Liquefied Petroleum Gas (LPG) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

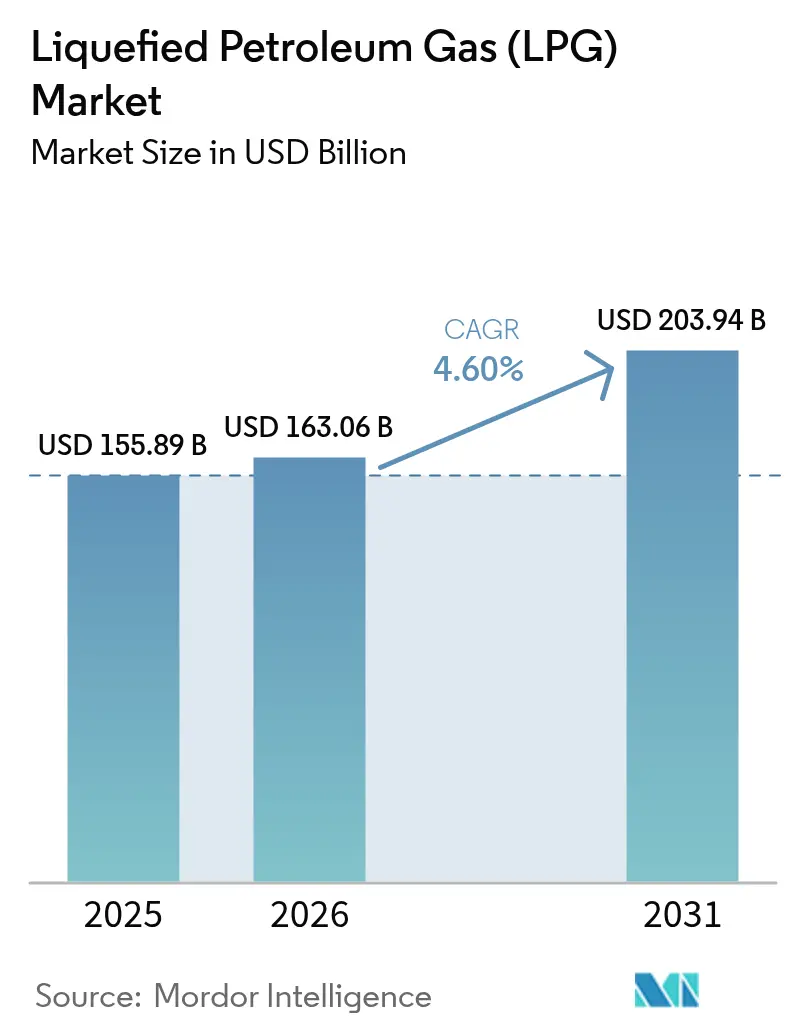

| Market Size (2026) | USD 163.06 Billion |

| Market Size (2031) | USD 203.94 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

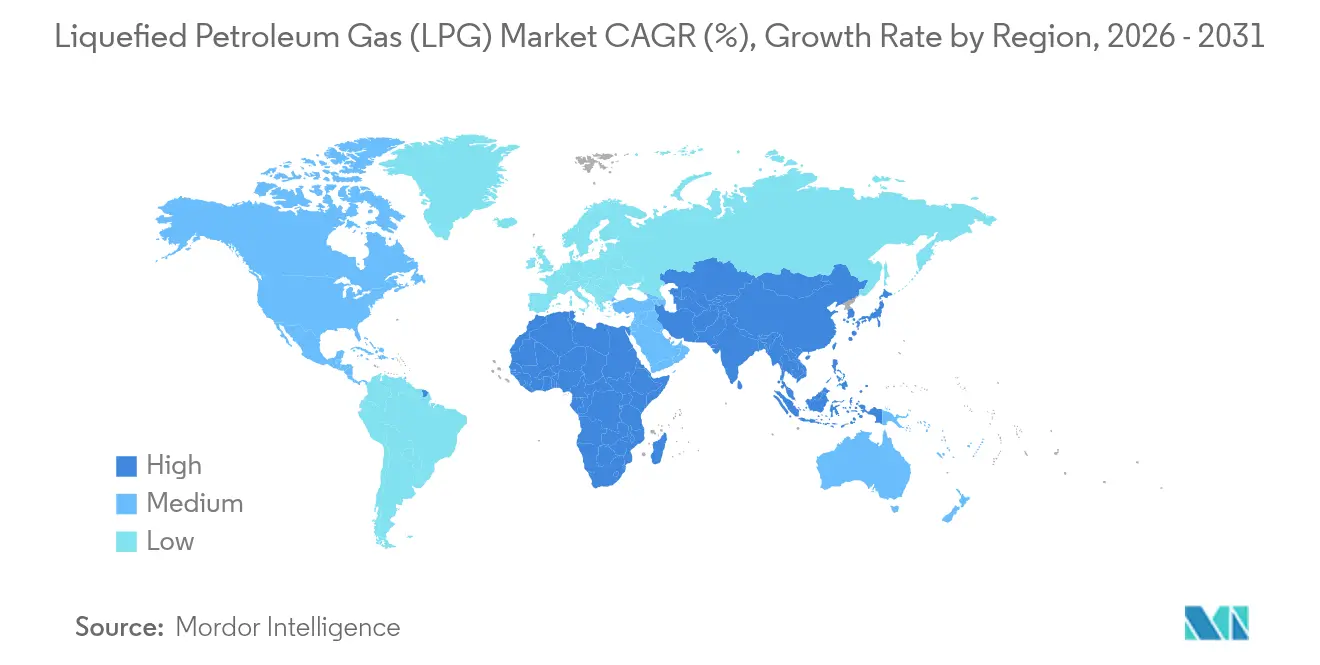

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

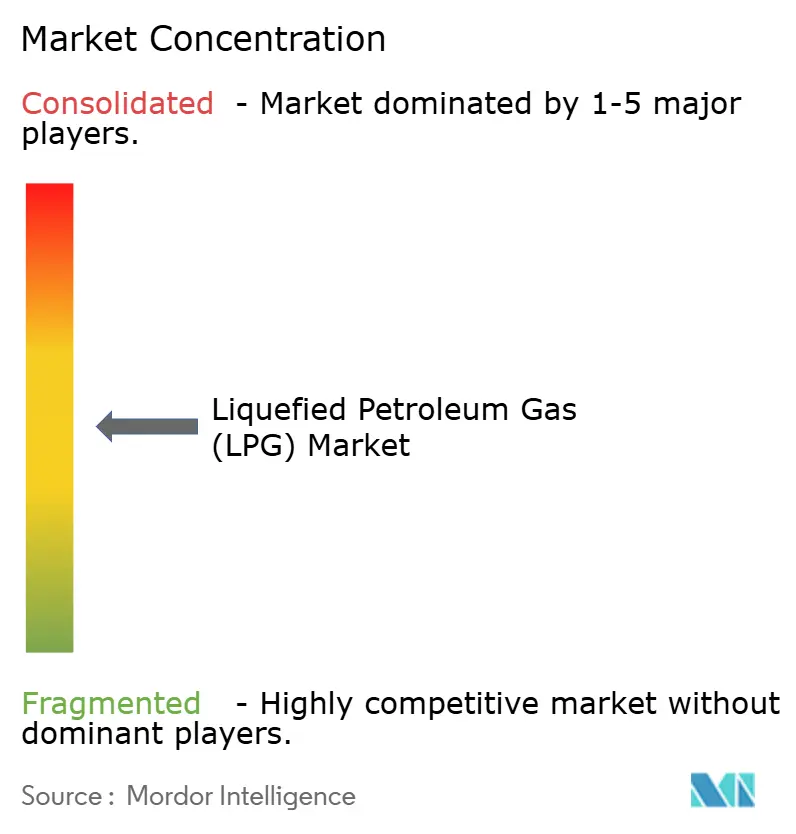

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquefied Petroleum Gas (LPG) Market Analysis by Mordor Intelligence

The Liquefied Petroleum Gas Market size was valued at USD 155.89 billion in 2025 and estimated to grow from USD 163.06 billion in 2026 to reach USD 203.94 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

Demand resilience is anchored by Asian petrochemical feedstock growth, large-scale rural cooking programs in India and Indonesia, and continuing substitution of high-sulfur fuels after IMO-2020 upgrades. Supply diversity widens as Qatar and the UAE lift output while North American producers maximize shale-derived volumes, yet export bottlenecks keep price swings frequent. Bio-LPG gains momentum under EU decarbonization rules, and pipeline investments in India, the United States, and West Africa seek to trim logistics costs and safety risks. Market participants, therefore, juggle a balanced opportunity set: stable household consumption, expanding petrochemical pull, and regulatory shifts that reward lower-carbon molecules.

Key Report Takeaways

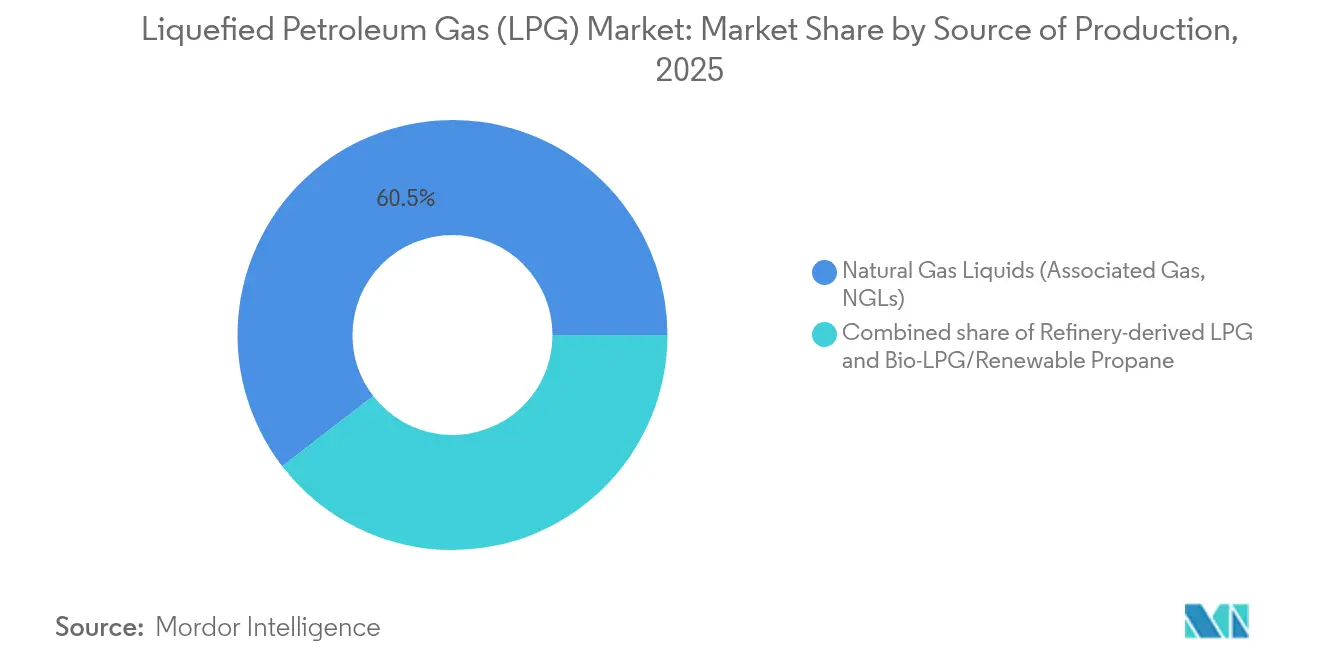

- By source, natural gas liquids commanded 60.45% of the liquefied petroleum gas market share in 2025; bio-LPG is projected to register the fastest 14.58% CAGR through 2031.

- By distribution, cylinder gas retained 57.35% of the lpg market size in 2025, whereas pipeline and virtual pipeline channels are forecast to accelerate at an 8.32% CAGR to 2031.

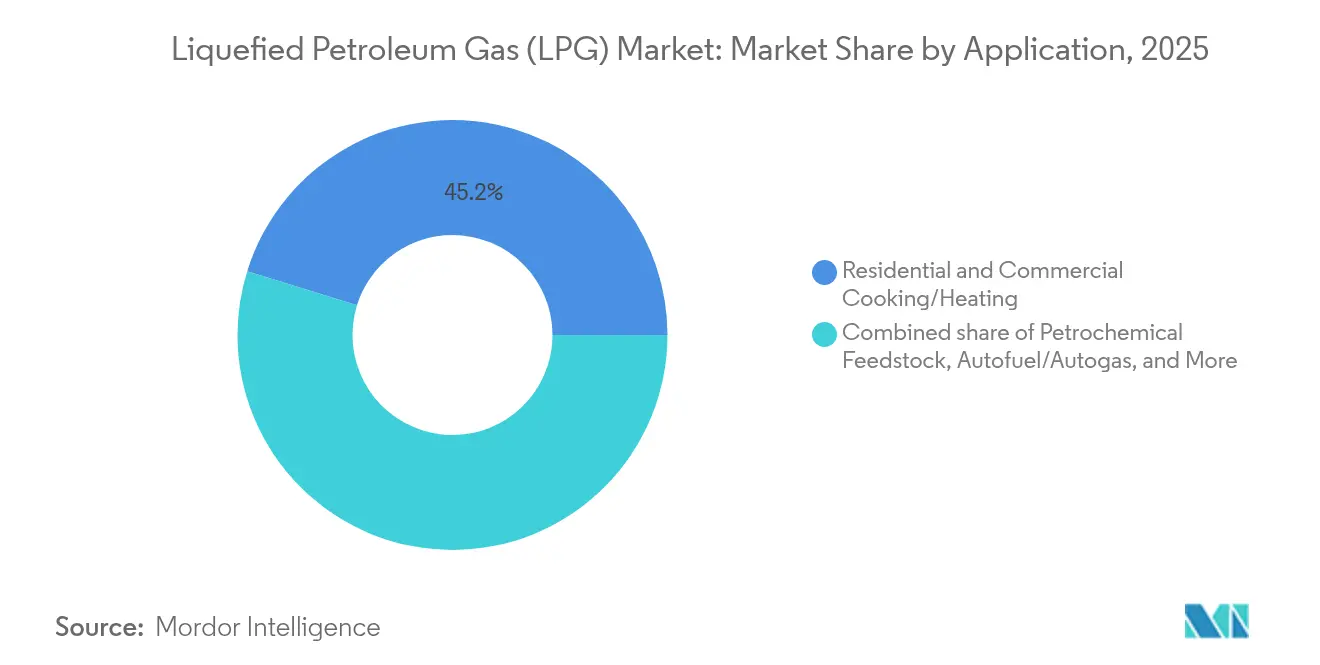

- By application, residential and commercial cooking held 45.20% of the liquefied petroleum gas market share in 2025; petrochemical feedstock is the fastest-growing use, advancing at a 7.72% CAGR during 2026-2031.

- By geography, Asia-Pacific led with a 43.60% revenue share in 2025 and is expected to post a 5.38% CAGR, supported by China’s 22.6 million-tonne PDH capacity and India’s rural access roll-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquefied Petroleum Gas (LPG) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward LPG-ready hybrid cook-stove programmes (India, Indonesia) | 0.80% | Asia-Pacific core, spill-over to Africa | Medium term (2-4 years) |

| Petrochemical feedstock demand boom in emerging Asia | 1.20% | Asia-Pacific, selective Middle East integration | Long term (≥ 4 years) |

| Accelerating refinery upgrades for IMO-2020 compliant fuels | 0.60% | Global, concentrated in Gulf Coast and Asia refineries | Short term (≤ 2 years) |

| Rural household electrification lag sustaining cylinder demand (Africa) | 0.40% | Sub-Saharan Africa, selective LATAM regions | Long term (≥ 4 years) |

| Subsidy reforms boosting commercial sector uptake (Middle East) | 0.70% | GCC countries, selective North African markets | Medium term (2-4 years) |

| Renewable-propane scale-up in North America & EU decarbonization agendas | 0.50% | North America & EU, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LPG-ready cook-stove programmes expand clean fuel access

Indonesia’s conversion of 50 million households from kerosene to LPG demonstrates rapid scalability and has become a reference model for other developing nations.[1]Source: Indonesian National Institute of Health, “Kerosene-to-LPG Conversion Success,” ncbi.nlm.nih.gov India’s Pradhan Mantri Ujjwala Yojana added 7.5 million new cylinder connections in 2024, driving a 24% import surge despite ongoing subsidy rationalization. West African governments now partner with the World Bank’s Global LPG Partnership to replicate these roll-outs, aiming to lift Cameroon’s penetration from 12% to 58% by 2030.[2]World Bank, “Global LPG Partnership Targets,” worldbank.org Persistent rural electrification gaps leave LPG competitively positioned versus electric cooking, particularly where grid reliability remains low. Therefore, continued subsidy targeting and last-mile distribution innovation are central to sustaining household uptake.

Petrochemical feedstock demand boom reshapes Asian trade flows

China’s propane dehydrogenation capacity climbed to 22.6 million t/y in 2024 and underpins steady seaborne imports despite cyclical economic slowdowns. India followed by committing USD 8 billion to a 1.5 million t/y ethane cracker at Vadinar that secures domestic feedstock and curbs foreign dependency. US ethane exports to China are projected to rise another 9-34% in 2025 as lower tariffs improve arbitrage economics. Tightening propylene balances have driven US polymer-grade prices beyond USD 0.40 per pound after LyondellBasell shuttered refinery units. In aggregate, more than USD 16 billion of Asian pipeline and storage infrastructure is set to anchor long-run lpg market growth by absorbing regional demand volatility.

Refinery upgrades for IMO-2020 multiply LPG supply points

Chevron’s Pasadena revamp lifted throughput capacity for lighter crudes to 125,000 b/d, improving LPG yield flexibility. Phillips 66 is weighing a USD 99 million expansion at Lake Charles, while Oman’s Duqm refinery has run 10% above nameplate since its debut, exemplifying an agile response to new marine sulfur caps. Global additions of 2.6-4.9 million b/d by 2028 are centered in China and India, with many units configured to maximize naphtha and LPG streams for petrochemical integration.[3]EIA, “Refinery Capacity Outlook,” eia.gov India’s refiners have already diverted barrels toward higher-margin polypropylene, trimming domestic LPG output 4.5% in Q2 2024. Africa’s growing refinery slate, led by Nigeria’s Dangote complex, will temper import reliance and broaden regional supply diversity.

Renewable propane scale-up introduces low-carbon competition

United Kingdom suppliers pledged GBP 600 million to achieve a fully renewable LPG pool by 2040, positioning bio-LPG as a mainstream decarbonization lever. US output crossed 4.5 million gallons in 2024 and could reach 100 million by 2030 under supportive state-level credits. OMV Petrom has allocated EUR 750 million to its Petrobrazi sustainable-fuels unit that will co-produce 250,000 t/y of bio-LPG once online in 2028. Carbon intensity studies indicate renewable propane delivers a four-fold reduction versus fossil propane, but US adoption remains modest where conventional supply keeps premiums tight. Europe’s carbon pricing and limited indigenous LPG offer more attractive economics, accelerating early commercial offtake agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility linked to US shale export arbitrage | -0.90% | Global, acute impact on Asia-Pacific imports | Short term (≤ 2 years) |

| Accelerating induction cooking penetration in urban China & EU | -1.10% | Urban China, EU metropolitan areas, Indonesia pilot programs | Medium term (2-4 years) |

| Stricter methane-intensity rules favoring piped natural gas over LPG | -0.60% | EU regulatory zone, potential US adoption | Medium term (2-4 years) |

| Cylinder logistics safety incidents undermining public perception (LATAM) | -0.30% | Latin America, selective emerging market spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price volatility driven by US export constraints

Gulf Coast terminal utilization hovered near 100% in 2024, sending Mont Belvieu cargo premiums to 32.5 c/gal before retreating when surplus propane hit storage. Enterprise’s 300,000 b/d Houston expansion will not materialize until late 2026, while the 400,000 b/d ONEOK-MPLX Texas City project arrives only in 2028, leaving an interim capacity crunch. With the United States exporting 70% of its 2.13 million b/d propane output, any arbitrage closure triggers rapid inventory builds and price instability. China’s position as the largest buyer magnifies geopolitical risk: a renewed tariff dispute could force Asian importers toward higher-priced Middle Eastern cargos. Volatility encourages heavier use of paper hedging, evidenced by a 43% surge in ethane and propane derivative trading volumes during 2024.

Induction cooking erodes urban LPG demand pockets

Indonesia’s government targets a 31% reduction in LPG use by 2050 by distributing induction stoves to 58 million households, potentially saving USD 4.9 billion in annual subsidies. Ecuador’s program to replace 4.3 million LPG stoves is projected to yield USD 1.162 billion in yearly savings once the hydro build-out lifts the electricity share to 83.6%. EU appliance efficiency standards and consumer incentives have accelerated induction uptake, particularly in dense apartment markets with convenient electric upgrades. IRENA reports electric cooking penetration among member states at only 8.9%, implying vast switch-over potential as grids strengthen. The combined effect diverts growth toward rural and commercial niches, obliging LPG suppliers to diversify beyond traditional residential cylinders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Production: Natural‐gas liquids dominance and rising bio-LPG adoption

Natural-gas liquids secured a 60.45% share of the liquefied petroleum gas market in 2025, buoyed by North American shale and Middle Eastern associated-gas projects that keep marginal costs low. Qatar’s North Field build-out will elevate national LPG output from 10.7 million t in 2024 to 17.6 million t by 2030, while three ADNOC Gas programs add 2.5 million t over the same horizon, strengthening regional supply security. Refinery-derived LPG has come under pressure as Indian and Chinese refiners pivot toward petrochemicals, trimming run rates for fuels blending streams. Although still modest, the lpg market size for bio-LPG is anticipated to expand at a 14.58% CAGR when measured from its 2025 baseline as EU mandates and state incentives unlock new production capacity. The segment benefits from drop-in compatibility and up to 90% lifecycle emissions cuts, enabling suppliers to layer premium pricing on corporate net-zero procurement contracts. Nonetheless, feedstock availability and competition with renewable diesel limit near-term scaling, particularly in North America, where conventional LPG oversupply narrows green premiums.

Adoption pathways differ across regions. Europe leans on used cooking oil and waste-based HVO routes, while the United States favors HEFA processes piggybacking on existing renewable diesel plants. Asia’s bio-LPG roll-out remains nascent but could accelerate as Japan and South Korea unveil aviation decarbonization strategies that integrate co-product streams. The lpg market share tilts toward renewable molecules, therefore deepens over the outlook, though absolute volumes remain led by fossil NGLs until at least 2030. This dual-track supply system encourages incumbents to hedge by investing in shale-linked expansions and emerging biorefineries.

By Distribution Channel: Cylinder resilience meets pipeline modernization

Cylinder deliveries accounted for 57.35% of the liquefied petroleum gas market in 2025, reflecting deep penetration into rural households across Asia and Africa. India’s 7.5 million new household beneficiaries illustrate the ongoing strength of cylinder demand even as composite designs improve safety after Worthington’s USD 98 million Hexagon Ragasco deal. Virtual pipeline services, using ISO tanks and trucked cryogenic trailers, offer flexible reach into remote mines and island communities where traditional steel pipe is uneconomic. As government safety mandates tighten, smart valves and IoT telemetry see wider deployment, reducing pilferage and accident risk.

The pipeline and virtual pipeline segment is forecast to post an 8.32% CAGR between 2026-2031. India inaugurated a USD 1.3 billion, 2,800 km line that will cover 25% of national demand by moving 8.3 million t per year while cutting truck miles and highway casualties. In North America, Enterprise and ONEOK investments add 700,000 b/d of export-linked pipeline capacity by 2028, positioning the region to capture higher volumes once berth slots clear. Latin American importers likewise consider small-bore pipelines coupled with coastal break-bulk storage to mitigate supply interruptions from cylinder mishaps. Collectively, the lpg market size allocated to pipeline channels widens as economies pursue cost and safety efficiencies.

By Application: Cooking solidity versus petrochemical surge

Residential and commercial cooking retained 45.20% of the liquefied petroleum gas market size in 2025, underpinned by persistent rural electrification deficits and ongoing subsidy structures. In India, cylinder usage still reaches more than 90% of households, and authorities intend to drive industrial uptake to 20% of total consumption by 2030, partly offsetting urban cooking erosion. Indonesia’s induction-switch program highlights the future risk to urban LPG volumes, but concurrent industrialization in ASEAN keeps commercial burner demand firm. Agriculture, food processing, and small manufacturing prize LPG’s clean flame and easy on-off control, ensuring a diversified application base despite headline stove conversions.

Petrochemical feedstock constitutes the fastest-growing end use at a 7.72% CAGR. China’s PDH build-out plus India’s ethane cracker projects pull incremental propane and butane cargoes into Asia, underpinning regional procurement even when macro demand softens. Global PDH capacity advanced at an 18% annual clip from 2021-2024, lifting propylene derived from LPG to 16% of the worldwide supply. The liquefied petroleum gas market share linked to PDH and steam-cracker streams thus rises steadily, with US exporters capturing arbitrage and Middle Eastern producers capitalizing on surplus associated gas. Autogas remains a niche but steady segment in commercial vehicle fleets across Turkey, Mexico, and Eastern Europe, where infrastructure is entrenched and battery-electric alternatives remain costly.

Geography Analysis

Asia-Pacific held 43.60% of the global LPG market revenue in 2025 and is expected to maintain a 5.38% CAGR to 2031 as petrochemical demand offsets urban induction conversions. China’s 22.6 million-t PDH capacity ensures sustained seaborne propane pull, even with domestic economic moderation. India’s 24% import surge in 2024 will taper as subsidies tighten, yet cooking gas remains critical for rural inclusion programs. Indonesia’s roadmap to cut LPG usage 31% by 2050 introduces headwinds, though Southeast Asian industrial and tourism expansions cushion overall volumes. Japan and South Korea keep steady industrial baseloads, whereas Vietnam and the Philippines are emerging bright spots thanks to population growth and robust construction sectors.

North America leverages a 2.13 million b/d propane production platform, exporting more than 70% of output despite dock congestion. Canada’s Keyera acquisition of Plains NGL assets for USD 5.15 billion integrates storage and fractionation, enhancing supply redundancy into Pacific basins. Mexico continues to benefit from cross-border pipeline connections that backstop domestic shortfalls, while specialty distributors expand virtual pipelines into underserved central plateau cities.

Europe grapples with post-Russian supply diversification: Poland’s dependence has pushed traders toward US and Middle Eastern cargos at premium freight rates. The United Kingdom’s GBP 600 million renewable propane drive signals strategic hedging, and OMV Petrom’s Petrobrazi investment cements Southeast Europe’s first major SAF-bio-LPG hub. Middle Eastern producers, chiefly Qatar and the UAE, add 9.4 million t of new capacity by 2030, enabling competitive offers into Asia and eroding US share in that corridor. Sub-Saharan Africa remains under-supplied; South Africa’s R1 billion Richards Bay storage came online to stabilize regional availability. Latin America’s LPG market growth is curtailed by cylinder safety incidents, but Colombia and Peru eye pipeline modernization to enhance reliability and lower end-user costs.

Mordor Intelligence provides coverage of the liquefied petroleum gas (lpg) market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The lpg industry is consolidating around integrated majors and infrastructure specialists. Abundant US shale liquids underpin low-cost feedstock, allowing exporters such as Enterprise Products and Phillips 66 to capture margin from export arbitrage. The USD 5.15 billion Keyera–Plains transaction broadens Canadian scale, while Phillips 66’s EPIC NGL purchase and Honeywell’s USD 1.81 billion Air Products LNG technology deal illustrate an intensified focus on high-barrier infrastructure and patented process know-how. Middle Eastern incumbents leverage sovereign backing to fund mega trains that can undercut spot prices into Asia. In Europe, independent distributors differentiate by early adoption of bio-LPG; niche players collaborate with refiners and waste managers to secure sustainable feedstock streams.

Technology innovation centers on digital telemetry for cylinders, AI-driven routing for bulk trucks, and methane-leak detection across gathering systems. ESG compliance is now integral to securing finance, nudging operators toward flaring minimization and renewable transition strategies. Regulations like forthcoming EU methane-intensity benchmarks incentivize upstream efficiency and may redirect trade toward lower-emission suppliers. Competitive whitespace remains in Africa and frontier Asian islands where virtual pipelines and micro-bulk systems can leapfrog traditional networks.

Liquefied Petroleum Gas (LPG) Industry Leaders

Shell plc

Exxon Mobil Corporation

TotalEnergies SE

BP plc

Saudi Aramco

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Keyera agreed to acquire Plains’ Canadian NGL business for USD 5.15 billion, expanding fractionation and export capacity.

- March 2025: India commissioned a USD 1.3 billion, 2,800 km LPG pipeline moving 8.3 million t/y, covering one-quarter of domestic demand.

- February 2025: OMV Petrom broke ground on a EUR 750 million Petrobrazi sustainable-fuels unit producing bio-LPG, SAF, and renewable diesel.

- November 2024: OQ Base Industries announced a potential USD 500 million IPO for its methanol-LPG unit.

Global Liquefied Petroleum Gas (LPG) Market Report Scope

Liquefied petroleum gas is a combustible mixture of hydrocarbon gases, including propane, propylene, butylene, isobutane, and n-butane. LPG is a fuel gas that is used in heating appliances, cooking equipment, and automobiles. It is called liquefied gas because it is easily transformed into a liquid.

The liquefied petroleum gas market is segmented by the source of production, application, and geography. By source of production, the market is segmented into crude oil and natural gas liquids. By applications, the market is segmented into residential, commercial & industrial, auto fuels, and others. The report also covers the market size and forecasts for the liquified petroleum gas market across major regions (North America, South America, Europe, Asia-Pacific, and Middle-East and Africa). For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| Refinery-derived LPG |

| Natural Gas Liquids (Associated Gas, NGLs) |

| Bio-LPG/Renewable Propane |

| Cylinder (Packaged) Gas |

| Bulk and Retail Bulk Supply |

| Pipeline and Virtual Pipeline |

| Residential and Commercial Cooking/Heating |

| Industrial and Commercial Processing |

| Autofuel/Autogas |

| Petrochemical Feedstock |

| Agriculture and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Source of Production | Refinery-derived LPG | |

| Natural Gas Liquids (Associated Gas, NGLs) | ||

| Bio-LPG/Renewable Propane | ||

| By Distribution Channel | Cylinder (Packaged) Gas | |

| Bulk and Retail Bulk Supply | ||

| Pipeline and Virtual Pipeline | ||

| By Application | Residential and Commercial Cooking/Heating | |

| Industrial and Commercial Processing | ||

| Autofuel/Autogas | ||

| Petrochemical Feedstock | ||

| Agriculture and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the LPG market?

The liquefied petroleum gas market size reached USD 163.06 billion in 2026 and is projected to hit USD 203.94 billion by 2031.

Which region leads the LPG market?

Asia-Pacific leads with a 43.60% share, supported by China’s petrochemical growth and India’s rural cooking initiatives.

What segment is growing fastest within the liquefied petroleum gas market?

Bio-LPG, within the source-of-production category, is forecast to expand at a 14.58% CAGR between 2026 and 2031.

How are export bottlenecks impacting LPG prices?

Near-saturated US Gulf Coast terminals have driven spot premiums as high as 32.5 c/gal, with relief expected only after major expansions go live in 2026-2028.

How does induction cooking affect future LPG demand?

Urban induction programs in China, the EU, and Indonesia threaten residential cylinder demand, shifting growth focus to rural, industrial, and petrochemical uses.

Why is renewable propane gaining traction?

Bio-LPG delivers up to 90% lower lifecycle emissions and aligns with EU and North American decarbonization mandates, creating a premium niche within the broader market.

Page last updated on: