Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

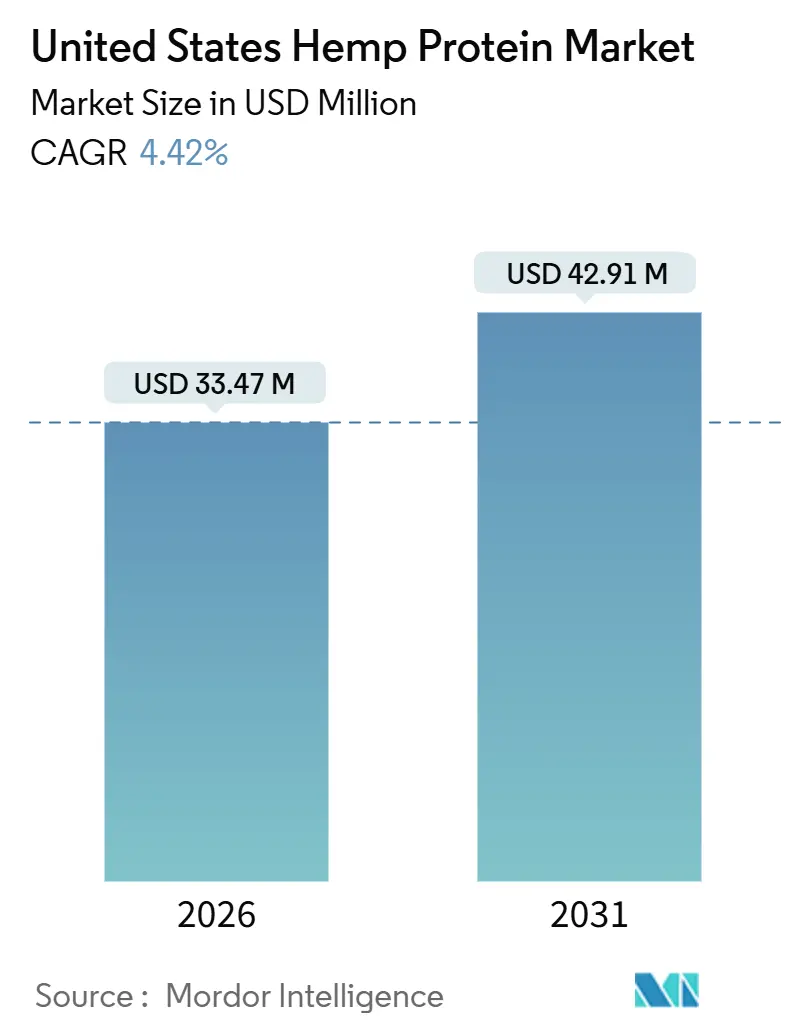

| Market Size (2026) | USD 33.47 Million |

| Market Size (2031) | USD 42.91 Million |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

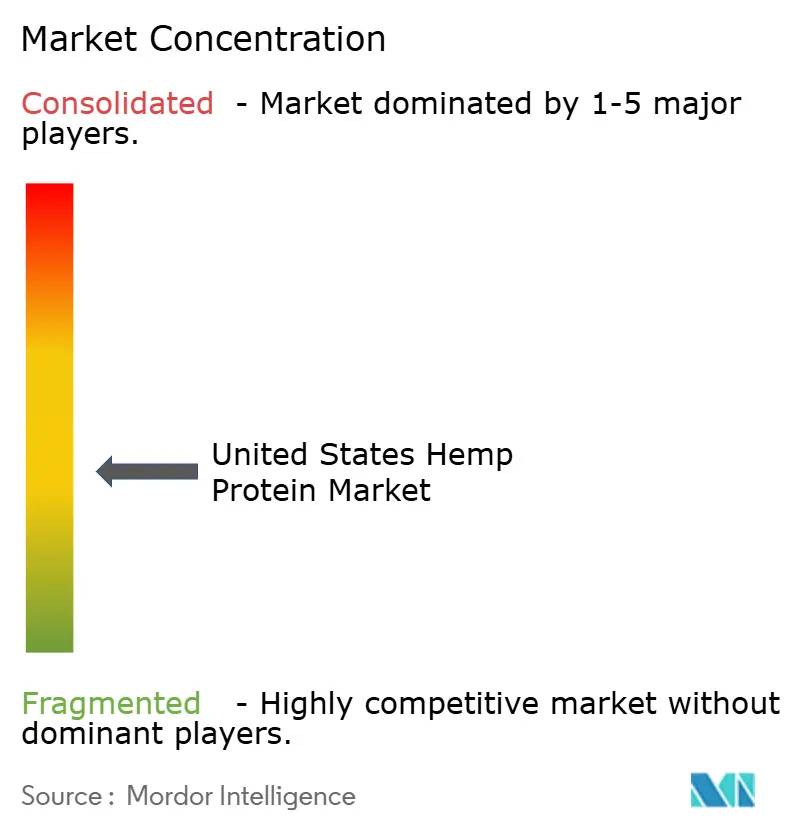

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hemp Protein Market Analysis by Mordor Intelligence

The United States hemp protein market is valued at USD 33.47 million in 2026 and is projected to reach USD 42.91 million by 2031, growing at a CAGR of 5.09% during the forecast period. This growth reflects rising consumer interest in plant-based, clean-label, and allergen-free protein sources. Hemp protein is increasingly used in sports nutrition, functional foods, dietary supplements, and ready-to-mix beverages, driven by its complete amino acid profile and sustainability credentials. Expanding vegan and flexitarian populations continue to support demand across food and nutrition segments. Food and beverage manufacturers are incorporating hemp protein into protein bars, powders, bakery products, and dairy alternatives to diversify offerings. Growth is further supported by improved hemp cultivation practices and product standardization. However, the market remains niche compared to soy and pea protein, limiting large-scale adoption.

Key Report Takeaways

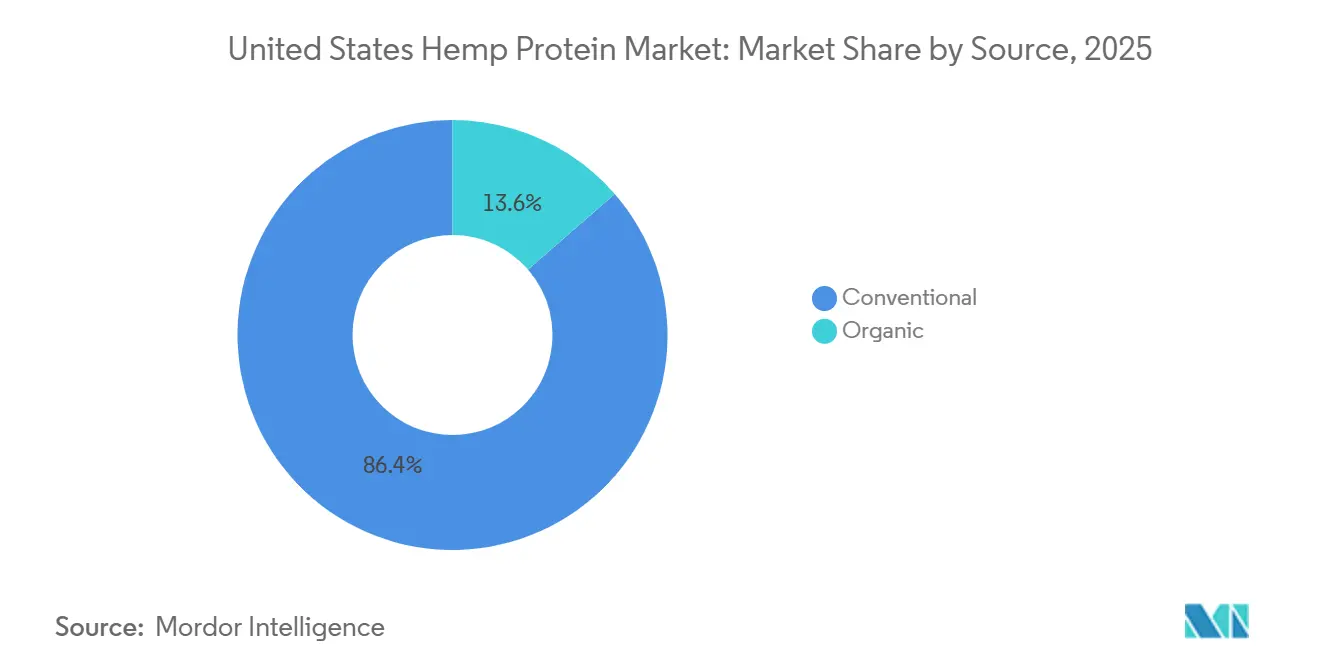

- By source, conventional formats held 86.38% of the United States hemp protein market share in 2025, while organic formats expanded at a 6.42% CAGR through 2031.

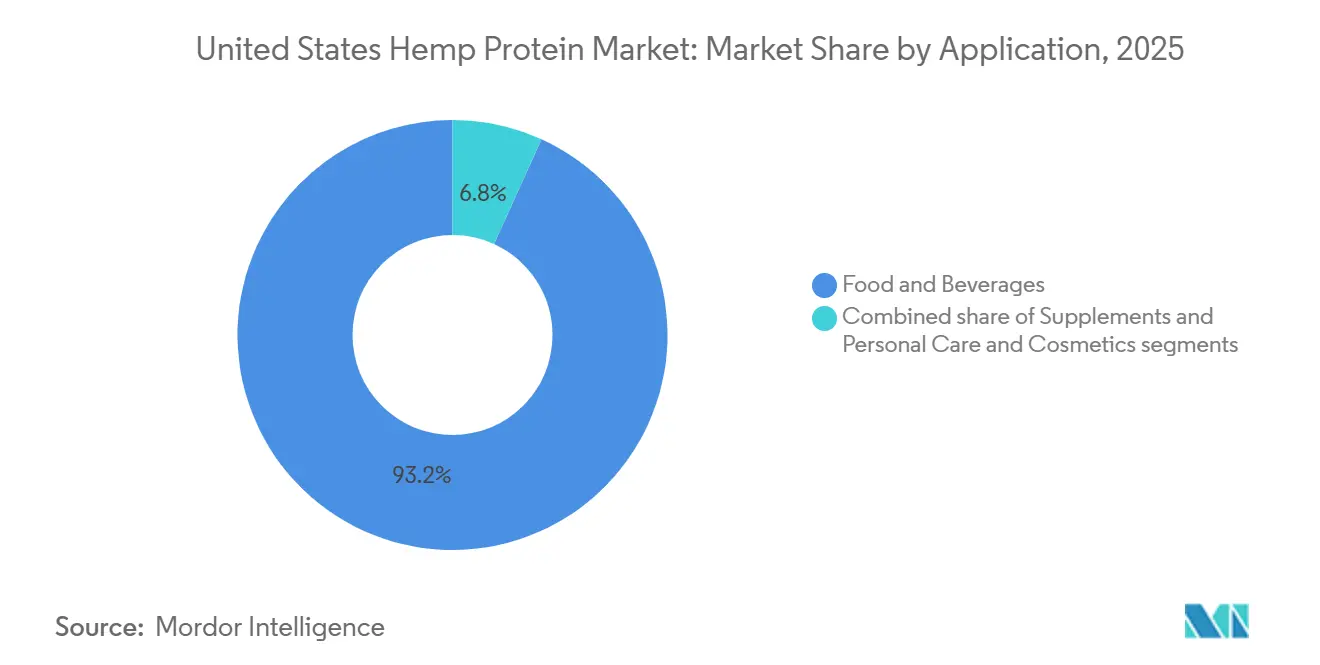

- By application, food and beverages accounted for 93.21% of the United States hemp protein market size in 2025; the supplements segment posted the fastest 6.89% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hemp Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for plant-based proteins | +1.2% | National, with concentration in West Coast and Northeast urban markets | Medium term (2-4 years) |

| Rising health and wellness awareness | +0.9% | National, strongest in metropolitan areas with high household income | Medium term (2-4 years) |

| Increased use in sports nutrition and fitness products | +0.8% | National, with early adoption in CrossFit and endurance athlete communities | Short term (≤ 2 years) |

| Expansion of vegan and vegetarian diets | +0.7% | National, led by Gen Z and Millennial demographics | Long term (≥ 4 years) |

| Rising interest in sustainable and eco-friendly ingredients | +0.6% | National, with premium positioning in coastal and college-town markets | Long term (≥ 4 years) |

| Growth of functional foods and supplements | +0.5% | National, driven by aging Baby Boomer cohort and wellness-focused consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer demand for plant-based proteins

The growing consumer demand for plant-based proteins is driving the U.S. hemp protein market, fueled by increasing health awareness, sustainability concerns, and changing dietary preferences. Reflecting this trend, the Good Food Institute reported that in 2024, approximately 60% of U.S. households purchased some form of plant-based food, showcasing the widespread adoption of plant-based diets beyond vegetarians and vegans[1]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry”, gfi.org. Consumers are actively seeking protein sources that are both nutritious and environmentally friendly, making hemp protein a popular choice due to its complete amino acid profile, high fiber content, and clean-label appeal. The rise of plant-based lifestyles across foodservice, retail, and direct-to-consumer channels further supports market growth. Additionally, hemp protein aligns with functional food trends, offering benefits such as muscle support, weight management, and gut health.

Rising health and wellness awareness

Consumers in the United States are increasingly prioritizing health and wellness, especially when it comes to protein intake, driving the hemp protein market. In 2024, 54% of U.S. adults surveyed emphasized protein content in their packaged food choices, a notable rise from 41% in 2020[2]Source: International Food Information Council, “2024 IFIC Food & Health SURVEY”, ific.org. This trend underscores a heightened awareness of protein's role in satiety, metabolic health, and muscle maintenance. As consumers become more educated about protein's dietary significance, there's a marked surge in demand for nutrient-dense, functional foods. Hemp protein stands out in this landscape, boasting a complete amino acid profile, high fiber content, and plant-based origins. As consumers seek products that bolster energy, aid recovery, and promote overall wellness, hemp protein emerges as a compelling alternative to conventional protein sources. This momentum is further fueled by a growing preference for clean-label and sustainable ingredients, solidifying hemp protein's position in the burgeoning plant-based protein market.

Increased use in sports nutrition and fitness products

In the U.S., the hemp protein market is surging, largely due to its rising popularity in sports nutrition and fitness products. This trend aligns with the nation's heightened emphasis on physical health and active living. By 2024, the U.S. boasted 77 million fitness club memberships, underscoring a vast audience eager for nutrition that boosts performance and aids recovery[3]Source: Health and Fitness Association, “How 77 Million Fitness Members Work Out: New HFA Data Reveals Shifting Equipment, Training, and Membership Trends”, healthandfitness.org. Hemp protein, celebrated for its complete amino acid profile and superior digestibility, is finding its way into protein powders, bars, and ready-to-drink shakes, all tailored for athletes and fitness buffs. Brands are capitalizing on hemp's plant-based, clean-label allure, catering to the growing demand for sustainable and functional protein. As consumers gravitate towards hemp protein for muscle upkeep, post-workout recovery, and holistic wellness, it emerges as a favored substitute for traditional animal-based proteins.

Expansion of vegan and vegetarian diets

The expansion of vegan and vegetarian diets is a prominent driver of the U.S. hemp protein market, reflecting a broader shift toward plant-based nutrition. Increasing numbers of consumers are adopting vegetarian or fully vegan lifestyles for health, ethical, and environmental reasons, creating strong demand for alternative protein sources. Hemp protein, with its complete amino acid profile, high fiber content, and clean-label positioning, serves as an ideal plant-based protein option. Retailers and foodservice providers are increasingly incorporating hemp protein into snacks, beverages, meal replacements, and protein supplements to cater to this growing demographic. Rising awareness of the environmental impact of animal-based proteins further supports its adoption, as consumers prioritize sustainable and nutrient-dense alternatives. This trend underscores the increasing integration of health, sustainability, and dietary preferences in shaping consumer choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty around hemp processing and labeling | -0.8% | National, with state-level variations in enforcement | Short term (≤ 2 years) |

| Limited consumer awareness compared to other plant proteins | -0.6% | National, most acute in Midwest and Southern states | Medium term (2-4 years) |

| Supply constraints of quality hemp biomass | -0.5% | National, concentrated in states with nascent hemp programs | Short term (≤ 2 years) |

| Taste and flavor profile limitations | -0.4% | National, affecting mainstream adoption across all demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory uncertainty around hemp processing and labeling

Ongoing regulatory uncertainties surrounding hemp processing and labeling pose a significant challenge to the U.S. hemp protein market. While the 2018 Farm Bill federally legalized hemp, state-level regulations and shifting FDA guidelines present compliance hurdles for manufacturers. Companies grapple with intricate rules on THC content limits, product labeling, and marketing claims, often leading to delayed product launches and heightened operational costs. These inconsistent state regulations further complicate interstate distribution and scaling efforts, stifling market expansion. Such uncertainties can dampen investor confidence and deter new entrants, especially smaller producers. Moreover, stringent testing and documentation requirements to ensure compliance extend production timelines and inflate costs.

Supply constraints of quality hemp biomass

Supply constraints of quality hemp biomass are a major restraint on the U.S. hemp protein market, limiting consistent production and scalability. Producing functional hemp protein powders requires high-quality hemp that's rich in protein and low in THC. However, cultivation faces challenges from climate variability, limited arable land, and the need for agricultural expertise. Inconsistent yields and variations in protein content can disrupt manufacturing and compromise product quality, posing challenges for producers of all sizes. Moreover, as the hemp cultivation sector in the U.S. is still maturing, it experiences seasonal supply fluctuations and elevated raw material costs. These challenges impede companies' abilities to reliably meet the surging consumer demand for plant-based protein products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Conventional Dominance Reflects Cost Sensitivity

Conventional hemp protein formats accounted for 86.38% of the United States hemp protein market in 2025, making them the clear mainstream choice among manufacturers and consumers. Their dominance reflects broad availability, established supply chains, and generally lower price points compared with organic alternatives. Conventional products are widely used in applications such as bakery mixes, smoothies, ready-to-drink beverages, and nutrition bars where cost competitiveness is critical. Many large-format retailers and mass brands still prioritize conventional sourcing to keep product pricing accessible. In addition, long-standing vendor relationships and certified processing infrastructure for conventional hemp protein reinforce its entrenched position.

Organic hemp protein, while smaller in absolute share today, is emerging as the fastest-growing format in the United States hemp protein market, with a projected CAGR of 6.42% during the forecast period (2026-2031). This growth is closely tied to rising consumer interest in clean-label, sustainably produced, and pesticide-free plant proteins. Health-conscious shoppers increasingly seek organic certifications as a shorthand for higher perceived quality and environmental responsibility. Brands targeting premium wellness, sports nutrition, and specialty retail channels are therefore leaning more heavily on organic hemp protein in their formulations. The format is also benefiting from broader momentum in organic food and beverages, where cross-category shoppers often trade up across multiple product types.

By Application: Food and Beverages Lead, Supplements Accelerate

Food and beverages accounted for 93.21% of the United States hemp protein market in 2025, making this the overwhelmingly dominant application segment. In this space, hemp protein is primarily used as a functional ingredient that enhances nutrition, texture, and binding rather than serving as the hero component on the label. It is widely incorporated into bakery goods, including breads, muffins, and bars, where it boosts protein content while contributing to structure. Snacks such as chips, crackers, and granola blends also leverage hemp protein to align with high-protein and better-for-you positioning. In plant-based beverages, hemp protein helps support the growth of dairy alternatives and fortified drinks aimed at flexitarian and vegan consumers.

Supplements, while representing only 6.79% of the United States hemp protein market in 2025, are set to grow the fastest, with a projected CAGR of 6.89% through 2031. This acceleration is closely linked to the expansion of sports nutrition products that incorporate hemp protein into powders, blends, and ready-to-drink shakes. Athletes and active consumers are increasingly interested in plant-based protein options that complement or replace traditional dairy-derived ingredients. The segment is also supported by elderly and medical nutrition products, where hemp protein can contribute to muscle maintenance, satiety, and overall protein intake. These specialized formulations frequently emphasize digestibility, amino acid profile, and alignment with broader wellness trends.

Geography Analysis

The United States hemp protein market is shaped by regions with favorable hemp cultivation conditions and supportive regulatory frameworks. States such as Colorado, Kentucky, Montana, Oregon, and North Dakota have emerged as key production hubs due to early adoption of hemp farming, suitable climate, and established agricultural infrastructure. These states benefit from proximity to raw hemp seed supply, enabling efficient processing into hemp protein powders and ingredients. Localized processing facilities help reduce logistics costs and improve supply chain efficiency. Strong farmer participation and state-level support programs further encourage production growth.

On the demand side, consumption of hemp protein is concentrated in health-conscious and urbanized regions, particularly the West Coast, Northeast, and parts of the Midwest. California, Washington, New York, and Massachusetts show higher uptake due to strong presence of vegan, organic, and functional food markets. These regions host a large number of natural food retailers, supplement brands, and sports nutrition companies that actively incorporate hemp protein into product formulations. Consumer awareness around plant-based nutrition and sustainability is notably higher in these markets.

The Midwest serves as a strategic processing and distribution corridor, supporting nationwide shipments. Companies are increasingly locating facilities near cultivation zones to ensure traceability and quality control. Regulatory clarity at the federal level has encouraged interstate trade, although state-level variations still influence expansion strategies. Overall, the United States hemp protein market’s geography reflects a balance between cultivation-focused states and consumption-driven metropolitan regions, supporting steady national growth.

Competitive Landscape

The United States hemp protein market exhibits moderate fragmentation, with a mix of established natural ingredient suppliers, niche plant-based brands, and emerging specialty processors. Unlike highly consolidated markets, no single player dominates outright; instead, competition arises from a wide range of companies varying in size, product focus, and distribution reach. Larger natural food and supplement companies leverage broad portfolios and strong retail presence to drive hemp protein adoption, while smaller niche brands often differentiate through unique formulations, organic certification, or clean-label positioning. This structure encourages continuous innovation and diverse product offerings.

Product differentiation and branding play a significant role in shaping competition. Many players compete on quality attributes such as protein content, flavor profile, organic or non-GMO certification, and sustainability credentials. Hemp protein is incorporated into powders, bars, shakes, and blended plant protein mixes, and companies that tailor products to specific consumer segments such as athletes, vegans, or wellness-oriented buyers tend to build stronger loyalty. Strategic partnerships with retailers and increased visibility through e-commerce platforms also influence competitive positioning, allowing innovative brands to rapidly expand national footprint without heavy investment in traditional distribution channels.

Price sensitivity and cost positions further influence competitive dynamics. Hemp protein typically carries a premium price relative to more established plant proteins like soy and pea, prompting companies to optimize production and sourcing efficiencies to remain competitive. At the same time, newcomers often enter the market with niche or value-added propositions such as flavored products, blended formulas, or functional enhancements (e.g., probiotics). Regulatory developments around hemp cultivation and processing standards also impact competition, as firms that can ensure compliance and consistent quality gain an advantage.

United States Hemp Protein Industry Leaders

Axiom Foods Inc.

ETChem Co.

Martin Bauer Group

Tilray Brands Inc.

NOW Foods LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Victory Hemp Foods unveiled North America's largest solvent-free processing line, dedicated to hemp heart protein (V-70) and oil (V-ONE), in Carrollton, Kentucky. Leveraging patented technology, this facility is poised to cater to the surging demand for allergen-free, nutrient-rich, and sustainable plant-based ingredients across the food, beverage, and cosmetics sectors.

- August 2024: Victory Hemp Foods completed an USD 2.5 million expansion of its Kentucky facility in Carroll County, adding 22 jobs and increasing production capacity by 40%. The project received support from the Kentucky Agricultural Development Board and positions the company to serve growing demand from bakery and snack manufacturers.

- April 2024: Panda Biotech launched commercial operations at its massive Panda Hemp Gin industrial hemp processing facility in Wichita Falls, Texas. Spanning about 500,000 square feet, it’s now the largest hemp processing plant in the Western Hemisphere, capable of processing around 10 metric tons of hemp per hour.

United States Hemp Protein Market Report Scope

United States hemp protein market is segmented by source into organic and conventional;by application into functional food, functional beverage, dietary supplements, pharmaceutical, personal care and other industrial uses.

By Source

| Organic |

| Conventional |

By Application

| Food and Beverages | Bakery |

| Snacks | |

| Confectionery | |

| Beverages | |

| Others | |

| Supplements | Sports/Performance Nutrition |

| Elderly Nutrition and Medical Nutrion | |

| Personal Care and Cosmetics |

| By Source | Organic | |

| Conventional | ||

| By Application | Food and Beverages | Bakery |

| Snacks | ||

| Confectionery | ||

| Beverages | ||

| Others | ||

| Supplements | Sports/Performance Nutrition | |

| Elderly Nutrition and Medical Nutrion | ||

| Personal Care and Cosmetics | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms