Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

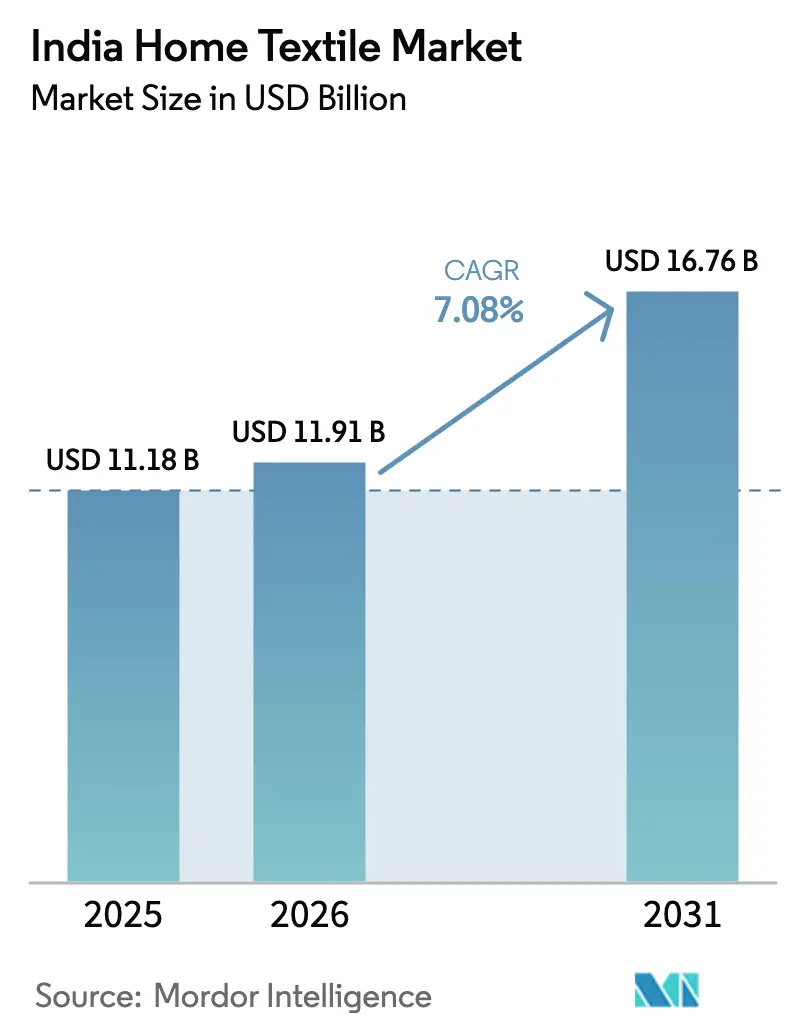

| Base Year Market Size (2025) | USD 11.18 Billion |

| Market Size (2026) | USD 11.91 Billion |

| Market Size (2031) | USD 16.76 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

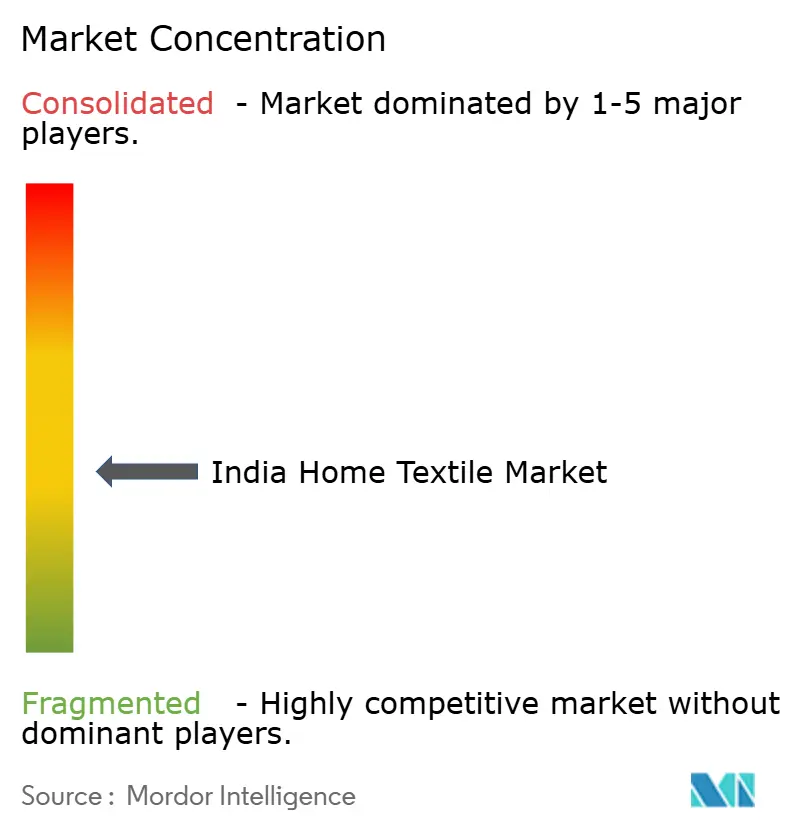

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Home Textile Market Analysis by Mordor Intelligence

The India Home Textile Market size was valued at USD 11.18 billion in 2025 and is estimated to grow from USD 11.91 billion in 2026 to reach USD 16.76 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031).

This rise defines the current market size trajectory of the India home textile market. Robust export contracts, sustained urban disposable-income growth, and active government production incentives continue to stimulate capacity additions even as cotton-price swings and new quality-control orders compress short-term margins. Leading manufacturers modernize spinning and finishing lines to support antimicrobial, temperature-regulating, and eco-certified fabrics, a move encouraged by consumer preference for premium, sustainable products in Tier-1 and Tier-2 cities. E-commerce channels, including quick-commerce pilots in metropolitan zones, strengthen omnichannel inventory visibility, cut delivery times, and improve basket sizes through algorithmic pricing. Export momentum is reinforced by a “China+1” sourcing pattern in the United States and the European Union, while integrated textile parks under the PM-MITRA scheme lower cap-ex for greenfield projects by offering subsidized land and common utilities. Parallel investments in zero-liquid-discharge systems and renewable power are increasingly viewed as defensive strategies to meet forthcoming EU Digital Product Passport rules.

Key Report Takeaways

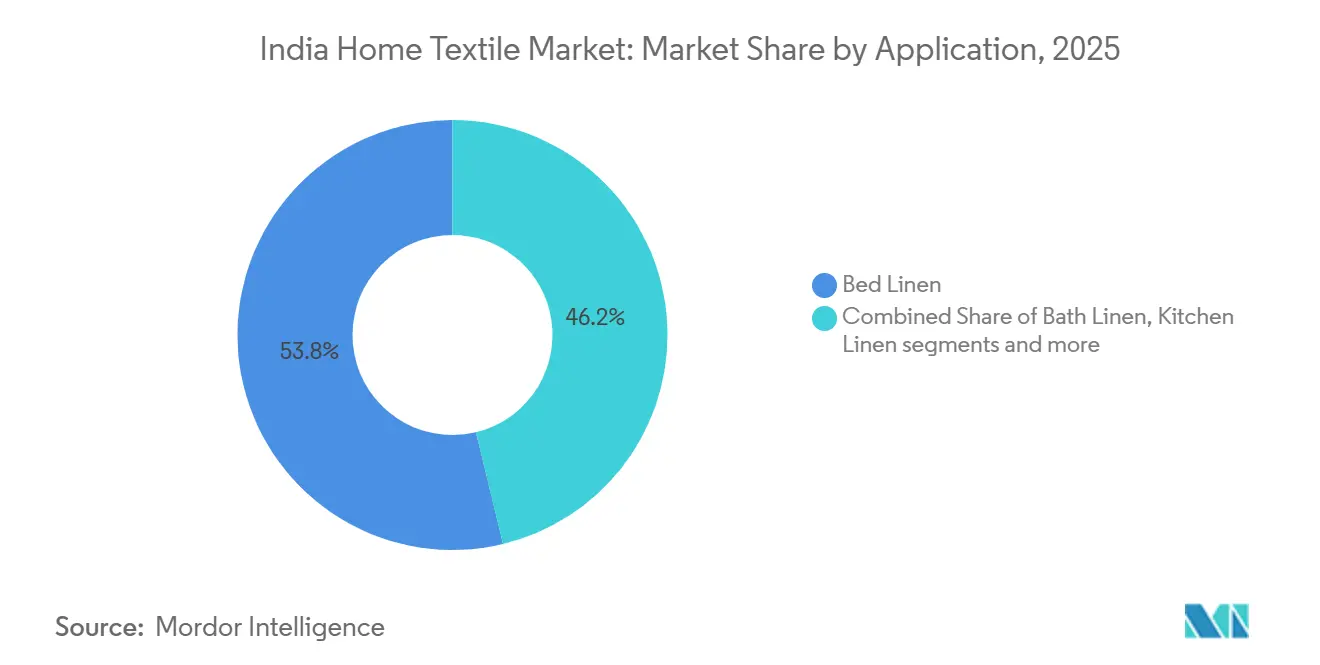

- By application, bed linen captured 53.77% of the India home textile market share in 2025, and bed linen is projected to expand at an 8.21% CAGR through 2031.

- By material, cotton retained 66.25% of the India home textile market size in 2025, while other materials (Wool, Hemp, Silk, Jute, Bamboo, etc.) are projected to rise at a 10.29% CAGR through 2031.

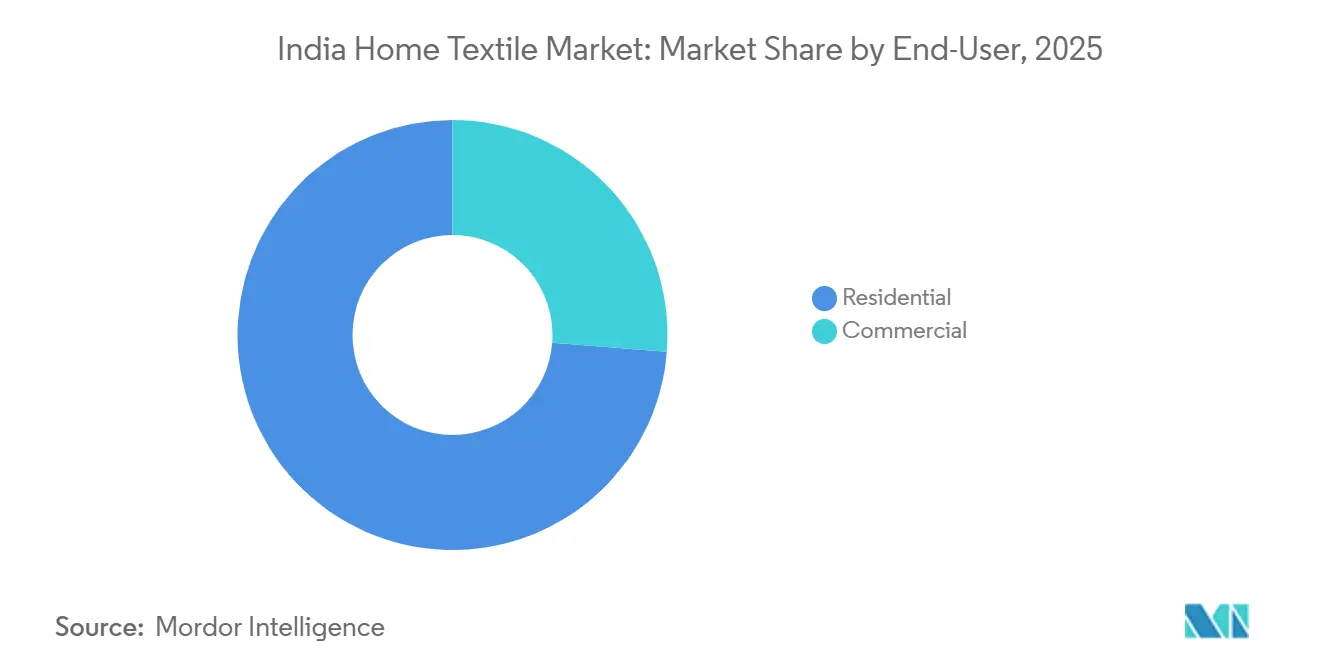

- By end-user, the residential segment commanded 73.75% of the India home textile market size in 2025, yet the residential segment is expected to accelerate at a 7.65% CAGR through 2031.

- By distribution channel, offline retail held 88.03% of the India home textile market share in 2025, while online channels are forecast to advance at an 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class spending power and rapid urban migration | +1.8% | National, Tier-1 and Tier-2 cities | Medium term (2–4 years) |

| Accelerating e-commerce adoption and omnichannel retail expansion | +2.1% | National, led by Maharashtra, Karnataka, and Delhi-NCR | Short term (≤ 2 years) |

| “China + 1” sourcing shift boosting India’s export orders from US & EU buyers | +1.5% | Gujarat, Tamil Nadu, Maharashtra | Medium term (2–4 years) |

| PLI scheme and PM-MITRA mega textile parks lowering capital intensity | +1.0% | Gujarat, Tamil Nadu, Telangana | Long term (≥ 4 years) |

| Eco-friendly & smart-textile innovations lifting average selling prices | +0.9% | Major metros | Long term (≥ 4 years) |

| Rapid hotel and serviced-apartment expansion swelling institutional linen demand | +1.8% | National, Tier-1 and Tier-2 cities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising middle-class spending power and rapid urban migration

Per-capita net national income advanced to FY24 at INR 188,892 and projected to rise further to INR 205,324 for FY25.[1]Ministry of Statistics and Programme Implementation, “National Accounts Statistics,” mospi.gov.in Urban households now allocate 4.2% of monthly spending to home furnishings versus 3.1% in 2020, and the Ministry of Housing projects urbanization will hit 40% by 2030, adding 60 million households. Branded products steadily replace unbranded bazaar offerings as first-time buyers migrate toward higher thread counts and durable finishes, shrinking the replacement cycle for bed linen from five to three years. Domestic retailers confirm that premium cotton and blended fabrics now attract consumers from middle-income bands seeking elevated aesthetics and hygiene benefits. This demand recalibration incentivizes mills to run finer cotton counts and invest in automated quality checks to maintain consistent texture and colorfastness.

Accelerating e-commerce adoption and omnichannel retail expansion

Online home-textile sales crossed INR 8,500 crore (USD 993.7 million) in 2024, realizing a 28% year-on-year increase as unified payments surpassed 131 billion transactions, lowering checkout friction[2]Source: National Payments Corporation of India, “UPI Ecosystem Statistics,” npci.org.in . Amazon and Flipkart added more than 50,000 SKUs from 1,200 sellers, using dynamic pricing to lift average order value by 18%. Welspun India’s direct-to-consumer portal synchronizes inventory across 200 stores to support same-day pickup, trimming cart abandonment by 15%. Quick-commerce platforms now deliver towels and sheets in 10 minutes across Bengaluru, Mumbai, and Delhi, compressing replenishment cycles and forcing incumbents to rethink last-mile strategies. These tech-enabled channels provide real-time demand signals that help mills adjust loom schedules and reduce finished-goods inventory.

“China + 1” sourcing shift boosting India’s export orders from US & EU buyers

eHome-textile exports reached USD 5.1 billion in the first nine months of 2024, up 9% from the same period in 2023 as India captured 34% of US bed-linen imports. Indian mills deliver 40-foot containers within six to eight weeks, faster than many Southeast Asian competitors, while Germany’s imports from India climbed 12% in 2024 as European retailers sourced GOTS-certified products [3]Source: Statistisches Bundesamt (Destatis), "Foreign Trade", https://www.destatis.de/EN/Themes/Economy/Foreign-Trade/_node.html. Government buyer-seller meets linked 500 SMEs with global buyers, speeding order visibility. Larger exporters sign multiyear contracts that pass through cotton-price escalations and hedge tariff risk. Logistics savings from Gujarat ports reinforce margin stability despite freight volatility.

PLI scheme and PM-MITRA mega textile parks lowering capital intensity

The production-linked incentive scheme allocates INR 10,683 crore (USD 1.25 billion) over five years, offering a 15% boost on incremental turnover for investments in man-made fiber and technical textiles. GHCL Textiles announced an investment of INR 215 crore (USD 25.1million) to add 25,000 spindles by Q2 FY26, following the successful installation of 40,000 spindles and 15 MW of renewable energy over the past two years[4]Source: Textile Magzine, "GHCL Textiles’ Strategic Investments and Capacity Expansion program", https://www.indiantextilemagazine.in/ghcl-textiles-strategic-investments-and-capacity-expansion-program/#:~:text=GHCL%20Textiles%20Limited%20is%20poised,within%20the%20next%20five%20years . Seven PM-MITRA parks provide plug-and-play infrastructure at INR 500 (USD 5.85) per square meter versus INR 2,000 (USD 23.4) to INR 3,000 (USD 35.1) market rates, easing entry barriers. Trident positions satellite units inside these parks to slash logistics costs by 12% and shorten lead times to ports. The combined effect of tax incentives, land subsidies and shared utilities lowers IRR thresholds and accelerates project sanctions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton prices and broader raw-material inflation squeezing margins | −1.9% | National, with concentration in cotton-dependent Gujarat and Maharashtra | Short term (≤2 years) |

| Uncertain tariffs and trade policies in key Western markets clouding export flows | −1.2% | West and South export-oriented hubs | Medium term (2–4 years) |

| Highly fragmented domestic supplier base causing inconsistent product quality | −0.8% | National, with focus on unorganized manufacturing clusters | Medium term (2–4 years) |

| Stricter BIS quality norms elevating compliance costs for small manufacturers | −0.6% | National, with greater burden on SME and micro-scale units | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Volatile cotton prices and broader raw-material inflation squeezing margins

Cotton prices spiked to INR 62,000 (USD 724.8) per candy in March 2024, an 18% rise since December 2023. The minimum support price for medium-staple cotton increased to INR 7,020 (USD 82.1) per quintal for the 2024-25 season, squeezing gross margins by up to 300 basis points. Polyester staple fiber averaged INR 95 (USD 1.11) per kilogram in 2024, a 12% year-on-year hike that compounded cost pressure. To mitigate volatility, manufacturers shift toward 60% cotton-40% polyester blends that reduce raw-material expenses by roughly 15%. Futures hedging and longer-term contracts offer partial insulation but remain underutilized among SMEs.

Uncertain tariffs and trade policies in key Western markets clouding export flows

The United States initiated a Section 301 review in late 2024 that could impose 10% to 25% duties on Indian home textiles, threatening price competitiveness. The EU’s Carbon Border Adjustment Mechanism from 2026 will levy charges on textiles produced with coal-based electricity, raising compliance challenges for mills in thermal-power-dependent states. Grid connectivity gaps and capital costs of INR 4 crore (USD 0.47 million) to INR 6 crore (USD 0.70 million) for a 1 MW solar setup slow immediate renewable transitions. Exporters respond by accelerating green-power purchase agreements and seeking carbon-neutral certifications. Industry associations lobby for tariff exemptions and smoother standards alignment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Anchors Market Leadership

The India home textile market by application was led by bed linen, accounting for 53.77% of the total market share in 2025. This was driven by strong replacement demand from urban households, stable export orders to the United States and European Union retailers, and a preference for premium products with higher thread counts. Hospitality chains boosted demand by shortening replacement cycles, while government initiatives like the One District One Product scheme promoted unique hand-loom designs.

Bed linen is projected to be the fastest-growing segment during 2026 - 2031, with a CAGR of 8.21%. Growth will be supported by increased adoption of branded labels among middle-income households, digital campaigns highlighting sustainability, and the expansion of direct-to-consumer channels. These factors ensure bed linen remains a key market segment and a primary growth driver across residential and hospitality applications.

By Material: Cotton Dominates While Niche Fibers Accelerate

Cotton accounted for 66.25% of the India home textile market size by material in 2025, driven by strong domestic production and consumer preference for its affordability and versatility. It remains central to domestic and export demand, supported by modernization under the Technology Upgradation Fund Scheme, enabling mills to produce finer counts. Synthetic fibers cater to price-sensitive households, while premiumization in bed and bath categories reinforces cotton’s dominance.

Materials like wool, hemp, silk, jute, and bamboo are projected to grow at a CAGR of 10.29% during 2026 - 2031. Growth is fueled by rising sustainability awareness, water scarcity driving demand for linen alternatives, and the premium appeal of hemp and jute in urban markets. Bamboo viscose, marketed as bamboo linen, is gaining traction for its silky texture and biodegradability, while recycled polyester appeals to eco-conscious consumers. These niche fibers are diversifying the market and aligning with global sustainability trends.

By End‑User: Residential Buyers Drive Demand Growth

The India home textile market in 2025 was led by residential buyers, comprising 73.75% of total demand. High urban home-ownership rates and strong replacement cycles drove this dominance. The top 20% of families favored branded products, while middle-income buyers opted for hypermarket private labels priced between INR 1,500 (USD 16.69) and INR 3,000 (USD 33.38). Government initiatives like the One District One Product scheme supported hand-loom designs, and direct-to-consumer channels enabled niche brands to target sustainability-conscious homeowners.

Residential demand is projected to grow fastest during 2026-2031, with a CAGR of 7.65%, driven by rising disposable incomes, premiumization trends, and digital campaigns promoting coordinated purchases across bed, bath, and kitchen categories. While commercial buyers, including hotels, healthcare institutions, and co-living spaces, remain significant, the residential segment anchors the market, ensuring stability and long-term growth across diverse consumer groups.

By Distribution Channel: Online Gains on Quick Commerce and D2C

Offline still accounted for 88.03% of sales in 2025, leveraging more than 3,000 mass-merchandise outlets. Online channels grew at an 11.02% CAGR, with Amazon and Flipkart processing 12 million orders and using algorithmic repricing to raise basket sizes. Quick-commerce start-ups now deliver in 10 minutes across three metros. D2C brands such as Maspar expanded same-day delivery to five cities, integrating 120 store inventories. Specialty showrooms, representing 15% of offline sales, curate coordinated sets to lift transaction values by 25%.

Mass merchandisers negotiate 40% to 50% factory discounts while stand-alone boutiques maintain relevance by offering exclusive weaves. Integrated omnichannel platforms synchronize SKUs across warehouses and shelves, improving turn rates. Digital payments adoption lowers cart abandonment and supports cash-flow cycles for online retailers. Real-time analytics feed upstream demand planning, enabling mills to minimize dead stock.

Geography Analysis

West India leads with Solapur producing 40% of terry towels and Surat specializing in synthetic bed linen. Solapur benefits from lower logistics costs due to local cotton sourcing, while Surat's proximity to major ports supports exports. The Sanand PM-MITRA park offers subsidized land prices, though Maharashtra's water scarcity necessitates costly zero-liquid-discharge systems.

South India holds a significant share, with Coimbatore and Tiruppur adopting compact spinning systems for export premiums. Bengaluru and Mysuru are emerging as smart-textile hubs integrating nanotechnology. North India relies on Delhi-NCR and Panipat power-loom clusters, producing millions of sheets annually within competitive price ranges.

East and North-East India are growing rapidly, supported by subsidies, reduced costs, and competitive wages. Assam promotes Guwahati as a hand-loom hub, while the Dedicated Freight Corridor enhances connectivity, making East-based mills competitive in northern markets.

Competitive Landscape

The India home textile market is moderately fragmented, with leading producers accounting for a significant share. Welspun's vertical integration reduces lead times significantly. Trident has expanded towel production capacity with substantial investments and secured numerous hotel contracts. Indo Count directs most of its production to United States retailers and has filed patents for innovative finishes. GHCL's Tamil Nadu facility uses automation to lower labor costs effectively. D2C brands hold a notable share of the premium segment, leveraging social media for growth. IKEA collaborates with multiple Indian suppliers and plans to increase sourcing in the coming years. Private labels from Reliance Retail and DMart offer competitive discounts. Compliance with BIS norms involves annual audits with associated costs.

While online retailing of home textiles is gaining momentum, it's still nascent. Shoppers in metropolitan areas, as well as Tier-2 and Tier-3 cities, are increasingly drawn to the convenience, broader selection, and ease of online shopping for home textiles. While large corporations leverage volume purchases, diverse product offerings, and savvy marketing, smaller businesses home in on specific segments, excelling through a broad product range and top-notch customer service.

Indian brands are making their mark on the global stage. For instance, in April 2025, Jaipur Rugs, a frontrunner in the luxury handmade carpet sector, took a significant step by acquiring the Shyam Ahuja brand. Their goal is to uphold the founder's original vision while elevating the brand's status on the global luxury stage.

India Home Textile Industry Leaders

-

Welspun Group

-

Trident Group

-

Indo Count Industries Ltd.

-

Himatsingka Seide Ltd.

-

GHCL Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Welspun Home Solutions inaugurated a terry-towel plant in Anjar, Gujarat, the world’s largest single-site towel facility, reinforcing its global leadership.

- June 2025: IKEA announced plans to lift India sourcing from 30% to 50%, deepening supply-chain integration.

- February 2025: The Union Budget 2025-26 launched the Mission for Cotton Productivity and doubled MSME credit guarantee limits to INR 10 crore, unlocking estimated funding of INR 1.5 lakh crore for textile enterprises.

India Home Textile Market Report Scope

Home textile or household textile is a textile segment comprised of components used in the domestic environment. It consists of various functional and decorative products mainly used in decorating houses. The fabric used for home textiles consists of both natural and man-made fibers. The study gives a brief description of the India home textile market and includes details on home textile sales, investment by the manufacturers, and the launch of new home textile products. The India home textile market is segmented by product, material, end-user, distribution channel, and region. By product, the market is segmented into bed linen, bath linen, kitchen linen, upholstery, and others. By material, the market is segmented into cotton, linen, synthetic fibres, and other materials. By end-user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into offline and online. The report also covers the market sizes and forecasts for the India home textile market in value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Carpets & Area Rugs |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Distribution Channels | |

| Online |

By Region

| North India |

| West India |

| South India |

| East India |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Carpets & Area Rugs | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Distribution Channels | ||

| Online | ||

| By Region | North India | |

| West India | ||

| South India | ||

| East India | ||

Key Questions Answered in the Report

What is the current value of the India home textile market?

The market was valued at USD 11.91 billion in 2026 and is projected to reach USD 16.76 billion by 2031.

Which application segment currently leads in revenue?

Bed linen leads with a 53.77% share in 2025 and is also the fastest‑growing segment, with an 8.21% CAGR during 2026–2031.

How fast are online sales of home textiles expanding in India?

Online channels are advancing at an 11.02% CAGR, propelled by large marketplaces and emerging quick-commerce models.

Why are linen and bamboo blends gaining popularity?

Consumers value breathability, lower water usage and biodegradability, driving a 12.65% CAGR for these blends during 2026-2031.

What incentives drive new textile investments?

The PLI scheme and PM-MITRA parks provide cash incentives, subsidized land at INR 500 (USD 5.85) per m² and shared infrastructure, lowering capital costs.

How fragmented is the supplier landscape?

The top five companies control about 40% of sales, leaving room for mid-tier and niche firms that focus on design innovation or artisanal products.

Page last updated on: