Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 15.46 Billion |

| Market Size (2031) | USD 22.86 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

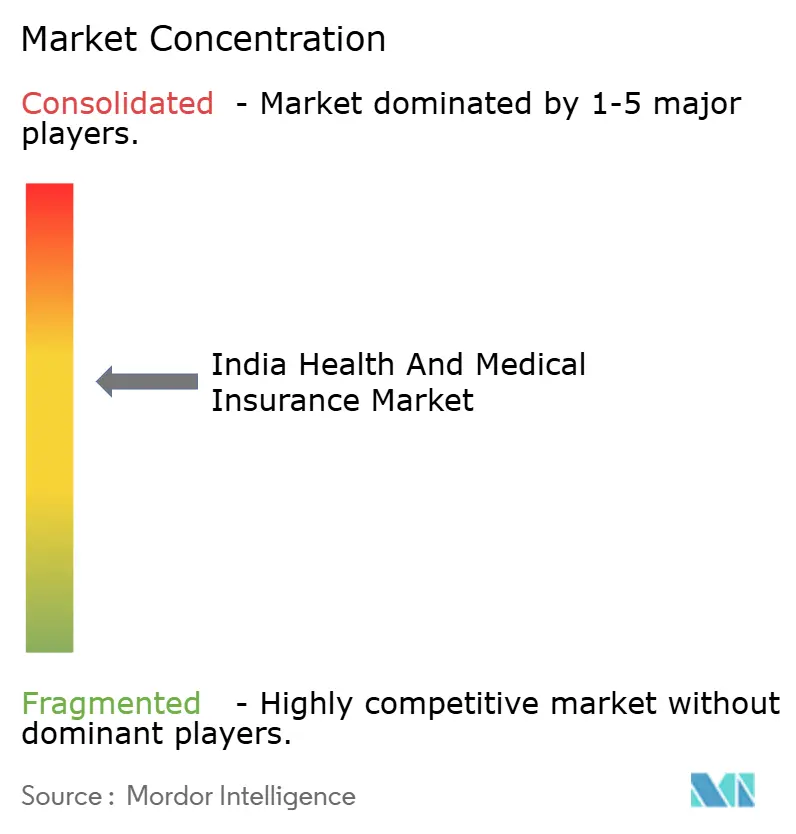

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Health And Medical Insurance Market Analysis by Mordor Intelligence

The India Health And Medical Insurance Market size in terms of gross written premiums value is expected to grow from USD 15.46 billion in 2026 to USD 22.86 billion by 2031, at a CAGR of 8.13% during the forecast period (2026-2031).

Growth is driven by increasing healthcare utilization, regulatory simplifications, and digitized workflows that enhance accessibility across demographics. Private-sector innovation and expanded distribution channels are boosting competition and insurance penetration in urban and semi-urban areas. Initiatives like the National Health Claims Exchange are improving transparency and reducing turnaround times, while government policies, including Ayushman Bharat’s expansion and regulator-mandated service standards, sustain demand across retail and group segments.

Medical cost inflation and advancements in clinical technology are prompting earlier adoption of insurance. Regulatory measures, such as stricter cashless approval and discharge standards, have improved service quality. API-driven issuance models are streamlining processes, reducing manual inputs, and enhancing distribution efficiency. Government initiatives, including Ayushman Bharat Health Account (ABHA) identity creation and National Health Claims Exchange (NHCX) claims routing, are fostering interoperability between hospitals and insurers, enabling consistent claims processing. The market is positioned for growth, driven by rising medical costs and digitized service delivery.

Key Report Takeaways

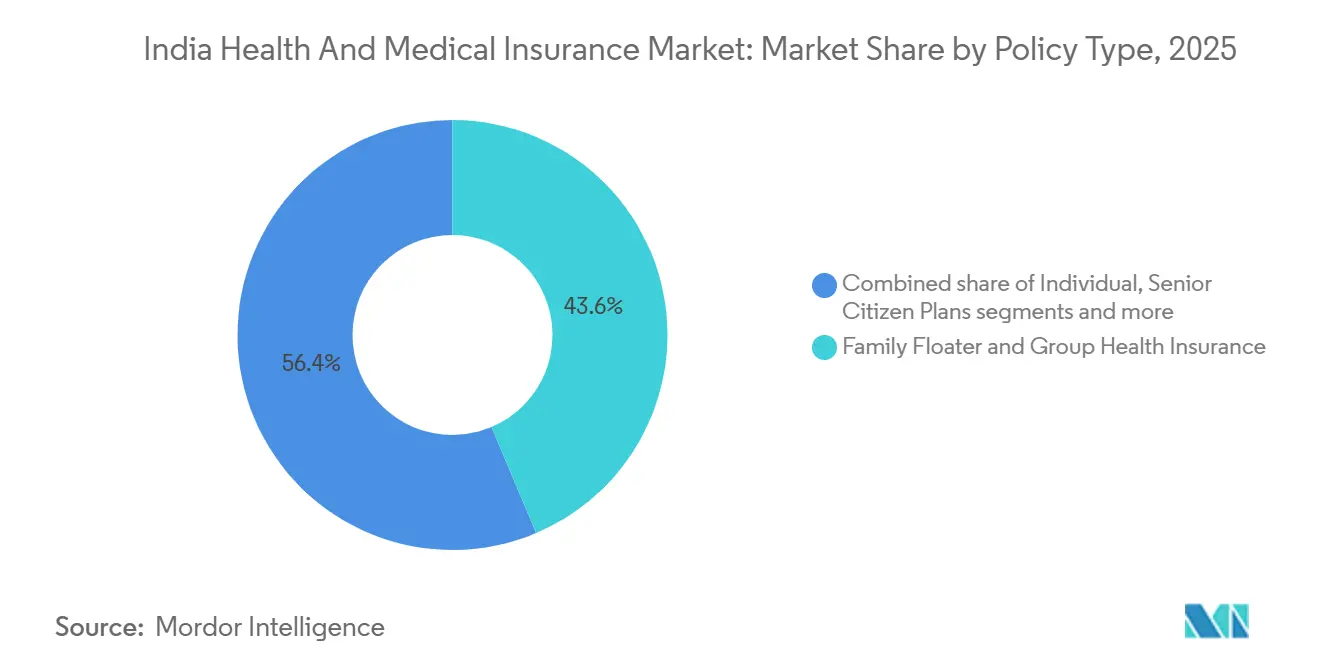

- By policy type, family floater and group health coverage led with 43.63% of the India health and medical insurance market share in 2025. Critical illness cover is projected to expand at a 17.50% CAGR through 2031.

- By coverage type, inpatient hospitalization accounted for 58.12% of the India health and medical insurance market share in 2025. Outpatient and day-care coverage is projected to record an 18.34% CAGR through 2031.

- By demographic age group, the 19-45 years cohort held 35.67% of the India health and medical insurance market share in 2025. The ≥61 years cohort is projected to grow at a 15.70% CAGR through 2031.

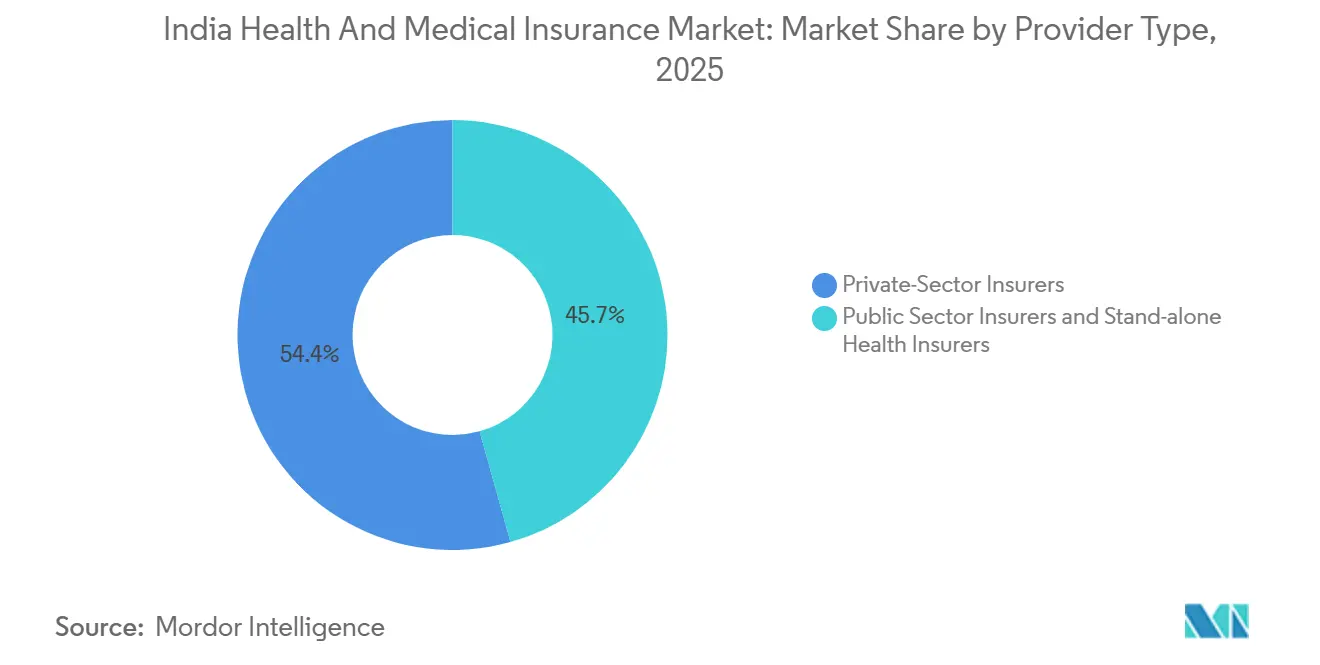

- By provider type, private-sector insurers held 54.35% of the India health and medical insurance market share in 2025. Stand-alone health insurers are projected to grow at a 17.32% CAGR through 2031.

- By distribution channel, agents and brokers held 49.18% of the India health and medical insurance market share in 2025. Digital and online channels are projected to post a 22.34% CAGR through 2031.

- By geography, West India led with 28.12% of the India health and medical insurance market share in 2025. South India is projected to grow at a 12.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Health And Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare costs elevating demand for financial protection | +2.1% | Global, particularly acute in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Government programmes and tax incentives | +1.8% | National, with early gains in Odisha, Delhi, Uttar Pradesh | Short term (≤ 2 years) |

| Growing middle-class income and health-risk awareness | +1.5% | APAC core, spill-over to tier-2/3 cities | Long term (≥ 4 years) |

| Digital distribution platforms expanding reach | +1.3% | Urban metros spreading to semi-urban centers | Medium term (2-4 years) |

| Uptake of OPD and wellness add-ons for retention | +0.8% | Tier-1 cities, corporate group policies | Medium term (2-4 years) |

| Wearable-driven dynamic pricing by insurtechs | +0.4% | Metro cities, tech-savvy demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Costs Elevating Demand for Financial Protection

Medical inflation and rising specialization in tertiary care have increased the financial burden on households, strengthening the role of indemnity health insurance as a risk management tool. Industry analyses point to cost escalation risks in India’s health system, which continues to shift treatment volumes toward higher-acuity settings and newer clinical technologies that carry premium price points. The regulator’s tighter service standards for cashless authorization windows improve predictability at admission and discharge, which reduces friction for policyholders and hospitals. Digital identity and claims rail deployment across the public health stack, including ABHA and the NHCX, enables standardized data flows that support faster adjudication and fewer documentation errors.[1]Press Information, “Update on National Health Claims Exchange,” Ministry of Health & Family Welfare, mohfw.gov.in Urban and peri-urban consumers are responding by selecting higher sum-insured slabs and renewing coverage consistently, particularly in segments sensitive to out-patient spending and elective procedures. The India health and medical insurance market is therefore supported by a structural shift toward pre-emptive financial protection as healthcare costs trend higher.

Government Programmes and Tax Incentives

Ayushman Bharat has scaled hospital coverage for eligible families at the national level and has broadened access by onboarding additional states and beneficiaries across income groups. The program’s digital rails, including the claims exchange and health IDs, create end-to-end traceability and provide the underpinnings for faster benefit realization in network hospitals across India. Parallel to public coverage expansion, regulator-led reforms have eased age restrictions, streamlined pre-existing disease waiting periods, and set service-level expectations that improve consumer confidence in private health insurance. The move toward Goods and Services Tax (GST) relief on select retail health policies reduced the all-in cost of coverage for many households, and insurers have communicated the direct pass-through of savings on policy pricing since the change took effect in September 2025. Collectively, these policy actions stimulate demand and help the India health and medical insurance market sustain growth across both group and retail products.

Growing Middle-Class Income and Health-Risk Awareness

Income growth and urbanization are changing purchase behavior as households prioritize financial protection for health risks alongside other essential expenses. Awareness of the cost of care and the role of preventive check-ups is rising, and this is evident in the growing preference for products that blend hospitalization benefits with outpatient and wellness services. The India health and medical insurance market is benefiting from improved digital literacy that simplifies discovery, comparison, and activation for first-time buyers. Younger families are using employer-provided benefits as a baseline, then adding retail policies and top-ups to close coverage gaps and protect against catastrophic events. The growing awareness of chronic disease risk has also increased interest in lump-sum benefits and specialized riders that complement standard indemnity coverage.

Digital Distribution Platforms Expanding Reach

Digital issuance and embedded insurance have reshaped acquisition models, with API-first platforms now supporting large shares of new policies and renewals across retail lines. At multiple private insurers, digital channels are operating at scale, with API integrations accounting for a material share of policy issuance and driving down manual processing rates for new business and endorsements. Insurers are upgrading core systems to cloud-native, automated stacks that deliver straight-through processing in medical underwriting and simplify claims intake for policyholders. One example is the deployment of Duck Creek OnDemand to build and launch a new health line in months, which is now enabling seamless issuance for customers with pre-existing conditions[2]Corporate Communications, “HDFC ERGO Becomes India’s First Insurer to Service Health Insurance Using Duck Creek OnDemand,” Duck Creek Technologies, duckcreek.com. Upcoming marketplace infrastructures such as Bima Sugam aim to unify quote, purchase, renewal, and claims tracking, which should reduce information asymmetry and boost transparency for consumers. These digital rails increase choice and speed, which strengthens the appeal of the India health and medical insurance market to younger and digitally native buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low rural penetration & trust deficit | -1.2% | Rural India, North/East regions (J&K, Bihar, Manipur) | Long term (≥ 4 years) |

| High claim ratios and medical inflation pressure | -0.9% | National, particularly urban hospitals | Short term (≤ 2 years) |

| Complex policy wording causing mis-selling concerns | -0.6% | National, with higher impact in tier-2/3 cities and rural areas | Medium term (2-4 years) |

| Data-privacy worries around health analytics | -0.4% | Urban metros, digitally-savvy demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Rural Penetration and Trust Deficit

Penetration gaps persist in rural and remote districts due to lower awareness, affordability constraints, and limited access to network facilities. Consumers in these regions often face information barriers and have fewer branch or advisor touchpoints to support policy purchase and claim filing. The India health and medical insurance market continues to rely on multi-pronged approaches, including women-led local distribution and simplified composite products, to bridge these gaps. Public digital rails can also help by lowering documentation burdens and improving cashless access where empanelled providers are available. Sustained ecosystem action combining insurer outreach, local health infrastructure, and targeted government programs remains essential to raise adoption and utilization in rural areas.

High Claim Ratios and Medical Inflation Pressure

Health insurers are managing higher incurred claim ratios relative to pre-pandemic baselines, shaped by broader coverage features and higher utilization of cashless pathways. Medical inflation still outpaces the headline consumer price index (CPI) in many categories, which complicates annual pricing cycles and requires stronger underwriting discipline. The regulator has emphasized financial prudence and solvency guardrails, while nudging carriers toward transparent communications when repricing becomes necessary. Insurers have responded with product redesigns, targeted repricing across books, and tighter fraud controls to stabilize combined ratios. These measures, along with operational digitization and hospital network management, are key to preserving unit economics as the India health and medical insurance market scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Policy Type: Corporate Demand and Catastrophic-Risk Products Reshape Portfolio Mix

Family floater and group health policies held the largest portfolio position with 43.63% of the India health and medical insurance market share in 2025, reflecting employer program breadth and household preference for shared-sum cover in urban centres. Employer-driven programs offer a base layer of protection that often becomes the springboard for retail top-ups among working-age families. The India health and medical insurance market has also seen greater interest in catastrophic-risk riders and lump-sum critical illness benefits that complement indemnity structures. This is consistent with rising awareness of lifetime costs associated with severe conditions, where a one-time payout can stabilize finances beyond hospitalization expenses. The resulting mix supports risk pooling at scale while improving flexibility for buyers seeking both day-to-day value and protection against high-severity events.

Critical illness cover is the fastest-growing policy type at a projected 17.50% CAGR from 2026 to 2031 as attention shifts to catastrophic events and income protection. Senior citizen plan uptake improved after the elimination of upper age limits for entry and the streamlining of pre-existing disease waiting periods, which has broadened access for older adults. The India health and medical insurance market is also seeing a steady pickup in top-up and super top-up adoption because these options expand coverage economically when the base policy is in place. Modular product design with customizable riders is resonating with younger cohorts who expect flexible benefits that align with their evolving life and health stages. Insurers continue to refresh policy constructs to balance affordability, coverage depth, and claim service under tighter service-level standards.

By Coverage Type: OPD Surge and Digital Wellness Redefine Benefit Scope

Inpatient hospitalization remained the coverage foundation with a 58.12% share in 2025, which reflects how policyholders value financial protection for high-acuity events. Standardized pre-authorization and discharge authorization service levels, set by the regulator, have improved timeliness for cashless care and enhanced predictability for beneficiaries and providers. The India health and medical insurance market continues to embed pre- and post-hospitalization features, room rent rules, and bundled services that together reduce out-of-pocket volatility. As care models evolve, carriers are integrating hospital and home-care capabilities to serve short-stay and step-down needs where clinically appropriate. Over time, this helps align indemnity features with modern clinical pathways while protecting policyholders from cost spikes.

Outpatient and day-care coverage is the fastest-growing benefit set at a projected 18.34% CAGR from 2026 to 2031 as consumers seek day-to-day value and earlier intervention options. Digital health touchpoints such as teleconsultation and e-pharmacy are now common in plan designs, and they support better care continuity at lower cost. The NHCX is architected to cut claim processing costs by standardizing payloads on Fast Healthcare Interoperability Resources (FHIR) and routing claims digitally, which improves feasibility for scaled OPD automation. The India health and medical insurance market is therefore moving toward more frequent-use benefits while preserving strong hospitalization coverage for high-severity events. This combination improves both perceived value and risk management outcomes for employers and retail buyers.

By Demographic (Age Group): Millennial Adoption and Senior Citizen Inclusion Broaden Risk Pool

The 19-45 years cohort held the largest demographic position at 35.67% in 2025, reflecting peak economic activity and family formation stages that prioritize financial protection. Younger buyers prefer flexible, modular plans with wellness-linked rewards, mental health consults, and out-patient benefits that improve daily utility. The India health and medical insurance market is also seeing stronger engagement with telemedicine and pharmacy benefits among this cohort, which helps cement renewal behaviour. As digital distribution expands, enrolment and service in this age band continue to improve due to simpler plan selection and faster issuance. Product features like age-locking of premiums until the first claim resonate with buyers concerned about long-term affordability.

The ≥61 years cohort is the fastest-growing segment at a projected 15.70% CAGR through 2031 after age-entry restrictions were removed and waiting periods were streamlined. Senior-friendly plan designs and service-level mandates for cashless approvals have eased access for older adults seeking first-time coverage or higher sums insured. The India health and medical insurance market is also supported by public safety nets for the elderly, which reduces catastrophic risk transfer to households and encourages voluntary private cover for incremental protection. Insurers continue to enhance protection features and upgrade provider networks to ensure that seniors can access quality care with predictable claim outcomes. This supports balanced risk pooling while broadening social protection against health shocks.

By Provider Type: Stand-Alone Health Insurers Outpace General Insurers Amid Profitability Challenges

Private-sector insurers held a 54.35% share in 2025 as both general and stand-alone carriers expanded product lines and distribution. General insurers continue to offer health alongside motor and property lines, while stand-alone health specialists deepen focus on retail indemnity and ancillary benefits. The India health and medical insurance market benefits from this mix because it promotes innovation and diversification in pricing and service models. Competitive differentiation is now visible in claims experience, onboarding friction, and embedded partnerships that bring health cover closer to everyday digital journeys. In parallel, underwriting discipline and solvency safeguards remain front and centre as medical inflation and claim frequencies evolve.

Stand-alone health insurers are the fastest-growing provider category at a projected 17.32% CAGR from 2026 to 2031, supported by focused retail strategies and data-led claims management. Several stand-alone players have publicly outlined growth and profitability paths that emphasize repricing actions, portfolio recalibration away from unprofitable segments, and fraud control investments. The India health and medical insurance market is also benefiting from product refresh cycles, broader hospital networks, and improved digital service across retail and group books. These actions have helped stabilize combined ratios at some carriers while supporting premium growth in key cities and adjacent districts. Sustained operational discipline will remain critical as new benefits and higher-sum policies scale across cohorts.

By Distribution Channel: Digital-First Models Disrupt Traditional Agency Networks

Agents and brokers held a 49.18% distribution share in 2025, supported by advisory-led sales for first-time buyers and senior customers who value in-person guidance. Agency networks continue to anchor retail growth and renewal stability because they help explain policy terms and navigate claims steps for households. The India health and medical insurance market still benefits from bancassurance and corporate channels for reach, but advisory remains pivotal in retail indemnity products. Renewal strength in agency-heavy portfolios indicates that service and education drive persistence in indemnity lines more than in pure benefit products. Insurers use training, digital tools, and standardized disclosures to keep advisory quality high and to ensure consistency in customer experience across geographies.

Digital and online distribution is the fastest-growing channel at a projected 22.34% CAGR from 2026 to 2031, driven by API issuance, partner integrations, and direct-to-consumer platforms. At several carriers, nearly half of new policies now move via APIs in comprehensive embedded ecosystems spanning mobility, commerce, and hospitality. Straight-through onboarding and automated medical underwriting, enabled by cloud-native core systems, reduce cycle times and manual interventions. The India health and medical insurance market benefits from these cost and speed gains because they enhance unit economics and widen access across age and income bands. Marketplace infrastructure such as Bima Sugam is expected to further streamline discovery, comparison, and post-sale service, which supports deeper digital adoption[3]Product Team, “Bima Sugam – India’s One-Stop Digital Insurance Platform,” Bima Sugam, bimasugam.co.in.

Geography Analysis

West India held a 28.12% share in 2025, driven by dense urban centers and a large middle-class population supporting retail and group demand. Employer-sponsored coverage in major cities complements retail growth among younger families and pre-senior demographics. The market benefits from diversified provider networks and strong tertiary care clusters, enabling higher sums insured. City-level price points and hospital density influence product adoption, shaping perceived value and renewal behavior. Distribution is supported by agency networks and digital platforms, leveraging the region's digital readiness.

South India is projected to grow at a 12.56% CAGR from 2026 to 2031 due to strong state-level implementation of public schemes and high health literacy. Public-private collaboration in hospital networks and claims processing supports higher utilization of cashless pathways in several states. The market is leveraging this base with expanded branch networks, advisor recruitment, and corporate tie-ups in IT and service hubs. Growth is further aided by preventive health awareness and willingness to pay for quality healthcare. As digital adoption expands, the region is expected to maintain a growth advantage.

North India shows mixed performance, with strong infrastructure and corporate demand in some states, contrasted by lower coverage in certain districts requiring targeted outreach. The market is addressing these gaps through advisory-led acquisition, digital servicing, and employer partnerships to enhance penetration.

East India offers growth potential due to nascent infrastructure in parts of the region and targeted state initiatives improving access. Enhancements in claims processing systems and hospital empanelment quality are critical for building trust and increasing adoption. Scaling the market will rely on public-private collaboration and gradual distribution growth in semi-urban and rural districts.

Regulatory Landscape

Health and medical insurance in India is regulated by the Insurance Regulatory and Development Authority of India (IRDAI) under the Insurance Act, 1938 and the IRDAI Act, 1999. Product design and conduct rules were tightened through the IRDAI (Insurance Products) Regulations, 2024. In May 2024, IRDAI issued the Master Circular on Health Insurance Business (dated 29 May 2024), consolidating dozens of earlier instructions into a single framework covering disclosures, claims servicing, portability, and service standards, and requiring non-compliant products to be modified by 30 September 2024. These measures reinforce uniform customer servicing expectations in cashless workflows while pushing insurers to broaden product availability across ages and medical conditions.

Public health-financing programs and digital public infrastructure also shape the operating environment. Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) provides INR 5 lakh per family per year cover for eligible households, and the scheme was expanded in October 2024 to extend treatment benefits up to INR 5 lakh per year to senior citizens aged 70 years and above irrespective of socio-economic status. The National Health Authority (NHA) has also rolled out tools such as the Hospital Engagement Module (HEM 2.0) to streamline hospital empanelment, supporting wider network participation and interoperability across payers and providers.

Value Chain Analysis

The value chain starts with product design, pricing, and risk management by public sector insurers, private general insurers, and stand-alone health insurers, operating within IRDAI product and conduct rules, including the May 2024 Master Circular. Distribution then runs through agents and brokers, bancassurance, corporate and group sales, and digital and online platforms that use API-led issuance and embedded partnerships. Underwriting and servicing are supported by insurtech and core-platform vendors, including cloud-native core adoption for health product build and straight-through medical underwriting, as well as ecosystem rails such as ABHA identity and the National Health Claims Exchange (NHCX), which standardize data movement between hospitals and insurers.

Claims administration and provider management sit at the operational center of the chain. Third Party Administrators (TPAs) registered with IRDAI provide claims processing and administrative services alongside insurer in-house claims teams for cashless and reimbursement workflows. Upstream dependencies include hospital networks (public and private), diagnostics, pharmacies, and home-care providers that affect utilization and claim severity, while downstream outcomes depend on claim turnaround times, cashless experience, grievance handling, and renewal persistence. Documentation variability and fraud or leakage control remain key bottlenecks, and these are being addressed through digital claims routing (NHCX), standardized service-level expectations under IRDAI guidance, and increasing use of AI-enabled claims platforms by large insurers and TPAs.

Competitive Landscape

The India health and medical insurance market remains moderately consolidated, with the top 20 carriers together capturing a substantial share of gross written premiums, while no single player dominates the overall space. Private-sector carriers hold a clear edge in product innovation and digital operations, with stand-alone specialists scaling retail-focused propositions and broader networks. Several leaders have announced technology modernizations that compress issuance and servicing times, reduce manual touchpoints, and improve underwriting precision. The result is a competitive cycle centred on claim experience, speed of service, and embedded distribution economics rather than price alone. Regulatory solvency and transparency expectations reinforce discipline as portfolios are repriced and redesigned in response to medical inflation.

Selected market leaders illustrate these shifts through concrete moves over 2025 and 2026. One private carrier deployed a cloud-native core to build and launch health business capabilities with high straight-through rates, which now supports customers with pre-existing conditions through automated underwriting. Another scaled API issuance such that nearly half of new policies flow through partner integrations with minimal manual processing, indicating that embedded models are reaching critical mass. The India health and medical insurance market is also seeing capital-raising and portfolio actions that support growth while strengthening solvency and operating resilience. Together, these steps reflect a focus on quality of growth and institutional strength, not just headline premium expansion.

White-space opportunities center on rural penetration, senior inclusion, OPD benefits, mental health cover, and prevention-led engagement anchored in digital rails. Marketplace infrastructure backed by industry stakeholders aims to unify discovery and service, which could shift acquisition costs and commission structures over time. As core systems modernize and claims rails mature, the India health and medical insurance market can improve predictability and customer experience at scale. Profitability will hinge on continued repricing discipline, fraud analytics, and portfolio hygiene, supported by regulatory guardrails for solvency and consumer protection. Across these themes, firms that execute consistently on service, technology, and transparency will be best placed to compound share over the medium term.

India Health And Medical Insurance Industry Leaders

New India Assurance Co. Ltd.

Star Health and Allied Insurance Co. Ltd.

ICICI Lombard General Insurance Co. Ltd.

HDFC ERGO General Insurance Co. Ltd.

Bajaj Allianz General Insurance Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digitized claims and consent-based health data rails create a concrete whitespace for insurers to expand OPD, day-care, and wellness-linked propositions with lower servicing friction. The Government of India launched Aarogya Setu 2.0 under the Ayushman Bharat Digital Mission (ABDM) in June 2026 as a unified gateway for personal health records, PM-JAY wallet integration, and private insurance claim access. In parallel, the NHCX portal standardizes claim data formats to support faster cashless settlements between hospitals and insurers. As smaller providers digitize through programs such as the Digital Health Incentive Scheme (DHIS) and lightweight HMIS stacks such as C-DACs eSushrut@Clinic, insurers can access a larger interoperable network for pre-auth, discharge, and post-treatment documentation flows.

Product and segment expansion opportunities are also reinforced by recent policy actions that broaden eligibility and encourage inclusion. AB PM-JAY's October 2024 expansion to cover all citizens aged 70 years and above (with benefits up to INR 5 lakh per year) increases hospital network throughput and supports consumer familiarity with cashless pathways, which private insurers can build on with top-ups, higher sum-insured retail covers, and critical illness or domiciliary options. On the supply side, insurer investments in automation and analytics, including AI-led claims intelligence deployments, support tighter fraud controls and more consistent claim outcomes. This helps insurers package higher-frequency benefits (OPD, diagnostics, teleconsults) alongside core inpatient indemnity in a more sustainable way.

Recent Industry Developments

- June 2026: Star Health and Allied Insurance Co. Ltd. entered into a three-year partnership with Amplify Health to deploy AI-powered claims intelligence and healthcare analytics across its operations. The arrangement is designed to support automated claims triage and fraud-leakage controls, enabling faster cashless decisioning at scale across a large retail-heavy book.

- November 2025: Allianz SE completed the sale of 9.84% in Bajaj Allianz Life Insurance and 9.90% in Bajaj Allianz General Insurance to Bajaj Finserv, following required approvals. The transaction shifted operational control to Bajaj Finserv, affecting governance and strategic execution in one of India's major general insurers with a meaningful health portfolio.

- May 2024: IRDAI issued the Master Circular on Health Insurance Business, consolidating multiple prior circulars into a single framework and tightening expectations on policyholder servicing and claims processes. The consolidation increased compliance standardization across insurers and intermediaries, accelerating product and process updates to align with the 2024 product regulations and service benchmarks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the value of health and medical insurance premiums written in India for medical cost coverage, including hospital treatment, day care procedures, and selected critical illness benefits sold through insurers.

Scope exclusions: Travel insurance, personal accident only covers, and credit linked covers are excluded, and we also do not count government scheme transfers as insurance premium market value.

Segmentation Overview

- By Policy Type

- Individual Health Insurance

- Family Floater and Group Health Insurance

- Senior Citizen Plans

- Critical Illness Cover

- Top-Up & Super Top-Up

- By Coverage Type

- In-patient Hospitalization

- Out-patient & Day-care (OPD)

- Domiciliary Treatment

- Maternity & Newborn Cover

- Alternative Treatments (AYUSH)

- By Demographic (Age Group)

- 0-18 Years

- 19-45 Years

- 46-60 Years

- ≥ 61 Years

- By Provider Type

- Public Sector Insurers

- Private Sector Insurers

- Stand-alone Health Insurers

- By Distribution Channel

- Agents & Brokers

- Bancassurance

- Digital / Online

- Direct Sales

- Corporate Sales (Group Policies)

- By Region

- North India

- South India

- East India

- West India

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the premium pool context and timeline using public, non paywalled sources such as IRDAI annual reports, Ministry of Finance releases, and the National Health Accounts (Government of India) for healthcare spend direction. We also reviewed RBI macro series for inflation and INR to USD trends, and used published findings from peer reviewed health financing and insurance penetration studies to keep assumptions realistic.

On the industry side, we used insurer annual reports, investor presentations, and product filings to understand premium mix shifts, policy duration practices, and claim cost commentary that impacts pricing. Select paid subscriptions were used only for insurer financials and intelligence, plus news and financials tracking, so that premium growth and major rule changes were not missed. The desk source list is illustrative, and many other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate premium growth drivers, loss ratio direction, and product level shifts (such as group versus retail and top up behavior) that desk sources often describe only at a high level. We spoke with insurers, distributors, healthcare payment stakeholders, and policy administrators across India to check assumptions on pricing, renewal behavior, and claim inflation across different customer types and major state clusters.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | |

| Mid tier: 42% | Functional/Unit leaders: 26% | |

| Smaller Players: 20% | Managers: 57% |

Market-Sizing & Forecasting

For sizing, the model is built mainly from a top-down premium pool reconstruction, where insurer level gross written premium by health line is aligned to regulator reporting and then adjusted for definitional items in scope. Once the premium pool is set, it is split and sense checked using selective bottom-up approximations, such as sampled premium per policy times estimated covered lives, channel mix checks, and roll ups of reported health premium for a sample of insurers, which are then used to tune the final total.

A few practical inputs were used to keep the numbers tied to real market movement, including reported health premium growth rates, medical inflation direction, claim frequency and severity commentary, mix shift between group and individual covers, average sum insured movement, and renewal versus new business contribution. Forecasts were developed using scenario analysis supported by simple trend fitting, where premium growth is linked to healthcare cost inflation and expected insurance penetration changes discussed by interviewees. When bottom-up signals were missing for smaller insurers or informal distribution pockets, gaps were handled through proportional allocation based on observed premium shares, then rechecked against industry wide totals.

Data Validation & Update Cycle

Outputs are checked against independent signals, such as regulator reported health premium totals, macro indicators that influence premium affordability, and sharp year on year jumps that can come from accounting changes or one time policy shifts. If a variance looks unusual, we revisit the assumption chain, recheck the desk source trail, and then reconnect with selected respondents to confirm what changed and when.

Before sign off, results go through multi step analyst review so that currency conversion timing, year labeling, and scope boundaries are consistently applied. The report is refreshed once each year, and interim updates are triggered when material events occur, such as major regulatory changes, large premium rate resets, or public disclosures that change the addressable premium pool. Right before delivery, a final pass is completed so clients receive the most current view.

Mordor Intelligence's India Health and Medical Insurance Market Size Versus Other Published Estimates

Published market sizes for India health and medical insurance can look far apart because sources do not always use the same premium definition, time basis, or inclusions around government supported coverage. Differences also show up when one estimate is built as premium written, another is built as revenue, and the currency conversion year is not aligned.

By tracking gross written premium definitions and constant dollar conversion timing, Mordor Intelligence sits closer to a regulator style premium pool, while some estimates mix new business only, broader revenue constructs, or a wider product bundle that pulls totals upward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.46 B (2026) | |

| Industry Research Firm A | USD 16.17 B (2025) | Frames the market as overall market value or revenue and uses a different base year, which can pull in items beyond written premium and makes year to year comparability harder. |

| Global Analytics Publisher B | USD 15.06 B (2024) | Uses GWP but also reports a separate new business premium lens, and the shorter forecast window with higher growth assumptions can create a steeper curve than a longer period view. |

Taken together, the spread is explained less by math and more by what is counted and which year is treated as the anchor. Our approach stays traceable to premium pool logic, uses clear inclusions and exclusions, and then cross checks the result with interview based reality checks so it can be repeated and updated without guesswork.

Key Questions Answered in the Report

What is the India health and medical insurance market growth outlook to 2031?

The India health and medical insurance market is projected to grow at an 8.13% CAGR through 2031, supported by rising medical costs, regulatory service standards, and scaled digital rails for issuance and claims.

Which channels are growing fastest in India health and medical insurance?

Digital and online distribution is the fastest-growing channel, with API-led issuance and embedded partnerships reducing manual steps and expanding access across retail cohorts.

How are government platforms influencing the India health and medical insurance market?

The National Health Claims Exchange and ABHA identity are improving interoperability, traceability, and claim processing speed, which enhances customer experience and lowers administrative costs.

Which policy types lead adoption in India health and medical insurance?

Family floater and group policies lead due to employer programs and shared-sum benefits for households, while critical illness cover is the fastest-growing as buyers prioritize catastrophic-risk protection.

What is the regional outlook for India health and medical insurance?

West India holds the largest share due to urban density and employer coverage, while South India is the fastest-growing region on the back of strong scheme implementation and high health literacy.

What are the key operational priorities for insurers in India health and medical insurance?

Priorities include repricing discipline, fraud analytics, portfolio hygiene, and technology modernization for straight-through onboarding and faster cashless claim decisions under regulator-led service benchmarks.

Page last updated on: