Potassium Humate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.30 Billion |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

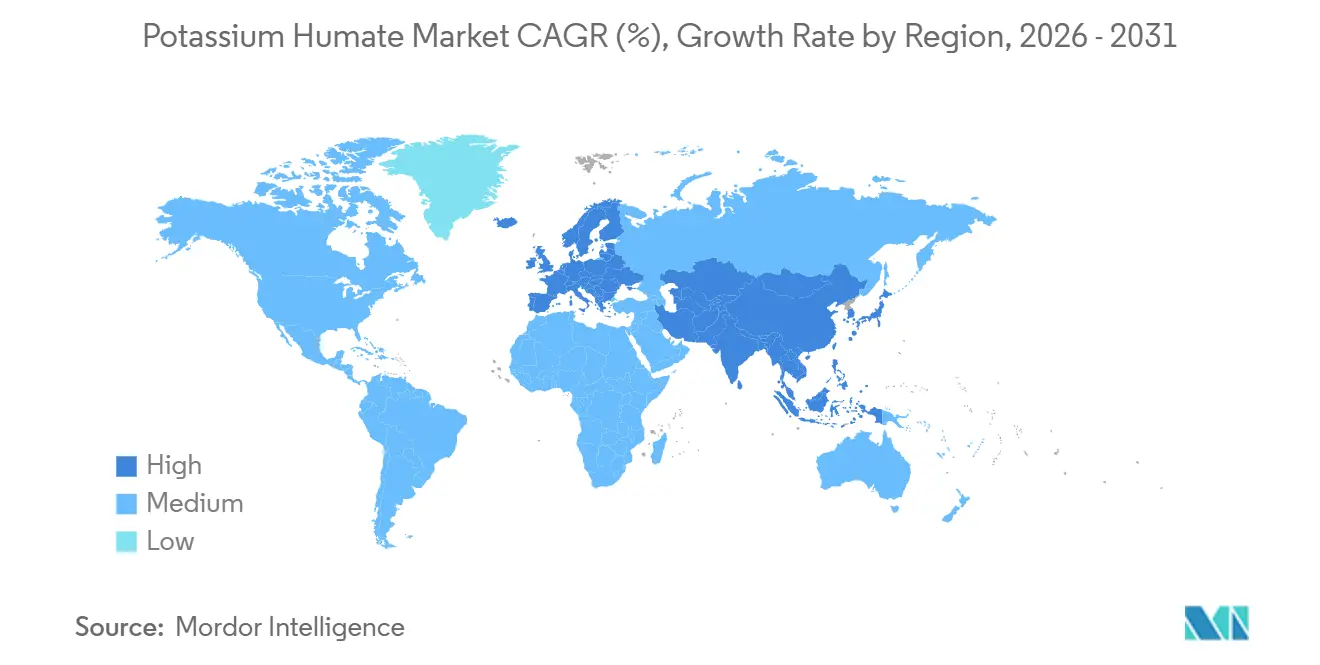

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

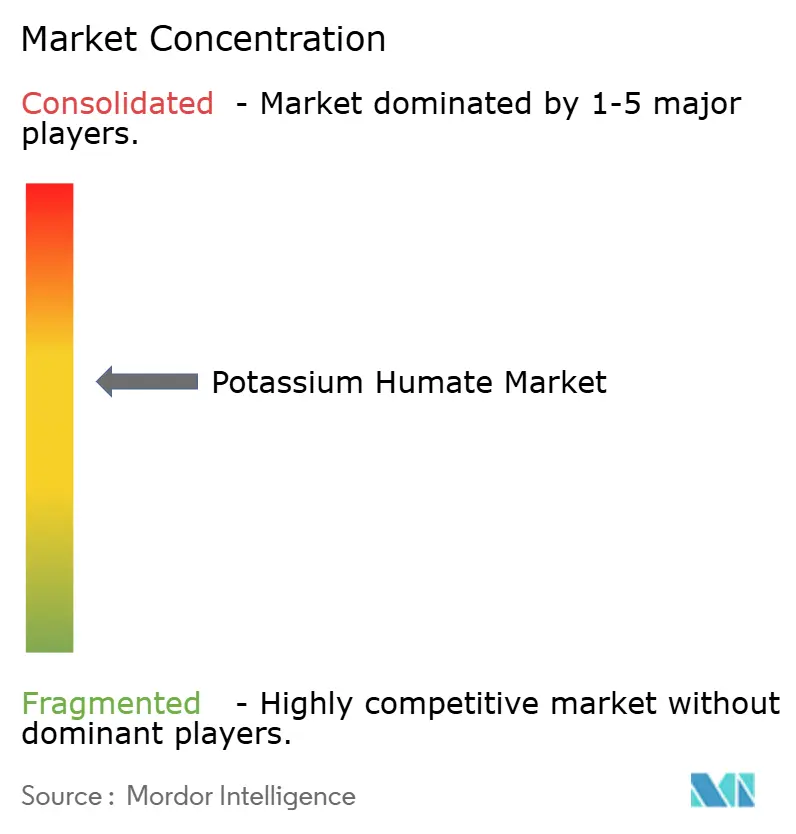

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Potassium Humate Market Analysis by Mordor Intelligence

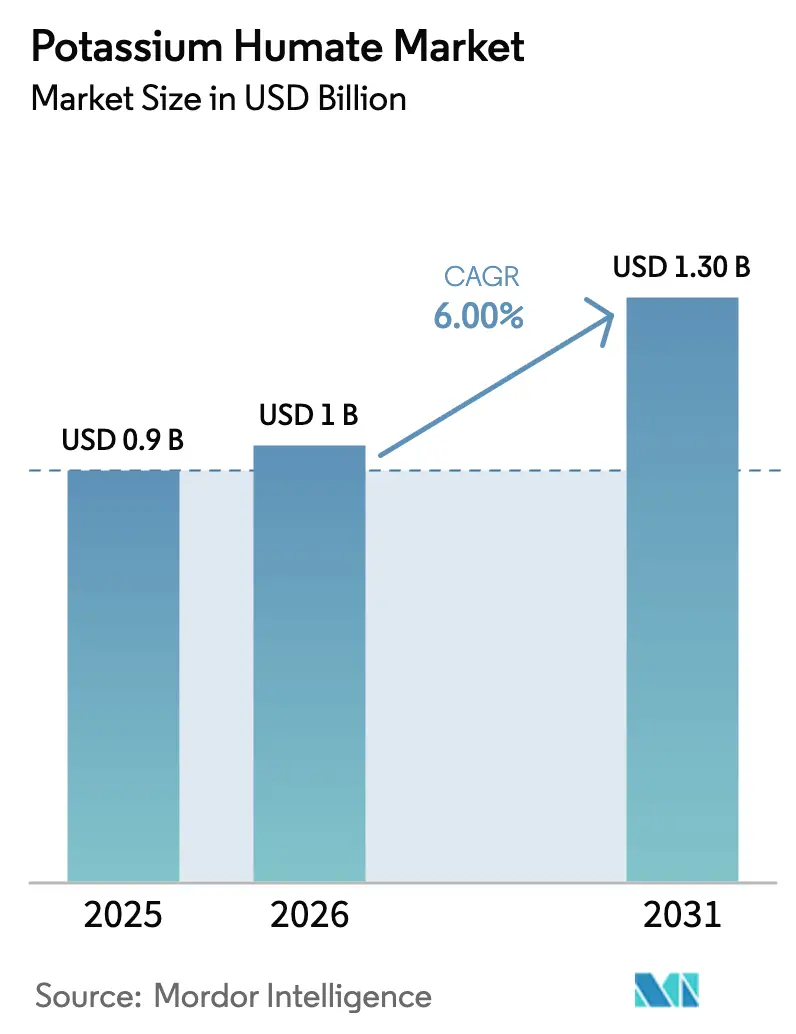

The potassium humate market size was valued at USD 0.9 billion in 2025 and is estimated to grow from USD 1.0 billion in 2026 to USD 1.3 billion by 2031, at a CAGR of 6.0% during the forecast period (2026-2031). This growth is driven by the increasing adoption of soil-health inputs, which help growers comply with stricter nitrogen runoff regulations while leveraging soil carbon revenue opportunities. The demand for biological soil conditioners is rising as regulatory bodies enforce stricter nutrient runoff limits, and farmers seek cost-effective solutions to enhance nitrogen use efficiency. Investments in leonardite extraction and advancements in liquid formulations are reducing production costs and increasing the market's addressable acreage. Despite supply chain vulnerabilities related to raw material concentration and freight disruptions, the expansion of global organic farmland and the adoption of precision drip irrigation systems are unlocking additional market potential. The competitive landscape is moderately concentrated, with the top five suppliers accounting for slightly over half of global revenue. This has led to ongoing consolidation and research and development partnerships, particularly in controlled-release coatings and fertigation blends.

Key Report Takeaways

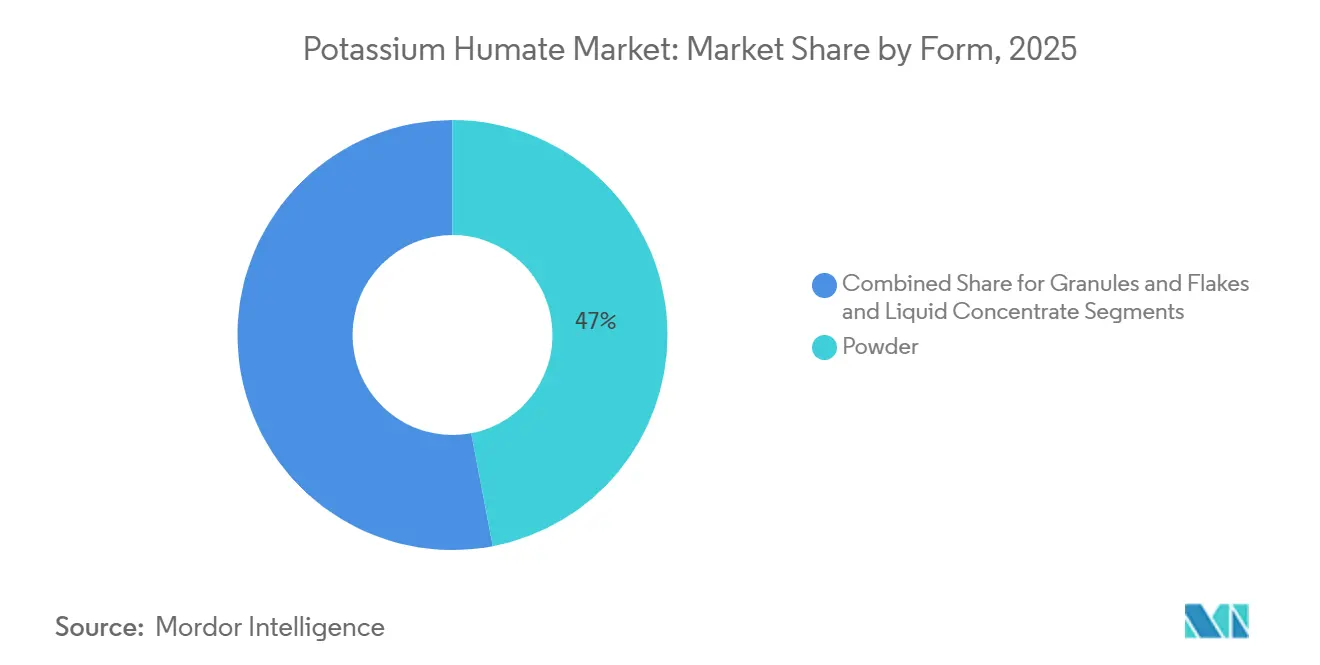

- By form, powder held the largest segment, 47% of the potassium humate market size in 2025, while liquid concentrate is the fastest-growing, forecast to expand at a 12.4% CAGR through 2026-2031.

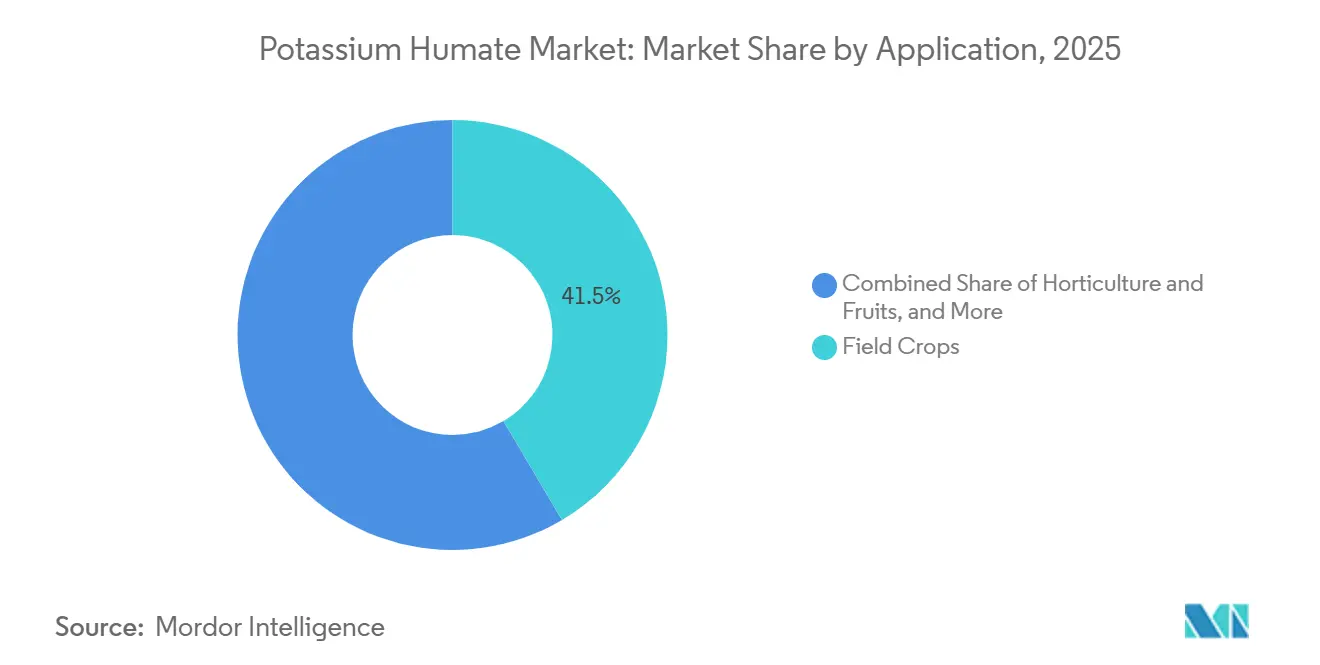

- By application, field crops accounted for the largest share at 41.5% of the potassium humate market size in 2025, while hydroponics and greenhouse are the fastest-growing, advancing at a 13.8% CAGR to 2026-2031.

- By geography, Europe led the potassium humate market size with 34% market share in 2025, while Asia-Pacific is the fastest-growing, projected to grow at a 11.9% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Potassium Humate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable agricultural inputs | +1.2% | Europe Union and North America with global spillover | Medium term (2-4 years) |

| Increasing global organic-farming acreage | +1.0% | Asia-Pacific and Europe | Long term (≥ 4 years) |

| Regulatory push to reduce chemical-fertilizer use | +1.3% | Europe Union core and North America | Medium term (2-4 years) |

| Growing use of water-soluble fertilizers in drip irrigation | +0.9% | Asia-Pacific and arid regions | Short term (≤ 2 years) |

| Carbon-credit monetization for humate-amended soils | +0.7% | North America and Europe Union pilots | Long term (≥ 4 years) |

| Patent cliff for polymer-coated urea enabling humate integration | +0.6% | North America, China and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Agricultural Inputs

Corporate sustainability mandates are shifting procurement budgets away from synthetic-only fertilizers toward soil conditioners that reduce nitrogen dependence. The European Farm to Fork strategy aims for a 20% reduction in fertilizer use by 2030, a target that is pushing growers toward humate blends, which improve nutrient-use efficiency without harming yields[1]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu. Potassium humate aids carbon sequestration by enhancing soil organic matter and promoting microbial activity, aligning with corporate Scope 3 emission-reduction goals. Major agribusinesses and food companies are increasingly adopting regenerative agriculture inputs, thereby increasing the appeal of humate-based products in sustainable sourcing initiatives.

Increasing Global Organic-Farming Acreage

According to FiBL statistics, certified organic cropland reached 98.9 million hectares in 2023, adding 2.6% year on year[2]Source: Research Institute of Organic Agriculture FiBL, “Organic Agriculture Worldwide: Current Statistics,” FiBL Statistics, fibl.org. Europe leads by land area, but Asia-Pacific adds producers the fastest, reflecting smallholder conversions in India, China, and Indonesia. Spain alone manages 2.99 million hectares under organic rules, although humate uptake is still higher in intensive vegetable systems than in broad-acre cereals. Because potassium humate is mined from naturally occurring leonardite and undergoes minimal processing, it qualifies for organic input lists worldwide. Its main competition is on-farm compost, where feedstocks are abundant, and labor is cheap, yet humate wins where clean drip systems and fast nutrient release are critical.

Regulatory Push to Reduce Chemical-Fertilizer Use

The European Union Nitrates Directive caps manure nitrogen at 170 kg per hectare yearly, while the February 2026 Recovered Nitrogen from Manure (RENURE) rules reward processed organic fertilizers that meet stricter safety limits. Humate-coated nitrogen blends let greenhouse tomato and cucumber growers stay within those nitrogen budgets while still reaching target yields. In the United States, nutrient pollution carries a high annual cost in water treatment and lost fisheries, so several states now reward precision-nutrient plans that rely on controlled-release humate coatings. These converging rules and costs push demand upward in every major farming region.

Growing Use of Water-Soluble Fertilizers in Drip Irrigation

Micro-irrigation acreage keeps climbing in water-stressed belts. Liquid potassium humate dissolves below 3.0 dS per meter electrical-conductivity thresholds, so it fits neatly into fertigation programs. Saudi Arabia and the United Arab Emirates bankroll drip infrastructure to conserve groundwater, and African greenhouse adoption is following the same script. Because humate enhances nutrient uptake and does not clog emitters, its use rises in lockstep with new drip installations, accelerating growth in the Potassium humate market. Potassium humate improves soil structure, enhances water retention, and promotes microbial activity, which are especially beneficial in arid and semi-arid regions utilizing micro-irrigation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of high-grade humic substances | −0.8% | North America and Europe | Short term (≤ 2 years) |

| Competition from microbial biostimulants | −0.6% | South America and Asia-Pacific | Medium term (2-4 years) |

| Stringent heavy-metal limits on leonardite-derived inputs | −0.5% | European Union and North America | Medium term (2-4 years) |

| Environmental, Social, and Governance (ESG) scrutiny of leonardite strip-mining in sensitive peatlands | −0.3% | North America, and then the European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Microbial Biostimulants

Microbial biostimulants are increasingly influencing the potassium humate market by providing farmers with alternative solutions that improve soil fertility, nutrient uptake, and plant growth, often marketed with eco-friendly or bio-based attributes. This trend introduces substitution pressure, potentially decreasing the demand for potassium humate while also creating pricing challenges for producers. Some microbial blends achieve higher yields at lower application rates compared to humates, further intensifying price competition. Microbial products face limitations such as shorter shelf life and sensitivity to pH variations, issues that chemically stable humates do not encounter. To address this, suppliers are co-formulating humic acids with microbial products to retain customers. While this strategy may mitigate some of the competitive pressures, it does not fully eliminate the challenges faced by the potassium humate market.

Environmental, Social, and Governance (ESG) Scrutiny of Leonardite Strip-Mining in Sensitive Peatlands

Surface mining can disturb peat hydrology and release stored carbon. Investors aligned with Science Based Targets now request third-party audits of mining footprints before signing supply contracts. Areas such as Alberta’s boreal wetlands and North Dakota’s mixed lignite seams have drawn significant attention[3]Source: Alberta Geological Survey, “Leonardite Resources,” ags.aer.ca. Compliance documentation raises project lead times and can divert investment toward less sensitive deposits or alternative humic sources. Although the impact is gradual, it is a credible drag on long-run growth for the Potassium humate market. Stricter Environmental, Social, and Governance (ESG) regulations may increase operational costs due to the need for enhanced monitoring, reporting, and mitigation measures, thereby reducing overall project profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Concentrates Gain Share in Precision Systems

Powder held the largest segment, 47% of the potassium humate market share in 2025, reflecting its fit with automated fertigation that now commands protected-crop production. This dominance is attributed to its versatility, extended shelf life, and ease of transportation. Farmers often prefer powdered potassium humate for large-scale field applications due to its ability to blend with other solid fertilizers and ensure uniform distribution across extensive farmland. Additionally, powdered forms are generally more cost-effective per metric ton, making them a practical choice for traditional soil amendment practices in key agricultural regions.

Liquid concentrate is the fastest-growing, forecast to expand at a 12.4% CAGR through 2026-2031. This growth is driven by the increasing adoption of precision agriculture techniques, such as fertigation and foliar spraying, which enable more targeted and efficient nutrient delivery. Liquid concentrates are particularly favored for high-value crops, greenhouse systems, and hydroponic setups due to their compatibility with automated irrigation systems and their ability to facilitate faster nutrient uptake.

By Application: Hydroponics Surges, Field Crops Anchor Volume

Field crops accounted for the largest share at 41.5% of the potassium humate market size in 2025, especially in American corn and soy belts, where humate-coated urea eases nitrogen caps. This is primarily due to the extensive cultivation of cereals, grains, and staple crops that benefit from potassium humate’s properties, including improved soil structure, enhanced water retention, and increased nutrient absorption. The large-scale cultivation of field crops and the focus on maximizing yields make this segment a stable and significant revenue source for potassium humate suppliers.

Hydroponics and greenhouses are the fastest-growing, advancing at a 13.8% CAGR to 2026-2031. Spain's citrus groves and India's vegetable belts aim to capitalize on organic premiums. This growth is driven by the rising adoption of controlled-environment agriculture, which emphasizes precise nutrient management to optimize crop quality and yield. Potassium humate is widely used in hydroponic solutions to enhance root development and nutrient uptake efficiency, making it a preferred additive in soilless systems and greenhouse setups where rapid plant growth is essential.

Geography Analysis

Europe led the potassium humate market size with 34% in 2025, this regional leadership is supported by a well-established agricultural infrastructure, high awareness of sustainable soil management practices, and regulatory frameworks that encourage the use of soil conditioners and specialty fertilizers. European farmers increasingly utilize potassium humate to improve soil fertility, boost crop productivity, and comply with soil health standards, ensuring steady demand in the region.

Asia-Pacific is the fastest-growing, projected to grow at a 11.9% CAGR through 2026-2031, this growth is driven by the rapid modernization of agriculture, increased adoption of high-efficiency fertilizers, and the need to enhance crop yields to meet the demands of growing populations. Investments in precision agriculture, greenhouse farming, and improved nutrient management practices across the region are driving rising demand for both powdered and liquid potassium humate products.

North America delivers the significant regional growth driven by carbon-credit payments, expanding greenhouse acreage, and patent-protected products such as HumiK ONE, creating a robust demand stack. South America expands, driven by Brazil’s dependency on imported nutrients and Argentina’s efforts to localize bioinput production. Domestic humate suppliers that integrate mining into blending can tap into rising import duties on finished fertilizers. Africa grows from a low base, powered by nascent greenhouse clusters in South Africa, Kenya and Egypt along with drip infrastructure subsidized by governments.

Competitive Landscape

The potassium humate market remains moderate, with the top five players including HGS BioScience (Paine Schwartz Partners, LLC), Humintech GmbH, Nutri-Tech Solutions Pty Ltd, Omnia Specialties, and Jing Feng Humic Acid accounting for a significant share of revenue in 2025. Geographic expansion strategies are primarily influenced by proximity to leonardite sources and regulatory considerations.

Market strategies focus on three key areas. The first is vertical integration to mitigate risks associated with oil price volatility. The second involves mergers, acquisitions, or partnerships that provide immediate access to grower networks or specialized technologies. The third strategy emphasizes service bundling, including remote sensing, soil testing, and carbon-credit documentation, to offer differentiation beyond product chemistry. Opportunities remain in Africa's greenhouse expansion, South America's import substitution efforts, and North America's scaling of controlled-environment agriculture, ensuring growth potential for both major players and agile regional competitors in the potassium humate market.

Collaborations with universities and agritech start-ups are prevalent, targeting advancements in controlled-release coatings, microencapsulation, and data-driven application models to address gaps in efficacy data. Patent activity has increased, focusing on solvent-free extraction methods and bio-based polymers that enhance humic purity while reducing environmental impact. Marketing efforts are increasingly centered on carbon sequestration and yield stability, positioning humic inputs as climate-smart solutions rather than traditional soil conditioners.

Potassium Humate Industry Leaders

HGS BioScience (Paine Schwartz Partners, LLC)

Humintech GmbH

Nutri-Tech Solutions Pty Ltd

Omnia Specialities

Jing Feng Humic Acid

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: A 3-year study (2021–2023) in Kazakhstan showed that foliar potassium humate combined with N-rich humic acid fertilizers enhanced potato yield by ~20%, increased starch content, and improved nutrient uptake. This aligns with the growing adoption of potassium humate in integrated nutrient management programs in Eastern Europe and Central Asia.

- August 2024: In foxtail millet trials, the application of foliar potassium humate at a rate of 80 kg/ha increased the photosynthetic rate by approximately 13%, resulting in a 12.7% yield improvement. This demonstrates the role of potassium humate in enhancing photosynthetic efficiency and crop performance, further validating its use in various crop applications to achieve higher yields and better resource utilization.

- February 2024: Huma's acquisition of Gro-Power has expanded its product portfolio to include granular humic fertilizers, such as potassium humate, while also enhancing its field support capabilities. This strategic move strengthens Huma's position in the market by offering a broader range of solutions and providing improved support to farmers, enabling them to adopt advanced nutrient management practices effectively.

Global Potassium Humate Market Report Scope

Potassium humate is a water-soluble potassium salt primarily sourced from leonardite or oxidized lignite. In agriculture, it serves as a soil conditioner and plant growth enhancer by improving soil structure, enhancing water retention, and promoting nutrient uptake. The potassium humate market report is segmented by form (powder, granules/flakes, liquid concentrate), by application (field crops, horticulture and fruits, and hydroponics and greenhouse), and by geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Powder |

| Granules/Flakes |

| Liquid Concentrate |

| Field Crops |

| Horticulture and Fruits |

| Hydroponics and Greenhouse |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Form | Powder | |

| Granules/Flakes | ||

| Liquid Concentrate | ||

| By Application | Field Crops | |

| Horticulture and Fruits | ||

| Hydroponics and Greenhouse | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the potassium humate market in 2025?

The Potassium humate market size reached USD 0.9 million in 2026 and is projected to hit USD 1.0 million by 2031 at a 6.0% CAGR.

What is driving demand for potassium humate in Asia-Pacific?

Government incentives for organic farming, rapid drip-irrigation adoption, and strong growth in controlled-environment agriculture are lifting regional consumption at an 11.9% CAGR.

Which format is growing fastest in the potassium humate market?

Liquid concentrate is the fastest-growing format, expanding at a 12.4% CAGR because it integrates easily with fertigation and precision-irrigation systems.

Why are humic products attractive for organic growers?

Humic acids are allowed under organic certification rules and improve nutrient-use efficiency and soil carbon, aligning with both compliance and yield goals.

Page last updated on: