Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 57.31 Billion |

| Market Size (2031) | USD 78.06 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

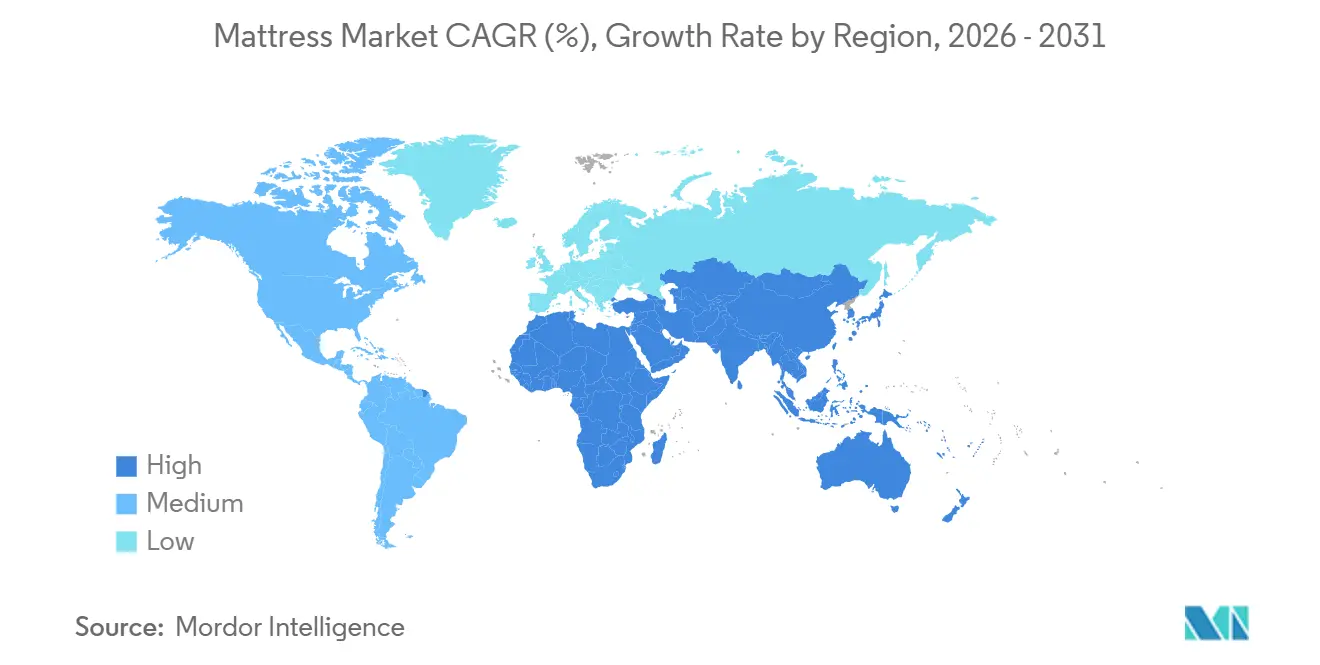

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

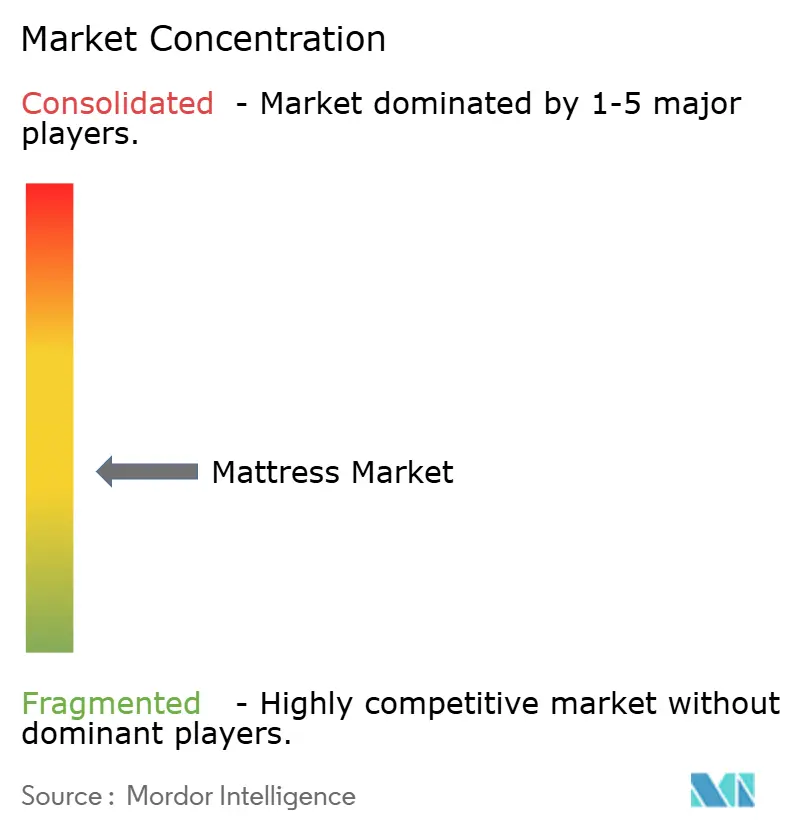

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mattress Market Analysis by Mordor Intelligence

The Mattress Market size is projected to be USD 53.95 billion in 2025, USD 57.31 billion in 2026, and reach USD 78.06 billion by 2031, growing at a CAGR of 6.38% from 2026 to 2031.

Regional variations and evolving consumer preferences are driving market growth. Asia-Pacific is emerging as the fastest-growing region, with an annual growth rate of 8.54%, fueled by the expansion of organized retail in Indian tier-2 cities and increasing product experimentation in Chinese secondary urban centers. In North America, the market maintains a large revenue base, although unit shipments are slowing as consumers extend mattress replacement cycles and redirect discretionary spending toward experiences such as travel and events. In Europe, market growth is increasingly shaped by sustainability initiatives, with the upcoming Ecodesign for Sustainable Products Regulation (expected by 2027) emphasizing digital product passports, traceability, and recycling readiness. This regulatory environment benefits larger manufacturers while challenging smaller players with higher compliance costs. Overall, the mattress market is expanding due to rising urbanization, increased consumer willingness to invest in comfort and premium sleep solutions, and growing retail penetration. Companies that leverage vertical integration, premium positioning, and sustainable product offerings are capturing a disproportionate share of earnings growth, even as raw material costs and regulatory requirements influence market dynamics.

Key Report Takeaways

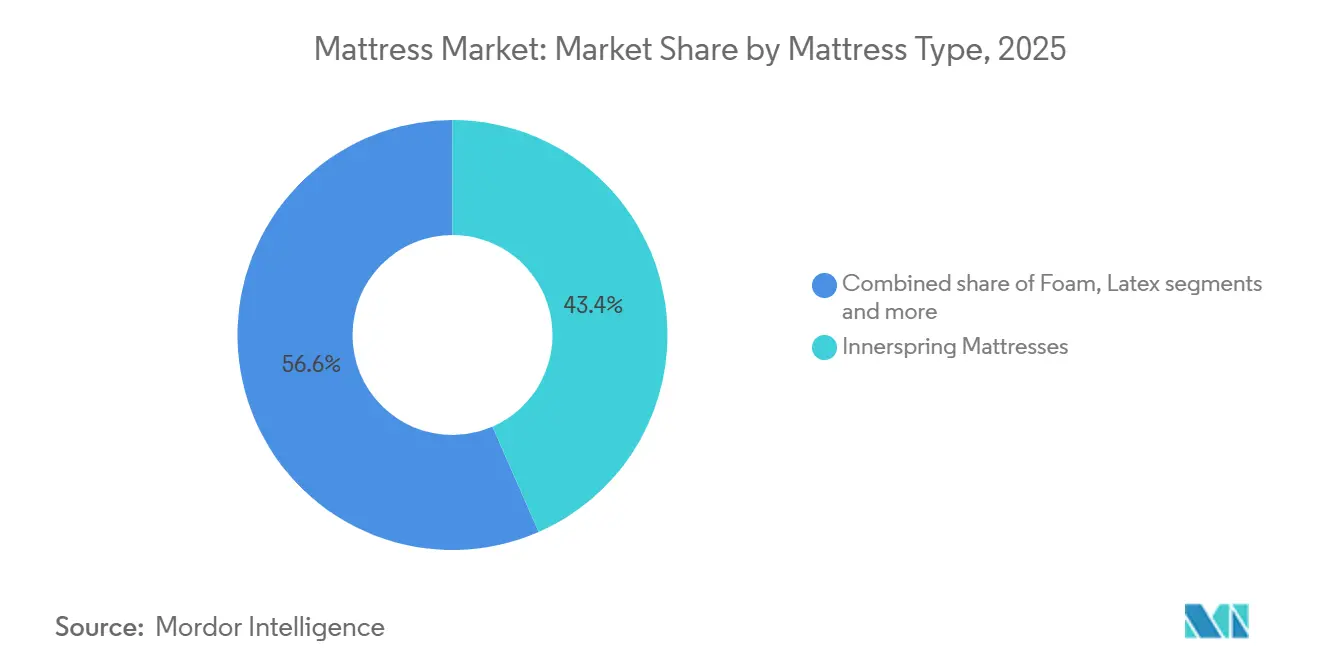

- By mattress type, innerspring led with 43.44% of the mattress market size in 2025, while latex is projected to expand at a 9.87% CAGR through 2031.

- By size, queen-size held 48.35% of the mattress market share in 2025, while king-size is forecast to advance at an 8.64% CAGR through 2031.

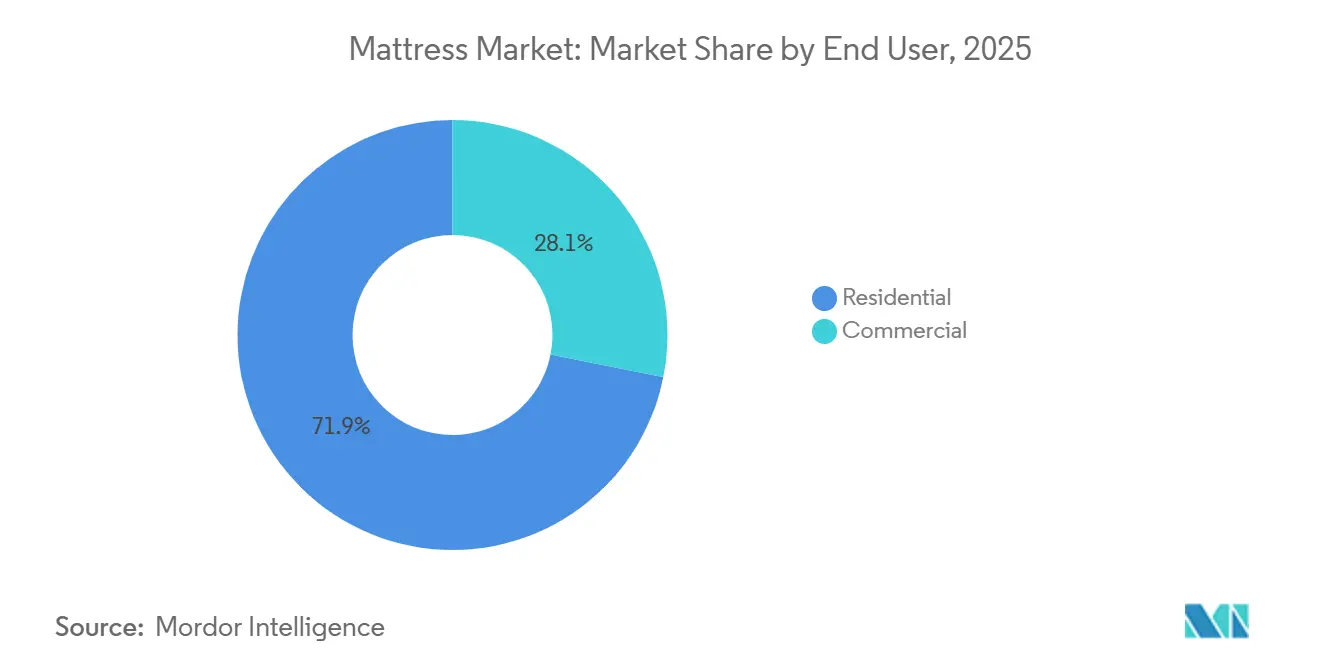

- By end user, residential accounted for 71.87% of the mattress market share in 2025, and is projected to grow at a 7.87% CAGR through 2031.

- By distribution channel, B2C captured 64.84% of the mattress market share in 2025, and within B2C, online is set to grow at an 8.28% CAGR through 2031.

- By geography, North America held 36.39% of the mattress market share in 2025, while Asia-Pacific is the fastest-growing region at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened sleep-health consciousness & premium spend shift | +1.8% | North America and Europe strongest | Medium term (2-4 years) |

| Direct-to-consumer e-commerce boom | +1.5% | Global, led by North America, expanding fast in Asia-Pacific | Short term (≤2 years) |

| Global hospitality & real-estate buildout | +1.2% | Asia-Pacific core, spill-over to Middle East and Latin America | Long term (≥4 years) |

| Breakthrough cooling & adaptive material technology | +1.0% | North America and EU lead; Asia-Pacific manufacturing hub | Medium term (2-4 years) |

| Regulatory push for circular, organic input adoption | +0.8% | EU leadership, North America following, Asia-Pacific emerging | Long term (≥4 years) |

| AI & IoT-powered smart mattress adoption | +1.1% | Global; early uptake in North America and Asia-Pacific tech hubs | Short-medium term (≤3 years) |

| Source: Mordor Intelligence | |||

Heightened sleep-health consciousness & premium spend shift

The State of Sleep Health in America report indicates that many United States adults struggle to get adequate restorative sleep, with 1 in 3 not meeting recommended levels, while over half (55%) consider good sleep a major priority[1]SleepHealth.org, “The State of Sleep Health in America in 2023,” sleephealth.org. This reflects a growing awareness of sleep’s importance for overall health and wellness, driving demand for products that enhance rest quality. In the United States, households increasingly seek mattresses that provide measurable benefits, including orthopedic support, temperature regulation, and allergen control, often guided by physician advice or wellness routines. Similar trends are emerging in urban India, where consumers view high-quality beds as long-term wellness investments, encouraging trade-up behavior toward premium designs. Brands are responding by emphasizing scientifically backed sleep benefits, durable construction, and advanced features that justify higher price points. Marketing is increasingly focused on objective outcomes rather than brand or price alone, supporting the global growth of premium mattresses.

Direct-to-consumer e-commerce boom

Digital-first buying journeys are reshaping the mattress market, but the most effective strategies now combine online convenience with in-person testing to reduce uncertainty about comfort and support. Omnichannel retail models link local showrooms with regional digital marketing and customer care, helping lower return rates and build consumer trust. In India, expanding logistics networks into tier-2 and tier-3 cities, flexible payment options, and localized content are making it easier for first-time buyers to access premium mattresses. Brands are enhancing e-commerce platforms with appointment-based consultations, home trials, and improved site experiences to address fit and delivery concerns that previously limited online adoption. This integrated approach strengthens lifetime value, boosts conversion in high-intent areas, and enhances resilience across demand cycles. The United States Census Bureau reports that retail e-commerce accounted for 16.4% of total United States retail sales in Q3 2025, highlighting sustained growth in online channels and the expanding role of D2C strategies in the mattress market[2]U.S. Census Bureau, “Quarterly Retail E Commerce Sales Report,” census.gov/retail/ecommerce.html.

Global hospitality & real-estate buildout

Beds are now a central component of the guest experience in many hotel brands, which lifts specifications for comfort, hygiene, and longevity. Hospitality operators test co-branded or branded checkout links to capture follow-on demand as travelers want the same experience in their homes after a good night’s sleep. Residential projects in Asia-Pacific add new housing stock and commission bundled bed-and-mattress packages to simplify setup and shorten delivery cycles for buyers. In the GCC, national development plans create multi-year pipelines in hospitality and residential nodes that require reliable mattress fulfillment within tight commissioning windows. This steady procurement supports high-volume runs, predictable receivables, and is often paired with structured after-sales service that reinforces brand reputation for the mattress market.

Breakthrough cooling & adaptive material technology

Thermal comfort and responsive support drive a steady wave of material innovation across foams, coils, and covers. Industry R&D focuses on conductive additives, phase-change coatings, and breathable constructions that preserve airflow while maintaining pressure relief and spine alignment. Trade publications track graphene and graphite infusions, advanced gel chemistries, and antimicrobial components designed to address heat, odor, and cleanliness concerns. Leading brands layer breathable covers, zoned foams, and adaptive cores to hold perceived temperature within comfortable bands without compromising support. Product cycles also emphasize durability through denser foams, stronger perimeter reinforcement, and hybrid builds that maintain form over years of use in the mattress market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petro-foam, coil & latex input costs | -1.2% | Global, with acute impact in manufacturing hubs | Short term (≤2 years) |

| Replacement-cycle lengthening in saturated markets | -0.8% | North America & Western Europe | Medium term (2-4 years) |

| EPR regulations elevating end-of-life disposal expenses | -0.6% | EU regulatory leadership; California pioneering in the US | Medium term (2-4 years) |

| Limited supply of certified bio-latex & natural fibers | -0.4% | Global, with sourcing concentrated in Southeast Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile petro-foam, coil & latex input costs

Feedstock volatility has raised the difficulty of budgeting core inputs, and quarterly swings in polyurethane resin pricing create margin pressure on entry-level assortments. Regional price trends show asynchronous movements, which complicates global sourcing and makes contract coverage and inventory position more critical for the mattress market. Shipping-route disruptions lifted container costs well above historical averages in 2024 and forced manufacturers to layer surcharges across quarters to manage working capital and landed costs. Latex markets tightened as weather and disease lowered yields in key producing countries, a pattern that continued into 2025 with expectations of production shortfalls that kept replacement costs elevated for latex-forward SKUs. Vertically integrated producers with captive foam capacity and scale procurement hold an advantage during these cycles because they can react faster to mix-shift and pass-through.

EPR regulations elevating end-of-life disposal expenses

Growing regulatory focus on sustainability is driving mattress manufacturers to manage end-of-life products more effectively. In 2025, California and Connecticut raised mattress recycling fees to USD 16 per unit under state EPR programs, increasing costs for manufacturers and retailers and influencing pricing and supply chain decisions[3]Mattress Recycling Council, “Recycling Fee for California and Connecticut Programs to Increase Jan 1, 2025,” mattressrecyclingcouncil.org. The United States stewardship programs are expanding large-scale mattress collection and recycling, creating predictable compliance costs across entry- and mid-price tiers. In Europe, mature EPR regimes are advancing recycling rates and introducing digital product passports, requiring investment in data systems and labelling that smaller brands may struggle to fund. Manufacturers are responding with modular designs, simplified materials, and clear dismantling instructions to streamline recycling, reduce waste, and maintain operational efficiency in the mattress market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mattress Type: Latex Growth Outpaces Innerspring Volume

Innerspring mattresses held a 43.44% market share in 2025, reflecting the scale of legacy demand and price accessibility in value-oriented channels for the mattress market. The format remains familiar for replacement purchases across mature markets, with regional suppliers catering to tight budgets and high turn ratios. Latex products are positioned on support, breathability, and allergen resistance, and they benefit from circular economy messaging in urban buyers who emphasize durable and recyclable builds. Hybrid constructions blend coils with latex or gel foams to create targeted responsiveness and airflow, and they continue to anchor new premium launches across brand portfolios. The result is a type of mix where entry price points lean on innerspring volume while higher tiers expand variety through latex-forward and hybrid options that defend premium price realization.

Latex is the fastest-growing segment at a CAGR of 9.87% through 2031, as consumers link firmness profiles and orthopedic benefits to better daily comfort and long-term posture management in the mattress market. Durability and ventilation resonate in humid climates, and dust-mite resistance carries additional weight in Indian metros with prolonged warm seasons. The value proposition supports above-average trade-up rates in urban channels as shoppers move from foam or basic spring builds to latex or hybrid designs. Suppliers strengthen the narrative with clearer material disclosures and independent certifications where feasible, which support trust at checkout. As education improves and test-lie opportunities widen, latex and hybrids continue to capture new-to-premium demand without displacing entrenched innerspring volume at the mass end.

By Size: King-Size Expansion Reflects Changing Space Preferences

Queen-size held 48.35% of the market in 2025, a function of room dimensions in standard apartments and the balance between surface area and footprint in the mattress market. The format remains the chief choice in mid-market master bedrooms and in new flat sales where developers design for queen footprints. Trading up to king-size has gained momentum as owners prioritize personal space, co-sleeping accommodations, and overall sleep comfort in core living spaces. Hospitality specifications also favor larger formats in suites and premium rooms, which influence consumer preference after stay experiences. Retailers reflect this mix with deeper queen assortments and targeted king expansions in metros and suburbs with larger average bedrooms.

King-size records the fastest growth rate at 8.64% through 2031 as post-2020 home layouts and discretionary comfort improvements remain in focus in affluent cohorts. The pattern shows up in India’s premium residential towers and independent housing, where bedroom layouts support bigger frames. As renovation cycles advance in upper mid-income households, larger mattresses migrate from aspiration to planned purchase in multi-year home budgets. Hospitality pipelines that specify premium bedding keep r egular volume flowing in king sizes, which sustains manufacturing runs and scale. With room-by-room planning and higher awareness of ergonomic benefits, larger formats hold share gains even as queen-size remains the anchor of the consumer stack for the mattress market.

By End User: Residential Volumes Drive Commercial Velocity

Residential accounted for 71.87% of 2025 demand and will grow at a CAGR of 7.87% through 2031, anchored by replacement cycles and first-time buying as housing additions accelerate across Asia-Pacific for the mattress market. The category benefits from heightened sleep-health awareness that reframes mattresses as wellness purchases with clear daily utility. Urban Indian customers often evaluate orthopedic support and cooling properties, which maintain momentum for latex and hybrid builds in premium sub-buckets. Retail education, in-home trials, and clear warranties reduce perceived risk, which helps close sales at higher price points. These dynamics support resiliency in residential volumes even when discretionary budgets rotate toward services in mature markets.

Commercial demand expands faster on a smaller base, with hotels, healthcare facilities, and student housing introducing consistent batch orders. Hotel operators prioritize guest sleep as a top satisfaction lever, which lifts specifications for comfort consistency, hygiene, and replacement planning. Healthcare facilities add antimicrobial surfaces and wipeable covers in higher-use beds, with procurement teams aligning to infection control requirements. Indian tier-2 cities see a new hospitality supply that pairs local tourism initiatives with modern room standards, which creates structured pipeline orders for the mattress market. Commercial buyers value predictable lead times and post-delivery service, which rewards suppliers with organized production and regional fulfillment capacity.

By Distribution Channel: Online Growth Reshapes B2C Dynamics

B2C channels captured 64.84% in 2025, supported by specialty formats and multi-brand furniture distribution in urban and semi-urban zones for the mattress market. Within B2C, online subchannels will post the fastest growth to 2031 as customers seek transparent specs and flexible payment options. At the same time, physical showrooms remain crucial because many buyers want to test feel, firmness, and edge support before committing to mid- and high-ticket purchases. The strongest results come from omnichannel paths that tie local retail to targeted digital outreach, at-home delivery, and live service for post-purchase support. This mix protects conversions, reduces returns, and steadies repeat purchases through coordinated customer engagement.

B2B channels serve hospitality and healthcare, along with residential developers who specify bundled bedroom solutions. Europe’s public and corporate procurement processes emphasize ESG criteria and recycling readiness, which favor vendors that can document content and end-of-life outcomes. In India, developers in growth corridors push for reliable schedules and durable support to streamline handovers, which rewards brands that can meet project timelines. These buyers often bypass retail markups to secure value while maintaining specification quality, which stabilizes order books for manufacturers. The channel mix continues to evolve as brands find the right balance between direct relationships, retail partners, and digital acquisition for the mattress market.

Geography Analysis

North America accounted for 36.39% of the mattress market in 2025, but shipments declined as replacement cycles lengthened and consumers shifted spending toward experiences. Extended Producer Responsibility programs and environmental fees are impacting pricing and margins for budget models. Brands are strengthening omnichannel strategies, using physical stores to boost online conversions through local fulfillment and test-and-try models. Larger players continue vertical integration, aligning foam capacity, retail banners, and brand portfolios to maintain service levels and working capital efficiency. In contrast, Asia-Pacific is the fastest-growing region at an 8.54% CAGR through 2031, driven by rising incomes, urbanization, and construction activity that fuels new households and hotels.

China’s secondary urban centers are adopting hybrid and gel-cooled mattresses, while tier-1 buyers focus on performance and brand trust. India’s organized retail is expanding into tier-2 and tier-3 cities, with delivery networks and payment options enabling first-time buyers. Southeast Asia and India face latex supply dynamics, with potential shortfalls prompting attention to sourcing alternatives. Consumers across the region increasingly differentiate by cooling, orthopedic support, and material transparency, boosting premium segment growth. Rising urban populations and disposable incomes further support demand for mid- and high-tier mattresses.

Europe is seeing growth in sustainability-focused mattresses, especially in Germany, Sweden, and the Netherlands, where digital product passports improve traceability and recycling readiness. Circular initiatives, such as foam-to-foam recycling, are reducing emissions and returning materials to furniture production, while mature EPR programs in France, Belgium, and the Netherlands are raising compliance requirements for manufacturers. In South America, trends are mixed; Brazil benefits from urban housing programs, but inflation is limiting purchasing power and extending replacement cycles. Chile, Peru, and Argentina are gradually adopting e-commerce, though logistics and payment challenges remain. Local manufacturers are leveraging cotton, wool, and eucalyptus to compete on price with imported foam and latex, while export-oriented producers pursue ISO and OEKO-TEX certifications for hospitality markets.

Competitive Landscape

The mattress market exhibits varying competitive intensity across regions, with consolidation dominating North America and Europe, while Asia-Pacific and select emerging markets remain fragmented. In February 2025, Tempur Sealy acquired Mattress Firm and rebranded the combined entity as Somnigroup, creating a vertically integrated structure with pro-forma sales near USD 8 billion and targets of USD 200 million by 2027[4]Somnigroup International, “Tempur Sealy Completes Name Change to Somnigroup International,” somnigroup.com. This integration aligns brand management, retail networks, and manufacturing assets, enabling better fixed-cost absorption and pricing discipline. Upstream suppliers are also moving downstream, as seen with Casper’s acquisition by a major foam producer, which stabilizes production volumes under contract arrangements. These developments raise the strategic bar for smaller brands, with vertical integration, omnichannel execution, and premium differentiation emerging as critical success factors in mature markets.

Product leadership leans on material and design advances that address thermal comfort, pressure relief, and hygiene. Trade sources document foam innovations, conductive and antimicrobial infusions, and hybrid architectures that target stability, edge support, and breathability. Retailers and DTC brands focus on fit and education through test-lie opportunities, live support, and simplified sizing to align products with shopper needs in India’s metros and beyond. Large retailers are investing in circularity by backing recycling infrastructure and introducing designs with modular components that speed dismantling. This innovation cycle reinforces premium positioning while helping producers manage end-of-life obligations as EPR regimes expand, which supports the long-run economics of the mattress market.

Brand portfolios balance mass and premium to reach diverse income tiers, and omnichannel execution connects physical and digital experiences to lift conversion. Showroom openings by digital natives continue in key metros, because many buyers want to confirm firmness and surface feel before purchase. Commercial accounts expand through hospitality and healthcare projects, with tender criteria leaning toward hygienic covers, antimicrobial layers, and documented materials. India and Southeast Asia remain fragmented at the regional level, with more than 50 brands competing on price as well as on hyperlocal blends such as coir-cotton, which are familiar to local buyers. Multinationals must either acquire at premium valuations to build reach or cede distribution to local incumbents that control last-mile logistics, which maintains a long tail of competitors in the mattress market.

Mattress Industry Leaders

Tempur Sealy International Inc.

Serta Simmons Bedding LLC

Sleep Number Corporation

Casper Sleep Inc.

Purple Innovation Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Emma Sleep partnered with OUR HOME in the Philippines, launching at SM City North EDSA, SM Megamall, and SM Mall of Asia with products including the Emma Bedframe, Diamond Hybrid 2.0, and Original Hybrid 2.0.

- January 2025: IKEA's Ingka Group earmarked over USD 1 billion for investments in three recycling ventures (RetourMatras for mattresses, Morssinkhof Rymoplast, and Next Generation Group for plastics) and one food-waste software firm (Winnow), expanding mattress-recycling capacity to 2.5 million units annually across seven facilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the mattress market as all newly manufactured sleeping surfaces that use innerspring, foam, latex, hybrid, gel, or similar core technologies and are sold as finished bed units to residential or commercial end users worldwide. Mattresses integrated into adjustable bases or sold in "-in-a-box" formats are counted within scope, while aftermarket toppers or loose bedding are not.

Scope exclusion: Mattress toppers, pads, pillows, and related linens lie outside this analysis.

Segmentation Overview

- By Mattress Type

- Innerspring Mattresses

- Foam Mattresses (including memory foam)

- Latex Mattresses

- Hybrid Mattresses

- Gel Mattresses

- Other Mattresses

- By Size

- Single-size

- Double-size

- Queen-size

- King-size

- Other Sizes

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2B/Directly from the Manufacturers

- B2C/Retail Channels

- Specialty Bedding and Mattress Stores

- Multi-brand Stores/Home Centers

- Online

- Other Distribution Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Aisa Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mattress producers, foam formulators, and large hospitality procurement heads across North America, Europe, and Asia Pacific. Discussions tested replacement-cycle assumptions, average selling prices, channel mix shifts, and emerging features (cooling foams, smart sensors), enabling us to refine desk findings and close data gaps before model sign-off.

Desk Research

We began by mapping supply-side fundamentals using open data from the United States Census Bureau housing starts, Eurostat building permits, UN Comtrade HS-9404 trade flows, and the International Sleep Products Association shipment reports. These were paired with consumer-side indicators such as WHO back-pain prevalence studies, Statista e-commerce penetration series, and national hotel pipeline figures from STR. Proprietary inputs from D&B Hoovers and Dow Jones Factiva helped size leading manufacturers and spot material price swings. The sources listed illustrate the breadth of public and paid inputs; many further references supported verification and clarification tasks.

Market-Sizing & Forecasting

A top-down demand pool was constructed from household stock, new dwelling completions, and hotel bed additions, which are then multiplied by replacement rates and unit penetration factors. Selected bottom-up checks, sampling producer revenues and online unit sales, validated totals. Key variables include average unit price trends, urbanization rates, e-commerce share, GDP per capita, and latex/PU foam cost indices. Forecasts apply multivariate regression blended with scenario analysis to reflect economic cycles and raw-material volatility. Expert inputs guide variable sensitivities and gap handling where bottom-up evidence is thin.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst audits, and final lead-analyst approval. Reports refresh annually, with interim updates triggered by supply shocks, regulatory shifts, or M&A events, so clients receive a timely baseline.

Why Mordor's Mattress Baseline Commands Reliability

Published estimates often diverge because firms select different product mixes, price assumptions, and refresh cadences.

Key gap drivers include a narrower "mattress-only" scope at some publishers, aggressive ASP escalation curves, or models based solely on producer revenue without adjusting for channel mark-ups and gray imports. Mordor's disciplined variable selection and yearly refresh keep our figures balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.82 B (2025) | Mordor Intelligence | |

| USD 46.48 B (2024) | Global Consultancy A | Excludes gel and medical hybrids; older base year; limited primary checks |

| USD 54.75 B (2024) | Industry Association B | Relies on manufacturer invoices; no adjustment for retail mark-ups or online DTC volumes |

The comparison shows that while totals cluster, our approach blends transparent scope choices, live primary validation, and cross-channel adjustments, giving decision-makers a dependable, reproducible benchmark.

Key Questions Answered in the Report

What is the current size and growth outlook of the mattress market?

The mattress market size is USD 57.31 billion in 2026 and is projected to reach USD 78.06 billion by 2031 at a 6.38% CAGR.

Which region will expand the fastest through 2031 within the mattress market?

Asia-Pacific is the fastest-growing region with an 8.54% CAGR through 2031 due to rising incomes, new housing, and broader retail reach.

How are regulations like EPR and digital product passports affecting the mattress market?

EPR programs add eco-fees and recovery mandates, and Europe’s digital product passports by 2027 require new traceability systems, which raise compliance costs but drive design for recyclability.

What channel strategies are shaping demand in the mattress market?

Omnichannel execution is central as online selection pairs with in-person testing in showrooms, which reduces return risk and lifts conversions in high-intent locations.

Which formats and materials are gaining traction in the mattress market?

Latex and hybrids gain share on ergonomic support, breathability, and thermal comfort, while innovations in foams and covers target cooler sleep and longer durability.

Page last updated on: