Thailand IT And Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.92 Billion |

| Market Size (2026) | USD 10.26 Billion |

| Market Size (2031) | USD 16.72 Billion |

| Growth Rate (2026 - 2031) | 10.26% CAGR |

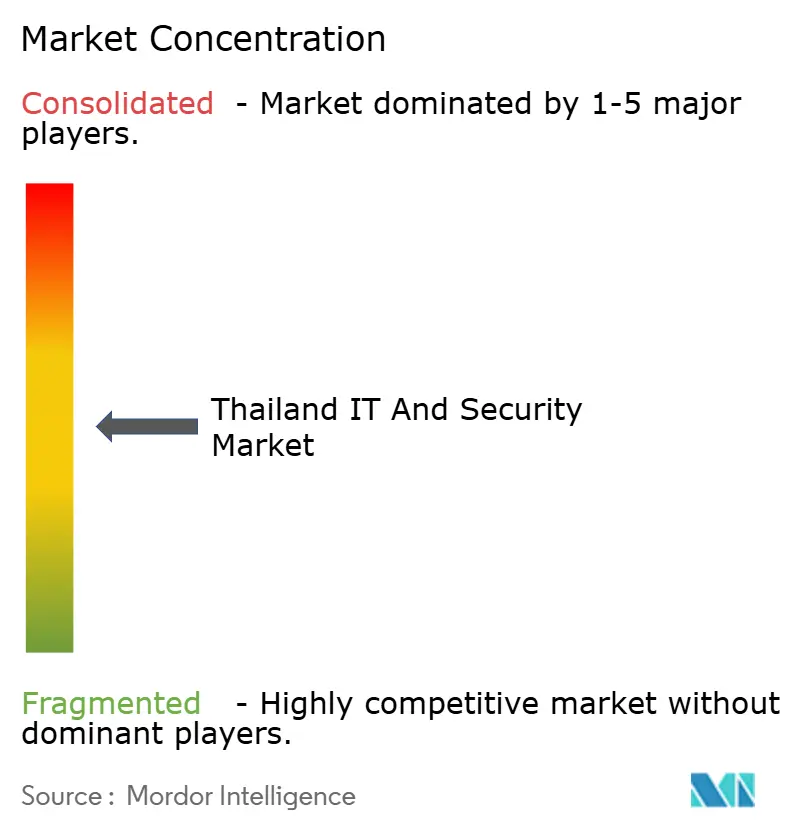

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand IT And Security Market Analysis by Mordor Intelligence

The Thailand IT and Security market size was valued at USD 9.92 billion in 2025 and is estimated to grow from USD 10.26 billion in 2026 to reach USD 16.72 billion by 2031, at a CAGR of 10.26% during the forecast period (2026-2031). Heightened cloud migration across 412 government entities, a USD 2.7 billion hyperscale data-center pipeline, and quantum-readiness mandates are pulling forward security investment and deepening the Thailand IT and Security market’s reliance on sovereign infrastructure. Converging 5G standalone coverage, which reached 92% of the population in 2025, is catalyzing edge-to-cloud architectures that demand micro-segmentation and zero-trust controls. Meanwhile, ISO-based compliance frameworks have moved from voluntary best practice to contractual prerequisite, aligning export-oriented manufacturers and digital retailers on the same security maturity path. Talent scarcity, semiconductor import dependence, and elongated procurement cycles in the provinces remain counterweights but have not derailed double-digit expansion of the Thailand IT and Security market.

Key Report Takeaways

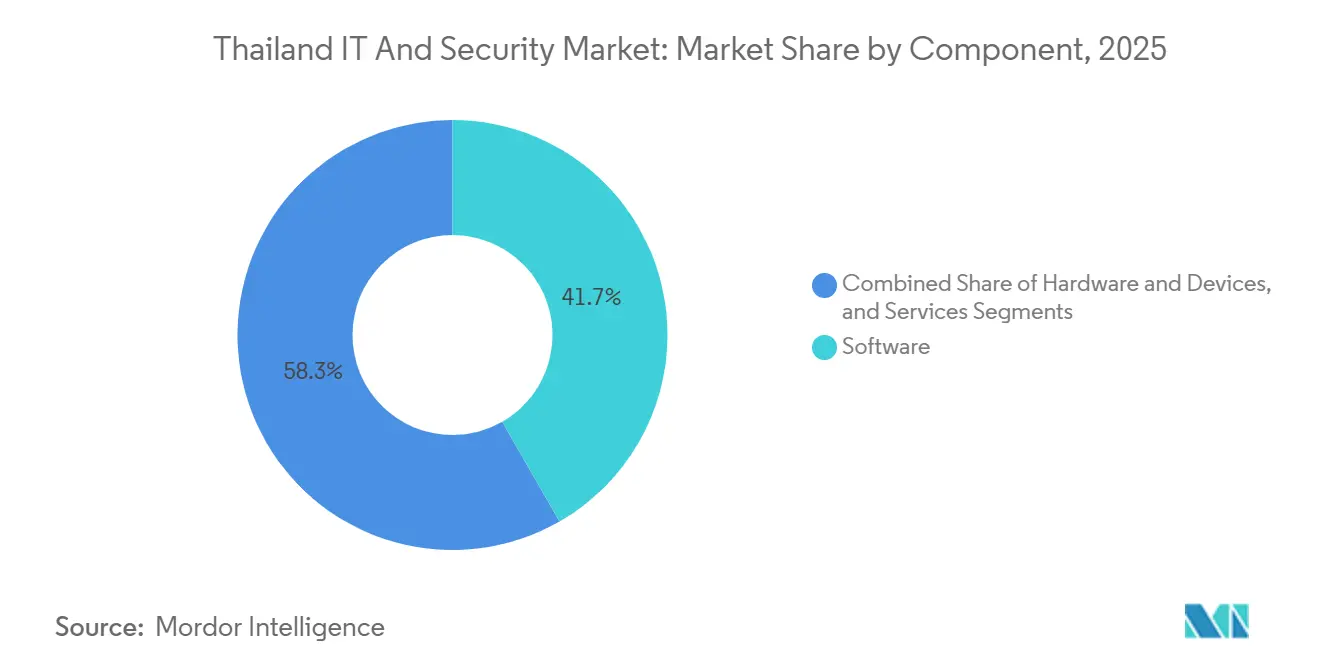

- By component, software led with 41.72% revenue share in 2025, while services are projected to expand at a 10.71% CAGR through 2031.

- By deployment mode, cloud captured 55.84% of 2025 spending, whereas hybrid architectures are forecast to advance at a 10.44% CAGR to 2031.

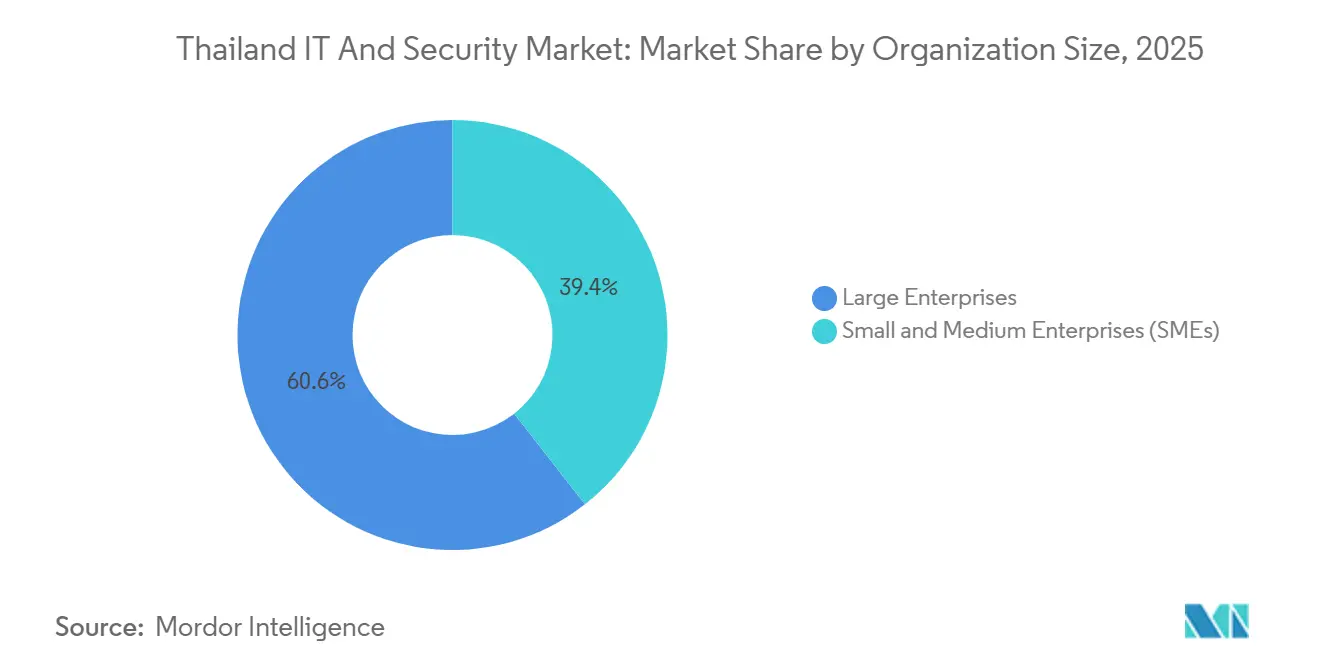

- By organization size, large enterprises commanded 60.57% of outlays in 2025; small and medium enterprises are set to grow at an 11.03% CAGR over 2026-2031.

- By end-user industry, banking, financial services, and insurance held 28.16% share in 2025, but healthcare is poised for the fastest 11.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand IT And Security Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first policy in Thai public sector | +1.8% | National, concentrated in Bangkok Metropolitan Administration and 76 provincial Digital Government Centers | Medium term (2-4 years) |

| Acceleration of 5G rollout enabling edge-to-cloud use-cases | +1.5% | National, with early 5G SA deployments in Eastern Economic Corridor (Chonburi, Rayong, Chachoengsao) | Short term (≤ 2 years) |

| E-commerce boom driving hyperscale data-center build-outs | +2.2% | National, with hyperscale facilities in Chonburi, Ayutthaya, and Bangkok suburbs | Medium term (2-4 years) |

| Board-level adoption of NIST CSF and ISO/IEC 27001 to meet export-market mandates | +1.3% | National, prioritized by automotive and electronics exporters in Eastern Economic Corridor and Samut Prakan | Long term (≥ 4 years) |

| Rise of Thailand PLUS near-shoring by Japanese and US manufacturers | +1.6% | National, with investment concentration in Eastern Economic Corridor and Northern provinces (Chiang Mai, Lamphun) | Medium term (2-4 years) |

| FinTech regulatory sandbox pushing open-API security spend | +1.2% | National, led by Bangkok-based banks and e-payment providers expanding to regional branches | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-First Policy in Thai Public Sector

The Digital Government Development Agency mandated that 70% of new public-sector workloads move to cloud infrastructure by 2027, compelling 412 agencies to migrate at least one mission-critical system before December 2026.[1]Digital Government Development Agency, “Policy Details,” DGA.OR.TH Contracts signed with National Telecom in 2025 already span 18 ministries and include ISO/IEC 27001-certified infrastructure, elevating spend on cloud security posture management and privileged access controls. Annual growth of 41% in public-sector purchases of these toolsets underscores how policy edicts translate into addressable demand. Yet nine-month tender cycles and coexistence with legacy on-premises assets require integrated monitoring across hybrid environments, increasing complexity and fueling uptake of managed security operations centers. The directive’s multi-factor authentication and five-year audit-log stipulations further lock in demand for identity-as-a-service and immutable storage.

Acceleration of 5G Rollout Enabling Edge-to-Cloud Use Cases

True Corporation and Advanced Info Service finished network consolidation in late 2024, resulting in a 5G standalone footprint that covered 92% of the population by mid-2025. Latency dropped below 10 milliseconds for industrial estates in Chonburi and Rayong, enabling machine-vision quality control, autonomous guided vehicles, and remote surgery pilots. These use cases require edge firewalls, micro-segmentation, and encrypted telemetry sync with cloud-based threat analytics, which together accounted for 62% of incremental edge-security budgets in 2025. Network slicing introduces fresh authentication challenges; only 19% of enterprises have deployed network-function-virtualization security, pointing to an untapped services opportunity. The 2G/3G shutdown completed in 2024 accelerated industrial controller upgrades, widening the Thailand IT and Security market as factories rushed to secure new radio gateways.

E-Commerce Boom Driving Hyperscale Data-Center Build-Outs

Thailand’s Board of Investment cleared USD 2.7 billion in data-center projects through 2025, with Google, Amazon Web Services, and Microsoft collectively adding 180 megawatts of capacity in Chonburi and Bangkok exurbs.[2]Board of Investment Thailand, “FDI Filings,” BOI.GO.TH E-commerce gross merchandise value reached THB 5.8 trillion (USD 165 billion) after growing 27.4% annually from 2022-2025, pressuring platforms such as Lazada and Shopee to meet sub-20-millisecond latency targets. Consequently, cloud-native web-application firewalls, API gateways, and distributed-denial-of-service mitigation claimed 34% of incremental security spend among the top-10 online retailers. Hyperscalers embed ISO/IEC 27017 and 27018 clauses into service-level agreements, easing compliance for merchants yet heightening dependency on imported cooling and power systems, 68% of which originate outside Thailand. Currency volatility remains a wild-card cost driver for physical security appliances within these sites.

Rise of Thailand PLUS Near-Shoring by Japanese and U.S. Manufacturers

The Thailand PLUS initiative attracted 127 foreign-direct-investment filings in 2025, including USD 890 million of Japanese-led expansions and a USD 300 million Foxconn electric-vehicle component plant. Automotive and electronics exporters now require ISO/IEC 62443 controls that converge operational-technology and information-technology defenses, spurring orders for industrial firewalls, security information and event management, and zero-trust segmentation. Foxconn’s Chachoengsao operations center monitors 1,200 endpoints and 47 SCADA nodes, illustrating the cyber-physical scale of demand. Nonetheless, only 14% of Thai engineers possess operational-technology security certification, forcing manufacturers to partner with local integrators and foreign specialists, a dynamic that expands the services revenue pool within the Thailand IT and Security market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented SME IT budget cycles | -1.4% | National, most acute in provincial SMEs outside Bangkok Metropolitan Region | Short term (≤ 2 years) |

| Shortage of 30,000 cyber-security professionals | -1.8% | National, with talent concentration in Bangkok and Chiang Mai | Long term (≥ 4 years) |

| Legacy MPLS contracts delaying cloud migration | -1.1% | National, affecting enterprises with multi-site operations and long-term telecom agreements | Medium term (2-4 years) |

| High dependence on imported semiconductors amid Baht volatility | -1.0% | National, impacting hardware procurement across all sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of 30,000 Cyber-Security Professionals

The National Cyber Security Agency calculated a 30,000-person talent gap through 2027, while Thailand’s CISSP cohort rose only from 385 to 431 between 2024 and 2025. Median security-operations-center analyst pay in Bangkok jumped 18% to THB 65,000 (USD 1,850) per month, pushing small and medium enterprises toward managed services they often struggle to manage and assess. Outsourcing grew 22% in 2025, but reliance on third-party incident response dilutes institutional knowledge and extends containment times. Limited specialist availability slows adoption of zero-trust network access-implemented by just 11% of organizations as of end-2025-and drags on uptake of security orchestration, automation, and response. Government scholarship programs and vendor-run academies are scaling, yet the lag in advanced certifications will continue to temper the Thailand IT and Security market’s growth trajectory.

Fragmented SME IT Budget Cycles

Small and medium enterprises make up 99.5% of Thailand’s 3.2 million registered firms, yet half lack formal credit lines, forcing 6- to 9-month procurement cycles that delay endpoint detection and response deployments.[3]Asia Foundation, “SME Finance Gaps,” ASIAFOUNDATION.ORG Multiple loan approvals and annual budget ratifications create stop-start purchasing that vendors struggle to forecast. Less than 20% of provincial merchants have adopted security-as-a-service bundles promoted by FinTech sandbox rules, despite rising ransomware threats. External contractors rotate every 12-18 months at most of these firms, resetting security baselines and prolonging exposure. The Office of Small and Medium Enterprises Promotion’s THB 500 million grant program covered 50% of security software costs in 2025, but uptake was constrained by application complexity and limited awareness, reinforcing the bifurcation between heavily secured large enterprises and vulnerable small and medium enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge on Compliance Advisory Demand

Services generated the fastest momentum, poised to rise at 10.71% CAGR to 2031 as enterprises outsource vulnerability assessments, penetration tests, and managed detection and response to local specialists. The Thailand IT and Security market size for professional services reached THB 2.1 billion (USD 60 million) in 2025 following the National Cyber Security Agency’s quarterly audit mandate. In contrast, software maintained the largest slice at 41.72% thanks to subscription-based endpoint protection and cloud-security posture management platforms that match operating-expense budgets. Hardware spent softened amid 14-week firewall lead times and Baht depreciation that inflated imported appliance costs.

Growth in services also mirrors regulatory intricacy. Government tenders require ISO/IEC 27001 certification, pushing agencies to engage third-party auditors and policy architects they lack in-house. Managed detection and response, especially for cloud workloads, expanded 28% in 2025 as small and medium enterprises lacking security-operations centers sought pay-as-they-grow contracts. This dynamic reinforces a structural shift in the Thailand IT and Security market toward expertise-driven offerings over pure technology resale.

By Deployment Mode: Hybrid Gains as Enterprises Balance Legacy and Cloud

Hybrid environments are projected to grow at a 10.44% CAGR, even though cloud held 55.84% of 2025 spending. Banks such as Kasikornbank moved fraud-detection models to Google Cloud while retaining customer databases on-premises, illustrating why secure tunneling, identity federation, and unified logging are indispensable. The Thailand IT and Security market share for cloud workload protection platforms widened as agencies under the Cloud First Policy adopted multicloud strategies that still tether to existing data centers.

Nevertheless, on-premises estates persist in defense, utilities, and healthcare, where sovereignty and latency push workloads to private clusters. Hybrid complexity has 62% of enterprises reporting policy-consistency challenges, fuelling demand for cloud-security posture management that spans Kubernetes clusters and hardware-based firewalls. Identity-as-a-service platforms compliant with the National Cyber Security Agency’s January 2025 standards are bridging these silos, underscoring how hybrid is not a transitional but a durable operating model within the Thailand IT and Security market.

By Organization Size: SMEs Accelerate on Sandbox Mandates

Large enterprises generated 60.57% of 2025 revenue, yet small and medium enterprises are projected to grow at an 11.03% CAGR through 2031. Open-API security rules for 47 licensed e-payment providers have cascaded to millions of merchants, pushing them toward cloud-based secure web gateways and zero-trust services they can activate in minutes. Cloudflare’s Thai customer count for zero-trust network access passed 1,200 in 2025, evidencing traction despite budget restraint.

Managed security bundles priced at THB 15,000 (USD 430) per month are lowering entry barriers, although many provincial firms still lack dedicated IT staff. The Office of Small and Medium Enterprises Promotion subsidy helped cover 50% of software fees, lifting the Thailand IT and Security market size for SME security subscriptions. Moving forward, stricter contractual clauses in supply-chain finance and export documentation are expected to lock security compliance into everyday business operations, shifting demand from discretionary to mandatory.

By End-User Industry: Healthcare Leads Growth on Telemedicine Mandates

Banking, financial services, and insurance retained the top spot with 28.16% of 2025 revenue after the Bank of Thailand tightened recovery-time objectives for critical systems. However, healthcare will post the swiftest 11.32% CAGR, propelled by the Ministry of Public Health’s order that 1,200 telemedicine platforms earn ISO/IEC 27001 certification by December 2026. Ransomware strikes on hospitals jumped 34% in 2025, accelerating network segmentation and off-site backup deployments.

Manufacturing security outlays grew 19% as Industry 4.0 adoption melded operational-technology and enterprise networks, generating new vectors that Foxconn’s Chachoengsao plant illustrated by integrating anomaly detection across 1,200 programmable logic controllers. Government and defense remained 18% of demand, with website firewall mandates across 412 agencies. Retail and e-commerce budgets surged 31% in response to USD 137 million in payment-fraud losses, while energy utilities spent USD 34 million safeguarding 2,400 SCADA endpoints under critical-infrastructure regulations. Each vertical’s regulatory driver cements a multi-lane growth path for the Thailand IT and Security market.

Geography Analysis

Bangkok Metropolitan Region continued to dominate spending, accounting for nearly 62% of the Thailand IT and Security market in 2025 owing to the concentration of headquarters, data centers, and government ministries. Cloud-connectivity density, coupled with a talent pool of 431 CISSP holders, fosters rapid adoption of AI-enabled security analytics. However, soaring office rents are nudging hyperscalers to establish availability zones in peripheral provinces such as Chonburi and Ayutthaya, redistributing capital expenditure while keeping support ecosystems centered in Bangkok.

The Eastern Economic Corridor, covering Chonburi, Rayong, and Chachoengsao, represented 18% of 2025 spending but showed the strongest regional growth outlook at a projected CAGR of 12.1%. Automotive and electronics exporters installing 5G private networks and industrial firewalls are prime contributors. Foxconn’s facility and 31 machine-vision deployments across WHA Industrial estates underscore how manufacturing security requirements integrate deeply into regional planning.

Northern provinces, led by Chiang Mai and Lamphun, are emerging talent hubs as universities collaborate with the National Cyber Academy. Although they held just 6% share in 2025, lower salary costs and government incentives are drawing managed-service providers to locate follow-the-sun security-operations shifts there. Over the forecast horizon, provincial digital-government centers and SME grants are expected to lift the Thailand IT and Security market size outside the capital, smoothing the geographic dispersion of security capability.

Competitive Landscape

Competition remains moderately fragmented. The top five vendors, Microsoft, Cisco, Fortinet, Palo Alto Networks, and Trend Micro, captured a considerable share in 2025, leaving headroom for regional integrators. Microsoft’s USD 2.85 billion pledge includes an AI-powered security-operations center built with True Internet Data Center, signalling an arms race to provide sovereign-AI capabilities that satisfy data-residency rules. Google Cloud’s Cybershield program embedded threat-intelligence feeds into 18 sectoral computer-emergency-response teams, fortifying its position within public-sector defense architectures..

Local specialists such as G-Able, MFEC, and SIAMDATA leverage Thai-language support and deep knowledge of Personal Data Protection Act nuances to edge out multinationals in compliance engagements. Elastic’s open-source security information and event management deployment across government agencies demonstrated price-performance disruption that challenges proprietary licensing models. Industrial security is another battleground: Fortinet and Palo Alto Networks tailor ruggedized firewalls for automotive production lines, while Cisco integrates OT-specific anomaly detection into its SecureX platform.

Artificial-intelligence differentiation is intensifying. Kasikornbank’s in-house fraud-detection engine cut false positives by 41% in 2025, illustrating how domain data empowers banks to outclass generic models. Vendors are responding with API-level integrations that allow clients to blend proprietary telemetry with pretrained algorithms. Barriers to entry continue to rise as ISO/IEC 27001 certification and local data-center presence become table stakes, effectively excluding vendors unwilling to invest in Thai approvals.

Thailand IT And Security Industry Leaders

Dell Technologies Inc.

Cisco Systems, Inc.

Advanced Info Service Public Co. Ltd. (AIS)

Microsoft Corporation

True Digital Group Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: G42 finalized a deal with True Internet Data Center to build a 30-megawatt sovereign-AI facility in Chonburi, aligning with cloud-first and critical-infrastructure mandates while keeping sensitive workloads inside national borders.

- October 2025: Microsoft announced a USD 2.85 billion expansion that includes an AI-driven cloud security operations center and Azure zones in Chonburi, plus training for 100,000 professionals on cloud security over five years.

- April 2025: Google Cloud launched Cybershield with the National Cyber Security Agency, integrating Web Risk API into 18 sectoral response teams and training 1,000 practitioners on Chronicle SIEM usage.

- March 2025: Advanced Info Service became Oracle Cloud Infrastructure’s distributor, bundling Cloud Guard security services for customers in banking, telecom, and manufacturing.

Thailand IT And Security Market Report Scope

As hacking incidents increase, the need to protect an organization's digital assets and network devices also increases. IT security is a set of cybersecurity strategies that prevent unauthorized access to organizational assets such as computers, networks, and data.

The Thailand IT and Security Market Report is Segmented by Component (Hardware and Devices, Software, and Services), Deployment Mode (On-premises, Cloud, and Hybrid), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, Government and Defense, Manufacturing, Healthcare, Retail and E-commerce, Energy and Utilities, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware and Devices |

| Software |

| Services |

| On-premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Defense |

| Manufacturing |

| Healthcare |

| Retail and E-commerce |

| Energy and Utilities |

| Other End-User Industries |

| By Component | Hardware and Devices |

| Software | |

| Services | |

| By Deployment Mode | On-premises |

| Cloud | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-user Industry | BFSI |

| Government and Defense | |

| Manufacturing | |

| Healthcare | |

| Retail and E-commerce | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

How fast is spending on cybersecurity services growing in Thailand?

Services revenue in the Thailand IT and Security market is projected to rise at a 10.71% CAGR between 2026-2031, fueled by compliance audits and managed detection and response.

Which sector will see the quickest adoption of advanced security controls?

Healthcare is forecast to post the fastest 11.32% CAGR through 2031 as telemedicine platforms must secure electronic health records under ISO/IEC 27001 mandates.

What drives hybrid deployment demand among Thai enterprises?

Banks and manufacturers must integrate legacy on-premises systems with multicloud workloads, so hybrid architectures are growing at a 10.44% CAGR and require unified security monitoring

Why is the talent shortage a pressing issue for Thai firms?

The National Cyber Security Agency identified a 30,000-person gap, pushing wage inflation and forcing many small and medium enterprises to outsource security operations, which can extend incident-response times.

How are hyperscalers influencing Thailand’s security landscape?

Investments from Microsoft, Google, and Amazon Web Services exceed USD 10 billion and bundle ISO-certified services, embedding hyperscalers into national cyber-defense architecture and accelerating cloud security adoption.

Page last updated on: