Healthcare Payer Network Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

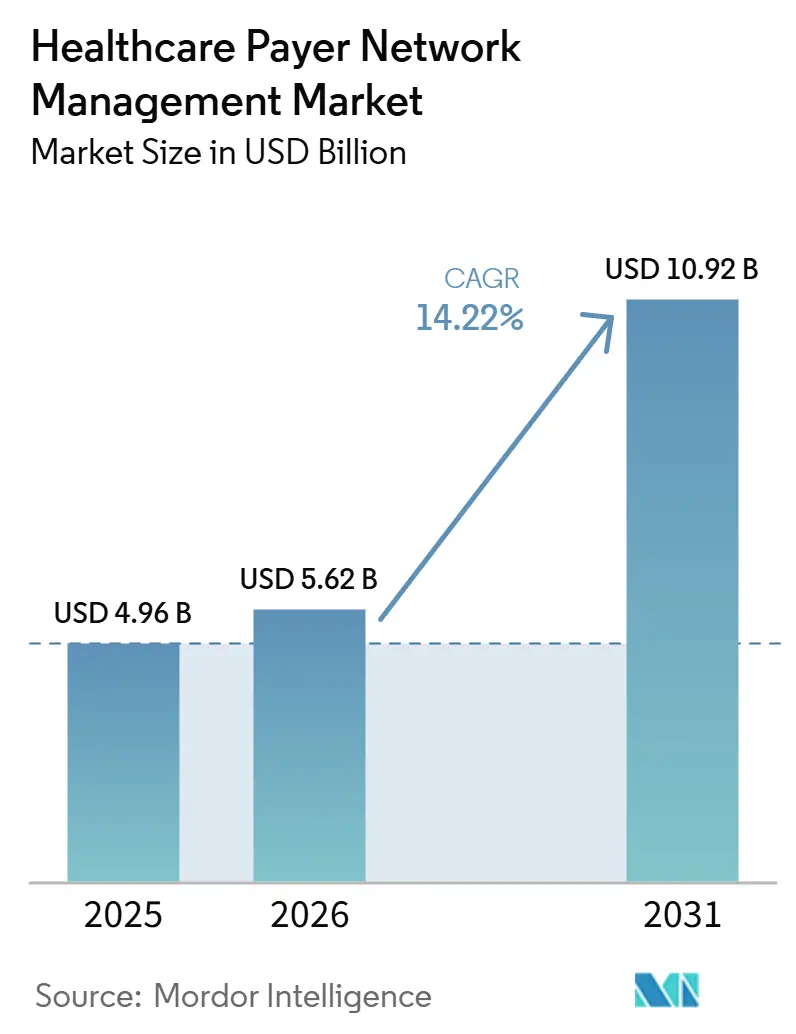

| Market Size (2026) | USD 5.62 Billion |

| Market Size (2031) | USD 10.92 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Payer Network Management Market Analysis by Mordor Intelligence

The healthcare payer network management market is expected to increase from USD 4.96 billion in 2025 to USD 5.62 billion in 2026 and reach USD 10.92 billion by 2031, growing at a CAGR of 14.22% over 2026-2031. Growth in the healthcare payer network management market reflects a structural shift, because payers are facing higher administrative complexity, tighter interoperability obligations, and a faster move toward AI-supported workflow redesign. The healthcare payer network management market is also being shaped by defensive modernization, as large plans try to protect control over member engagement, provider network performance, and back-office execution while newer technology-led competitors widen their reach. Cloud migration is becoming more central in the healthcare payer network management market, since payer-to-payer API deadlines and directory accuracy pressure are pushing buyers toward systems that can support real-time data exchange at scale. Services demand is rising alongside software spending, because many plans still need outside help to manage credentialing, contracting, provider data governance, and compliance-heavy operational work inside the healthcare payer network management market. Competition remains active and moderately concentrated, with large IT services firms, payer software vendors, and niche specialists using acquisitions, interoperability expansion, and workflow automation to improve their position in the healthcare payer network management market.

Key Report Takeaways

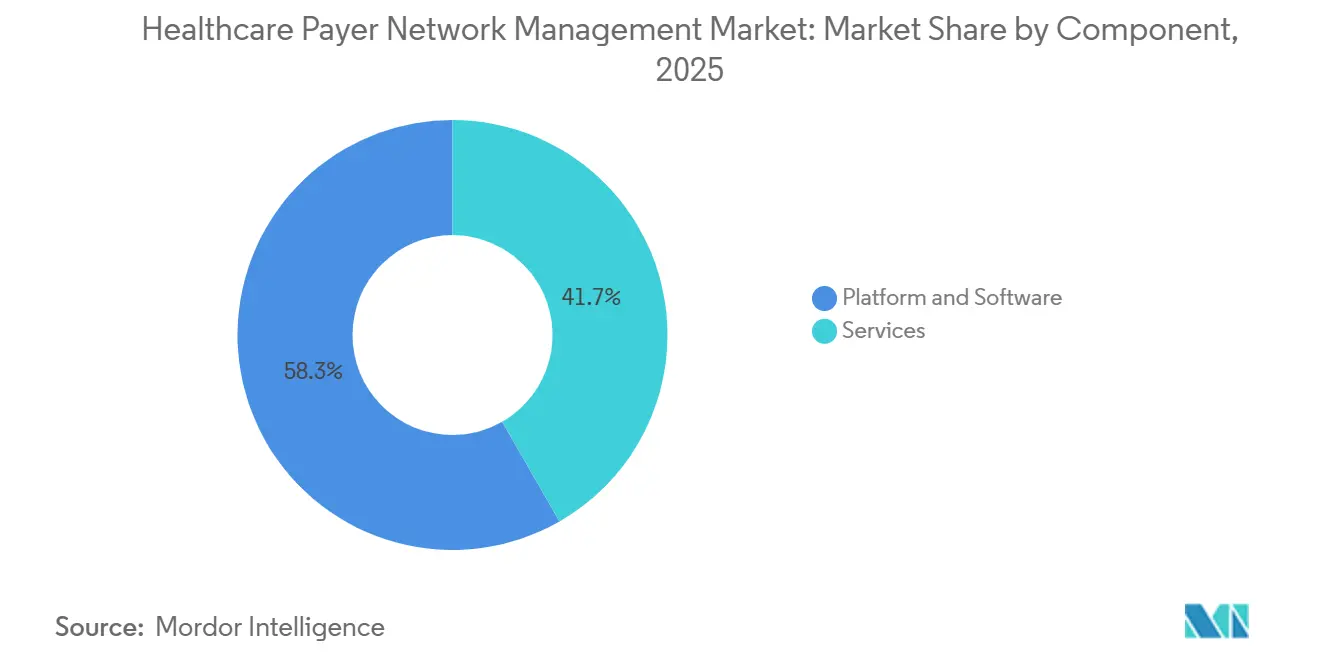

- By component, platform and software led with 58.32% share in 2025, while services are forecast to expand at a 15.48% CAGR through 2031.

- By deployment mode, cloud-based led with 63.74% share in 2025, and it is also projected to grow fast at a 16.02% CAGR through 2031.

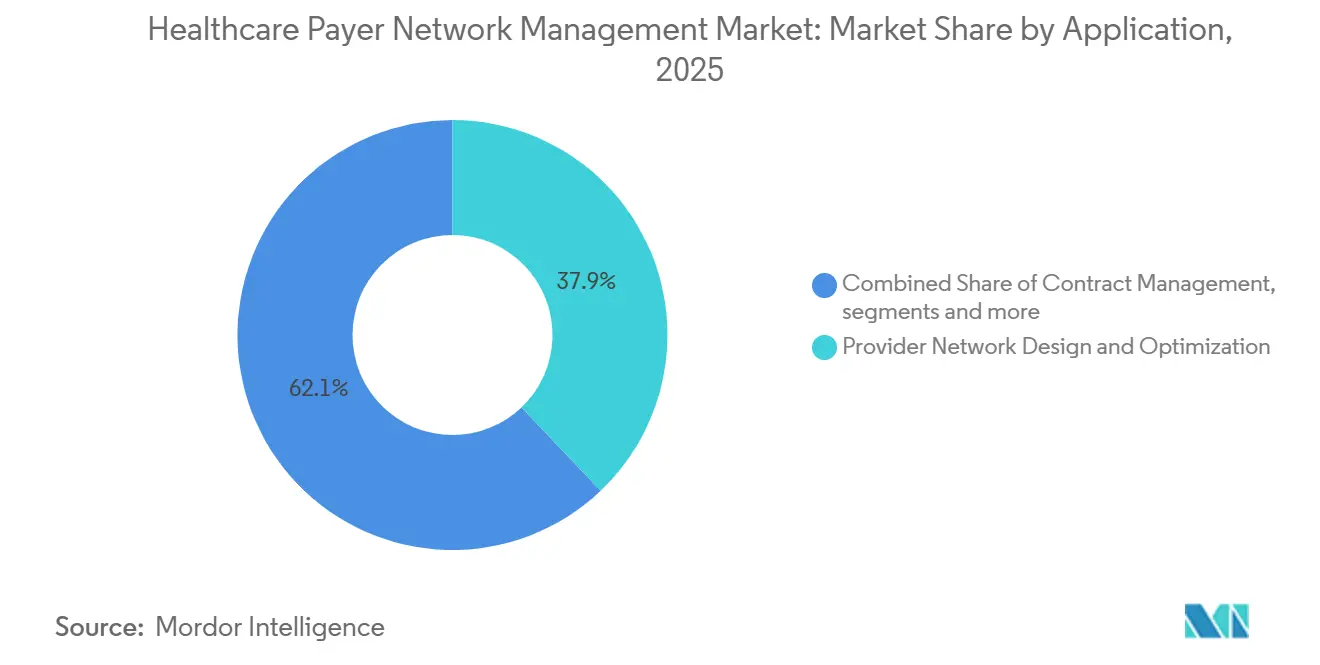

- By application, provider network desktop accounted for 37.86% share in 2025, while provider data management is expected to advance at a 16.84% CAGR through 2031.

- By end-user, public health insurance held 54.27% share in 2025, while private health insurance is projected to grow at a 15.91% CAGR through 2031.

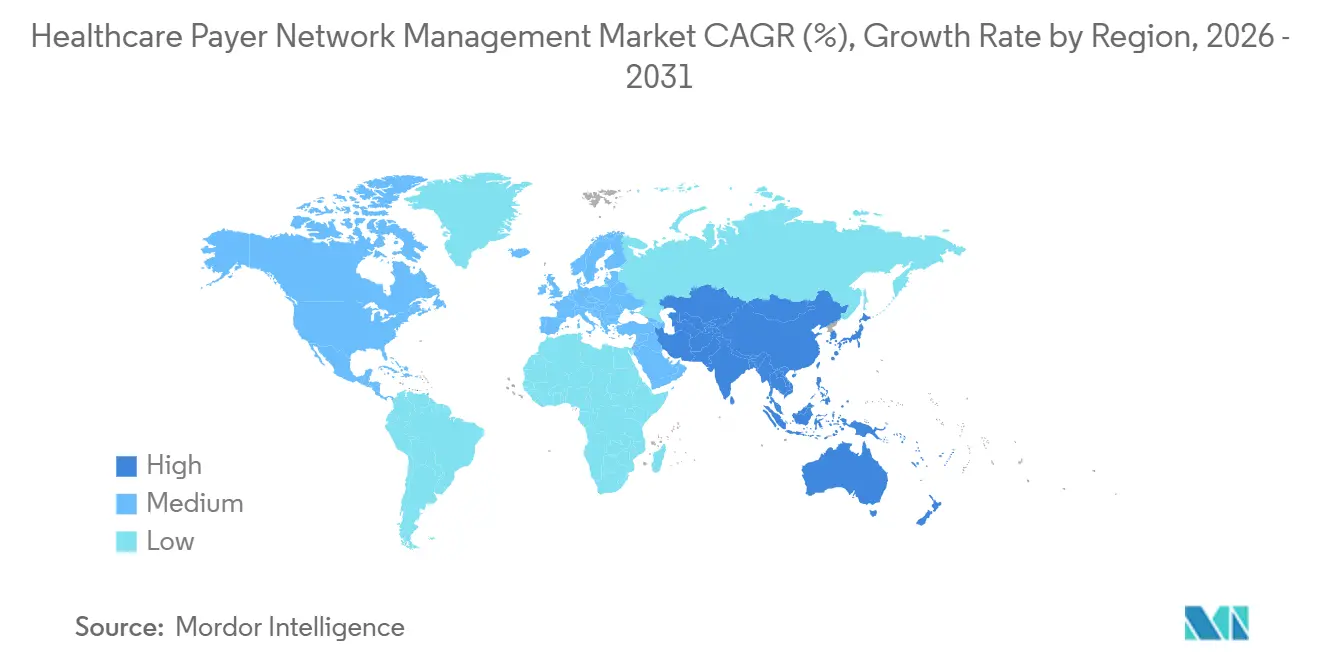

- By geography, North America accounted for 41.68% share in 2025, while the Asia-Pacific is expected to advance at a 17.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Payer Network Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of AI for Cost Containment and Fraud Prevention | +3.6% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Need for Provider Directory Accuracy and Compliance Automation | +2.8% | North America dominant, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Value-Based Care and Reimbursement Optimization | +2.9% | North America, with spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Real-Time Provider Data Governance | +1.9% | Global | Medium term (2-4 years) |

| Expansion of Virtual-First and Hybrid Provider Networks | +1.6% | North America and Europe | Short term (≤ 2 years) |

| Cross-Payer API Connectivity for Credentialing and Contracting | +1.8% | North America, expanding to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of AI for Cost Containment and Fraud Prevention

AI is moving from pilot work to broader deployment, as payers try to reduce administrative effort and improve the speed of decisions across utilization management, provider contracting, and related network operations. Innovaccer reported in May 2026 that 75% of surveyed health plan C-suite executives plan to spend more than USD 10 million on AI within 3 to 5 years, which shows that investment plans are now moving beyond limited experimentation.[1]Innovaccer Inc., “Nearly 80% of Health Plans Now Prefer Vendor-Built AI Over In-House, Innovaccer Survey Finds,” Innovaccer, innovaccer.com The same survey showed that nearly 80% of health plans prefer vendor-built AI over in-house development, which supports the view that payer workflows still need outside expertise and domain-specific implementation support. It also found that 86% of plans are not yet fully operationalizing AI and that 46% cite interoperability gaps as the main barrier, which ties AI returns directly to better data exchange and cleaner provider information flows. In the healthcare payer network management market, that connection is directing spending toward platforms and service models that can automate network workflows only when upstream data is accurate and accessible. The healthcare payer network management market is therefore benefiting not only from AI budgets, but also from the operational work needed to make those budgets usable in day-to-day payer environments.

Shift Toward Value-Based Care and Reimbursement Optimization

Value-based care is expanding the scope of network management, because payers now have to track provider performance, shared-savings logic, quality metrics, and attribution rules across a wider contract base. Interwell Health reported in 2025 that 2-thirds of provider organizations increased participation in value-based care programs, and most expected a positive revenue shift from that participation, which increases pressure on payers to strengthen contracting and analytics support.[2]Interwell Health, “Healthcare Utilization Trends in 2025, How Health Plans Use Value-Based Care to Manage Costs,” Interwell Health, interwellhealth.comThe same shift matters in the healthcare payer network management market because network teams can no longer manage complex reimbursement structures with manual contracting tools and disconnected provider records. Alternative payment models account for at least 45% of healthcare payments, which is a scale at which fragmented operational processes become harder to sustain. As this mix grows, the healthcare payer network management market sees stronger demand for integrated provider data management, because weak attribution data can distort payment calculations and create disputes. Vendors that combine contracting, analytics, and provider data workflows are therefore better aligned with how payer buying criteria are changing in the healthcare payer network management market.

Cross-Payer API Connectivity for Credentialing and Contracting

The CMS Interoperability and Prior Authorization Final Rule requires affected payers to implement payer-to-payer, provider access, and prior authorization APIs, with most provisions taking effect by January 1, 2027.[3]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule CMS-0057-F Fact Sheet,” CMS, cms.gov This matters in the healthcare payer network management market because compliance depends on real exchange of claims, encounter, and authorization information through HL7 FHIR standards, not on a simple reporting overlay. In the healthcare payer network management market, that pressure is reinforcing cloud adoption, since older on-premises setups are less suited to high-frequency and bidirectional API exchange. Payers that approach the rule only as a minimum compliance task may keep operating costs higher, while peers that build broader provider data networks can improve accuracy and workflow speed inside the healthcare payer network management market.

Expansion of Virtual-First and Hybrid Provider Networks

Virtual-first care has moved beyond a temporary access solution and now functions as a distinct network design that needs dedicated credentialing, directory management, and claims support. This shift is important for the healthcare payer network management market because virtual providers must be contracted, classified, displayed, and maintained in ways that fit the same operational standards as physical care networks. The challenge is not limited to adding providers into the system, because payer directories also have to keep virtual care visibility current after contracting, credentialing, and workflow changes. That raises demand for platforms that treat virtual provider taxonomy and hybrid network composition as core functions rather than optional add-ons inside the healthcare payer network management market. It also expands the role of desktop and provider data tools, which now need to support telehealth, at-home care, and AI-enabled service models in a unified operating view. As hybrid care grows, the healthcare payer network management market gains momentum from the higher number of updates, contracts, directory adjustments, and member-facing data checks that plans must complete accurately.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Core Administrative System Integration Friction | -1.9% | Global, most pronounced in North America and Europe | Long term (≥ 4 years) |

| Provider Data Fragmentation Across Multiple Sources | -1.6% | Global | Medium term (2-4 years) |

| Cybersecurity And Privacy Exposure in Shared Network Data Flows | -1.4% | Global | Short term (≤ 2 years) |

| High Change-Management Burden for Manual Operations Teams | -1.2% | Global, especially mid-market payers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Core Administrative System Integration Friction

Legacy core administrative systems remain one of the hardest barriers in payer modernization, because they sit across claims, enrollment, network data, and payment logic at the same time. In the healthcare payer network management market, this means that even a well-designed network platform can struggle if the surrounding architecture cannot support stable integration and workflow orchestration. Module-by-module replacement is difficult, because a change in one area can disrupt payment rules, eligibility handling, or downstream claims processing. CMS interoperability requirements now raise the cost of delay, since many older environments do not support the required FHIR-based API capabilities in a native way. The result in the healthcare payer network management market is a two-speed investment pattern, where large national plans move faster while mid-market and government-sponsored plans often modernize more gradually. That uneven readiness also lengthens vendor sales cycles and makes implementation depth just as important as feature breadth in the healthcare payer network management market.

Provider Data Fragmentation Across Multiple Sources

Provider data fragmentation remains a structural problem, because inaccuracies in credentialing, enrollment, and directory records flow into claims routing, network adequacy filings, and prior authorization decisions. Symplr reported in 2025 that data silos, integration complexity, and inconsistent data flow remain common across health plans, which shows that many directory issues start upstream rather than inside the directory itself. In the healthcare payer network management market, those conditions keep demand high for provider data management systems, but they also limit how much any single platform can fix without better input discipline from provider organizations. The core issue remains that providers often control the original information, while payers still carry the compliance and member-facing consequences when data is wrong in the healthcare payer network management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground in A Platform-Heavy Structure

Platform and software held 58.32% of the healthcare payer network management market share in 2025, while services are projected to expand at a 15.48% CAGR through 2031. Software remained the largest component because payer organizations still need core systems for credentialing, directory maintenance, contract life cycle management, and provider performance tracking. Those platforms also act as the main operating layer for compliance activity, which helps preserve software demand even when implementation timing varies by payer size. In the healthcare payer network management market, software spending is especially durable where buyers want one control point for provider records, contract terms, and workflow rules. Services are growing faster because value-based care, API readiness, and provider data cleanup create ongoing work that many payer teams do not have the scale to manage alone.

Within the services category, implementation support, managed operations, and analytics advisory are all expanding, but they are doing so for different operational reasons. Near-term compliance projects tied to the January 2027 payer-to-payer API deadline should keep implementation demand elevated through the next cycle. Managed service models are also gaining favor in the healthcare payer network management market because they help plans convert recurring manual work into more structured operating models. Advisory work continues to matter as well, since payers often need help connecting provider data policy, contract design, and workflow automation into one operating approach. The segment mix should therefore remain platform heavy, but the fastest momentum in the healthcare payer network management market should continue to sit with vendors that combine software and hands-on execution.

By Deployment Mode: Cloud Becomes the Default Operating Model

Cloud-based deployment accounted for 63.74% share of the healthcare payer network management market size in 2025 and is projected to grow at a 16.02% CAGR through 2031. Cloud remained the leading model because payer network workflows now depend on frequent data exchange, faster updates, and broader integration across provider, claims, and authorization functions. In the healthcare payer network management market, deployment choice is therefore becoming a compliance decision as much as a technology decision. Buyers are also using cloud migration to reduce upgrade lag and improve the speed at which provider network changes appear across connected workflows.

Cotiviti completed its acquisition of Edifecs in March 2025, and that move added interoperability capability that supports faster FHIR-based connectivity. The deal shows how vendors in the healthcare payer network management market are using acquisitions to close architecture gaps more quickly than internal development cycles would allow. On-premises deployments still retain relevance in government-administered settings and large organizations with strict data localization needs. Over the forecast period, cloud should keep widening its lead because the operational benefit is now linked to compliance timing, platform extensibility, and faster automation rollout.

By Application: Core Desktop Tools Lead, While Provider Data Management Expands Fastest

Provider network desktop tools held 37.86% of application share in 2025, while provider data management is expected to grow at a 16.84% CAGR through 2031. The desktop category remained the largest because payer teams still need a central workspace for network adequacy review, geographic coverage monitoring, and provider recruitment decisions. In the healthcare payer network management market, provider data management is expanding faster because directory accuracy, credentialing, and enrollment quality now affect compliance, payment integrity, and member experience at the same time. This makes data stewardship less of a support function and more of a core operating requirement inside the healthcare payer network management market.

Claims and reimbursement applications remain closely tied to this segment, because routing accuracy still depends on current network information. Other applications, including prior authorization connections and population health modules, are also growing as payers try to reduce the number of disconnected point tools in use. In the healthcare payer network management market, this creates a clear edge for vendors that connect provider directory, contract management, and provider data management within one modular platform. Buyers are increasingly favoring connected application layers that reduce integration work while still supporting specialized workflows where needed.

By End-User: Public Payers Provide Scale While Private Payers Push Faster Change

Public health insurance held 54.27% of the end-user base in 2025, while private health insurance is forecasted to rise at a 15.91% CAGR through 2031. Public programs remained the larger base because Medicare, Medicaid, and CHIP operate at scale and face direct compliance expectations that make technology adoption harder to defer. Medicaid managed care is especially important in the healthcare payer network management market because state program expansion and federal interoperability rules keep directory, credentialing, and claims requirements active. Private plans are growing faster because they are investing more aggressively in AI-supported network optimization, value-based contract analytics, and member-facing service improvements. This leaves the healthcare payer network management market dependent on two different buying patterns, one centered on compliance-heavy volume and one centered on competitive differentiation.

That split shapes vendor strategy across the healthcare payer network management market because suppliers need products that fit both public program complexity and commercial plan speed. As a result, vendors with configurable workflows and broad integration support are better positioned than suppliers that only fit one payer model. The healthcare payer network management market should, therefore, continue to reward vendors that balance regulatory readiness with operational flexibility.

Geography Analysis

North America held 41.68% of global share in 2025, giving the region the largest position in the healthcare payer network management market. The United States drives that lead because it has a dense mix of commercial, Medicare, and Medicaid plans, and each line of business generates a high volume of provider network transactions. CMS now sets the near-term spending pace through the January 1, 2027 deadlines for interoperability and prior authorization APIs. Directory accuracy and surprise billing compliance also keep provider data, credentialing, and workflow modernization high on payer investment plans across the region. Canada and Mexico remain smaller within the healthcare payer network management market, but claims modernization and provider data upgrades are supporting gradual adoption of newer platforms and services.

Europe held the second-largest regional position in 2025, and the healthcare payer network management market there is advancing through payer digitization, data exchange reform, and stronger policy attention to health information infrastructure. Germany’s statutory health insurance federation also called for stronger AI-based fraud detection and broader data governance reform in 2025, which supports continued interest in payer-side data tools and workflow modernization. Across the wider region, the healthcare payer network management market is being shaped by interoperability initiatives and privacy requirements that push payers toward more consistent provider and member data exchange. That combination should sustain demand for platforms that can balance network efficiency with stricter governance requirements.

Asia-Pacific is projected to grow at a 17.23% CAGR through 2031, making it the fastest-expanding geography in the healthcare payer network management market. Japan’s Digital Agency expanded the Public Medical Hub from 183 municipalities at the end of 2024 to 604 municipalities by May 10, 2026, bringing the platform close to nationwide coverage and creating a stronger base for connected payer workflows. China’s National Healthcare Security Administration reported that basic medical insurance coverage exceeds 95% of the population, which supports long-term demand for claims and network infrastructure as managed care activity becomes more complex. South America and the Middle East and Africa remain smaller today, but supplementary insurance reform and broader health system modernization are creating clearer entry paths for vendors in the healthcare payer network management market.

Competitive Landscape

The healthcare payer network management market has a moderately concentrated structure that combines payer software specialists, interoperability vendors, and large IT services firms across the same broad workflow chain. Cotiviti, HealthEdge, Quest Analytics, Symplr, Innovaccer, Zelis, Cognizant, IBM, Infosys, and Wipro all compete across different parts of the healthcare payer network management market, though they do not all compete with the same product depth or delivery model. Zelis acquired Rivet in January 2026 to add AI-powered revenue cycle analytics to its healthcare payments platform, which already serves more than 750 payers. These moves show that larger vendors in the healthcare payer network management market are buying capabilities that improve speed in interoperability, analytics, and workflow automation.

Innovaccer also acquired Humbi AI to strengthen actuarial intelligence and contracting copilot capabilities within its broader payer platform. Availity launched Availity Extend in April 2026, turning its network into a platform where organizations can build AI and automation directly into eligibility, prior authorization, claims, and payment workflows. In the healthcare payer network management market, those strategies raise switching costs because automation becomes embedded in daily payer and provider workflows rather than sitting outside them. The competitive center is therefore shifting toward vendors that can combine data connectivity, configurable workflows, and practical deployment support in one operating model.

White-space demand remains strongest in mid-market payer modernization, Medicaid managed care network upgrades, and Asia-Pacific expansion. Smaller AI-native firms are entering the healthcare payer network management market through partnership routes, especially in virtual provider credentialing, directory monitoring, and predictive network adequacy workflows. CMS interoperability deadlines and provider data requirements also act as a technical screen that favors vendors with FHIR-ready architecture and deeper integration capacity. The overall competitive picture in the healthcare payer network management market remains active rather than winner-take-all, because buyers still spread spending across enterprise platforms, managed services, and niche specialists that solve specific workflow gaps.

Healthcare Payer Network Management Industry Leaders

Optum Inc.

Cognizant

Infosys Limited

Quest Analytics LLC

Availity, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: HealthEdge launched Haven, a generative AI-powered nurse assistant embedded in HealthEdge GuidingCare, designed for health plans managing Medicaid, Medicare, and dual-eligible populations. Haven reduces care manager call preparation time from 8 minutes to under 60 seconds and enables 23% more member interactions per shift, directly addressing payer administrative cost pressures.

- April 2026: Availity unveiled Availity Extend, a platform enabling AI and automation to be built directly on the Availity network, which connects more than 4,000 payers and 3.5 million providers. The product allows organizations to orchestrate eligibility, prior authorization, claims, and payment steps within a single compliant automated workflow.

- March 2026: Innovaccer launched Galaxy UM, an AI-powered utilization management platform enabling health plans to automate prior authorization end-to-end, from request intake and clinical data extraction to medical necessity evaluation and real-time provider communication.

- February 2026: HealthEdge GuidingCare launched the Decision Intelligence Ecosystem, integrating 3 clinical AI vendors, Anterior, Latitude Health, and Case Health AI, into its utilization management platform, giving health plans modular access to next-generation decision automation.

Global Healthcare Payer Network Management Market Report Scope

According to the report’s scope, the healthcare payer network management market refers to the segment of payer operations focused on building, maintaining, and optimizing provider networks. It includes provider contracting, credentialing, directory management, network adequacy compliance, and performance analytics, ensuring payers deliver cost‑effective, high‑quality care through well‑structured provider networks.

The healthcare payer network management market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into platform and software and services. By deployment mode, the market is segmented into cloud-based and on-premises. By application, the market is segmented into provider network design and optimization, contract management, provider data management and credentialing, claims and reimbursement management, and other applications. By end-user, the market is segmented into public health insurance and private health insurance. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Platform and Software |

| Services |

| Cloud-Based |

| On-Premises |

| Provider Network Design and Optimization |

| Contract Management |

| Provider Data Management and Credentialing |

| Claims and Reimbursement Management |

| Other Applications |

| Public Health Insurance |

| Private Health Insurance |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Platform and Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Application | Provider Network Design and Optimization | |

| Contract Management | ||

| Provider Data Management and Credentialing | ||

| Claims and Reimbursement Management | ||

| Other Applications | ||

| By End-User | Public Health Insurance | |

| Private Health Insurance | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the healthcare payer network management market?

The healthcare payer network management market is expected to be valued at USD 4.96 billion in 2025, increase to USD 5.62 billion by 2026, and reach USD 10.92 billion by 2031, registering a CAGR of 14.22% during the forecast period (2026-2031).

Which part of healthcare payer network management leads revenue today?

Platform and software led component revenue with 58.32% share in 2025, reflecting payer reliance on systems for credentialing, directory maintenance, and contract management.

Which deployment model is gaining the most traction with payers?

Cloud-based deployment led with 63.74% share in 2025 and is also the expected to be the fastest-growing model at a 16.02% CAGR through 2031, helped by API and interoperability requirements.

Which region matters most for current revenue and future growth?

North America led with 41.68% share in 2025, while Asia-Pacific is projected to be the fastest-growing region with a 17.23% CAGR through 2031.

Page last updated on: