rubicon for waste routes and Remix for transit planning deliver verticalized solutions that prove value inside one budget cycle, challenging monolithic suites. The spread of open-source frameworks like FIWARE loosens vendor lock-in, forcing incumbents to compete on managed services and outcome-based pricing.

Regulatory compliance is fast becoming a decisive differentiator. Vendors that document third-party ISO 27001 audits and continuous vulnerability scanning now clear procurement gates more smoothly. Simultaneously, sovereign-data rules motivate suppliers to carve out national data centers or hybrid deployment modes, a service layer that smaller rivals struggle to replicate. The competition dynamic, therefore, revolves less around hardware innovation and more around platform breadth, compliance assurance, and service quality, reinforcing the evolving nature of the smart cities market.

Smart Cities Industry Leaders

Cisco Systems Inc.

Siemens AG

Huawei Technologies Co. Ltd.

Schneider Electric SE

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Siemens secured a EUR 380 million (USD 415 million) contract with the City of Berlin to build an integrated operations center scheduled for completion in 2027.

- September 2025: Microsoft partnered with India’s central government to roll out Azure digital-twin tools in 25 Smart Cities Mission municipalities, coupled with training for 5,000 public-sector IT staff.

- August 2025: Schneider Electric bought a 60% stake in GridBeyond for EUR 120 million (USD 131 million), adding virtual power plant capabilities to its portfolio.

- July 2025: Huawei committed USD 500 million to open a smart-city R and D hub in Shenzhen focused on 5G-Advanced and AI-based video analytics.

Global Smart Cities Market Report Scope

A smart city is an urban area that uses different types of electronic methods and sensors to collect data. Insights gained from that data are used to manage assets, resources, and services efficiently. This data is used to improve operations across the city.

The Smart Cities Market Report is Segmented by Solution (Smart Mobility Management, Smart Public Safety, Smart Healthcare, Smart Building, Smart Utilities, Smart Security, Others), Component (Hardware, Software, Services), Deployment Model (Cloud, On-Premise), End-User (Government and Municipal, Residential, Commercial and Industrial, Transportation and Logistics, Utilities Providers, Other End-User), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smart Mobility Management |

| Smart Public Safety |

| Smart Healthcare |

| Smart Building |

| Smart Utilities |

| Smart Security |

| Other Solutions |

| Hardware |

| Software |

| Services |

| Cloud |

| On-Premise |

| Government and Municipal |

| Residential |

| Commercial and Industrial |

| Transportation and Logistics |

| Utilities Providers |

| Other End-User |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Solution | Smart Mobility Management | |

| Smart Public Safety | ||

| Smart Healthcare | ||

| Smart Building | ||

| Smart Utilities | ||

| Smart Security | ||

| Other Solutions | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-Premise | ||

| By End-User | Government and Municipal | |

| Residential | ||

| Commercial and Industrial | ||

| Transportation and Logistics | ||

| Utilities Providers | ||

| Other End-User | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the smart cities market in monetary terms?

The smart cities market size stands at USD 1.96 trillion in 2026 and is forecast to reach USD 4.06 trillion by 2031.

Which solution area generates the most revenue for cities today?

Smart utilities currently lead, holding 28.44% of total revenue due to advanced metering and grid-modernization mandates.

Which segment is expanding the fastest through 2031?

Smart public safety platforms are projected to grow at a 17.24% CAGR as municipalities adopt AI-enabled video analytics and gunshot detection.

Why is cloud deployment gaining share in municipal projects?

Cloud services combine compliance-ready data residency with scalable AI toolkits, driving a 17.86% CAGR while meeting sovereignty mandates.

Which region is expected to see the quickest growth?

Africa is set to post an 18.09% CAGR through 2031 as cities leapfrog legacy infrastructure and deploy 5G-anchored broadband and solar-powered sensors.

How are suppliers differentiating themselves amid rising competition?

Vendors now compete on compliance certifications, open-API interoperability and managed service guarantees rather than hardware alone.

Page last updated on: