Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

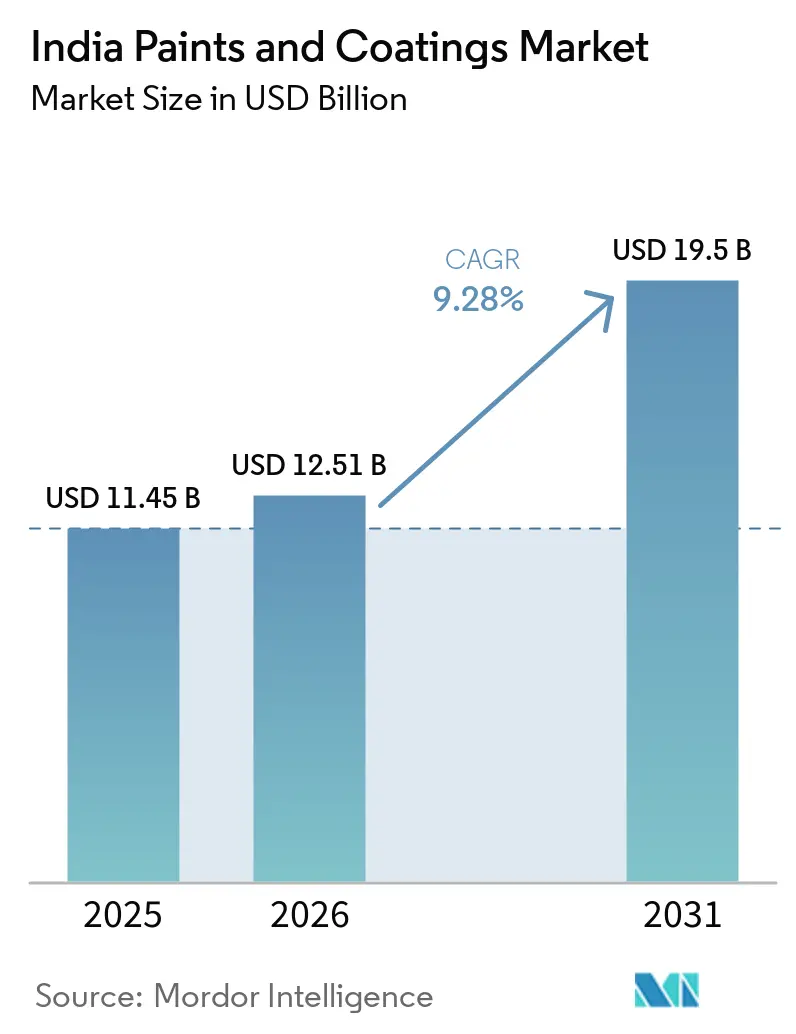

| Base Year Market Size (2025) | USD 11.45 Billion |

| Market Size (2026) | USD 12.51 Billion |

| Market Size (2031) | USD 19.5 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

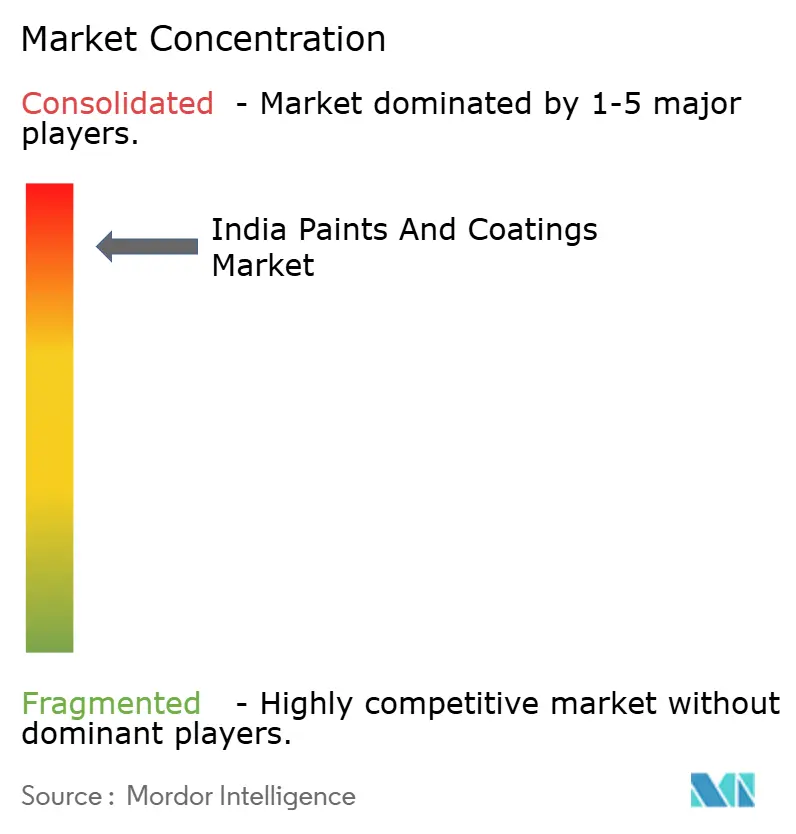

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Paints and Coatings Market Analysis by Mordor Intelligence

The India Paints and Coatings Market size is expected to increase from USD 11.45 billion in 2025 to USD 12.51 billion in 2026 and reach USD 19.5 billion by 2031, growing at a CAGR of 9.28% over 2026-2031. Sustained public-sector infrastructure spending, the rollout of production capacity that will nearly double by FY 2027, and deeper penetration into tier-II through tier-IV towns are combining to lift volumes even as competitive discounting squeezes margins. Enforcement of volatile organic compound (VOC) limits by the Bureau of Indian Standards (BIS) and the Central Pollution Control Board (CPCB) is steering formulators toward water-borne chemistries, while farm-to-factory migration and a rising urban middle class are shortening decorative repaint cycles. Capacity additions are already supporting economies of scale that lower per-liter production costs and enable wider dealer coverage. At the same time, organized waterproofing and protective coatings for highways, metros, and water infrastructure are opening new revenue pools for suppliers that can offer performance warranties and technical service.

Key Report Takeaways

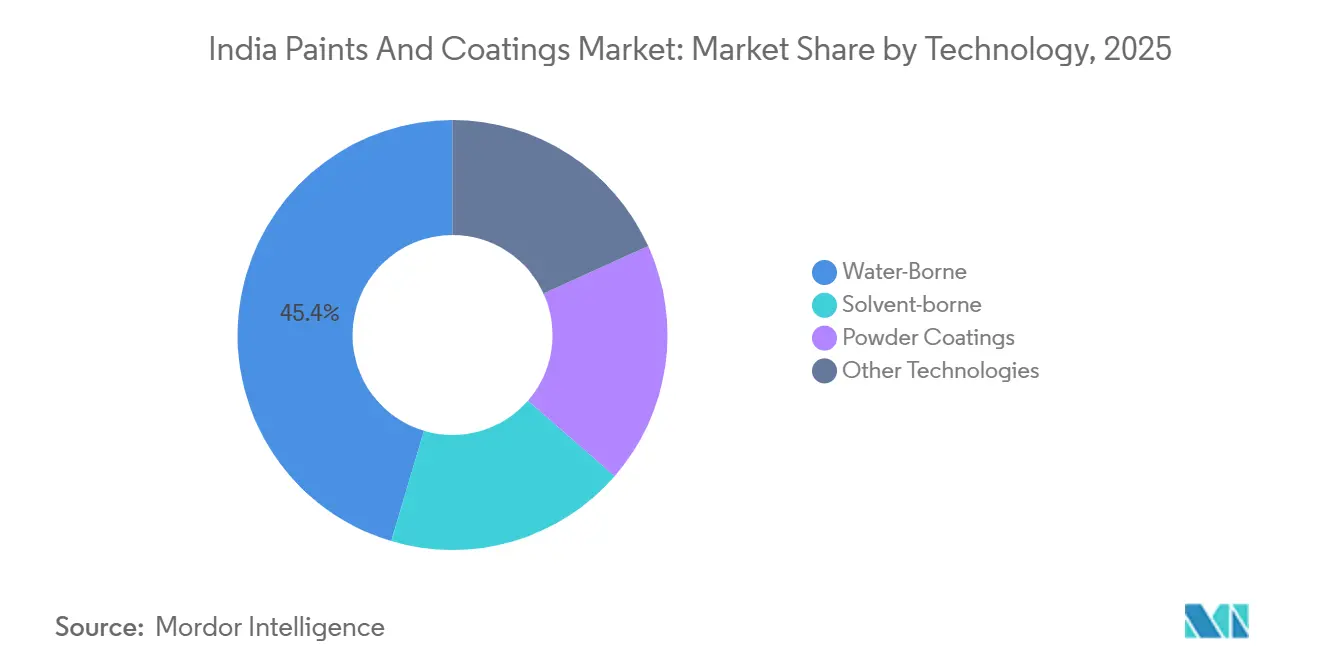

- By technology, water-borne coatings held 45.41% revenue share of the India paints and coatings market in 2025 and are projected to log the fastest 9.72% CAGR to 2031.

- By resin type, acrylic captured 36.48% of the India paints and coatings market share in 2025 and is forecast to expand at a 9.56% CAGR over 2026-2031.

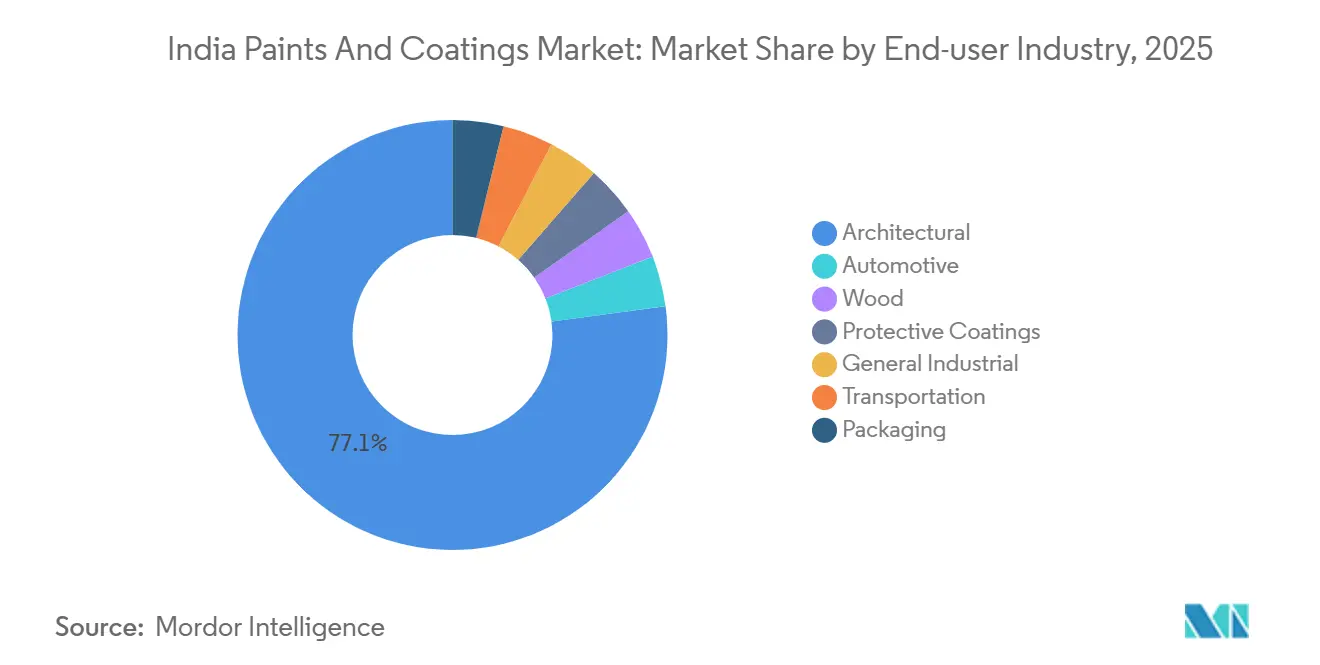

- By end-user industry, architectural applications accounted for 77.12% of the India paints and coatings market size in 2025 and are advancing at a 9.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Paints and Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Construction Pipeline (Housing and Infrastructure) | +3.2% | National, with concentration in tier-I/II cities and PMAY-targeted rural/semi-urban clusters | Medium term (2-4 years) |

| Shortening Decorative Re-paint Cycle among Urban Homeowners | +1.8% | Urban metros and tier-I cities; spillover to tier-II by 2028 | Long term (≥ 4 years) |

| Post-COVID Recovery in Automotive and Industrial Production | +1.5% | National, with automotive hubs in Maharashtra, Tamil Nadu, Gujarat leading | Short term (≤ 2 years) |

| Emergence of Organised Waterproofing After-market | +1.1% | Urban and coastal regions; expanding to tier-II/III towns | Medium term (2-4 years) |

| Capacity-Doubling Plans up to FY-27 Creating Economies of Scale | +1.4% | National; new plants in Odisha, Andhra Pradesh, West Bengal, Rajasthan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Construction Pipeline (Housing and Infrastructure)

In 2023-24, government capital expenditure surged, marking a threefold increase from FY 2015. Initiatives like the Smart Cities Mission, Bharatmala corridors, and metro-rail expansions are fueling a consistent demand for protective, floor, and architectural coatings. The Jal Jeevan Mission, which has provided rural tap-water connections, is spurring a heightened need for anti-corrosive coatings in treatment plants and pipelines. The Pradhan Mantri Awas Yojana-Urban (PMAY-Urban) has successfully delivered houses by 2024, directly benefiting decorative coating volumes. Meanwhile, industrial coatings are in demand due to the regular maintenance needs of national highways.

Shortening Decorative Re-paint Cycle among Urban Homeowners

Disposable-income gains and digital color-visualization tools are reducing the average repaint interval by 2031[1]Press Information Bureau, “Infrastructure Expansion in India Witnesses Significant Growth in Recent Years: Economic Survey 2023-24,” Ministry of Finance, pib.gov.in . Premium low-odor emulsions allow same-day reoccupation, supporting higher-value product mixes. National manufacturers are using contractor-training programs to position water-borne offerings as cost-effective over a full repaint cycle, countering price-only pitches from local players.

Post-COVID Recovery in Automotive and Industrial Production

In 2023-24, vehicle production surged, with electric vehicle sales witnessing significant growth[2]Society of Indian Automobile Manufacturers, “Vehicle Production Statistics FY 2024,” siam.in . This uptick in vehicle output bolstered the demand for electrocoats, primer-surfacers, and top-coat lines, especially those tailored for lightweighting and low-bake specifications. Additionally, as Indian Railways rolled out new pairs of Vande Bharat trains, the need for fire-retardant and anti-graffiti finishes drove an increase in industrial coatings volumes.

Emergence of Organised Waterproofing After-market

Stricter BIS specifications for cementitious and polymer-based systems and sustained monsoon damage awareness have moved waterproofing from a discretionary add-on to a core purchase in both new-build and repair workflows. Multi-year performance warranties from organized suppliers are winning share from unorganized trades, especially in coastal and high-rainfall regions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-Linked Raw-Material Price Volatility | -1.2% | National; acute in regions dependent on imported TiO2 and petrochemical derivatives | Short term (≤ 2 years) |

| Stricter BIS/CPCB VOC and Lead Regulations | -0.6% | National; compliance costs highest for MSMI segment | Medium term (2-4 years) |

| Margin Compression from Intensifying Price-Based Competition | -0.9% | National; most severe in metros and tier-I cities with high new-entrant presence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Crude-Linked Raw-Material Price Volatility

In 2024-2025, titanium dioxide (TiO2), a key component constituting a significant portion of paint formulation costs, saw its prices fluctuate. These swings were largely influenced by global supply disruptions and fluctuations in crude oil prices, which in turn impact petrochemical-derived binders and solvents. Inflation in raw materials led to margin compression, with gross margins declining as companies absorbed rising input costs to maintain their volume share. Industry margins also contracted due to heightened competitive intensity, which hampers the industry's ability to fully pass on cost increases. Additionally, volatility in zinc and aluminum prices impacts color-coated steel coatings, commonly used in roofing and cladding. Compounding the challenge, import competition prices these products lower than domestic offerings, further squeezing margins for local manufacturers. The sector grapples with the challenge of passing on raw material inflation. Intense price competition, especially from new entrants like Birla Opus and JSW Paints, has led companies to optimize formulations, trim packaging costs, and ramp up automation efforts to maintain their operating leverage.

Stricter BIS/CPCB VOC and Lead Regulations

Facilities must now achieve at least 95% efficiency in the destruction and removal of VOCs. Additionally, decorative formulations are required to maintain lead levels below 90 ppm. Smaller producers feel the pinch of compliance capital expenditures, leading to an accelerated wave of consolidation in the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Coatings Anchor the Shift from Solvents

Water-borne products held 45.41% of India's paints and coatings market share in 2025 and are projected to grow at a 9.72% CAGR through 2031. Regulatory pressure, coupled with improved film-property parity versus solvent systems, underpins adoption in both decorative and general industrial applications. Water-based UV-curable urethane-acrylate systems are gaining a foothold in wood finishes, while powder coatings continue to build in appliance and automotive exterior trims. Solvent solutions still dominate marine and heavy-duty segments that require rapid curing and extreme chemical resistance, but investments in catalytic-oxidation units raise operating costs, nudging OEMs toward hybrid or high-solid alternatives.

Second-generation water-borne emulsions use core-shell and redispersible-powder technologies to overcome scrub-resistance and humidity-cure limitations, enabling faster re-coat windows in tropical climates across the Paint Industry in India. Powder coatings are enjoying growth in the northern manufacturing corridor, supported by appliance cluster expansion around Delhi-NCR. High-solid alkyd and radiation-curable inks fill specialty gaps in metal packaging and flexible-film lamination, diversifying technology portfolios.

By Resin Type: Acrylic Chemistry Commands over One-Third of Revenue

Acrylic resins accounted for 36.48% of India's paints and coatings market share in 2025 and are on track for a 9.56% CAGR to 2031. Advanced water-borne acrylics deliver exterior durability, while bio-sourced acrylic copolymers derived from soybean oil reduce crude exposure and align with extended producer-responsibility targets for carbon reduction. Alkyds retain relevance in economy interior emulsions but cede ground as distributors add low-VOC acrylic lines in semi-urban outlets. Polyurethane resins grow fastest in wood finishing and automotive clear coats, where gloss retention and chemical resistance command premium price points. Epoxies dominate protective and marine sectors, benefiting from offshore oil-and-gas investments and coastal infrastructure maintenance. Polyester resins power appliance powder-coat lines, while vinyl and silicone chemistries satisfy fire-retardant and high-temperature niches in rail stock and process equipment.

By End-User Industry: Architectural Paints Remain the Revenue Backbone

Architectural applications represented 77.12% of India's paint and coatings market size in 2025 and are forecast to expand at a 9.51% CAGR to 2031. Urban housing initiatives, combined with deeper rural penetration where organized penetration is below 10%, continue to lift decorative volumes. Product bundling—primers, putty, texture finishes, and waterproofing—helps suppliers offset margin pressure through higher average selling prices. Automotive coatings gain from rising vehicle production and electrification, with electro-coat and heat-dissipation finishes enjoying early specification wins in battery enclosures. Highway expansions and the expanding footprints of logistics parks bolster both the protective and general industrial segments. Meanwhile, packaging coatings are capitalizing on growth in the domestic packaging sector, a trend that's closely tied to the surge in e-commerce.

Geography Analysis

India's paints and coatings market sees nearly a quarter of its revenue coming from Tier-I and metropolitan regions, which, despite solid annual volume gains, are witnessing a compression in repaint cycles. Major OEM plants and industrial users, particularly in the western and northern clusters of Maharashtra, Gujarat, and Delhi-NCR, drive the demand for automotive, powder, and protective formulations. Meanwhile, southern states, with Tamil Nadu at the forefront, are leading the charge in water-borne technologies, thanks to earlier regulatory enforcement and a more sophisticated contractor base.

Tier-II to Tier-IV towns emerge as the fastest-growing regions, accounting for a significant share of the incremental decorative volumes. A denser dealer network, bolstered by tinting-machine subsidies from leading manufacturers, not only shortens delivery lead times but also nudges rural consumers away from unbranded lime-wash solutions towards recognized emulsion systems. Furthermore, infrastructure initiatives like the Bharatmala and Smart Cities programs are paving the way for robust industrial-coating opportunities, especially in central and eastern corridors near new logistics parks and multimodal terminals.

Historically, the northeast and coastal belts faced challenges due to high humidity and cyclone damage, but they are now emerging as hotspots for waterproofing and high-performance exterior coatings. Government incentives for road and rail projects in border areas are broadening the scope for protective coatings, and with port modernization along the eastern seaboard, there's a surge in demand for marine maintenance.

Competitive Landscape

The Indian paints and coatings market is highly consolidated in nature. Capacity build-outs and automated lines lower fixed costs per liter, enabling entrants to price below incumbents without sacrificing gross margin. Established players respond by increasing dealer credit, adding premium textures, and promoting emotion-led campaigns that shift the purchase trigger away from price alone. Industrial coatings specialists exploit service depth and OEM relationships to insulate earnings from retail price wars. Investments in artificial-intelligence demand forecasting and digital plant controls improve batch consistency and cut material waste, freeing cash for research and development on low-VOC chemistries. Backward integration into titanium dioxide contracts and bio-based resin development hedges feedstock volatility, while joint ventures with local resin producers secure raw-material availability. Rural and semi-urban white spaces host the next wave of consolidation in the Paint Industry in India as smaller regional firms struggle with compliance, capex, and dealer incentive costs. Organized suppliers that combine tinting-machine deployment with contractor-training academies are positioned to capture a disproportionate share once the current rebate cycle normalizes around FY 2028.

India Paints and Coatings Industry Leaders

Asian Paints

Berger Paints India Limited

Kansai Paint Co., Ltd. (Kansai Nerolac Paints Limited)

JSW

Birla Opus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Akzo Nobel India announced acquisition by JSW Paints, with the latter merging into the listed entity through a mix of equity and debt financing supported by Deutsche Bank and MUFG.

- August 2024: Berger Paints committed INR 2,000 crore (~USD 228.84 million) for two greenfield factories in Bengal and Odisha, expected to lift total output capacity by as much as 30% once Khurdha goes on-stream in 2027.

India Paints and Coatings Market Report Scope

Paints and coatings are utilized in the architectural, automotive, wood, industrial, transportation, and packaging industries. They are intended for several applications, such as corrosion resistance, damage prevention, decorative reasons, and others.

The Paint Industry in India is segmented by technology, resin type, and end-user industry. On the basis of technology, the market is segmented into water-borne, solvent-borne, powder coatings, and other technologies. On the basis of resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. In the end-user industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging. For each segment, the market sizing and forecasts were made on the basis of value (USD).

By Technology

| Water-Borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies |

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Others |

By End-user Industry

| Architectural |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

| By Technology | Water-Borne |

| Solvent-borne | |

| Powder Coatings | |

| Other Technologies | |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Others | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

What is the current value of the Paint Industry in India?

The market is valued at USD 12.51 billion in 2026 and is projected to reach USD 19.50 billion by 2031, registering a 9.28% CAGR.

How fast will water-borne coatings grow in India through 2031?

Water-borne formulations are expected to register a 9.72% CAGR, outpacing solvent-borne alternatives.

Which resin type leads demand in India?

Acrylic systems command more than one-third of total revenue and are expanding as bio-based variants enter portfolios.

How does infrastructure spending influence demand in the Paint Industry in India?

National highway, metro-rail, and housing programs collectively raise protective and decorative paint volumes by supporting continuous new-build and maintenance work.

Why are margins under pressure despite rising volumes in the Paint Industry in India?

New entrants use price discounts and higher dealer incentives to gain share, forcing incumbents to absorb part of raw-material inflation and intensify marketing outlays.

Page last updated on: