Market Overview

| Study Period | 2021 - 2031 |

|---|---|

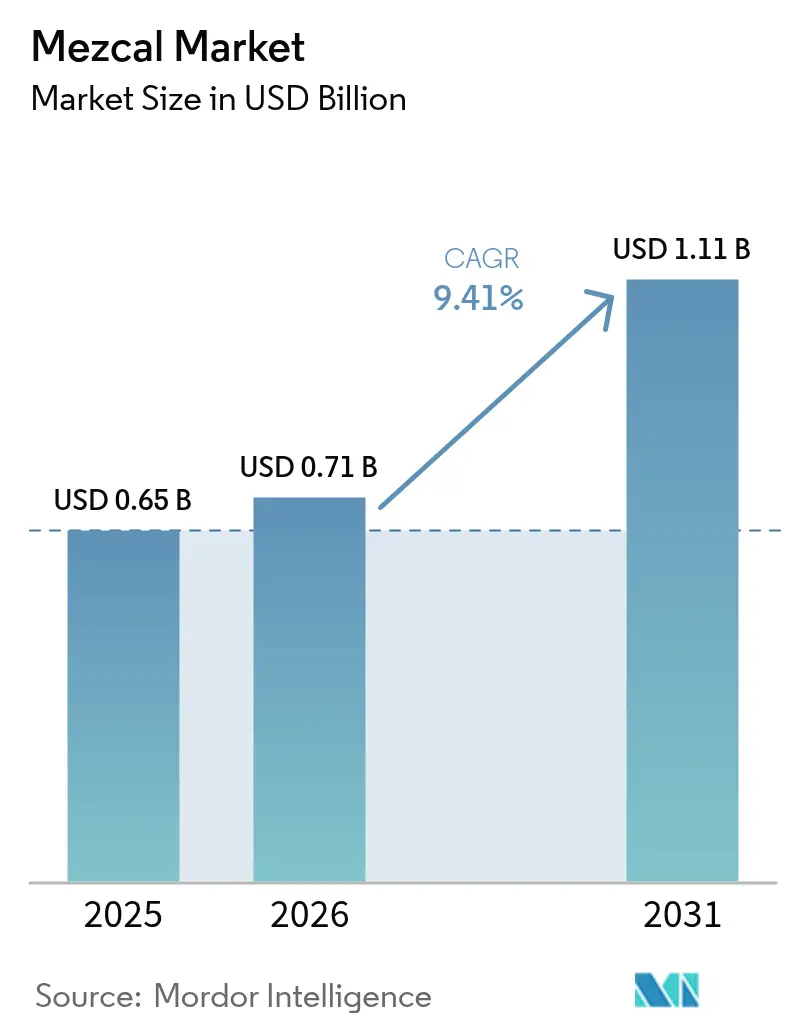

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.11 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

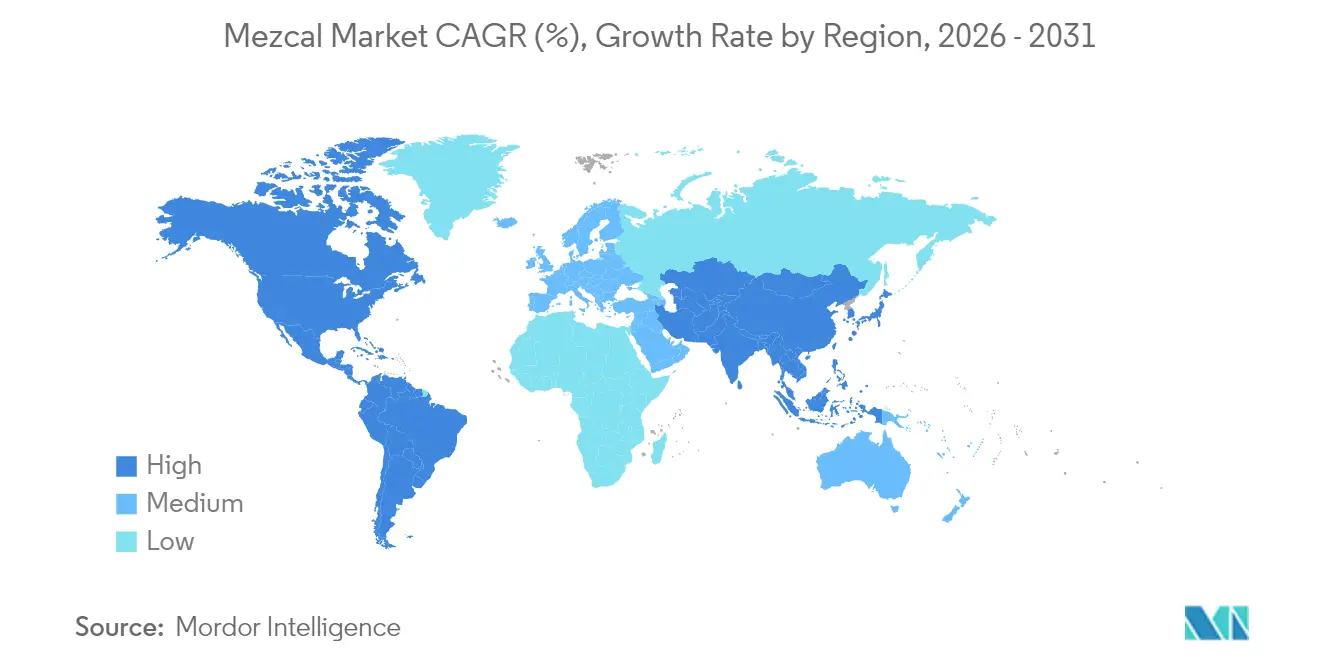

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mezcal Market Analysis by Mordor Intelligence

Mezcal market size in 2026 is estimated at USD 0.71 billion, growing from 2025 value of USD 0.65 billion with 2031 projections showing USD 1.11 billion, growing at 9.41% CAGR over 2026-2031. As consumers increasingly gravitate towards provenance-rich beverages, multinational distillers are making strategic acquisitions, infusing fresh capital into traditional communities and underscoring a strong commercial confidence. While North America currently leads in volume, Asia Pacific's rapid double-digit growth positions it as the emerging powerhouse, marking mezcal's evolution from a regional specialty to a global luxury staple. The Consejo Regulador del Mezcal (CRM) certification not only safeguards mezcal's authenticity but also curbs swift industrial growth, bolstering its premium status. Concurrently, there's a push towards sustainable agave farming and biodiversity initiatives, aiming to stabilize raw material supplies in the face of potential constraints.

Key Report Takeaways

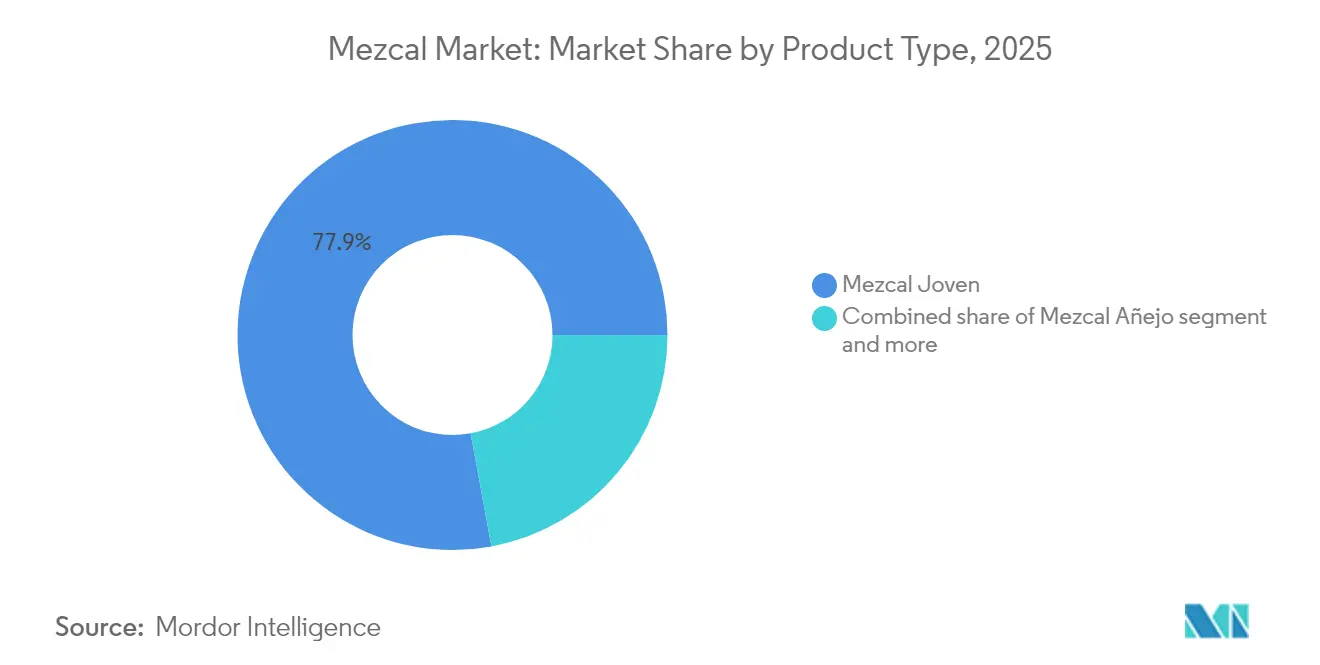

- By product type, Mezcal Joven commanded 77.90% of 2025 revenue, whereas Mezcal Añejo is projected to expand at a 12.62% CAGR through 2031.

- By production method, Ancestral expressions led with a 93.44% mezcal market share in 2025, while Artisanal mezcal is rising at an 11.10% CAGR.

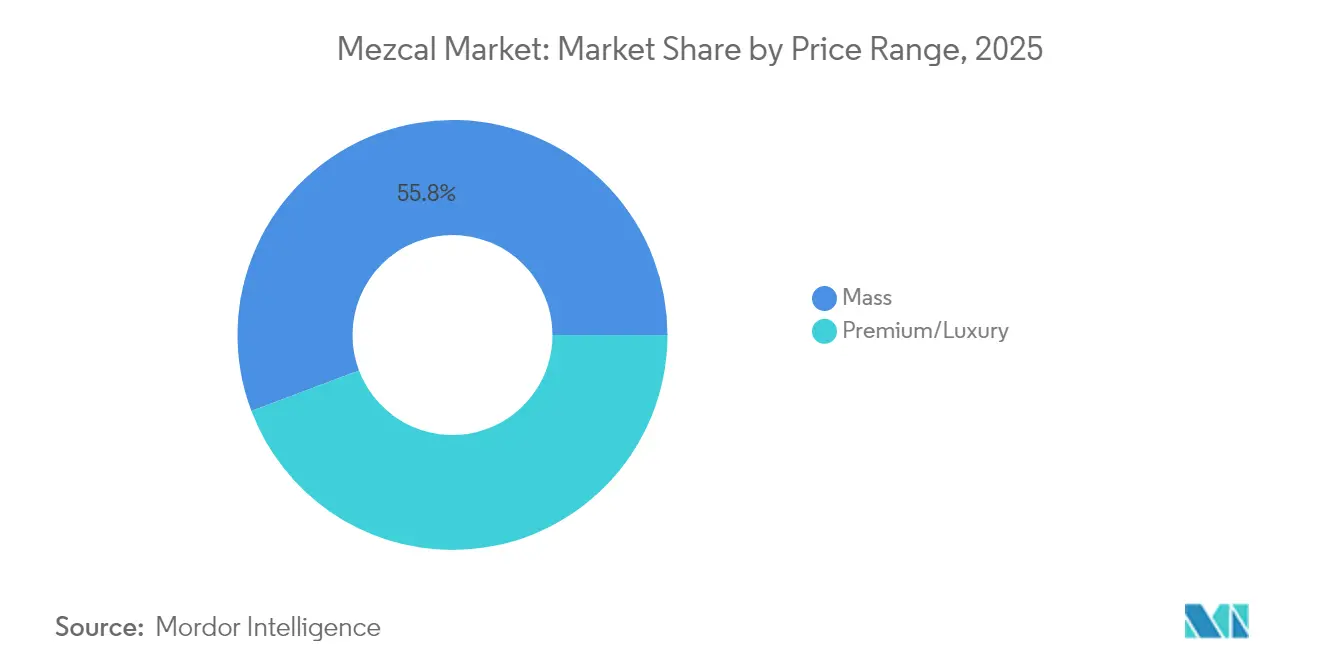

- By price range, the mass segment accounted for 55.76% of 2025 sales, while premium offerings are growing at a 11.45% CAGR.

- By distribution channel, on-trade venues captured 68.38% of the 2025 value; off-trade is outpacing at a 10.44% CAGR.

- By geography, North America dominated with a 57.64% share in 2025, while the Asia Pacific is forecast to record a 12.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mezcal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and artisanal appeal | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Innovation in ready-to-drink (RTD) mezcal cocktails | +1.8% | North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| Influence of Mexican cuisine | +1.5% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Diversification of flavor profiles | +1.3% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Strategic investments boosting brand awareness | +1.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Sustainability and biodiversity certification premiums | +1.0% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization and artisanal appeal

As consumers increasingly prioritize quality over quantity, the mezcal category's premiumization trajectory aligns with broader trends in the spirits industry. Premium mezcal segments, expanding at an 11.64% CAGR, are significantly outpacing mass market growth. This surge is fueled by discerning consumers who seek authentic, craft-produced spirits with compelling provenance stories. Tesla's foray into the mezcal market, debuting a limited-edition bottle priced at USD 450, underscores the potential of luxury positioning to command hefty price premiums, all while upholding artisanal production methods[1]Source: Tesla, “Tesla Mezcal Launch,” teslamezcal.tesla.com. The allure of artisanal production isn't just a marketing ploy; it's evident in the tangible production nuances. Techniques like traditional tahona milling and wild yeast fermentation yield distinct flavor profiles, justifying the premium pricing. Further bolstering this trend, the San Francisco World Spirits Competition's 2025 nod to diverse regional expressions underscores the value of terroir-driven differentiation as a lasting competitive edge.

Innovation in ready-to-drink (RTD) mezcal cocktails

Mezcal's growth is being driven by innovations in the ready-to-drink (RTD) segment, which capitalizes on the spirit's distinctive smoky profile, setting it apart from vodka and gin alternatives. As the RTD spirits segment surges, mezcal brands find new avenues to connect with consumers, especially those who might be daunted by neat spirits, all while familiarizing them with mezcal's unique flavor. Diageo's heightened emphasis on RTDs, underscored by its investments in Crown Royal RTD and Ketel One Botanical, underscores the corporate world's acknowledgment of RTDs as pivotal for the premium spirits market[2]Source: Diageo plc, “Annual Report 2022,” diageo.com. Innovations in this space aren't limited to basic cocktails; they also encompass novel cask finishes. A prime example is Ilegal's Caribbean Cask Finish Reposado, which melds rum barrel nuances with traditional mezcal aging. Such product innovations empower brands to command premium prices and broaden the contexts in which mezcal is enjoyed, moving beyond just sipping.

Influence of Mexican cuisine

As Mexican cuisine gains global popularity, mezcal consumption in restaurants and bars worldwide sees a natural boost. With a commanding 68.93% market share, the on-trade channel underscores mezcal's robust presence in food service. Here, savvy bartenders and sommeliers play a pivotal role, guiding consumers on serving techniques and ideal food pairings. This connection to cultural authenticity resonates deeply, especially as diners seek experiences that transcend mere meals to include traditional beverages. Regional Mexican restaurants are now spotlighting mezcal, offering flights and tastings that turn curious diners into passionate enthusiasts. This influence isn't confined to dining; retail channels also feel the impact. Placing mezcal alongside Mexican food products and highlighting it during cultural festivities like Día de Muertos significantly boosts sales.

Diversification of flavor profiles

Mezcal's flavor diversity, stemming from over 30 agave species and diverse production methods, caters to a wide range of consumer tastes. This inherent segmentation enables brands to hone in on specific consumer groups while staying true to the category's authenticity. This stands in contrast to other spirits that often lean on artificial flavoring for distinction. Forward-thinking producers are venturing into unconventional ingredients. A prime example is Paquera's Wagyu-infused ancestral mezcal, highlighting the adaptability of traditional methods to premium additions. Brands are also diversifying by exploring various agave types. Chinga Quedito, for instance, is spotlighting rare Sierra Negra expressions, not only fetching collector premiums but also enlightening consumers on biodiversity preservation. Such strategies foster a unique differentiation that's challenging for industrial producers to mimic, solidifying mezcal's artisanal identity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited agave supply and long cultivation cycles | -1.9% | Global, most acute in Mexico production regions | Long term (≥ 4 years) |

| Stringent regulatory environment | -1.2% | Global, with varying intensity by import market | Medium term (2-4 years) |

| Prevalence of counterfeit and low-quality products | -0.8% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Economic and geopolitical uncertainties | -1.4% | Global, with concentration in key export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited agave supply and long cultivation cycles

Agave cultivation, with maturation periods spanning 7 to 30 years based on the species, faces inherent supply constraints that hinder the scalability of mezcal production. Overharvesting of wild agave has surged to critical levels in regions known for traditional production. This has compelled producers to increasingly depend on cultivated varieties, which often lack the nuanced complexity of their wild counterparts. Climate change further exacerbates these supply challenges in agave-growing regions, introducing water stress and temperature fluctuations that hinder plant development and sugar content. Traditional producers grapple with tough decisions: uphold the authenticity of wild agave sourcing or meet the rising demand with a consistent supply. This mismatch between cultivation cycles and market growth leads to price volatility, posing a threat to smaller producers who may not have the financial cushion to endure supply shortages.

Stringent regulatory environment

Mexico's Consejo Regulador del Mezcal (CRM) enforces denomination of origin regulations that both protect authenticity and create market access barriers, potentially stunting category growth. These regulations mandate specific production methods, geographic origins, and agave varieties, hindering the industrial scaling techniques seen in other spirit categories. International trade adds another layer of complexity, with diverse import requirements, labeling standards, and taxation policies across markets, placing a compliance burden on smaller producers. The tequila industry's recent enforcement of additive disclosure rules hints at possible similar restrictions for mezcal, potentially impacting product formulations and marketing claims. Furthermore, proposed U.S. tariffs of up to 25% on Mexican goods threaten export-dependent mezcal producers, especially smaller brands that heavily depend on access to the U.S. market, according to Drinks International[3]Source: Drinks International, “What Tariffs Could Mean for Mezcal,” drinksint.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Joven Dominance Amid Añejo Innovation

In 2025, Mezcal Joven captures a commanding 77.90% of the market share, underscoring a clear consumer preference for unaged expressions. These unaged variants not only highlight the pure essence of agave but also celebrate traditional production methods. The segment's widespread appeal can be attributed to its accessibility for newcomers and its lower production costs, especially when juxtaposed with aged counterparts. This makes Mezcal Joven the primary driver for the category's expansion. Yet, it's Mezcal Añejo that's witnessing the most rapid ascent, boasting a 12.62% CAGR through 2031. This surge is fueled by trends leaning towards premiumization and innovative aging techniques, helping products stand out in saturated markets. A case in point is Clase Azul's San Luis Potosí release, which underscores the power of premium positioning and artisanal packaging, allowing aged expressions to fetch retail prices as high as USD 370.

Mezcal Reposado finds its niche in the middle, striking a balance by offering a touch of aging complexity without the prolonged production times that Añejo expressions demand. Meanwhile, specialty types like Abocado and Pechuga cater to niche markets, where traditional methods yield distinct flavor profiles, justifying their premium pricing. This segmentation not only highlights mezcal's adaptability to varied consumer tastes but also its commitment to authenticity through age-old production techniques. Innovations in the aged category, such as Ilegal's Caribbean Cask Finish, further illustrate how producers can carve out a unique identity while staying true to the category's essence.

By Production Method: Ancestral Traditions Drive Premium Value

In 2025, Ancestral Mezcal, with its authentic pit-oven cooking and clay pot distillation techniques, commands a dominant 93.44% share of the mezcal market. This stronghold underscores consumers' readiness to pay a premium for artisanal products, especially those that honor age-old techniques and uplift traditional communities. Meanwhile, Artisanal Mezcal, despite its smaller slice of the market, is on an upward trajectory, boasting an impressive 11.10% CAGR. This growth is attributed to producers who, while embracing modern quality controls, remain steadfast in their traditional flavor development methods. Such segmentation in production methods not only establishes distinct value hierarchies but also empowers brands to justify their pricing based on authenticity and labor intensity.

Industrial Mezcal caters to the price-sensitive segment of the market. However, it grapples with authenticity issues, curtailing its chances for premium positioning. Regulatory bodies enforce a production method classification system, ensuring transparency and shielding traditional producers from industrial competitors misusing mezcal designations. Recent advancements, like real-time fermentation tracking systems, are revolutionizing production monitoring. These innovations empower artisanal producers to uphold quality consistency without straying from their traditional methods. By emphasizing ancestral techniques, these producers carve out sustainable competitive advantages, making it challenging for large-scale industrial players to encroach on mezcal's premium market standing.

By Price Range: Mass Market Foundation Supports Premium Growth

In 2025, the mass market segment commands a dominant 55.76% share, laying a robust foundation for category infrastructure and enticing consumer trials. Meanwhile, premium segments are outpacing the rest, boasting an impressive 11.45% CAGR. This surge underscores effective brand elevation strategies, positioning mezcal alongside esteemed spirits like single malt whisky and aged rum. This two-pronged approach caters to both the everyday consumer and the aspirational buyer, all while upholding authentic production standards across varied price points. The allure of premium positioning is heightened by limited production runs and compelling artisanal narratives, fostering a sense of scarcity and piquing collector interest

Price segmentation empowers producers to tap into diverse consumer motivations, whether it's casual sipping, gift-giving, or marking special occasions. A case in point: Tesla's USD 450 limited edition, showcasing how luxury branding can command hefty premiums without compromising on artisanal authenticity. The upward trajectory of the premium segment hints at effective consumer education, cultivating a deeper appreciation for the nuances of production and the significance of terroir. While mass market accessibility is vital for broadening the category's reach, it also serves as a gateway for consumers, many of whom may eventually gravitate towards premium offerings as their palate matures and knowledge deepens.

By Distribution Channel: On-Trade Education Drives Off-Trade Growth

In 2025, on-trade venues account for 68.38% of mezcal sales, underscoring the category's dependence on skilled bartenders and servers. These professionals play a pivotal role in educating consumers about serving techniques and flavor nuances. This dominance of on-trade venues not only highlights the importance of experiential marketing but also emphasizes the potential for consumer education, fostering loyalty that transcends individual brand preferences. Meanwhile, off-trade channels are witnessing a robust expansion at a 10.44% CAGR. This growth is largely attributed to premium retail positioning and the rise of direct-to-consumer platforms, effectively bringing mezcal to consumers' doorsteps. Such dynamics underscore mezcal's journey, transitioning from a niche bar specialty to a prominent retail offering.

Within the off-trade landscape, specialty liquor stores stand out. They offer curated selections and employ knowledgeable staff, mirroring the educational benefits typically found in on-trade settings. The surge of e-commerce is evident, with platforms like Drizly boasting a staggering 600% year-over-year increase in mezcal sales. This highlights the platform's prowess in catering to premium spirit enthusiasts who prioritize convenience and variety. As distribution channels evolve, producers face the challenge of tailoring marketing strategies and educational content for each avenue, all while ensuring a unified brand message. While on-trade venues play a pivotal role in establishing brand awareness and encouraging consumer trials, the burgeoning off-trade segment offers avenues for volume growth and enhanced profit margins.

Geography Analysis

In 2025, North America commands a dominant 57.64% share of the mezcal market, underscoring its status as the leading export destination for the spirit. In 2023, the U.S. alone imported about 7 million liters out of the 7.8 million liters of mezcal exported worldwide, according to Drinks International. North America's advantages include its geographical closeness to Mexico, well-established distribution channels for premium spirits, and a discerning consumer base that values artisanal production. Yet, the region faces challenges: proposed U.S. tariffs, potentially reaching 25% on Mexican imports, threaten this growth trajectory, especially for smaller producers reliant on U.S. access. Meanwhile, Canada is emerging as a promising market, showing heightened interest in premium spirits and facing fewer regulatory hurdles than some global counterparts. While North America's mature spirits landscape offers a platform for premium branding, it simultaneously intensifies competition for both shelf space and consumer loyalty.

Asia Pacific is on track to be the fastest-growing region, boasting a projected CAGR of 12.18% through 2031. A burgeoning middle class and a growing demand for premium international spirits drive this surge. China's burgeoning cocktail scene and penchant for luxury items naturally bolster the demand for premium mezcal. Simultaneously, Australia's well-established spirits market serves as a gateway for artisanal brands. The region's growth is underscored by its increasing visibility at global spirits competitions and rising import volumes. However, challenges loom: regulatory intricacies and a cultural unfamiliarity with agave spirits can hinder market entry. Japan's refined spirits culture and its admiration for artisanal methods hint at a promising avenue for premium mezcal. Yet, breaking into this market demands hefty investments in consumer education and brand establishment, given the general lack of awareness about mezcal's production and consumption nuances among Asian consumers.

Europe, while mature, presents a fragmented landscape with diverse consumer tastes and regulatory frameworks. The continent's fondness for artisanal spirits and products with protected designations of origin bodes well for authentic mezcal. Leading the charge in consumption are Germany, the U.K., and France, all of which boast established premium spirits markets and a burgeoning cocktail culture. The successful defense of tequila's denomination rights by the Consejo Regulador del Tequila in European trademark disputes underscores the critical nature of intellectual property protection for Mexican spirits on the global stage. Meanwhile, South America, the Middle East, and Africa, though currently under-penetrated, hold promise for future growth as global spirits distribution networks broaden and consumer sophistication matures.

Competitive Landscape

In the mezcal market, fragmented competition presents opportunities for both multinational spirits giants and artisanal producers to carve out their niches through distinct positioning strategies. Major players like Diageo, Pernod Ricard, and Campari Group have made strategic acquisitions, infusing the market with robust distribution networks and marketing prowess, all while striving to uphold the artisanal essence that underscores the category's authenticity. Drawing from their deep-rooted experience in the tequila market and expertise in premium spirits, these corporations aim to elevate mezcal brands on a global scale. However, they grapple with the challenge of upholding traditional production methods amidst rising volume demands.

Brands that adeptly navigate the tightrope between authenticity and accessibility are reaping the rewards. A case in point is Del Maguey, which has managed to retain its market leadership even as celebrity-backed competitors like Dos Hombres have surged. New entrants are shaking up the landscape, emphasizing sustainability, pioneering packaging solutions, and adopting direct-to-consumer models that sidestep the conventional three-tier distribution system. While technology's footprint in the industry is still modest, it's on the rise. Some producers are harnessing fermentation monitoring systems and solar-powered distillation techniques, aiming for consistent quality without compromising their artisanal roots.

Untapped potential lies in flavored variants, ready-to-drink (RTD) applications, and regions where mezcal has yet to make significant inroads. The Consejo Regulador del Mezcal (CRM) oversees the regulatory landscape, safeguarding authentic producers while posing challenges for newcomers eyeing mezcal designations. As more multinational entities awaken to mezcal's burgeoning potential and the ongoing trend of consumer premiumization fuels category growth, the intensity of competition is poised to escalate.

Mezcal Industry Leaders

Pernod Ricard

Diageo PLC

Campari Group

William Grant & Sons Ltd

Bacardi Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Ilegal Mezcal launched Reposado Caribbean Cask Finish, introducing rum barrel influences to traditional mezcal aging processes. The innovation demonstrates how producers can create differentiation while maintaining category authenticity through creative aging techniques.

- August 2024: Paquera Mezcal introduced limited-edition Wagyu-infused ancestral mezcal, suspending Montana Wagyu beef in clay pots during distillation to create unique flavor profiles. The product exemplifies premium positioning strategies that command collector pricing through innovative ingredient integration.

- February 2024: Clase Azul México announced its third mezcal offering, Clase Azul Mezcal San Luis Potosí, featuring green agave from high-altitude growing regions and artisanal packaging priced at USD 370 retail. The launch demonstrates geographic expansion within Mexico's mezcal production zones.

- January 2024: Tesla launched a limited-edition mezcal at a USD 450 retail price, featuring hand-blown glass bottles inspired by Oaxacan pottery and traditional production methods. The celebrity brand entry signals mainstream recognition of mezcal's luxury positioning potential.

Global Mezcal Market Report Scope

Mezcal is a distilled alcoholic beverage made from different types of agave. The global mezcal market has been segmented by product type, distribution channel, and geography. By product type, the market is segmented as mezcal joven, mezcal reposado, mezcal anejo, and other product types of mezcal. By distribution channel, the market is segmented into on-trade channel and off-trade channel, that is further segmented into online and offline retail channels. The study also analyzes the mezcal market in emerging and established markets across the globe, including North America, Europe, and the Rest of the World. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Mezcal Joven |

| Mezcal Reposado |

| Mezcal Añejo |

| Other Types (Abocado, Pechuga) |

By Production Method

| Artisanal Mezca |

| Industrial Mezcal |

| Ancestral Mezcal |

By Price Range

| Mass |

| Premium/Luxury |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Mezcal Joven | |

| Mezcal Reposado | ||

| Mezcal Añejo | ||

| Other Types (Abocado, Pechuga) | ||

| By Production Method | Artisanal Mezca | |

| Industrial Mezcal | ||

| Ancestral Mezcal | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the mezcal market?

The mezcal market size is USD 0.71 billion in 2026 and is projected to reach USD 1.11 billion by 2031.

Which region shows the fastest growth for mezcal?

Asia Pacific leads with a forecast 12.18% CAGR due to rising cocktail culture and premium-spirits demand

How does limited agave supply affect producers?

Long cultivation cycles of 7-30 years constrain output, drive raw-material price volatility, and pressure smaller palenques

What channel sells most mezcal today?

On-trade venues, especially bars and restaurants, account for 68.38% of sales because bartenders educate consumers at the point of consumption.

What is driving premium-priced mezcal growth?

Consumer willingness to pay for provenance, limited editions, and sustainability credentials pushes premium segments to an 11.45% CAGR.

Page last updated on: