United States Humate Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

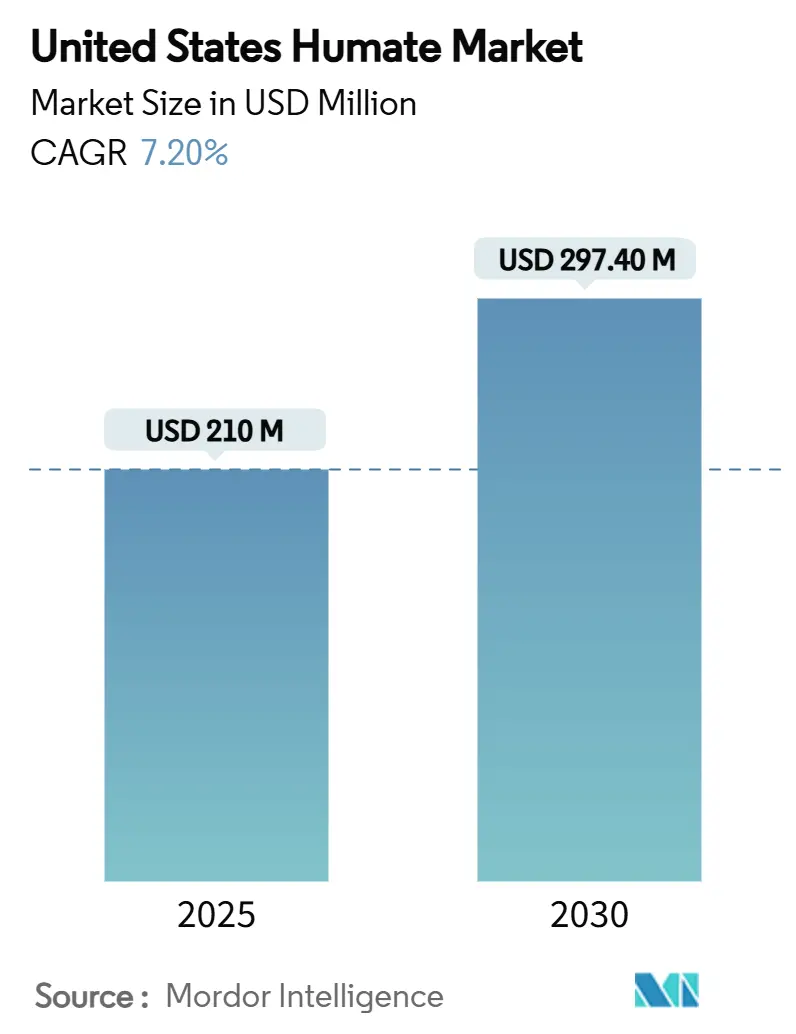

| Market Size (2025) | USD 210 Million |

| Market Size (2030) | USD 297.40 Million |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

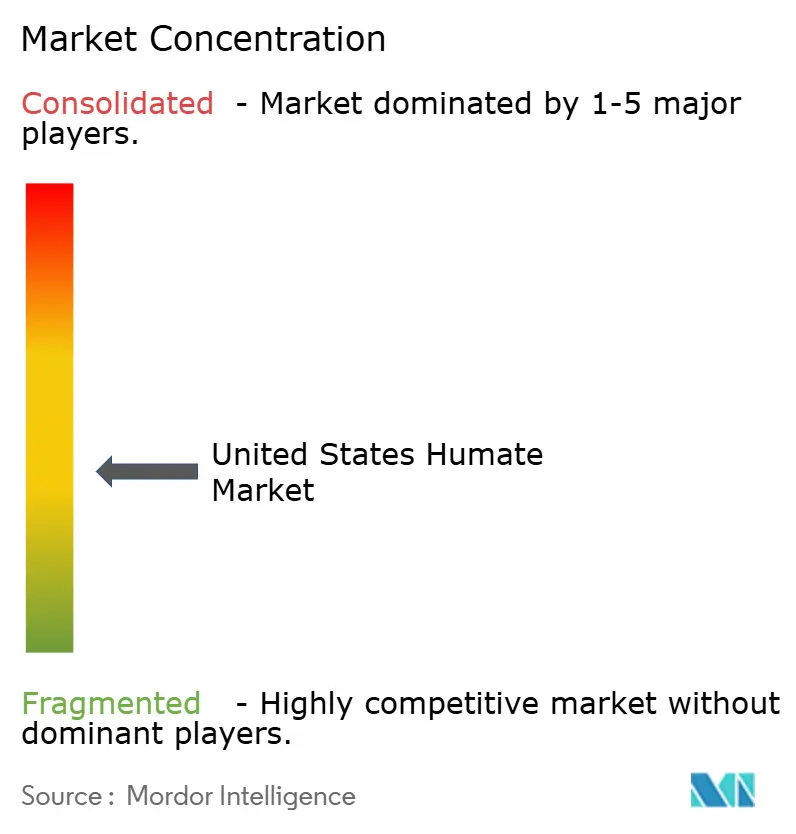

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Humate Market Analysis by Mordor Intelligence

The humate market size in the United States stands at USD 210 million in 2025 and is projected to reach USD 297.4 million by 2030, expanding at a 7.2% CAGR over the forecast period. Rising adoption of regenerative agriculture, mounting regulatory pressure on nutrient runoff, and growing carbon-credit programs are accelerating demand for humate-based soil amendments. Leonardite-sourced powders and granules dominate current purchasing patterns because they integrate seamlessly with existing fertilizer equipment, yet liquid formulations are surging as fertigation and controlled-environment systems seek precise nutrient delivery. Competitive intensity remains moderate with players racing to lock in feedstock and patent new dispersing technologies, while niche firms pursue high-margin environmental remediation or animal nutrition applications. Incentives under the Inflation Reduction Act and USDA conservation programs are creating fresh revenue streams by monetizing the carbon-sequestration benefits of humic substances.

Key Report Takeaways

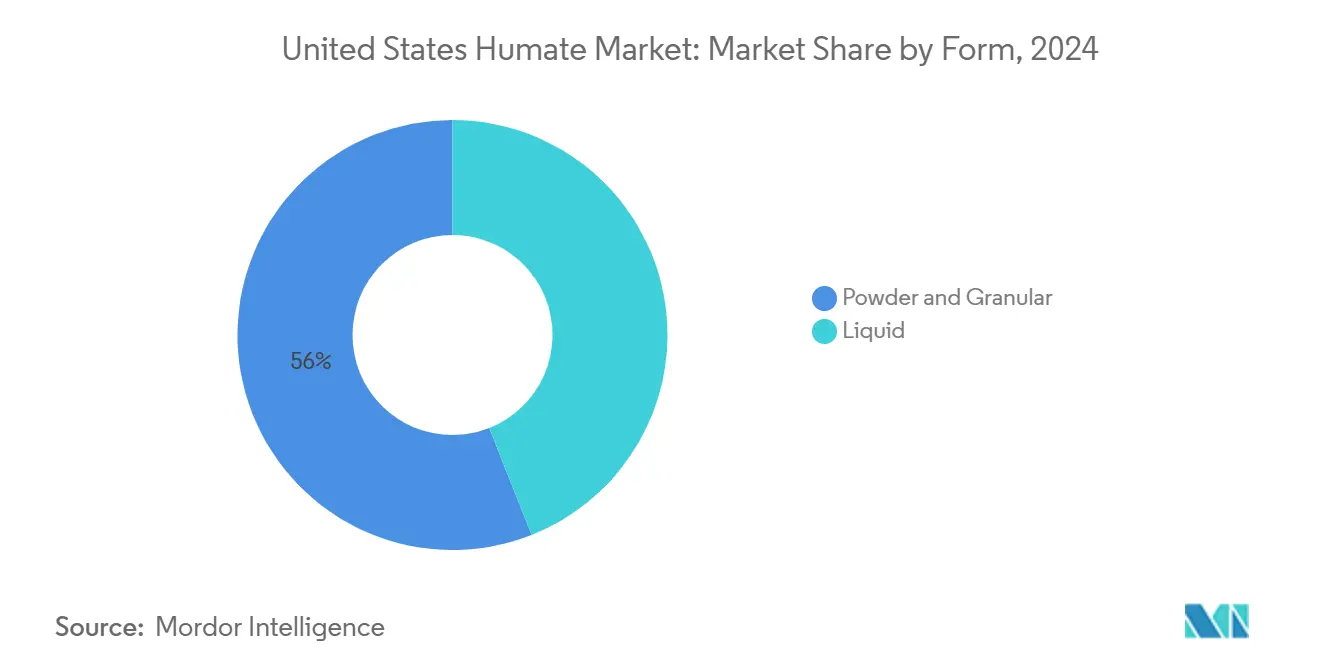

- By form, powder and granular products accounted for 56% of the United States humate market size revenue in 2024, while liquid formulations are projected to grow at a CAGR of 11.5% during 2025-2030.

- By product type, humic acid captured 46.2% of the United States humate market share in 2024, while fulvic acid is poised for the fastest growth, at a 10.8% CAGR, through 2030.

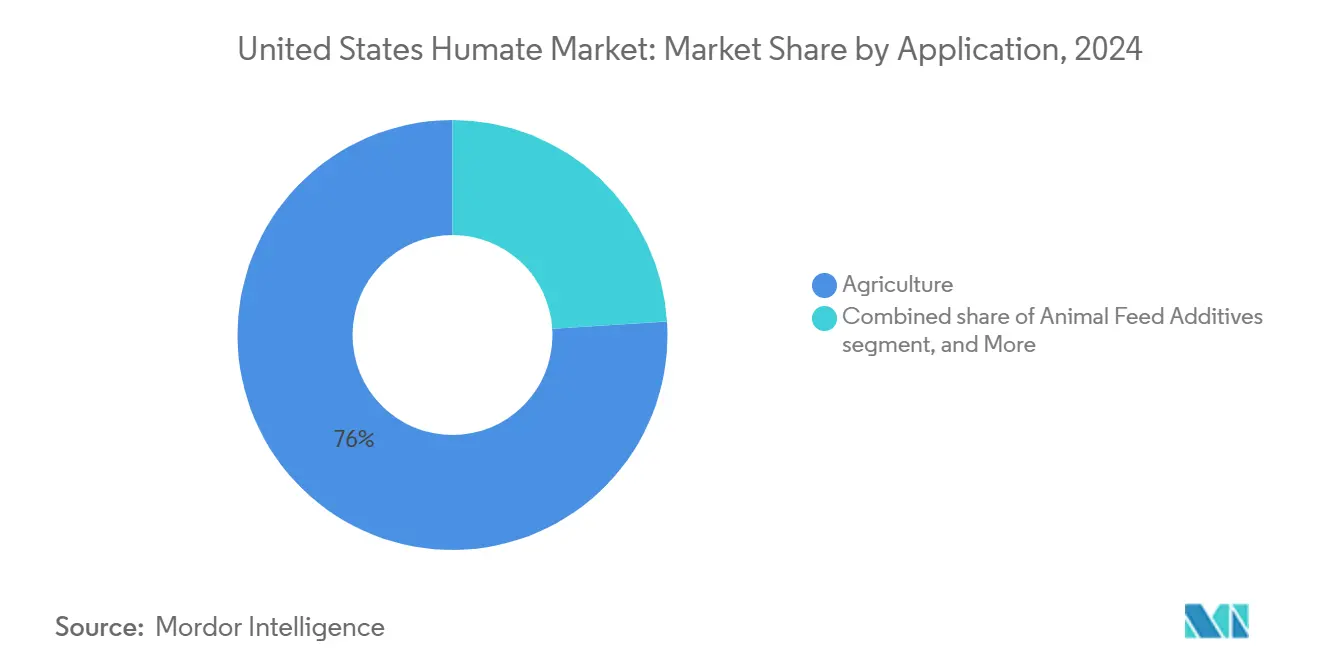

- By application, agriculture commanded 76% of the humate market in 2024, while animal feed additives are projected to expand at a 13.2% CAGR between 2025 and 2030.

- By source material, Leonardite contributed 62.2% of 2024 sales, with peat-derived humates rising at a 10.5% CAGR over the forecast horizon.

United States Humate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward certified organic and regenerative farming | +1.8% | National, with concentration in California, Iowa, and Illinois | Medium term (2-4 years) |

| Federal and state nutrient-runoff regulations | +1.5% | Midwest and South, particularly Iowa, Nebraska, and Minnesota | Short term (≤ 2 years) |

| Carbon-credit incentives for humate soil amendments | +1.2% | National, with early adoption in Midwest corn belt | Long term (≥ 4 years) |

| Uptake in controlled-environment agriculture additives | +1.0% | West Coast and Northeast greenhouse operations | Medium term (2-4 years) |

| Humate-based seed-coat biostimulants | +0.9% | National, with focus on corn and soybean regions | Short term (≤ 2 years) |

| Drought-resilient turf management demand | +0.8% | Southwest and West regions, and golf course markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Certified Organic and Regenerative Farming

Organic and regenerative certification standards permit naturally occurring humic deposits while disallowing synthetic fortifiers, steering growers toward high-quality humate inputs that meet the United States Department of Agriculture (USDA) National Organic Program rules [1]Source: USDA National Organic Program, “Humic Acid Extraction,” ams.usda.gov. The USDA committed USD 10 million in transition funding and USD 24.8 million in market-development grants during 2024, reaching more than 49,000 producers [2]Source: USDA NRCS, “Conservation Practice Standard 336,” nrcs.usda.gov. Meta-analysis confirms the agronomic benefits of incorporating humic acid into fertilization regimes, showing 12% higher yields and 27% greater nitrogen-use efficiency, particularly in temperate zones with ≥300 mm rainfall and moderate pH soils. These performance gains, coupled with premium crop pricing and impending nitrogen-rulemaking, keep the humate market on a robust growth trajectory.

Federal and State Nutrient-Runoff Regulations

Environmental Protection Agency (EPA)-identified nitrate impairments in Midwestern watersheds and the FDA’s 2024 produce-water rule compel farms to curb leaching losses, a requirement that humates satisfy by binding nutrients in the root zone. Financial carrots reinforce regulatory sticks. Natural Resources Conservation Service (NRCS) Conservation Practice Standard 336 reimburses growers who apply soil-carbon amendments, including qualifying humate products, under Environmental Quality Incentives Program (EQIP) contracts. State programs such as New Mexico’s Healthy Soil grants add localized incentives.

Carbon-Credit Incentives for Humate Soil Amendments

Indigo Ag’s Carbon program enrolled 6.9 million acres and issued 296,000 credits by 2024, proving that humate-enhanced soil carbon can be monetized at scale. USDA follow-on funding of USD 8 million for soil-carbon measurement partnerships and a USD 7.7 billion pool for climate-smart practices amplify the revenue case for growers adopting humic substances. Rigorous protocols under registries such as Climate Action Reserve ensure additionality and permanence, enabling premium pricing for credits tied to documented humate applications.

Uptake in Controlled-Environment Agriculture Additives

Hydroponic lettuce exposed to 1,000 mg/L humic acid nutrient solutions shows significantly higher uptake of K, P, Ca, Mg, and micronutrients compared to lower doses. Greenhouse tomato trials echo these gains, reporting improved fruit quality and richer rhizosphere microbiomes. Because fertigation systems enable precise metering, Controlled Environment Agriculture (CEA) operators are willing to pay premiums for concentrated liquids that deliver quick bioavailability, thereby expanding the humate market well beyond open-field agriculture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of product-quality testing standards | -0.8% | National, affecting all market segments | Long term (≥ 4 years) |

| Volatile leonardite feedstock costs | -0.6% | Western states with mining operations | Short term (≤ 2 years) |

| Competition from microbial biostimulants | -0.5% | National, concentrated in high-value crops | Medium term (2-4 years) |

| Shipping restrictions on high-carbon inputs | -0.3% | Interstate commerce, Animal and Plant Health Inspection Service (APHIS) regulated | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Product-Quality Testing Standards

Inconsistent assays inflate fulvic-acid claims, eroding buyer trust. Although the Lamar UV-Vis method is recognized by the Association of American Plant Food Control Officials (AAPFCO), only a portion of suppliers have adopted it, leaving room for adulterated products in the channel. Absent a federal definition, states rely on disparate protocols, complicating interstate commerce and dampening premium-brand pricing potential. The market fragmentation caused by quality inconsistencies prevents premium pricing for high-quality products and limits the development of performance-based marketing strategies that could drive broader adoption across agricultural sectors.

Volatile Leonardite Feedstock Costs

Leonardite mining faces rising operating costs from reclamation mandates and diesel price swings. Alberta’s deposits can be produced for under USD 62 per metric ton, yet logistics inflate delivered costs for US processors [3]Source: Alberta Geological Survey, “Evaluation of Leonardite Resources,” ags.aer.ca. The development of alternative extraction technologies, including biological conversion processes that can transform lower-grade coal into humic acids, offers potential supply diversification but requires significant capital investment and regulatory approval that may not materialize within the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder and Granular Reliability versus Liquid Precision

Powder and granular products retained 56% of the United States humate market share in 2024, reflecting compatibility with existing dry-fertilizer spreaders and ease of blending with NPKs. Dispersing-granule technology breaks particles into micro-size fragments at the soil surface, extending root-zone coverage without extra passes. Research showing faster uptake in sandy soils underpins the expansion of liquids into specialty crop belts and coastal vegetables. Greater uniformity also helps growers document outcomes for carbon-credit verification, indirectly strengthening demand for liquid SKUs.

Liquids, growing at 11.5% CAGR, appeal to fertigation and drip systems that demand meter-by-meter accuracy. Concentrated formulations at 16-18% humic-acid content lower freight costs and boost shelf stability, sustaining scale-up across greenhouses and pivot-irrigated acres. The shift toward liquids signifies wider precision-ag adoption. Real-time weather, soil-moisture probes, and variable-rate pumps allow growers to modulate doses, optimizing cost per unit of yield.

By Product Type: Humic Acid Stronghold amid Fulvic Momentum

Humic acid accounted for 46.2% of the United States humate market sales in 2024, as it remains the primary soil-structuring agent for improving cation-exchange capacity and water retention. Farmers value its visible black coloration as a quality cue and its proven compatibility with ammonium and urea fertilizers. Potassium humate remains a smaller slice yet attracts operations seeking dual nutrient and biostimulant functions.

Fulvic acid, expanding 10.8% annually, owes its momentum to its low molecular weight and chelating power that delivers micronutrients directly into cell membranes. Trials under low-phosphorus stress showcased enhanced root morphology and faster biomass accumulation. As testing standards tighten, premium suppliers spotlight mineral-sourced fulvic acids from lignite or peat, distancing themselves from biochemical extracts that degrade faster.

By Application: Agriculture Core, Feed & Remediation Rising

Agriculture represented 76% of the humate market in 2024. Corn, soybean, cotton, and specialty growers utilize humic acids to unlock tied-up nutrients and buffer saline soils, thereby supporting both yield and environmental stewardship goals. The animal feed segment, growing at a 13.2% CAGR, attracts producers seeking antibiotic alternatives. Humic acid supplementation has demonstrated improved feed conversion ratios and enhanced immune markers in broilers and dairy herds.

Environmental remediation, although nascent, utilizes humic surfactants to extract heavy metals and Polychlorinated Biphenyls (PCBs) from contaminated sites, achieving pollutant removal rates of 68-75% in pilot studies. Agencies tasked with mine-land reclamation and coastal cleanup projects provide a pipeline for specialty-grade humates tailored to pH-extreme environments.

By Source Material: Leonardite Bulk Leader, Peat Innovation Upswing

Leonardite contributed 62.2% of 2024 revenues because of its high humic-acid concentration and established mining infrastructure in North Dakota, Wyoming, and New Mexico. Long-term supply contracts between miners and formulators shield the value chain from short-term price spikes. Peat-derived materials, growing 10.5% yearly, are gaining credibility as alkaline-extraction yields rise and life-cycle assessments favor renewable feedstocks. Sourcing from highly decomposed peats with low ash content yields fertilizers that comply with K2O/TOC performance ratios.

Lignite and weathered coal sit in between as biological conversion advances could unlock high-purity humic acids while capturing methane and Volatile Fatty Acids (VFAs) as coproducts, as outlined in patents that achieve up to 95% conversion efficiency. Scale commercialization, however, hinges on capital intensity and regulatory approvals that extend beyond the forecast window.

Geography Analysis

Midwestern operations form the epicenter of humate adoption. Iowa growers applying humic liquids at 5 gallons per acre report statistically significant corn-yield lifts and positive ROI even without carbon-credit revenue. Indiana and Illinois cooperatives are bundling humic packages with variable-rate nitrogen services to comply with watershed discharge limits while sustaining yield targets. Land-grant universities deliver field-day demonstrations that bolster peer-to-peer learning, accelerating word-of-mouth diffusion across row-crop counties.

The South is the fastest-advancing region. Cotton and peanut growers appreciate humic buffering against salt injury and heat stress, while turf managers on golf courses from Texas to Georgia use humic applications to improve drought resilience. Field research in Tennessee confirmed that incorporating 10-30% humic acid into foliar UAN mixes reduces leaf burn and preserves chlorophyll content. Regulatory clarity arrived in July 2025 when Mississippi’s amended Plant and Soil Amendment Law codified biostimulant claims, de-risking market entry for compliant brands.

The West and Northeast present niche yet premium opportunities. California CEA facilities integrate liquid humates into closed-loop fertigation for tomatoes, berries, and leafy greens, leveraging documented gains in micronutrient uptake and root vigor. Proximity to leonardite mines shortens supply routes for processors in Wyoming and New Mexico, supporting competitive delivered pricing to Western specialty-crop and turf markets. In the Northeast, greenhouse ornamentals and hydroponic herbs favor high-purity humic extracts that align with local sustainability mandates and retailer traceability audits.

Competitive Landscape

The humate market is moderately fragmented but displays accelerating consolidation. HGS BioScience Inc.’s USD 30 million senior financing announced in November 2024 funds capacity expansion across six North American plants, vaulting the firm into the world’s largest extracted-humate supplier. Bio Huma Netics Inc.’s March 2025 acquisition of Gro-Power integrates bio-stimulants, composts, and microbial solutions under one umbrella, heralding a shift toward full-suite soil-health platforms.

Technology moats are widening. The Andersons Inc. commercialized Dispersing Granule technology, which breaks down into sub-100-micron particles upon contact with moisture, increasing root interception while minimizing dust during handling. Emerging entrants are piloting enzymatic and microbial conversion of low-grade coal into humic acids, chasing cost and sustainability advantages. Patent filings underscore the race with methodologies that achieve near-total humic extraction and co-generate methane could redefine feedstock economics if scaled before 2030.

Quality assurance is evolving into a competitive lever. Brands investing in independent ISO 17025 lab certification and transparent UV-Vis assays are winning distribution through ag-retail networks that focus on ESG compliance. Conversely, firms peddling overstated fulvic claims risk delisting as state regulators align with Association of American Plant Food Control Officials (AAPFCO) definitions. Market participants are therefore prioritizing assay standardization, QR-coded lot tracing, and documented field trials to defend shelf space.

United States Humate Industry Leaders

The Andersons Inc.

Humintech GmbH

HGS BioScience, Inc.

Black Earth Humic LP (WestMET Group)

Faust Bio-Agricultural Services, Inc (BioAg)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: HGS BioScience secured USD 30 million in financing from Crown Partners to expand its humate powder and granule manufacturing operations across 6 North American plants serving over 20 countries.

- October 2024: The Biden-Harris administration made up to USD 7.7 billion available for climate-smart practices on agricultural lands, including USD 5.7 billion from the Inflation Reduction Act specifically targeting conservation practices that incorporate soil carbon amendments like humates.

- February 2024: Bio Huma Netics Inc. finalized its acquisition of Gro-Power Inc., broadening its product mix to include humate-rich composts and specialized soil conditioners.

United States Humate Market Report Scope

| Powder and Granular |

| Liquid |

| Humic Acid |

| Potassium Humate |

| Fulvic Acid |

| Agriculture |

| Animal Feed Additives |

| Environmental Remediation |

| Leonardite |

| Peat |

| Lignite |

| By Form | Powder and Granular |

| Liquid | |

| By Product Type | Humic Acid |

| Potassium Humate | |

| Fulvic Acid | |

| By Application | Agriculture |

| Animal Feed Additives | |

| Environmental Remediation | |

| By Source Material | Leonardite |

| Peat | |

| Lignite |

Key Questions Answered in the Report

What is the current size and growth outlook for the US humate market?

The humate market size is USD 210 million in 2025 and is forecast to reach USD 297.4 million by 2030, reflecting a 7.2% CAGR.

Which form of humate is gaining popularity fastest?

Liquid humate formulations are expanding at an 11.5% CAGR because fertigation and controlled-environment systems value precise dosing and rapid plant uptake.

How are carbon-credit programs influencing humate adoption?

Growers integrating humate applications into carbon-sequestration practices can earn verified credits, turning soil amendments from cost centers into revenue streams.

Why is leonardite the leading raw material?

Leonardite contains high humic-acid concentrations and benefits from established mining infrastructure in North Dakota, Wyoming, and New Mexico, delivering consistent quality and scale economies.

What regulatory trends favor humate usage?

Nutrient-runoff mandates, USDA conservation incentives, and state soil-health grants all encourage humate deployment by subsidizing or reimbursing compliant practices.

Which non-agricultural segments offer growth potential?

Animal feed additives and environmental remediation both show double-digit CAGRs owing to humic acids gut-health support and pollutant-binding properties, respectively.

Page last updated on: