Supercapacitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

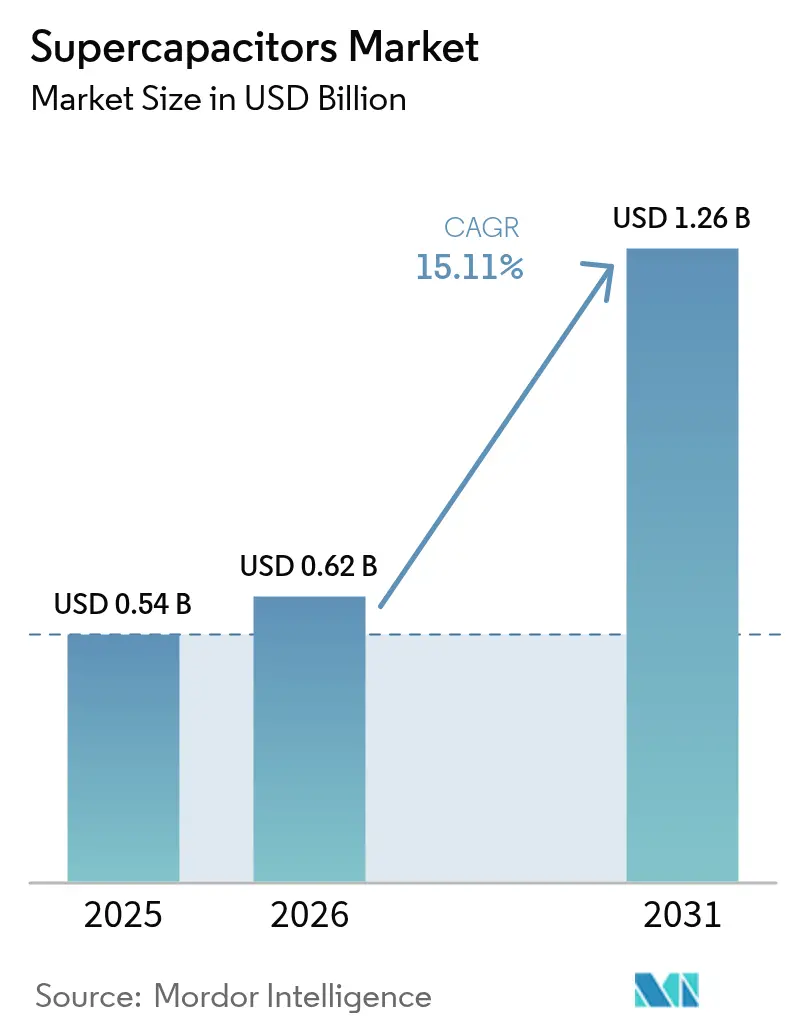

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 15.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

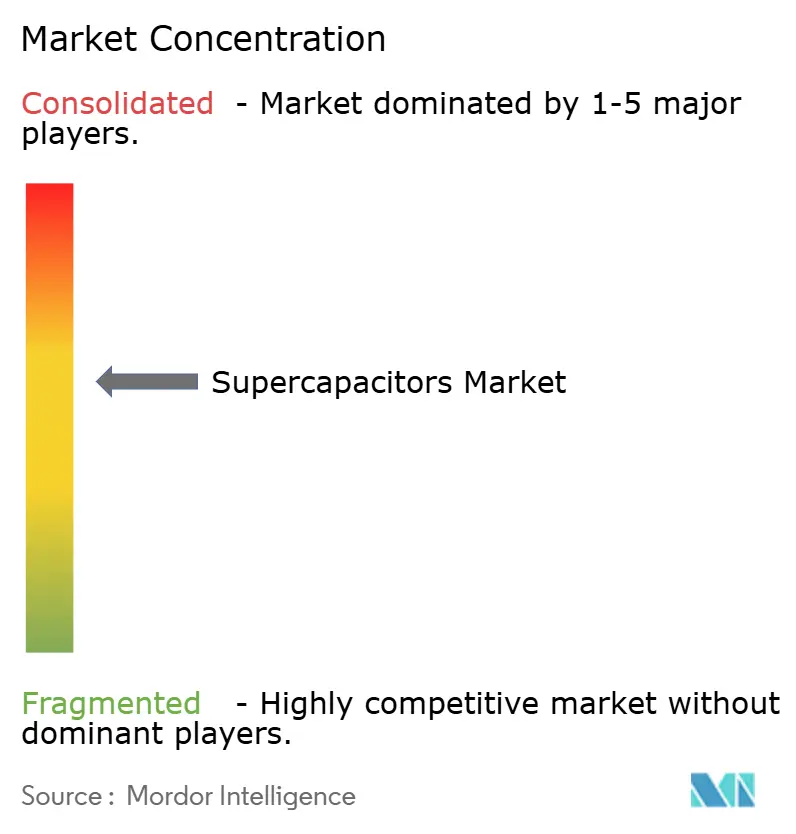

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supercapacitors Market Analysis by Mordor Intelligence

The supercapacitors market size is expected to grow from USD 0.54 billion in 2025 to USD 0.62 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 15.11% CAGR over 2026-2031. Growth is supported by electrification rules such as the European Union’s 48-volt mild-hybrid mandate, datacenter demand for uninterruptible power during artificial-intelligence (AI) surges, and grid-modernization projects that blend batteries with supercapacitors for rapid frequency response. [1]Dina Genkina, “Will Supercapacitors Come to AI’s Rescue?” IEEE Spectrum, spectrum.ieee.org China continues to anchor production and research, while Korean manufacturers pivot toward energy-storage systems as their lithium-ion share slips. Product innovation centres on hybrid designs that lift energy density toward battery-like levels and graphene electrodes that enable ultra-thin wearables. Supply-chain risks around activated-carbon prices and ionic-liquid electrolytes temper near-term margins but also encourage regional diversification.

Key Report Takeaways

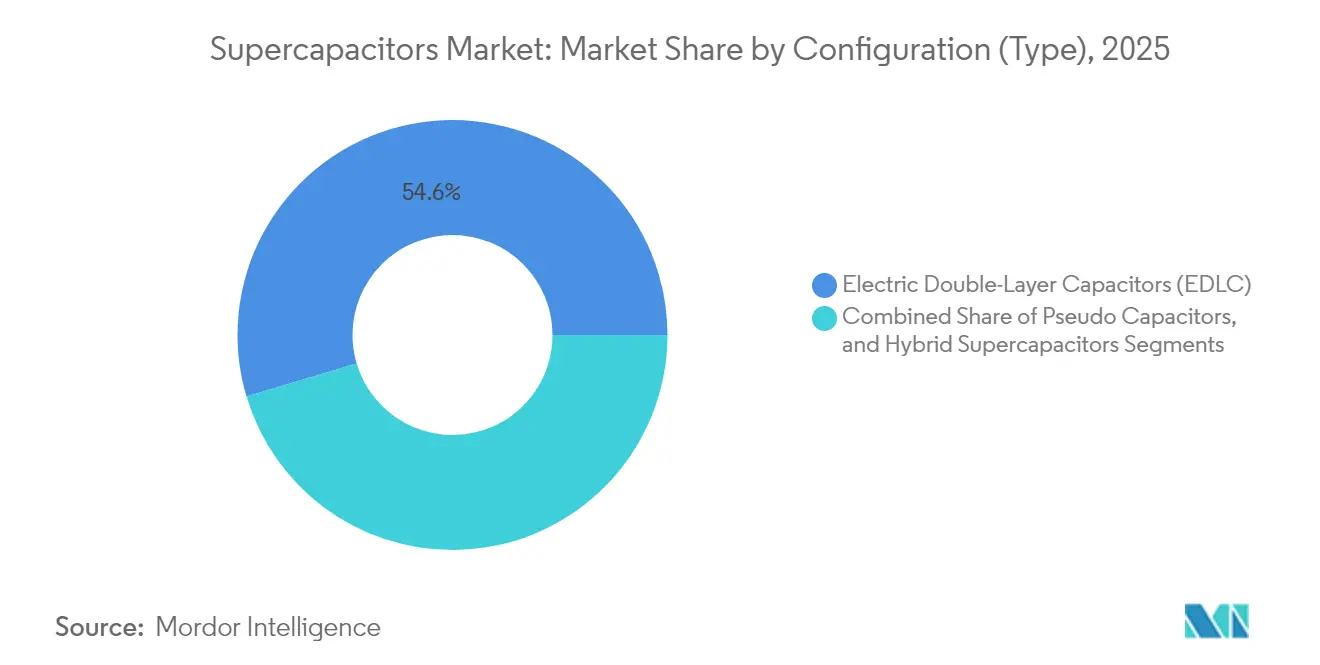

- By configuration, Electric Double-Layer Capacitors led with 54.62% of the supercapacitors market share in 2025, while Hybrid Supercapacitors are projected to expand at an 17.62% CAGR through 2031.

- By form factor, modules commanded 57.12% share of the supercapacitors market in 2025, and packs are forecast to grow at 16.95% CAGR to 2031.

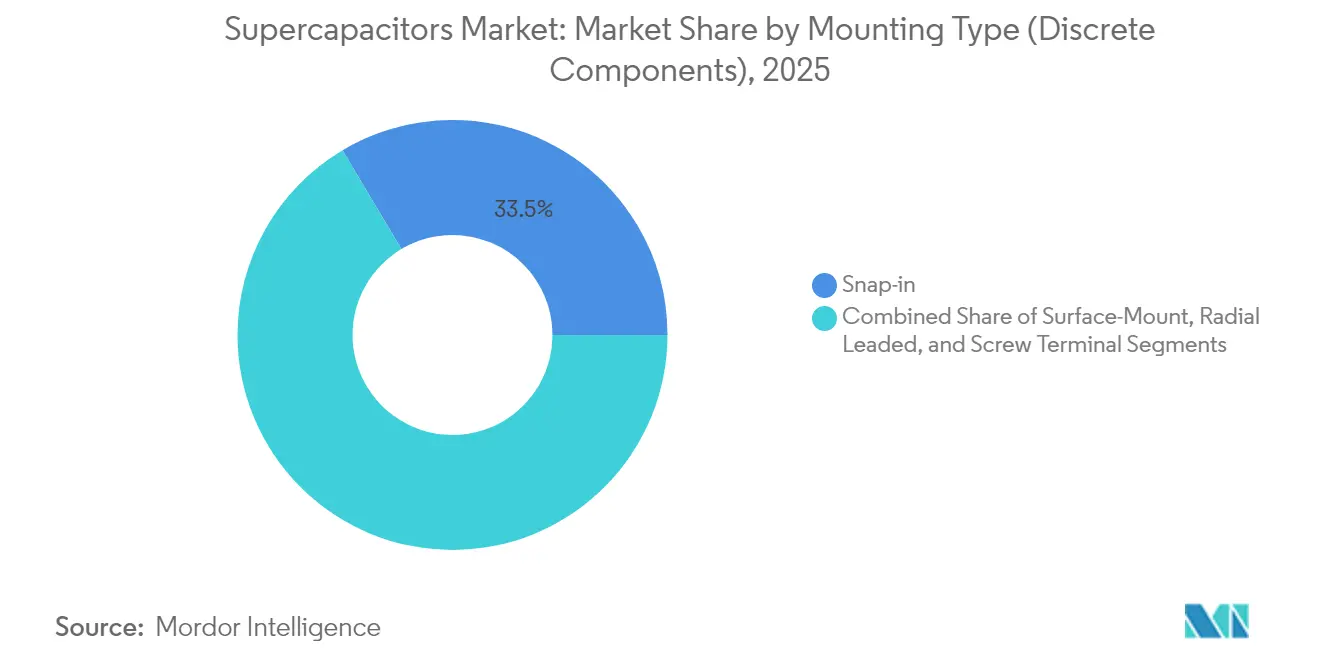

- By mounting type, snap-in devices held 33.54% revenue share in 2025, whereas surface-mount units are advancing at 21.45% CAGR through 2031.

- By end-user industry, automotive and transportation accounted for 37.95% of the supercapacitors market in 2025, and data-center applications are set to rise at 20.76% CAGR to 2031.

- By geography, China led with 27.88% share of the supercapacitors market in 2025, while Korea and Rest of Asia are expected to post a 15.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supercapacitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets | +3.20% | Global, early gains in China & Europe | Medium term (2-4 years) |

| Grid-scale battery-supercapacitor hybrid storage | +4.10% | North America & EU, APAC core | Long term (≥ 4 years) |

| Graphene-based electrode breakthroughs enabling ultra-thin wearables | +2.80% | Global | Long term (≥ 4 years) |

| EU 48 V mild-hybrid mandate accelerating demand for 12–48 V modules | +3.50% | Europe, North America follow-on | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

Urban transit agencies are scaling regenerative-braking systems that pair batteries with supercapacitors, recovering up to 85% more kinetic energy than battery-only setups. Mercedes-Benz’s Intouro hybrid bus cut fuel use by 5% using a 48-volt supercapacitor pack that endures millions of charge cycles without degradation. Chinese cities were first movers and now link hybrid depots to the grid for both vehicle charging and grid-stability services. System suppliers integrate algorithms that shift power between supercapacitors and batteries to match route topography, which lowers total cost of ownership. As electric-bus procurements rise, this capability strengthens the competitive position in mass-transit electrification.

Grid-scale battery-supercapacitor hybrid storage

Utilities value supercapacitors for instant frequency regulation. Demonstrations showed a 17.43% reduction in frequency-drop rates versus standalone lithium-ion arrays, delivering economic benefits 3.2-times greater than battery-only solutions. The U.S. Department of Energy projects levelized storage costs of USD 0.337 per kWh by 2030 as automated cell production scales. Operators also cite environmental advantages because supercapacitors avoid cobalt and nickel. These factors position the supercapacitors market as an essential grid-forming resource that complements long-duration batteries under high-renewable penetration scenarios.

Graphene-based electrode breakthroughs enabling ultra-thin wearables

Research teams delivered energy densities near 75 J/cm³ using oriented two-dimensional nanomaterials in polymer matrices, the highest reported for polymer dielectrics. Plasma-treated carbon nanowalls doubled areal capacitance, offering manufacturable pathways to high-performance electrodes. Analysts now see graphene supercapacitors displacing electrolytic capacitors in vehicle inverters within the next two years. Wearable device brands prize the combination of millisecond-level charging and flexible form factors. These breakthroughs expand the addressable applications for the supercapacitors market beyond power buffering into true energy-storage roles in consumer electronics.

EU 48 V mild-hybrid mandate accelerating demand for 12–48 V modules

Euro 7 emissions rules published in May 2024 effectively require 48-volt architectures that rely on belt-starter or integrated-starter generators. Automotive suppliers estimate 10–20 kW of power assist plus robust energy recuperation, tasks where supercapacitors outperform batteries on cycle life. [2]Onsemi, “48-Volt Systems for Mild Hybrid Electric Vehicles and Beyond,” onsemi.com Tier-one firms are redesigning electrical platforms and locking multi-year volume contracts for supercapacitor modules. Similar regulatory pathways in North America suggest global replication, reinforcing a structural tailwind through mid-decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Activated-carbon precursor price volatility inflating BOM costs | -2.1% | Global manufacturing hubs | Short term (≤ 2 years) |

| Certification gaps (IEC 62391) limiting residential adoption | -1.8% | Global, harmonization needed | Medium term (2-4 years) |

| Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration | -2.7% | Global automotive | Long term (≥ 4 years) |

| Ionic-liquid electrolyte supply-chain bottlenecks | -1.9% | Global, concentration risks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Certification gaps (IEC 62391) limiting residential adoption

IEC 62391 testing procedures prolong qualification timelines and raise costs, especially for smaller firms. Comparative studies show the standard takes longer than Maxwell and QC/T 741-2014 protocols, stretching product launches by up to 12 months. The heavy focus on high-current testing is mismatched with typical household power profiles. This administrative hurdle slows the supercapacitors market from penetrating residential energy-storage segments where simplified compliance would unlock new demand.

Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

Commercial supercapacitors still cluster near 10 Wh/kg, far below lithium-ion cells at 250 Wh/kg, limiting their role to power-assist rather than primary propulsion. Although laboratory work on carbon nano-onion cores is promising, scalable manufacturing remains elusive. Automakers therefore adopt hybrid architectures that pair batteries with supercapacitors instead of full substitution. Until a material breakthrough reaches volume production, This plateau caps the addressable revenue in long-range electric vehicles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Configuration: Hybrid designs gain momentum

Electric Double-Layer Capacitors maintained a 54.62% share of the supercapacitors market in 2025, reflecting established production lines and proven durability in industrial power buffering. Hybrid Supercapacitors are on track for an 17.62% CAGR to 2031 as they merge battery-like energy storage with classic capacitor power delivery. The hybrid approach answers OEM calls for devices that can ride through seconds-long voltage dips and also sustain longer discharge profiles.

Rapid R&D advances, including lithium-ion capacitor variants, narrow the energy-density gap and extend operating temperatures. Pilot projects in automotive inverters and grid-forming systems showcase cycle lifetimes beyond one million cycles. These traits position hybrids as the next performance benchmark within the supercapacitors industry.

By Form Factor: Packs scale for utility projects

Module assemblies captured 57.12% of the supercapacitors market in 2025 thanks to integrated balancing circuitry and drop-in compatibility for buses, cranes, and wind turbines. Pack configurations, however, are projected to grow 16.95% annually as grid operators and EV makers opt for higher-voltage stacks that exceed 800 V. The market size for pack-level products could double by 2031 as utilities deploy them for sub-second frequency response.

Cell products retain relevance in wearables and industrial controllers where board-level integration and cost sensitivity remain critical. Vendors now offer modular architectures that let customers scale energy in 50-volt increments, shortening project design cycles. Advanced thermal-management features further widen adoption across harsh-duty environments.

By Mounting Type (Discrete Components): Surface-mount rises with miniaturization

Snap-in terminals delivered 33.54% revenue in 2025, favoured by automotive and industrial clients who prize mechanical robustness. Surface-mount devices are set for a 21.45% CAGR on the back of consumer electronics miniaturization. Compact footprints allow designers to place supercapacitors directly beside processors, trimming parasitic inductance.

High-frequency prototypes operating at 44 kHz underline opportunities in switch-mode power supplies. Radial-leaded and screw-terminal units maintain niche positions for high-current rail applications. The diverse mounting landscape illustrates tailored engineering that strengthens the supercapacitors market against single-use disruption.

By End-User Industry: Datacenters emerge as high-growth niche

Automotive and transportation applications held 37.95% of the supercapacitors market in 2025, anchored by 48-V mild-hybrid systems and regenerative braking modules. Datacenters and telecom are poised for 20.76% CAGR till 2031 as AI workloads drive power-quality needs beyond lead-acid capabilities.

Consumer electronics adopt supercapacitors for ultra-fast charging wearables, while utilities integrate them into battery-hybrid storage fields for inertial support. Industrial robotics and defence sectors value long cycle life in extreme temperatures. These multi-sector uses reinforce the broad opportunity envelope sustaining growth.

Geography Analysis

China controlled 27.88% of global revenue in 2025 due to scale in activated-carbon processing and a deep research base that publishes 65.4% of high-impact papers. Domestic demand from electric-vehicle makers and state-backed grid projects underpins volume growth. State policies that prioritise local energy-storage content further entrench supply-chain ecosystems for the supercapacitors market.

Korea and the broader Asia region are set for a 15.96% CAGR through 2031, propelled by LG Energy Solution, Samsung SDI, and SK On investments that exceed USD 20 billion in new capacity. Korean firms channel expertise in electrode coatings toward pack-level storage systems aimed at North American utilities. Japan contributes precision manufacturing for high-reliability automotive modules, while Southeast Asian nations attract assembly plants seeking diversified supply bases.

The United States leverages Inflation Reduction Act incentives to localise production and deploy supercapacitor-based UPS units in hyperscale datacenters. Europe remains regulation-driven, with the Euro 7 framework spurring automotive demand and grid-modernization funds supporting hybrid storage pilot plants. Emerging regions in Latin America and the Middle East trial supercapacitor packs for microgrid stability, signalling long-term addressable growth.

Competitive Landscape

The supercapacitors market exhibits moderate concentration. Maxwell Technologies (Tesla), Skeleton Technologies, and Eaton command core patents and automated factories that lower per-cell costs. Skeleton earmarked EUR 600 million for a French SuperBattery hub that fuses capacitor and battery chemistries, illustrating a pivot toward integrated storage portfolios.

Intellectual-property stakes remain contentious; Tesla’s 2025 lawsuit against CAP-XX over Maxwell patents underscores legal barriers to entry. Component shortages in ionic-liquid electrolytes and price spikes in coconut-shell-derived activated carbon pressure gross margins, yet also incentivise regional sourcing to improve resilience.

New entrants carve niches in graphene-electrode wearables and high-frequency power electronics. Partnerships, such as Flex with Musashi Energy for AI datacenter storage, mirror a broader trend of joint ventures that bundle system integration expertise with novel cell chemistries. Collectively, these dynamics shape a competitive but opportunity-rich environment for the supercapacitors industry.

Supercapacitors Industry Leaders

Maxwell Technologies Inc. (Tesla Inc.)

Eaton Corporation plc

Skeleton Technologies SA

CAP-XX Ltd.

Kyocera Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tesla sued CAP-XX in Texas federal court alleging infringement of Maxwell Technologies’ patents.

- January 2025: Panasonic launched its “Panasonic Go” initiative at CES 2025, highlighting circular-economy partnerships for battery and supercapacitor production.

- November 2024: Skeleton opened an R&D unit at LUT University in Finland ahead of a planned Leipzig Superfactory capable of 4 million cells annually.

- August 2024: Flex and Musashi Energy Solutions partnered to commercialise hybrid supercapacitor systems for AI datacenters, with production slated for 2025.

Global Supercapacitors Market Report Scope

Supercapacitors (or ultracapacitors) utilize high surface area electrode materials and thin electrolytic dielectrics to achieve high capacitance values. They have more capacitance than conventional capacitors and store more energy. Supercapacitors can be of various types, such as double-layer, pseudo, and hybrid capacitors. They can be used for different end-user industries, such as consumer electronics, energy and utilities, industrial, and automotive.

The Supercapacitors Market is segmented by end-user (consumer electronics, energy, and utilities (grid applications, wind, and others), industrial (automotive/transportation (bus and truck, rail and tram, 48 V mild hybrid car, micro hybrids, and other cars, heavy vehicle), and geography (United States, Europe, China, Japan, Korea and rest of Asia, and rest of the world). The market sizes and forecasts are provided in value (USD) for all the above segments.

| Electric Double-Layer Capacitors (EDLC) |

| Pseudocapacitors |

| Hybrid Supercapacitors |

| Cell |

| Module |

| Pack |

| Surface-Mount |

| Radial Leaded |

| Snap-in |

| Screw Terminal |

| Consumer Electronics | Wearables | |

| Smartphones and Tablets | ||

| SSD and Memory Backup | ||

| Energy and Utilities | Grid Frequency Regulation | |

| Renewable Integration (Wind, Solar) | ||

| Microgrid and UPS | ||

| Industrial Equipment | Robotics and Automation | |

| Power Tools | ||

| Heavy Machinery and Cranes | ||

| Automotive and Transportation | Passenger Cars | 48 V Mild Hybrid |

| Start-Stop Micro Hybrid | ||

| Commercial Vehicles | Buses | |

| Trucks | ||

| Rail and Tram | ||

| Aviation and Aerospace | ||

| Data Centers and Telecom | ||

| Defense and Space | ||

| Others (Medical Devices, Agri-drones) | ||

| United States |

| Europe |

| China |

| Japan |

| Korea and Rest of Asia-Pacific |

| Rest of the World |

| By Configuration (Type) | Electric Double-Layer Capacitors (EDLC) | ||

| Pseudocapacitors | |||

| Hybrid Supercapacitors | |||

| By Form Factor | Cell | ||

| Module | |||

| Pack | |||

| By Mounting Type (Discrete Components) | Surface-Mount | ||

| Radial Leaded | |||

| Snap-in | |||

| Screw Terminal | |||

| By End-User Industry | Consumer Electronics | Wearables | |

| Smartphones and Tablets | |||

| SSD and Memory Backup | |||

| Energy and Utilities | Grid Frequency Regulation | ||

| Renewable Integration (Wind, Solar) | |||

| Microgrid and UPS | |||

| Industrial Equipment | Robotics and Automation | ||

| Power Tools | |||

| Heavy Machinery and Cranes | |||

| Automotive and Transportation | Passenger Cars | 48 V Mild Hybrid | |

| Start-Stop Micro Hybrid | |||

| Commercial Vehicles | Buses | ||

| Trucks | |||

| Rail and Tram | |||

| Aviation and Aerospace | |||

| Data Centers and Telecom | |||

| Defense and Space | |||

| Others (Medical Devices, Agri-drones) | |||

| By Geography | United States | ||

| Europe | |||

| China | |||

| Japan | |||

| Korea and Rest of Asia-Pacific | |||

| Rest of the World | |||

Key Questions Answered in the Report

What is the current value of the supercapacitors market?

The supercapacitors market is valued at USD 0.62 billion in 2026 and is projected to reach USD 1.26 billion by 2031.

Which configuration leads the supercapacitors market?

Electric Double-Layer Capacitors hold 54.62% of market revenue, but hybrid designs are growing fastest at 17.62% CAGR.

Why are datacenters adopting supercapacitors?

AI workloads create power spikes that supercapacitors handle better than batteries, enabling reliable uninterruptible power while meeting sustainability goals.

How does the EU 48 V mandate affect demand?

Euro 7 rules effectively require 48-volt mild-hybrid systems, driving substantial uptake of 12–48 V supercapacitor modules in European vehicles.

What limits supercapacitors in long-range electric vehicles?

Commercial energy density remains near 10 Wh/kg, far below lithium-ion levels, restricting supercapacitors to power-assist rather than primary propulsion.

Which region is growing fastest in the supercapacitors market?

Korea and the broader Asia region are set for a 15.96% CAGR through 2031 due to strategic investments by leading battery manufacturers.

Page last updated on: