Lab Automation For In-Vitro Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

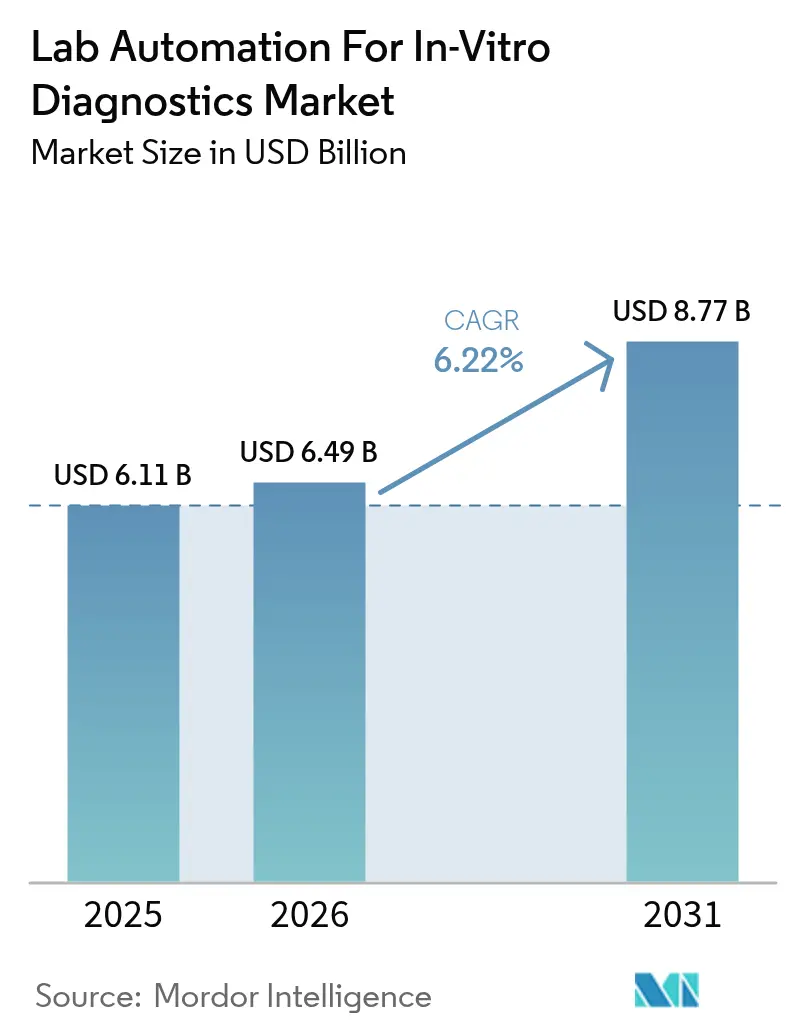

| Market Size (2026) | USD 6.49 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lab Automation For In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Lab Automation For In-Vitro Diagnostics market size was valued at USD 6.11 billion in 2025 and estimated to grow from USD 6.49 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Rising chronic-disease screening volumes, persistent workforce shortages, and the integration of artificial-intelligence quality algorithms push laboratories toward fully automated, high-throughput platforms. North America remains the reference region because stringent oversight speeds adoption, while Asia-Pacific accelerates the fastest as hospital chains invest in decentralized genomics capacity. Equipment innovation centers on miniaturized micro-fluidic formats that support point-of-care testing, and connectivity software now ranks with robotics as a prime selection criterion. Major suppliers pursue vertical integration so that hospitals can source pre-analytics, analytics, and post-analytics modules from a single vendor.

Key Report Takeaways

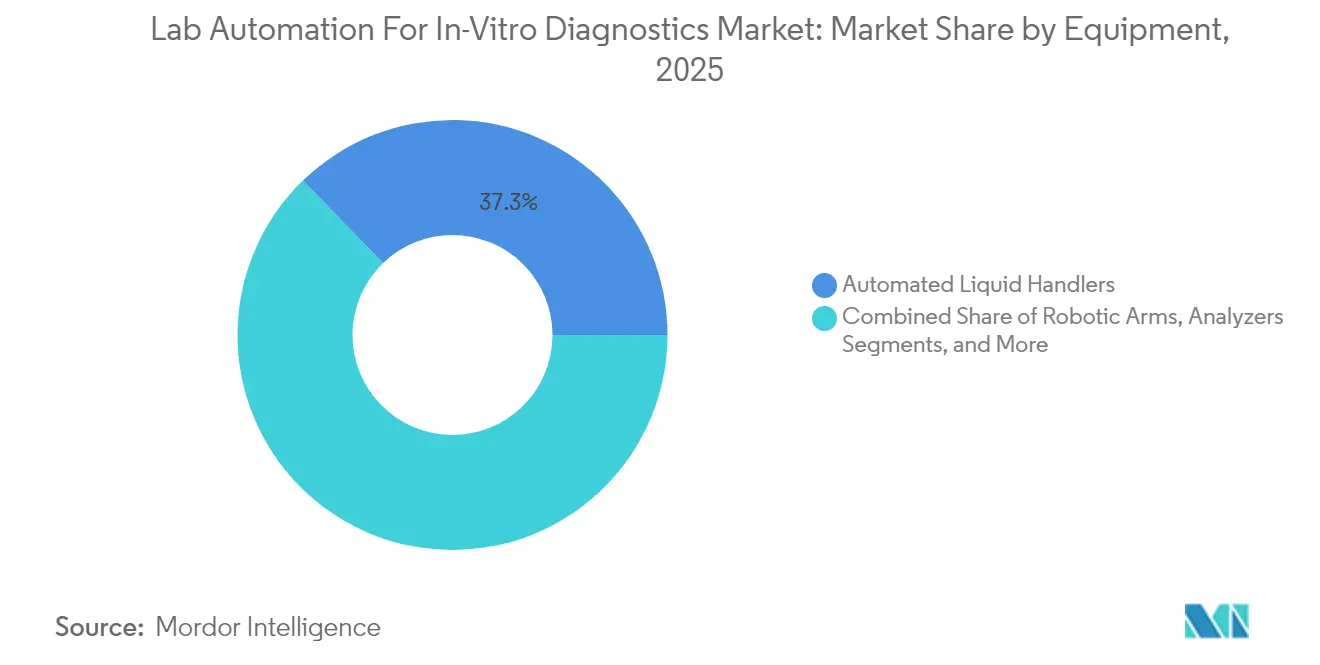

- By equipment, automated liquid handlers held 37.25% of Lab Automation For In-Vitro Diagnostics market share in 2025, and micro-fluidic platforms are advancing at a 6.66% CAGR to 2031.

- By process step, pre-analytical sample preparation led with 42.20% revenue share in 2025, while data management and connectivity records the highest projected CAGR at 6.86% through 2031.

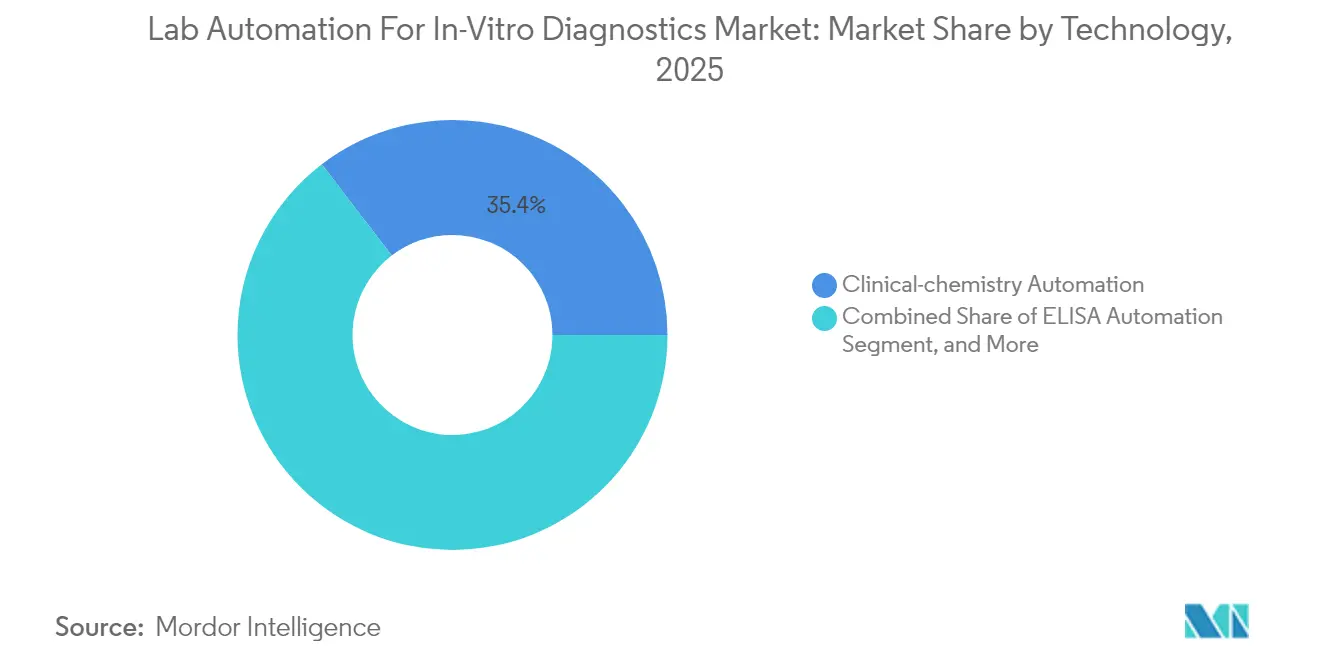

- By technology, clinical-chemistry automation accounted for 35.40% of the Lab Automation For In-Vitro Diagnostics market size in 2025 and molecular and PCR automation is rising at a 7.12% CAGR to 2031.

- By end user, hospitals and reference laboratories commanded 51.10% of demand in 2025 in the Lab Automation For In-Vitro Diagnostics market, whereas biopharma and biotechnology companies show the fastest growth trajectory at 6.74% through 2031.

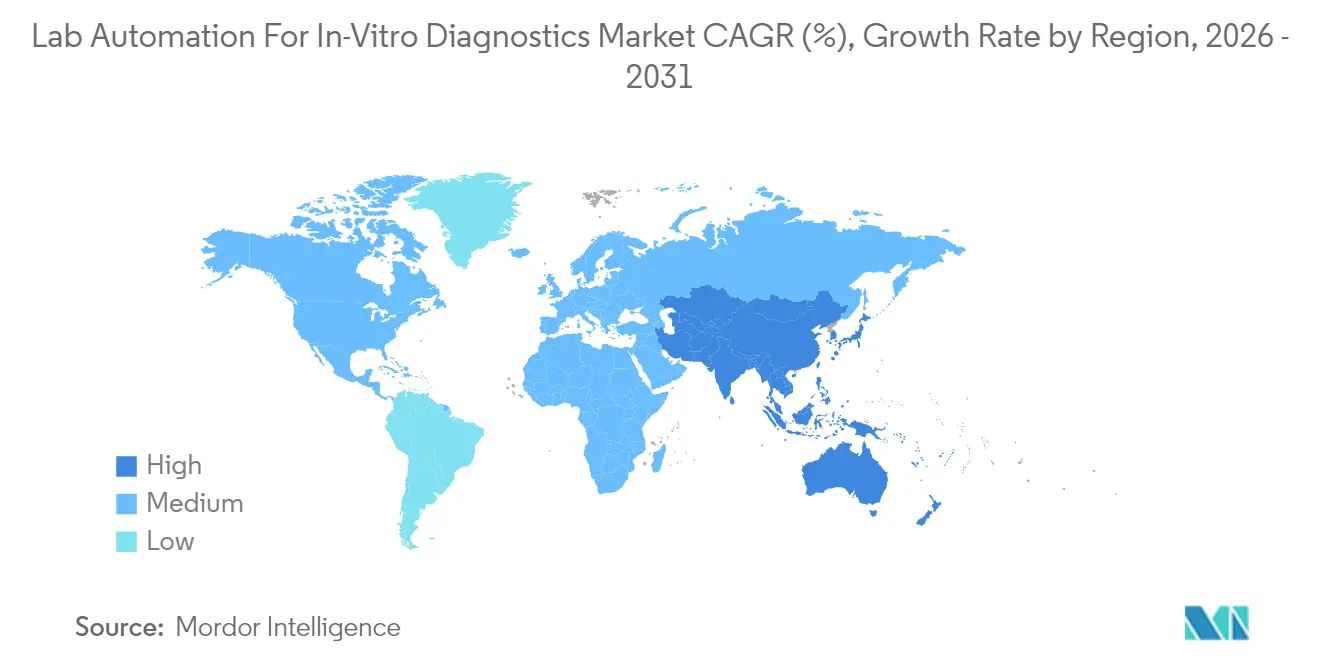

- By geography, North America commanded 38.20% of demand in 2025 in the Lab Automation For In-Vitro Diagnostics market, whereas Asia-Pacific show the fastest growth trajectory at 6.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lab Automation For In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for high-throughput sample processing | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising test volumes from chronic-disease burden | +1.5% | Global, with highest impact in Asia-Pacific | Long term (≥ 4 years) |

| Shortage of skilled technicians accelerating automation | +1.8% | North America and Europe primarily, expanding to APAC | Short term (≤ 2 years) |

| AI-driven closed-loop QC algorithms | +0.9% | North America and Europe early adoption, global expansion | Medium term (2-4 years) |

| Decentralization of genomics to hospital labs | +0.7% | Global, with early gains in urban centers | Long term (≥ 4 years) |

| EU IVDR traceability mandates | +0.4% | Europe primarily, with spillover to export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for High-Throughput Sample Processing

Centralized laboratories now process thousands of daily specimens, and manual workflows cannot meet the 15–20% annual volume growth recorded since 2024.[1]Thermo Fisher Scientific, “Fourth Quarter and Full Year 2024 Results,” thermofisher.com Integrated workcells address this pressure by unifying liquid handling, incubation, and detection in a single production line. Health-system procurement teams increasingly value sample-per-hour metrics above capital cost, shifting tender evaluations toward fully automated configurations. High throughput also supports consolidated quality management because fewer touchpoints lower cumulative error risk. Vendors respond with modular designs that scale from 500 to 5,000 samples per shift, allowing hospitals to phase investments as test menus expand.

Rising Test Volumes from Chronic-Disease Burden

Population aging and universal screening initiatives generate sustained demand for assays that track diabetes, cardiovascular markers, and oncology biomarkers. Each oncology patient may require multiple molecular panels, effectively multiplying the requisition count per clinical encounter.[2]Abbott Laboratories, “Automated Testing Platform Launch,” abbott.com Developing economies add volume rapidly because public health programs extend diagnostics to rural clinics yet transmit specimens to urban hubs, further taxing central laboratories. Automation delivers consistent pipetting precision necessary for PCR and NGS assays, improving reproducibility across expanding test menus. Government payers favor automated platforms when cost-per-result decreases as batch sizes grow.

Shortage of Skilled Technicians Accelerating Automation

Vacancy rates for experienced molecular technologists exceed 20% in the United States, and educational pipelines cannot replenish retirees quickly enough.[3]American Association for Clinical Chemistry, “Laboratory Workforce Shortage Drives Automation,” aacc.org Laboratories reassign remaining personnel to interpretive tasks while robots assume repetitive pipetting and plate handling. Salary inflation shortens the automation payback period to three years in high-volume core labs. Vendors now embed user-friendly interfaces so that generalists can supervise systems after a brief training course, reducing onboarding times versus legacy manual protocols.

AI-Driven Closed-Loop QC Algorithms

Machine-learning models embedded in instruments detect drift patterns and trigger preventive maintenance before results fall outside control limits.[4]Siemens Healthineers, “AI-Powered Laboratory Automation,” siemens-healthineers.com Real-time optimization trims reagent consumption by adjusting aspiration heights dynamically, preserving assay accuracy while cutting operating cost. Continuous feedback minimizes the need for manual calibration, harmonizing performance across multi-site hospital networks. Automated flagging of questionable results shortens exception handling cycles and elevates overall laboratory uptime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment and ROI uncertainty | -1.1% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Interoperability issues with legacy LIMS | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Cyber-security risks for networked analyzers | -0.6% | Global, with heightened concern in regulated markets | Long term (≥ 4 years) |

| Robotics-component supply-chain volatility | -0.7% | Global, with particular impact on new installations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and ROI Uncertainty

Comprehensive automation suites cost USD 500,000-5 million, a hurdle for mid-size private laboratories. CFOs struggle to model savings from error reduction or faster turnaround, lengthening approval cycles. Maintenance contracts and software licenses add recurring fees that elevate total cost of ownership beyond sticker price. Tier-two hospitals sometimes postpone investment until patient volumes reach thresholds that assure a three-to-five-year payback.

Interoperability Issues with Legacy LIMS

Many older information systems lack modern HL7 or FHIR compatibility, requiring middleware that erodes automation efficiency. Mapping sample IDs between platforms introduces bottlenecks that offset robotics throughput. Middleware also raises cyber-security exposure when multiple translation layers complicate patch management. Laboratories embarking on digital-first strategies often replace LIMS before adding new automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Liquid Handlers Drive Adoption

Automated liquid handlers accounted for 37.25% of Lab Automation For In-Vitro Diagnostics market share in 2025, underscoring their role as the backbone of molecular and immunoassay workflows. Robotic grippers and machine-vision modules enable these platforms to integrate centrifugation, heating, and real-time error detection, raising yield per batch. Growing test complexity encourages laboratories to layer ultraviolet decontamination and HEPA filtration into handler enclosures, protecting sensitive nucleic-acid assays. Integrated workcells bundle storage, pipetting, and detection in one chassis, helping facilities conserve floor space while achieving end-to-end automation.

The micro-fluidic segment records the quickest momentum at a 6.66% CAGR. Miniaturized cartridges carry out multiplex PCR, immunoassay, and ELISA reactions with microliter volumes, curbing reagent expense and biohazard waste. Hospitals adopt tabletop micro-fluidic analyzers in emergency departments to provide molecular respiratory panels within an hour. Research centers value the platform for single-cell analytics and organ-on-chip projects that traditional robots cannot handle at scale.

By Process Step: Connectivity Ascends

Pre-analytical sample preparation still represents 42.20% of 2025 revenue because barcoding, aliquoting, and decapping remain foundational tasks. Advances in adaptive grippers and artificial-vision inspection lower hemolysis and clot detection errors, improving downstream result integrity. Yet laboratories increasingly measure return on investment by complete turnaround time, causing attention to migrate toward data orchestration.

Data management and connectivity posts a 6.86% CAGR, benefiting from middleware that unifies analytical islands into a real-time dashboard. Cloud-hosted platforms synchronize instrument performance, reagent inventory, and quality metrics across multi-hospital networks, supporting enterprise-wide decision making. Vendors integrate application programming interfaces that feed anonymized data into research pipelines, converting routine diagnostics into discovery assets while meeting privacy regulations.

By Technology: Molecular Workflows Accelerate

Clinical-chemistry automation captured 35.40% of the 2025 Lab Automation For In-Vitro Diagnostics market size thanks to high-volume assays such as electrolytes and metabolic panels. Consolidated analyzers offer photometric, turbidimetric, and ion-selective modules in one carousel, streamlining maintenance for core labs. Immunoassay systems expand chemiluminescent detection ranges, enabling simultaneous viral and hormone panels.

Molecular and PCR automation grows at 7.12% as infectious-disease surveillance and oncology demand multiplex biomarkers. Pre-assembled extraction cartridges and closed pipetting channels eliminate contamination risk integral to PCR. Library-prep robots for next-generation sequencing scale sample capacity from 48 to 384 per run, meeting oncology tumor-profiling demands in regional cancer centers. Vendors pair robotics with AI-driven variant-calling software, shrinking the analysis bottleneck that once offset bench-side processing gains.

By End User: Research Sector Outpaces Healthcare

Hospitals and reference laboratories retained 51.10% market share in 2025 because core labs process chemistry and hematology panels for inpatient and outreach services. Emergency departments push short turnaround targets that make on-site automation unavoidable. Reference laboratories leverage 24/7 robotic lines to win health-system outsourcing contracts by guaranteeing same-night reporting.

Biopharma and biotechnology companies register a 6.74% CAGR, using robotics to expedite lead identification, biomarker validation, and companion-diagnostic co-development. Automation ensures lot-to-lot reproducibility critical for regulatory filings. Biotech startups prefer cloud-connected disposable-tip systems that align with flexible R&D workflows without dedicated maintenance staff.

Geography Analysis

North America’s 38.20% revenue contribution in 2025 mirrors the region’s stringent quality standards and early reimbursement for molecular diagnostics. U.S. health networks expand centralized testing hubs that courier specimens overnight, stimulating orders for high-throughput integrated lines. Canada’s public plans fund provincial genomics centers that adopt micro-fluidic automation to manage limited technician rosters.

Europe demonstrates balanced adoption as IVDR rules enforce electronic traceability and proficiency testing. Germany anchors vendor revenue with its dense hospital laboratory base, while the Netherlands champions early field trials of cloud-connected workflow managers. United Kingdom procurement favors service contracts that bundle hardware, reagents, and informatics under operating leases, easing budget approvals during NHS modernization.

Asia-Pacific leads expansion at 6.66% CAGR through 2031. China subsidizes regional diagnostic chains that outfit multi-story labs with robotic sorters and track-and-trace conveyors. India’s private hospitals set up molecular suites using mid-capacity liquid handlers to compete on oncology turnaround time. Japan’s super-aging society keeps per-capita test volumes high, and domestic vendors partner with universities to pilot AI-enabled quality modules. ASEAN economies focus on micro-fluidic point-of-care devices for infectious diseases where central lab access is limited.

Regulatory Landscape

Regulation for lab automation in in-vitro diagnostics is tightening around software validation, traceability, and quality-system alignment as instruments become more connected and algorithm-driven. In the European Union, IVDR implementation continues to raise evidence and documentation requirements for automated systems that include data interpretation. In 2026, EU Commission actions, including mandatory use of EUDAMED for the first four modules and updates to IVDR harmonized standards via Implementing Decision (EU) 2026/1313, reinforce the need for up-to-date technical documentation, labeling, and UDI-linked device records.

In the United States, FDA oversight is converging on ISO-aligned manufacturing and broader control of diagnostic software and laboratory workflows. The Quality Management System Regulation (QMSR), aligning 21 CFR Part 820 with ISO 13485:2016, takes effect in 2026 for medical device and IVD manufacturers, increasing expectations for design controls, supplier management, and software change control in automated platforms. Separately, the FDA LDT Final Rule (2024) introduces a phased transition for many laboratory-developed tests, with registration requirements beginning May 6, 2026 for covered categories. This adds compliance urgency for labs that automate LDT-heavy molecular menus and for vendors supplying automation plus interpretation software.

Value Chain Analysis

The value chain spans component and consumables suppliers (robotics, sensors, specialty plastics, reagents, and assay consumables), automation OEMs (liquid handlers, integrated workcells, and micro-fluidic platforms), and software layers (middleware, LIMS integration, cybersecurity, and remote monitoring). Downstream, distribution occurs through direct enterprise sales and channel partners into hospitals, reference labs, and biopharma. Recent product and approval activity illustrates how regulatory clearance and clinical performance claims shape adoption: Roche received FDA 510(k) clearance in March 2026 for cobas c 703 and cobas ISE neo analytical units to increase capacity and automation efficiency, while Waters announced an IVDR CE mark in April 2026 for the BD BACTEC FXI Culture System. Together, these moves highlight the compliance and evidence burden tied to high-throughput automated workflows.

Integration and service delivery are increasingly defined by partnerships across automation specialists, IVD manufacturers, and lab workflow providers, particularly where bottlenecks sit in pre-analytical handling and interface friction rather than the analyzer alone. QIAGEN partnering with Inpeco (announced May 2026) to develop a fully automated Sample-to-Insight workflow is one example, and ABB Robotics collaborating with Roche Diagnostics (initiated July 2026) to develop autonomous mobile manipulators for pathology slide handling and sample movement is another. Such collaborations influence procurement, shifting value from standalone instruments toward validated end-to-end systems that include installation, interoperability engineering, and ongoing software updates.

Competitive Landscape

Industry structure is moderately consolidated. Roche, Danaher, and Abbott anchor portfolios that cover sample prep to LIS connectivity, locking in customers who prefer single-supplier support. Roche deepened molecular reach by acquiring cartridge-based PCR automation, broadening menu depth for hospital labs. Danaher’s latest liquid handler embeds vision analytics that auto-adjust dispense volumes, reducing reagent wastage. Abbott’s all-in-one PCR instrument, approved by FDA in late 2024, targets near-patient oncology testing.

Specialists such as Tecan and Hamilton compete through customizable deck layouts and open-software ecosystems that attract research institutions. Micro-fluidic innovators license polymer-chip patents to major IVD firms, inserting their technology into distributed analyzers. Artificial-intelligence startups collaborate with tier-one instrument makers to co-develop predictive maintenance modules that extend instrument uptime guarantees.

Value-added service models gain traction: vendors bundle reagent rentals, operator training, and remote performance dashboards into monthly fees, easing budget constraints for mid-tier hospitals. Open-architecture initiatives attempt to break vendor lock-in by promoting standardized robotic interfaces, yet proprietary consumable patents remain a formidable moat.

Lab Automation For In-Vitro Diagnostics Industry Leaders

Cognex Corporation

Thermo Fisher Scientific Inc.

Danaher Corporation

Siemens Healthineers AG

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening where laboratories need end-to-end automation that reduces manual steps beyond the analyzer, particularly in microbiology and molecular diagnostics, while meeting more demanding traceability and quality requirements. The April 2026 IVDR CE mark announcement for the BD BACTEC FXI Culture System points to continued investment appetite for fully automated, high-throughput microbiology platforms that standardize pre-analytical variables, such as blood volume measurement, and support consistent downstream processing. In parallel, Bruker introduced the MyGenius PRO sample-to-answer PCR system in April 2026, signaling productization of compact molecular automation that shortens workflows and supports decentralized testing in hospital labs.

Informatics and connectivity also remain a practical opportunity area because interoperability issues with legacy LIMS and rising cybersecurity requirements limit realized throughput from installed robotics. The May 2026 step-up in EU EUDAMED requirements and the 2026 US FDA QMSR transition increase the value of vendors that can supply validated software documentation, change-control discipline, and UDI-linked traceability in addition to hardware. Partnerships that close integration gaps, such as QIAGEN and Inpeco (May 2026) and ABB Robotics with Roche Diagnostics (July 2026), offer a pathway for laboratories to automate pre-analytical transport, sample logistics, and chain-of-custody tasks that affect turnaround time and staffing efficiency.

Recent Industry Developments

- July 2026: ABB Robotics and Roche Diagnostics initiated a collaboration to develop autonomous mobile manipulators for pathology slide handling and sample movement in clinical laboratories. The work targets automation of intra-lab logistics, extending automation benefits from bench-level robotics into pre- and post-analytical transport. This supports laboratories pursuing higher throughput with fewer manual handoffs, while also raising the importance of validated safety, tracking, and integration interfaces.

- July 2025: Thermo Fisher Scientific introduced the Oncomine Comprehensive Assay Plus for the Ion Torrent Genexus System. The release expands menus that can be run on automated molecular workflows, reinforcing the trend toward sample-to-report solutions that combine instruments, assays, and software. Broader assay coverage strengthens platform stickiness in hospital and reference labs standardizing precision-medicine pipelines.

- October 2024: Abbott gained FDA clearance for an integrated PCR workcell aimed at acute-care laboratories. The clearance supports near-patient molecular testing where automation reduces hands-on time and variability in urgent workflows. It also signals ongoing regulatory acceptance of more integrated automation footprints in clinical settings, shaping vendor roadmaps for compact, connected systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers lab automation systems and related solutions used inside in vitro diagnostics workflows to handle, move, prepare, store, and analyze patient samples, along with connectivity that helps labs run these steps with less manual work.

Scope exclusions: We exclude general purpose research automation that is not used for IVD testing, and we also exclude consumables and general lab furniture that do not directly automate a diagnostic workflow.

Segmentation Overview

- By Equipment

- Automated Plate Handlers

- Automated Liquid Handlers

- Robotic Arms

- Automated Storage and Retrieval Systems

- Analyzers

- Integrated Workcells

- Micro-fluidic Platforms

- By Process Step

- Pre-analytical (Sample Prep)

- Analytical

- Post-analytical

- Data Management and Connectivity

- By Technology

- Clinical-chemistry Automation

- Immunoassay Automation

- Molecular and PCR Automation

- NGS Library-prep Automation

- ELISA Automation

- By End User

- Hospitals and Reference Laboratories

- Clinical Diagnostics Laboratories

- Academic and Research Institutions

- Biopharma and Biotechnology Companies

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Our desk research starts by pinning down the addressable IVD lab workflow and the typical automation touchpoints that show up across pre-analytical, analytical, and post-analytical steps. Public sources are used to ground the demand context, such as CDC laboratory guidance and data releases, FDA device databases and recall notices, OECD health statistics, WHO health systems indicators, and select peer reviewed journal articles on lab throughput and error reduction.

We then map the supply side using company filings, investor presentations, product brochures, and reputable press releases to understand where revenue is likely to sit across major automation modules and integrated systems. A paid subscription for company financials and news is used to cross-check reported segment revenues, and a patent database helps confirm which automation technologies are seeing sustained development. The desk sources listed here are not exhaustive, and many other public references were also used to collect data, validate assumptions, and clarify points during analysis.

Primary Interviews and Surveys

Primary work was used to pressure test what we built from public information, mainly around installed base patterns, typical upgrade cycles, and how labs decide between modular automation and more integrated lines. We spoke with a mix of automation suppliers, lab directors, procurement teams, and workflow managers across APAC, EMEA, and the Americas so that regional adoption differences and budget realities could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 21% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 22% | EMEA: 29% |

| Smaller Players: 22% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where lab testing volumes and automation penetration signals are used to reconstruct the spend pool for IVD lab automation, and then it is distributed across major equipment categories and regions. To keep the totals realistic, the result is corroborated with selective bottom-up checks like sampled system pricing times unit shipment proxies, channel feedback on typical deal sizes, and a light roll-up of supplier revenue exposure to IVD automation.

Key inputs used in the model include (illustrative) the mix of immunoassay, clinical chemistry, and molecular testing in routine diagnostics, the share of labs with high throughput needs, typical replacement and upgrade cycles for automation modules, average selling price movement by equipment class, and the pace of lab consolidation that pushes standardization. When data gaps exist (for example, smaller lab networks or private providers with limited disclosure), assumptions are filled using regional peer averages and then corrected through interview feedback.

For forecasting, we rely on scenario analysis supported by a simple multivariate regression on drivers that tend to move together with automation spend, such as diagnostic testing growth, lab labor cost pressure, and capital budget direction. Once the model outputs settle into a reasonable range across scenarios, the final forecast is selected based on what primary respondents describe as the most likely adoption path over the next five years.

Data Validation & Update Cycle

Validation is handled through several checks that compare the model outputs against independent signals, such as reported diagnostic instrument placements, lab capacity expansion announcements, and regional healthcare spending direction. If a region or equipment line shows an unusual jump, the drivers and pricing assumptions are rechecked, and follow-up outreach is triggered to confirm whether a one-time event or a real trend is being captured.

Before sign-off, the work goes through a multi step internal review, including arithmetic checks, logic reviews on assumptions, and a consistency scan across historical years. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, large lab network expansions, or meaningful pricing shifts. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Vitro Diagnostics Lab Automation Market for Market Sizing Compared With Other Published Estimates

Published market sizes for IVD lab automation often do not match because firms count different product sets, choose different base years, and convert currencies at different times. Even when the topic label looks the same, the inclusion of software, service contracts, or broader lab robotics can move the total by a noticeable amount.

Some external estimates fold in general lab automation used in research settings or add long term service and consumables as a bundled value. In Mordor Intelligence, the market is counted around IVD-focused automation equipment and workflow connectivity that is directly tied to diagnostic lab operations, with adjacent non-IVD research automation kept out to avoid overstating demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.49 B (2026) | |

| Industry Publisher A | USD 5.87 B (2024) | Uses an earlier base year and may not fully capture the recent post-pandemic automation refresh cycle, which can understate current demand in high throughput labs. The scope description is lighter on workflow connectivity and can treat integrated systems and modular automation differently, which shifts the total. |

| Global Publisher B | USD 5.60 B (2024) | Runs on a shorter forecast window and a more conservative spend progression that can compress the near-term value. The definition appears broader in geography detail but less explicit on what is excluded (for example, whether some research lab automation revenue is included), which can create a different starting point. |

The spread in published values is mainly explained by base-year choice and what gets counted as IVD-only automation versus adjacent lab automation categories. By keeping the scope tied to identifiable IVD workflow demand signals and then cross-checking totals with pricing and adoption feedback, our estimate stays transparent and easier to replicate year to year.

Key Questions Answered in the Report

What is the current value of the Lab Automation For In-Vitro Diagnostics market?

The segment is valued at USD 6.49 billion in 2026 and is projected to reach USD 8.77 billion by 2031.

Which equipment type holds the largest share?

Automated liquid handlers lead with 37.25% of 2025 revenue.

Which process segment is expanding the fastest?

Data management and connectivity is growing at a 6.86% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Government health-care investments and expanding hospital genomics labs push regional growth to a 6.66% CAGR.

How are AI algorithms influencing laboratory automation?

Embedded machine-learning models predict maintenance needs and fine-tune assay parameters, reducing downtime and reagent waste.

Page last updated on: