Market Overview

| Study Period | 2021 - 2031 |

|---|---|

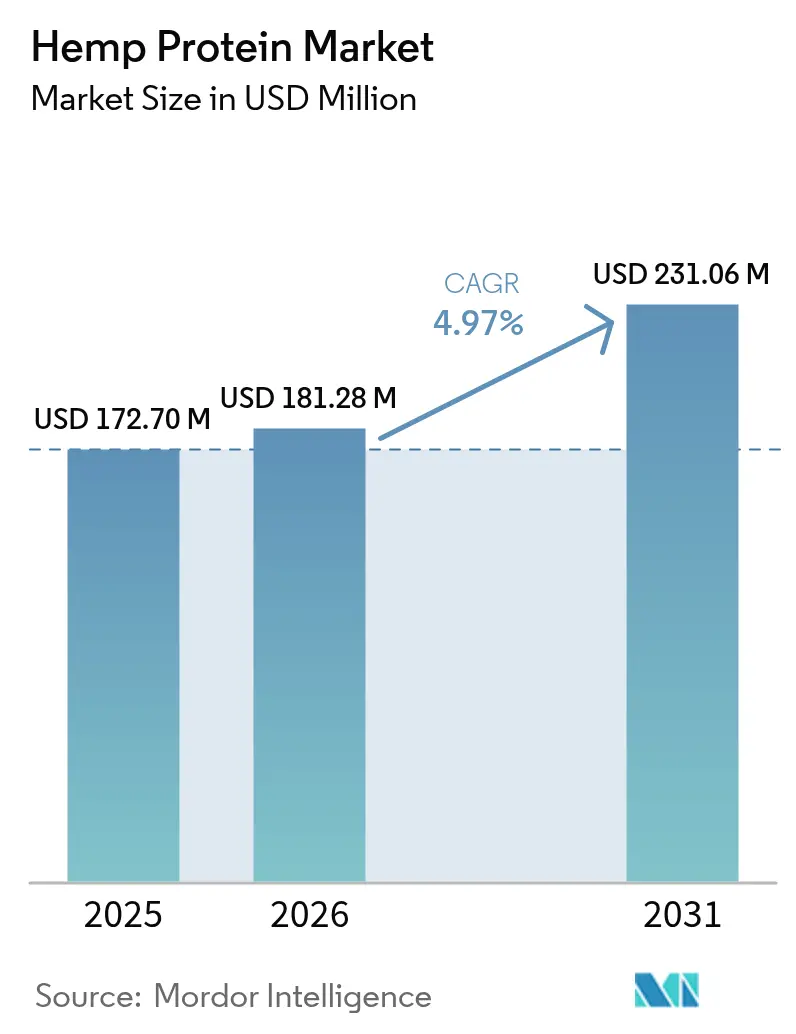

| Market Size (2026) | USD 181.28 Million |

| Market Size (2031) | USD 231.06 Million |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hemp Protein Market Analysis by Mordor Intelligence

The hemp protein market size is expected to grow from USD 172.70 million in 2025 to USD 181.28 million in 2026 and is forecast to reach USD 231.06 million by 2031 at 4.97% CAGR over 2026-2031. This growth trajectory highlights the significant evolution of hemp protein from a niche supplement to a widely recognized and mainstream source of complete, plant-based protein. The increasing demand for hemp protein is primarily driven by several factors, including the removal of cultivation restrictions by national regulatory authorities, the expansion of vegan product portfolios by sports-nutrition brands, and the growing consumer emphasis on sustainable sourcing as a critical factor in purchasing decisions. The market's resilience is underpinned by key regional developments, such as North America's liberalized agricultural policies, Europe's stringent eco-design mandates, and Asia-Pacific's advanced agronomic expertise, which collectively contribute to the robust growth of the hemp protein market. Additionally, the competitive landscape remains highly dynamic, shaped by ongoing market consolidation, the strategic advantages of early adoption of organic certifications, and continuous advancements in functional ingredient innovation. These factors are expected to drive further opportunities and challenges within the market, ensuring its sustained growth and evolution over the forecast period.

Key Report Takeaways

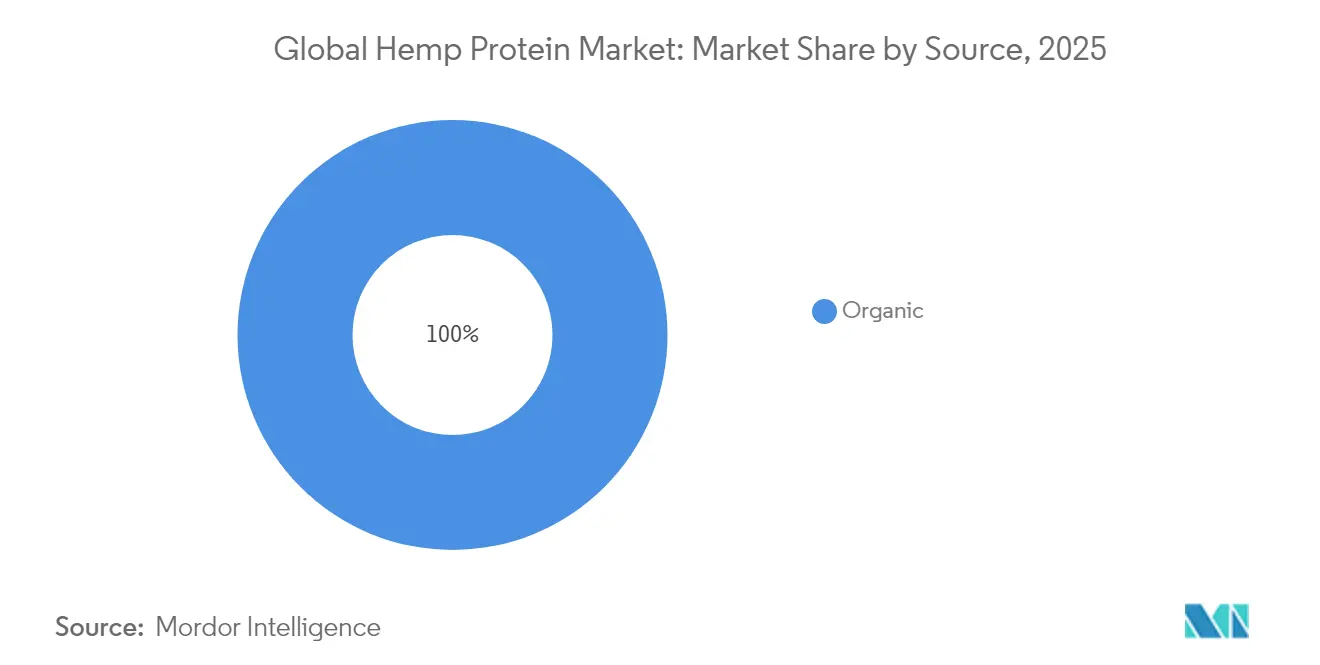

- By source, conventional formats retained 83.35% of the hemp protein market share in 2025, yet organic products are projected to register a 5.98% CAGR through 2031.

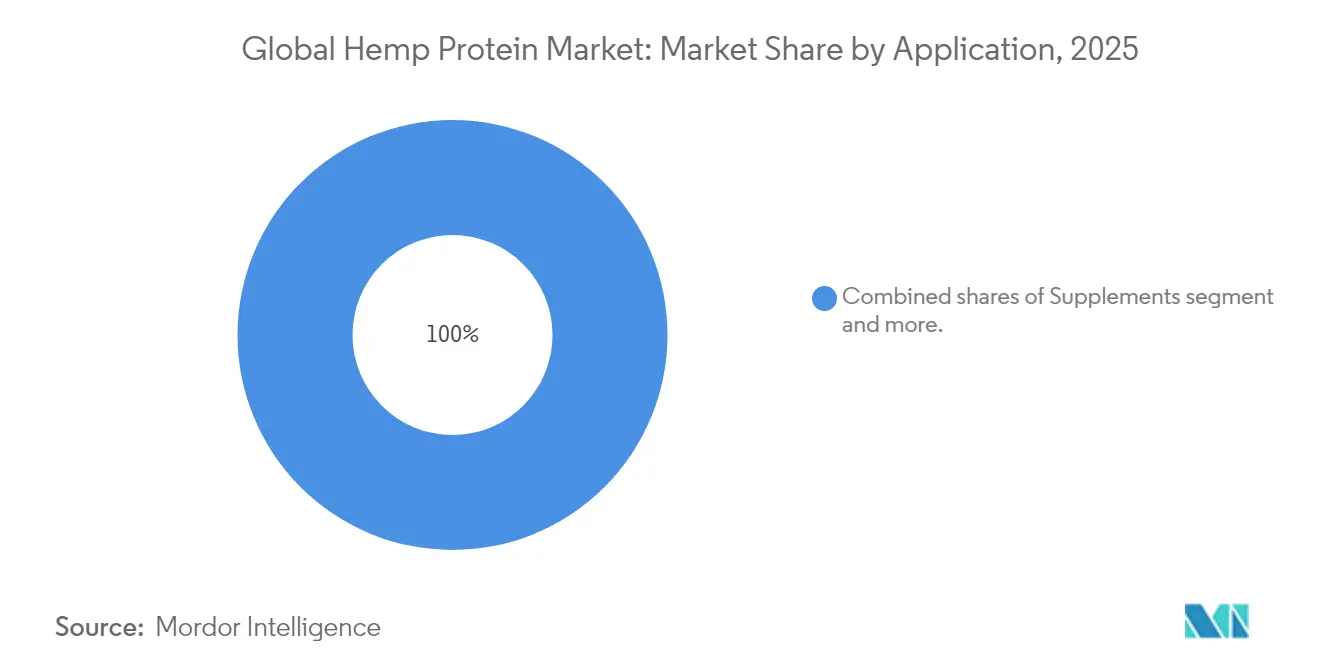

- By application, the food and beverage category controlled 94.55% revenue in 2025, whereas supplements are set to expand at a 5.76% CAGR to 2031.

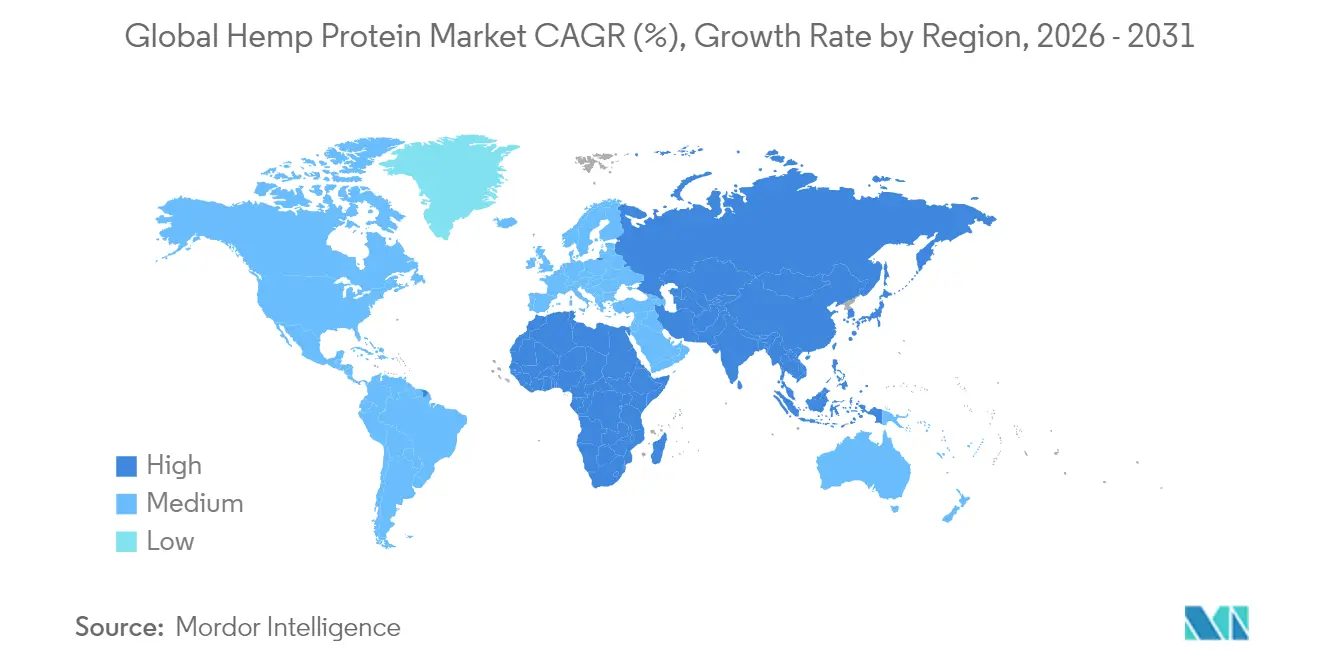

- By geography, Asia-Pacific commanded 47.20% of the hemp protein market size in 2025, while North America is expected to log the fastest 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemp Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of plant-based and vegan protein sources | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing prevalence of lactose and soy allergies | +0.8% | North America and Europe expanding to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory relaxation for industrial hemp cultivation | +1.0% | North America and Europe, selective Asia-Pacific | Long term (≥ 4 years) |

| Expansion in functional foods and nutraceuticals | +0.9% | Global, premium developed markets | Medium term (2-4 years) |

| Growth in sports and nutritional supplements | +0.7% | North America and Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Increasing demand for organic and clean-label products | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of plant-based and vegan protein sources

Consumer transition toward plant-forward diets extends beyond lifestyle into supply-chain strategy, and the hemp protein market benefits because hemp cultivation needs less water than soy, wheat, or pea. According to the Good Food Institute, in 2024, around 40% of adults in Germany and the UK plan to increase their plant-based food consumption. Health reasons account for 48% of this shift, while environmental concerns represent 29%, and animal welfare considerations comprise 25%[1]Source: The Good Food Institute, " State of the Industry 2024", www.gfi.org. Companies are leveraging the dual-purpose nature of hemp crops, which enables the simultaneous recovery of fiber and protein, thereby reducing the cost per functional unit. The European Union's Circular Economy Action Plan, which targets the development of sustainable textiles by 2030, has significantly increased the demand for hemp stalks. This growing demand not only enhances the economic value of hemp but also lowers the overall cost of protein feedstock. For example, Manitoba Harvest and Brightseed have recently launched an upcycled hemp-hull fiber supplement. This product utilizes material that was previously considered waste, effectively transforming circularity into a profitable margin opportunity.

Growing prevalence of lactose and soy allergies driving alternative proteins

As dietary preferences increasingly move away from dairy-derived and soy proteins, hypoallergenic hemp formulations are gaining prominence by securing "free-from" labels, which enable them to command higher price points. A double-blind crossover study, published in the American Journal of Clinical Nutrition, demonstrated that hemp seed protein and its hydrolysate significantly reduced blood pressure when compared to casein. This pivotal finding has elevated hemp from being merely a macronutrient to a nutraceutical with potential health benefits. The market has responded to this shift: In February 2025, The Simply Good Foods Company acquired the allergen-free shake brand OWYN for USD 280 million, emphasizing the growing commercial importance of allergen-conscious product positioning. Additionally, as the FDA enforces stricter labeling regulations for plant-protein analogs, hemp protein's minimal and straightforward ingredient profile emerges as a distinct competitive advantage in the market.

Regulatory relaxation for industrial hemp cultivation

The normalization of hemp cultivation is enhancing supply chain stability, enabling large-scale food manufacturers to expand from niche health food markets into mainstream grocery channels. The recent feed approval has established a regulatory precedent for the safety of hemp protein across various applications, reducing compliance challenges for human food manufacturers. Panda Biotech's flagship hemp processing facility in Texas, with a capacity to process 10 metric tons of industrial hemp per hour, highlights the infrastructure scale required to support mainstream adoption. This facility employs a zero-waste process powered by renewable energy, addressing sustainability concerns while achieving industrial-scale efficiency. In China, industrial hemp breeding programs, particularly in Heilongjiang and Yunnan provinces, are focused on optimizing yields and enhancing quality traits, potentially creating supply chain advantages for protein extraction applications.

Expansion in functional foods and nutraceuticals

Hemp protein, recognized for its distinctive bioactive compounds, is establishing itself as a premium functional ingredient rather than a standard commodity protein. This differentiation enables higher pricing, supported by emerging clinical evidence highlighting its health benefits. The increasing production of functional foods, particularly in China. The export value of health and functional food in China was USD 4,275 million in 2024[2]Source: China Chamber of Commerce for Import and Export of Medicines and Health Products, "Analysis of China's foreign trade situation of nutritional and health foods 2024", www.cccmhpie.org.cn (as reported by the China Chamber of Commerce for Import and Export of Medicines and Health Products), which is driving this demand. Brightseed scientists have identified bioactive lignanamides in hemp hulls, specifically N-trans-caffeoyltyramine and N-trans-feruloyltyramine, which demonstrate positive effects on gut health. These findings are now leveraged on functional beverage labels. Additionally, Applied Food Sciences has developed PurHP-75™, a product containing 75% protein and texturizing fibers that replicate the mouthfeel of meat, creating opportunities in the hybrid meat-alternative market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory challenges and legal uncertainties | -0.7% | Global, especially cross-border | Long term (≥ 4 years) |

| Competition from alternative protein sources | -0.5% | Global, mostly developed markets | Medium term (2-4 years) |

| Inconsistent global THC thresholds | -0.4% | Export-dependent regions | Medium term (2-4 years) |

| Taste and texture limitations in food uses | -0.3% | Consumer-facing, developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory challenges and legal uncertainties

Although hemp cultivation, transportation, and processing are legal in many regions, farmers and processors often require specialized licenses. Regulatory authorities enforce rigorous testing and documentation to verify THC compliance, resulting in higher costs and delays. Inconsistent regulations regarding hemp content frequently lead to border delays, import restrictions, or product seizures for hemp protein products. These issues disrupt supply chains and limit global distribution, particularly in key markets such as the EU, China, and certain Middle Eastern countries. Differing rules on THC thresholds and novel-food approvals create significant scientific and legal challenges. In the EU, any new hemp derivative intended for consumption requires a detailed safety dossier. Additionally, Italy's 2024 court-supported bans on specific hemp products underscore the unpredictability of regulatory policies. However, established players with a recognized GRAS portfolio are well-positioned to capitalize on these market conditions.

Competition from alternative protein sources

The rapid expansion of the pea protein market sets a challenging benchmark for hemp protein suppliers, who must not only achieve comparable growth but also prioritize consumer education regarding the superior amino-acid density of hemp protein. According to Agriculture and Agri-Food Canada, 36 new products featuring pea protein-based nutritional and meal replacement drinks were launched in Canada in 2023[3]Source: Agriculture and Agri-Food Canada, "Sector Trend Analysis – Plant-based protein food and drink trends in Canada", www.agriculture.canada.ca. Pea protein continues to strengthen its position as a dominant competitor within the market. In May 2025, Bunge announced a significant investment of EUR 484 million to establish a new soy processing plant in the United States, while Louis Dreyfus introduced a state-of-the-art pea-isolate production facility in Saskatchewan. These strategic initiatives underscore the substantial scale and cost efficiencies leveraged by established players in the soy and pea protein markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Organic Growth Accelerates Despite Conventional Dominance

In 2025, conventional cultivation remained dominant, contributing 83.35% of the hemp protein market's volume. Cost-conscious mass retail channels prefer lower-priced conventional inputs, while established agronomic practices continue to drive annual yield improvements. However, organic acreage is experiencing notable growth, as hemp's natural pest resistance minimizes certification costs. For example, Lithuania's emerging organic hemp exporters demonstrate how farmers can transition to premium categories without incurring significant agrochemical conversion expenses.

Organic product launches align with this agronomic trend. The global natural and organic food market is expanding, with protein-rich products outperforming the average growth of the category. Brands effectively leverage the consumer trust associated with organic certifications to justify premium pricing, enabling them to absorb higher raw material costs. The Hemp Fiber and Grain Association has introduced dedicated organic hemp grain programs that directly communicate price signals to farmers, ensuring a sustainable supply for processors. As a result, the organic segment is projected to achieve a 5.98% CAGR through 2031, exceeding the growth rate of the broader hemp protein market by over 100 basis points.

By Application: Supplements Drive Innovation Beyond Food Dominance

In 2025, food and beverage formulations represented a significant 94.55% of total revenue, with hemp being incorporated into bakery mixes, dairy alternatives, and ready-to-drink shakes. The expansive scale of the mass-market grocery sector means that even small percentage changes can result in substantial tonnage increases. Hemp's mildly nutty flavor integrates effectively into bars and cereals, while its natural emulsifying properties enhance the quality of plant-based milks. Recent advancements in protein isolates, such as Burcon's commercial-scale launch, provide formulators with a neutral-tasting, nearly undetectable option, enabling higher inclusion rates.

Conversely, the supplement sector stands out as the primary growth driver, with a strong CAGR of 5.76%. The increasing adoption of sports nutrition products is a key factor in this growth. Endurance athletes are progressively substituting dairy with hemp, which offers a complete amino acid profile and improved gut comfort. Success stories like OWYN have drawn the attention of larger strategic players, keeping them vigilant for acquisition opportunities. During the forecast period, analysts anticipate that capsule, gummy, and powder SKUs will increasingly occupy shelf space traditionally dominated by whey products. In the personal care segment, formulators are leveraging hemp peptides for their topical benefits. TRI-K's facility expansion highlights the commitment of ingredient suppliers to capitalize on this emerging opportunity.

Geography Analysis

In 2025, Asia-Pacific held a leading 47.20% share of the hemp protein market. China's breeding programs in Heilongjiang and Yunnan are enhancing seed yields and protein concentration, resulting in exportable surpluses for both fiber and food applications. Producers in the region are leveraging low production costs to supply high-volume clients in the snack and bakery industries. In contrast, Australia remains a smaller market participant, with its industry council working to secure funding for livestock-feed compliance, which could slow short-term growth.

North America is anticipated to achieve the highest CAGR of 5.29% through 2031, driven by coordinated policy measures and infrastructure improvements. For example, Panda Biotech's zero-waste mill in Texas supports multiple downstream users, effectively reducing logistical challenges between growers and processors. Furthermore, Canadian public funding, such as Protein Industries Canada's USD 6.9 million grant for alternative proteins, is advancing research and development efforts, particularly in developing concentrates with improved solubility. This investment aligns with a broader shift toward plant-based nutrition and alternative proteins. Hemp protein, with its complete amino acid profile, is especially appealing to vegan and vegetarian consumers. Europe offers a balanced growth opportunity. The region's annual demand for vegetable proteins provides hemp processors with a viable market, supported by sustainability goals aligned with the EU Green Deal. However, challenges such as the high costs of Novel Food dossiers and inconsistent national THC regulations increase market risks, as evidenced by Italy's recent ban on oral CBD products. In North America, consumers are increasingly adopting plant-based proteins for purposes such as muscle building, weight management, and overall wellness. This trend is particularly prominent among fitness-conscious millennials and Gen Z, who favor hemp protein for its high fiber content, essential fatty acids, and digestibility.

Competitive Landscape

The global hemp protein market is moderately fragmented, with the presence of various players. Leading manufacturers in the hemp protein market focus on leveraging opportunities posed by emerging economies like India and China to expand their revenue base. Midsized companies are increasingly adopting vertical integration strategies to address the challenges posed by raw material price volatility. Manitoba Harvest serves as a notable example of this approach, utilizing its in-house farming network to achieve cost efficiencies in production. Additionally, the company has formed strategic partnerships, such as its collaboration with Brightseed, to expand its portfolio with premium bioactive product lines, further enhancing its market position. The major players operating in the market include Axiom Foods Inc., Manitoba Harvest Hemp Foods, Martin Bauer Group, and ETChem, among others.

Innovation remains a critical factor in differentiating competitors within the market. Burcon leverages its proprietary filtration technology to develop neutral-flavored protein isolates, effectively overcoming longstanding texture issues in high-inclusion formulations. This advancement enables the company to meet the evolving demands of food manufacturers seeking improved ingredient functionality.

Regulatory assets play a pivotal role in shaping competitive leadership within the market. Companies that possess GRAS (Generally Recognized As Safe) notices, such as those for hemp seed protein, are well-positioned to offer U.S. clients streamlined compliance solutions. This capability provides a significant advantage during the supplier selection process, as food manufacturers prioritize regulatory assurance. Furthermore, impending regulatory changes in the United States, which aim to eliminate self-affirmed GRAS status, are expected to intensify the competitive landscape. These reforms are likely to create a wider gap between established players with robust resources and emerging start-ups, further solidifying the dominance of resource-rich incumbents.

Hemp Protein Industry Leaders

-

Axiom Foods Inc.

-

Manitoba Harvest Hemp Foods

-

Martin Bauer Group

-

ETChem

-

Tilray Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Victory Hemp Foods has unveiled North America’s largest processing line for hemp heart protein and oil, catering to the surging demand for its allergen-free, nutrient-rich ingredients.

- January 2025: TRI-K Industries has enhanced its manufacturing capabilities at a state-of-the-art facility in Derry, New Hampshire, with a focus on sustainable proteins and peptides for beauty and personal care applications. This expansion enables TRI-K to better serve global markets with high-quality ingredients, including exploring the potential use of hemp protein in cosmetics.

Global Hemp Protein Market Report Scope

Global hemp protein market is segmented by source into organic ad conventional;by application into functional food, functional beverage, dietary supplements, pharmaceutical, personal care and other industrial uses.Also, the study provides an analysis of the functional flour market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

By Source

| Organic |

| Conventional |

By Application

| Food and Beverage | Bakery |

| Snacks | |

| Confectionary | |

| Beverages | |

| Supplements | Sport/Performance Nutrition |

| Elderly Nutrition and Medical Nutrition | |

| Personal Care and Cosmetics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Organic | |

| Conventional | ||

| By Application | Food and Beverage | Bakery |

| Snacks | ||

| Confectionary | ||

| Beverages | ||

| Supplements | Sport/Performance Nutrition | |

| Elderly Nutrition and Medical Nutrition | ||

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hemp protein market?

The hemp protein market is valued at USD 181.28 million in 2026.

How fast is the hemp protein market expected to grow?

Industry forecasts show a 4.97% CAGR, taking market value to USD 231.06 million by 2031.

Which region leads hemp protein sales today?

Asia-Pacific holds the largest share at 47.20% of global revenue.

Which region is projected to grow the quickest?

North America is forecast to expand at a 5.29% CAGR through 2031 on the back of regulatory liberalization and new processing capacity.

Page last updated on: