Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.82 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

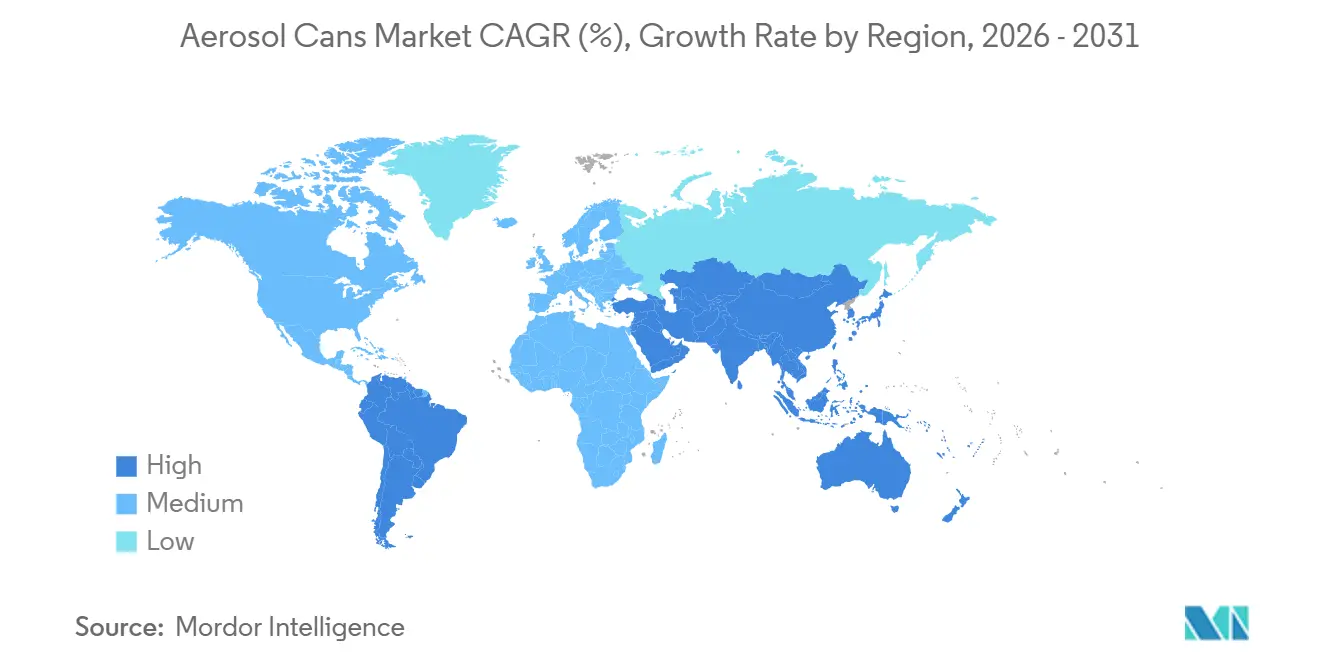

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerosol Cans Market Analysis by Mordor Intelligence

The aerosol cans market size is expected to grow from USD 8.37 billion in 2025 to USD 8.82 billion in 2026 and is forecast to reach USD 11.46 billion by 2031 at a 5.38% CAGR over 2026-2031. Personal-care brands are stepping up investments in mono-material aluminium and plastic formats that simplify recycling, while converters race to qualify compressed-gas propellant lines that avoid volatile organic compound limits. The shift toward below-100 ml packs is accelerating because subscription and direct-to-consumer models reward lighter parcels and trial-size variety. Aluminium fees under extended producer responsibility schemes are nudging brand owners to source post-consumer recycled content, and new carbon-free primary aluminium is gaining early traction in premium deodorant and hairspray launches. Competitive intensity remains moderate because regional specialists and technology start-ups can still carve out niches despite the scale advantages of Ball Corporation, Crown Holdings, Ardagh Metal Packaging, and Trivium Packaging.

Key Report Takeaways

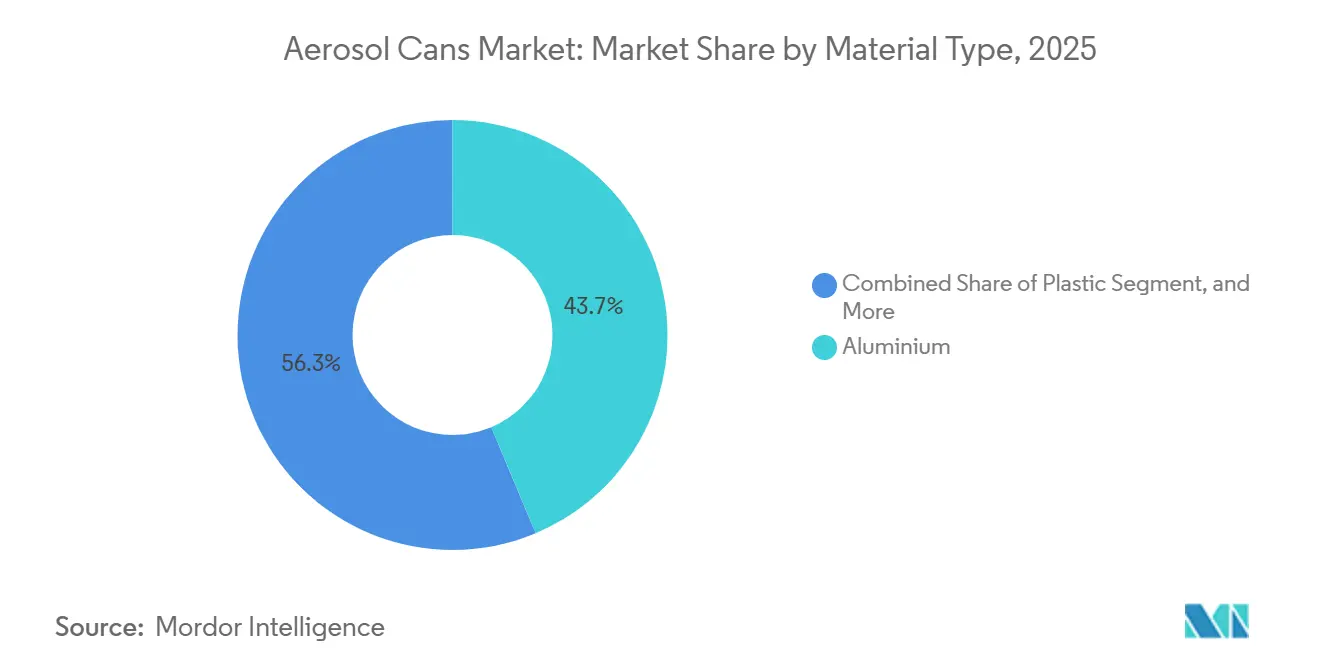

- By material type, aluminium led with 43.67% of the aerosol cans market share in 2025, while plastic is advancing at a 6.39% CAGR through 2031.

- By can type, two-piece designs held 47.94% share of the aerosol cans market size in 2025 and are growing at a 5.94% CAGR through 2031.

- By propellant type, liquefied gas retained a 52.63% share in 2025, whereas compressed gas is expanding at a 5.91% CAGR through 2031.

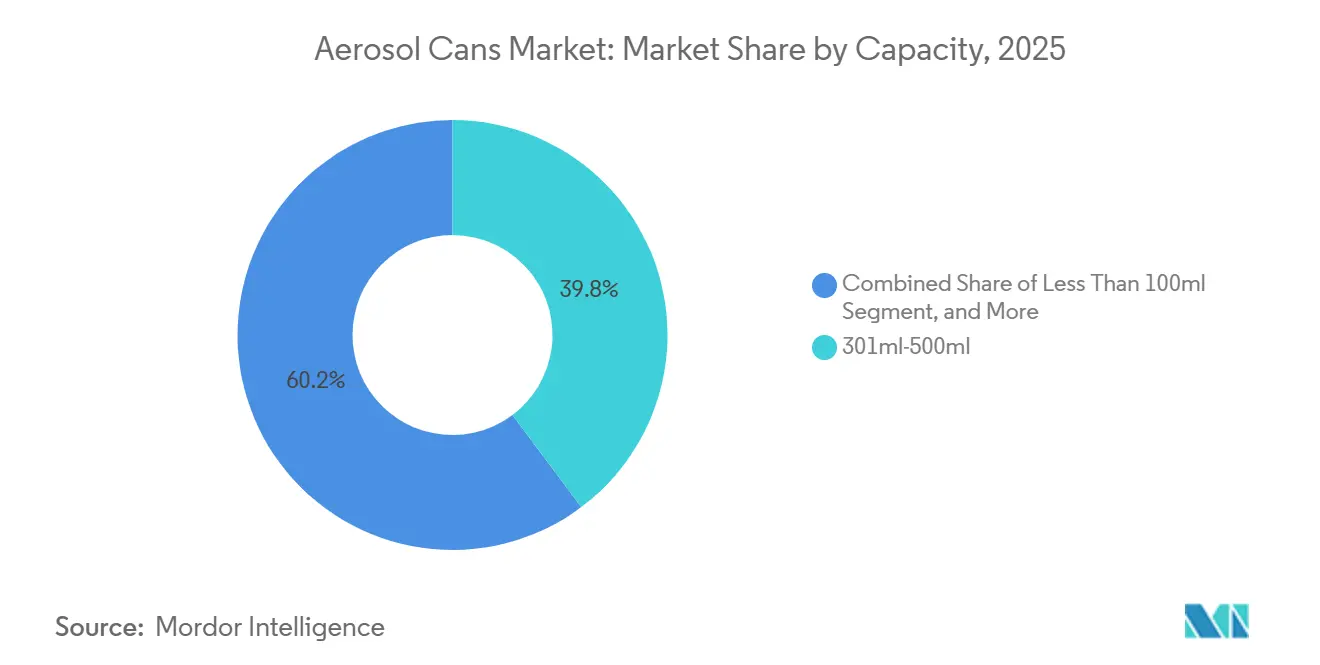

- By capacity, 301 ml-500 ml formats accounted for 39.77% of the market share in 2025, and packs below 100 ml are growing at a 6.17% CAGR through 2031.

- By end-user industry, personal care and cosmetics accounted for 54.82% of demand in 2025, while healthcare and pharmaceutical aerosols are pacing at a 6.74% CAGR through 2031.

- By geography, Europe commanded a 32.46% share in 2025, and Asia-Pacific is forecast to grow at a 6.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerosol Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recyclability and Circular Economy Alignment | +1.2% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Surging Demand from Personal-Care and Cosmetics | +1.5% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Transition to Low-VOC/Green Propellants | +0.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| E-Commerce Shelf-Ready Differentiation | +0.7% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Regulatory Push for Mono-Material Packaging | +0.8% | Europe and United Kingdom, emerging in Canada and Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Nutraceutical/OTC Aerosol Formats | +0.5% | North America and Europe, nascent in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recyclability and Circular Economy Alignment

Aluminium recycling rates exceed 75% worldwide, and steel surpasses 85% in Europe, so regulators view both substrates as cornerstones of a circular economy.[1]Lynn L. Bergeson, “Forecast for U.S. Federal and International Chemical Regulatory Policy 2026,” Bergeson & Campbell P.C., lawbc.com The United Kingdom’s extended producer responsibility fees, GBP 266 per tonne for aluminium and GBP 259 per tonne for steel, directly reward cans with higher post-consumer recycled content. Beiersdorf’s 2024 pledge to reach 50% recycled aluminium trims, with embodied carbon roughly 40% lower, is encouraging retailers to demand similar commitments. European Union rules, effective 2026, insist that all packs be recyclable by 2030, and prototypes like Purple Holding’s cup-free Click and Spray cut aluminium use by 5% while simplifying sortation. Converters unable to redesign for mono-material formats face climbing fees and shrinking shelf space as retailers rank suppliers on recyclability metrics.

Surging Demand from Personal-Care and Cosmetics

China’s online aerosol sales topped 5 billion cans in 2025, rising 12.6% year-over-year on deodorant, dry-shampoo, and sunscreen adoption.[2]Circle Economy Foundation, “Sustainable Aerosol Packaging Market Supply Chain and Competitive Analysis 2026-2034,” knowledge-hub.circle-economy.com Sunscreen sprays have overtaken lotions on beaches because they apply faster and limit hand contact, a preference tied to post-pandemic hygiene awareness. Salvalco’s Nebula actuator, released in February 2025, pairs with inert nitrogen or compressed air to deliver a drier spray, supporting gender-neutral branding. Miniature cans below 100 ml, expanding at 6.17% CAGR, let brands seed new formulas through subscription boxes without heavy inventory. Cosmetic aerosols remain lightly regulated compared with hazardous goods, though the 2025 United Nations update may trigger label revisions for certain fragrance loads.

Transition to Low-VOC/Green Propellants

Nitrogen and compressed air are growing at a 5.91% CAGR because they eliminate hydrocarbon VOCs and remove flammability warnings, easing transport and warehousing.[3]Sarah McCrady, “Introducing Our New Nebula Actuator,” Salvalco, salvalco.com Eco-Valve, underpinned by University of Salford research, delivers spray quality comparable to liquefied gas without the ignition risk. U.S. EPA rules and California alignment limit VOC mass, nudging brands toward non-reactive gases. Dimethyl ether offers an interim solution with lower global warming potential, though supply outside Asia-Pacific is limited. Bag-on-valve technology, popular in pharma and food, keeps propellant separate, enabling preservative-free formulas despite higher component costs.

E-Commerce Shelf-Ready Differentiation

Formats under 100 ml thrive online because lighter parcels cut freight, and unboxing videos reward transparent, sculpted plastic cans that pop on mobile screens. Summit Packaging’s new Toluca plant adds 250 million units of regional capacity, shortening lead times for North American fulfillment centers. Polypack’s Compact wrapper groups aerosols into twin- and triple-packs at 240 bottles per minute, enabling brands to bundle subscription orders without downtime. Europe’s 2027 digital-label deadline forces QR codes on cans, favoring converters that already host traceability and recycling data online.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and Disposal Regulations | -0.6% | North America and Europe, emerging in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Volatility in Aluminium and Steel Prices | -0.8% | Global, acute where raw materials are imported | Short term (≤ 2 years) |

| Rise of Refillable and Concentrated Formats | -0.4% | Europe and North America, nascent in Asia-Pacific | Medium term (2-4 years) |

| Consumer Eco-Perception of Aerosols | -0.3% | Europe and North America, limited impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Disposal Regulations

United States EPA 40 CFR Part 59 and parallel California rules cap VOC levels in hairsprays and cleaners, so formulators face extra testing and longer product-development cycles. The September 2025 United Nations revision introduced a warming-potential hazard class, compelling label changes by 2026-2027. European amendments that take full effect in 2026 add QR codes and mandate 10-year online hosting of hazard data, a cost burden for small converters. Brazil’s 2025 update requires Portuguese labeling on imports, and the EPA is narrowing PFAS reporting thresholds, adding uncertainty for cans with fluorinated coatings. Partial cans may be classified as hazardous at disposal, inflating reverse logistics costs for refill programs.

Volatility in Aluminium and Steel Prices

London Metal Exchange aluminium traded between USD 2,200 and USD 2,700 per tonne during 2024-2025, a 23% swing that squeezed converters without hedging access. Steel showed similar turbulence amid energy spikes and Chinese capacity cuts. Alcoa and Ball’s first commercial cans use a carbon-free ELYSIS metal mix made from recycled feedstock, with primary supply, demonstrating a route to stabilize costs but at a premium. Plastipak’s USD 53.8 million upgrade in Louisiana aims to increase recycled-plastic input, signalling a wider hedge against volatility in virgin-material prices. Smaller converters that lack access to futures markets face the harshest margin pressure, accelerating mergers and vertical integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminium Dominance Meets Plastic Innovation

Aluminium maintained 43.67% of 2025 demand as the substrate of choice for personal care, household, and food sprays. Its infinite recyclability and compatibility with high-speed impact-extrusion lines secure volume leadership, even as plastic cans expand at a 6.39% CAGR. The aerosol cans market's contribution from plastic remains modest but growing, as transparent walls, custom contours, and lower mold costs enable rapid e-commerce launches. ELYSIS carbon-free metal, blended 50-50 with post-consumer scrap, underpins premium deodorant lines that seek low-carbon credentials without sacrificing performance.

Lightweight aluminium keeps freight bills low, an advantage amplified by online sales, whereas tinplate and steel are tied to price-sensitive cleaners and automotive lubes. Hybrid and composite bodies face rising fees because European rules penalize packs that frustrate sortation. Beiersdorf’s push for 50% recycled aluminium exemplifies how retailers and regulators reward closed-loop sourcing. Plastic uptake concentrates in miniatures for travel and nutraceutical sprays, while aluminium continues to dominate mainstream 150–500 ml deodorant and hairspray volumes.

By Can Type: Two-Piece Efficiency Drives Market Share

Two-piece cans held a 47.94% share in 2025 thanks to drawing-and-ironing processes that trim metal use, omit welded side seams, and enable line speeds above 300 cans per minute. That efficiency underpins a 5.94% CAGR to 2031, outstripping one-piece and three-piece formats. One-piece bodies serve niche pharmaceutical and food aerosols where hermetic integrity overrides unit cost. Three-piece welded cans persist in large-diameter household and industrial SKUs but face recycling penalties due to the difficulty of sorting seam sections.

Summit Packaging’s Toluca plant installs high-speed regulator-valve lines optimized for two-piece shells, affirming the capital-investment bias toward this architecture. Purple Holding’s Click and Spray eliminates the need for a valve-mounting cup, cutting aluminium use by 5% and shaving seconds off changeovers while boosting recyclability. As extended producer responsibility fees rise, brands may favor two-piece cans that use simpler mono-material components and meet 2030 recyclability deadlines more easily than welded bodies.

By Propellant Type: Compressed Gas Gains on Liquefied Incumbents

Liquefied hydrocarbons maintained a 52.63% share in 2025 because of their low cost, droplet size, and decades of consumer familiarity. Yet compressed gases, chiefly nitrogen and air, are advancing at 5.91% CAGR as formulators prioritize zero-VOC labels and non-hazardous shipping. Salvalco’s Eco-Valve delivers a comparable spray pattern with nitrogen, removing flammability icons from the can. Dimethyl ether offers a lower-warming alternative in Asia-Pacific, but scarce Western supply holds back growth.

Bag-on-valve pouches isolate product from propellant, ticking preservative-free and 360-spray boxes for pharma and suncare lines, even though unit cost rises. The 2025 United Nations classification update may require global warming disclosures on hydrocarbon labels, potentially accelerating the shift to nitrogen. While the aerosol cans market will still lean on liquefied gas through 2031, compressed gas is poised to own the premium tier and win share wherever logistics, insurance, and hazard-class simplification justify its higher fill-weight ratio.

By Capacity: Miniaturization Accelerates for E-Commerce

Cans sized 301 ml-500 ml delivered 39.77% of 2025 volume because they balance consumption convenience with store-shelf impact. However, sub-100 ml packs are sprinting at a 6.17% CAGR to 2031, fueled by subscription-box bundling, airline carry-on rules, and lower dimensional-weight freight charges. The 101 ml-300 ml band still plays strongly in promotional and travel retail, while sizes above 500 ml cater to garage, industrial, and grout-sealer applications.

Polypack’s Compact shrink-wrapper enables twin- and triple-pack aerosol bundles at 240 units per minute, allowing brands to sell try-me kits online without retooling. Beijing HKKY Medical’s 2 ml menthol inhaler illustrates extreme miniaturization in wellness segments that demand single-dose convenience. Plastic cans thrive in these pocket sizes because transparency and playful shapes shine on social feeds, whereas aluminium retains dominance in core 150 ml deodorant canisters, where line speeds and cost per spray still rule.

By End-User Industry: Healthcare Outpaces Personal Care

Personal care and cosmetics accounted for 54.82% of demand in 2025, covering deodorant, hairspray, dry shampoo, and sunscreen. Growth is slowing in mature Western markets, nudging brands toward premium, sustainable, and gender-neutral propositions. Healthcare and pharmaceutical sprays, including metered-dose inhalers and nasal mists, are growing at a 6.74% CAGR as aging populations and respiratory health awareness drive unit volumes. Haleon’s Otrivin Nasal Mist, powered by Aptar Pharma’s microdroplet pump, demonstrates how propellant-free pumps can complement or even replace traditional aerosol valves in drug delivery.

Patent filings around aerosolized vitamins B12 and melatonin point to nutraceutical crossovers that extend beyond traditional albuterol or fluticasone inhalers. Household, automotive, paint, and food aerosols account for the remaining 45.18% and grow modestly, as concentrate-refill models and strict VOC caps temper demand. The healthcare segment, backed by stringent dose-accuracy requirements, pushes converters to invest in clean-room lines and bar-code traceability, reinforcing barriers to entry for general-purpose fillers.

Geography Analysis

Europe accounted for 32.46% of global demand in 2025, buoyed by Germany and France, where personal-care aerosols accounted for more than half of volumes. Producer-responsibility fees GBP 266 per tonne on aluminium in the United Kingdom and the European Union’s 2030 recyclability mandate push brands toward post-consumer recycled content, mono-material valves, and compressed-gas propellants. EU digital-label rules taking hold in 2027 require QR codes linked to 10-year online hazard data, pressing converters to build robust information systems. Europe’s tight regulatory net positions the region as a launchpad for low-carbon aluminium blends and cup-less valve designs before worldwide rollouts.

Asia-Pacific is the fastest-growing region, with a 6.33% CAGR through 2031, as China and India urbanize and middle-class purchasing power rises. China sold more than 5 billion personal-care cans online in 2025, up 12.6% year over year, making digital channels the prime battlefield. Japan and South Korea focus on premium suncare and pharma sprays, while India’s deodorant boom attracts regional fillers. Local capacity expansions in Southeast Asia and India shorten supply chains and insulate brands from freight volatility. Although regulatory pressure on VOCs and recyclability lags Europe, governments are signalling intent to converge, prompting multinationals to pre-empt future rules with greener propellants.

North America shows steady albeit slower expansion as market maturity intersects with VOC ceilings and rising consumer interest in refillable alternatives. EPA standards and OSHA alignment with United Nations labels compel reformulation budgets and hazard-data updates. Mexico emerges as a cost-competitive fill hub tied into the United States retail, exemplified by Summit Packaging’s Toluca plant, which feeds e-commerce replenishment centers. South America, led by Brazil, offers moderate upside, tempered by currency fluctuation and route-to-market complexity. Middle East and Africa markets remain nascent; demand clusters in the Gulf Cooperation Council states and South Africa, where Western personal-care brands enjoy premium positioning but face limits on price elasticity.

Competitive Landscape

Four multinationals, Ball Corporation, Crown Holdings, Ardagh Metal Packaging, and Trivium Packaging, frame a market where the top five players hold roughly 55% of global volume, leaving space for local specialists and technology challengers. Strategy levers center on vertical integration into recycled-metal streams, regional manufacturing footprints, and proprietary valves that enable compressed-gas systems. Alcoa and Ball’s partnership on ELYSIS carbon-free aluminium illustrates how material innovation differentiates premium offerings and hedges against volatile spot metal prices.

Regional converters invest in capacity near consumption hotspots to reduce freight costs and enhance responsiveness. Summit Packaging’s Toluca site exemplifies localized scale paired with ISO and BRC certifications that satisfy multinational brand audits. Disruptors such as Alternative Packaging Solutions and Purple Holding deploy intellectual property that eliminates pressurization or reduces component count, capturing sustainability-minded contracts. Salvalco licenses Eco-Valve and Eco-Inverted across Asia-Pacific and Europe, earning royalties while widening nitrogen adoption.

Midsize fillers that lag on compressed-gas capabilities or digital-label readiness risk delisting as retailers align with circular-economy scorecards. Consolidation is likely as raw-material volatility and compliance investments stretch weaker balance sheets. Partnerships between dispensing-technology firms and converters are intensifying to fast-track market entry for nutraceutical and over-the-counter aerosol formats that demand pharmaceutical-grade controls.

Aerosol Cans Industry Leaders

Ball Corporation

Crown Holdings, Inc.

Ardagh Metal Packaging S.A.

Trivium Packaging B.V.

Mauser Packaging Solutions Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Alcoa, Ball Corporation, and Unilever launched personal and home-care aerosol cans using 50% ELYSIS carbon-free aluminium blended with 50% post-consumer scrap.

- November 2025: Plastipak Packaging unveiled a USD 53.8 million expansion of its Rapides Parish, Louisiana plant, adding warehouse space and up to five new recycled-plastic production lines, with project completion slated for Q4 2026.

- November 2025: Polypack introduced the Compact shrink-wrapper capable of multipacking aerosols at 240 bottles per minute with zero tool changes.

- August 2025: Summit Packaging Systems opened a 3,500 m² aerosol facility in Toluca, Mexico, equipped with two high-speed regulator-valve assembly lines for 250 million units per year.

Global Aerosol Cans Market Report Scope

The Aerosol Cans Market Report is Segmented by Material Type (Aluminium, Steel, Tinplate, Plastic, Other Material Types), Can Type (One-Piece, Two-Piece, Three-Piece), Propellant Type (Compressed Gas, Liquefied Gas, Bag-on-Valve), Capacity (Less Than 100ml, 101ml-300ml, 301ml-500ml, More Than 500ml), End-User Industry (Personal Care and Cosmetics, Household Care, Automotive and Industrial, Healthcare and Pharmaceutical, Food and Beverage, Paints and Varnishes, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Aluminium |

| Steel |

| Tinplate |

| Plastic |

| Other Material Types |

By Can Type

| One-Piece |

| Two-Piece |

| Three-Piece |

By Propellant Type

| Compressed Gas | |

| Liquefied Gas | Hydrocarbon |

| DME | |

| Other Liquefied Gas | |

| Bag-on-Valve |

By Capacity

| Less Than 100ml |

| 101ml-300ml |

| 301ml-500ml |

| More Than 500ml |

By End-User Industry

| Personal Care and Cosmetics |

| Household Care |

| Automotive and Industrial |

| Healthcare and Pharmaceutical |

| Food and Beverage |

| Paints and Varnishes |

| Other End-User Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Aluminium | ||

| Steel | |||

| Tinplate | |||

| Plastic | |||

| Other Material Types | |||

| By Can Type | One-Piece | ||

| Two-Piece | |||

| Three-Piece | |||

| By Propellant Type | Compressed Gas | ||

| Liquefied Gas | Hydrocarbon | ||

| DME | |||

| Other Liquefied Gas | |||

| Bag-on-Valve | |||

| By Capacity | Less Than 100ml | ||

| 101ml-300ml | |||

| 301ml-500ml | |||

| More Than 500ml | |||

| By End-User Industry | Personal Care and Cosmetics | ||

| Household Care | |||

| Automotive and Industrial | |||

| Healthcare and Pharmaceutical | |||

| Food and Beverage | |||

| Paints and Varnishes | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the aerosol cans market be by 2031?

It is forecast to reach USD 11.46 billion, expanding at a 5.38% CAGR from 2026 to 2031.

Which end-user industry segment is growing fastest within aerosol cans?

Healthcare and pharmaceutical segment is projected to grow at 6.74% CAGR, outpacing personal care.

Why are compressed-gas propellants gaining traction?

Nitrogen and air eliminate VOC concerns, remove flammability hazards, and help brands achieve non-hazardous shipping status.

What drives miniaturization of aerosol packaging?

Sub-100 ml cans reduce freight, meet airline carry-on rules, and boost subscription-box sampling.

How are regulations influencing aerosol can design?

Europe’s 2030 recyclability mandate and extended-producer-responsibility fees are pushing converters toward mono-material, easily recyclable cans.

Who are the leading aerosol can suppliers?

Ball Corporation, Crown Holdings, Ardagh Metal Packaging, and Trivium Packaging together hold the largest combined share though the market remains moderately concentrated.

Page last updated on: