Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 70.82 Billion |

| Market Size (2031) | USD 91.47 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

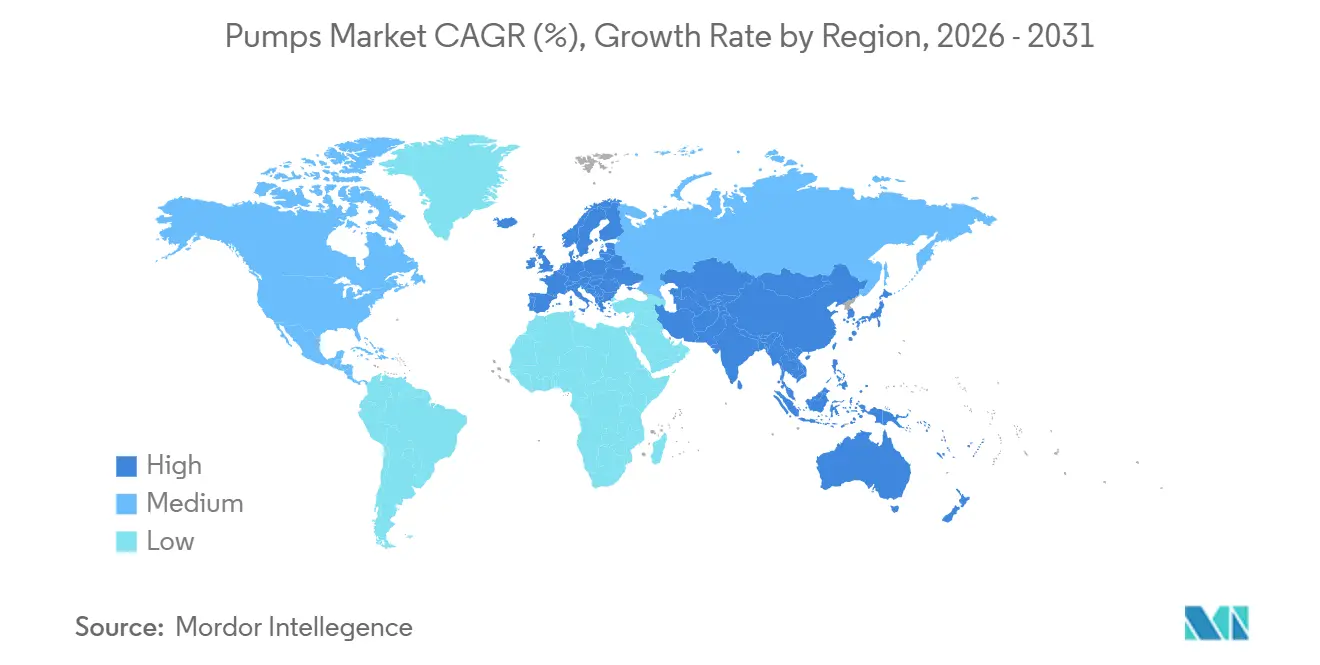

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

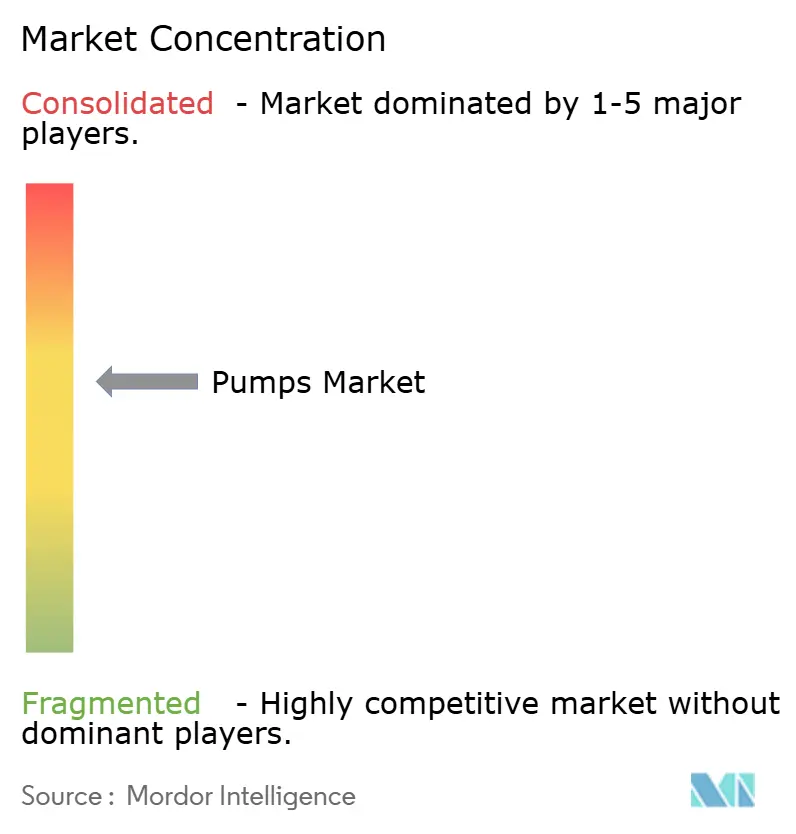

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pumps Market Analysis by Mordor Intelligence

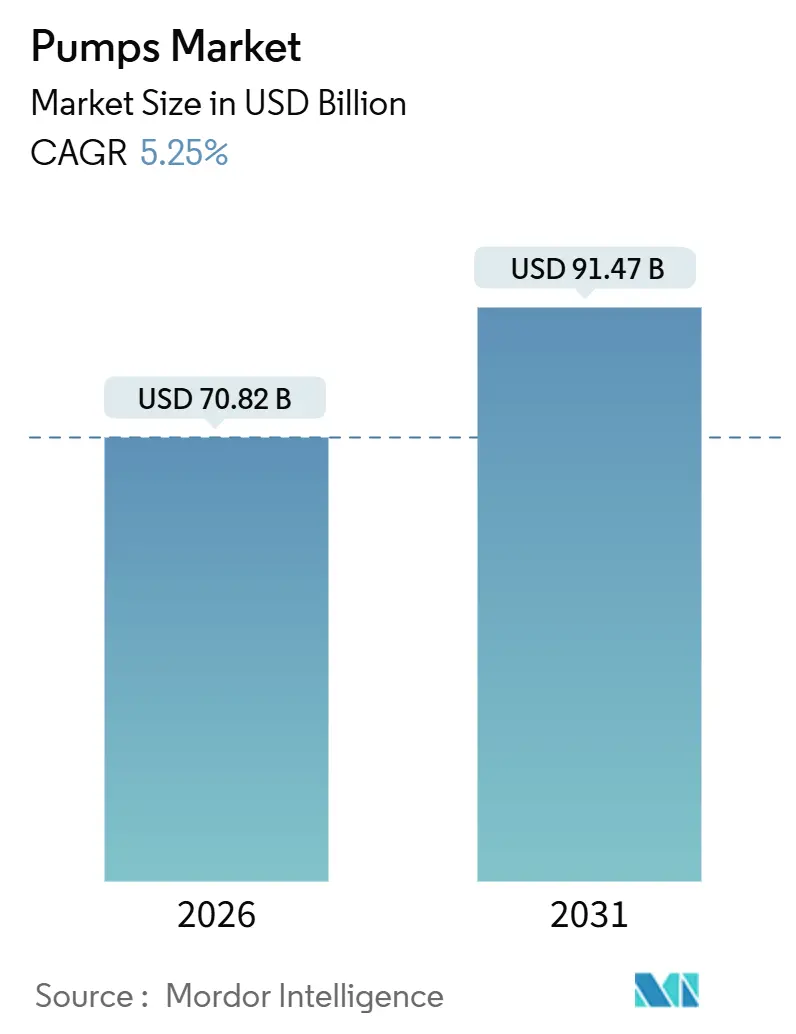

The Pumps Market size is estimated at USD 70.82 billion in 2026, and is expected to reach USD 91.47 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

Sustained spending on municipal water systems, escalating CAPEX for desalination across MENA and Asia-Pacific, and regulatory pressure for tertiary wastewater treatment in Europe are anchoring unit volumes. At the same time, solar-powered systems for off-grid irrigation and the gradual adoption of magnetically driven sealless designs in bioprocessing are reshaping the competitive playbook. Chinese manufacturers continue to compress margins in standardized centrifugal lines, compelling Western incumbents to focus on engineered-to-order niches and digital service overlays. Raw-material volatility, particularly nickel-linked duplex stainless steel, remains the principal earnings headwind for mid-tier assemblers, while thermal-coal retirements in OECD countries curb circulation-pump replacements. Across these cross-currents, the pump market maintains mid-single-digit growth visibility thanks to desalination, shale midstream additions, and district cooling projects that require large, high-reliability units.

Key Report Takeaways

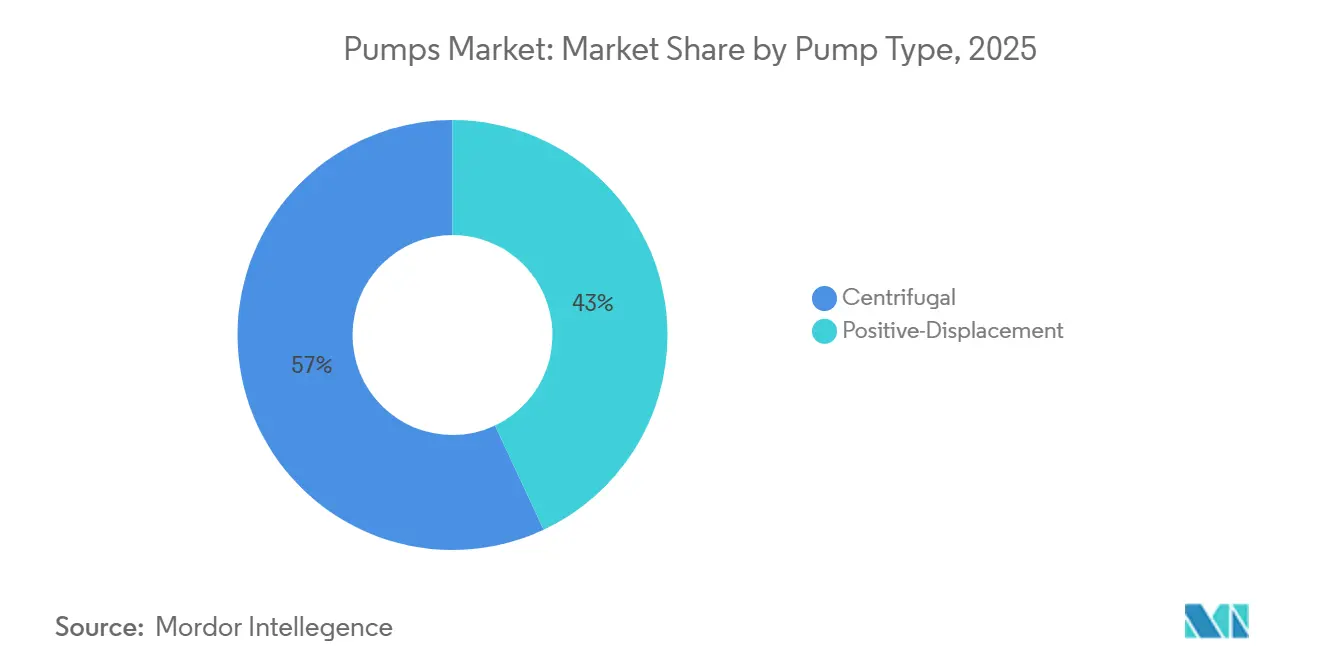

- By pump type, centrifugal designs captured 56.97% of 2025 revenue in the pump market share and are forecast to advance at a 6.00% CAGR through 2031.

- By drive technology, electric-motor installations accounted for 74.90% of the pump market size in 2025, while solar and other renewables delivered the highest 9.30% CAGR to 2031.

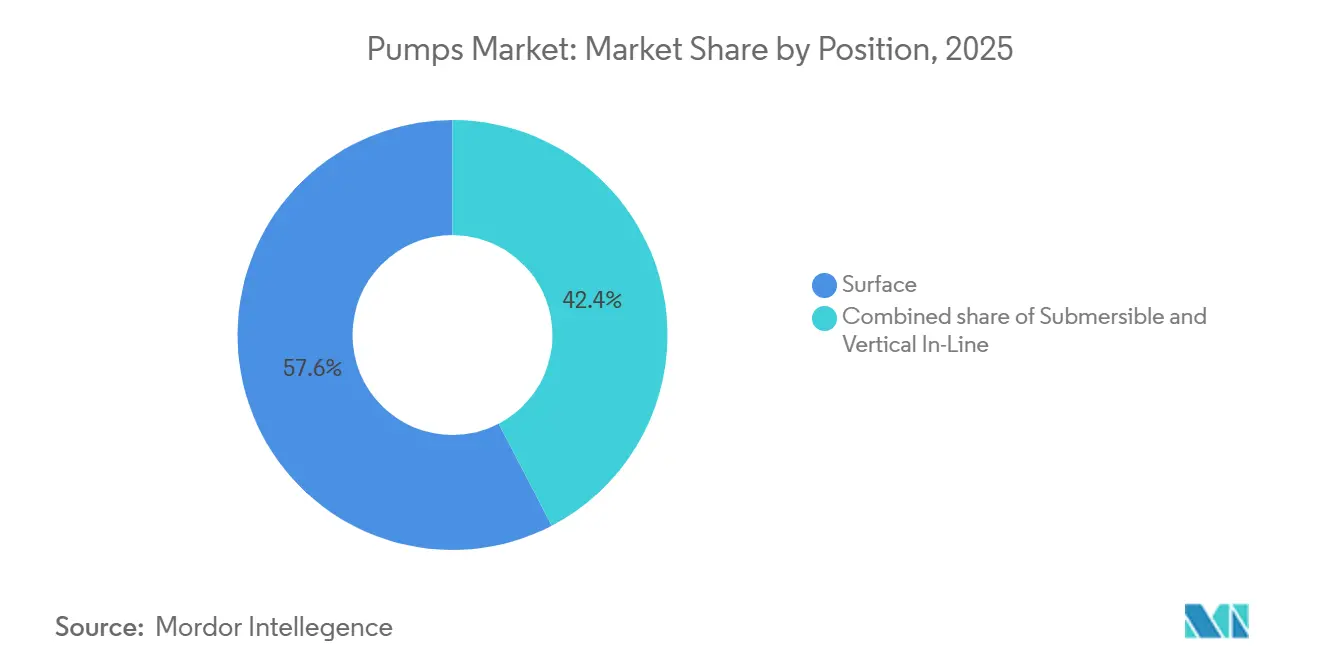

- By position, surface pumps held a 57.63% pump market share in 2025; submersible variants register the fastest 8.30% CAGR through 2031.

- By application, water and wastewater commanded 52.11% of the pump market size in 2025 and will grow at 5.85% through 2031.

- By geography, Asia-Pacific generated 53.27% of 2025 revenue and is expected to post a 5.90% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating CAPEX in Desalination Projects across MENA & APAC | 1.2% | MENA core (Saudi Arabia, UAE, Qatar), APAC (India, China coastal provinces) | Medium term (2-4 years) |

| Stringent Wastewater Reuse Mandates in Europe & North America | 0.9% | EU-27, United Kingdom, United States, Canada | Short term (≤ 2 years) |

| Rapid Expansion of Shale & Deepwater O&G Projects in US Gulf & Brazil | 0.8% | United States (Gulf of Mexico, Permian Basin), Brazil (Santos Basin pre-salt) | Long term (≥ 4 years) |

| Surging District Cooling & Heating Installations in Nordics & Middle East | 0.7% | Nordic countries (Sweden, Denmark, Finland), Middle East (UAE, Qatar, Saudi Arabia) | Medium term (2-4 years) |

| Electrification of Agricultural Irrigation (Solar Pumps) in India & Africa | 0.7% | India (Rajasthan, Gujarat, Maharashtra), Sub-Saharan Africa (Kenya, Ethiopia, Nigeria) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating CAPEX in Desalination Projects across MENA & APAC

Saudi Arabia’s National Water Strategy directs USD 13 billion to reverse-osmosis capacity through 2030, pulling forward demand for high-pressure centrifugal units with duplex stainless-steel internals that resist chloride stress cracking. The UAE’s Abu Dhabi Water and Electricity Authority awarded a USD 1.1 billion contract in March 2025 for the Taweelah RO-3 plant, which specifies 12 multistage centrifugal pumps rated at 1,200 m³/h each. India’s Jal Jeevan Mission earmarked INR 60,000 crore (USD 7.2 billion) in 2025-26 for coastal desalination pilots, mandating energy-recovery devices that cut lifecycle pumping costs by up to 30%. China’s 14th Five-Year Plan adds 2.9 million m³/day of desalination by 2027, with utilities pre-qualifying pump OEMs under ISO 9001 and API 610 standards. Each 100,000 m³/day module demands 8-12 feed pumps plus matching brine-circulation units, advancing near-term bookings for centrifugal lines.

Stringent Wastewater Reuse Mandates in Europe & North America

The EU’s updated Urban Wastewater Treatment Directive obliges tertiary treatment for towns above 10,000 population equivalents by December 2030, prompting 6,200 facilities to retrofit 4-6 additional variable-frequency-drive pumps per site.[1]European Commission, “Urban Wastewater Treatment Directive Revision,” europa.eu In California, the 2023 Water Resilience Portfolio targets 30% recycled-water use by 2030, releasing USD 2.8 billion for treatment-plant upgrades that incorporate booster pumps to compensate for membrane pressure drops. Pending U.S. PFAS limits will force 12,000 public systems to install new pumping stages linked to granular activated carbon trains. Utilities favor OEMs offering corrosion-resistant alloys and IE3-plus motor efficiencies, accelerating order flow in the short term.

Rapid Expansion of Shale & Deep-water O&G Projects in US Gulf & Brazil

US Gulf of Mexico output is set to reach 2.1 million bpd by 2027, raising demand for electric submersible pumps certified to 10,000 psi.[2]U.S. Energy Information Administration, “Gulf of Mexico Oil Production Forecast,” eia.gov Petrobras has allocated USD 102 billion through 2029 to pre-salt developments that each require 30-40 API 610 centrifugal pumps for crude transfer and seawater injection. Onshore, Permian midstream operators deploy multiphase pumps accommodating >90% gas-liquid ratios, with bookings up 22% year on year at Baker Hughes. Long project lead times provide visibility yet expose OEMs to commodity-price swings that can delay final investment decisions.

Surging District Cooling & Heating Installations in Nordics & Middle East

Dubai targets 1.2 million refrigeration tons of district cooling by 2030, each chiller plant using 600-1,200 kW circulation pumps sized for 3,000 m³/h flow. Sweden’s district heating penetration reached 91% of residences by 2025, prompting retrofits with variable-speed pumps that cut energy use 15-20%. Grundfos landed a EUR 18 million order in June 2025 for 240 IoT-enabled pumps across Helsinki’s 1,400-km network. Qatar’s Lusail plant employs 16 vertical in-line pumps rated at 450 kW each to serve 200,000 residents. Regulations such as EU Ecodesign and ASHRAE 90.1 are phasing out fixed-speed units, cementing growth for high-efficiency models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Nickel & Stainless-Steel Prices Inflating BoM | -0.6% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Proliferation of Low-cost Chinese Manufacturers Compressing Margins | -0.5% | Global, most pronounced in Asia-Pacific and Middle East municipal segments | Medium term (2-4 years) |

| Declining Thermal Power Pipeline in OECD Curtailing Circulation Pumps | -0.4% | OECD countries (Germany, UK, United States, Japan) | Long term (≥ 4 years) |

| Long Municipal Replacement Cycles (15–20 yrs) Limiting Annual Sales | -0.3% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Nickel & Stainless-Steel Prices Inflating BoM

Nickel spot prices rose 18% in Q1 2025 before easing 9% by year-end, pushing duplex stainless-steel surcharges up 7-11% at European mills.[3]London Metal Exchange, “Nickel Price Dashboard,” lme.com A 10% nickel move raises impeller and casing costs 4-6%, squeezing equipment margins 150-200 bp among mid-tier OEMs. Flowserve recorded a USD 42 million material-inflation headwind in 2024 despite escalation clauses on long-cycle orders. Smaller Asian fabricators lacking hedging programs face deeper margin erosion because material substitution is limited in chloride-rich or sour-gas services. Bid validity periods have shortened, and some contractors insist on owner-supplied materials to mitigate exposure.

Proliferation of Low-cost Chinese Manufacturers Compressing Margins

Chinese brands, including Leo, Shimge, and CNP, now hold 15-20% of global municipal and light-industrial volume, offering API 610-equivalent units at 60-70% of Western list prices and extending 24-month payment terms. Xylem cited lost bids in Indonesia and the Philippines due to aggressive pricing in its Q3 2024 earnings call. Grundfos responded with a lower-cost line launched in 2024 that trims the bill of materials by 15-20%. While engineered-to-order petrochemical and subsea pumps remain protected by metallurgical traceability and multi-year service contracts, Chinese entrants are reinvesting profits into R&D for high-temperature, high-pressure models that could erode this buffer after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Dominance Anchors Installed Base

Centrifugal designs accounted for 56.97% of 2025 revenue in the pump market and will register a 6.00% forecast CAGR on the back of desalination modules, municipal upgrades, and HVAC retrofits. The Ras Al Khair facility in Saudi Arabia alone operates 18 multistage centrifugal pumps rated at 1,800 m³/h, highlighting the scale advantage centrifugal frames command in high-flow, moderate-head duty.[4]Sulzer AG, “Ras Al Khair Desalination Reference Case,” sulzer.com Their mature supply chain, standardized footprints under ANSI B73.1 and ISO 2858, and broad aftermarket network cut lifecycle costs 20-30% relative to positive-displacement alternatives. Progressive-cavity, diaphragm, and gear pumps together form the remainder of the market, finding steady but niche growth in viscous-fluid and metering applications where self-priming or shear-sensitive handling is non-negotiable.

Positive-displacement models retain firm footholds in pharmaceuticals, dairy, and heavy-oil transfer. The US FDA’s 2024 guidance on continuous biologics manufacturing is pivoting facilities toward single-use diaphragm pumps that eliminate cross-contamination risk. In Canada’s Athabasca region, screw pumps able to lift 10,000 cP crude are replacing centrifugal units that stall under high viscosity. However, centrifugal units will continue to dominate the pump market size for water, wastewater, and HVAC thanks to modular designs, lower capital intensity, and easier field maintenance.

By Drive Technology: Electric Motors Lead, Solar Surges

Electric motors powered 74.90% of installations in 2025, a share expected to erode only modestly as IE3 and IE4 efficiency mandates accelerate retrofits across Europe and North America. Variable-frequency drives integrated with induction motors can slash energy draw 20-30% by matching pump speed to real-time demand. Diesel and gas engines now mainly serve remote or emergency settings because compliance with Tier 4 Final and Stage V exhaust limits adds USD 8,000–15,000 in after-treatment costs above 56 kW.

Meanwhile, solar-driven configurations, a slender 6.50% of 2025 volume, are scaling fastest at a 9.30% CAGR. India’s PM-KUSUM subsidy has already deployed 1.8 million systems, shrinking farmer payback periods to four years. Pay-as-you-go models leveraging mobile money in Kenya, Ethiopia, and Nigeria distribute capital costs over 24–36 months, removing the upfront barrier for smallholders. At the premium end, magnetically driven sealless pumps serve life-science and fine-chemical plants where zero leakage outweighs 40-50% higher list prices; Flowserve logged a 12% jump in 2024 orders for such units. The drive-technology split consequently bifurcates: grid-tied electric motors hold entrenched positions in urban industry, solar expands off-grid acreage, and mag-drive variants protect high-value sterile-transfer niches.

By Position: Surface Pumps Prevail, Submersibles Gain in Deepwater

Surface-mounted pumps supplied 57.63% of 2025 shipments in the pump market, favored for ease of service and lower capex in municipal plants and HVAC loops. Horizontal split-case pumps dominate water-utility trunk lines because technicians can replace impellers without disturbing pipework, limiting outages to six hours. End-suction models account for most building-services installations under 30 kW, where compact footprints outweigh marginal efficiency gains.

Submersible units, 28.07% of 2025 demand, will clip along at an 8.30% CAGR to 2031 as deepwater projects in Brazil and the US Gulf of Mexico mature and municipal lift stations prioritize noise abatement. Petrobras plans to install 240 electric submersible pumps rated for 10,000 psi downhole duty through 2029. Xylem’s clog-resistant sewage models are extending the mean time between services to 36 months in urban lift stations. Vertical in-line units retain utility where floor space is constrained, yet coal retirements in OECD regions are thinning their installed base in thermal power settings. The position split, therefore, reflects a balance between maintenance access, energy efficiency, and duty depth, with submersibles climbing where suction-lift losses or acoustic limits dominate decision criteria.

By Application: Water and Wastewater Anchor Demand

Water and wastewater projects delivered 52.11% of 2025 revenue in the pump market and will advance at a 5.85% CAGR, reflecting aging mains in North America and mandated tertiary treatment across Europe. The American Water Works Association pegs US utility capex needs at USD 1 trillion by 2040, of which pumps comprise roughly 10%. Each reverse-osmosis train added under the EU desalination push necessitates eight or more 60-bar feed pumps, ensuring steady centrifugal order flow. Chemical and petrochemical sites, by contrast, are seeing delayed FIDs due to ethylene oversupply in China and the Middle East, limiting upside to a 4.90% CAGR.

HVAC and building services represent 11.20% of 2025 turnover and are rising at 5.10% on district cooling in Dubai, Doha, and Riyadh, plus heat-pump retrofits across Scandinavia. Oil and gas covers 9.80% of sales; growth tilts toward subsea artificial lift and shale midstream while onshore drilling retreats in North America. Mining, food and beverage, and life-science customers each carve out smaller but healthy niches, the latter benefiting from sealless designs that avoid batch contamination in biologics plants.

Geography Analysis

Asia-Pacific commanded 53.27% of the 2025 global revenue in the pump market and is projected to grow at a 5.90% CAGR to 2031. India’s Jal Jeevan Mission alone needs 2.5–3 million submersible borehole pumps plus 800,000 boosters for elevated storage, while PM-KUSUM underwrites solar sets for 3.5 million smallholders. China adds nearly 3 million m³/day of desalination by 2027 in Tianjin, Qingdao, and Dalian. Southeast Asian manufacturing growth at 8.3% is spurring industrial-process demand in Vietnam and Thailand.

Europe accounted for 21.40% of 2025 revenue and advances at a 4.70% CAGR. Tertiary-treatment retrofits under the Urban Wastewater Directive affect 6,200 plants, while decarbonizing district heating across Sweden and Denmark stimulates variable-speed pump upgrades. Coal retirements eliminate some boiler-feed replacements, yet Thames Water’s USD 5.5 billion Tideway Tunnel requires 36 large units by 2027.

North America held 14.60% of 2025 turnover, forecast to expand at 4.90%. Deepwater development, notably Shell’s Whale project and BP’s Mad Dog 2, locks in submersible orders, while California’s recycled-water mandate drives tertiary-treatment retrofits. Canada’s heavy-oil segment relies on progressive-cavity pumps, balancing lost thermal-coal circulation demand.

South America delivered 6.30% of 2025 sales and grew at 5.60% on Brazil’s pre-salt projects and Chilean copper mine expansions. Middle East and Africa, 4.43% of 2025 value, outpace at 6.10% CAGR thanks to desalination CAPEX and solar-pump rollouts in Kenya, Ethiopia, and Nigeria.

Competitive Landscape

The top five suppliers, Flowserve, Grundfos, Xylem, KSB, and Sulzer, collectively command roughly 30–35% of global revenue, evidencing moderate fragmentation in the pump market. Western leaders are migrating toward engineered-to-order niches requiring exotic metallurgy, API 610 compliance, and digital performance guarantees. Flowserve reported a 12% year-on-year rise in magnetically driven pump orders for bioprocessing in its 2024 filings. Chinese challengers such as Leo Group, Shimge, and CNP have grabbed up to 20% share in municipal and light-industrial tenders by pricing 20–30% below Western lists and matching warranty periods. To defend margins, Grundfos introduced a value-priced line in 2024 and invested EUR 250 million in a 120,000 m² Indian plant that will produce 1.2 million units annually by 2026.

Digitalization is now table stakes. Grundfos iSOLUTIONS counts 180,000 connected pumps transmitting real-time data to the cloud, lowering unplanned downtime by 25–30%. Xylem Vue monitors 1.2 million metering endpoints, feeding analytics that stretch asset life 15–20%. Smaller regional fabricators struggle to finance comparable platforms and may seek partnerships or consolidation. Value-chain newcomers include African pay-as-you-go solar financiers unbundling hardware from service and additive-manufacturing startups printing titanium impellers that trim lead time 60%.

In this landscape, hybrid solar-diesel packages for remote mining, digital twins for predictive maintenance in district heating, and modular desalination skids for island utilities represent white-space opportunities. Conversely, standardized water-distribution pumps face commodity pricing, with Chinese imports achieving 95% on-time delivery. Over the medium term, expect M&A centered on software or material science capabilities rather than pure capacity.

Pumps Industry Leaders

Flowserve Corporation

Grundfos Holding A/S

KSB SE & Co. KGaA

Sulzer Ltd.

Xylem Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AAON introduced Alpha-Class ECO, PRO, and EXTREME air-source heat pumps capable of full-capacity heating at 5 °F, creating new demand for variable-flow circulation sets.

- March 2025: Honeywell completed its USD 2.2 billion acquisition of Sundyne, bolstering its Energy and Sustainability Solutions division.

- January 2025: Liberty Energy and Cummins partnered to launch a variable-speed natural-gas engine designed for hydraulic-fracturing pump fleets, targeting mid-2025 rollout.

- December 2024: Sumitomo purchased PT Resource Equipment Indonesia, expanding its rental fleet of large mine-dewatering pumps.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global pumps market as the value generated from first-sale centrifugal and positive-displacement pumps, complete units only, supplied to industrial, municipal, agricultural, building-services, and energy customers worldwide. Devices such as dedicated medical infusion, microfluidic, and HVAC circulators rated below 0.5 hp are treated as separate niches and left outside the calculation.

Scope exclusion: Aftermarket spare parts, rental fleets, and pump-motor packages sold solely as finished HVAC circulators are excluded to preserve apples-to-apples comparability.

Segmentation Overview

- By Pump Type

- Centrifugal

- Positive-Displacement

- By Drive Technology

- Electric Motor

- Diesel/Gas Engine

- Solar/Renewable

- Magnetically-Driven/Sealless

- By Position

- Surface

- Submersible

- Vertical In-Line

- By Application

- Water and Wastewater

- Chemical and Petrochemical

- HVAC and Building Services

- Oil and Gas (Upstream, Midstream, Downstream)

- Food and Beverage

- Mining and Metals

- Power Generation (Thermal, Nuclear, Renewables)

- Pharmaceuticals and Biotech

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- NORDIC Countries

- Russia

- Turkey

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Nigeria

- Qatar

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews are held with pump design engineers at OEMs, procurement managers at EPC firms, water utility asset heads across Asia-Pacific and the Gulf, and regional distributors. These dialogues test desk-based assumptions, surface typical price bands by flow class, and flag adoption barriers that numbers alone cannot reveal.

Desk Research

We begin with publicly available cornerstones such as UN Comtrade shipment records, the Hydraulic Institute statistical yearbook, USGS mineral flow tables, Eurostat PRODCOM output runs, and trade association briefs from organisations such as the China General Machinery Association. Annual reports, 10-Ks, and investor decks supply segment revenue splits, while technical journals shed light on emerging efficiency mandates. Our analysts also interrogate paid resources, D&B Hoovers for company financials and Dow Jones Factiva for deal flow, to cross-check market share signals. This list is illustrative; many additional sources feed our evidence pool.

Market-Sizing & Forecasting

A top-down build anchored in national production plus net trade volumes is employed, which is then sense-checked through selective bottom-up roll-ups of quoted revenues from leading manufacturers. Key variables shaping the model include municipal water infrastructure capex, active rotary-rig counts, global industrial production indices, average selling-price movements, renewable-powered pump penetration, and five-year replacement cycles. Multivariate regression linked to these drivers produces the forecast, while scenario analysis captures swings in commodity prices and policy shifts. Where bottom-up gaps appear, price-per-unit benchmarks from field interviews are applied conservatively.

Data Validation & Update Cycle

Outputs move through anomaly checks, peer review, and senior analyst sign-off. Models refresh each year, and we trigger interim updates when material events, large infrastructure bills and major mergers, distort baselines. A final validation pass occurs immediately before publication so clients receive the freshest view.

Why Mordor's Pumps Market Baseline Proves Dependable

Published estimates often diverge because firms choose different pump classes, geographic mixes, and refresh rhythms.

Key gap drivers include narrower scope that omits agricultural solar sets, overly optimistic ASP escalation, or infrequent updates that miss 2024's input-cost dip. Mordor's page covers all mainstream pump architectures, applies price curves vetted with distributors, and resets assumptions annually, which keeps our 2025 value crisp.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 68.27 B (2025) | Mordor Intelligence | - |

| USD 61.32 B (2024) | Global Consultancy A | Excludes solar irrigation sets and uses biennial refresh |

| USD 59.65 B (2024) | Industry Publisher B | Relies mainly on customs codes, limited primary validation |

These contrasts show that our disciplined scope choices and yearly recalibration give decision-makers a balanced, transparent baseline they can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current global pump market size?

The pump market size reached USD 70.82 billion in 2026.

How fast is the pump market expected to grow?

Revenue is forecast to rise at a 5.25% CAGR, pushing value to USD 91.47 billion by 2031.

Which region leads demand for pumps?

Asia-Pacific generated 53.27% of 2025 revenue thanks to desalination build-outs and industrial expansion.

What pump type holds the largest market share?

Centrifugal models accounted for 56.97% of 2025 revenue.

Why are solar-powered pumps growing quickly?

Subsidies such as India’s PM-KUSUM and mobile-money financing in Africa cut ownership costs, fueling a 9.30% CAGR for solar drives.

Page last updated on: