Silicon Carbide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

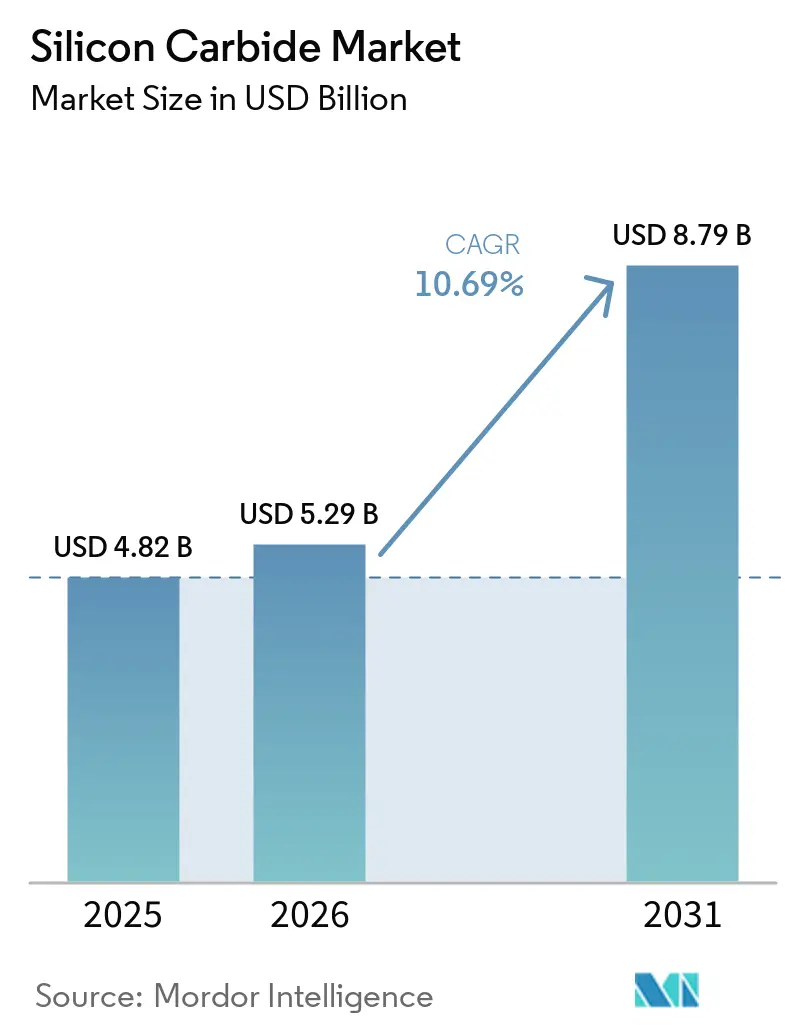

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 8.79 Billion |

| Growth Rate (2026 - 2031) | 10.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicon Carbide Market Analysis by Mordor Intelligence

The Silicon Carbide Market size is projected to expand from USD 4.82 billion in 2025 and USD 5.29 billion in 2026 to USD 8.79 billion by 2031, registering a CAGR of 10.69% between 2026 to 2031. Demand is accelerating on two parallel tracks: power-semiconductor substrates for traction inverters, datacenter power supplies, and renewable-energy converters, and industrial ceramics for blast furnaces, high-temperature heat exchangers, and ballistic armor. Device makers are shifting to 8-inch wafers, a geometry that cuts per-die cost by 1.8 times and secures design wins in 800-volt electric-vehicle platforms. Black silicon carbide retained dominance in 2025 but premium-priced green grade is outpacing overall growth as wafer-polishing and precision-lapping volumes climb. Government subsidies in Asia-Pacific, North America, and Europe are compressing fab payback periods, intensifying capacity additions while raw-material volatility and environmental compliance costs favor vertically integrated suppliers.

Key Report Takeaways

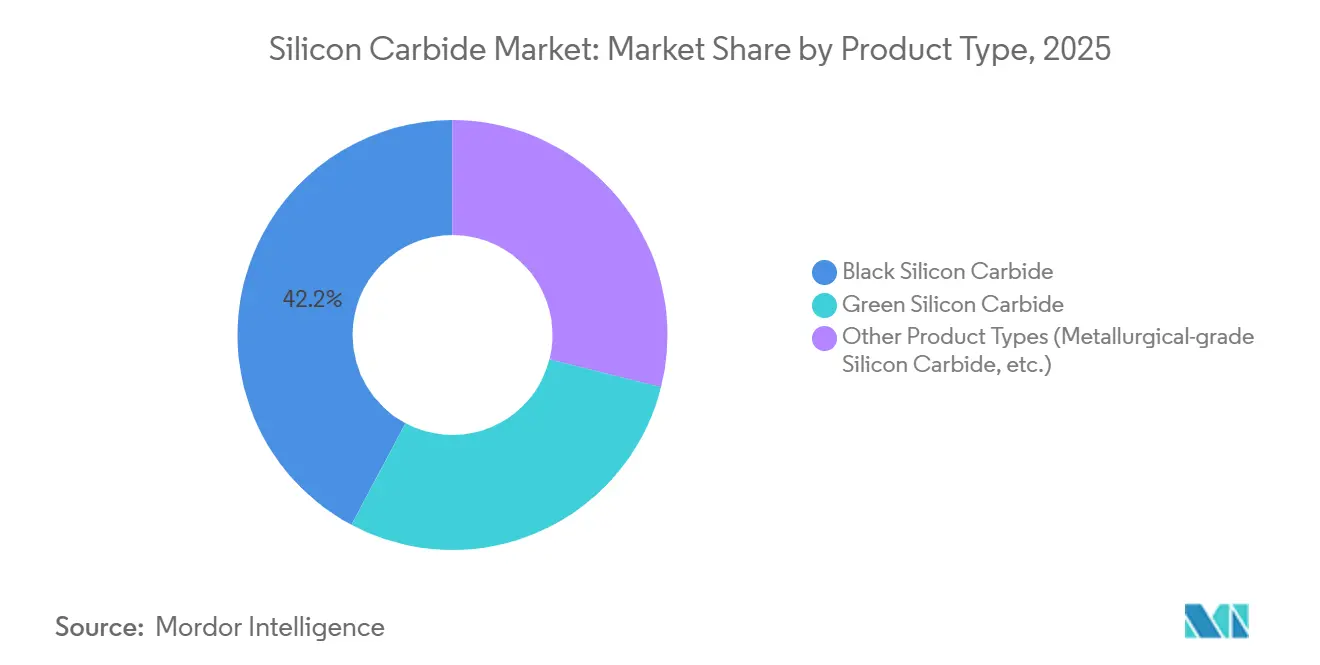

- By product type, black silicon carbide captured 42.22% of the silicon carbide market share in 2025, whereas green silicon carbide is projected to post a 13.56% CAGR through 2031.

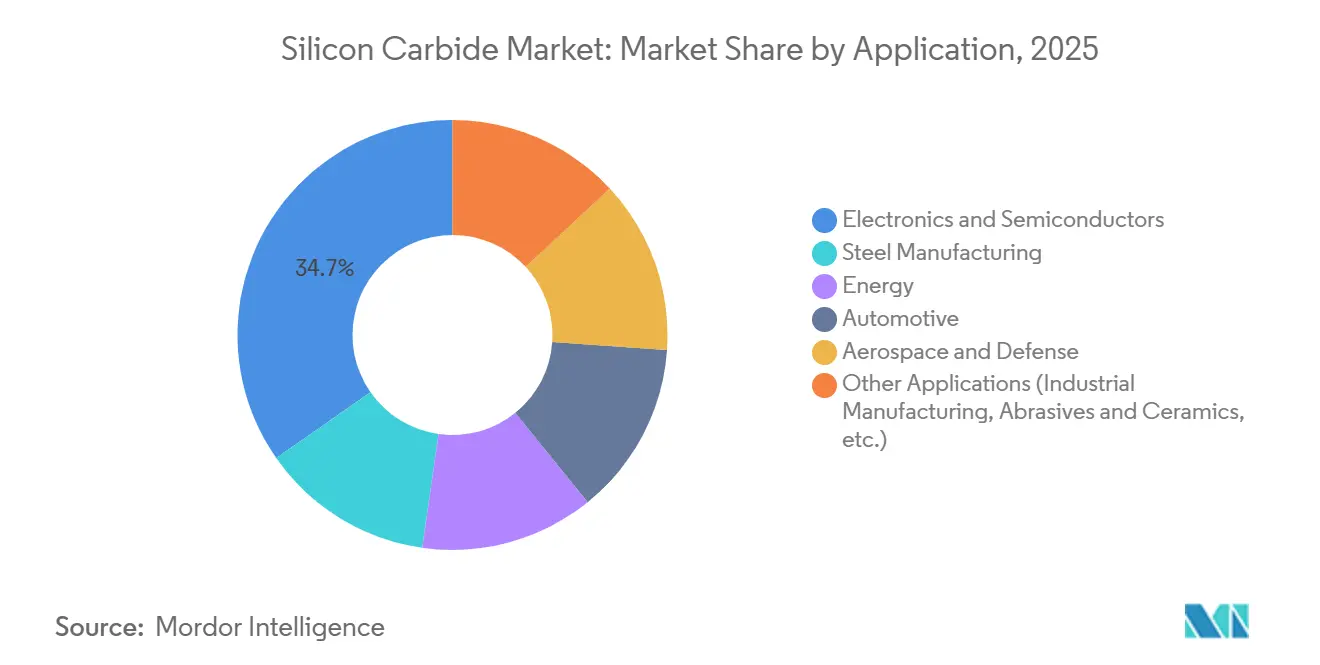

- By application, electronics and semiconductors led with 34.70% the silicon carbide market share in 2025, while automotive is forecast to expand at a 12.65% CAGR to 2031.

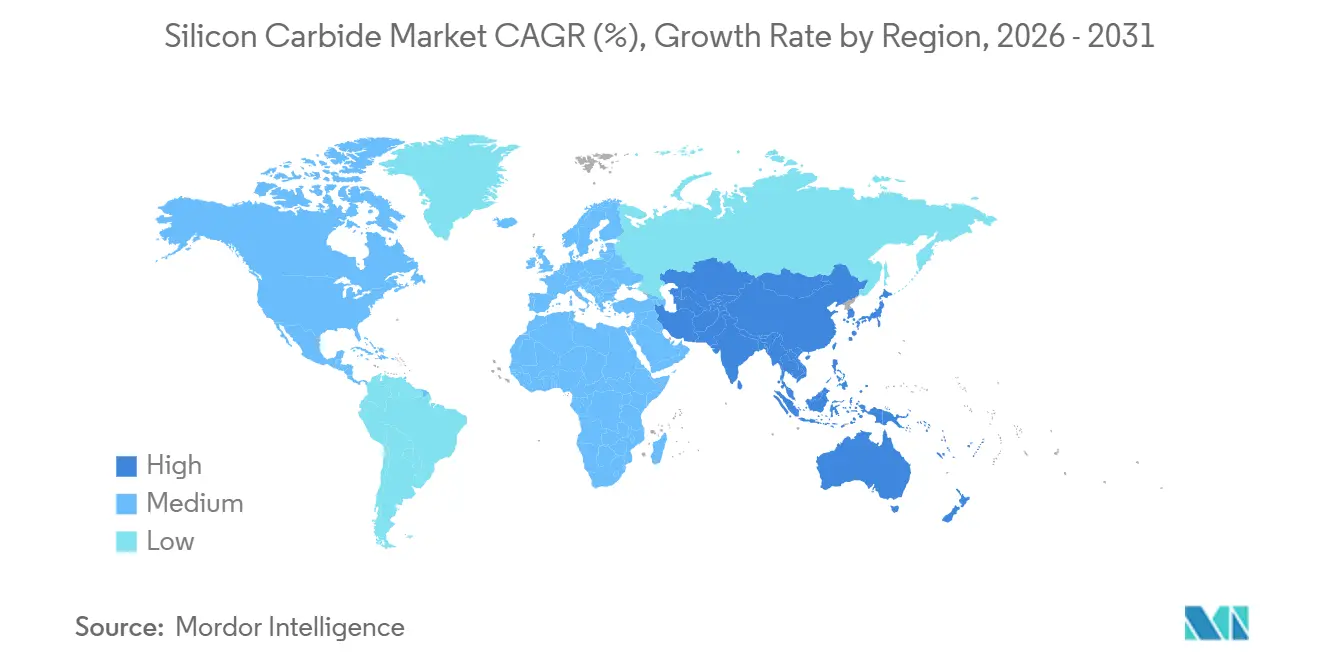

- By geography, Asia-Pacific accounted for 52.89% of the silicon carbide market size in 2025 and is advancing at a 12.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Silicon Carbide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand from Power Electronics | +3.2% | Global, with peak uptake in APAC and North America | Medium term (2-4 years) |

| Increasing Utilization in Renewable Energy | +2.4% | Global, led by Europe and China solar/wind installations | Long term (≥ 4 years) |

| Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment | +1.1% | North America, Europe industrial sectors; APAC steel mills | Medium term (2-4 years) |

| Government Incentives for Wide-Band-Gap Fabs | +2.8% | North America (CHIPS Act), Europe (EU Chips Act), APAC national programs | Short term (≤ 2 years) |

| Growing Usage in Aerospace and Defence Industry | +0.9% | North America and Europe defense contractors; selective APAC programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Power Electronics

Power-electronics modules absorbed 38% of global SiC substrate output in 2025, up from 22% in 2022, as automakers locked multiyear supply agreements for 800-volt traction inverters in the silicon carbide market. Tesla’s dual-sourcing strategy in 2024 spurred widespread qualification activity among battery-electric-vehicle manufacturers seeking cost parity with internal-combustion platforms. Industrial motor drives using SiC modules trimmed HVAC energy use by 18% and now influence new ASHRAE 90.1 code revisions[1]ASHRAE, “Standard 90.1-2025 Update,” ashrae.org . Datacenters pilot SiC-based UPS units that boost round-trip efficiency to 98.2%, a critical gain as AI inference workloads lift rack densities beyond 50 kW.

Increasing Utilization in Renewable Energy

Solar-farm inverters and wind-turbine converters represented 19% of SiC device revenue in 2025, rising from 14% in 2023 as utilities pursue higher efficiency to curb the levelized cost of electricity in the SIC market. China’s National Energy Administration mandates 98.5% minimum inverter efficiency for solar plants above 50 MW, achievable only with SiC or costly multilevel silicon alternatives. Europe’s NordLink HVDC upgrade posted 0.4% lower losses after integrating SiC modules, translating into EUR 12 million annual savings at current power prices. Energy-storage systems using SiC reach 99.1% round-trip efficiency, extending lithium-iron-phosphate cell life by reducing thermal stress.

Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment

Refractory and structural ceramics consumed 28% of black-grade output in 2025, servicing furnaces and kiln linings that operate above 1,400 °C. Indian and Southeast Asian steel mills retrofit electric-arc furnaces with SiC-bonded refractories that extend campaign life from 180 to 240 heats, lowering outage frequency and cutting refractory cost per ton of steel by 14%. Aerospace propulsion adopters leverage reaction-bonded SiC nozzles to raise turbine-inlet temperatures and add 3% thrust. Semiconductor capital-equipment suppliers deploy SiC susceptors for wafer-temperature uniformity within ± 2 °C supporting demand growth in the silicon carbide market.

Government Incentives for Wide-Band-Gap Fabs

The U.S. CHIPS and Science Act allocated USD 3.2 billion for compound-semiconductor projects, granting Wolfspeed USD 750 million in direct funding for its North Carolina 8-inch fab scheduled for late 2027 ramp. Europe’s Chips Act unlocked EUR 2.7 billion for a Dresden joint venture between STMicroelectronics and Infineon. Japan’s METI issued JPY 92 billion (USD 620 million) to ROHM and Showa Denko, while China’s State Council green-lit 15 new epitaxy lines targeting 1.2 million 6-inch-equivalent wafers a year. These incentives compress fab payback periods from 12 years to 7 years, crowding the supply curve and intensifying price pressure on commodity-grade substrates in the silicon carbide market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Cost of Raw Materials | -1.4% | Global, acute in regions dependent on Chinese silicon-metal exports | Short term (≤ 2 years) |

| Availability of Substitutes | -0.8% | North America and Europe for sub-600V applications; limited impact in APAC automotive | Medium term (2-4 years) |

| Tight Particulate-Emission Norms for SiC Grinding Plants | -0.6% | Europe and North America; selective enforcement in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Cost of Raw Materials

Silicon-metal feedstock accounted for up to 42% of SiC powder cost and traded between USD 1,800 and USD 2,100 per t in 2025 as Chinese capacity was curbed under dual-control energy policies. Petroleum coke rose 19% on refinery maintenance and OPEC cuts, squeezing gross margins for non-integrated powder mills by 3-5 points. Two U.S. mills idled assets in mid-2025 after failing to pass cost increases to grinding-wheel customers. Vertical integration helps STMicroelectronics’ captive powder synthesis trimmed per-wafer material expense by 11%.

Tight Particulate-Emission Norms for SiC Grinding Plants

The EU Industrial Emissions Directive cut particulate limits from 10 mg/m³ to 5 mg/m³ in 2024, forcing closed-loop dust-capture systems that add USD 4–6 million per line and lift annual operating expense by up to USD 500,000[2]European Commission, “Industrial Emissions Directive Revision,” europa.eu . California’s South Coast AQMD adopted similar thresholds in 2025, prompting one facility to relocate to Mexico. China drafted matching standards for 2027, but enforcement varies by province. Analysts expect 12-15% of global black-SiC grinding capacity in the SIC market, mainly subscale family-owned mills, to shutter by 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Green Silicon Carbide Gains on Precision Demand

Black silicon carbide accounted for 42.22% of revenue in the silicon carbide market in 2025, supported by refractory, abrasive, and metallurgical applications where cost outweighs purity. Green silicon carbide on the other hand is projected to expand at a 13.56% CAGR through 2031. Other product types, chiefly metallurgical-grade SiC for deoxidizing steel, fill the remainder.

Green grade commands 1.8-2.2 times the price of black material due to higher synthesis temperatures and tighter impurity control, yielding Mohs hardness of 9.5 that suits wafer lapping. Within the SIC market, The migration to 8-inch device wafers is a direct catalyst; each 8-inch wafer consumes 40% more polishing slurry than a 6-inch equivalent. Solar manufacturers adopted green-SiC saw wires in 2025, cutting kerf loss from 120 µm to 95 µm and boosting cell yield by 4.2%. U.S. Army ballistic plates deployed hot-pressed green-SiC tiles that deliver 18% lower areal density than boron carbide.

By Application: Automotive Acceleration Challenges Electronics Leadership

Electronics and semiconductors retained 34.70% of application revenue in the silicon carbide market in 2025, yet automotive is advancing at a 12.65% CAGR to 2031, reflecting rapid EV adoption. Traction inverters in long-range EVs standardize on 1,200-V SiC MOSFETs; Tesla’s 2025 Model 3 refresh integrated a 48-module SiC inverter that cut switching losses by 54% and added 11 miles of EPA range. Onboard chargers now achieve 96.5% efficiency and 3.2 kW/L power density using SiC, enabling under-seat installation.

Energy applications, including solar, wind, and grid-tied storage, are projected to account for a moderate share of revenue in 2025, driven by the use of silicon carbide in power electronics. The industrial segment is expected to consume a notable portion of black-grade tonnage for refractories and abrasives. Aerospace and defense achieve gross margins exceeding 50% due to stringent qualification requirements. The silicon carbide market size for high-purity substrates is supported by multiyear supply contracts in the automotive and renewable sectors, ensuring stable utilization rates.

Geography Analysis

Asia-Pacific held 52.89% of the silicon carbide market revenue in 2025 and is forecast to grow at 12.24% annually to 2031. China’s SICC and TankeBlue shipped 680,000 6-inch-equivalent wafers in 2025 after State Council approval for 15 new lines. Japan’s JPY 92 billion subsidy to ROHM and Showa Denko targets 40% domestic automotive self-sufficiency by 2028. South Korea’s SK Siltron ran the world’s largest 8-inch SiC fab in 2025 and will double capacity by 2027.

North America accounted for a significant silicon carbite market share, led by Wolfspeed and onsemi. CHIPS Act funding of USD 2 billion underpins onsemi’s Czech fab, yet permitting delays shifted first-wafer milestones to late 2026, conceding a qualification head-start to Asian rivals. Canada is emerging as a silicon-metal supplier, while Mexico attracts relocated grinding capacity following California’s tighter emissions rules.

In Europe, Germany’s EUR 2.7 billion Dresden joint venture will build 8-inch substrates and epitaxy, strengthening the region’s position in the silicon carbide market while NordLink’s HVDC upgrade showcased SiC’s efficiency advantage. South America and the Middle-East and Africa combined made up lower demand, focused on steel refractories and oil-field equipment. Brazil’s Gerdau and Argentina’s Ternium pilot SiC-bonded ladles; Saudi Arabia’s NEOM project specified SiC inverters for a 2.6-GW green-hydrogen plant.

Competitive Landscape

The global market is moderately concentrated: the top five substrate suppliers, Wolfspeed, Infineon Technologies AG, STMicroelectronics, Semiconductor Components Industries, LLC, and ROHM CO., LTD., controlled 47% of wafer revenue in 2025. Device makers are backward-integrating; STMicroelectronics bought a 60% stake in a European substrate JV for EUR 450 million, aiming for 200,000 8-inch wafers annually by 2027.

Technology leadership hinges on 8-inch yield. Wolfspeed holds 47 U.S. patents on micropipe mitigation, while ROHM focuses on low basal-plane dislocation epitaxy. Chinese startups undercut prices by up to 25% with state-backed capital but exhibit twice the defect rate of Tier-1 peers. Standards bodies are crafting IEC 62148 qualification rules that will favor suppliers with ISO 26262 and AEC-Q101 credentials, reinforcing entry barriers.

White-space prospects center on more than 3.3 kV devices for medium-voltage drives, SiC-on-insulator RF substrates, and SiC-diamond composites for extreme-temperature propulsion. Silicon carbide companies that achieve 85% yield on 8-inch wafers—versus today’s 72% average—can lower per-die cost by 1.8 times, winning automotive Tier-1 mandates.

Silicon Carbide Industry Leaders

Infineon Technologies AG

Semiconductor Components Industries, LLC (onsemi)

STMicroelectronics

ROHM CO., LTD.

WOLFSPEED, INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: WOLFSPEED, INC. developed a single-crystal 300mm (12-inch) silicon carbide wafer, marking a notable advancement in silicon carbide technology. This innovation drove the demand for advanced ceramics in wafer processing and device fabrication.

- December 2025: Coherent Corp. introduced a 300 mm conductive Silicon Carbide (SiC) platform designed to improve thermal efficiency, power density, and switching speeds in AI data centers. The platform featured low resistivity and defect density, enabling effective management of high-power thermal loads while supporting thinner and more efficient optical components for VR/AR applications and power electronics.

Global Silicon Carbide Market Report Scope

Silicon carbide is a hard refractory material that is a synthetically produced crystalline compound of silicon and carbon. It has been an essential material for sandpapers, grinding wheels, and cutting tools. However, it has found applications in refractory linings and heating elements for industrial furnaces, in wear-resistant parts for pumps and rocket engines, and in semiconducting substrates for light-emitting diodes.

The silicon carbide market is segmented by product type, application, and geography. By product type, the market is segmented into black silicon carbide, green silicon carbide, and other product types (e.g., metallurgical-grade silicon carbide). By application, the market is segmented into electronics and semiconductors, steel manufacturing, energy, automotive, aerospace and defense, and other applications (e.g., industrial manufacturing, abrasives, and ceramics). The report also covers market size and forecasts for silicon carbide in 28 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Black Silicon Carbide |

| Green Silicon Carbide |

| Other Product Types (Metallurgical-grade Silicon Carbide, etc.) |

| Electronics and Semiconductors |

| Steel Manufacturing |

| Energy |

| Automotive |

| Aerospace and Defense |

| Other Applications (Industrial Manufacturing, Abrasives and Ceramics, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Product Type | Black Silicon Carbide | |

| Green Silicon Carbide | ||

| Other Product Types (Metallurgical-grade Silicon Carbide, etc.) | ||

| By Application | Electronics and Semiconductors | |

| Steel Manufacturing | ||

| Energy | ||

| Automotive | ||

| Aerospace and Defense | ||

| Other Applications (Industrial Manufacturing, Abrasives and Ceramics, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the silicon carbide market?

The silicon carbide stands at USD 5.29 billion in 2026 and is projected to reach USD 8.79 billion by 2031, growing at a 10.69% CAGR from 2026.

Which segment is expanding fastest within silicon carbide applications?

Automotive is pacing at a 12.65% CAGR on the back of 800-volt EV traction inverters.

Why is green silicon carbide growing faster than black grade?

Precision wafer-polishing, 8-inch substrate adoption, and higher hardness for photovoltaic wire-sawing are driving its 13.56% CAGR.

Which region leads silicon carbide consumption?

Asia-Pacific held 52.89% of 2025 revenue and is forecast to keep outpacing other regions at a 12.24% CAGR.

Page last updated on: