Pallets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

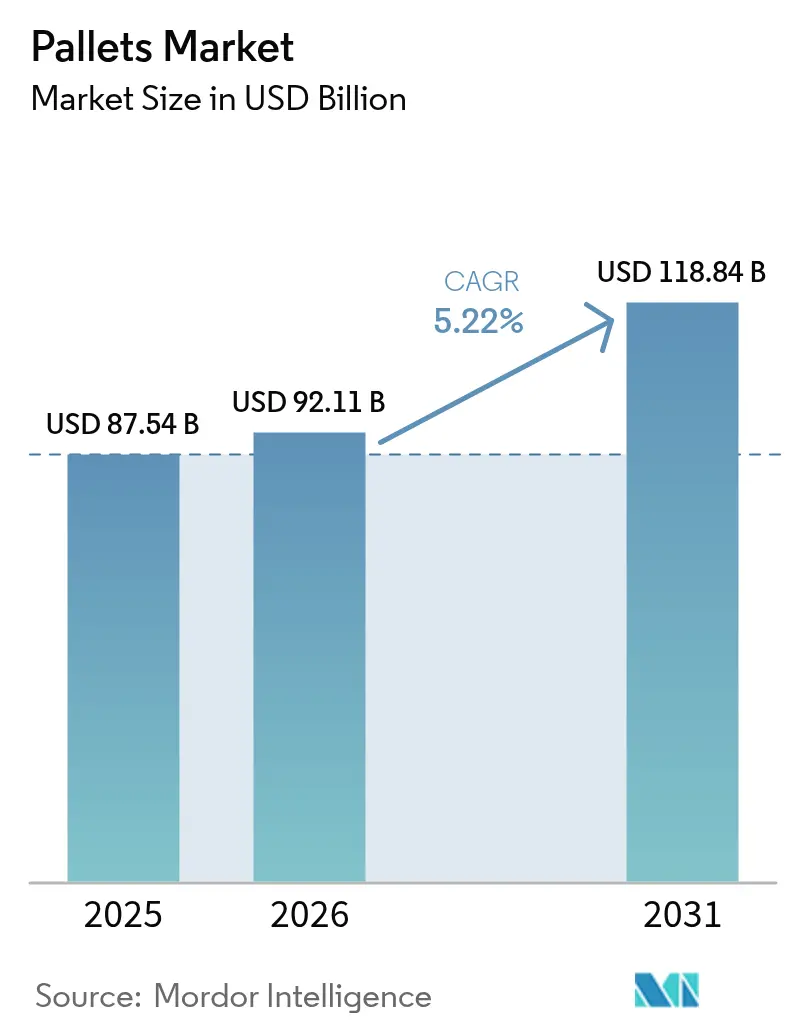

| Market Size (2026) | USD 92.11 Billion |

| Market Size (2031) | USD 118.84 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pallets Market Analysis by Mordor Intelligence

The pallets market size in 2026 is estimated at USD 92.11 billion, growing from 2025 value of USD 87.54 billion with 2031 projections showing USD 118.84 billion, growing at 5.22% CAGR over 2026-2031. Robust e-commerce activity, automation-ready warehouse design and global alignment with ISPM-15 standards underpin demand. Companies are prioritizing block pallets to avoid costly recalibration of automated storage and retrieval systems, while plastics gain share in food, beverage and pharmaceutical chains that require non-porous contact surfaces. Regional pooling models are scaling rapidly in Asia-Pacific, helped by cross-border trade initiatives that favor certified, track-and-trace assets. At the same time, lumber price volatility and weak reverse-logistics for plastics in parts of South America and Africa hold growth below potential. Despite these frictions, technology-enabled pooling and bio-composite innovations continue to open cost-efficient and sustainable pathways for users.

Key Report Takeaways

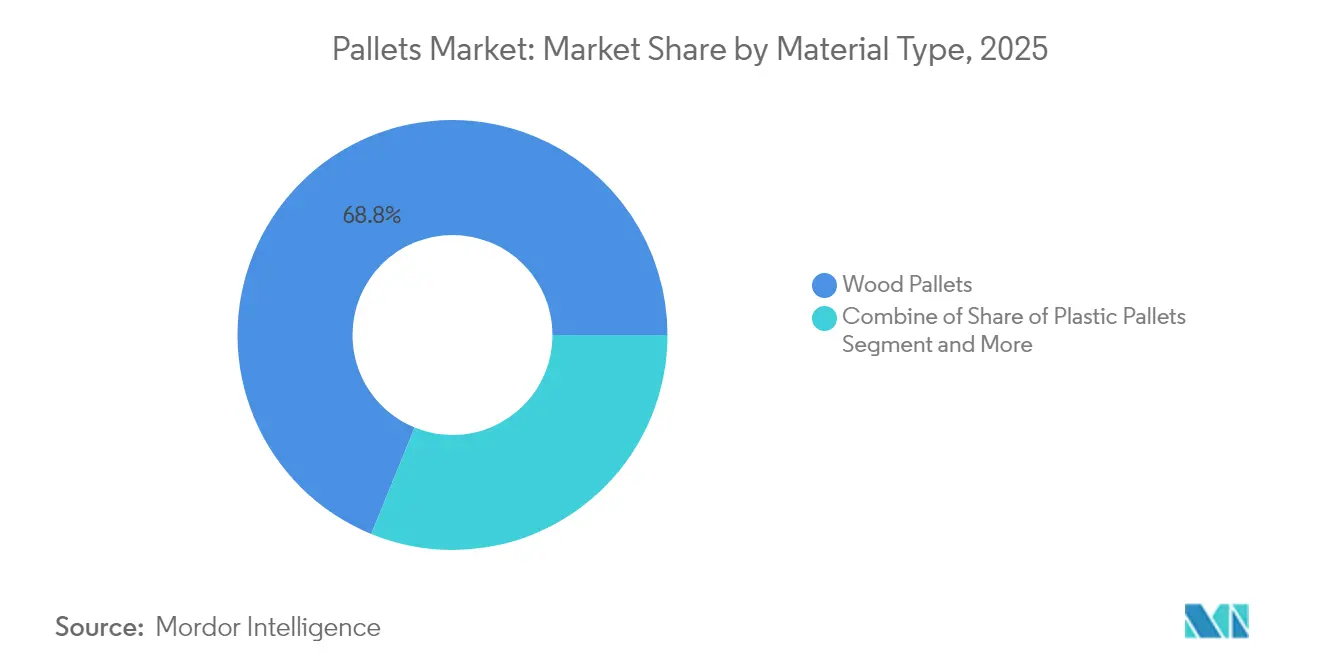

- By material type, wood held 68.83% of pallets market share in 2025; plastic is projected to register the fastest 7.02% CAGR through 2031.

- By design, block pallets led with 54.78% revenue share in 2025, whereas customized formats are expected to expand at a 7.28% CAGR to 2031.

- By pallet type, rackable solutions accounted for 44.86% of the pallets market size in 2025; nestable variants are advancing at a 6.76% CAGR to 2031.

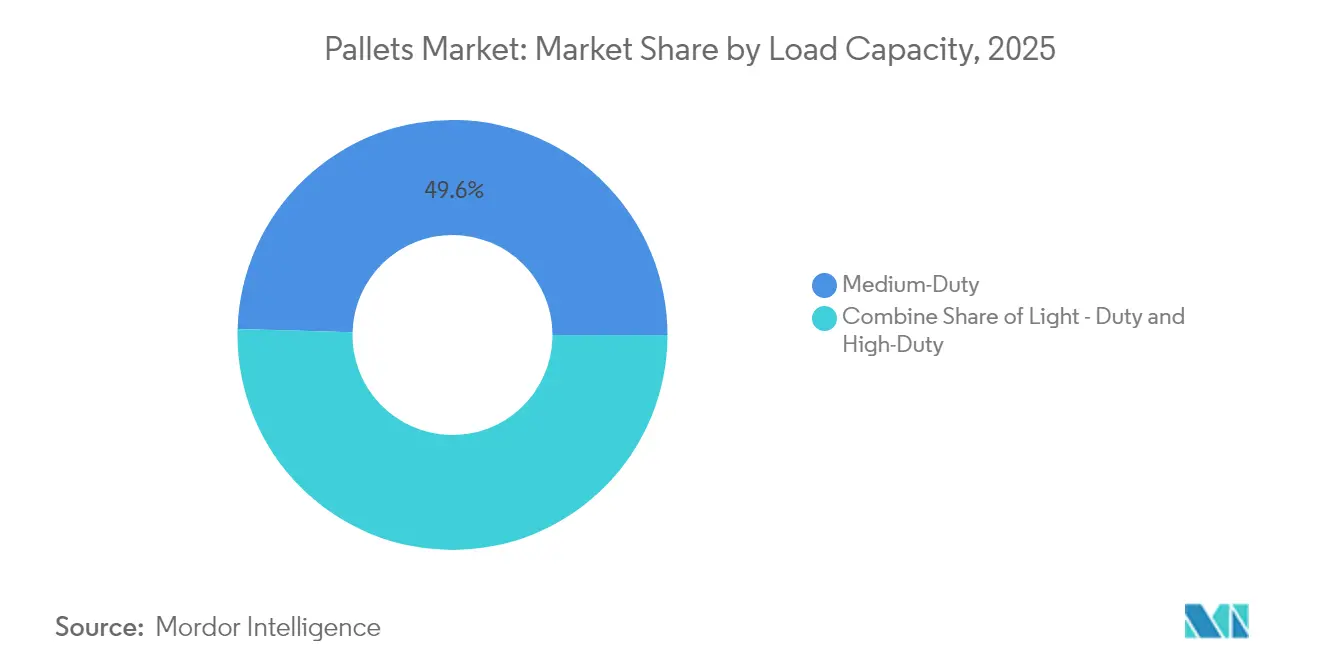

- By load class, medium-duty pallets dominated with 49.55% share in 2025; high-duty units are set for a 6.15% CAGR through 2031.

- By end-user industry, logistics and warehousing commanded 34.92% share of the pallets market size in 2025, while pharmaceutical and healthcare applications are growing at 8.53% CAGR to 2031.

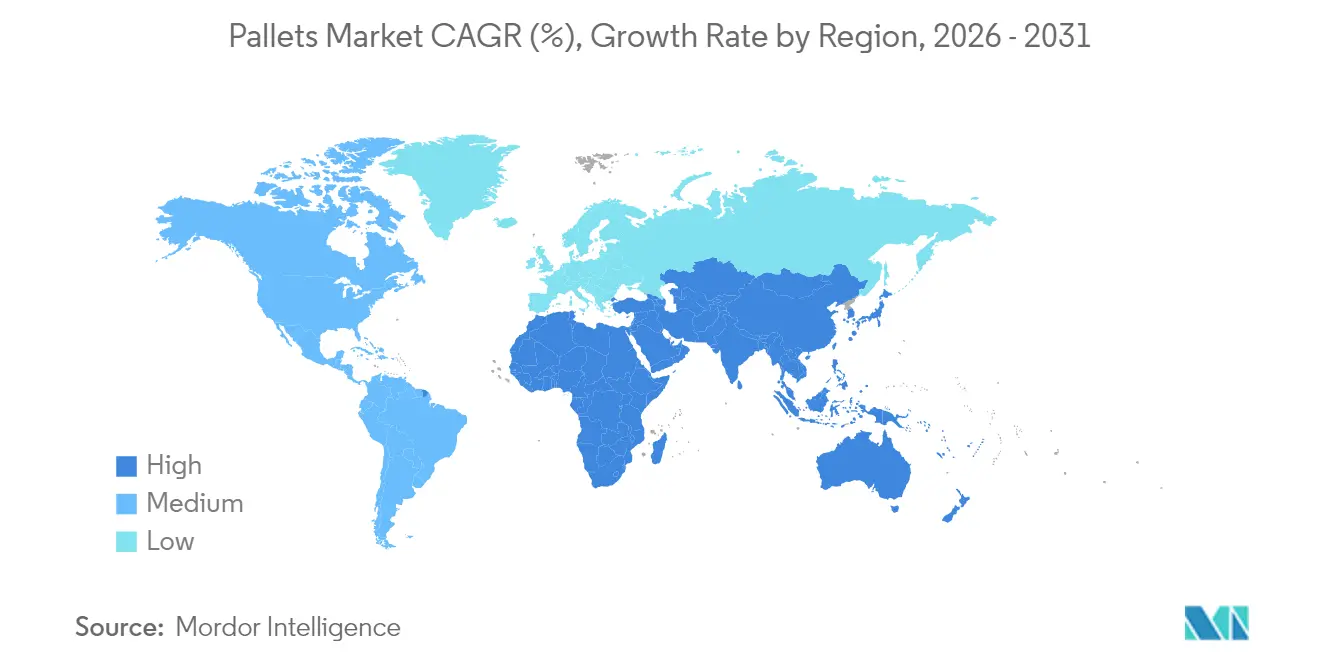

- By geography, Asia-Pacific captured 44.66% of pallets market share in 2025 and is rising at a 6.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pallets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfilment centres driving block-pallet adoption | +1.2% | North America & Europe | Medium term (2-4 years) |

| Regulatory push for ISPM-15 pallets fuelling pooling | +0.8% | Asia-Pacific core; spill-over to MEA | Long term (≥ 4 years) |

| Hygienic plastic pallets demand from FSMA and EU compliance | +0.6% | Global; concentrated in NA & EU | Medium term (2-4 years) |

| RTP uptake in pharma cold-chain logistics | +0.9% | Global; early gains in Oceania & India | Short term (≤ 2 years) |

| Warehouse robotics requiring dimensionally consistent pallets | +0.7% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Net-zero targets accelerating bio-composite pallets | +0.4% | China & SE-Asia; pilot programs in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce fulfilment centres driving block-pallet adoption

High-velocity omnichannel warehouses are standardising on block formats to secure four-way access and structural integrity. Deviation from the reference block specification can trigger USD 50,000–200,000 recalibration costs per site, locking operators into dimensionally consistent units.[1]AutoStore System, “9 Steps on How To Master Palletizing,” autostoresystem.comThroughput improvements of up to 30% and robotic mixed-case palletising gains of 288% have been recorded, reinforcing the preference for block designs.

Regulatory push for ISPM-15 pallets fuelling pooling in Asia-Pacific

The ISPM-15 framework now spans 182 countries and levies roughly USD 45 million in annual penalties, forcing shippers toward certified pooling networks that guarantee heat-treated assets. [2]European Pallet Association, “ISPM15 – Protection of International Ecosystems,” epal-pallets.orgPooling volumes in Asia-Pacific have risen 23% since 2024, aided by digital traceability devices that keep compliance data linked to each pallet.

Hygienic plastic pallets demand from FSMA and EU 1935/2004 compliance

Food and pharma operators are switching to plastics that remain below 10 mg/dm² migration limits mandated by EU rules. [3]European Commission, “Legislation,” food.ec.europa.eu Plastic units cut bacterial contamination risk by 99.9% and perform reliably from -20 °C to 40 °C.

RTP uptake in pharma cold-chain logistics across Oceania and India

Reusable packaging in cold chains is set to lift utilisation from 30% to 70% by 2030, slashing life-cycle costs up to 60%. Investments such as Cold Chain Technologies’ EUR 12 million Netherlands plant illustrate the infrastructure build-out supporting this shift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| Volatile lumber prices from US-Canada tariffs | -0.7% | North America; spill-over globally | Short term (≤ 2 years) |

| Weak reverse-logistics for plastic pallets in South America and Africa | -0.5% | South America & Africa | Medium term (2-4 years) |

| High cost and weight limiting metal pallets in EMEA air-freight | -0.3% | EMEA air-freight corridors | Long term (≥ 4 years) |

| Fragmented ASEAN standards hindering pooling scalability | -0.4% | ASEAN region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile lumber prices from US-Canada tariffs

A 14.54% duty on Canadian softwood swings wood input costs by as much as 40% per quarter, forcing manufacturers to hedge purchases and compress margins. The exposure encourages investment in alternative fibres such as corn stover panels now in pilot production.

Weak reverse-logistics for plastic pallets in South America and Africa

Recovery rates below 40% double ownership costs versus pooled models, discouraging plastic uptake even where climate benefits exist. Sparse road networks and low pooling penetration complicate collection economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Wood Dominance Faces Sustainability Pressures

Wood retained 68.83% of pallets market share in 2025, underpinned by a USD 8–12 unit price advantage. However, tariff-driven cost inflation, ISPM-15 heat-treatment fees and customer decarbonisation targets are eroding this lead. Brambles sources 78% certified timber and plants two trees for each harvested one to sustain its pool, yet users still seek lighter, recyclable options.

Plastic pallets are tracking a 7.02% CAGR through 2031 as hygiene and reusability requirements mount. Adoption accelerates where total cost of ownership offsets higher acquisition prices, especially in pharma and food sectors bound by strict contact-material rules. Bio-composites derived from rice husk and corn stover offer biodegradability within two months, meeting both regulatory and corporate carbon objectives. These attributes are gaining traction across Asia-Pacific, where agricultural residues are abundant and waste-reduction policies supportive.

By Design: Block Pallets Enable Automation Integration

Block formats commanded 54.78% of the pallets market in 2025 due to four-way access and robotic compatibility. Automated fulfilment floors report 15–20% faster handling relative to stringer alternatives.

Customized pallets are growing 7.28% CAGR as operators demand RFID inserts, sensor slots and deck surfaces tailored to specific conveyor coefficients. Hybrid builds that marry wooden decks to plastic runners balance friction optimisation with cost, supporting the rising automation installed base in grocery and apparel distribution.

By Pallet Type: Rackable Solutions Dominate Warehouse Operations

Rackable options held 44.86% of pallets market size in 2025, enabling 40–50% higher storage density in high-bay racking. Nestable units are advancing at a 6.76% CAGR as shippers prioritise back-haul efficiency; nested stacks cut empty-transport costs by as much as 70%.

Stackable and other niche designs continue to serve specialty sectors, such as fresh-produce exporters that need temporary field storage before cross-dock transfer, or hazardous-materials handlers that require steel reinforcement for safety compliance.

By Load Capacity: Medium-Duty Applications Drive Volume

Medium-duty formats captured 49.55% share by accommodating 1,000–2,500 kg loads typical of mainstream consumer-goods flows. High-duty variants above 3,000 kg are projected to rise 6.15% CAGR, fuelled by reshoring of metal-working and machinery production requiring heavier payloads.

Light-duty pallets remain the choice for apparel, lightweight electronics and parcel fulfilment, where low tare weight minimises shipping costs and manual handling injury risk.

By End-User Industry: Logistics Infrastructure Expansion Drives Demand

Logistics and warehousing users represented 34.92% share of pallets market size in 2025, reflecting consolidation of third-party logistics and omnichannel distribution. Operators such as CHEP manage multi-client share-and-reuse pools that optimise pallet turns and curb waste.

Pharmaceutical and healthcare pallets market demand is growing fastest at 8.53% CAGR to 2031. Temperature-controlled pools that maintain 2–8 °C for 96 hours underpin vaccine, biologics and specialty-drug shipments, complemented by reusable insulated shippers. Food, beverage and automotive users remain steady consumers, each dictating distinct load, hygiene and automation parameters.

Geography Analysis

Asia-Pacific led with 44.66% of pallets market share in 2025 and is expected to post a 6.23% CAGR. Manufacturing hub consolidation in China and India, plus e-commerce acceleration in Southeast Asia, continue to lift volume. Loscam’s pool expansion illustrates how cross-border asset rotation lowers repositioning miles and reduces imbalances.

North America ranks second as automation retrofits and near-shoring policy drive pallet upgrades. Lumber tariffs inject volatility but also promote alternative fibres and plastic adoption. Mexico’s deeper integration into US supply chains generates fresh demand for ISPM-15-certified pallets serving both domestic and export lanes.

Europe’s market benefits from circular-economy law, carbon pricing and high labour costs that favour automation. Implementation of reusable pallet schemes compresses waste, while bio-composite pilots in Germany and the Nordics test next-generation materials. Middle East, Africa and South America exhibit high latent potential yet remain constrained by reverse-logistics and standards fragmentation, although national logistics plans in Saudi Arabia and Brazil point to upside beyond 2027.

Competitive Landscape

The top five suppliers account for about 25% of global capacity, signalling a moderately fragmented field where regional specialists and innovators can thrive. Brambles (CHEP) leverages more than 550,000 IoT trackers to boost utilisation and sustainability reporting. ORBIS invested in a 660,000 sq ft Texas plant to align production with Mexico-US corridors, creating 190 new jobs.

Patent filings concentrate on shape optimisation and sensor integration for robot handling. Regional players pursue niche advantages: PalletBiz scaled an Eastern Europe plant to serve specialty timber segments, while CornBoard targets biomass composites that bypass lumber pricing cycles.

Sustainability finance is rising, with Brambles issuing a EUR 500 million green bond to fund low-carbon asset pools. Partnerships such as Barilla–CHEP in Italy highlight brand owners’ preference for reusable supply-chain components that cut emissions and avoid virgin wood use.

Pallets Industry Leaders

Falkenhahn AG

CABKA Group GmbH

CHEP (Commonwealth Handling Equipment Pool)

Palettes Gestion Services

PalletOne, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ORBIS Corporation opened a new 660,000 sq ft manufacturing site in Greenville, Texas

- February 2025: Brambles sold its CHEP India unit to LEAP India Private Limited.

- January 2025: Brambles priced a EUR 500 million green bond to fund sustainable pallet pools.

- December 2024: Barilla expanded reusable pallet use with CHEP in Italy, cutting 3,700 t CO₂ annually

Global Pallets Market Report Scope

The study tracks the demand based on the consumption of pallets globally across various end users listed in the study. The study factors in the impact of several geopolitical factors on the overall supply chain of the market, in addition to the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The pallet market is segmented by types (wood, plastic, metal, and corrugated paper), end user (transportation & warehousing, food & beverage, pharmaceutical, retail, and other end user), and geography (North America [United States and Canada], Europe [United Kingdom, France, Germany, Italy, Spain, and Rest of Europe], Asia-Pacific [China, Japan, India, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Argentina, Mexico, and Rest of Latin America], and Middle East and Africa [Saudi Arabia, South Africa, Egypt, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Wood |

| Plastic |

| Metal |

| Corrugated Paper/Composite |

| Block |

| Stringer |

| Customized |

| Nestable |

| Rackable |

| Stackable |

| Other Pallet Types |

| Light - Duty Pallets |

| Medium - Duty Pallets |

| High - Duty Pallets |

| Food and Beverage |

| Chemical |

| Pharmaceutical and Healthcare |

| Retail and E-Commerce |

| Logistics and Warehousing |

| Automotive |

| Other Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Wood | ||

| Plastic | |||

| Metal | |||

| Corrugated Paper/Composite | |||

| By Design | Block | ||

| Stringer | |||

| Customized | |||

| By Pallet Type | Nestable | ||

| Rackable | |||

| Stackable | |||

| Other Pallet Types | |||

| By Load Capacity | Light - Duty Pallets | ||

| Medium - Duty Pallets | |||

| High - Duty Pallets | |||

| By End-User Industry | Food and Beverage | ||

| Chemical | |||

| Pharmaceutical and Healthcare | |||

| Retail and E-Commerce | |||

| Logistics and Warehousing | |||

| Automotive | |||

| Other Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the pallets market?

The pallets market size reached USD 92.11 billion in 2026 and is projected to climb to USD 118.84 billion by 2031.

Which material segment is growing fastest?

Plastic pallets are expanding at a 7.02% CAGR through 2031, outpacing other materials due to hygiene and regulatory benefits.

Why are block pallets preferred in automated warehouses?

They provide four-way access and dimensional consistency, delivering 15–30% faster handling and avoiding costly system recalibration.

How significant is Asia-Pacific in the global pallets market?

Asia-Pacific commanded 44.66% of pallets market share in 2025 and remains the fastest-growing region at a 6.23% CAGR.

What role do pooling networks play in market growth?

Pooling lowers total cost of ownership, ensures ISPM-15 compliance and supports circular-economy goals, driving widespread adoption across regions.

Page last updated on: